Embed Size (px)

Citation preview

News Update as @ 1530 hours, Monday 23 March 2015

Feedback: [email protected]: [email protected]

Business Reporters

HARARE - The Deposit Protection Corpo-ration (DPC) says it has so far compen-sated 15.6 percent of insured Interfin Bank deposits and 8.1 percent of Allied Bank deposits while compensation for Afrasia Bank’s depositors will commence soon.According to reports, Interfin, whose banking license was cancelled in 2012, owes depositors more than $60 million while Allied bank owes at least $14,7 mil-lion to its depositors, of which $1,3 will be paid by the DPC.

DPC will also pay out $3,3 million to 18 000 Afrasia depositors. DPC through the Deposit Protection Fund is mandated to compensate at least 90 percent of depos-itors up to the maximum insurable limit.

In emailed responses to questions from BH24, DPC public relations manager Allen Musadziruma said payments to Allied and

Interfin bank depositors began on Feb-ruary 23 and March 3 respectively while payments to Genesis Investment Bank, Royal Bank and Trust Bank depositors is in progress.

“DPC was appointed by the High Court as provisional liquidator of AfrAsia Bank on Wednesday 18th of March 2015. We

hope to commence payments soon once the requisite administrative procedures have been finalised. At least 83 percent of AfrAsia depositors will be paid in full as they have balances below the insurable

limit of $500,” he said.

DPC has in the past said struggling banks

were not paying premiums towards the fund, putting strain on the DPC when it is time to compensate depositors.How-ever, Musadziruma said the fund is able to meet its statutory obligation of compen-sating small depositors of failed banking institutions as per its mandate.

“Depositors with balances below $500 are paid through convenient payment channels such as mobile phone and bank transfers. Clients with balances above the insurable limit of $500 will still be paid their deposits through the liquidation pro-cess on a pro-rata basis,” he said.He said the closure of banks is negatively affect-ing depositor confidence in the banking system.

“However, the existence of an explicit deposit protection scheme helps to pro-tect depositors by providing a guarantee of compensation in the event of a mem-ber bank failure,” he said. ●

DPC compensates 16pc of Interfin depositors

By Tawanda Musarurwa

HARARE - The Zimbabwe Energy Reg-ulatory Authority (ZERA) maintains that despite challenges on the supply side of electricity, the energy tariff is in line with what is prevailing in the region.

Zimbabwe has an average end user tariff of 9.86 US cents per kilowatt hour (c/kWh). And according to a regional comparison done by the regulator, Angola and Zambia offer a significantly cheaper electricity tariff rate to the extent of subsidies in those two coun-tries.

Angola's average end user tariff cur-rently stands at 5.4c/kWh, while in Malawi it stands at 9c/kWh, and Namibia has an average tariff of 17c/kWh.Zambia's average end user tariff is 6c/kWh, while that of Lesotho stands at 9.3c/kWh and that of Swaziland at 10.3c/kWh.

Mozambique's energy tariff stands at 9c/kWh, and that South Africa (the municipalities) is at 11.7c/kWh, and that of the power utility Eskom is at 8c/

kWh. ZERA chief executive officer Engi-neer Gloria Magombo said "there has not been a significant change in the average tariff over the past four years," despite a couple of adjustments during that period.

In 2009, the national average tariff (USc/kWh) was 7.53, a figure which remained flat in 2010, but increased to 9.83 in 2011. It remained unchanged again in 2012, but rose marginally to 9.86 in 2013.

Last year, ZERA turned down a request by the national power utility Zimbabwe Electricity Supply Authority (ZESA) to increase tariffs by a 5 percent margin.

The Zimbabwe Electricity Transmission and Distribution Company (ZETDC) had applied for a 5 percent upward review of the electricity tariff from the 9.86c/kWh to 10,36c/kWh on the basis that this was in line with its rev-enue requirement of $890.60 million for supply of 8 594 gigawatt per hour (Gw/h) of electricity. Engineer Mag-

ombo however said the regulator will initially allow new (independent power projects) coming on board to charge a higher tariff to cover the cost of expen-sive borrowings.

"But an issue we have found with new projects coming in now is that of lack of access to long-term funding, and access to medium-term funding comes at a higher cost and what that does is that the tariffs of these new projects will be higher than normal," she said. ●

2 NEWS2 NEWS

Zim electricity tariff competitive in the region: ZERA

BH24

By Funny Hudzerema

HARARE – Government has launched the National Bio-fuels Policy, which is expected to reduce Zimbabwe's dependence on importing fuel from other countries and allow for the use of local non-renewable resources.

Speaking at the launch of the National Bio-fuels Policy Deputy Minister of Energy and Power Development Tsitsi Muzenda said the production of bio-fu-els can have a broad impact on the economy.

“Our country is a net importer of fossil fuel energy, its current requirements are about 2,5 million and 1,5 mil-

lion litres of diesel and petrol per day respectively.

Widespread use of bio-fuels can there-fore reduce the country’s dependence on imported petroleum products, sta-bilise fuel prices, ensure energy secu-rity to promote rural development and investment reduce poverty and create employment,” she said.

Currently the Government has estab-lished bio-diesel processing plants with capabilities of handling 10 000 litres per day in Mutoko and 60 000 litres per day at Mt Hampden, which are then part-nered with Greenfuel to produce sug-arcane based bio-ethanol fuel.

Muzenda said the National Bio-fuels Policy will spearhead the use of local resources and implement the opera-tions local bio manufacturing plants in the country. In 2013 the Government introduced a mandatory five percent blending of bio-ethanol with petrol, which was then raised to 15 percent last year.

Establishment of the policy was sup-ported by the European Union in sup-port of the country's fuel sector. She added that the policy was in line with the EU’s Renewable Energy Directive of 2009 which set targets for the con-sumption of renewable energy in the EU’s transport sector from 2 percent in 2005 to 6 percent in 2010 and eventu-ally 10 percent in 2020.

“Such global developments have opened opportunities for bio-fuels investments in developing countries such as Zimbabwe that have suitable land and water requirements,” said Muzenda.

The National Bio-fuels Policy will now undergo the consultative process for three months both locally and interna-tionally before being submitted to Cab-inet in May for approval. ●

44 NEWS

Govt launches National Bio-fuels Policy

BH24

By Rumbidzai Zinyuke

Lowveld sugar producer Tongaat Hul-lets has engaged Government over a request for a license for continuous supply of fuel grade ethanol to the local market.

The company’s Triangle mill has an ethanol plant with an installed capacity of 41 million litres and has been pro-ducing only 24 million litres due to low demand.

Tongaat Hullet managing director Mr Sydney Mutsambiwa recently told Parliamentarians that the company has already been issued with several temporary licenses to meet national demand but was now seeking a license for continuous supply.

“We do have the capacity, it’s just a question of ensuring that the regu-latory requirements by Zimbabwe Energy Regulatory Authority are met to a level that allows us to have continu-ous production capacity. We have been engaging government in this respect and we are advised that due consid-eration is being given to that request. So we await to see where we go from

here,” he said. Under the country’s mandatory blending policy, only Green Fuel is licensed to trade the commodity for petrol blending purposes.

Triangle has however been granted several temporary licenses to meet demand over the past several years. Mr Mutsambiwa said the ethanol plant at Triangle has since been upgraded to

produce fuel grade ethanol at 93 per-cent.

“In the current year we are geared to produce fuel grade ethanol for supply to the local market as required by the implementing agent who in the last time was the National Oil Infrastruc-ture Company, the government arm responsible for fuel retailing,” he said.

The company is also seeking to add 29 000 hectares of land to its out growers in an effort to more than double its out-put by 2018.

Tongaat Hulett Limited, owns a 50,3 percent interest in Hippo Valley and 100 percent of Triangle Zimbabwe Lim-ited. ●

66 NEWS

Tongaat Hullet seeks ethanol license

BH24

HARARE – The equities market recov-ered slightly to close the week in the positive as the industrial index gained 0.33 to close on 162.36.

Old Mutual gained 2 cents to close at 239 cents and Innscor moved up 1,51 cents to trade at 56,51 cents. Bever-ages maker Delta and Econet traded unchanged 109 cents and 52 cents respectively.

Counters in the negative territory included cigarette manufacturer BAT which eased 10 cents to 1160 cents, Mash Holdings lost 0,20 cents to close at 2 cents and Padenga slid 0,10 cents to settle at 9 cents.

Volumes were down on yesterday and supported by trades in Econet, Seedco and Delta to reach $678 706. Despite today’s gain the industrial index lost 0.34 this week compared to last week.

The Mining index retreated by 0.12 to close at 48.42 after Hwange slipped 0,10 cents to close at 4 cents. Bindura, Falgold and RioZim were unchanged

at 4,49 cents, 0,50 cents and 7 cents respectively. Week on week the min-ing index dropped 1.37. —BH24 Reporter •

8 ZSE REVIEW

Old Mutual, Innscor push ZSE recovery

BH24

A rally that made Nigerian bonds the best performers in Africa in March risks coming to an end as the credit rating of the continent’s biggest economy slides deeper into junk.

Standard & Poor’s lowered its assess-ment on Nigeria one level to B+, four levels below investment grade, on March 20, while changing its outlook to stable from negative. Naira bonds returned 2 percent this month, the most among 31 emerging markets after Russia and the Dominican Republic, according to Bloomberg indexes. Naira debt lost 5 percent in February.

Nigeria’s economy is sputtering under the weight of a more than 50 percent plunge since June in the price of oil, its main export, and an insurgency by Isla-mist militants before elections on March 28. While the central bank has stemmed a slide in the naira with 17 foreign-ex-change restrictions since September, policy makers may devalue the currency after the vote, so it doesn’t make sense to buy local bonds, according to Alan Cameron, an economist at Exotix Part-ners LLP in London.

“A downgrade worsens public and inves-tor perception of the economy, which is

already being hit,” Kunle Ezun, an analyst at Ecobank Transnational Inc. in Lagos, said by phone last week. Borrowing costs will increase because of the negative sig-nal it sends, he said.

Nigeria’s currency lost 18 percent against the dollar in the past six months, the steepest decline among 24 African cur-rencies tracked by Bloomberg after the Zambian kwacha. It touched an all-time

low of 206.32 per dollar on Feb. 12. The naira advanced 0.1 percent to 199.05 as of 8:43 a.m. in Lagos on Monday. — Bloomberg ●

REGIONAL NEWS 10

Nigeria’s fall deeper into junk risks Africa’s best bond rally

BH24

12 DIARY OF EVENTS

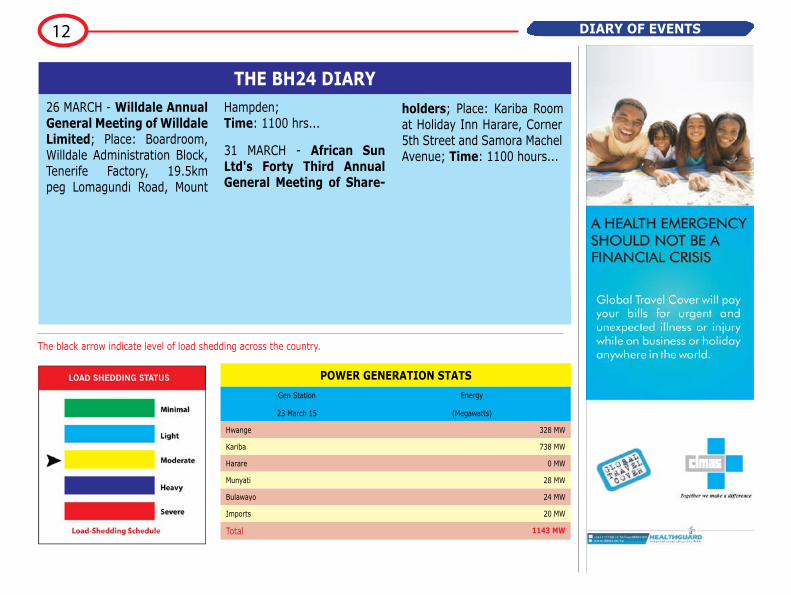

The black arrow indicate level of load shedding across the country.

POWER GENERATION STATS

Gen Station

23 March 15

Energy

(Megawatts)

Hwange 328 MW

Kariba 738 MW

Harare 0 MW

Munyati 28 MW

Bulawayo 24 MW

Imports 20 MW

Total 1143 MW

26 MARCH - Willdale Annual General Meeting of Willdale Limited; Place: Boardroom, Willdale Administration Block, Tenerife Factory, 19.5km peg Lomagundi Road, Mount

Hampden; Time: 1100 hrs...

31 MARCH - African Sun Ltd's Forty Third Annual General Meeting of Share-

holders; Place: Kariba Room at Holiday Inn Harare, Corner 5th Street and Samora Machel Avenue; Time: 1100 hours...

THE BH24 DIARY

BH24

14 ZSE

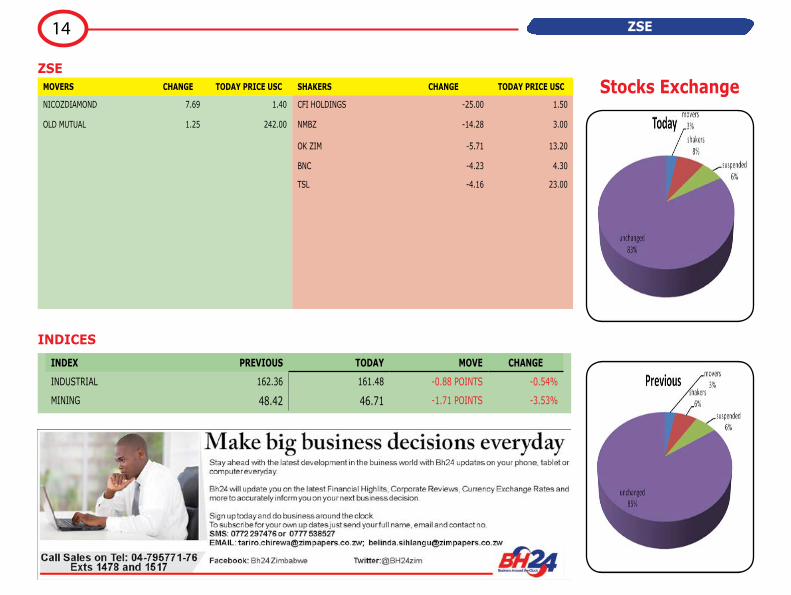

ZSEMOVERS CHANGE TODAY PRICE USC SHAKERS CHANGE TODAY PRICE USC

NICOZDIAMOND 7.69 1.40 CFI HOLDINGS -25.00 1.50

OLD MUTUAL 1.25 242.00 NMBZ -14.28 3.00

OK ZIM -5.71 13.20

BNC -4.23 4.30

TSL -4.16 23.00

INDICES

INDEx PREVIOUS TODAY MOVE CHANGE

INDUSTRIAL 162.36 161.48 -0.88 POINTS -0.54%

MINING 48.42 46.71 -1.71 POINTS -3.53%

Stocks Exchange

15 AFRICA STOCKS

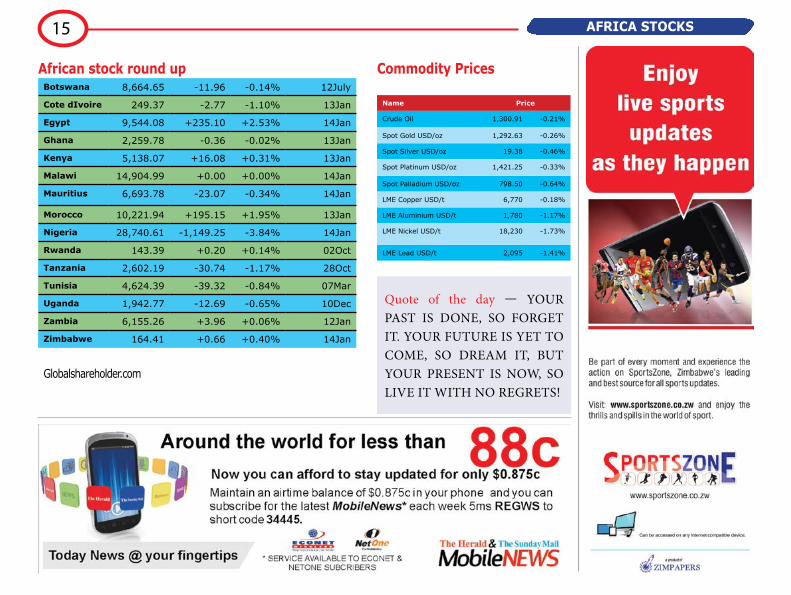

Botswana 8,664.65 -11.96 -0.14% 12July

Cote dIvoire 249.37 -2.77 -1.10% 13Jan

Egypt 9,544.08 +235.10 +2.53% 14Jan

Ghana 2,259.78 -0.36 -0.02% 13Jan

Kenya 5,138.07 +16.08 +0.31% 13Jan

Malawi 14,904.99 +0.00 +0.00% 14Jan

Mauritius 6,693.78 -23.07 -0.34% 14Jan

Morocco 10,221.94 +195.15 +1.95% 13Jan

Nigeria 28,740.61 -1,149.25 -3.84% 14Jan

Rwanda 143.39 +0.20 +0.14% 02Oct

Tanzania 2,602.19 -30.74 -1.17% 28Oct

Tunisia 4,624.39 -39.32 -0.84% 07Mar

Uganda 1,942.77 -12.69 -0.65% 10Dec

Zambia 6,155.26 +3.96 +0.06% 12Jan

Zimbabwe 164.41 +0.66 +0.40% 14Jan

African stock round up Commodity Prices

Name Price

Crude Oil 1,300.91 -0.21%

Spot Gold USD/oz 1,292.63 -0.26%

Spot Silver USD/oz 19.38 -0.46%

Spot Platinum USD/oz 1,421.25 -0.33%

Spot Palladium USD/oz 798.50 -0.64%

LME Copper USD/t 6,770 -0.18%

LME Aluminium USD/t 1,780 -1.17%

LME Nickel USD/t 18,230 -1.73%

LME Lead USD/t 2,095 -1.41%

Quote of the day — Your past is donE, so ForgEt it. Your FuturE is YEt to comE, so drEam it, but Your prEsEnt is now, so livE it with no rEgrEts!

Globalshareholder.com

Gold retained gains from a three-day rally on Monday to trade near its high-est in two weeks, boosted by a weaker dollar and caution from the Federal Reserve on the timing of a possible hike in U.S. interest rates.

Spot gold was little changed at $1,182.55 an ounce by 0715 GMT. It climbed to $1,187.80 on Friday, its highest since March 6, as the dollar tumbled.

The greenback has been under pres-sure since last Wednesday when the Fed sounded a cautious note on the health of economic recovery in the United States, and slashed its median estimate for the federal funds rate.

Market players' consensus expectation for a U.S. interest rate increase has shifted, with most of Wall Street's top banks now expecting the Fed to hold off until at least September and

the odds for a June hike fading, a Reu-ters poll showed.

"With the rate hike not expected until September, some unwinding of short positions on gold are expected and a weaker dollar in the interim is also set to boost demand for gold," said Phillip

Futures analyst Howie Lee.

Traders said the next key level for gold is $1,200 on the upside.

Gold had dipped to a four-month low before the Fed meet last week as con-cerns mounted over higher U.S. inter-est rates which could dent demand for non-interest bearing bullion. But it has

recovered since.

The dollar started trade in Asia on the defensive, after a volatile few days in the wake of the Fed's dovish steer, which cast doubts on bullish positions in the greenback.

Despite the modest gain in bullion prices, data showed that investor sen-timent has not improved drastically.

SPDR Gold Trust, the world's largest gold-backed exchange-traded fund, said its holdings fell 0.72 percent to 744.40 tonnes on Friday - the lowest since late January.

Hedge funds and money managers slashed their bullish bets in gold and silver futures and options for a sixth straight week in the week ended March 17, U.S. Commodity Futures Trading Commission data showed on Friday.

In the physical markets, demand seemed to have weakened compared to last week's levels.

In China, the second biggest consumer, premiums eased to $4-$5 an ounce, lower from Friday's levels of $6-$7. —Reuters ●

16 INTERNATIONAL NEWS

Gold near 2-week high

By Charles Dhewa

Farmers and traders have to juggle more than three variables to be suc-cessful which is why adaptation chal-lenges are more current than technical challenges. Unfortunately formal insti-tutions like banks do notunderstand all these variables and farmers’ coping mechanisms.

Consequently, farmers and traders continue to be subjected to the same credit bureau rules meant for the for-mal sector. It looks like forcing formal institutions to understand the indig-enous commerce (‘informal sector’) is like forcing a large plane to land on an airport designed for Helicopters and small planes.

While formal institutions tend to focus on topical knowledge spewed from educational institutions, this knowledge has problems adjusting to local practi-cal contexts that are typical of indige-nous commerce. Instructive teaching and learning are useless in indigenous commerce.

A credit bureau for indigenous com-

merce should take into account how traders and farmers deconstruct and reconstruct knowledge in complex markets where cash and barter deals co-exist.

By not capturing barter deals and rela-tionships, a formal credit bureau fails to capture a critical component of indige-nous commerce. Whether farmers and traders follow recommendations from formal banks is a hit-or-miss scenario because they are chasing many varia-bles as indicated above.

In indigenous commerce, there is no guarantee that banking manuals,

financial research reports and recom-mendations will be translated into real financial solutions.

Knowledge should be more analytical than operational financial institutions are to understand indigenous com-merce.

This is because knowledge is just one essential ingredient of competency in indigenous commerce with trust and relationships being some of the most important ingredients.

What is important is not knowing about the world of banking but knowing what

is required to actually go out and make a difference in the real world.

In indigenous commerce, learning hap-pens fast within networks of traders and farmers who bypass the classical reporting loop.

When traders and farmers learn from each other according to their lines of business, they immediately put knowl-edge into practice without waiting for someone to document what is going on in the market.

ICTs are enhancing learning that happens through direct knowledge

17 analysis

Why indigenous commerce deserves its own Credit Bureau

17 ANALYSIS

exchange in the market without going through some hierarchical filter. In this case, traders and farmers in the mar-ket frontline of markets constitute deep sources of practical wisdom.

However, there are limits to how farm-ers and traders can learn from other people's experience.

Social learning processes like those happening in indigenous commerce cannot be mandated formally from the top or cut short before going through their full cycles.

Adaptive challenges faced by trad-ers and farmers in agriculture mar-kets require co-creating of solutions, whether financial or economic.

Trader and farmer experiences can-not be photocopied and dumped in Zimbabwe. Otherwise we end up with well articulated and analyzed business models which do not speak to the real-ity on the market.

Understanding what farmers and trad-ers are struggling with on the ground is the basis for a relevant credit bureau.

Unfortunately, Zimbabwean institu-tions like banks and development part-

ners are failing to grasp and distinguish adaptive from technical issues con-fronting the agriculture sector.

While the technical angle emphasizes knowledge from experts such as bank-ers, the agriculture sector is in the throes of adaptive challenges where solutions are not known and have to be co-created by farmers, traders, academics, consumers, transporters, development partners and policy mak-ers.

A strong credit bureau will have to evolve from perspectives from all these clusters. It can’t emerge from throwing technical solutions at the issues. Turn-ing adaptive challenges into technical problems and solutions is a big mistake that has to be avoided.

The idea behind a Credit Bureau for Market Traders

eMKambo has set out to mobilize ideas and institutions toward creating a Credit Bureau for traders and farm-ers operating in indigenous commerce. This initiative will build the confidence of financial institutions so that they start taking traders as borrowers rather than just anticipated savers.

Negative perceptions about people’s markets like Mbare, Malaleni, Sakubva and many others have prevailed for a long time, cementing some level of reluctance by financial institutions to lend money to traders.

Existing formal credit bureaus that are used to assess individuals’ creditworthi-ness are not entirely relevant because they focus on employment-based bor-rowing histories.

On the other hand, the people’s market is populated by people who have never been formally employed. This means there business or transaction history will be missing from the formal credit bureau.

Traders are responsible for moving more than 60% of the food that flows into urban areas from production zones. In fact, markets like Mbare are the first ports of call for all the food that ends up in many urban markets and small markets run by vendors in high density areas.

Money and relationships are respon-sible for moving all this food. A credit bureau that captures all these dynam-ics is needed.

Features of an ideal indigenous com-merce credit bureau

The Indigenous Commerce Credit Bureau that eMKambo is crafting pro-vides vital and up to the minute infor-mation about each trader and farmer.

This information will be available for serious financiers keen to advance loans to traders. Towards consolidat-ing the credit bureau, eMKambo has already compiled the following details for each of the close to 10 000 traders that deal in food and other commodi-ties in 20 markets across Zimbabwe:

1. Name and Surname.

2. Gender.

3. Date of birth.

4. Contact address.

5. Stall address.

6. Trading years.

7. Commodity specialization.

8. Average volumes traded per day/week/month/year.

9. Average revenue per day/week/

18 ANALYSIS

month/year.

10. Profits realized per day/week/year.

11. Loans (formal or informal) applied before.

12. Repayment history.13. Current loan (formal or informal) status.

14. Social capital (relationships)

A scale of scores is being designed for each trader or farmer. The level of default determines the score. The higher the score the better. If a trader changes from poor performance to a better performance the score is increased. Before writing off a trader, many aspects are considered. Some traders prefer holding their cash as stock not as physical cash so they are never liquid. The business cycle differs

with the type of produce traded.

Vegetables usually do not take up more than three days on the stall and this implies within three days the trader would have realized a profit. In instances where a trader is selling dried grains the stock might take about a week or more. This means traders spe-cializing in different commodities have to be treated differently. The Indige-nous Commerce Credit Bureau sets scores in ways that differentiates trad-ers and farmers in line with the nature of their businesses.

The main advantages of having a Credit Bureau for the Agriculture mar-ket traders include:•

• Traders become aware of the importance of discipline in business. Recording all their transactions will

make them see if they are making a profit, loss or if they are breaking even hence giving them room for business growth.

• Increasing traders’ chances of obtaining loans and support from other stakeholders interested in agriculture because the credit bureau enhances confidence in the trader’s business.

• The credit bureau shows busi-ness trends for each trader or farmer – an indicator of progress and what needs improving from operational or policy angles.

Developing scorecards appropriate for traders and farmers working in indig-enous commerce requires a combi-nation of technical modeling skills and practical knowledge of how people’s markets function on a daily basis. However, since the scorecard in the credit bureau does not replace human judgment but complements human intelligence, eMKambo has financial literacy officers whose roles include providing the humane judgement that is critical for sustaining relationships in indigenous commerce. - eMkambo *The writer can be contacted on the following emails: [email protected] / [email protected] ●

19 ANALYSIS

![7315 About Zera · 2019. 9. 12. · About ZERA The Zimbabwe Energy Regulatory Authority (ZERA) is a statutory body established by the Energy Regulatory Authority Act [Chapter 13:23]](https://img.pdfslide.us/doc/110x75/6122cbc99cc3b553717da7c8/7315-about-zera-2019-9-12-about-zera-the-zimbabwe-energy-regulatory-authority.jpg)