Embed Size (px)

Citation preview

Trends in Banking

(Part-III)

India’s Apple-The HDFC Bank

(HDFC Bank’s Aditya Puri has

created India’s most valuable Bank)

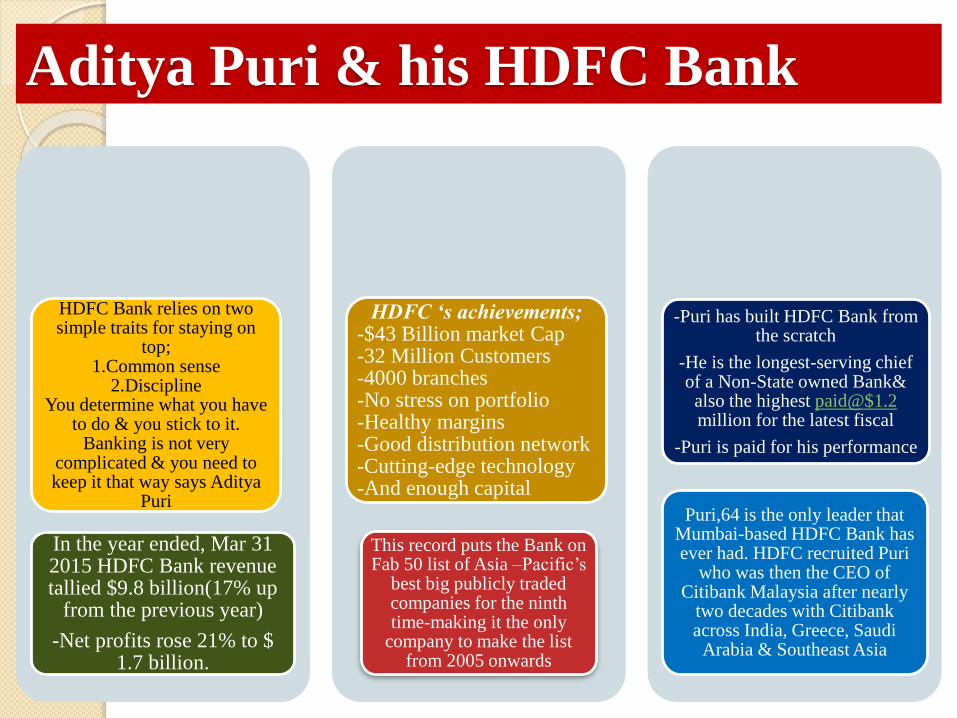

Aditya Puri & his HDFC Bank

HDFC Bank relies on two simple traits for staying on

top;1.Common sense

2.DisciplineYou determine what you have

to do & you stick to it. Banking is not very

complicated & you need to keep it that way says Aditya

Puri

In the year ended, Mar 31 2015 HDFC Bank revenue tallied $9.8 billion(17% up

from the previous year)

-Net profits rose 21% to $ 1.7 billion.

HDFC ‘s achievements;-$43 Billion market Cap-32 Million Customers-4000 branches-No stress on portfolio-Healthy margins-Good distribution network-Cutting-edge technology-And enough capital

This record puts the Bank on Fab 50 list of Asia –Pacific’s

best big publicly traded companies for the ninth time-making it the only

company to make the list from 2005 onwards

-Puri has built HDFC Bank from the scratch

-He is the longest-serving chief of a Non-State owned Bank&

also the highest paid@$1.2million for the latest fiscal

-Puri is paid for his performance

Puri,64 is the only leader that Mumbai-based HDFC Bank has ever had. HDFC recruited Puri

who was then the CEO of Citibank Malaysia after nearly

two decades with Citibank across India, Greece, Saudi

Arabia & Southeast Asia

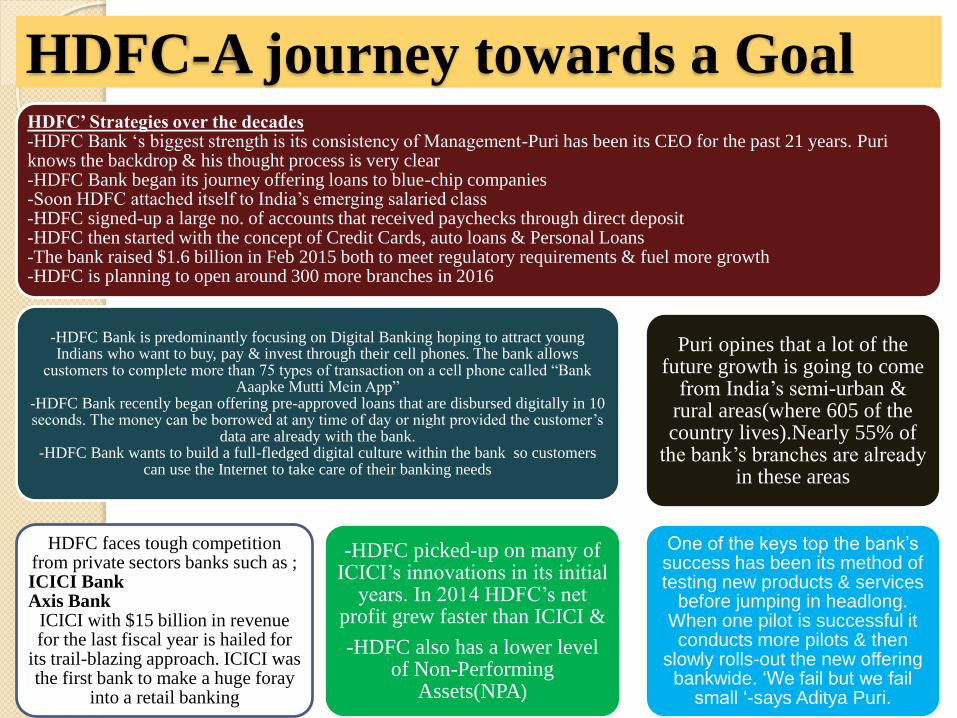

HDFC-A journey towards a GoalHDFC’ Strategies over the decades-HDFC Bank ‘s biggest strength is its consistency of Management-Puri has been its CEO for the past 21 years. Puriknows the backdrop & his thought process is very clear-HDFC Bank began its journey offering loans to blue-chip companies-Soon HDFC attached itself to India’s emerging salaried class-HDFC signed-up a large no. of accounts that received paychecks through direct deposit-HDFC then started with the concept of Credit Cards, auto loans & Personal Loans-The bank raised $1.6 billion in Feb 2015 both to meet regulatory requirements & fuel more growth -HDFC is planning to open around 300 more branches in 2016

-HDFC Bank is predominantly focusing on Digital Banking hoping to attract young Indians who want to buy, pay & invest through their cell phones. The bank allows

customers to complete more than 75 types of transaction on a cell phone called “Bank Aaapke Mutti Mein App”

-HDFC Bank recently began offering pre-approved loans that are disbursed digitally in 10 seconds. The money can be borrowed at any time of day or night provided the customer’s

data are already with the bank.-HDFC Bank wants to build a full-fledged digital culture within the bank so customers

can use the Internet to take care of their banking needs

HDFC faces tough competition from private sectors banks such as ;ICICI BankAxis Bank

ICICI with $15 billion in revenue for the last fiscal year is hailed for

its trail-blazing approach. ICICI was the first bank to make a huge foray

into a retail banking

-HDFC picked-up on many of ICICI’s innovations in its initial

years. In 2014 HDFC’s net profit grew faster than ICICI &

-HDFC also has a lower level of Non-Performing

Assets(NPA)

Puri opines that a lot of the future growth is going to come

from India’s semi-urban & rural areas(where 605 of the country lives).Nearly 55% of

the bank’s branches are already in these areas

One of the keys top the bank’s success has been its method of testing new products & services

before jumping in headlong. When one pilot is successful it conducts more pilots & then

slowly rolls-out the new offering bankwide. ‘We fail but we fail

small ‘-says Aditya Puri.

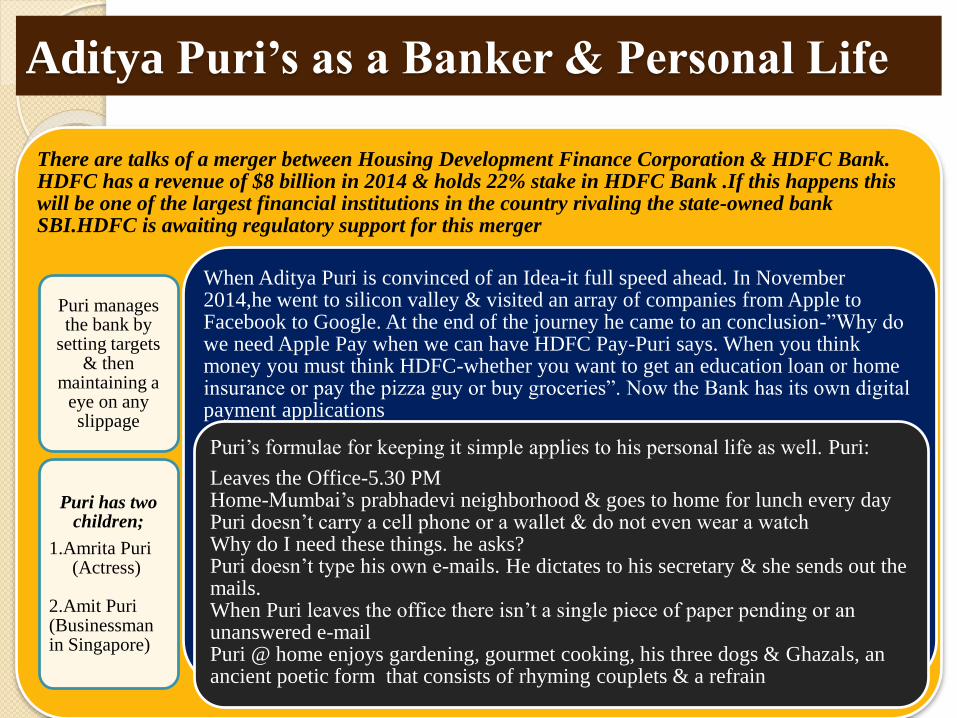

Aditya Puri’s as a Banker & Personal Life

There are talks of a merger between Housing Development Finance Corporation & HDFC Bank. HDFC has a revenue of $8 billion in 2014 & holds 22% stake in HDFC Bank .If this happens this will be one of the largest financial institutions in the country rivaling the state-owned bank SBI.HDFC is awaiting regulatory support for this merger

Puri manages the bank by

setting targets & then

maintaining a eye on any slippage

Puri has two children;

1.Amrita Puri(Actress)

2.Amit Puri(Businessman in Singapore)

When Aditya Puri is convinced of an Idea-it full speed ahead. In November 2014,he went to silicon valley & visited an array of companies from Apple to Facebook to Google. At the end of the journey he came to an conclusion-”Why do we need Apple Pay when we can have HDFC Pay-Puri says. When you think money you must think HDFC-whether you want to get an education loan or home insurance or pay the pizza guy or buy groceries”. Now the Bank has its own digital payment applications

Puri’s formulae for keeping it simple applies to his personal life as well. Puri:

Leaves the Office-5.30 PMHome-Mumbai’s prabhadevi neighborhood & goes to home for lunch every dayPuri doesn’t carry a cell phone or a wallet & do not even wear a watchWhy do I need these things. he asks?Puri doesn’t type his own e-mails. He dictates to his secretary & she sends out the mails.When Puri leaves the office there isn’t a single piece of paper pending or an unanswered e-mailPuri @ home enjoys gardening, gourmet cooking, his three dogs & Ghazals, an ancient poetic form that consists of rhyming couplets & a refrain

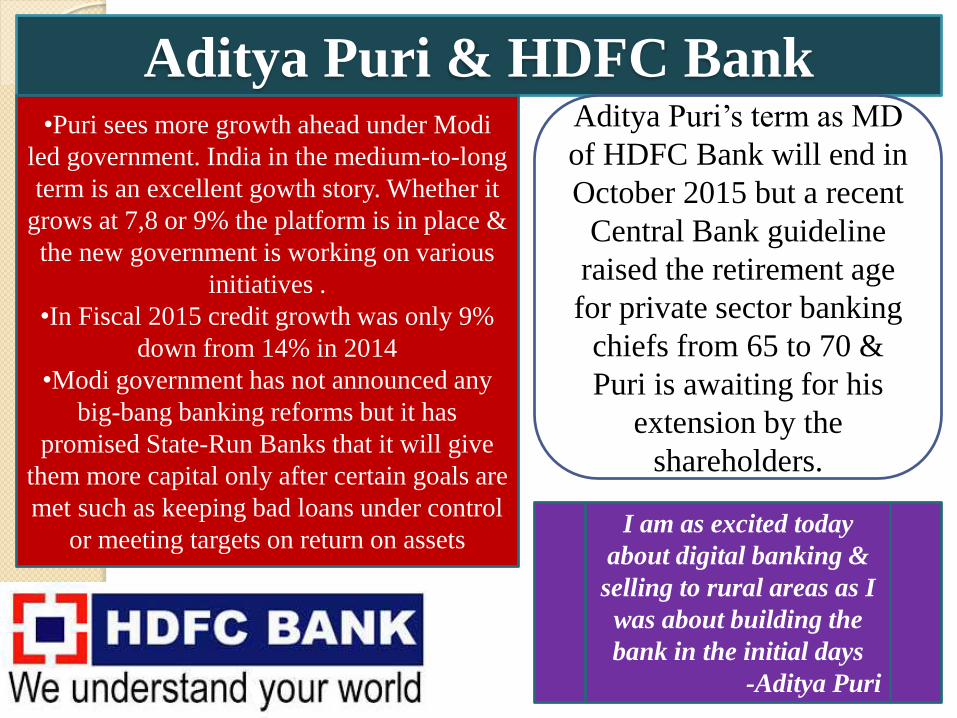

Aditya Puri & HDFC Bank•Puri sees more growth ahead under Modi

led government. India in the medium-to-long

term is an excellent gowth story. Whether it

grows at 7,8 or 9% the platform is in place &

the new government is working on various

initiatives .

•In Fiscal 2015 credit growth was only 9%

down from 14% in 2014

•Modi government has not announced any

big-bang banking reforms but it has

promised State-Run Banks that it will give

them more capital only after certain goals are

met such as keeping bad loans under control

or meeting targets on return on assets

Aditya Puri’s term as MD

of HDFC Bank will end in

October 2015 but a recent

Central Bank guideline

raised the retirement age

for private sector banking

chiefs from 65 to 70 &

Puri is awaiting for his

extension by the

shareholders.

I am as excited today

about digital banking &

selling to rural areas as I

was about building the

bank in the initial days

-Aditya Puri

Protect your Bank from

various Frauds

Digital Financial Transactions while convenient also pose a

threat to your money. Here’s what not to do?

When you carry cash, you run the risk of loosing the money or getting robbed.

Similarly there are risks involved in digital & online banking as well.

According to a June report by PricewaterhouseCoopers Pvt

Ltd(PwC)-As financial institutions use more digital banking channels, the new

technologies make them more susceptible to fraud

The above statement doesn’t mean that one should avoid digital

transactions completely. In fact it’s a convenient & cost-effective method. All one has to do is be aware of the

risks & not disclose any confidential information

such as passwords or PIN

Go Digital

Every Bank’s new Formulae to customers

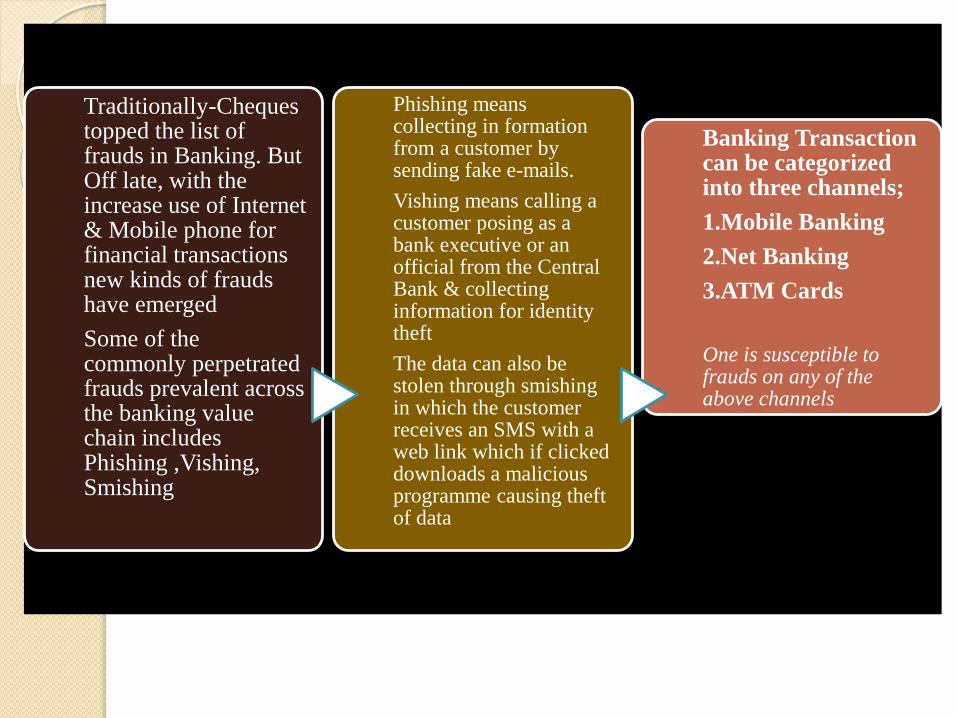

Traditionally-Chequestopped the list of frauds in Banking. But Off late, with the increase use of Internet & Mobile phone for financial transactions new kinds of frauds have emerged

Some of the commonly perpetrated frauds prevalent across the banking value chain includes Phishing ,Vishing, Smishing

Phishing means collecting in formation from a customer by sending fake e-mails.

Vishing means calling a customer posing as a bank executive or an official from the Central Bank & collecting information for identity theft

The data can also be stolen through smishingin which the customer receives an SMS with a web link which if clicked downloads a malicious programme causing theft of data

Banking Transaction can be categorized into three channels;

1.Mobile Banking

2.Net Banking

3.ATM Cards

One is susceptible to frauds on any of the above channels

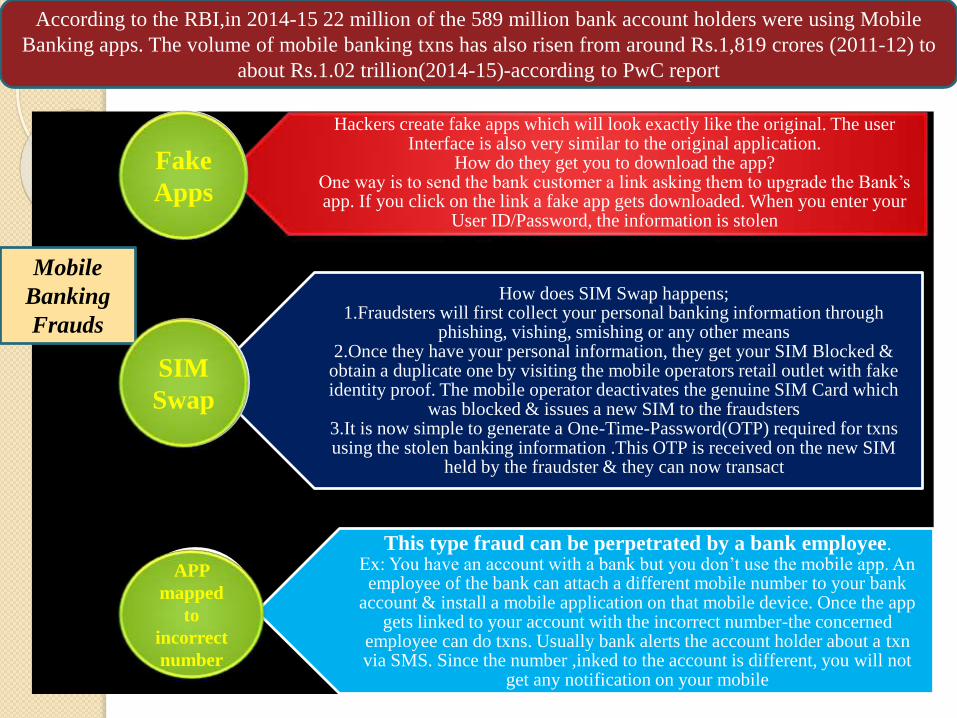

Hackers create fake apps which will look exactly like the original. The user Interface is also very similar to the original application.

How do they get you to download the app?One way is to send the bank customer a link asking them to upgrade the Bank’s app. If you click on the link a fake app gets downloaded. When you enter your

User ID/Password, the information is stolen

How does SIM Swap happens;1.Fraudsters will first collect your personal banking information through

phishing, vishing, smishing or any other means2.Once they have your personal information, they get your SIM Blocked &

obtain a duplicate one by visiting the mobile operators retail outlet with fake identity proof. The mobile operator deactivates the genuine SIM Card which

was blocked & issues a new SIM to the fraudsters3.It is now simple to generate a One-Time-Password(OTP) required for txnsusing the stolen banking information .This OTP is received on the new SIM

held by the fraudster & they can now transact

This type fraud can be perpetrated by a bank employee.Ex: You have an account with a bank but you don’t use the mobile app. An employee of the bank can attach a different mobile number to your bank

account & install a mobile application on that mobile device. Once the app gets linked to your account with the incorrect number-the concerned

employee can do txns. Usually bank alerts the account holder about a txnvia SMS. Since the number ,inked to the account is different, you will not

get any notification on your mobile

Mobile

Banking

Frauds

According to the RBI,in 2014-15 22 million of the 589 million bank account holders were using Mobile

Banking apps. The volume of mobile banking txns has also risen from around Rs.1,819 crores (2011-12) to

about Rs.1.02 trillion(2014-15)-according to PwC report

Fake

Apps

SIM

Swap

APP

mapped

to

incorrect

number

The Point-of-Sale(POS) terminals where you swipe your cards for a transaction & the ATM use the same channels for the Bank called base 24 switch through which your card txn go through. Here fraud may happen if your card gets cloned or skimmed through the POS or ATM

Cloning

Cloning can happen online as well as offline. For Ex: Say you swiped your card at a restaurant where the POS is misused to clone cards or you enter your card details at a fake shopping site. Once you enter the details the fraudsters clone the cards with your details & then use the information to make online purchase. When you use Debit & Credit Cards, theft of identity by use of card readers in restaurants & shops is often done with the help of restaurant waiters & shop sales-persons.

Skimming

This involves a machine or camera that is installed at an ATM to pick up card information & PIN Numbers when customers use their cards. A fraudster acquires this data & withdraws money from the machine

ATM

Card

Frauds

Net Banking Frauds

• Net Banking is now acknowledged as a traditional channel for transaction & has been attached too. The two primary sources of Net Banking fraud are executed through Malware

Net Banking Frauds

• It would either be through stealing passwords from customers or stealing customer details from bank systems. The intent is to access the password for the account to enable siphoning of funds

Net Banking Frauds

• Hackers can also obtain access to a persons mobile phone through malware or cloned/fraudulently obtained SIM Card & then use the information to gain access to the Net Banking Channel

• A secondary & more indirect approach is to hijack a person’s Net Banking session through his/her computer using a malware so that it appears as a legitimate transaction from the account holders computer

Whose liability is it?

If you have been a victim of any of these frauds what should you do?

According to a Master Circular by RBI on “Frauds-classification & reporting”, the central bank has put the responsibility to

provide protection against & fight frauds on banks exposing them to a completely new

horizon of financial risks. Further banks are now required to report to the RBI complete

information on frauds & the follow-up action

While banks are mandated to prevent frauds ,as a customer we can too take

some steps to protect ourselves. Ethical hackers(people who hack to evaluate the level of security & without any malicious

intent)say that users should be very careful when using banking or other apps on which financial txns can be conducted

1.Don’t jailbreak your phone,(Jail breaking is the process of removing hardware restrictions & thus allowing free apps)

2.’Check what you download & run on your phone’. Don’t use WhatsApp for confidential information instead use

encrypted app

3.Limit your Debit Card usage at PoS Terminals & use it only as an ATM Card for cash withdrawl. Try to use Credit

Cards at PoS because if a fraud takes place you can raise a dispute & it is not your money

4.You can also rub off the CVV Number(at the backside of the ATM Card) to be extra careful. But remember it so that you

can continue using the card for dong online txns.

5.Use computer that have anti-virus software for doing financial txns

6.Don’t share passwords, PIN’s & OTP(One-Time-Passwords) with anyone

7.Do not click/log into any links sent on e-mails that require you to revalidate your credentials like User ID/Password

Anup George Rebello

Asst.Manager

The Catholic Syrian Bank Ltd