Embed Size (px)

DESCRIPTION

Durante la 53ava reunión del BID en Montevideo, Uruguay, la revista Euromoney publicó su Guía Uruguay 2012 (en idioma ingles).

Citation preview

The 2012 guide toM

arch

201

2

Published in conjunction with:

uruguay

Open for investment 2Uruguay has come a long way in the past 10 years, growing and diversifying its economy. Foreign investors have responded

Reduced vulnerabilities, increased confidence 4Interview with Finance and Economy Minister, Dr Fernando Lorenzo

Uruguay rises 10 places in 6Euromoney’s country risk ratingsEconomists’ sentiments sharply improved in 2011 as Uruguay scored highly across a range of political, economic and structural indicators. Above-average scores indicate the country has good grounds to expect an upgrade from the rating agencies

Towards investment grade 8Since its debt crisis in 2003, Uruguay has built up a reputation as one of Latin America’s most prudent and consistent sovereign borrowers. Ratings agencies have taken notice

FDI set to stay at record level 10In the past 10 years, Uruguay has become a key destination for FDI, attracted by the country’s rich human and natural resources and stable political environment

Roundtable: Uruguayan financial leaders 11

Natural advantages 13Long a favoured destination for visitors from neighbouring Argentina and Brazil, Uruguay is increasingly attracting tourists from further afieldß

This guide is for the use of professionals only. It states the position of the market as at the time of going to press and is not a substitute for detailed local knowledge.

Euromoney Institutional Investor PLCNestor HousePlayhouse YardLondon EC4V 5EXTelephone: +44 20 7779 8888Facsimile: +44 20 7779 8739 / 8345

Chairman and editor-in-chief: Padraic FallonDirectors: Sir Patrick Sergeant, The Viscount Rothermere, Richard Ensor (managing director), Neil Osborn, Dan Cohen, John Botts, Colin Jones, Diane Alfano, Christopher Fordham, Jaime Gonzalez, Jane Wilkinson, Martin Morgan, David Pritchard, Bashar Al-Rehany

Editor: Sarah MinnsJournalist: Jason MitchellPrinted in the United Kingdom by: Wyndeham Group

© Euromoney Institutional Investor PLC London 2012Euromoney is registered as a trademark in the United States and the United Kingdom.

Contents

Open for investmentUruguay has come a long way in the past 10 years, growing and diversifying its economy. Foreign investors have responded. Jason Mitchell reports

Uruguay has become one of the most attractive countries in Latin America for foreign direct investment during the past decade because of strong economic growth and a solid rule of law.

The country - with a total population of 3.3 million - has one of the highest rates of FDI against GDP in Latin America: in 2010, the overall economy was valued at $39.0 billion and total FDI amounted to $2.35 billion, giving an overall rate of 6%. Within Latin America, only Chile had a higher rate at 7.4%. Peru had a rate of 4.8%, Brazil 2.3%, Colombia 2.3%, Argentina 1.7%, Paraguay 1.5% and Ecuador 0.6%.

“As a proportion of GDP, Uruguay is investing much more today than it did historically,” says Luis Porto, vice-minister of Economy and Finance. “Today, the overall investment rate is around 20% while historically it was around 13% to 14%. FDI inflows have been a major contributor to a higher investment rate. The goal is to increase that rate to around 25%.”

Over the last decade, Uruguay has been transformed. Traditionally, the country was seen by investors as an economic appendage to Argentina but that is no longer the case. When Argentina experienced its economic meltdown between 2001 and 2002, Uruguay was also particularly vulner-able. At that time, around 45% of bank deposits in Uruguay belonged to Argentines, today the figure is only around 15%. Argentina was also one of the country’s most important export market but today Uruguayan exports to Argentina account for only 7.3% of its total goods exports (nowadays, 20.3% are destined to Brazil and 8.3% to China).

Changing economyDuring the past 10 years, Uruguay has diversified its economy dramati-cally. It used to be one of the main offshore financial centres for the rest of Latin America, especially rich Argentines and Brazilians. That industry is far less important to the country than it once was. Agriculture has been the backbone of the economy for decades and Uruguay has made big strides in increasing its agricultural exports - especially meat and dairy products - during the past few years. The country has moved up the sup-ply chain and its companies export a lot of ‘gourmet’-type produce today. Soya plays a less important role in the economy than in Argentina but

recent investment in that sector means that soya exports are also likely to pick up during coming years.

Today, Uruguay has very much its own economic trajectory, quite independent from Argentina or any other Latin American country. For example, Uruguay has an inflation rate of around 8% while Argentina’s rate is at around 25%.

During the past decade, Uruguay has become a highly fashionable tour-ist destination (the total number of foreign visitors jumped to 3.5 million last year from 2.1 million in 2005). For many decades, Punta del Este, the country’s main resort, was a well-known playground for the rich but during the past 10 years many more visitors from around the world have come. Uruguay is one of only 10 countries in the world that receives more foreign visitors annually than its resident population. Many foreigners, especially Argentines and Brazilians, have bought holiday homes in Punta or neighbouring resorts such as La Barra and Jose Ignacio.

However, it’s not only Punta that is becoming more attractive to tourists: many new hotels are opening up in Montevideo. Colonial hotels that fell into disuse are being restored to their former glory. For example, Sofitel, the luxury French hotel group, is bringing back to life a grand hotel near the beach in the upmarket Carrasco neighbourhood of the city. This will be the most luxurious hotel in Uruguay, if not the region, when it opens later this year, and will feature 116 rooms and include a casino and spa.

Colonia del Sacramento, a small city in the south west, by the River Plate, facing Buenos Aires, has also taken off during the past 10 years. It has a beautiful historic quarter, which is a World Heritage Site, and many Uru-guayans and Argentines now have holiday homes in the city.

A construction boom is also under way in Montevideo - whose greater metropolitan area has a population of 1.8m people. Many new office building and residential blocks are being built. The city’s charming his-toric centre is carefully being restored.

Pulp and miningBetween 2005 and 2007, Botnia, a Finnish paper producer, invested $1.2 billion in a pulp mill at Fray Bentos on the River Uruguay, which divides the country from Argentina. At the time, this was the biggest foreign investment ever in Uruguay. The annual capacity of the mill is 1.1 million UPM pulp mill in Fray Bentos

03 04 05 06 07 08 09 10 11

0.8 5.0 7.5 4.1 6.5 7.2 2.9 8.5 6.0Source: Central Bank of Uruguay. For 2011 the figure is estimated

1. Real GDP growth, 2003-2011

03 04 05 06 07 08 09 10 11

16.9 13.1 12.2 11.4 9.2 7.6 7.3 6.7 6.0Source: National Bureau of Statistics. Annual Average

2. Unemployment rate, 2003-2011

2012

Gui

de to

Uru

guay

3

tons of eucalyptus pulp for which the mill uses around 3.5 million cubic metres of eucalyptus wood. In December 2009, Botnia sold its interest in the plant to another Finnish pulp producer, UPM.

Today, Montes del Plata, an Uruguayan pulp producer 50:50 owned by Chilean forestry group Arauco and Swedish-Finnish forestry company Stora Enso, is investing $2 billion in a new pulp mill at Punta Pereira, a free trade zone in the department of Colonia, 190km west of Montevideo. The plant will produce 1.3 million tonnes of pulp a year, and it will have a 160MW biomass-based power generation unit.

The project also includes a river port terminal and barge terminals with yards for wood storage, as well as a wood chip plant. The eucalyptus plantations that will feed the mill are located throughout Uruguay.

Minera Aratirí, the Uruguayan subsidiary of Anglo-Swiss mining group Zamin Ferrous, also plans to invest $3 billion in open-cast iron ore mines on the border of Durazno, Florida and Treinta y Tres departments, in the geographic centre of the country. The project - which could have some environmental impact - has not yet received the go-ahead from the government.

It would involve the construction of a plant, a pipeline, pumping stations and the country’s first deep-water port. Aratirí would extract magnetite, which has a high iron content. Reserves of 250 million tons have been discovered but it is estimated that they could surpass 1.1 billion tons.

Uruguay is also building up an important business in logistics. The country is gradually becoming the distribution centre for the Mercosur trading bloc zone, with the port of Montevideo as the hub port for the region. Last year, the port handled 518,120 containers, a 28% increase on the 2010 volume of 405,593 containers, according to Uruguay’s National Administration of Ports.

During the past decade, a large number of multinational groups have opened regional or global customer service centres in the country. They have taken advantage of Uruguay’s highly-skilled labour force, which includes a large number of graduates bilingual in Spanish and English. Outsourcing has become one of the main drivers of the services sector in the country. Uruguayans are also highly computer literate and software development is a growing industry.

Quality of life“Uruguay has become much more prosperous during the past five years,”

says Jean Shaw, vice-president of global customer support at Sabre Hold-ings, a global travel technology company headquartered in Southlake, Texas, which already has more than 900 employees in Uruguay but is expanding further. “There are a lot more cars on the roads, for example. The country attracted our business here eight years ago because of the high level of education and talent. That is one of the main factors that continues to bring investors to Uruguay.”

Uruguay is a beautiful country: it has 500km of beaches, often consisting of white sand and clear and pure blue seas. Even the capital, Montevideo, has beaches - such as Pocitos and Carrasco - right on its doorstep. Most of the coastal cities - including Montevideo - have a rambla, or an avenue that runs parallel to the beach. An important part of the Uruguayan way of life, they are popular with walkers and joggers.

Uruguay has a total geographic area of 176,215 sq km, greater than England and Wales combined. A lot of the interior of the country consists of rolling, green landscape. International Living magazine regularly ranks Uruguay number one in Latin America for the quality of life.

The country is also rated highly be a number of international organisa-tions. The IFO-Getulio Vargas Economic Climate Index ranked Uruguay second in Latin America (behind Chile) in its January 2012 survey. Trans-parency International ranked it in 25th place worldwide on its ranking of least corrupt countries in 2011 (only Chile had a lower ranking within Latin America). The Economist Intelligence Unit ranked it in 17th place on its Global Democracy index in 2011, the best rating for any Latin American country. According to the 2011 Legatum Prosperity Index, Uruguay is the 29th most prosperous country in the world, first in Latin America and third in the Americas, behind Canada and the United States. The Heritage Foundation ranked Uruguay in 29th position on its economic freedom index globally in 2012 - only Chile beat it in Latin America.

Uruguay also treats domestic and foreign investors equally. Invest-ments do not require prior authorization or registration and there is free transferability of capital and profits. Investment projects may qualify for corporate income tax rebates ranging from 51% to 100% of the amount invested.

Uruguay has created a diversified, modern economy in the past decade. The country is efficiently managed and the government sets great store by maintaining the rule of law. This is one of the main reasons why it has been so successful, and will cotinue to be, in attracting FDI.

Source: Ministry of Economy and Finance

3. Global fiscal and primary results, 2003-2011

-4

-2

0

2

4

2003 2004 2005 2006 2007 2008 2009 2010 2011

Perc

enta

ge te

rms

of G

DP

Global �scal result

Primary result

Source: Central Bank of Uruguay

4. Global and Net debt, 2003-2001

0

20

40

60

80

100

120

2003 2004 2005 2006 2007 2008 2009 2010 Sept.2011

Perc

enta

ge te

rms

of G

DP

Global public debt

Net debt

Reduced vulnerabilities, increased confidenceQ: what are the most successful aspects of the Uruguayan economy today?The country has experienced nine years of growth above the average of Latin America and overall rates of expansion during the period have been much better than during Uruguay’s history.

Exports of goods has been the main motor of economic growth. This has created a lot of employment opportunities. The strong fiscal stability has been one of the economy’s main anchors. Debt against GDP is low compared to other countries and this means that the economy has no real vulnerabilities.

The sovereign does not have to re-pay much debt during the next four years and the markets now allow it to issue debt with a average time to maturity of more than 12 years at favourable rates.

Q: how has the economy progressed during the past decade?Uruguay has taken full advantage of the favourable international envi-ronment for its exports during the past decade and it has been careful to create credibility for its macroeconomic policies.

Uruguay has reduced its vulnerabilities markedly during the past decade. It’s economy is much more diversified today. We have seen an inter-nationalisation of the economy. Important sectors include software, outsourcing, logistics and tourism. The country has maintained a strong rule of law and that has strongly encouraged foreign direct investment.

Q: what challenges does the economy face today?One of the short-term challenges is to confront problems at the interna-tional level, especially in relation to events in the eurozone. However, the country should be able to do this easily in the same way that it coped with the international crisis during 2008 to 2009.

In the longer term the country faces two major challenges: firstly, there must be massive investment in infrastructure to help business develop-ment throughout Uruguay; and secondly, there has to be a rise in worker productivity and an increase in human resources. Improved training is key to this.

The government estimates that economic growth will be 4% this year and that level should be sustainable in future years. Currently, inflation stands at around 8% but the Central Bank has a target of 4% to 6%. One of the country’s main objectives this year is to ensure that inflation is brought within or closer to the target range.

Q: why is Uruguay an attractive destination for foreign direct investment?Uruguay has been attracting a lot of FDI and will continue to do so

because of the excellent business opportunities in the country. There really are many opportunities in many sectors, in many activities. The government is committed to ensuring that the best possible business climate exists in the country. That is one of the reasons we have pursued such a prudent macroeconomic policy. The country has had a very long tradition of a strong rule of law and that is of utmost importance for foreign investors.

The current level of industrial action in the country is much lower than it experienced in the Nineties. There are some disputes today but these are limited to the public sector and have little impact on the private sector. There has been a transformation in the administration of the public sec-tor and this has greatly improved its efficiency.

Q: why is Uruguay viewed favourably by the markets?The financial markets have a favourable view of Uruguay because economic policy has been conducted well during the past 10 years, the government has completed all its main economic goals, and the state has respected the rule of law completely. The markets have been impressed by the evolution of the country’s sovereign debt during the past decade. The debt burden has become much more manageable.

Q: when do you think the country will achieve investment grade?Uruguay has been waiting a long time for investment grade. However, I think the country will achieve it sooner or later, it is only one notch below it now. The ratings agencies take many criteria into account but the truth is that Uruguay’s economic fundamentals are better than those of some Latin American countries that already have investment grade. They are also better than some European countries with investment grade. The economic dynamics are important, economic growth has not started to flatten out.

Finance and Economy Minister, Dr Fernando Lorenzo

2012

Gui

de to

Uru

guay

5

Uruguay can already issue sovereign debt at favourable rates and even at rates below countries that have investment grade. The markets are acting more quickly than the ratings agencies. The importance of achieving investment grade should not be over-estimated but it would help the country to access international markets if there was a deterioration in the international outlook and less global liquidity. During turbulent mo-ments, markets differentiate between those countries with investment grade and those without - that is why it is very useful to have it. Uruguay and its people have made a huge effort to improve the economy during the past 10 years. There has been a decade of sacrifice. It would be good to see that rewarded with investment grade.

Q: what are the main infrastructure projects planned for the country?We are planning many new infrastructure projects in all the main areas, including energy and transport. We have been considering strongly new sources of renewable energy. We want to become more inter-connected with Brazil, so that that country can provide us with more electricity. We are also looking at how we can use more liquefied natural gas and that would involve the development of a re-gasification terminal. We also want to improve energy efficiencies and we are encouraging people to use less energy.

In terms of transport, we plan a major upgrade of the highway network. Many existing roads will be improved. We are also looking at rehabilitat-ing the railway network, which has fallen largely into disuse during the past few decades. We also want to ensure that Uruguay has the fastest internet connection available, the best broad band on offer.

The state has a plan for infrastructure and it will invest as much as it can afford. It is important that the state creates the right framework for the development of infrastructure projects. We are also examining carefully the feasibility of private participation in infrastructure or PPI projects. One of the biggest challenges is to ensure that infrastructure is maintained and remains of a high quality. We are considering all types of agreement and mechanisms with private sector involvement. Perhaps the state can guarantee a project in some way and that can help to ensure that it receives long-term financing.

Q: has the eurozone crisis impacted upon Uruguay in any way? how would a double-dip recession in the developed world and/or a significant slowdown in China impact upon Uruguay?The main consideration for Uruguay is what happens in the principal Asian countries, China and India. They are important export destinations for us. Also, what happens in the two other BRICs, Brazil and Russia, is of major concern to us. Obviously, Brazil is a giant neighbouring country but Russia is one of the bigger importers of our meat, as well. During the past decade, Uruguay’s economy has expanded more rapidly than Brazil’s.

Uruguay offers many competitive products. Soya has not been such an important export for Uruguay compared to Argentina, say. Cattle is very important to the Uruguayan economy - the country has more than 15m ha of cattle-grazing land. Wool and dairy products are also significant parts of the economy. Natural resources are also playing a more impor-tant role.

Uruguay has a very open economy. However, the country today is in a much better position to absorb external shocks. Many of the country’s former vulnerabilities have been removed. We saw this during the 2008 to 2009 period, when the country emerged pretty much unscathed. This is because of all the hard work we have done over the years.

• Finance and Economy Minister, since 1 March 2010.

• Economist, graduated from the Faculty of Economics Sciences and Business of the University of the Republic of Uruguay in 1984.

• 1985, Diplome d’Etudes Approfondies en Economie et Finances Internationales at the University of Paris IX-Dauphine.

• 1997, Ph.D. in Economics from University of Carlos III in Madrid.

• 2005-2008, director of macroeconomic and financial advisory at the Ministry of Economy and Finance, Uruguay. 2005-2008

• Former director of trade policy advisory at the Ministry of Economy and Finance, Uruguay.

• Since 2009, President of Network of Economic Research of Mercorsur.

• National and international consultant on economic and financial subjects.

• 2006-2008, Director and researcher at the Centre for Economic Research (CINVE-Uruguay).

• Author of publications and reseach about macroeconomy, trade and international finance, and quantitative methods applied to the economy.

• Teacher in post-graduate studies in economy at the Economic Department of the Social Sciences Faculty (University of the Republic, Uruguay) and of the University ORT (Uruguay).

Dr FernanDo Lorenzo, biography

Uruguay rises 10 places in Euromoney’s country risk ratingsEconomists’ sentiments sharply improved in 2011 as Uruguay scored highly across a range of political, economic and structural indicators. Above-average scores indicate the country has good grounds to expect an upgrade from the rating agenciesIn the latest results of Euromoney’s Country Risk ratings (ECR), economists responded to Uruguay’s strong growth prospects and the continued reform agenda of its policy-makers by awarding the country improved scores across a range of political, economic and structural risk metrics. As a result, Uruguay climbed 10 places in Euromoney’s risk rankings during 2011, to 65th globally.

Key drivers behind the improved risk ranking included higher scores in the survey categories for bank stability, monetary policy/currency stability and employment. While the results were in keeping with the positive economic trends observed in the aggregated scores for Latin America, they indicate an improved level of confidence among analysts in both Uruguay’s macro-prudential regulatory framework and the monetary policies pursued by the central bank. The improvement drove an overall increase of 1.3 points in Uruguay’s economic score (out of 100).

The survey results also revealed a sharp improvement in economists’ views of the levels of political risk posed to investors in Uruguay’s economy. Survey scores in the categories for regulatory policy, information access/transparency, government stability and the risk of government interfer-ence/non-repatriation of capital have all seen substantial improvements in the past twelve months. The improvements, which coincide with the con-tinued growth of foreign direct investment in the country in recent years, point to the renewed credibility of Uruguay’s state institutions, corporate governance and legal framework in the eyes of international investors. This assessment is consistent with Uruguay’s improved score in ECR’s access to capital markets indicator, which rose sharply during 2011.

In global terms, Uruguay’s overall country risk score places the country in the third tier in ECR’s five-tier system. Typically, Tier 3 countries are emerg-ing economies with improving structural characteristics and stable politi-cal systems. The country’s ECR score, the eighth highest in Latin America, ranks Uruguay alongside established borrowers in the international capital markets including Romania, Bulgaria, Jordan and the Philippines.

Given the continued debate surrounding the hesitancy of the credit rat-ing agencies to award Uruguay an investment grade rating, it is notable

that several investment grade countries including India, Croatia, Russia and Hungary are ranked alongside Uruguay in the ECR system. Indeed, Uruguay receives a higher score from economists than four countries with investment grade ratings: Morocco, Tunisia, Barbados and Kazakhstan.

A comparison with Uruguay’s BB-rated peer group provides additional evi-dence in Uruguay’s favour. Uruguay receives consistently higher (ie, more favourable) scores for economic, political and structural risk than the aver-age score for BB-rated sovereigns, outscoring its peer group in 13 of ECR’s 15 qualitative variables. In both the economic and structural sections, economists award Uruguay scores in line with the average for sovereigns with a BBB rating (structural risk categories include demographics, hard and soft infrastructure and labour market/industrial relations).Uruguay also outperforms its peers in the political risk section, where Uruguay’s score is five points higher than the BB average. Uruguay’s score for corrup-tion is favourable and is the region’s second best, after Chile.

However, several areas continue to drag on Uruguay’s overall rating. Uruguay’s score in the access to capital indicator undershoots the BB aver-age, suggesting that further efforts are required to attract international investment. Increased transparency in the banking sector is necessary to improve Uruguay’s score for bank stability, a key metric in the economic survey, where the country marginally undershoots the BB average. Uru-guay’s below-average score in the monetary/policy currency stability sec-tion illustrates that Uruguay’s inflation rate, which remains above target, continues to be a concern.

Given Uruguay’s strong GDP growth outlook, it is likely that its economic scores will continue their upward trajectory in 2012. A further positive shift in market perception towards Uruguay, as measured by ECR’s access to capital markets section, would significantly improve Uruguay’s country risk score, and bring the country’s overall score into line with the average for investment grade sovereigns.

Five analysts take part in Euromoney’s Country Risk survey for Uruguay: Andrea Keenan (AM Best), Victoria Marklew (Northern Trust), Nicole Perel-muter and Guillermo Diaz (CAF) and Philipp Mayer (Erste Group).

Uruguay: outperforming its rating peers eCr economic political Structural Debt Credit access to capital score (100) (100) (100) (100) indicators (10) ratings (10) markets (10)Uruguay 50.3 55.8 51.5 55.8 5.0 3.8 3.8BB Average 45.1 48.7 46.8 43.6 4.2 3.2 4.7Source: ECR, Standard and Poor’s (December 2011). Credit rating score is derived using the average of Fitch, S&P and Moody’s rating for each country.

2012

Gui

de to

Uru

guay

7

Towards investment gradeSince its debt crisis in 2003, Uruguay has built up a reputation as one of Latin America’s most prudent and consistent sovereign borrowers. Ratings agencies have taken notice

International fi nancial markets are already factoring in that Uruguay will achieve investment grade soon. The credit ratings agencies are expected to grant the sovereign this status this year.

On 26 January, Moody’s revised its rating outlook to positive from stable for the Ba1 rating of the government of Uruguay, because of a steady im-provement in Uruguay’s sovereign credit profi le. It says that the govern-ment has shown a strong and continued commitment to fi scal discipline, which has resulted in moderate fi scal defi cits and better debt metrics.

Currently, Moody’s ratings of the government of Uruguay are Ba1 as long-term issuer (domestic and foreign currency), Ba1 for senior unsecured (domestic and foreign currency) and (P)Ba1 for senior unsecured shelf (foreign currency).

“Along with an enhanced ability to manage adverse economic and fi nancial conditions, the government’s credit profi le has been improv-ing gradually -- but steadily -- moving closer in line with that present in higher-rated sovereigns,” says Mauro Leos, a senior credit offi cer at Moody’s, clearly indicating that the sovereign is being considered for an upgrade.

On 30 January, Moody’s changed to positive from stable the outlook for the Ba2 long-term global foreign currency deposit ratings of Banco Santander, Banco Itaú and Lloyds TSB in the country. It also changed the outlook to positive from stable of the Ba1 and Aa2.uy foreign cur-rency deposit ratings of the two government-owned banks, Banco de la República Oriental and Banco Hipotecario, on its global and national scales, respectively.

Reducing vulnerabilitiesThe credit rating agencies say that the sovereign has not yet achieved investment grade because of some underlying vulnerabilities embed-ded in the government debt structure, mostly relating to the share of foreign currency-denominated debt. However, the government has been making a big eff ort to reduce these vulnerabilities through recent liability management operations.

Between 5 and 15 December, Uruguay issued a $2 billion equivalent global UI bond, a local currency, infl ation-indexed bond maturing in 2028. With Citi and HSBC acting as joint bookrunners, the issue created a new benchmark for the sovereign and the off ering represented one of the largest local currency bonds ever issued by a sovereign in the region. In a testament to the extent to which the fi nancial markets now respect the sovereign, the issue was able to proceed successfully despite the extreme turbulence in international markets at the time.

The off ering’s main goals were to reduce foreign currency borrowings to a lower risk level and to support the credit rating; to extend portfolio maturities; and to raise incremental cash to pre-fund possible 2012 cash needs. It achieved these objectives in four steps. First, on 5 December, it raised $1 billion equivalent in new benchmark 2028 global UI bonds, with a coupon of 4.375%. The fi nal, oversubscribed order book was made up

of more than 30 major institutional investors from the US, Latin America and Europe.

Secondly, between 5 and 9 December, it repurchased $1 billion equiva-lent of short-dated dollar-denominated and euro bonds. This involved a fi xed price cash tender off er and the foreign exchange bonds were bought at their market value.

Thirdly, the transaction extended the maturity of $725 million equivalent 5% global UI bonds, due in 2018, by exchanging them for the new 2028 global UI bond. The exchange off er had a 53% success rate.

On 12 December, after the successful completion of the exchange, the sovereign took the fourth step of expanding its global UI 2028 off ering by $275 million equivalent new cash, also issued at par price with 4.375% coupon.

Overall, the transaction - which involved Uruguay’s fi rst global bond since 2009 and the fi rst UI bond since 2007 - meant that the republic increased the proportion of the central government’s Uruguayan peso-denomi-nated debt to 49% of the total amount of debt. The average maturity has also increased to 12.3 years.

Warm welcome“I think rating agencies will look favourably on the recent funding and liability management transaction pursued by the republic, as it further reduces currency risk while extending the average life of the sovereign’s debt profi le, already one of the longest in the region,” says Juan Pablo Gallipoli, a vice-president in debt capital markets at HSBC.

“The deal was well received by real-money accounts and, through the combination of the new issue and exchange components of the trade, resulted in the creation of the largest local-currency benchmark for the sovereign. It is also one of the largest local-currency bonds in global format for the region and brings additional visibility and liquidity to Uruguay’s peso curve.

“While the overarching liability management transaction was complex, including the sovereign’s fi rst peso-to-peso exchange, the investment decisions made by holders were very straightforward, a factor that con-

Source: Bloomberg and JPMorgan

Th e evolution of Uruguay, Latam and Global EMBI 2010-2012

100

150

200

250

300

350

400

450

500

01/2010 04/2010 07/2010 10/2010 01/2011 04/2011 07/2011 10/2011 01/2012

EMBI Global

EMBI Uruguay

EMBI Brazil

EMBI Peru

EMBI Colombia

tributed to deliver high participation rates for the trade, especially for the sovereign’s top priority targets.”

He adds that it is healthy for a country to align the currency composition of its debt stock with that of its revenue profile, as Uruguay has consist-ently aimed to do.

Azucena Arbeleche, director of the debt management unit at Uruguay’s Ministry of Finance, says: “The country has a very conservative and very cautious approach to debt management. Uruguay has built up a strong financial cushion, which means it can easily run counter-cyclical policies”.

“We don’t really understand why credit ratings agencies feel that the economy still has some vulnerabilities. During the past decade, we have worked very hard to improve the country’s economic fundamentals. Our strong financial cushion means that we can be very opportunistic in the international markets and only have to tap them when we see a clear window. Sometimes we do it to preserve our dollar yield curve.”

Moody’s says that there are other factors behind the country’s positive credit outlook, including sustained economic growth supported by struc-tural aspects that have consolidated the medium-term potential growth prospects; improved government financial buffers, supported by an ample Central Bank cash reserve; a transition towards a more diversified export structure; and a track record of policy continuity, coupled with enhanced policy predictability.

The ratings agency says the external environment is likely to be char-acterized by an extended period of low global growth and persistent global financial turmoil in the short term. It says that Uruguay - as well as the rest of the region - is likely to be tested during the next year to 18 months. This creates an opportunity for it to assess the country’s credit resilience to see if it is comparable to that typically associated with invest-ment grade-rated sovereigns.

In July, Standard & Poor’s upgraded Uruguay’s rating by one notch to BB+, only one notch below investment grade. “The upgrade on Uruguay incorporates its growing track record on the implementation of prudent and consistent economic policies,” said Sebastián Briozzo, a Standard & Poor’s credit analyst, at the time of the upgrade.

Last July, Fitch also upgraded Uruguay’s long-term foreign currency issuer default rating to BB+ from BB, reflecting the agency’s opinion that Uruguay’s external and fiscal vulnerabilities had reduced. It says that it

made this move because of improvements in its external and fiscal sol-vency ratios, strengthened external liquidity, and the enhanced currency composition and maturity structure of government debt. High GDP per capita income, strong social indicators and a solid institutional frame-work underpin Uruguay’s creditworthiness.

Fitch adds that growth performance and outlook remain quite favour-able. Its five-year average growth increased to 6.2% in 2010, consider-ably higher than the BB-graded median over the same period. Reduced trade and financial links with Argentina make Uruguay less vulnerable to economic developments in its neighbour, it says.

Prudent and consistentIn 2003, Uruguay suffered from a severe sovereign debt crisis, largely brought about by the country’s past dependence on Argentina, which itself experienced an economic meltdown between 2001 and 2002. How-ever, since that time, it has built up a reputation as one of Latin America’s most prudent and consistent sovereign borrowers. Since 2003, it has lowered its overall cost of funding across currencies and instruments, and improved the republic’s credit ratings markedly.

In May 2003, the sovereign rescheduled $5.1 billion of debt, which helped to eliminate any financing gaps until 2005. The voluntary ex-change - which was open to holders of Brady bonds, eurobonds, samurai bonds and domestic securities - had a 93% participation rate.

In February 2006, Uruguay pre-paid $430 million of extraordinary loans from the World Bank and Inter-American Development Bank. In August and November 2006 Uruguay made two prepayments to the IMF of ap-proximately US$916 million and US$1.1 billion, respectively, thereby dis-charging all outstanding obligations to the IMF. In October 2006, it issued an aggregate principal amount of $602 million of 8% bonds due 2022 and an aggregate principal amount of $277 million of 7.625% bonds due 2036. It tendered $275 million.

In December 2007, it conducted a global offering, which involved the purchase of $116 million out of $435 million eligible in dollars and euros. It also had a local offering, whereby $74 million was purchased out of $401 million eligible and $50 million UI equivalent was purchased out of $1.1 billion UI equivalent that was eligible.

In June 2008, three concurrent exchange offers took place, targeting more than $2.9 billion of bonds and resulting in the extension of around $800 million of multi-currency external and domestic debt.

2004 2005 2006 2007 2008 2009 2010 2011roll over riskAverage maturity (yrs) 7.4 7.9 12.1 13.6 13.0 12.7 12.3 12.3% debt due in one year 11.3 16.0 4.8 2.9 2.3 3.6 5.5 2.4Liquid assets CG/amortization due in 1 year 0.3 0.3 0.4 0.7 1.6 1.4 0.7 4.0(1

interest rate risk% debt that refixes rate in 1 yr 32 34 22 18 20 11 15 6.4Average time to refix (yrs) 4.9 6.6 11.1 12.3 11.9 12.0 11.3 11.7Duration (yrs) 5.6 8.0 8.9 10.5 9.9 10.3 10.4 10.2% debt with fixed rate 77 78 82 83 81 91 88 94Foreign Currency risk % local currency debt 11 11 15 26 28 31 34 49

Uruguay central government debt risk indicators

Source: Debt Management Unit, Ministry of Economy and Finance (1) Amortizations of the next 12 months starting in December 2011

2012

Gui

de to

Uru

guay

9

“A number of factors are attracting foreign groups to the country, including the solid rule of law, tax and fiscal incentives, and the stable social and political environment”

FDI set to stay at record level

Uruguay’s fast-growing economy has attracted record levels of foreign direct investment and is expected to attract a similar level this year.

Between 2004 and 2011, the economy expanded at 6% a year and the government is forecasting that it will grow by 4% this year (independent economic consultancies estimate growth will be in the region of 5%). FDI inflows in 2010 stood at around 6% of GDP and it is estimated that they reached a similar level last year.

Huge investments - such as one of $2 billion by Montes del Plata, the pulp producer 50:50 owned by Chilean forestry firm Arauco and Swedish-Finnish forestry group Stora Enso - should help to boost FDI rates to even higher levels in the future.

Domestic investors lead the wayFDI inflows have consolidated investment by domestic companies, which has pushed the investment rate up to around 20% of GDP from a historic

level of around 14%. In January, Ancap, the state-owned oil company, announced plans to invest $330 million in the modernization of an oil refinery at La Teja, a neighbourhood of Montevideo. It expects to have four new highly efficient and environmentally-friendly refining units up and running by the second quarter this year.

Between last year and 2013, Antel, the state-owned telecommunications company, plans to invest $180 million in fibre-optic cables throughout the country, providing much faster internet connections. By September last year, it had already invested $30 million of the total and some 85,000 homes, mostly in the capital, had high-speed access. The investment should raise the speed of transmission from 14.4 megabits a second - the fastest possible through copper cables - to between 50 and 100 Mbit/s. It expects to invest $100 million in the new technology this year, so that a further 240,000 homes have access to fast internet.

Modernizing the economy“Uruguay has been attracting foreign investment from companies around the world,” says Roberto Villamil, executive director at Uruguay XXI, the country’s investment and export promotion agency. “State-backed companies themselves are heavily investing in new infrastructure and, combined with the foreign direct investment, this is helping to modernize the Uruguayan economy. A number of factors are attracting

foreign groups to the country, including the solid rule of law, tax and fis-cal incentives, and the stable social and political environment.”

The country has attractive free zone, free port and free airport regimes, and broad investment-related tax exemptions. It also provides access to Mercosur, the free trade zone including Argentina, Brazil and Paraguay, which has a total GDP of $2 trillion. The country offers the best labour value for money in the region and has a convenient time zone between the US and Europe. It has world-class free port facilities in Montevideo, the strategic regional hub for South America’s southern cone.

“Salaries have increased markedly in Uruguay during the past decade,” adds Villamil. “However, remuneration packages for chief executives, chief financial officers and middle management are lower than those in Brazil, Argentina and Chile.”

Up to 450,000 Uruguayans live overseas - including an estimated 116,000

in Argentina - but many are returning home because they perceive many economic opportunities in the country.

Back to the soilAn example of a highly successful local business is Union Agriculture Group, a diversified agricultural company founded in 2008. The com-pany started with only 6,000 hectares of land but now owns a total of 95,000ha. It is among the top five land owners in the country and is the only one of the five that was set up by Uruguayans (big Argentine groups are important landowners). It plans to list on the New York Stock Ex-change this year and will become the first Uruguayan company to do so.

“If you want to invest in farmland, Uruguay is the place to go,” says Juan Sartori, UAG’s executive chairman. “The country has a high level of secu-rity. It is the only country in the region where there are virtually no restric-tions on agricultural exports. Brazil and Argentina were the first countries in the region to embrace more intensified agricultural production. We are starting to catch up.”

He says that in 2003 only 10,000ha of land in the country was planted with soya beans but that by 2010 that level had reached 1 million ha. However, the country has the potential for up to 6 million ha to be planted with the crop.

In the past 10 years, Uruguay has become a key destination for FDI, attracted by the country’s rich human and natural resources and stable political environment

UAG produces a range of crops - including rice, soya and wheat - on a rotation basis to preserve the quality of the soil. The land is also used for cattle grazing as part of the rotation cycle and to ensure that it is 100% utilised.

The company plans to list 20% of its equity in New York and expects to raise around $200 million. Since 2008, it has raised $350 million from investors around the world - mostly family offices or high-net-worth individuals - who took equity stakes in the business.

“We are holding off the listing at the moment until market conditions improve,” says Sartori. “We are all ready to carry out the IPO but we want to do it at the right moment when valuations have recovered. I hope we will set an example for other Uruguayan companies that want to come to the market in the future. The Montevideo stock market is quite illiquid, so New York presents a good alternative. I believe we will see many more high-quality companies from the country - which of course are of an ap-propriate size - seek a listing in the future.”

Montes del Plata says it was attracted to Uruguay mostly because of its natural setting, the excellent political and economic environment, and the country’s strong economic performance. It says it only takes 10 years

to harvest eucalyptus plantations in the country because of the high soil quality; in other countries with poorer soil conditions it can take much longer.

“The high-quality soil provides a big production advantage,” says Erwin Kaufmann, general manager at Montes del Plata. “However, the political environment is also important - parties on the left and the right all recog-nize the importance of maintaining the rule of law. The country has had the right macroeconomic policy for a long time now. It is also reassuring to know that it will continue to move in the right direction.”

The company is financing the construction of the mill from its own funds, as well as international loans. European export agencies - which support

overseas sales from their countries with direct loans for capital goods - have also helped. The fact that the pulp mill was granted free zone status, providing important tax relief, has also been a huge advantage.

The pulp mill - at Conchillas, in the Colonia department, on the River Plate - is only 250km from the eucalyptus forests. This will help to keep transport costs down.

Human resourcesUPM - the Finnish forestry group that took over control of the huge pulp mill at Fray Bentos from another Finnish group, Botnia, in December 2009 - says that human talent was one of the factors that lured it to Uruguay.

“The country has excellent human resources,” says Alberto Brause, direc-tor of corporate relations and business development for Latin America at UPM and a Uruguayan who used to live in the US but returned to the country because of the employment opportunities. “When Botnia first invested in the pulp mill it sent staff out from Finland to train locals but they were surprised at just how quickly Uruguayans picked up the skills. Uruguay is now sending experts to Finland and we even send them to Africa when we are considering projects in that continent.”

UPM employs 3,400 staff directly in the country, including 500 university graduates. Some 400 of its staff work in laboratories or research and development.

The Uruguayan government believes there are many opportunities for foreign companies in private participation in infrastructure (PPI) projects, either through the construction of the projects or through managing them post-construction. The country is embarking on major infrastruc-ture projects in new roads, railways, ports, prisons and social housing. The government has set an upper limit of the net present value of its financial obligations of 7% of GDP and annual payments to the private partner cannot exceed 0.5% of GDP.

It says that some 2,000km of new roads are being considered but their development would be over a 20- to 30-year period. It would like to up-grade the country’s ports so that they are suitable for larger ocean-going

vessels. The potential investment ranges in size from $400 million to $1 billion, depending on how the ports are modernized. The government says the railway network is now antiquated and has high maintenance costs. It would like to revamp and expand the whole network. A new prison will entail an investment in the order of $220 million.

Uruguay has become one of the most attractive destinations for FDI in the Americas during the past 10 years. The country has a high quality, educated work force that still offers labour value for money. The govern-ment is one of the most business-friendly in Latin America and sets very few restrictions on exports. The free zone regimes have created a power-ful incentive for foreign investors and the country is expected to receive even greater sums in FDI in the future.

“Parties on the left and the right all recognize the importance of maintaining the rule of law. The country has had the right macroeconomic policy for a long time now”

Source: Central Bank of Uruguay

Current account and Foreign direct investment, 2003-2011

-6

-4

-2

0

2

4

6

8

2003 2004 2005 2006 2007 2008 2009 2010 Sept.2011

Perc

enta

ge te

rms

of G

DP

Current account

Foreign direct investment

2012

Gui

de to

Uru

guay

11

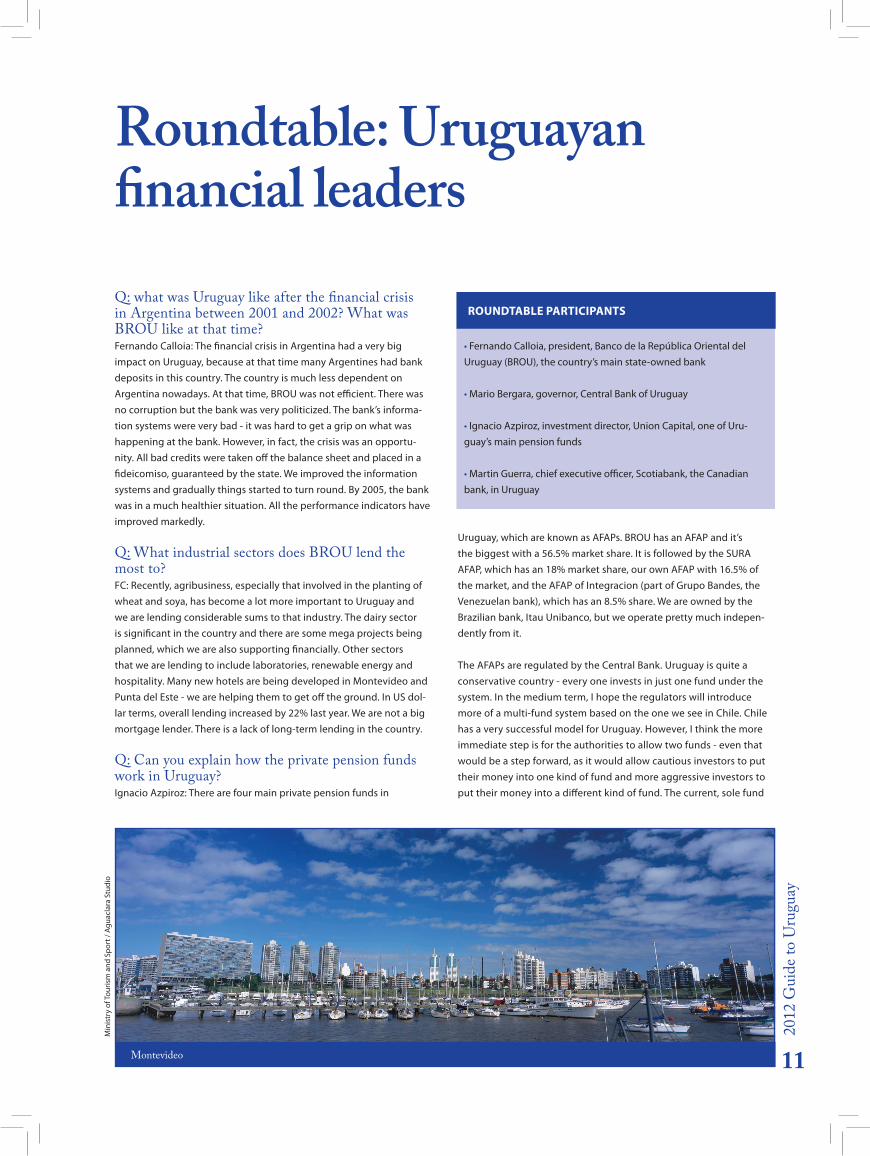

Roundtable: Uruguayan financial leadersQ: what was Uruguay like after the financial crisis in Argentina between 2001 and 2002? What was BROU like at that time?Fernando Calloia: The financial crisis in Argentina had a very big impact on Uruguay, because at that time many Argentines had bank deposits in this country. The country is much less dependent on Argentina nowadays. At that time, BROU was not efficient. There was no corruption but the bank was very politicized. The bank’s informa-tion systems were very bad - it was hard to get a grip on what was happening at the bank. However, in fact, the crisis was an opportu-nity. All bad credits were taken off the balance sheet and placed in a fideicomiso, guaranteed by the state. We improved the information systems and gradually things started to turn round. By 2005, the bank was in a much healthier situation. All the performance indicators have improved markedly.

Q: What industrial sectors does BROU lend the most to?FC: Recently, agribusiness, especially that involved in the planting of wheat and soya, has become a lot more important to Uruguay and we are lending considerable sums to that industry. The dairy sector is significant in the country and there are some mega projects being planned, which we are also supporting financially. Other sectors that we are lending to include laboratories, renewable energy and hospitality. Many new hotels are being developed in Montevideo and Punta del Este - we are helping them to get off the ground. In US dol-lar terms, overall lending increased by 22% last year. We are not a big mortgage lender. There is a lack of long-term lending in the country.

Q: Can you explain how the private pension funds work in Uruguay?Ignacio Azpiroz: There are four main private pension funds in

Uruguay, which are known as AFAPs. BROU has an AFAP and it’s the biggest with a 56.5% market share. It is followed by the SURA AFAP, which has an 18% market share, our own AFAP with 16.5% of the market, and the AFAP of Integracion (part of Grupo Bandes, the Venezuelan bank), which has an 8.5% share. We are owned by the Brazilian bank, Itau Unibanco, but we operate pretty much indepen-dently from it.

The AFAPs are regulated by the Central Bank. Uruguay is quite a conservative country - every one invests in just one fund under the system. In the medium term, I hope the regulators will introduce more of a multi-fund system based on the one we see in Chile. Chile has a very successful model for Uruguay. However, I think the more immediate step is for the authorities to allow two funds - even that would be a step forward, as it would allow cautious investors to put their money into one kind of fund and more aggressive investors to put their money into a different kind of fund. The current, sole fund

• Fernando Calloia, president, Banco de la República Oriental del Uruguay (BROU), the country’s main state-owned bank

• Mario Bergara, governor, Central Bank of Uruguay

• Ignacio Azpiroz, investment director, Union Capital, one of Uru-guay’s main pension funds

• Martin Guerra, chief executive officer, Scotiabank, the Canadian bank, in Uruguay

rounDtabLe partiCipantS

Montevideo

Min

istr

y of

Tour

ism

and

Spo

rt /

Agua

clar

a St

udio

can only invest in high-quality sovereign bonds and only up to 15% overseas. Some 1.2 million workers in Uruguay - out of the country’s total workforce of 1.6 million - are affiliated to one of the private pen-sion schemes.

Q: What is the role of the Central Bank in Uruguay?Mario Bergara: Following the financial crisis of 2002 to 2003, some financial institutions were closed in the country. There have been big regulatory changes since then and we have moved much closer to best international practices. There is much more rigorous regulation in place these days. The bank’s charter was changed in 2008, before then the charter was quite confusing. The bank is in charge of super-vising the whole financial system, pension funds, the capital markets and currency exchange system. That gives us a lot of control over the whole financial system and we have been able to devise consistent

rules for the whole system. In 2009, a new law for capital markets was introduced: before this legal change those markets were more based on self-regulation. The law sets standards and is helping to promote the country’s capital markets.

Today, we regulate 14 banks, including BROU. The most important private banks include Santander, Itau, BBVA and Citi. Non-residents make up around 20% of all deposits today - Argentines make up around 15% of all deposits in the system but that is way down from 2002 when they accounted for around 45% of all deposits.

The Central Bank has a very high level of reserves of $10 billion to $11 billion, more than 20% of GDP. That is a very high proportion compared to GDP, one of the highest in Latin America and creates a significant cushion for the Uruguayan economy. Overall, credit in the economy is low at only 22% of GDP - there is a lot of margin for that to expand in the future. There is a great deal of liquidity in the Uru-guayan financial system - it’s amazing. Banks’ solvency is double the capital required by the rules - we will not have any problem fulfilling the Basle III requirements. Non-performing loans peaked in 2008 at 1.5% of all credit, they are now under 1%. There is a superintendency in charge of supervising the banks - although it reports to the Central Bank, it operates quite autonomously from the Central Bank. Some 30% of the bank’s staff are employed by the superintendency. A meet-ing takes place every three months at which we decide the appropri-ate level for interest rates.

Q: Do you think there should be a new law for the private pension funds?MB: The new legislation is held up in the Congress, currently. The legislation would introduce two funds in which people can invest.

Q: What is inflation like in Uruguay?MB: We have always to be concerned about inflation. Uruguay has a history of very high inflation. However, since 2003, the inflation rate has always been in single digits. All our figures are highly transpar-ent and credible. Currently, the rate is 8%, compared with, say, 6.5% in Brazil. Our target range is 4% to 6%. The government has worked very hard to ensure that the fiscal situation is good. Almost every year economic growth has surpassed the government’s forecasts. We have learned that high inflation is a very bad thing, so we will not let it get out of control in the country. Even in Russia and India inflation is around 10%. There is no inflation spiral in Uruguay. The reason why the rate is above the target range is because commodity prices have gone through the roof and the economy has been growing for seven years above its long-term potential rate of growth. I don’t think people are too concerned about the inflation rate being slightly above the target range. The country’s benchmark interest rate is now

at 8.75%. It’s difficult to say when inflation will start to drop, because that depends on international prices. Domestic demand also remains strong. However, I think we will see a gradual reduction during the next 18 months - as long as it goes in the right direction, that is the main thing.

Q: Why did Scotiabank decide to start a business in Uruguay?Martin Guerra: In July last year, Scotiabank completed the purchase of NBC, a Uruguayan banking group, and of Pronto, a consumer credit card business, from Advent International, the private equity company. We acquired Pronto because we thought it had a very interesting and very innovative consumer credit model. NBC is a bank with a similar ethos to our own; it’s much more of a traditional bank, and we thought it was a great opportunity to acquire both businesses. Pronto has around 250,000 active clients, mostly with credit cards or loans. We now have around 37 branches in the country through the consumer credit side of the business and a further 48 branches on the banking side.

Q: Why is Uruguay such an attractive country to invest in?MG: I think the strong rule of law is the main factor. The country has very strong institutions, a very strong democracy. Furthermore, there has been macroeconomic stability for a long time. I am very optimistic about Uruguay. I think it will have investment grade by the end of next year. I think the markets have factored in the probability of in-vestment grade by some 80% to 90%. The credit ratings agencies are a bit concerned about the rate of inflation, 8% is too high. However, the government is concerned about the rate and is putting in place policies to contain inflation.

“The government has worked very hard to ensure that the fiscal situation is good. Almost every year economic growth has surpassed the government’s forecasts”

2012

Gui

de to

Uru

guay

13

Natural advantagesLong a favoured destination for visitors from neighbouring Argentina and Brazil, Uruguay is increasingly attracting tourists from further afield

The number of foreign tourists visiting Uruguay jumped to 3.5 million last year, from 2.1 million in 2005, according to the Ministry for Tourism and Sports.

The number of Brazilians visiting Uruguay increased to 430,000 last year, from 170,000 in 2005. Many cross the border and go shopping in Uru-guay, as a ‘free shop’ exists and prices are lower. Many more Brazilians also travel to the coastal resort of Punta del Este and the capital, Montevideo. Argentines have long been very active buyers in Uruguay’s second home property market but Brazilians are also more and more attracted to this market. Brazilians perceive the country as a safe, and close destination.

Between 2007 and 2009, Argentines found it difficult to visit Uruguay while the Botnia pulp mill was being developed on the River Uruguay, because environmental activists closed the bridges that connect the two countries. The number of Argentine visitors dropped to 1.98 million but, since the end of the dispute, the figure increased to 2.47 million in 2010.

Wider appealAccording to the Ministry for Tourism and Sports, the country attracted 60,000 Chilean tourists last year, 130,000 Latin American tourists from outside the Mercosur zone, 110,000 North American tourists and 180,000 Europeans. Up to 15,000 Germans and up to 17,000 British visited the country.

Today, there are 91 flights a week between São Paulo and Uruguayan airports and 34 flights a week between Santiago and Uruguayan airports, underlining how interconnected Uruguay has become.

“Argentine tourists represent a very mature but important market for us,” says Benjamin Liberoff, Uruguay’s national director for tourism. “However, Brazilians are becoming a more and more significant market.”

One reflection of the importance of Argentina to Uruguay is the estimate that Argentines own close to 300,000 properties in the country. In particular, Argentines from two of the country’s main cities, Rosario and Cordoba, have had very close links with Uruguay historically and many

have bought second homes in or around Punta del Este.

“Argentine visitors also come to the country for economic reasons,” adds Liberoff. “They have been very prominent in modernizing farming and the agricultural industry in the country. They have been at the forefront of soya production in Uruguay. The strong rule of law in Uruguay has been one of the factors that has attracted them.”

He adds that many Argentines have settled in the country permanently and this can be seen if you visit the best schools in Punta or Colonia, where many of the pupils come from Argentine families. It has also become more common for Argentines to live and work in Buenos Aires during the week but to spend the weekends in their second homes in Colonia, which is just a short distance across the River Plate from the Argentine capital.

Punta del Este has a short peak summer season, which starts immediately after Christmas and lasts until the third week of January. During this pe-riod, the city is brimming in private jets belonging to wealthy individuals from around the world. Its marina is also full of luxurious yachts.

The local government of Maldonado department, in which Punta del Este is located, plans to develop a major convention centre and exhibition hall near the old airport of El Jagüel, which today is only used by helicopters. This is expected to bring many more visitors to Punta during the off-peak season (although hotel occupancy between April and November is already at the reasonably healthy level of 70%).

The land for the project costs $14.5 million with a 30-year lease and the construction cost is $24 million. An additional $4 million is being spent on the business plan and the convention centre’s promotion. It is being financed through the issuance of a fideicomiso, a type of fiduciary trust common in Latin America and backed by investors.

The conference centre will be able to host a total of 5,500 people, includ-ing 2,500 in the main halls and the rest in the side halls. The centre’s construction is expected to start in the first quarter next year..

Capital investmentsMontevideo is also attracting a great deal more investment in hotels. As well as the refurbishment of the grand hotel in Carrasco by Sofitel, the luxurious French hotel chain - which includes the development of an important casino - many international groups are converting historic buildings in the city’s old town into luxury boutique hotels.

Last year, the city’s hotel capacity increased by 850 new rooms and it is expected to expand by a further 1,200 rooms within the next 18 months.

Since the start of the last decade, the country has promoted itself with the slogan ‘Uruguay Natural’. More and more foreign visitors are coming to the country to make the most of its beautiful beaches and to enjoy its lush, green interior. Increasingly, Uruguay is finding a place on the international tourist map.

Punta del Este

Min

istr

y of

Tour

ism

and

Spo

rt /

Indi

as S

tudi

o