Embed Size (px)

Citation preview

TRUMPONOMICS, TURBULENCE & THE MARKETSJames Holt, Senior Investment Specialist

November 2017

2

HOW MANY THOUGHT YOU’D SEE THIS IMAGE?

3 NFIBSmall Business Trends Survey, Sep 2017

US SMALL BUSINESS CONFIDENCE: LARGEST EVER BOUNCE

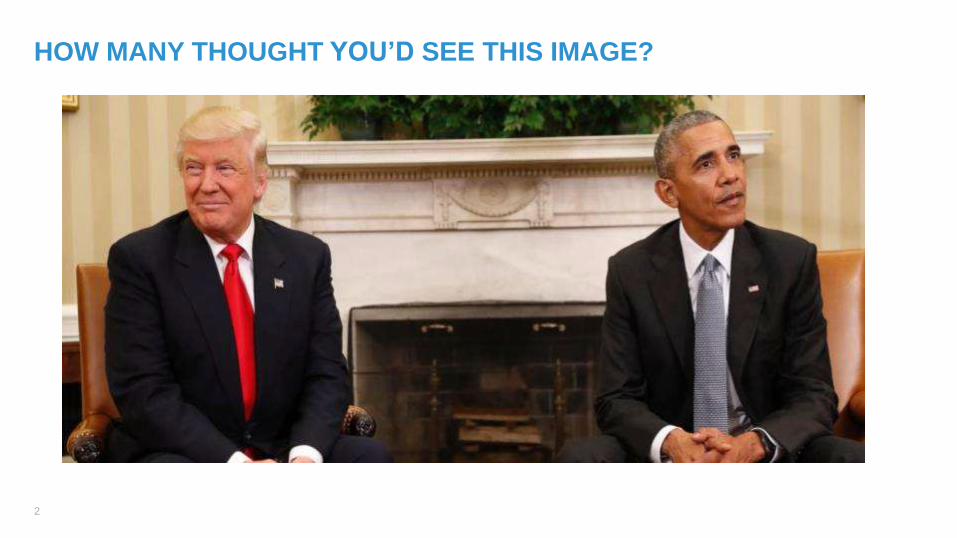

WHICH IS FEEDING INTO “NOWCAST” GROWTH ESTIMATES

4 Source: Fulcrum, Gavyn Davies

5

TRUMP: WHERE DO WE BEGIN?......

BUT WE’VE ACTUALLY SEEN ALL THIS BEFORE

6

7

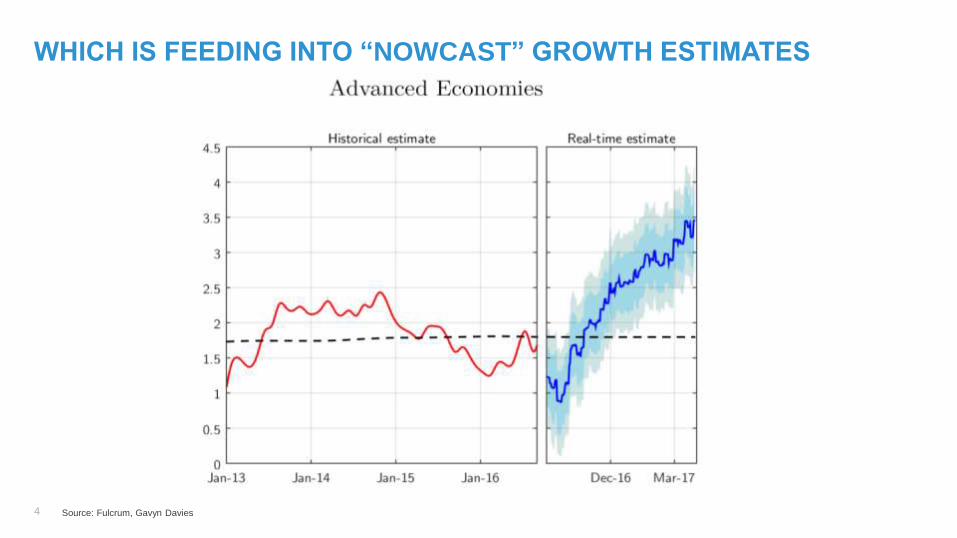

DEFUNCT ECONOMISTS…..

LAFFER CURVE

SUPPLY SIDE ECONOMICS

MERCANTILISM

GAME THEORY

MONETARISM

KEYNESIANISM

WEALTH EFFECT: TOBINS Q

FREE MARKETS

BORDER ADJUSTMENT TAX

8

TRUMP BUMPS & THUMPS FOR EQUITIES & BONDS

1.1

1.3

1.5

1.7

1.9

2.1

2.3

2.5

2.7

2.9

3.1

Aug 14 Aug 15 Aug 16 Aug 17

US 10 yr Treasury Yield

1850

1900

1950

2000

2050

2100

2150

2200

2250

2300

2350

2400

2450

2500

Aug 14 Aug 15 Aug 16 Aug 17

US S&P500

Source: FactSet

9

TRUMPONOMICS: SEPARATING RHETORIC AND REALITY

• Individuals: Reduce 7 tax rates to 4 with and lower top rate

• Corporates: cut tax rate from 35% to 15% (one off tax amnesty of 10%)

• CGT and div tax rate of 20% and eliminate estate tax

• ~ $ 1 trillion infrastructure and defence stimulus

• Abandon or renegotiate FTAs and firm action against China

• Republican Congress: tax reform or tax cuts or chaos?

The market

loves the

green bits

The market

hates this bit

Keep an eye on this space

Congress options on the last point:

• Border Adjustment tax would be a radical reform. Very “America First”

• Cutting spending (e.g. Medicare) could also fund tax reforms

• They might just “do a Reagan” and cut taxes without cutting spending: Fed may react

HOW DID WE GET HERE?INTEREST RATES IN 2007 AND 2016 BY COUNTRY: CASH RATE AND 10-YR BOND RATE

10

0%

1%

2%

3%

4%

5%

6%

7%

2007

2016

-1%

Cash

rate

10-yr

yield

Cash

rate

Cash

rate

Cash

rate

Cash

rate

Cash

rate

Cash

rate

Australia UK United States Canada Germany France Japan

10-yr

yield

10-yr

yield10-yr

yield10-yr

yield

10-yr

yield10-yr

yield

Source: Perpetual Investments May 2017.

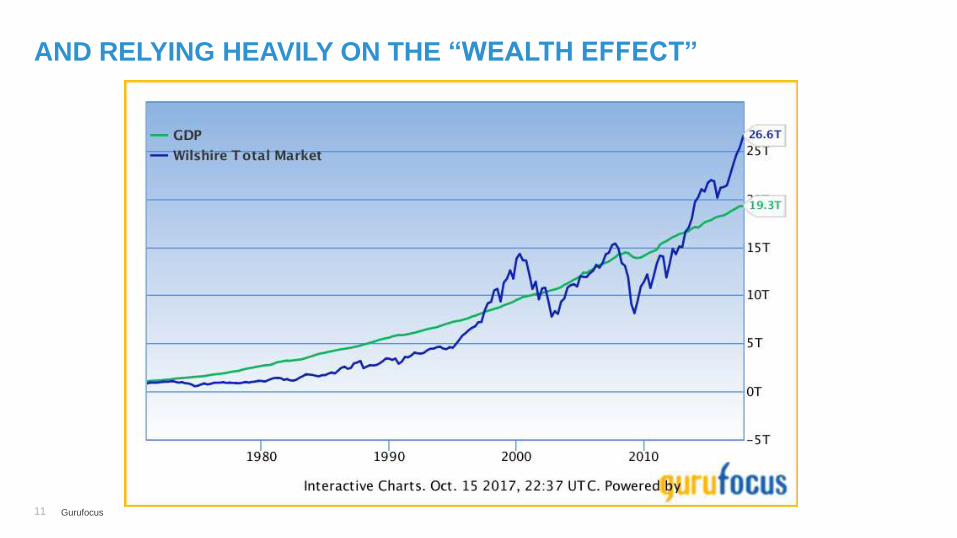

AND RELYING HEAVILY ON THE “WEALTH EFFECT”

11 Gurufocus

HOW DOES THE AVERAGE AMERICAN JOE FEEL?

12

EUROPE: POLITICAL FLASHPOINTS TRUMPING EU

13

• European growth has rebounded, but too little too late for voters?

• Still pressure on the UK until there is certainty

• But more pressure on Europe with 2017/18 events:

• Netherlands March 2017

• French election in April / May 2017

• UK election June 2017

• German elections September 2017

• Italian elections not due until 2018 but may be earlier

CHINA: TURNING POINT

Source: Gerard Minack14

AND CHINA IS EVOLVING

15

• Shift to consumer driven economy under way

• But debt is surging and needs to be brought under control

BUT THERE IS TOO MUCH DEBTGOVERNMENT DEBT AS A SHARE OF GDP (%)

0%

50%

100%

150%

200%

250%

300%

350%

400%

Japan Belgium Holland Spain Italy UK US Canada China Aust. Germany Brazil India Mexico Russia

15 07 15 0715 0715 0715 0715 0715 0715 0715 0715 0715 0715 0715 0715 0715 07

Household debt

Corporate debt

Government debt

Source: UBS Australia Limited and Factset as at 11th January 2016. 16

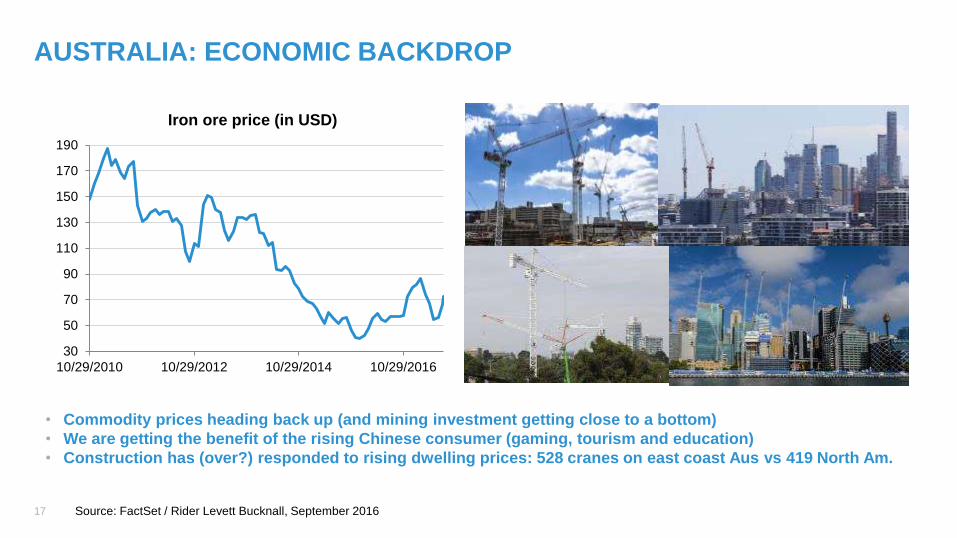

AUSTRALIA: ECONOMIC BACKDROP

Source: FactSet / Rider Levett Bucknall, September 2016

• Commodity prices heading back up (and mining investment getting close to a bottom)

• We are getting the benefit of the rising Chinese consumer (gaming, tourism and education)

• Construction has (over?) responded to rising dwelling prices: 528 cranes on east coast Aus vs 419 North Am.

17

30

50

70

90

110

130

150

170

190

10/29/2010 10/29/2012 10/29/2014 10/29/2016

Iron ore price (in USD)

18

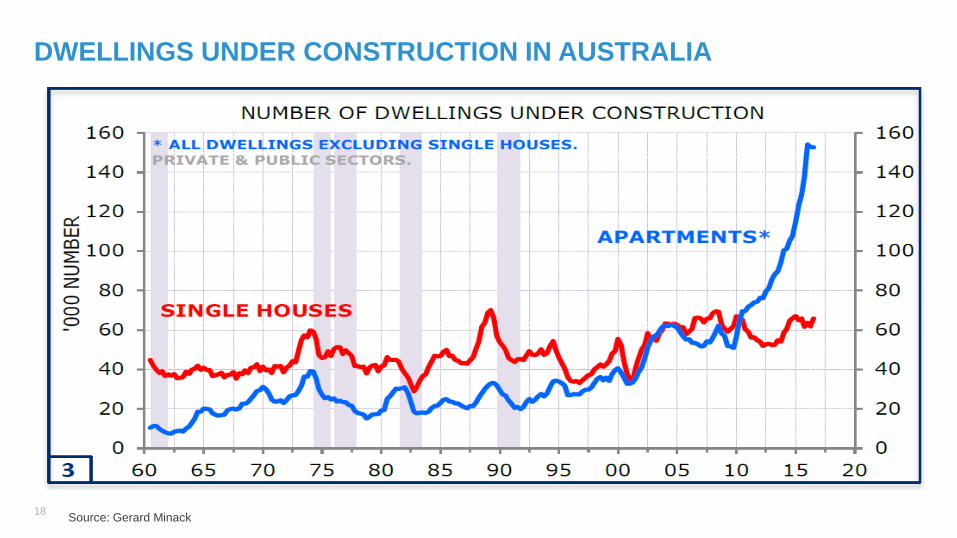

DWELLINGS UNDER CONSTRUCTION IN AUSTRALIA

Source: Gerard Minack

19

VALUE VS GROWTH

Source: FactSet

20

SOME GROWTH BUBBLE EXAMPLES

66,000

10,000,000

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

Cars sold

Car sales in 2016

Cars sold by Tesla in 2016 Cars sold by GM in 2016

0

10

20

30

40

50

60

Price to sales

Price to sales ratios

Snapchat Google

Snapchat yet to make a

profit

Yet trades at 5x Google

P/S

Market Cap:

$54 billion

Market Cap:

$54 billion

Factor Netflix YY Inc.

Subscribers/users 100 million 140 million

NPAT $524m $305m

Market Cap $83 billion $3.76 billion

P/E (based on 2018E) 158x 12x

FactSet as at 21 July 2017

POSITIONED TO PERFORM GOING FORWARDKEY FUND POSITIONS

21

Source: Perpetual.

COMPANY TYPE COMPANY RATIONALE

Consumer BrandsGrowing defensive businesses with longevity in

earrings

Strong free cashflow , balance sheets and

dividendsDiverse customer bases, strong cashflow

Fast growing Asian companies Structural tailwinds in the services sector

Banks with low cost deposits Market leaders with leverage to rising US interest rates

Monopolies/oligopolies High barriers, low capex, stable growing earnings

Online digital advertising companies Dominant search, shift to mobile, rapid E growth

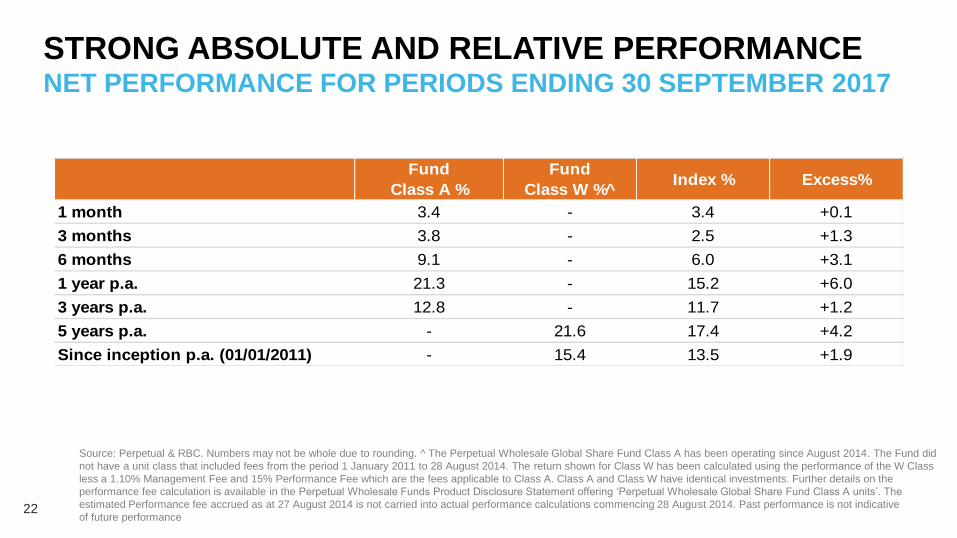

STRONG ABSOLUTE AND RELATIVE PERFORMANCENET PERFORMANCE FOR PERIODS ENDING 30 SEPTEMBER 2017

22

Source: Perpetual & RBC. Numbers may not be whole due to rounding. ^ The Perpetual Wholesale Global Share Fund Class A has been operating since August 2014. The Fund did

not have a unit class that included fees from the period 1 January 2011 to 28 August 2014. The return shown for Class W has been calculated using the performance of the W Class

less a 1.10% Management Fee and 15% Performance Fee which are the fees applicable to Class A. Class A and Class W have identical investments. Further details on the

performance fee calculation is available in the Perpetual Wholesale Funds Product Disclosure Statement offering ‘Perpetual Wholesale Global Share Fund Class A units’. The

estimated Performance fee accrued as at 27 August 2014 is not carried into actual performance calculations commencing 28 August 2014. Past performance is not indicative

of future performance

Fund

Class A %

Fund

Class W %̂Index % Excess%

1 month 3.4 - 3.4 +0.1

3 months 3.8 - 2.5 +1.3

6 months 9.1 - 6.0 +3.1

1 year p.a. 21.3 - 15.2 +6.0

3 years p.a. 12.8 - 11.7 +1.2

5 years p.a. - 21.6 17.4 +4.2

Since inception p.a. (01/01/2011) - 15.4 13.5 +1.9

ETHICAL SRI FUNDPORTFOLIO POSITIONING AS AT 30 SEPTEMBER 2017

23

Source: RBC

TOP 10 OVERWEIGHTS TOP 10 UNDERWEIGHTS

Bega Cheese +5.0 BHP Billiton -5.4 Not in ethical universe

Qube Holdings +4.1 Commonwealth Bank of Australia -4.0

Reece +2.9 Ex-index CSL -3.9 Not held

Graincorp Class A +2.7 Wesfarmers -3.0 Not in ethical universe

Freedom Foods Group +2.7 Woolworths -2.1 Not in ethical universe

Janus Henderson Group +2.6 Rio Tinto -1.8 Not in ethical universe

Fletcher Building +2.6 Transurban Group -1.6 Not in quality universe

Bluescope Steel +2.4 Woodside Petroleum -1.4 Not in ethical universe

Nick Scali +2.4 Scentre Group -1.4 Not held

Boral +1.9 Telstra Corporation -1.3

OVERWEIGHT % UNDERWEIGHT %

ETHICAL SRI FUNDNET PERFORMANCE FOR PERIODS ENDING 30 SEPTEMBER 2017

24 Source: Perpetual & FactSet. Numbers may not be whole due to rounding. Performance figures shown are net fees / pre tax for the Wholesale Ethical SRI Fund. Index used is the

S&P/ASX 300 Accumulation Index

FUND % INDEX % EXCESS %

Financial year to date -0.5 0.8 -1.3

3 months -0.5 0.8 -1.3

1 year 4.5 9.0 -4.5

2 years p.a. 11.5 11.2 +0.3

3 years p.a. 9.5 7.1 +2.4

4 years p.a. 8.6 6.8 +1.8

5 years p.a. 13.7 9.9 +3.8

7 years p.a. 12.9 7.7 +5.3

10 years p.a. 7.8 2.9 +4.9

Since inception p.a. (24/04/2002) 11.9 8.0 +3.9

KEY LEARNING OUTCOMES

25

• Trumponomics: sort the hype vs reality

• If shift from deflation to reflation is true then profound implications

• Everything that has worked well (gearing, yield trade, carry trade, growth etc) could be coming to an end of a long run

• Everything that hasn’t worked may be in vogue (value, quality, clean balance sheets etc) could come back into vogue

This presentation has been prepared by Perpetual Investment Management Limited (PIML) ABN 18 000 866 535, AFSL 234426 for financial advisers only. It is general information only and is not intended to provide you with financial advice. To the extent permitted by law, no liability is accepted for any loss or damage as a result of any reliance on this information. The PDS for the relevant funds, issued by PIML, should be considered before deciding whether to acquire or hold units in the fund. The PDS can be obtained by calling 1800 022 033 or visiting our website www.perpetual.com.au. No company in the Perpetual Group (Perpetual Group means Perpetual Limited ABN 86 000 431 827 and its subsidiaries) guarantees the performance of any fund or the return of an investor’s capital. Total return shown for the Perpetual's Funds have been calculated using exit prices after taking into account all of Perpetual’s ongoing fees and assuming reinvestment of distributions. No allowance has been made for taxation. Past performance is not indicative of future performance.

26