Embed Size (px)

Citation preview

1© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

Rohit Nagraj, Assistant Manager, Investment Research

Purushottam Pande, CMT, Technical Analyst, Investment Research

Mohak Bhuta, Analyst Investment Research

GOLD WILL IT SHINE IN THE NEAR TERM ?

Thematic Report by

2© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

GOLD Sheen OffGold prices slumped below USD1,100/ounce last week owing to a strong US dollar, easing concerns over Greece’s exit from the Eurozone, signing of the Iran nuclear deal, signs of a rate hike by the US Fed by late 2015, and low demand. Even the net long positions from the Commodities Futures Trading Commission (CFTC) indicate that the near-term outlook for gold is weak. In this article, we have tried to analyze demand dynamics, futures position on CFTC, and technical charts to understand the near-term outlook for gold.

3© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

FALLING GOLD PRICES

Global debt meltdown benefitted Gold since 2008

Lackluster Gold demand in Q1 2015

The precipitous fall in equity markets worldwide

after the 2008 global debt meltdown led to an

increase in gold prices to c.USD 1,900/ounce

in August 2011 from c.USD 730/ounce in

October 2008. Growth rates across geographies/

economies slumped in 2009, and signs of

recovery were visible from late 2010. As a safe

bet, investors continued to invest in gold, the

prices of which reached an all-time high by mid-

2011. Later, investors diverted their attention

to other asset classes that had taken the brunt

of the meltdown with higher earnings potential

returns in the future. The broad-based recovery

across economies further reinforced the view to

invest in other asset classes. As a result, gold

lost its sheen and its prices started correcting.

A surge in the dollar index with the US economic

recovery led to further correction in gold prices.

Our technical analysis reveals a bearish outlook

for gold over the next three months.

The recent gold demand trend suggests that

demand relatively weak in the last few quarters.

In addition, gold demand has been declining

on a year-on-year (YoY) basis since 2011. This

is attributable to low demand from key markets

such as China and India. Nonetheless, gold

demand in India increased 15% YoY, while that

in China declined 7% YoY in Q1 2015. Gold

demand in India could increase in the future due

to falling global prices, but the Indian rupee-US

dollar exchange rate would need to be watched

out for simultaneously. A substantial fall in the

Chinese stock market in H1 2015 is expected to

keep demand for gold weak in the near term. An

analysis of the demand side indicates weak near-

term gold demand, keeping the prices at bay.

Gold demand stable in recent quarters (tonnes) Gold demand stable in recent quarters (tonnes)

Source: www.gold.org

1,246 1,056 1,010 1,090 1,033 1,039 1,050 1,079

-500

0

500

1,000

1,500

2,000

2Q20

13

3Q20

13

4Q20

13

1Q20

14

2Q20

14

3Q20

14

4Q20

14

1Q20

15

Jewellery Total barand coin invest.

ETFsand similar

Technology Central banks

3,127 3,096 3,115 3,777 3,674

4,213 4,728 4,690 4,436 4,212

-500

500

1,500

2,500

3,500

4,500

5,500

6,500

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

4© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

Falling net long positions on CFTC

Strong US Dollar to limit rise in Gold prices

Declining net positions on CFTC

Uptrend in gold prices limited by strong US dollar

Source: CFTC

Source: Thomson Reuters

On the CFTC, gold net long positions currently

(week ending July 14, 2015) stand at 47,824,

the lowest since January 2014. This indicates

investors being averse to gold trading-related

risks. Even overall long positions have been

hovering in a narrow band, thereby indicating low

interest from investors.

The gold and US dollar indices had a negative

correlation between 2000 and YTD 2015. The

negative correlation, which currently stands

at -0.7, indicates that a US strong dollar index

would be unfavorable for gold and vice versa.

Recent comments from the US Fed suggest that

the US Fed is likely to raise interest rates in H2

2015, which would limit uptrend in gold prices in

the near term.

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

3,50,000

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

60

70

80

90

100

110

120

130

140

0

250

500

750

1,000

1,250

1,500

1,750

2,000

Jan-

00Ju

l-00

Jan-

01Ju

l-01

Jan-

02Ju

l-02

Jan-

03Ju

l-03

Jan-

04Ju

l-04

Jan-

05Ju

l-05

Jan-

06Ju

l-06

Jan-

07Ju

l-07

Jan-

08Ju

l-08

Jan-

09Ju

l-09

Jan-

10Ju

l-10

Jan-

11Ju

l-11

Jan-

12Ju

l-12

Jan-

13Ju

l-13

Jan-

14Ju

l-14

Jan-

15Ju

l-15

Gold Dollar Index

Gold prices plateaued at USD 1,899/ounce

5© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

Gold to lose sheen temporarily

Technical commentary

Broader data on gold demand, CFTC positions,

and the US dollar index indicate that the near-

term outlook for gold would remain challenging.

Gold demand has picked up in India. Meanwhile,

the slump in the Chinese stock market would

impact demand for the yellow metal in China.

We believe that fundamental factors are currently

unfavorable for gold and, thus, its prices are

likely to remain low in the near term.

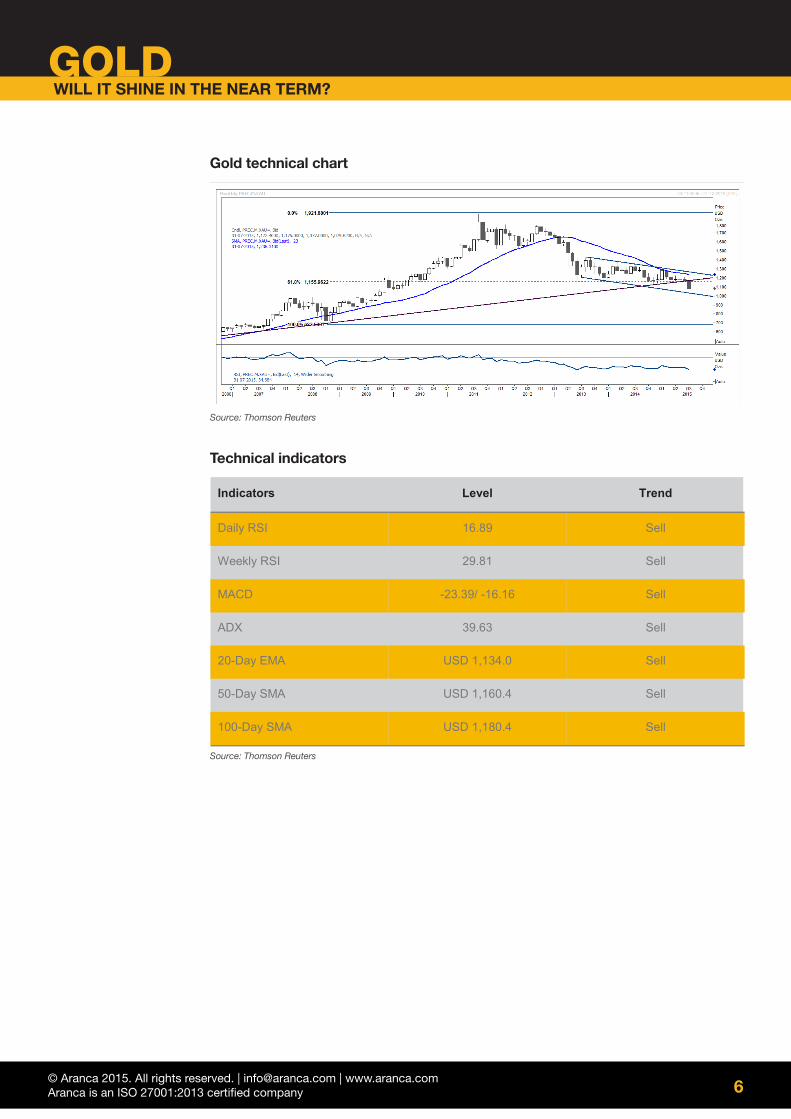

As evident from the chart, gold has been trading in

a downward sloping trend channel, experiencing

selling on each rise. The theme of strong US

dollar and weak commodities is playing well.

However, the factor that aids in betting on a weak

gold is that although gold is a safe haven, it did

not gain any visible strength amid Grexit fears.

Rather each rise has been sold off into. On the

monthly charts, RSI continues to hover in the

negative territory, supporting the bearish outlook

on the commodity. It has currently breached the

support of the 61.8% retracement of the rise

experienced since 2008. This indicates sustained

downward pressure on the commodity. The trend

remains bearish. An immediate decline towards

the lower channel support looks likely from here.

TECHNICAL VIEW BEARISH(GOLD SPOT — USD 1,090.4)

Key support/ resistance levels

6© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

Technical indicators

Source: Thomson Reuters

Gold technical chart

Source: Thomson Reuters

7© Aranca 2015. All rights reserved. | [email protected] | www.aranca.com Aranca is an ISO 27001:2013 certified company

GOLD WILL IT SHINE IN THE NEAR TERM?

This report is published by Aranca, a customized research and analytics services provider to global clients.

The information contained in this document is confidential and is solely for use of those persons to whom it is addressed and may not be reproduced,

further distributed to any other person or published, in whole or in part, for any purpose.

This document is based on data sources that are publicly available and are thought to be reliable. Aranca may not have verified all of this information

with third parties. Neither Aranca nor its advisors, directors or employees can guarantee the accuracy, reasonableness or completeness of the

information received from any sources consulted for this publication, and neither Aranca nor its advisors, directors or employees accepts any

liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of this document or its contents or otherwise arising in

connection with this document.

Further, this document is not an offer to buy or sell any security, commodity or currency. This document does not provide individually tailored

investment advice. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The

appropriateness of a particular investment or currency will depend on an investor’s individual circumstances and objectives. The investments

referred to in this document may not be suitable for all investors. This document is not to be relied upon and should not be used in substitution for

the exercise of independent judgment.

This document may contain certain statements, estimates, and projections with respect to the anticipated future performance of securities,

commodities or currencies suggested. Such statements, estimates, and projections are based on information that we consider reliable and may

reflect various assumptions made concerning anticipated economic developments, which have not been independently verified and may or may not

prove correct. No representation or warranty is made as to the accuracy of such statements, estimates, and projections or as to its fitness for the

purpose intended and it should not be relied upon as such. Opinions expressed are our current opinions as of the date appearing on this material

only and may change without notice.

© 2015, Aranca. All rights reserved.

DISCLAIMER

INVESTMENT RESEARCH | BUSINESS RESEARCH | IP RESEARCH | BUSINESS VALUATION