Embed Size (px)

Citation preview

The role and performance of accelerators in the

Australian startup ecosystem

Role Name Organisation Chief Investigator Dr Martin Bliemel UNSW Australia Co-Investigator/s Dr Ricardo Flores

Dr Saskia De Klerk

Dr Morgan Miles

UNSW Australia

UNSW Canberra

University of Canterbury, NZ Student Investigator/s Bianca Costas &

Pedro Monteiro UNSW Study Abroad /

Science Without Borders

(SWB, CNPq)

Thanks!

While we have been researching accelerators for a while, this particular project would not have been

possible without the help of

Thanks for:

- The funding

- Adding legitimacy when approaching accelerators and startups

- Showing genuine interest in the report

About us

Diverse research team (creative industries, nanobio commercialization, international business,

corporate venture capital), mainly based at UNSW (Sydney + Canberra)

Been doing field research about the evolution of accelerators for a couple years

• 2013 conference paper: http://ssrn.com/abstract=2422173

• 2015 conference paper: http://ssrn.com/abstract=2757536

UNSW has its own entrepreneurial ecosystem that is poorly understood, sporadically connected and

operates in context of a larger ecosystem

Context

“No nation in the G20 recorded a steeper drop in patenting than Australia did in the decade to 2012.”

Ian Chubb, Chief Scientist, The Australian, Nov 27, 2015, p. 12.

“The innovation package…(is to achieve) the aim of translating research into economic benefit.” Sarah

Martin, The Australian, Nov 27, 2015, p. 1-2.

TechSydney (launched last week as part of Vivid): “Sydney's global startup ecosystem ranking slipped

from #12 in 2012 down to #16 in 2015.”

#IdeasBoom: Incubator Support Programme starting at $8m, promised to grow to $23m. Disclaimer:

“Programme guidelines and the launch of the programme will occur after the election”

Context

Very low economic diversification *

Late to the VC scene

- Bad timing

- Lacking in experience; Accel out-investing AVCAL

Startup Compass (2015)

- Technologically good, but ..

- “Lacking in startup experience”

Policies in flux:

- CSEF (back to the drawing board)

- Visas (SIV, Entrepreneur) (‘have your say’)

- Employee Stock Options (recently updated)

- R&D Tax (5.3 in 2015 Re:think tax discussion paper)

* http://atlas.cid.harvard.edu/explore/tree_map/export/aus/all/show/2014/

Global context and trends: Hype or here-to-stay?

Genesis?

- 1993 Earliest accelerator (Richards, 2002)

- 2005 Y Combinator is born

- 2009 Seed-db launched. Lists 15 accelerators

2015:

- 786 (f6s.com)

- 592 (CrunchBase Venture Program), with 60% outside the US

- 215 (Seed-db)

- 400 applications (SBA)

- 100+ cities (Founder Institute)

- 70+ across 6 continents & 100+ cities (GAN)

- 70 new accelerators in 3 years (Israel)

- 30 new accelerators in 3 years (Canada)

- 55 (Startupfactories.eu, funded by NESTA)

- 100 corporate accelerators (Future Asia Ventures, 2014/5)

http://www.brookings.edu/research/papers/2016/02/17-startup-accelerator-programs-hathaway

Overarching project scope

Specifically: The scope of this project was to assess the value-add of Australian incubators and

accelerators to the high-growth innovative startups they support, as well as to the local, regional and

national innovation ecosystems. This scope includes exploring their impact on the development of

entrepreneurial networks, improving the performance of the supported startups, and providing

generally positive economic and social outcomes.

While the focus was nominally on incubators and accelerators, other support organisations for startups

were considered, including co-working spaces, angel groups, mentoring programs and training

services. (effectively tripling the scope!)

Generally: Helping DIIS (and others) make sense of:

- Industry reports

- Mass media

- Academic literature

- Field research

Disclaimer:

The project was completed largely over a 2-3 month window while juggling a full-time course load and developing a

MOOC in entrepreneurship (live next week).

Who read the report?

Presentation structure

1. Introduction to the phenomenon: startups and ecosystems in Australia

2. Background literature

3. Field research 1: Support organisations

– Business models

– Performance metrics

– Performance (if available!)

4. Field research 2: Startups

– Why seek support?

– What worked?

5. Policy suggestions

– Bridging (picking winners)

– Buffering (open to any firm)

– Boosting (open to any person)

1. Introduction

‘Startups’ = high growth potential new ventures that need help to achieve their full potential

Required resources:

- People (with a vision, initiative, persistence, … and ideally experience)

- Seed Capital (from founders, friends/fools/family, angels, grants, revenues …)

- ESPIE BITS #IdeasBoom ?

Enabling resources:

- Affordable rent (office and home)

- Preferred service providers

- Feedback (from customers, mentors, investors, industry experts, …)

- a well-connected ecosystem [Kauffman Foundation, 2015]

Strangler, D., & Bell-Masterson, J. (2015) Measuring an Entrepreneurial Ecosystem. www.kauffman.org

Ecosystem Startup

1. Introduction: Australia ecosystem maps

1. Introduction: Australian ecosystem elements

Accelerators:

- 22+ (2015 StartupAus)

- 14 (2015 f6s.com)

- 7 (2015 CrunchBase; US Centric)

Co-working spaces

- 55 (SydStart 2014)

- Up to 130 (2015 Global Coworking Unconference Conference, Sydney)

Angel Organizations

- 12 (Vitale et al., 2006; Dept of Industry, Tourism, and Resources)

- + Sydney Angels, Innovation Bay, ..

Startups

- “over 1,000” (2012 Silicon Beach / Startup Genome)

- ~1,300 (2013 “The Startup Economy”)

- “1,000 tech startups in Australia, or 0.047% of all Australian Businesses” (2014 “Crossroads”)

- “1,200 tech startups in Australia, or 0.06% of all Australian businesses” (2015 “Crossroads”)

- “1,333 responses [..] 385 validated startups” (2015 Startup Muster)

- 365 (2015 CrunchBase)

- 3,113 in Australia and New Zealand (2015 f6s.com)

2. Background literature: Messy!

What are incubators / accelerators? And what do they do?

Confusion in industry: (deliberate or not)

“There was a lot of baggage with the word ‘incubator’’. So, for a long time, we didn't call ourselves

an incubator because it was very negative. We called ourselves a commercialization hub. We

called ourselves an accelerator (before any of the current accelerators started using that label), a

precinct, an ecosystem … lots of words […] but not the I-word” (Bliemel & Flores, 2015).

Confusion in the literature:

• Accelerators are (unfortunately) conceptually linked to incubators (von Zedtwitz 2003; Carayannis

& von Zedtwitz, 2005; Grimaldi & Grandi, 2005; Pauwels et al., 2015)

• Papers about ‘accelerators’ focus on incubators (e.g., Malek et al., 2014)

2. Literature: What is a (business) incubator?

2. Literature: What is a (business) incubator?

First generation?

Second generation?

Third generation?

Fourth generation?

Technology incubator?

Core business model:

- Bricks & mortar

- Some seed funding

- On-demand support

Source: http://www.wired.co.uk/magazine/archive/2011/10/how-to/how-to-build-a-business-incubator

2. Literature: Incubators First & second generation: Occupancy driven

- “In the early days, if you had a heartbeat and more than a dollar in the bank account, you were

welcomed in with loving arms”

Third generation: Value driven

- Churning the “space fillers [and] zombie companies” and “replacing them with high quality, high-

growth businesses, refining our value proposition to our portfolio companies and really focusing

on the value that we can create as an incubator for our incubatees”

- Providing seed capital was also important as a mechanism “to introduce some mutual obligation

to our clients. […] We know that if we have a small piece of equity in the business, we are on level

playing field with the founders. We’re aligned with them. They’ll listen to us because they don't see

us as a landlord sitting in the room, we're a shareholder”

But still high cost of operations (bricks & mortar plus salaries):

- “..there is a group of mentors who sit around the accelerator [..]. We, through our scale, have

chosen to take a different approach by bringing that talent in-house. So the vast majority of the

value that’s delivered to our portfolio of companies is from people who are on the payroll”

* Quotes from Bliemel, M., & Flores, R. (2015) “Defining and Differentiating Accelerators: Insights from The Australian Context”

Academy of Management, Vancouver, BC

2. Literature: Incubators, according to accelerators ..

“Incubator means life support. I hate the term incubator. It has absolute connotations. It's got a higher

education connotation attached to it. Basically, we're going to keep you alive until you potentially fall

across the line and succeed, while hopefully ensuring that you don't quite fail. We're an accelerator.

Our goal is to find teams with highly advanced prototypes [..] because you can't go fast to market with

anything else because of the realities of the technology. So we're about fast-to-market with

enlightened teams with highly advanced prototypes coming to us saying ‘We need six months of work

to finish this off. Will you help us out? Will you pay for us for six months?’ It's for profit. [..] We're talking

about maximizing the chances of success, as opposed to just barely not failing, which is what I see a

typical incubator thing is: ‘We just don't want you to fail. If you're still alive in 10 years, that's a good

thing.’ [..] In my opinion, if you're not a billion dollar company in 10 years, you've actually stuffed up”

(Bliemel & Flores, 2015)

2. Literature: So, what is a (business) accelerator?

Source: http://www.twincities.com/ci_22800822/u-ms-growth-accelerator-aims-boost-small-businesses

Source: MCIC newsletter

2. Literature: Accelerators, according to incubators

“I think the concept of accelerators is kind of naive. It takes longer to build a business that's going to

sustain; you can't just dress up the entrepreneurs and send them out and IPO them. Although we are

getting faster at what we do-it took us about 11 months to graduate KickFire. [..] We did have a

company in and out in two months, but I don't think we helped them that much and they basically left

as soon as they got funding.“(Richards, 2002, p. 151)

2. Literature: An emerging strict definition

Miller & Bound (2011): five main features:

1) [cohort] An application process that is open to all, yet highly competitive;

2) Provision of pre-seed investment, usually in exchange for equity;

3) A focus on small teams not individual founders;

4) Time-limited support comprising programmed events and

5) Intensive mentoring cohorts or ‘classes’ of start-ups rather than individual companies

Challenges:

• Some features overlap (e.g. 1, 4 & 5 are all related to cohorts)

• No mention of terms for equity

• No mention of co-location (peer learning)

2. Literature: Broad ‘definition’

An accelerator is anyone who calls themselves an accelerator

Trying to be as inclusive as possible …

“[It’s] a huge gray area but we loosely define accelerators as cohort programs making equity

investments” (private email)

2. Literature: Accelerators’ 5 defining features 1) Standardised seed investing:

if no equity is involved 0%

if seed investing occurs, but each deal is different 50%

if all startups are offered the same terms 100%

2) Cohort model with DemoDay: *

if there is no cohort model 0%

if there is a cohort model, but no DemoDay 50%

if there is a cohort model with DemoDay 100%

3) Full-time co-location:

if entrepreneurs can remain wherever they currently operate 0%

if participation involves part-time co-location (OR is a full-time commitment) 50%

if participation involves full-time co-location 100%

4) Structured programme: (not necessarily cohort or full-time!)

if there is no program or workshops 0%

if workshops are offered in an ad hoc manner 50%

if multiple workshops are offered as a coherent structured programme 100%

5) Mentoring:

if there is no (formal) mentoring involved 0%

if mentoring is on-demand, in-house or informal 50%

if mentoring is formally facilitated and coordinated 100%

* The cohort model is the foundation for the other features (van Huijgevoort 2012; Dempwolf et al. 2014; Bliemel et al.,

2014; Bliemel & Flores, 2015, Shane, 2015)

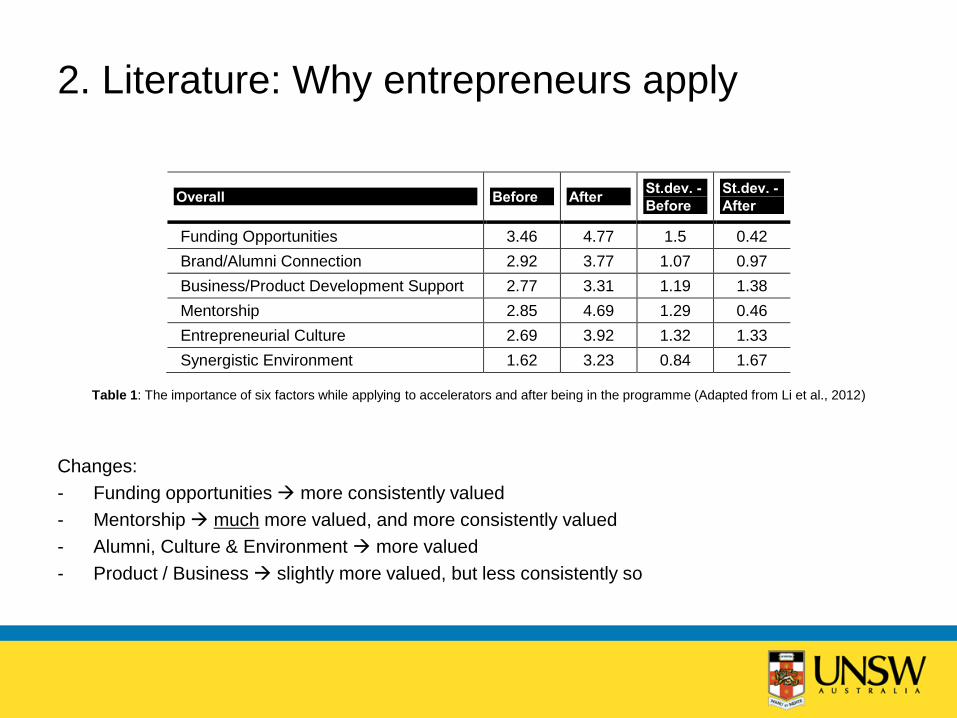

2. Literature: Why entrepreneurs apply

Table 1: The importance of six factors while applying to accelerators and after being in the programme (Adapted from Li et al., 2012)

Changes:

- Funding opportunities more consistently valued

- Mentorship much more valued, and more consistently valued

- Alumni, Culture & Environment more valued

- Product / Business slightly more valued, but less consistently so

Overall Before After St.dev. -

Before

St.dev. -

After

Funding Opportunities 3.46 4.77 1.5 0.42

Brand/Alumni Connection 2.92 3.77 1.07 0.97

Business/Product Development Support 2.77 3.31 1.19 1.38

Mentorship 2.85 4.69 1.29 0.46

Entrepreneurial Culture 2.69 3.92 1.32 1.33

Synergistic Environment 1.62 3.23 0.84 1.67

2. Literature: Incubator and accelerator

Performance metrics Too many (Mian, 1994; Mian, 1997; Bearse, 1998; Sherman & Chappell, 1998; Lewis, 2001; Feeser &

Willard, 1989; Colombo & Delmastro, 2002; Voisey et al., 2006; Wang et al., 2008; Bruneel et al.,

2010; Ganamotse, 2011; Cukier & Middleton, 2012; Garibay et al., 2013; Dempwolf et al., 2014)

E.g. Cukier W. (2012):

2. Literature: Practical impact metrics

Pragmatists: Measure only what really matters (e.g., Barrehag et al., 2012; Kempner, 2013; DEEP

Centre; 2015):

- Survival

- Follow-on funding (FoF)

- Jobs

- Revenues

Challenge:

- Entrepreneurship has power-law distributions (Crawford et al., 2015; Andriani & McKelvey, 2007):

- (i) most die, (ii) some do well, (iii) only a few do really well.

- The performance of (iii) trumps caring about (i) and (ii).

2. Literature: Evidence of accelerators’ impact

Selected matched-pairs samples

Broad sample of incubators (Colombo & Delmastro, 2002; Amezcua, 2010)

- No significant difference in economic performance

Broad sample of accelerators (Hallen, Bingham & Cohen, 2014/2016, n = 164 pairs)

- No significant difference in economic performance

- But … “several substantive learning and network development benefits”

Y Combinator and TechStars vs. other US accelerators (Smith & Hannigan, 2015, n = 389 pairs)

- All: No significant difference in economic performance

- YC/Techstars only: More likely to be acquired, and acquired faster

Random matched-pairs sample (*)

Those who get accelerated twice: (n = 132 “pairs”)

- More likely to get follow-on funding (FoF)

- Higher valuation for each round

* http://blog.imranghory.org/going-through-multiple-accelerators-the-data (Jan 28, 2016)

2. Literature: Indirect impact to consider

(aka a beacon effect)

What happens when an accelerator enters a region?

- Recruiting events More applications

- Guest / mentor talks More interconnections in the community

- DemoDay Others get inspired

- More entrepreneurs turn up & think bigger

- More investors want in on the deal flow

- Searching for $ / startups gets easier

Fehder & Hochberg (2014): Year 1 Year 2 per region (n = 38 regions)

- # of deals: 104% increase

- # of investors: 97% increase

- $$ invested: 1,830% increase

- N/A: Is this specific to the accelerator’s sectoral focus, or beyond?

3. Startup supporters: Method

Initial scope: Identified organisations in Australia who use the accelerator label.

Expanded scope: included at least one of each type of organisation.

46 organisations targeted (more potential targets emerging since then)

- 10 accelerators: AngelCube, ANZ Innovyz Start, Griffin, H2 Ventures, IgnitionLabs, Melbourne

Accelerator Program (MAP), RightPedal, Slingshot, StartMate, Venture Catalyst

- 2 incubators: ATP Innovations (ATPi), iAccelerate

- 1 germinator: Pollenizer

- 1 angel group: Innovation Bay

- 1 mentoring: TiE Sydney

- 2 co-working spaces: SpaceCubed, The Start Society’s iCentral

Structured interviews about their business model, metrics, and performance

3. Startup supporters: They are startups, too

They’re very young

AND they frequently change and hybridize business models

A

B A: ~15% ..

B: .. are 3+ yrs old

3. Accelerator business models Seed funding

- $20-50K (deliberately low) for 7.5-10% (0% for uni)

- $20-500k in-kind (via partners)

- 2-6 page deal sheet. FoF-friendly

Cohorts

- 100-200 applications (“L”-distribution)

- Typically 10 startups / year

- Teams w/ prototypes, traction and ambition

- 1 local DemoDay, sometimes 1+ overseas

Co-location

- High emphasis on peer learning b/w teams

- Usually full-time (also part-time for uni)

- At accelerator + grace period (associated co-working space or incubator)

Programme:

- 3-6 months

- Contact w/ teams and w/ cohort

- Multiple topics: Advice/ guidance with respect to technology, growth hacking, regulatory, etc” as well as “Lean, IP,

Governance, Sales, Pitching, HR, Technology, regulatory, grant application, MVP designs, R&D tax.”

Mentors

- 10-60 active, up to 150 total

- Contact w/team or w/cohort

- Hours, days or on-demand availability

- Usually unpaid (sometimes expenses paid)

3. Accelerator performance

The primary metrics for 10+ accelerators (also with

incubation) were:

- Follow-on funding: 47% of 7 accel’s cohorts

- Exits (& multiples): too early to tell

- Reputation: too early to tell

- Global impact: too early to tell

The secondary metrics for accelerators (also with

incubation) were:

- Ecosystem development: too early to tell

- Growing and sustainable startups (startups’

revenues, positive cashflow and jobs): $40-100k, up

to 30-50 jobs per cohort

Additional considerations:

- Number of interactions within & beyond ecosystem

3. Incubator performance Primary metrics and performance (if available):

- Growing and sustainable startups

- uni-based: startups are too early stage

- ATPi: $45m revenues for portfolio

- Exits (& multiples): ATPi: 8 since 2009

Secondary metrics:

- Global (niche) impact

- Follow-on funding

- ATPi: $121m since 2006

- iAccelerate: 10 startups

- Successful grants: ATPi: $28M

- Ecosystem development: ATPi : 70 / iA: 35

- Reputation: ATPi: 9/10 NPS, awards

- Survival

- Number of jobs created: ATPi: 350+

- Number of products launched: ATPi: 100+/year

Other: Pitch wins

3. Pre-accelerators (Data: N/A or too early)

Business model: Experiential learning cohorts

Primary metrics and performance (if available):

- Just get started (& create jobs). If not with your

current idea, then with your next one

- Founders who ‘fail’ the program are encouraged to

return

- Learning (from program's materials and

interactions)

- Number of interactions within & beyond ecosystem

- Reputation

Secondary metrics:

- Follow-on funding: Global FI franchise reports that

~45% (globally) have received $100k or more

funding from external investors (not friends/family).

- Exits (& multiples)

3. Germinators Business model: Ad hoc, co-founding, with full-time programme

Primary metrics and performance (if available):

- Exits (& multiples): 8/15

Secondary metrics:

- Follow-on funding: n/a

Germinators are more like angel investors (i.e, ad hoc, higher equity) than accelerators or incubators.

Aside: Germination is now only one of many different business models Pollenizer pursues

3. Co-working spaces

Primary metrics and performance (if available):

- Number of interactions: SpaceCubed: 600

- Ecosystem development:

- iCentral: 65-70 startups / 130 ppl

- SpaceCubed: 700 ppl

Secondary metrics:

- Growing and sustainable startups (startups’

revenues, positive cashflow and jobs)

- Global (niche) impact

- Reputation

- Follow-on funding

- iCentral: 8% of startups

- SpaceCubed: via affiliated accelerators

- Exits (& multiples)

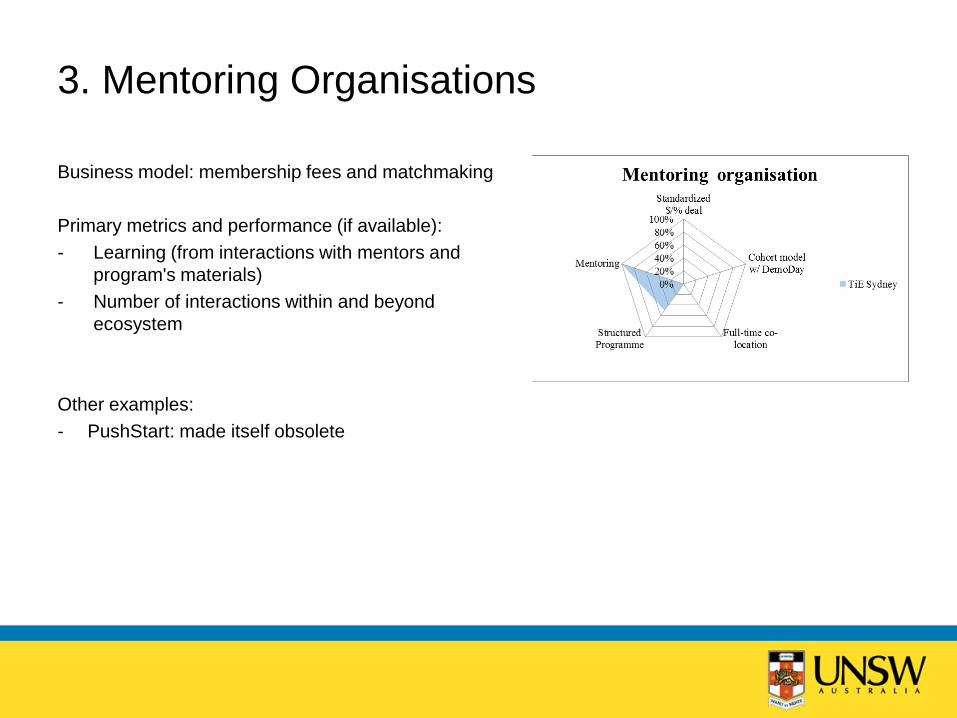

3. Mentoring Organisations

Business model: membership fees and matchmaking

Primary metrics and performance (if available):

- Learning (from interactions with mentors and

program's materials)

- Number of interactions within and beyond

ecosystem

Other examples:

- PushStart: made itself obsolete

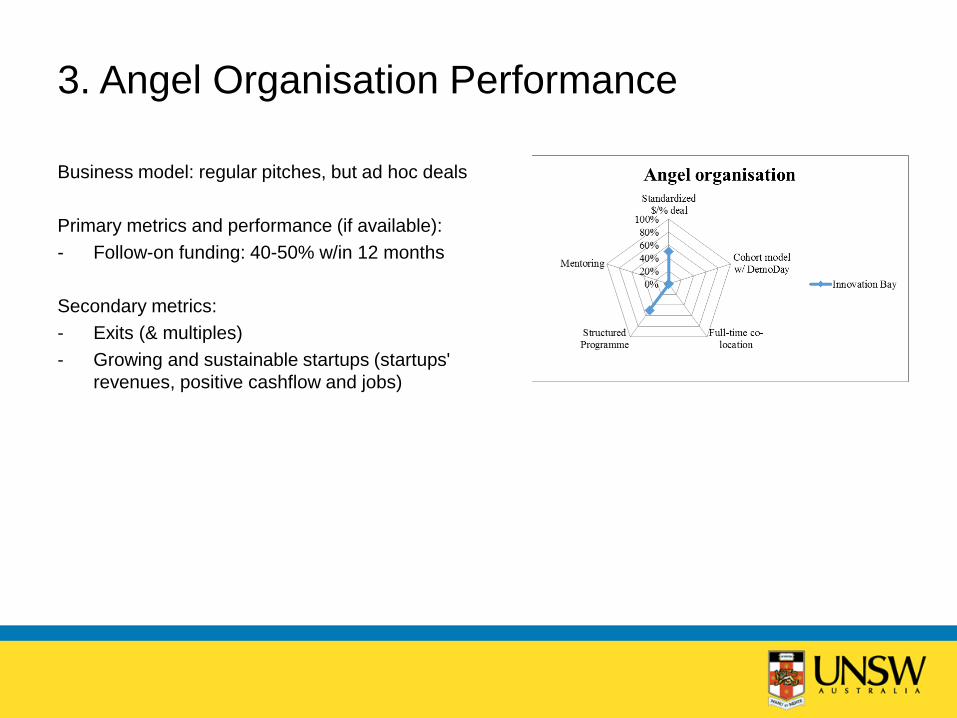

3. Angel Organisation Performance

Business model: regular pitches, but ad hoc deals

Primary metrics and performance (if available):

- Follow-on funding: 40-50% w/in 12 months

Secondary metrics:

- Exits (& multiples)

- Growing and sustainable startups (startups'

revenues, positive cashflow and jobs)

3. Summary

Business models:

- Very different archetypes

- Many hybrids

Metrics:

- Short-term metrics are at best leading indicators

- Long-term metrics are not available yet

Frequent changes in business model make it difficult to establish business model performance link

4. Startups: Method Long form survey: (intro page + 58 questions across multiple pages)

- Launch at SydStart: 2,000 hardcopy invitations in swag bag: 0 responses

- Lists/groups campaign: Silicon Beach Australia, Sydney Startups fb groups: 1 response

Short form: (17 questions on 1 page)

- Twitter campaign: Direct requests to participate and RT: 368 76 usable responses

- 44 supported + 32 independent

A

B A: ~35% ..

B: .. are 2+ yrs old

4. Year launched vs year supported

Incorporation can be done:

- After receiving support (e.g., pre-accelerators, mentoring, co-working)

- Upon receiving support (e.g., germinators, accelerators)

- Prior to receiving support (e.g., angel groups, accelerators, incubators, co-working)

Get support

then launch

Get support

with launch

Launch, then

get support

4. Utility of support gained vs. expectations

Impact of support received:

- 6% No impact (neutral)

- 40% Somewhat positive impact

- 47% Significantly positive impact

In comparison to expected impact:

- 2% Did not meet any expectations

- 7% Fell somewhat below my expectations

- 12% Fell slightly below my expectations

- 16% Met my expectations

- 7% Slightly exceeded my expectations

- 28% Somewhat exceeded my expectations

- 28% Significantly exceeded expectations

Impact was positive AND exceeded expectations (NPS was also almost always 5+)

Unsurprising

Interesting. So what were they expecting?

4. Support sought vs gained

Rank Reason to join Responses

1 contacts 14

2 mentors 13

3 technical 12

4 training 12

5 cash 5

6 investors 5

7 operators 4

8 office 3

9 peers 2

10 accreditation 1

11 (no-other-options) 1

12 communication 1

Rank Best aspects Responses Change in Rank

1 training 20 3

2 mentors 19 0

3 contacts 12 -2

4 peers 9 5

5 cash 8 0

6 space 8 2

7 technical 7 -4

8 investors 6 -2

9 communication 5 3

10 reputation 1 -

11 government 1 -

4. Milestones achieved

Rank Milestone Responses

1 product-market fit

24

2 revenues 16

3 investment 12

4 prototype 9

5 profits 5

6 launch 4

7 award 4

8 hires 4

9 grants 3

10 design 2

11 communication 2

12 partnerships 1

13 patents 1

14 publications 1

Accelerating growth or product-market fit in preparation for growth?

4. Comparison to independent startups

Relatively low numbers (44 supported + 32 independent)

- Similar age and experience

Milestones by independent: very low numbers: 6 usable responses w/ 9 keywords:

- No mention of product-market fit (n/a or simply not taught to think in those terms)

- A few startups reflected significant revenues (scale-free distribution; both groups)

- A few startups reflected significant job growth (scale-free distribution; both groups)

No obvious difference

5. Policy suggestions: Industry reports

Most comprehensive for startups is likely 2015 Crossroads report.

Most relevant to accelerators is likely 2015 OECD report (albeit broad, not deep)

Here: more focus on accelerators and other support organizations, also reinforcing these other reports

and their suggestions.

5. Policies accessed / suggested by accelerators

Few. Most were only indirectly relevant to them, but were directly relevant to their startups.

Suggestions included:

- ESOP improvements (some considered this fixed’)

- Tax deductions (R&D, CGT)

- Entrepreneur Visa (else have to turn-away international applicants)

- Guest speaker / mentor travel costs (Singapore / Chile)

- Bankruptcy laws (improving)

- Matched funding for early stage investors and accelerators (lacking)

- SEIS (in UK) (absent)

- Crowd Sourced Equity Funding (incl better education to mom’s/pop’s about affordable loss)

“The only policy that matters is the R&D tax grant and it is the life blood of the Australian startup

industry (both StartMate and at Blackbird). Every other policy is just noise compared to the universal

positive impact of the R&D Tax grant. Don't touch it or make it more generous for 'startups', according

to the ESOP definition.”

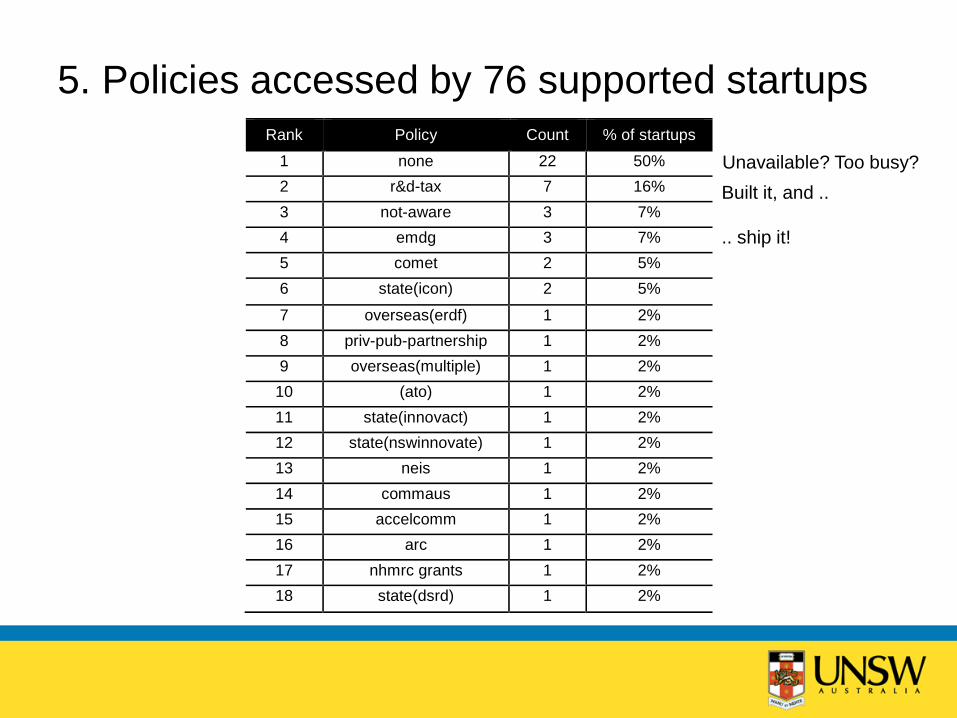

5. Policies accessed by 76 supported startups

Unavailable? Too busy?

Built it, and ..

.. ship it!

Rank Policy Count % of startups

1 none 22 50%

2 r&d-tax 7 16%

3 not-aware 3 7%

4 emdg 3 7%

5 comet 2 5%

6 state(icon) 2 5%

7 overseas(erdf) 1 2%

8 priv-pub-partnership 1 2%

9 overseas(multiple) 1 2%

10 (ato) 1 2%

11 state(innovact) 1 2%

12 state(nswinnovate) 1 2%

13 neis 1 2%

14 commaus 1 2%

15 accelcomm 1 2%

16 arc 1 2%

17 nhmrc grants 1 2%

18 state(dsrd) 1 2%

5. Policies by 32 independent startups Rank Policy Count % of startups

1 none 21 66%

2 r&d-tax 10 31%

3 emdg 3 9%

4 other 3 9%

5 export-credit 1 3%

6 cleantech-ip 1 3%

Unavailable? Too busy?

Rank Policy Count

1 find-matching-seed 11

2 esop 9

3 cgt 6

4 more 5

5 seis(uk) 4

6 r&d-tax(quarterly) 4

7 accel 4

8 tax 3

9 visa-tech 3

10 stem 3

Accessed:

Desired:

Built it, and ..

.. ship it!

Equity (and valuations)

Equity

Equity

5. Policies: Big differences across ‘startups’

Health sciences startups take years to break even

- A biotechnology startup in our sample accessed 6 different programs over 10 years (COMET,

Commercialisation Australia, Accelerating Commercialisation, ARC and NHMRC Grants, R&D Tax

Rebate) and was still pre-revenue.

Internet startups can be profitable within days

- An internet startup in our sample that was launched mid-2015 and supported by Blue Chilli states

“Cash flow positive week 1” as a significant milestone without having accessed any government

policies.

In closing

1. Accelerator model is distinct and highly complementary to incubators, mentors, education, co-

working, and angel groups. But, there are MANY hybrid models and changing models

2. Short-term impact is about learning and networks.

Interestingly, entrepreneurs don’t really know what to expect.

They can always learn more and meet more people, thus building out the ecosystem

3. Longer-term impact is too early to tell. It’s almost futile to attribute back to accelerators if their

business models change so much

4. Policy accelerators are too early stage to pick winners (like VC). It’s about selectively helping each

cohort to have a ‘fair go’, while inspiring others to do the same. But, creating an accelerator takes

specific skills and deep networks (mentors, VCs, service providers, potential customers, ..).

Extensions - Continue this project (ongoing, ideally endorsed by each accelerator)

- Startups: bit.ly/accelerating_aus

- Supporters: bit.ly/startup_supporters

- Do entrepreneurs really develop entrepreneurial capabilities? (in progress)

- NZ lead, looking for Aus partners for pre- & post-acceleration survey:

https://www.surveymonkey.com/r/7RMTZCC

- The role of university education (incl. extra curricular) in training entrepreneurs

- More emphasis on R&D commercialization (e.g. university & CSIRO)

- Regional ecosystem comparison: Adelaide / Brisbane / Melbourne / Sydney (in discussions)

- Closer look at daily operations & interactions to link mechanisms and metrics (ethnography?)

Suggestions welcome, incl. potential collaborators & funding suggestions (sometimes easier to

supervise a PhD/post-doc than to DIY)

Meanwhile: UNSW How to Validate your Startup Idea MOOC

- Preregister at http://bit.ly/startup_MOOC

- Coursera page goes live 7 June (~0830 AEST)