Embed Size (px)

Citation preview

© Oliver Wyman CONSULTING ACTUARIES

WHAT’S TRENDING IN REINSURANCE? 2015 Life and Annuity Symposium

May 4, 2015

Alberto Abalo FSA, MAAA, CERA

1 © Oliver Wyman 1

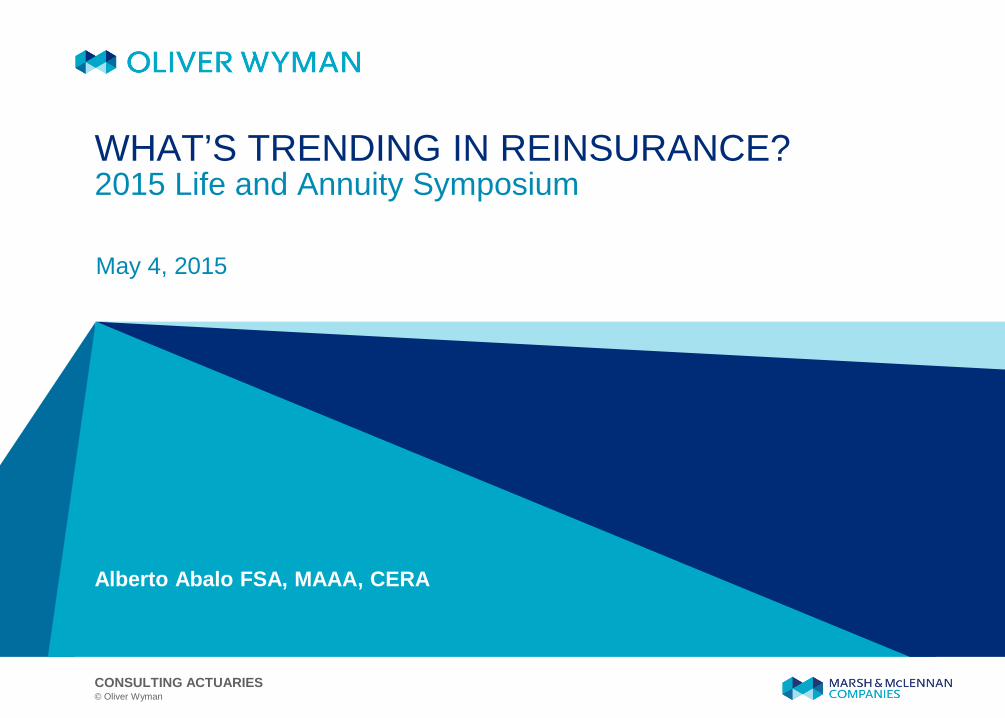

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013Amt. Retained 675 705 809 952 1,089 1,207 1,212 1,148 1,168 1,218 1,260 1,186Amt. Reinsured 1,078 1,043 1,037 844 724 683 658 596 505 461 446 443% Reinsured 61.5% 59.7% 56.2% 47.0% 39.9% 36.1% 35.2% 34.2% 30.2% 27.5% 26.1% 27.2%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Cession rates have been on the decline…

U.S

. Bill

ions

U.S. ordinary individual life insurance sales

Source: Society of Actuaries Life Reinsurance surveys, conducted by Munich American Re

2 © Oliver Wyman 2 DILBERT © 2004 Scott Adams. Used By permission of UNIVERSAL UCLICK. All rights reserved.

3 © Oliver Wyman 3

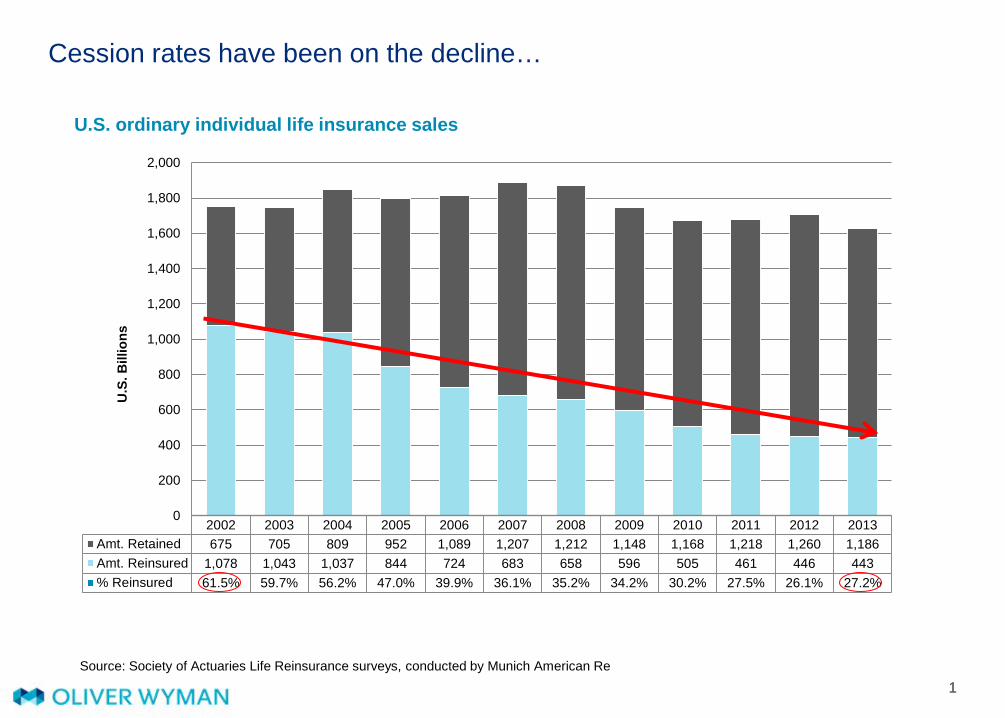

2011 2012 2013Amt. Retained 1,218 1,260 1,186Amt. Reinsured 461 446 443% Reinsured 27.5% 26.1% 27.2%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

…but the market appears to have reached equilibrium Consistent level of ceded new business 2011 – 2013

U.S

. Bill

ions

U.S. ordinary individual life insurance sales

Source: Society of Actuaries Life Reinsurance surveys, conducted by Munich American Re

Year-over-year increase in

cession rates for the first time in

11 years

4 4 © Oliver Wyman

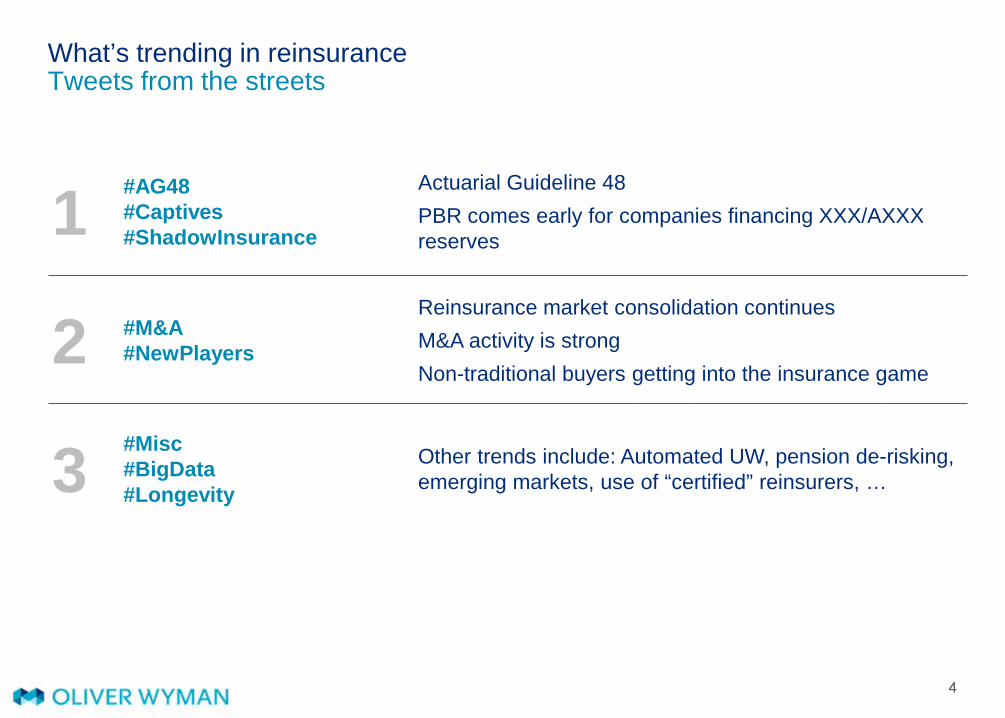

What’s trending in reinsurance Tweets from the streets

1 #AG48 #Captives #ShadowInsurance

Actuarial Guideline 48 PBR comes early for companies financing XXX/AXXX reserves

2 #M&A #NewPlayers

Reinsurance market consolidation continues M&A activity is strong Non-traditional buyers getting into the insurance game

3 #Misc #BigData #Longevity

Other trends include: Automated UW, pension de-risking, emerging markets, use of “certified” reinsurers, …

#AG48 Actuarial Guideline 48

1

6 © Oliver Wyman 6

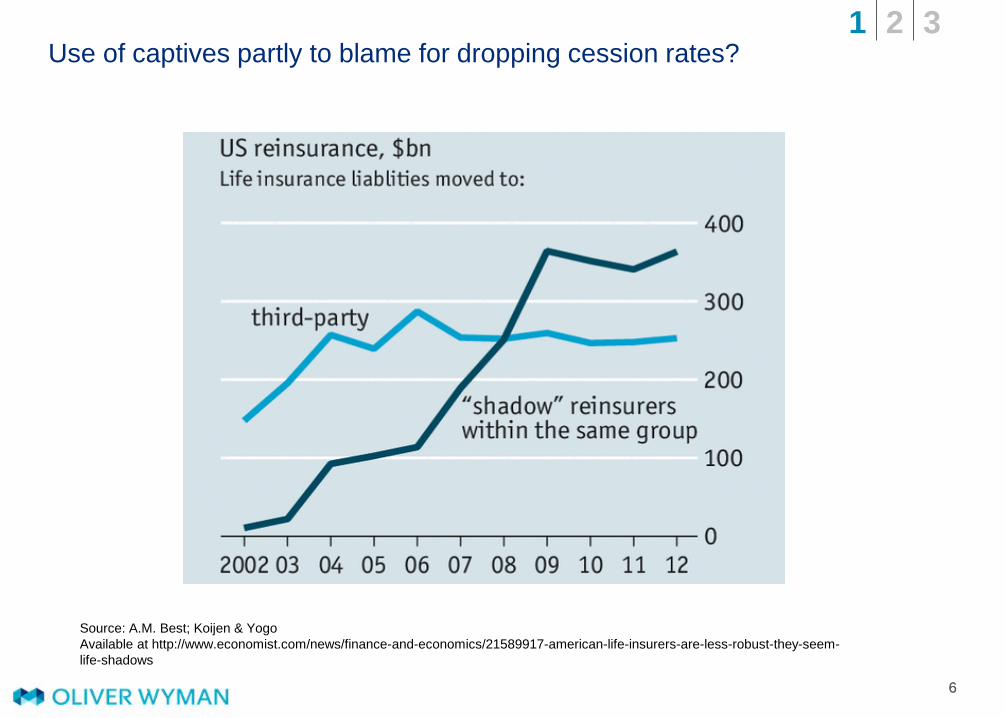

Use of captives partly to blame for dropping cession rates?

Source: A.M. Best; Koijen & Yogo Available at http://www.economist.com/news/finance-and-economics/21589917-american-life-insurers-are-less-robust-they-seem-life-shadows

1 2 3

7 © Oliver Wyman 7

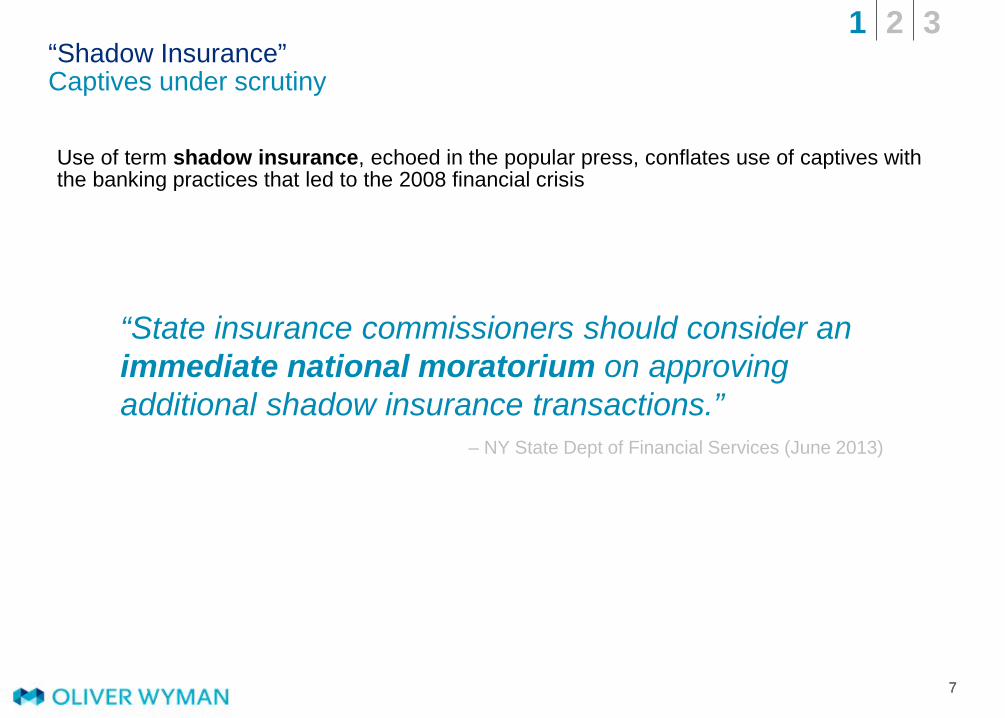

“Shadow Insurance” Captives under scrutiny

Use of term shadow insurance, echoed in the popular press, conflates use of captives with the banking practices that led to the 2008 financial crisis

“State insurance commissioners should consider an immediate national moratorium on approving additional shadow insurance transactions.”

– NY State Dept of Financial Services (June 2013)

1 2 3

8 © Oliver Wyman 8

9 9 © Oliver Wyman

2013 2014

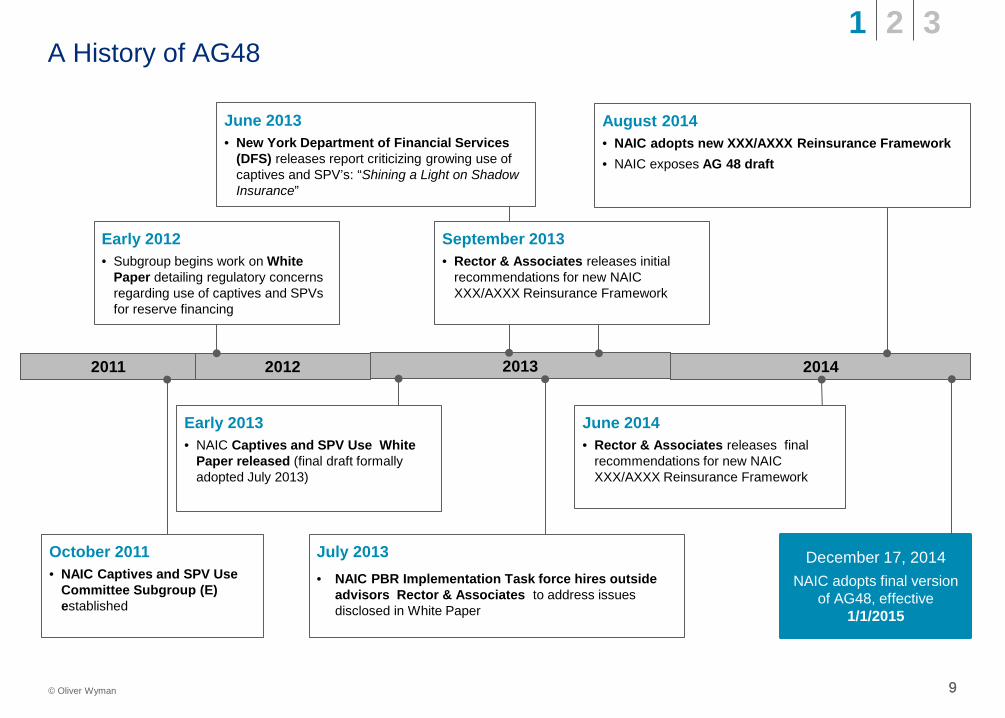

A History of AG48

October 2011 • NAIC Captives and SPV Use

Committee Subgroup (E) established

August 2014 • NAIC adopts new XXX/AXXX Reinsurance Framework • NAIC exposes AG 48 draft

2012 2011

June 2013 • New York Department of Financial Services

(DFS) releases report criticizing growing use of captives and SPV’s: “Shining a Light on Shadow Insurance”

December 17, 2014 NAIC adopts final version

of AG48, effective 1/1/2015

July 2013 • NAIC PBR Implementation Task force hires outside

advisors Rector & Associates to address issues disclosed in White Paper

Early 2012 • Subgroup begins work on White

Paper detailing regulatory concerns regarding use of captives and SPVs for reserve financing

September 2013 • Rector & Associates releases initial

recommendations for new NAIC XXX/AXXX Reinsurance Framework

June 2014 • Rector & Associates releases final

recommendations for new NAIC XXX/AXXX Reinsurance Framework

Early 2013 • NAIC Captives and SPV Use White

Paper released (final draft formally adopted July 2013)

1 2 3

10 © Oliver Wyman 10

Impact of AG48 on reserve “redundancy” Term insurance

While AG48 creates an additional layer of reporting requirements, the newly required level of primary asset for a typical term product is not too dissimilar from the economic reserve in this example

Illustrative example

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30

Res

erve

s

Period

Stat reserve (XXX)

Economic reserve

AG48

1 2 3

11 © Oliver Wyman 11

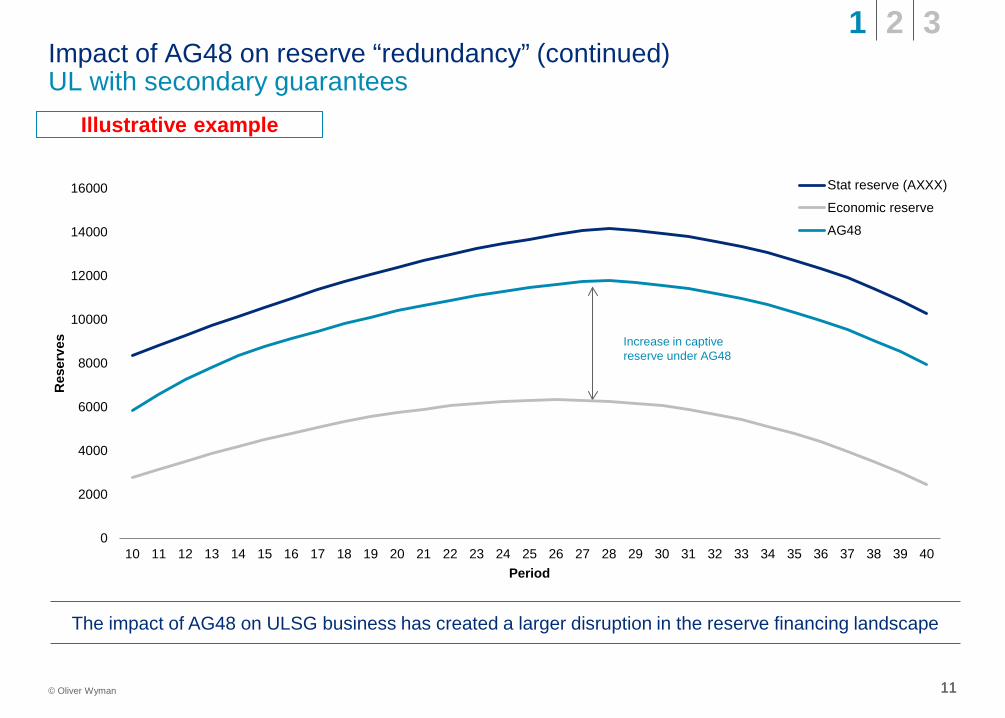

Impact of AG48 on reserve “redundancy” (continued) UL with secondary guarantees

The impact of AG48 on ULSG business has created a larger disruption in the reserve financing landscape

Increase in captive reserve under AG48

Illustrative example

0

2000

4000

6000

8000

10000

12000

14000

16000

10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40

Res

erve

s

Period

Stat reserve (AXXX)

Economic reserve

AG48

1 2 3

12 12 © Oliver Wyman

Industry reaction The response from insurers and reinsurers has been varied

1 2 3 4 Slowdown in 2015 captive activity

Warehousing

Renewed interest in traditional reinsurance

Re-evaluation of product offering

• Observable rush to close deals in YE 2014

• Followed by slowdown in 2015 captive activity

• Some insurers holding on to business to achieve scale due to decreased levels of redundancy

• Begrudgingly accepting strain associated with carrying this business

• AG48 not intended to apply to “traditional” reinsurers

• Co-insurance and mod-co transactions could be seen as alternative to financing mid-sized blocks of inforce business

• Many insurers have taken a “wait-and-see” approach with respect to the financing implications and have not yet re-priced their products

• 2015 has already seen some carriers take ULSG products off the shelf, without replacement

1 2 3

#M&A Market consolidation and new market entrants

2

14 © Oliver Wyman 14

Rest of Market 4% General Re Life

3% Hannover Life Re

11%

Munich American Re

15%

RGA Re 19%

Swiss Re 20%

SCOR Life Re 28%

Rest of Market 5%

General Re Life 3%

Transamerica Re 15%

Munich American Re

12%

RGA Re 22%

Swiss Re 12%

SCOR Life Re 3%

Generali USA Life Re 7%

Scottish Re (US) 16%

Canada Life 5%

US Individual Life reinsurance market share Then and now

2005 market share 2013 market share

Source: Society of Actuaries Life Reinsurance surveys, conducted by Munich American Re

Top 5 as % of total 2013 2005

77% 93%

1 2 3

15 © Oliver Wyman 15

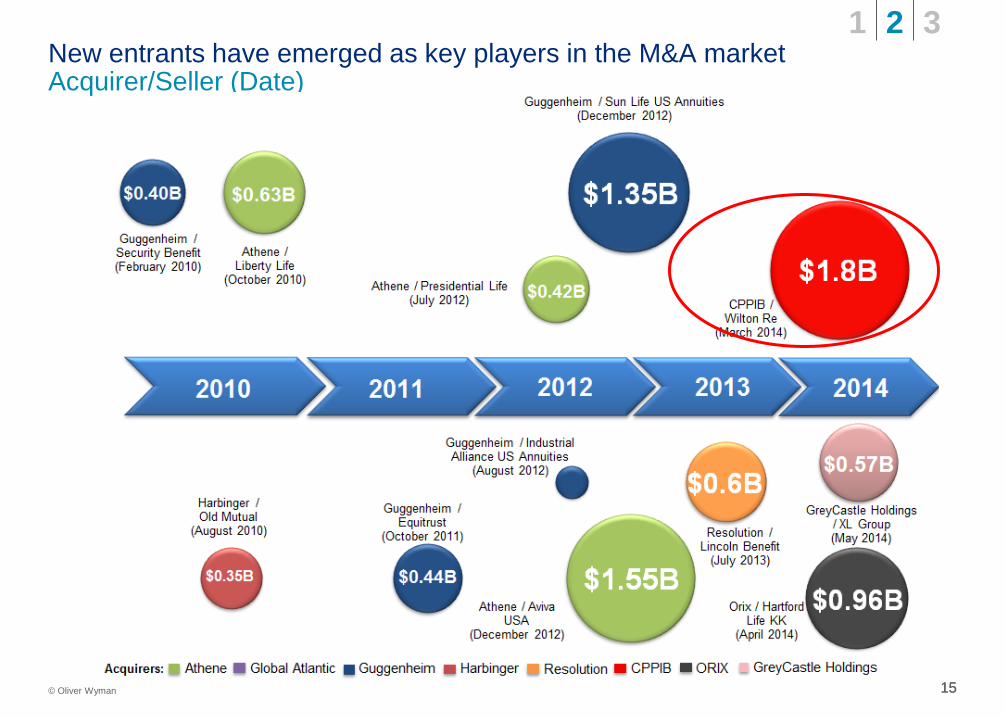

New entrants have emerged as key players in the M&A market Acquirer/Seller (Date)

1 2 3

#Misc Other trends

3

17 © Oliver Wyman 17

Increased sales through automated underwriting

Target: Middle market & millennials

• Convenience

• Faster turnaround

Solution: Rules engines

• Automated underwriting

• Straight-through processing

Byproduct: Predictive Analytics

• Big data

• Predictive underwriting

1 2 3

18 © Oliver Wyman 18

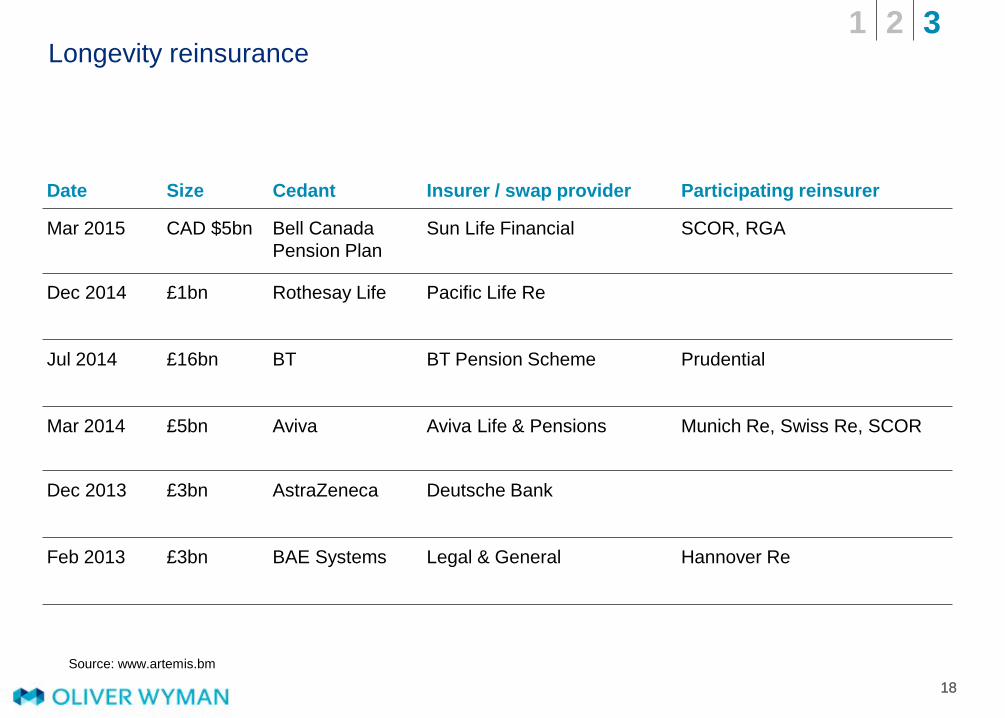

Longevity reinsurance

Date Size Cedant Insurer / swap provider Participating reinsurer

Mar 2015 CAD $5bn Bell Canada Pension Plan

Sun Life Financial SCOR, RGA

Dec 2014 £1bn Rothesay Life Pacific Life Re

Jul 2014 £16bn

BT BT Pension Scheme Prudential

Mar 2014 £5bn Aviva Aviva Life & Pensions Munich Re, Swiss Re, SCOR

Dec 2013 £3bn

AstraZeneca Deutsche Bank

Feb 2013 £3bn

BAE Systems Legal & General Hannover Re

Source: www.artemis.bm

1 2 3

19 © Oliver Wyman 19

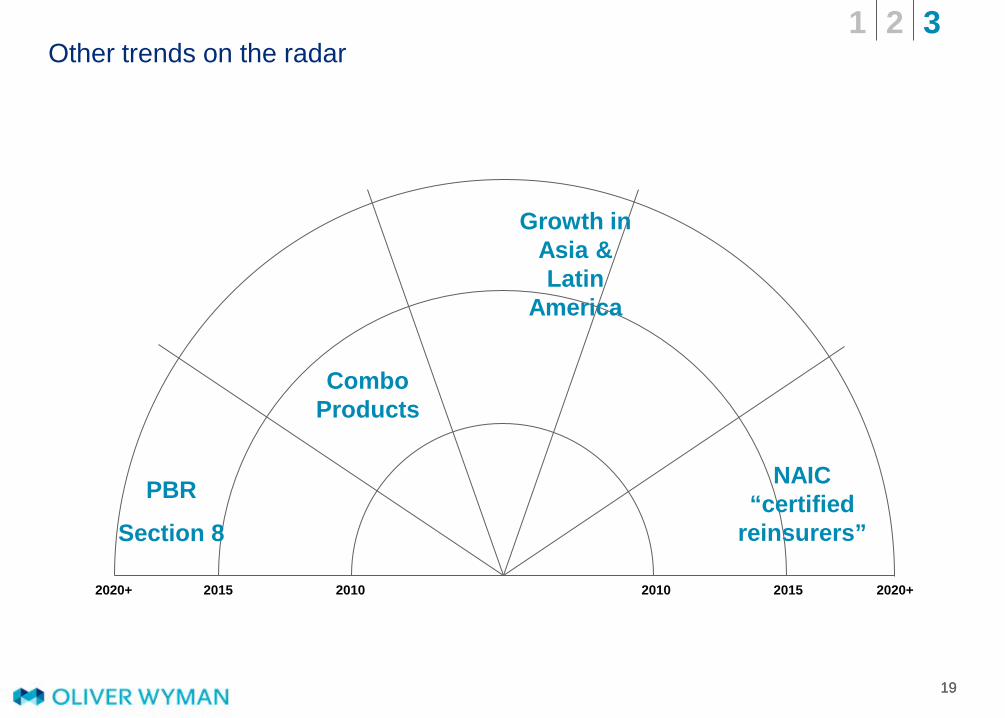

Other trends on the radar

2020+ 2020+ 2015 2015 2010 2010

Growth in Asia & Latin

America

PBR

Section 8

NAIC “certified

reinsurers”

Combo Products

1 2 3

20 20 © Oliver Wyman

Reports of my death have been greatly exaggerated.

Mark Twain