Embed Size (px)

Citation preview

Presentation: The revival and transformation of Europe’s largest onshore oilfield; the Patos-

Marinza field

Leonidha Çobo, General Manager, Bankers Petroleum Albania Ltd

TSX | AIM: BNK Leonidha Çobo PhD, VP & General Director

March 2015

The revival and transformation of Europe’s

largest onshore oilfield

The Patos Marinza

Disclaimer

Certain information contained herein respecting the Company, the Company's properties or

anticipated financial results or performance of the Company or its properties constitutes

forward-looking information. Such forward-looking information, including but not limited to,

statements with respect to anticipated rates of production, the estimated costs and timing of

the Company's planned work program and reserves determination involve many known and

unknown risks, uncertainties and other factors which may cause the actual costs and results

of the Company and its operations to be materially different from estimated costs or results

expressed or implied by such forward-looking statements. Such factors include, but are not

limited to, risks related to international operations including political risks, general risks

associated with petroleum operations (such as commodity prices, production delays,

production costs, exchange rate fluctuations and environmental costs and risks) and risks

associated with equipment procurement and equipment failure. Although the Company has

attempted to take into account important factors that could cause actual costs or results to

differ materially, there may be other factors that cause costs of the Company's program or

results not to be as anticipated, estimated or intended. There can be no assurance that such

statements will prove to be accurate as actual results and future events could differ materially

from those anticipated in such statements. The forward-looking statements contained herein

are made as of the date hereof and the Company undertakes no obligations to update or

revise any forward-looking statements or information, whether as a result of new information,

future events or otherwise. Accordingly, readers should not place undue reliance on forward-

looking information.

3

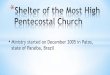

Company Overview

Stock Exchange Symbol: BNK TSX – Toronto | AIM – London

Total Shares 261 Million (285 Million fully diluted)

Share Price $ 2.69 (as of March 11, 2015)

Market Capitalization CDN $772 Million

Liquidity 2 Million shares/day (3 months average)

Research Coverage 15 analysts provide coverage

Bankers Petroleum Ltd. is an international E&P company with

operational focus in Albania.

4

Canada United StatesUnited Kingdom FranceAustralia & NZ Other EuropeAsia

Ownership by Region

Assets Overview

Patos-Marinza Oilfield

• Largest onshore oilfield in Europe

• 100% W.I. and operatorship

• 191 Million Barrels – 2P Reserves

Kuçova Oilfield

• 100% W.I. and operatorship

• 12 Million Barrels 2P Reserves

• Drilled first horizontal well in 2014

Block F Exploration Acreage

• Prospective for natural gas

CORE FOCUS AREA ACCESSIBLE TO REGIONAL AND INTERNATIONAL MARKETS

5

Investment Highlights

Capital Investment (CAPEX) ~ 1.3 billion USD ~500 million last 2 years

Large Primary Reserves 203 Million barrels 2P 5.4 Billion barrels OIIP

Strong Record of Production

Growth 1.2 million tons production in 2014 ~ 6 million tons produced since 2004

Contribution to Albanian State

Finances and its Agencies

~500 million USD since 2004 ~230 million USD as Royalty Tax

~190 million USD to Albpetrol as PEP&ASP

~80 million USD as C&C, excise, local taxes, personal etc.

Largest FDI in Albania 35% of FDI for the first three quarters of 2014

701 million USD total FDI for Q1-Q3 2014

Strong Balance Sheet 2014 year end cash position of $73 million 2015 capital program fully-funded

6

Albania’s largest producer, foreign investor and contributor to Albanian Economy

-

4,000

8,000

12,000

16,000

20,000

1939 1944 1949 1954 1959 1964 1969 1974 1979 1984 1989 1994 1999 2004 2009 2014

(bo

pd

)

Albpetrol Bankers AAP

History of Patos-Marinza

1928 – 1990 Patos-Marinza was first discovered by APOC (Anglo Persian Oil Co.) and developed in stages.

1990 Fall of Communism in Albania

1995 – 2004 AAP (Anglo Albanian Petroleum, a JV between Premier Oil , IFC, OMV, and Albpetrol) signed a

concession agreement, but due to contract terms, weak oil price environment and technical

challenges, the foreign partners relinquished the field in early 2004.

2004 - 2007 Bankers Petroleum negotiated and signed a new PA & LA in July 2004 and grew production from

400 to 6,000 bopd through reactivation of legacy vertical wells.

2008 – 2012 Growth of production from 6,000 to 15,000 bopd through development and delineation drilling of

new horizontal wells across 11 different reservoir zones and multiple areas of the field.

2013 - 2014 Two year average production growth of 17.5% through a strategy of primary development with

horizontal wells, validating secondary recovery techniques, and reducing costs through operational

efficiencies in the field

Average Historical Patos-Marinza Production

7

0

2,500

5,000

7,500

10,000

12,500

15,000

17,500

20,000

22,500

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Pro

duction (

bopd)

Ho

rizo

nta

l We

lls: 4

29

Ve

rtica

l We

lls: 1

07

8

KNOWLEDGE TEAM AND INFRASTRUCTURE TO DELIVER STEADY GROWTH

Bankers Quarterly Production

• Operational flexibility to adjust pace of drilling with oil prices

Execute Horizontal Drilling Program

• 19 polymer and 4 water flood patterns to end of 2014

• Initial production results are performing in line or exceeding expectations

• Up to 20 - 30 polymer conversions anticipated in 2015

Accelerate Polymer Flood Program

• Optimize treating process and sourcing to reduce diluent costs

• Install flow lines to reduce infield trucking

• Reduce energy costs through alternate fuel use

Operational Improvements to

Reduce Costs

Three-Part Operational Strategy

9

Reserves Value / Metrics

December 31, 2014

Reserves 125 Mbbls 203 Mbbls

Patos-Marinza 122 Mbbls 191 Mbbls

Kuçova 3 Mbbls 12 Mbbls

Reserve Life Index 17 years 27 years

Net Present Value

at 10% After Tax (US$ Millions) $734 $1,802

Per Share ($CDN) Exchange rate as of Feb. 20, 2014

$3.49 $8.57

Finding and development costs $22.57/bbl $12.69/bbl

Future capital (Millions) $2,001 $2,115

Number of Hz wells (at Patos-Marinza)

870 882

10

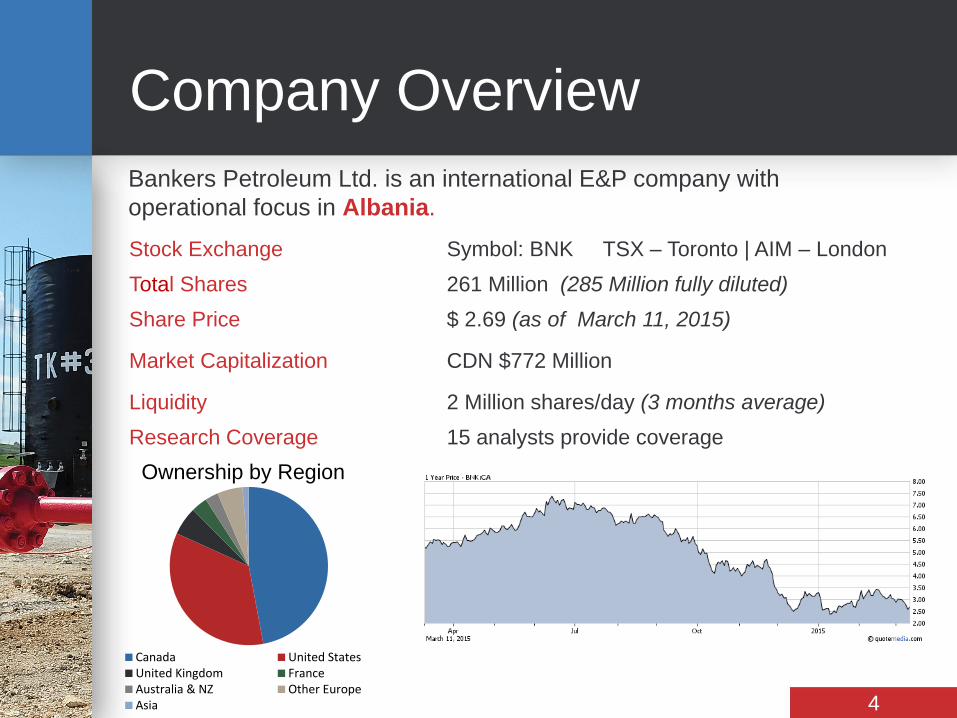

Reservoir Characteristics & Development Strategy

Primary Development

• Horizontal Drilling & Reactivation of Existing Wells

Secondary and Tertiary Development

• Reduced Space Pattern Drilling

• Water Flood – Viscosity 50cP to 500cP

• Polymer Flood – Viscosity 500cP to 2500cP

• Additional Core & Data Collection for Tertiary

• Tertiary - Viscosity > 2500cP

Reservoir Description

• Well Depth: 300 to 2,000m

• Sandstone Reservoir

• Up to 300m Gross & 200m Net Oil Pay

• Porosity 25 to 30%, Permeability 100 to 2,000md

• API 5° to 20°, Live Oil Viscosity 50cP to 80,000cP

Wa

ter a

nd P

oly

me

r Flo

od 8

–20 A

PI

I Gora

ni I D

riza I M

arin

za

50 m

Prim

ary

Horiz

onta

l Drillin

g 8

-20 A

PI

Tertia

ry D

evelo

pm

ent 5

–10 A

PI

Composite Type Section

11

Primary Development and Margin Expansion $125 Million

• 2 drilling rigs, 60 horizontal wells to be drilled

• Gathering and flow line systems

• 1 water disposal well

• Large programs for electrification, pump upsizing,

and other OPEX reductions

EOR Development $28 Million

• Capital allocated for 20 wells to be converted for

water and polymer injection

• Associated facilities

• Shifting from pilot to development phase of the EOR

project

2015 Capital Program of $153 M

12

Drilling Workovers Facilities Disposal Others

Facilities Well Conversions

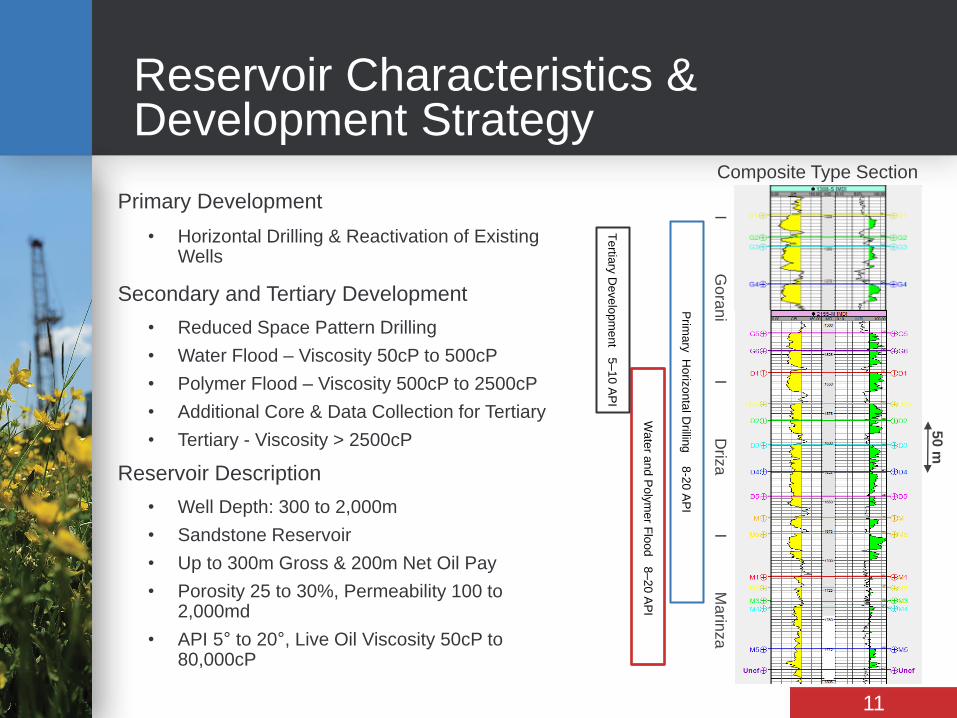

Development Program

• 60 primary horizontal wells to be

drilled in 2015

• 558 horizontal wells drilled to the

end of Q4 2014 (includes 24

lateral redrills)

• 20 – 30 EOR conversions

planned in 2015

• 23 patterns in place to date

(includes 19 polymer flood and 4

water flood patterns)

• 882 future horizontal well

locations and ~54 future EOR

patterns (based on 2P Recovery

Case YE2014)

Historical Drilling Program by Zone 2014 locations in red

Marinza & Bubullima

Gorani Upper Driza

Lower Driza

13

Netbacks

Netback ($/bbl) 2013 2014 Q4 2014

Brent $108.66 $98.95 $76.58

Sales Price

(% of Brent)

$85.39

(79%)

$77.26

(78%)

$57.29

(75%)

Royalties $14.22 $11.39 $8.36

Transportation $2.44 $2.38 $2.46

Energy $2.88 $2.25 $2.21

Well Servicing $2.77 $2.25 $2.18

Other $5.25 $5.75 $6.17

OPEX $13.34 $12.63 $13.02

Net Diluent $7.29 $5.67 $7.19

Transportation &

Terminal Fees $2.81 $2.21 $1.71

Sales &

Transport $10.10 $7.88 $8.90

Netbacks $47.73 $45.36 $27.01

14

$0

$10

$20

$30

$40

$50

$60

2009 2010 2011 2012 2013 2014

2015 Sales Contracts

Export Market

• 55% of 2015 volumes will be sold to the export market

• All export volumes committed to contracts at 79-80% of Dated Brent

• Counterparties in the Mediterranean, the United States

Domestic Market

• 45% of 2015 volumes will be sold to domestic refiners

• Agreement for 74% of Dated Brent FOB Vlora

15

Export Partners REPSOL

Spain

OMV

Austria

ENI

Italy

API

Italy

MOCOH

Trader

16

Surface Infrastructure Optimization

Lease Construction Well Pad Tie ins, Treating, Testing, Sour

Handling, Control & Automation

Satellite Treating

Facility

(Pad D/H, Sat 3)

Central Treating Facility (CTF)

Fier Hub Storage Sales Oil Transfer

Storage at PIA

(increasing storage &

loading capacity)

Tanker

(increasing load size

from 20,000 to

40,000MT)

Production

Gathering System

Disposal Pipeline

Water Disposal System

Disposal sites WTP

EOR Program

• 23 EOR patterns in operation at end of 2014, positive results to date

• 11.3 million barrels 2P Reserves booked in 2014

• 20 – 30 projected conversions in 2015 • half of planned conversions are expansion to existing patterns, half will be testing new areas

with high viscosity and thicker reservoir zones

• Polymer Flood

• 1st Polymer pattern initiated late Q1 2013

• 19 injection wells in 3 different zones at the end of 2014, distributed evenly in the D5, D4 and D3

• Viscosity range tested: 700 – 1,600 cP

• Water flood

• 1st pattern initiated in late Q2 2013

• 4 injection wells in the Upper Marinza (M0 and M) formation at the end of 2014;

• Viscosity range tested: 10 – 700 cP (best results in lower viscosity (<150 cP)

17

EOR Well Performance

18

0

1

2

3

4

5

6

7

8

9

10

0

50

100

150

200

250

0 10 20 30 40 50 60

Patt

ern

Co

un

t

Oil R

ate

(b

bl/

d)

Months On Injection

Average Polymer Flood Profile

1P Recovery Case (7%) 2P Recovery Case (8%) 3P Recovery Case (10%)

Oil Rate Primary Recovery Case Pattern Count

(6%)

0

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014

0

50

100

150

200

250

300

350

2009 2010 2011 2012 2013 2014

Strong Balance Sheet

CAPEX (Millions of US$)

LIQUIDITY at December 31, 2014

Adjusted Cash Flow* (Millions of US$)

Working capital of 201 Million; CASH of $73 Million

Credit Facilities Facility Utilized Approved

Raiffeisen Bank $20 Million $0 Million $20 Million

IFC / EBRD $204 Million $104 Million $100 Million

Total $224 Million $104 Million $120 Million

Financial hedge (Put Option) in place 2015 - 6,000 bopd at $80/bbl Dated Brent 19

* Before contract settlement expense

Previous Albpetrol well

Re-activated well

LIABILITY MANAGEMENT BY CONTINUOUS CLEAN-UP

Health, Safety, Environment &

Community Relations

Environmental

•Clean-up and remediation

•Meeting International

standards

Economic Development

•Agricultural Programs

•Supporting Sustainable

business

Stakeholder Engagement

•Building Capacity

•Reducing Impacts

•Occupational Training

Health & Safety

•Creating safe work environments

•Trained and competent workforce

20

Corporate & Social Responsibility

21

Corporate & Social Responsibility

Program

Community Investments by Year

TOTAL

2012 2013 2014

Economic Development $ 190,628 $ 532,116 $ 740,327 $ 1,463,071

Quality of Life Improvement $ 288,851 $ 497,894 $ 375,022 $ 1,161,767

General Local Plans/ Compliance/ Other

$ 33,774 $ 690,213 $ 231,240 $ 955,227

TOTAL $ 513,253 $ 1,720,223 $ 1,346,589 $ 3,580,065

Examples of Investments: • Economic Development: 690 students have graduated from Bankers

Vocational and English Training Programs to date • Quality of Life Improvements: Bankers collaborates with local Communes

and Municipalities to invest in local roads, schools, parks and health clinics • General Local Plans: In 2013, Bankers supported seven Communes and

Municipalities in our area to develop General Local Plans

David French

President & CEO

Rob Carss

VP, HSSE

Doug Urch

Executive VP Finance

& CFO

Leonidha Çobo

VP & General Director

Albania

Suneel Gupta

Executive VP & COO

Mark Hodgson

VP, Business

Development

Bayne Assmus VP, Production & Operations

Craig Nardone

VP, Exploration &

Development

Management Team

22

Board of Directors

Robert Cross, Chairman Private investor; over 20 years experience financing companies in the resource sector and is on the board of several Canadian energy and mining companies

Abdel (Abby) Badwi, Vice Chairman

Retired from President and CEO of Bankers Petroleum in April 2013; more than 40 years experience in the exploration, development and production of international oil and gas fields. Previously President and CEO of Rally Energy Corp.

Eric Brown President, E.M.Brown Consulting Corporation. Previously held the position of Regional Managing Partner for Meyers Norris Penny, LLP

General Wesley Clark (ret.) CEO, Wesley Clark & Associates since 2004; Chairman of Rodman & Renshaw from February 2006. Senior Fellow, UCLA’s Burkle Centre for International Relations

David French President and CEO, Bankers Petroleum since April 2013; 23 years experience in the development and production of oil and gas fields in North America and overseas. Previously held the position of VP, Business Development, of Apache Corporation

Jonathan Harris Business Consultant, Genet Consulting Ltd since February 2005; Chief Operating Officer and Director of Anglo-African Minerals Plc from May 2009 to February 2012; Previously COO of Tribeka Ltd and director of Eastern Platinum Ltd. London, UK based

Phil Knoll President, Corridor Resources from October 2010 to September 2014; Executive Vice President, Duke Energy from March 2002 to July 2005; Director of Corridor Resources, AltaGas Utility Group; former Director of Rally Energy

Ian McMurtrie Previously Executive VP, Exploration & Development, Bankers Petroleum Ltd. and Vice President, Exploration of Rally Energy Corp. Former Chairman, Porto Energy Corp.

John Zaozirny Vice-Chairman, Canaccord Financial Inc.; Previously Counsel, McCarthy Tetrault LLP. Currently on the Board of Directors for numerous Canadian oil and gas companies

23

Analyst Coverage

Canaccord Genuity Christopher

Brown

Industrial Alliance

Securities Amin Haque

CIBC Dave Popowich Mackie Research Mark Heim

Cormark Securities Garett Ursu Pareto Securities Aaditya Chintalapati & Thomas Aarrestad

Credit Suisse David Phung RBC Capital Markets Al Stanton

Dundee Capital

Markets David Dudlyke Scotiabank Gavin Wylie

FirstEnergy Darren Engels TD Securities Jamie

Somerville

GMP David Beddis Wood & Company Robert Rethy

Haywood Securities Darrell Bishop

24

Thank You