Embed Size (px)

Citation preview

Basic concepts in auditing

Definition: Audit is an independent examination,Of financial information,Of any entity whether profit making or not, irrespective of its size & legal structure, When such an examination is conducted with a view to express an opinion thereon.

MEANING:

Audit Evidence refers to any information obtained by the auditor so that he can draw conclusions & express opinion on the financial statement

Features of audit evidence:

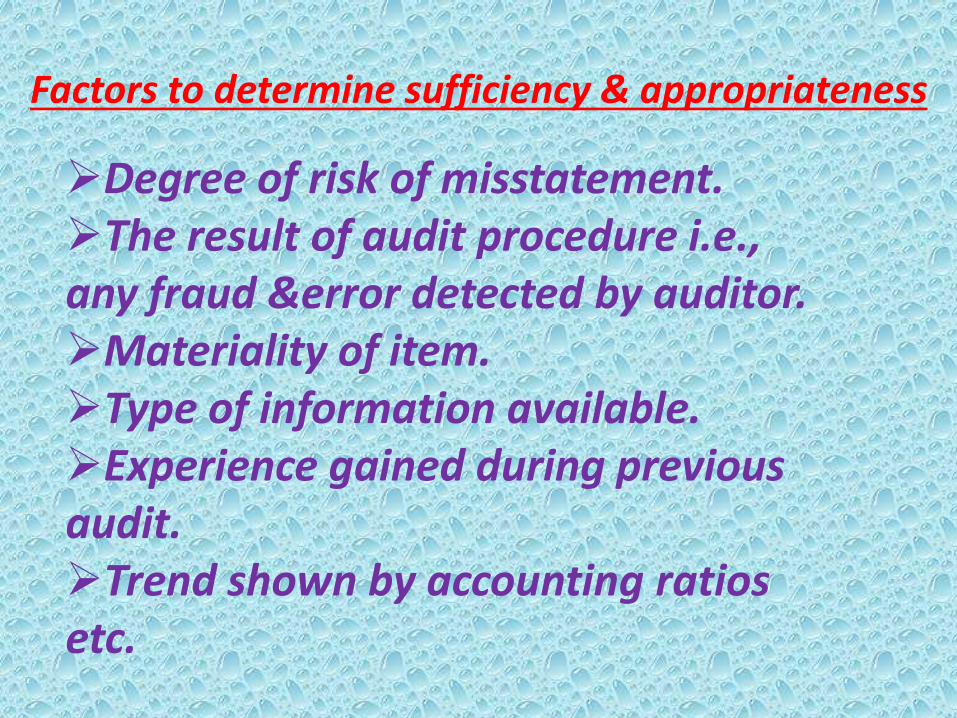

Factors to determine sufficiency & appropriateness

Degree of risk of misstatement.The result of audit procedure i.e., any fraud &error detected by auditor.Materiality of item.Type of information available.Experience gained during previous audit.Trend shown by accounting ratios etc.

Types of audit evidence

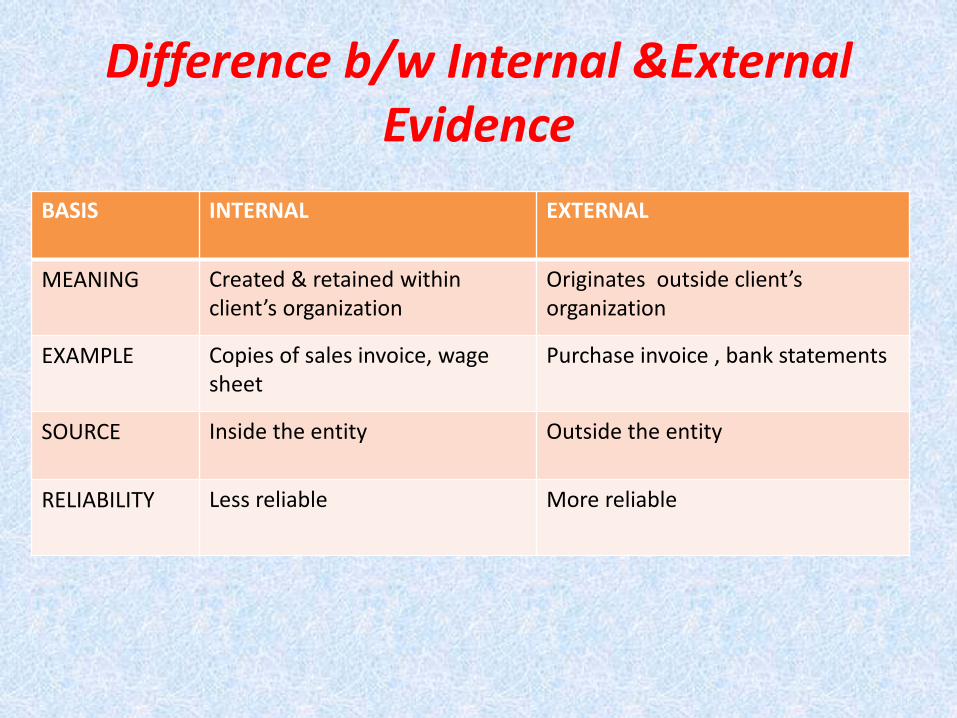

Difference b/w Internal &External Evidence

BASIS INTERNAL EXTERNAL

MEANING Created & retained within client’s organization

Originates outside client’s organization

EXAMPLE Copies of sales invoice, wage sheet

Purchase invoice , bank statements

SOURCE Inside the entity Outside the entity

RELIABILITY Less reliable More reliable

Compliance proceduresSubstantive procedures

Compliance procedures are performed to

check designing, operating effectiveness and

continuity of I.C. system. Auditor performs

compliance procedures in respect of the

following assertions relating to internal

control system:

EXISTENCE:that the internal control exists.

OPERATING EFFECTIVENESS: that the I.C.

system is operating effectively.

CONTINUITY:that the internal control has

been so operated

throughout the period.

Substantive procedures are performed to check completeness,

accuracy and validity of transactions and balances. Auditor

performs substantive procedures in respect of following

assertions relating to data produced by accounting system:

MEASAUREMENT: that a transaction is recorded in the proper

period at proper amount.

PRESENTATION AND DISCLOSURE: an item is disclosed, classified

and described as per recognized accounting policies and

relevant statutory requirements, if any.

EXISTENCE: that an asset or liability exists at a given date.

VALUATION: that an asset or liability is recorded at an appropriate

carrying value.

Methods to obtain evidence

Inspection Observation Inquiry and

confirmationComputation

Analytical review

Reperformance

Relationship b/w materiality and

audit risk