Embed Size (px)

Citation preview

Give Missed Call : 08049336177SMS JeTrade to : 9601336677

SEBI REGISTRATION NO.:NSE:INB/F/E 230823233, BSE:INB/F 010823233, MCX SX:INE:260823233 and NSDL:IN-DP-NSDL-166-2000 NCDEX:TMID 00749 / FMC REG NO.NCDEX / TCM / TCM / CORP / 0736 MCX: TMID 29040/FMC REG NO.MCX/TC/CORP/0963Note* : Dealing in commodity segment through it’s grop company jhaveri credit & capital Ltd. Distributer for IPOs & Mutual Funds. Past performance is not a measure for future returns

JHAVERI SECURITIES LTD301/302, Payal Tower-II, Sayajigunj Vadodara - 390020, Web.: www.jhaveritrade.com I www.jetrade.in

Ph.: + 91 265-3071200

Faster Smarter & Simpler

Trade Whenever & Wherever

For Demo & More Detail No Hidden Charges

Easy to Operate

Trade in EQUITY / FUTURE / OPTION

Common Market Watch for all Segment i.e. BSE,NSE & NSEFO

Live Price Movement

Live Chart

Track your DP Holding & Balance

Global Market

Jhaveri Research

FREE OF COST

www.jhaveritrade.com

Market View

Last week the market has scaled yet another high and ended above 8450/28300. The stimulus talks in euro zone and in Japan coupled with the rate cut by china is fueling the world market. India has many reasons for the rise and new high in themarket. The talks of remarkable reforms / new bills to be introduced in the winter session of the parliament starting from 24thNovember and some more aggressive reforms on LPG front are some of the few reasons. The mega deal by KotakMahindra bank and ING Vysya bank has really put the financial and banking sector on fire. But the most important thing atpresent is to select the stock which can go higher from this level. In the time of golden decade and mega trend one has to bemore selective and has to adjust his strategies to find companies that are set to ride the overall up swing. Such companiestypically fall in three categories and are set to break new ground and succeed in today's market.

Three kinds of companies to watch for are,a) Organic revenue generatorsb) Efficiency vendorsc) Innovators

Organic revenue generator companies are the companies that can grow at brisk pace without much capital cost. They haveto spend little but can grow remarkably, for e.g. Page industries and nestle. They have good brands and ability to groworganically and competition cannot hurt them because of their branding. Capital expenditure is also low with minimumadvertising or hiring cost. Such business has secular growth embedded in them. Next in line are efficiency vendors, thiscompanies sell efficiencies or help in productivity improvement. Take the case of Honeywell automation and UCAL fuel. Itoffers solution to reduce operational cost, improve efficiency and reduce down time for any particular business. In short,such companies help other companies to realize and get more value from their existing operations. In the time of morecapital expenditure and picking up of investment cycle, this companies being specialized in their operations have first moveradvantage and are better placed then others. The last category is innovators. As the name suggests, this companiesinnovates and grab the market share with good pricing power. Unfortunately, India does not provide many cases in thiscategory except some information technology and health care companies.

In short, these three categories of companies are set to ride the mega trend started in the Indian market. So far as the megadeal of ING and Kotak bank, it is the largest ever deal seen in the Indian banking space. The last such merger was of bank ofRajasthan with ICICI bank. Taking the different parameters of customer and deposit base, asset quality increase inpresence, branches and network, capital adequacy, etc., the deal really makes sense to the merged entity and particularlythe Kotak Mahindra bank.

Kamlesh JhaveriManaging DirectorJhaveri Securities Ltd.

Selection of the scripts is all important at present in the market

Why Equity Sip ?Transparency Cost Effective Goal Based

Investment of `1000 per month

cond

ition

app

ly*

Call+91 265 3071200, +91 99254 20000Email : [email protected] Web : www.Jetrade.in

www.jhaveritrade.com

Issue Theme

1

Winter Session of Parliament

US is out, Japan is in

How it will benefit to India ?

Cabinet reshuffle : Past record along with strong pragmatism holds key

Why this is important ?

The Federal Reserve has been flooding the U.S. economy with cheap money through its bond- buying program since thefinancial meltdown of 2008-2009. This provided much needed liquidity to the economy. so much cheap money in the market,interest rates (the price of money) practically fell to zero.

The latest round (QE3) was announced in September 2012, with monthly purchases of $85 billion in treasuries andmortgage-backed securities. The FED began has started reduction of purchases in January 2014, cutting them by $10billion per meeting.

On October 28-2014, The Federal Reserve confirmed it will end an asset-purchase programmed keep interest rates low fora “considerable time.” ( No specific timeline has given)Bank of Japan will increase its purchases of longer-term debt, building on a stimulus plan first announced a year and a halfago. The bank will now make asset purchases at an annual pace of around 80 trillion yen, an increase from the previous 60to 70 trillion yen target range.

The bank's decision was far from expectation as five board members voted in favor of additional stimulus, while four votedagainst the proposal. The programme is designed to stimulate Japan’s economy by encouraging more lending and thusmore spending. The actions are meant to boost “Abenomics” (Economics + Shinzo Abe), an ambitious plan for economicreforms described by Japan’s Prime Minister ShinzoAbe.

The additional stimulus package from the Japanese central bank is positive news for India, and with macros situation wellbalanced, India stands out compared to other emerging market economies. Some of this excess liquidity will be coming toIndia compared to other emerging market economies because within the emerging markets, India appears to have thestrongest potential on the back of solid fundamentals, enough potential for a re-rating in valuations and a stable-yet-dynamicgovernment at the central.

In recent cabinet expansion, Modi government expands his ministry with the induction of four cabinet ministers, and 17ministers of state, three with independent charge.

The reshuffle fills gaps and addresses the need of departments that require urgent attention to ensure a quick economic revival. Infrastructure is a key area of focus for the government and Prime Minister Modi is believed to be particularly keen tosee a turnaround of the department.The expansion has also given direction at enhancing the government’s mental capacity required to deal with a situation andmembers strength.Proven track record matters :As the focus is clearly on governance and aptitude of those being inducted. For instance, in hisprevious position as the power minister, Suresh Prabhu came up with the landmark legislation of Electricity Reforms Act,2003. As Prabhu might have more success than his predecessor Sadananda Gowda in driving change in the Railwaydepartment.

www.jhaveritrade.com

Issu

e Th

eme

2

All eyes on winter session of parliament

Q2 FY15 : Healthy bottom line, weak top line growth of Indian Inc.

Conclusion

The government proposed that the winter session of Parliament begin on 24 November and last for a month—a crucialperiod that could present lawmakers with a packed agenda of 67 Bills awaiting passages. The committee suggested a totalof 22 sittings in the session during the course of which the government will try to pass 67 Bills—eight pending in the LokSabha and 59 in the Rajya Sabha.

After daily opposition disruptions in proceedings during the last UPAgovernment, the previous session of Parliament in July-August this year was a productive one in terms of actual hours of sittings, business transacted and debates. According to areport by the PRS Legislative Research, the Lok Sabha’s productivity in the budget session was 104%, while the RajyaSabha was at 99%.

The bills which are likely to be discussed in winter sessions are :• The Insurance Laws (Amendment) Bill which seeks to raise the cap on foreign direct investment (FDI) in insurance to

49% and which was sent to the select committee in the previous budget session.• Goods and Services Tax (GST) ConstitutionAmendment Bill, which has been delayed due to lack of consensus among

the states and centre.• The LandAcquisition and Rehabilitation and Resettlement Bill.• Labor reforms through amendments in the FactoriesAct,ApprenticesAct and Labor Laws Act.

A recovery remained intangible for India Inc. in the second quarter. Although India is the new star among the emergingmarkets but India Inc's quarterly numbers indicate that the possibility of a slower than anticipated pace of industrial recoverynow looks more prominent than it was a quarter ago.

During the quarter ended September 30, the net profit (adjusted for exceptional items) of 2,432 companies (excludingbanking & financial and oil & gas ones) rose 41.8% on a YoY basis — the fastest pace in at least three years — but their netannual sales growth drooping to 5.9%, slowest in five quarters.

The profitability was boosted by last year’s low base and lower operational cost, especially with a drop in sales & marketingexpenses, finance cost and depreciation

Stability in the rupee-dollar exchange rate and the recent decline in international commodity prices are likely to aid marginsin the coming quarters as well, though the net impact would get moderated by lower top-line growth.

Everybody knows that Prime Minister is amongst such highly reputed politician, who is well-known for his public speakingskills and has that dedication to take India reach to a developed level with his abilities. In last six months, Modi and his teamhas taken various steps to spur economic growth such as Diesel de -control, rail fare hike and manage constructive view onGST. However, as winter session is in progress, all eyes on how Modi is able to convince oppositions who have gangs uprecently and push up the reform agenda. We believe that Investors are ready to pay premium valuations on newgovernment's promise to turnaround the Indian economy via big bang reform measures. As there is no near term negativenews for the market and key benchmarks have seen stellar performance this year, we have positive / bullish outlook on themarket.

Winter Session of Parliament

www.jhaveritrade.com3

Power Sector Update

Sector Analysis

Power Sector Update

Normal power deficit continues to stay lower

Power generation

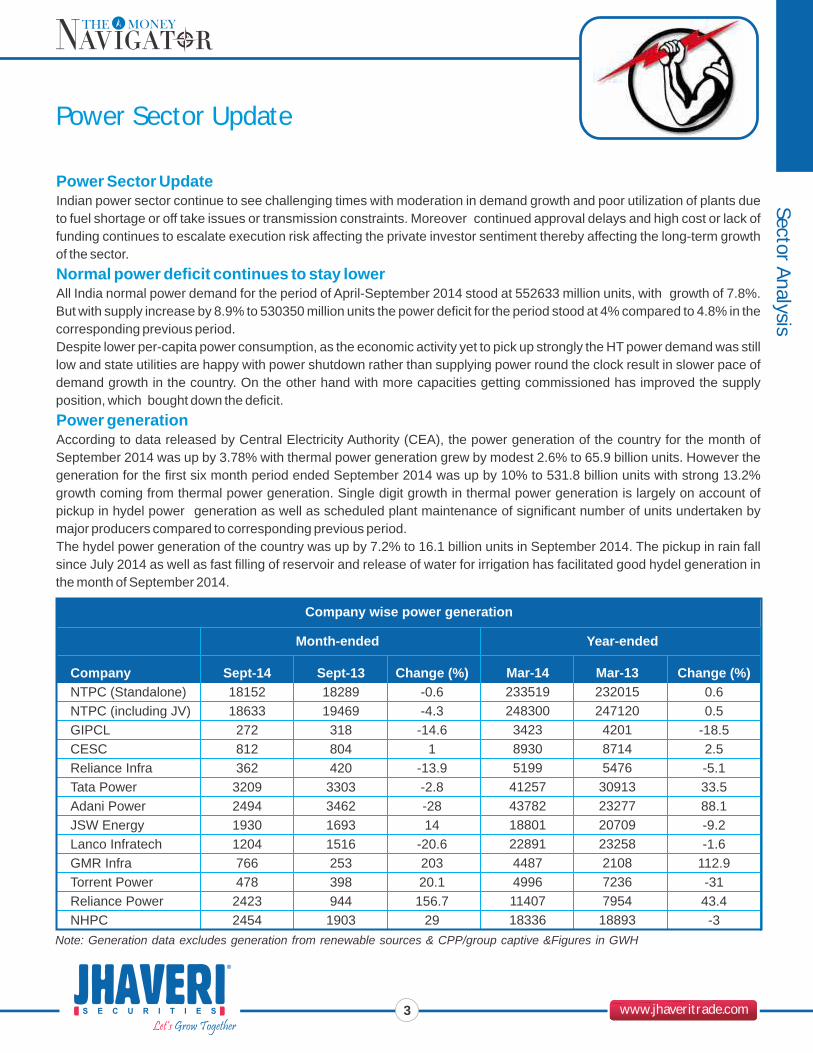

Indian power sector continue to see challenging times with moderation in demand growth and poor utilization of plants dueto fuel shortage or off take issues or transmission constraints. Moreover continued approval delays and high cost or lack offunding continues to escalate execution risk affecting the private investor sentiment thereby affecting the long-term growthof the sector.

All India normal power demand for the period of April-September 2014 stood at 552633 million units, with growth of 7.8%.But with supply increase by 8.9% to 530350 million units the power deficit for the period stood at 4% compared to 4.8% in thecorresponding previous period.Despite lower per-capita power consumption, as the economic activity yet to pick up strongly the HT power demand was stilllow and state utilities are happy with power shutdown rather than supplying power round the clock result in slower pace ofdemand growth in the country. On the other hand with more capacities getting commissioned has improved the supplyposition, which bought down the deficit.

According to data released by Central Electricity Authority (CEA), the power generation of the country for the month ofSeptember 2014 was up by 3.78% with thermal power generation grew by modest 2.6% to 65.9 billion units. However thegeneration for the first six month period ended September 2014 was up by 10% to 531.8 billion units with strong 13.2%growth coming from thermal power generation. Single digit growth in thermal power generation is largely on account ofpickup in hydel power generation as well as scheduled plant maintenance of significant number of units undertaken bymajor producers compared to corresponding previous period.The hydel power generation of the country was up by 7.2% to 16.1 billion units in September 2014. The pickup in rain fallsince July 2014 as well as fast filling of reservoir and release of water for irrigation has facilitated good hydel generation inthe month of September 2014.

CompanyNTPC (Standalone)NTPC (including JV)GIPCLCESCReliance InfraTata PowerAdani PowerJSW EnergyLanco InfratechGMR InfraTorrent PowerReliance PowerNHPC

Company wise power generation

Month-ended Year-ended

Sept-141815218633

272812362

3209249419301204766478

24232454

Sept-131828919469

3188044203303346216931516253398944

1903

Change (%)-0.6-4.3

-14.61

-13.9-2.8-2814

-20.620320.1

156.729

Mar-14233519248300

342389305199

41257437821880122891448749961140718336

Change (%)0.60.5

-18.52.5-5.133.588.1-9.2-1.6

112.9-3143.4-3

Mar-13232015247120

420187145476

30913232772070923258210872367954

18893Note: Generation data excludes generation from renewable sources & CPP/group captive &Figures in GWH

www.jhaveritrade.com

Power Sector Update

4

Sect

or A

naly

sis Sharp jump in short term power price inAug 2014

Storage levels at major reservoirs stood at 93% of corresponding period last year

Conclusion

Our Preferred Stocks

Short term electricity volume traded in August 2014 was up by 5.8% to 9634.14 million units compared to corresponding previous month. In August 2014 while the bilateral trader/power exchange, bilateral direct and power exchange was up by21.9%, 6% and 3.9% respectively the unscheduled interchange (UI) volume was down by 16%. While the bilateral marketprice was flat the rate at IEX, PXIL and UI was up by 109%, 95% and 141% respectively. The average power price in shortterm market barring bilateral market has witnessed impressive rise. While the bilateral market average price forApril-August2014 was down by 5.4% the rate at IEX, PXIL and UI was up by 28.9%, 50.8% and 63.6% respectively over correspondingprevious period.

The healthy monsoon rain fall activity started from July 13, 2014 has facilitated improvement in reservoir levels across thecountry. The water storage in 85 important reservoirs (including 37 reservoirs having hydro power of more than 60MW thatstood at 35% of the total storage capacity of these reservoirs as end of July 24, 2014 has improved to 66% as end ofAugust28, 2014. The storage capacity of these reservoirs has further increased to 77% ( of total storage capacity as the end ofSeptember 11, 2014. But the present storage capacity of these 85 important reservoirs is 93% of the storage ofcorresponding period of last year. Similarly the reservoir levels of North, East, West, Central and Southern region as end ofSeptember 11, 2014 stood at 83%, 75%, 78%, 82% and 72% of the total storage levels respectively. the reservoir levels arestill lower than same period of last year and this is likely to lower the hydel power generation.

Power sector caught in structural issues witnessed mid single digit power deficit on the back of strong new generationcapacity coming on stream as well as subdued growth in demand Inspite huge growth potential due to low per-capita powerconsumption compared to other developing and developed countries and still elusive uninterrupted power supply scenarioin the country.To improve investor confidence and sustainable growth of the sector the issues related to inadequate fuel availability, lack ofclarity around new bidding norms for long-term PPAs, transmission corridor issues, high T&D losses and weak financialcondition of the Discoms need to be addressed in a meaningful manner. The government though has demonstrated aresolve to address the structural issues impacting the power sector the impact of the same at ground level is yet to bewitnessed. Moreover the uncertainty created by cancellation of captive coal mines has to be solved with re auction of thesame at the earliest in transparent manner.

CompanyYearNTPCPower GridCESCTata Power

EPSFY15E10.910.425.52.6

FY16E12.712.149.74.2

FY15E13.113.829.733.6

FY16E11.311.915.221.0

FY15E9.311.213.47.5

FY16E8.3

10.78.86.5

FY15E9.98.05.711.0

FY16E10.57.9

10.013.1

FY15E9.9

14.15.75.3

FY16E10.814.610.08.4

P/E(X) EV/EBITDA(X) ROCE(X) ROE(%)

www.jhaveritrade.com5

CCL Products (India) Ltd.

Com

pany Analysis

Company Overview

Investment rationalGreenfield Operations in Vietnam to help growth

Logistical benefit

Duty structure is one of the improvement in Vietnam

Indian operation : Maximum capacity utilization is expected

CCL Products (India) Ltd (CCL) is India’s largest private label instant coffee companysupplying to premium brands in ~80 countries. Through its subsidiaries, the company has also set up an agglomeration plant in Switzerland (to penetrate Europe) and a spraydried and concentrated liquid coffee plant in Vietnam.

CCL's wholly owned step down subsidiary in Vietnam, M/s. Ngon Coffee CompanyLimited, has commenced commercial production in FY14. The presence in Vietnamhelps the company to cater to the coffee needs of ASEAN countries and also this is inclose proximity to many South-East Asian nations, Japan, Korea, China etc. Most ofthese countries have granted Vietnam a most favored nation status with reduced or nilduty structures in addition to having savings on logistics.

The company's new plant is in coffee producing zone and the unit is likely to savesignificant amount on per tonne basis on the logistics front. As logistic cost is higher onper tonne basis in consolidated financials, the savings would be ~$150-160/tonne.

Vietnam is most important nation for reduced or nil duty structures for export. As instantcoffee exports to Japan from Brazil and India attract effective duties of ~15% and ~6%while it is only ~1%-2% in the case of Vietnam. Company’s products are competitive inthe export market. This price advantage should help the company to tap new markets inthe long term.

Company's current installed capacity is 88% in FY14 at its Guntur plant in AndhraPradesh, CCL is expected to operate at an maximum capacity utilization of 90-92% innext two years due to :

“Accumulate” CMP : `143 TGT : `186Company Basics

BSE IDNSE SymbolGROUPEQUITY ( in Cr.)MKT.CAP ( in Cr.)

`

`

519600CCL

B26.61

1803.49

Financial BasicsFV ( )EPS ( )P/E (x)P/BV (x)

`

`

2.006.12

24.425.11

Investment Rationale

Investment Horizon: 12 months

Share Holding PatternHolder's Name

Foreign

Institutions

Promoters

Non. Promoters

Public & Others

Govt. Holding

% Holding

13.65

9.95

44.54

6.82

25.05

0.00

ROI : 30%

ValuationsCurrently, CCL is trading at `143.WeRecommend “Accumulate” with aTarget Price of `186 based onforward P/E of 20.00x with anexpected earnings per share of`6.00 in FY2017E.

www.jhaveritrade.com6

CCL Products (India) Ltd.

CCL Product (India) LtdCompany Structure

StandaloneBusiness Jayanti Pte Ltd

India Operations(15,000 tpa)

Ngon CoffeeCompany

Spray Dried10,000 tpa

Concentrated Liquid5,000 tpa

100 %

Product Portfolio

Exports Domestic(In House Brands )

Packaging Options

Source: Company

ContinentalSpeciale

ContinentalPremium

ContinentalSupreme

FreezeConcentrated

LiquidFreezeDried

SprayDried

Powder

SprayDried

Granules

CansJar Drums BulkBoxes Bag in Box Sachets

Com

pany

Ana

lysi

s

a) Increasing global consumption of coffeeb) Consumer preference is shifted to instant coffee in the Emerging Marketsc) Strong relationships with global clients.

CCL has already enetred into retailing of coffee with brand like Spéciale, Premium and Supreme and market test practicehas been already completed in AP. Other manufacturers like Nestle and HUL do not have manufacturing capacities So overlonger term CCL has advantage as compared to others. Fro Example : while Nestle ’s pure coffee (freeze dried) is priced at`250/jar, CCL’s brand is priced at a relatively lower price of `110/jar. We believe that company will expand it other states alsoonce test marketing is finished.

Surprisingly, CCL operates on fixed margins, without carrying the risk of coffee price volatility. CCL buys green coffee beansby importing these (~75%) from Global markets (Vietnam, Indonesia, Africa countries) as well as the domestic market(~25%), primarily from southern state Karnataka.Moreover, as far as margins are concerned, the company remains unaffected by fluctuations in the green coffee beansprices or the coffee prices as it places orders for green coffee only on receiving the order for instant coffee and makes back-to-back arrangements for green beans.

Retailing of instant coffee : Next phase of growth from company

Sourcing :AKey CompetitiveAdvantage

CCL Products (India) Ltd.

www.jhaveritrade.com7

Com

pany Analysis

NorthAmerica : the next big market for CCL

Q2 FY 15 conference call update

NorthAmerica is one of the largest instant coffee consumers at ~80,000tn-100,000tn.As of now, CCLsells less than 2,000 tnand mostly in bulk quantity. CCL was not able to tap the North American market because of increased availability ofadulterated coffee from Brazil and Mexico. The adulterated coffee is available at ~US$4.0/tn with a 90-day credit periodwhereas CCLcoffee is available at ~US$8.35/tn with zero credit.

There are strict regulations on coffee adulteration in the European Union and Russia, but it is not the case in the US. CCLfeels that it will be one of the beneficiaries once the law is formally in place in North America which would curb the supply ofadulterated coffee (from Brazil and Mexico), as it happened in Russia and the EU earlier. In order to seize such anopportunity, CCL is setting up a packaging facility in North America at a cost of US$8mn-US$10mn.

Margins in domestic operations are lower because of steps taken to add clients. To get clients, which will benefit in thelong run, CCL supplied its products at attractive prices, thereby hurting its margins. However, the margins areexpected to bounce back in 2HFY15. 3Q and 4Q are better quarters than 1Q and 2Q on account of seasonality.The management has given volume guidance of ~20,000tn (India/Vietnam: 15,000tn/5,000tn) for FY15 and out ofthis 90% has already been pre-sold.The Vietnam plant operated at ~40% of its capacity in 1HFY15 and is expected to operate at ~50% in FY15 (~60% in2HFY15). In 1HFY15/2HFY15, Vietnam has achieved/expected to achieve volume of 2,000tn/3,000tn, respectively.As per the management, total volume is expected to increase 25% at 25,000tn in FY16. Vietnam plant’s volume isexpected to increase 50% from 5,000tn in FY15 to 7,500tn (75% capacity utilizations) and Indian operations’ volumeis likely to increase 16% from 15,000tn to 17,500tn.CCL is expanding its Indian operations from 15,000tn to 20,000tn at a cost of ~Rs200mn through brown fieldexpansion and by adding balancing equipment by 2QFY16.

•

•

•

•

•

Key Finacials

Total Income

EBITDA

Reported Profit After Tax

Net Sales

Other Income

Total Expenditure

Interest

EBIT

Depreciation

PBT

Tax

Deferred Tax

Q2 FY 14

154.85

33.72

21.31

154.64

0.21

121.13

1.79

31.93

3.5

28.43

7.5

-0.38

Q3 FY 14

164.96

34.25

18.70

164.76

0.2

130.72

1.94

32.31

3.55

28.75

10

0.05

Q4 FY 14

164.87

32.69

17.95

164.48

0.4

132.19

1.41

31.28

2.41

28.87

10.4

0.52

Q2 FY 15

195.74

37.81

21.45

195.35

0.39

157.94

1.19

36.61

2.37

34.25

12.18

0.62

Q1 FY 15

132.98

25.63

15.7

132.6

0.38

107.34

1.85

23.78

2.41

21.38

5.82

-0.14

www.jhaveritrade.com

CCL Products (India) Ltd.

Com

pany

Ana

lysi

s

8

YearEquity Paid UpNet worthCapital EmployedGross Block (Excl. Reversal. Res.)Net Working Capital ( Incl. Def. Tax)Current Assets ( Incl. Def. Tax)Current Liabilities and Provisions ( Incl. Def. Tax)Total Assets/LiabilitiesGross SalesNet SalesOther IncomeValue Of OutputCost of ProductionSelling CostPBIDTPBDTPBITPBTPAT after Minority Interest & P/L Asso.Co.Adjusted PAT

FY 1113.3

217.16437.63359.68119.39191.6372.24

509.87365.41363.87

9.78377.29316.45

9.9474.5258.5855.2639.3226.4524.58

FY 1213.3

239.74507.62363.33151.64214.7963.15

570.77504.95502.22

2.01498.45398.3113.7789.1274.2769.0254.1736.2436.21

FY 1313.3

278.38580.42465.21213.44299.55

86.1666.52655.34650.74

1.88662.89539.5813.88

123.15102.4994.5173.8547.4347.42

FY 1426.61

352.79644.86525.17239.2

319.3780.17

725.02721.52716.82

2.64711.74569.9214.27

145.73128.67116.6399.5764.4264.43

Year

Debt-Equity Ratio (x)

Long Term Debt-Equity Ratio

Current Ratio

Interest Cover Ratio

PBIDTM (%)

APATM (%)

ROCE (%)

RONW (%)

(x)

(x)

(x)

FY 11

1.09

0.48

1.03

3.47

20.39

7.24

12.58

12.56

FY 12

1.07

0.44

0.97

4.65

17.65

7.18

14.6

15.86

FY 13

1.1

0.45

1.05

4.57

18.79

7.24

17.37

18.31

FY 14

0.94

0.41

1.24

6.84

20.2

8.93

19.04

20.41

( ` in Cr )

Qualified Institutional Placement

JSL Classroom

www.jhaveritrade.com9

QUALIFIEDINSTITUTIONAL

PLACEMENTS

What is QIP ?

How is the price decided ?

Main advantages of raising money via the QIB route:

Main advantages for QIB’s :

• A QIP is a capital raising tool wherein a listed company can issue equity shares, fully and partly convertible

debentures, or any security (other than warrants) that is convertible to equity shares. This is the only other speedy

method of private placement whereby a listed company can issue shares or convertible securities to a select group of

investors.• But unlike in an IPO or an FPO (further public offer), only institutions or qualified institutional buyers (QIBs) can

participate in a QIP issuance. QIBs include mutual funds, domestic financial institutions such as banks and insurance

companies, venture capital funds, foreign institutional investors, and others.

• The QIP will be priced not less than the average of the weekly high and low of the closing prices of the equity shares

during the two weeks preceding the “relevant” date. The “relevant” date will be the opening date of the issue, as

decided by the company’s board.

Advantages for the issuing company1) Speed : The regulatory oversight of SEBi is far more relaxed when money is raised via the QIP route. There is no long

wait for document approval by a SEBI dealing officer as is the case when a company does an IPO, FPO or rights

issue. The whole process can complete in 4-5 days, provided of course that the issuer company manages to get

willing QIBs buyers.2) Cost efficiency : IPO/ Rights / FPO are an expensive affair. A large team of bankers, auditors, lawyers have to be

involved and the approval could take 4-5 months if not more. Further, the fees to be paid to the exchange are far

lesser in case of a QIP.

1) Ability to buy large stakes : Let’s say a large institution/ investor is convinced about the long term business

fundamentals of a business and would like to partner in the business by becoming a part stakeholder. Further, the

investor wants to hold a larger stake (think 10-15%).In such a scenario issuing new shares by increasing capital is the

only pragmatic way to bring in a new investor for two reasons :• If the investor tries to buy from secondary / open market, it will create a lot of volatility in the price of the listed share

which will lead to expensive valuations and distort the very value at which the investor was willing to acquire the stake

i.e. it will make the purchase price unattractive for the large investor.• If the company’s long term fundamentals are genuinely attractive, it will be hard to find sellers, especially at the price at

which the new investor would like to acquire the stake.

2) No Lock-In : Unlike investing in an IPO where accredited investors (or QIB buyers) must hold on to their shares for a

certain period of time (typically 1 year), a Qualified Institutional Placement allows the investor to exit/ sell the stock at

any point of time post its listing on the exchange.

www.jhaveritrade.com

Monthly Technical Picks

Mon

thly

Tec

hnic

al P

icks

10

On Weekly Chart, Stock has given Breakout of itscontinuation Flag Pattern. Here, Breakout Point is 1590.Weekly RSI is in positive crossover suggesting buyinginterest.Also Stock is trading above its 40 Week IMA.

On Weekly Chart, Stock has taken support of lower lineof its Andrew Pitchfork pattern and currently tradingabove lower line. Now, Stock is likely to test median lineof the Pattern. Weekly RSI is in positive crossoversuggesting buying interest at every minor correctionseen in the stock on weekly basis. Also Stock is tradingabove its 40 Week IMA.

On Weekly Chart, Stock has given breakout of its upperarm of its likely symmetrical triangle Pattern. Here,Breakout point is 162. Weekly RSI is in positivecrossover suggesting fresh buying interest intact at thislevel.Also Stock is trading above its 40 Week IMA.

On Weekly Chart, Stock has given breakout of its Cupand Handle Pattern. Here, Breakout point is 63. WeeklyRSI is in positive crossover suggesting buying interest. Also Stock is trading above its 40 Week IMA.

BUY BTWN 60.50-63.50 TGT 69.85-74 SL 55.50

LT BHEL

HINDALCO DISHTV

BUY BTWN 256-266 TGT 284-295 SL 240BUY BTWN 1590-1640 TGT 1738-1774 SL 1519

BUY BTWN 160-166 TGT 177-182 SL 150

www.jhaveritrade.com

Mutual Fund

11

Avast majority of risk averse investors prefer bank fixed deposits to debt mutual fund schemes. Perception of risk and lack offinancial awareness are the contributing factors. For investors who are willing to sacrifice the comfort of guaranteed returns,long term income funds are better investment options than fixed deposits over a tenure of three years or more. While bankshave offered around 8.5 – 9% interest rates for a 3 year term deposits, top long term income funds have given returns of 9.5 –10.7% over the last 3 year period. Further over tenures of three years or more, debt funds enjoy tax advantage over fixeddeposits due to the long term capital gains tax with indexation. If we add the difference in pre-tax returns and the tax benefit,the post tax returns of long term income funds has been substantially higher than the bank fixed deposits.

Over a three year tenure top performing long term income funds have given 1.5 – 2% higher returns compared to fixeddeposits. On Rs1 lac investment the returns from income funds over a three year investment horizon would be Rs 2,000 to6,000 higher compared to fixed deposits on a pre-tax basis. On a post tax basis the difference in returns will be even higher,as we will discuss later in the article. The chart below shows the trailing three year annualized returns of the top incomefunds.

Returns of top long term income funds

Long Term Bonds Pre-Tax Returns

Long Term Income Funds are better investmentoptions than FDs over a 3 year horizon

BANK FIXED DEPOSITS

DSP BLACKROCK STRATEGIC BOND FUND

UTI BOND FUND

CANARA ROBECO DYNAMIC BOND FUND

TATA INCOME FUND

ICIC PRUDENTIAL INCOME OPPORTUNITIES FUND

IDFC DYNAMIC BOND FUND

HDFC HIGH INTEREST FUND - DYNAMIC PLAN

BNP PARIBAS FLEXI DEBT FUND

RELIANCE DYNAMIC BOUND FUND

UTI DYNAMIC BOUND FUND

8.5%

9.5%

9.5%

9.5%

9.8%

9.9%

10.1%

10.2%

10.2%

10.5%

10.7%

www.jhaveritrade.com

Mut

ual F

und

Long Term Income Funds are better investmentoptions than FDs over a 3 year horizon

12

While the top long term income funds outperformed fixed deposits over three year tenure, these funds gave higher pre-taxreturns than fixed deposits even in the last 12 months, despite prevailing high interest rates. The chart below shows trailingone year returns of the top income funds.

We have been in the grip of high interest rates for a long time due to stubborn inflation. However inflation has been easingover the past four months. In September inflation was 6.7%. Some bond market operators are expecting the RBI to cut ratesas early as December, but the majority of economists are of the view that RBI will start cutting rates in February 2015. The 10year Government Bond yield has started inching down from historical high levels. It is now at 8.3% compared to 9% at thebeginning of the year. That is why we have seen the long term income funds giving good returns in the last one year.

Outlook for Long Term Income Funds

9.0%

10.8%

9.8%

9.9%

9.6%

12.3%

9.9%

11.8%

9.7%

10.7%

12.1%

BANK FIXED DEPOSITS

DSP BLACKROCK STRATEGIC BOND FUND

UTI BOND FUND

CANARA ROBECO DYNAMIC BOND FUND

TATA INCOME FUND

ICIC PRUDENTIAL INCOME OPPORTUNITIES FUND

IDFC DYNAMIC BOND FUND

HDFC HIGH INTEREST FUND - DYNAMIC PLAN

BNP PARIBAS FLEXI DEBT FUND

RELIANCE DYNAMIC BOUND FUND

UTI DYNAMIC BOUND FUND

www.jhaveritrade.com

Mutual Fund

13

9.5

9

8.5

8

7.5

7

9.5

9

8.5

8

7.5

7

Implied Yield on 10 Year Bond

Jul / 11 Jun / 12 Jul / 12 Jun / 13 Jul / 13 Jun / 14 Jul / 14

Source : Ministry of Finance

The 10 year Government Bond yield is expected to fall to 7% in FY 2015 – 2016. Bond prices have an inverse relationshipwith interest rates. As interest rate goes down bond prices increase, leading to higher potential returns from long termincome funds over the next 2 to 3 years. When we move to benign interest rate environment, the returns of long term incomefunds can potentially be even higher than the recent short term returns.

Income Funds are not risk free

Tax Benefit

It is important that investors understand that income or debt funds are not risk free. It is equally important that investorsunderstand the nature of the risk, so that they can make an objective investment decision, without being swayed byperceptions. There are three kinds of risk that income or debt funds are exposed to.

• Interest Rate risk: If interest rate goes down bond prices and returns will increase. Conversely, if interest rategoes up bond prices and returns will decrease. In the context of India's macro-economic outlook and the interestrate environment, the probability of interest rate going up is very low.

• Re-investment risk: If the bonds in the income fund portfolio mature and the proceeds are re-invested in loweryield bonds, then the returns will decrease. Re-investment risk is lower if the average maturity of the bonds in theportfolio is longer. Long term income funds typically have longer maturity bonds in their portfolio, as we will see inthe table below.

• Credit risk: Credit risk relates to the risk of default. If the credit rating of the bond worsens the bond price willdecline and the returns will be lower. As far as credit risk is concerned, the top long term income funds have highquality bonds in their portfolio.

Some significant taxation changes were made for debt funds in the last Budget. The holding period of long term capital gainsis now 3 years.If the holding period is less than 3 years, then the returns will be taxed as per the income tax rate of theinvestor. If the holding period is more than 3 years, long term capital gains tax of 20% will apply. However, indexation benefits

Long Term Income Funds are better investmentoptions than FDs over a 3 year horizon

www.jhaveritrade.com

Mut

ual F

und

Long Term Income Funds are better investmentoptions than FDs over a 3 year horizon

14

are allowed for calculation of long term capital gains. Fixed Deposit interest, on the other hand, is taxed as per the income taxrate of the investor, irrespective of the holding period. Indexation benefit reduces long term capital gains tax significantly.Therefore for tenures of 3 years or more, income funds have a significant tax advantage over fixed deposits, especially forinvestors in the higher tax bracket.

Let us see the difference between post tax returns of a long term income fund and fixed deposit with the help of an example.Let us assume you invested Rs 1 lac in UTI Dynamic Bond Fund on November 1, 2011. Let us see how your post tax returnscompare with a Rs 1 lac investment in fixed deposit at 9% over the same tenure.

Investment (November 1,2011)

Pre - Tex Return

Investment Value (November 1, 2014)

Indexed Cost (Inflation Index 2010 - 2011 : 785 ; 2014 - 2015:1025)

Taxation

Tax

Post Tex Return

`1,00,000

10.7%

`1,35,547

`1,30,573

20% on LT Capital Gains with indexation

`995

`34,552

`1,00,000

9%

`1,29,503

N/A

Income Tax (as per the tax rate of the investor, 30%)

`8,851

`20,652

Post Tex Return Calculation UTI Dynamic Bond Fund Fixed Deposit

Say...Good Bye toIPO Forms

Say...Good Bye toIPO Forms

www.jhaveritrade.com I www.jetrade.in

How can I capitalize on this Opportunity?

Apply in multiple family a/c to maximize allotment

Apply on click – First cum first serve basis

Greater allotment without any rejection

To get registered for Online IPO,Please contact your branch or SMS “JeTrade IPO” on 9601336677

• Can be applied anywhere anytime

• You can apply IPO against ledger balance / RTGS

• Shorter IPO cycle – Total 7-10 days from announcement to allotment

• Approx 30 -35 IPO/FPO & ETFs under pipeline in F.Y.2014-15

Apply IPO Online Why should I go for Online IPO?

301/302, Payal Tower-II, Sayajigunj Vadodara - 390020, Ph.: + 91 265-3071200Web.: www.jhaveritrade.com I www.jetrade.in

DISCLAIMER : Trading and Investment decision taken on your consultation are solely at the discretion of the traders/investors.We are not liable for any loss, which occur as a result of our recommendations. This document hasbeen prepared on the of publicly available information, internally developed data and other sources believed to be reliable.

NSE:INB/F/E 230823233 BSE: INB/F 010823236 NSDL: IN-DP-NSDL-166-2000, MCX-SX: INE 26082333 AMFI ARN 3524 MCX: TM 29040 / FMC REG NO. MCS / TC / CORP / 0963 MCDEX: TM 00749 / FMC REG NO.NCDEX / TCM / CORP / 0736 / NSELTM 10110* Note: Dealing in Commodity Segment through its group company Jhaveri Credits & capital Ltd.Distributors for IPOs & Mutual Funds. Past performance is not a measure for future returns.

For Demo & More Detail For Demo & More Detail Give Missed Call

08049336177SMS JeTrade to

9601336677

`̀00APPLICATIONAPPLICATIONCHARGESCHARGES

Trading Options Benefit of Online Trading

Trade Whenever & WhereverPaper Less Trading100% control Over your InvestmentCall-N-Trade FacilityQuick Technical Support-(Live Chat/support)

Date Time in IST Country/EventCurrencyMon Dec 1

Tue Dec 2

Wed Dec 3

Thu Dec 4

Fri Dec 5

Mon Dec 8Tue Dec 9

Wed Dec 10

Thu Dec 11

Fri Dec 12

Mon Dec 15

Tue Dec 16

6:30am

All Day

6:30am

6:15pm

12:30pm

All DayAll Day7:00am

7:00pm

11:00am

7:00pm

3:30pm

7:15am1:45pm2:15pm8:30pm

1:30pm3:30pm8:30pm

7:15am1:45pm2:15pm3:30pm6:45pm7:00pm8:30pm9:00pm

7:00pm

7:00pm

8:30pm

1:15pm9:00pm11:31pm

8:30pm

7:00pm

7:45pm

4:30pm

Manufacturing PMI

Total Vehicle Sales

Non-Manufacturing PMI

Minimum Bid Rate

German Factory Orders m/m

Eurogroup MeetingsECOFIN MeetingsCPI y/y

Core Retail Sales m/m

Industrial Production y/y

Empire State Manufacturing Index

German ZEW Economic Sentiment

HSBC Final Manufacturing PMISpanish Manufacturing PMIItalian Manufacturing PMIISM Manufacturing PMI

Spanish Unemployment ChangePPI m/mConstruction Spending m/m

HSBC Services PMISpanish Services PMIItalian Services PMIRetail Sales m/mADP Non-Farm Employment ChangeRevised Nonfarm Productivity q/qISM Non-Manufacturing PMICrude Oil Inventories

ECB Press ConferenceUnemployment Claims

Non-Farm Employment ChangeTrade BalanceUnemployment RateFactory Orders m/m

PPI y/yFrench Industrial Production m/mCrude Oil Inventories10-y Bond Auction

Retail Sales m/mUnemployment ClaimsImport Prices m/mBusiness Inventories m/m

PPI m/mCore PPI m/m

Capacity Utilization RateIndustrial Production m/m

ZEW Economic SentimentGerman Buba Monthly Report

CNY

USD

CNY

EUR

EUR

EUREURCNY

USD

CNY

USD

EUR

CNYEUREURUSD

EUREURUSD

CNYEUREUREURUSDUSDUSDUSD

EURUSD

USDUSDUSDUSD

CNYEURUSDUSD

USDUSDUSDUSD

USDUSD

USDUSD

EUREUR

Date Time in IST Country/EventCurrencyWed Dec 17

Thu Dec 18

Fri Dec 19

Mon Dec 22

Tue Dec 23

Wed Dec 24

Fri Dec 26

Mon Dec 29Tue Dec 30

Wed Dec 31

3:30pm

12:30am

12:30pm

2:25pm

7:15am

All Day

All Day

1:15pm1:30pm

All Day

7:00pm

9:00pm

1:00am2:30pm7:00pm

2:30pm

12:30pm1:30pm

2:00pm

2:30pm

7:00pm

8:15pm8:30pm

7:00pm9:00pm

8:25pm

2:30pm

8:15pm8:30pm

12:30pm6:45pm8:30pm9:00pm

Final CPI y/y

FOMC Economic Projections

German PPI m/m

German Unemployment Change

HSBC Flash Manufacturing PMI

German Bank Holiday

German Bank Holiday

French Consumer Spending m/mSpanish Flash CPI y/y

German Bank Holiday

Final Core CPI y/yCPI m/mCore CPI m/mCurrent AccountCrude Oil Inventories

FOMC StatementFederal Funds RateFOMC Press ConferenceGerman Ifo Business ClimateUnemployment Claims

Current Account

Existing Home Sales

German Retail Sales m/mFrench Flash Manufacturing PMIFrench Flash Services PMIGerman Flash Manufacturing PMIGerman Flash Services PMIFlash Manufacturing PMIFlash Services PMICore Durable Goods Orders m/mFinal GDP q/qPersonal Spending m/mFlash Manufacturing PMINew Home Sales

Unemployment ClaimsCrude Oil Inventories

Revised UoM Consumer Sentiment

M3 Money Supply y/yPrivate Loans y/yChicago PMICB Consumer Confidence

GfK German Consumer ClimateADP Non-Farm Employment ChangePending Home Sales m/mCrude Oil Inventories

EUR

USD

EUR

EUR

CNY

EUR

EUR

EUREUR

EUR

EURUSDUSDUSDUSD

USDUSDUSDEURUSD

EUR

USD

EUREUREUREUREUREUREURUSDUSDUSDUSDUSD

USDUSD

USD

EUREURUSDUSD

EURUSDUSDUSD