Embed Size (px)

Citation preview

#RIC16

The Death Of Pureplay Retail: Investigating the Top Trends and Tactics

Driving Industry Change

Maureen Mullen, Co-‐Founder, Chief Strategy Officer, L2, Inc.

BENCHMARKING DIGITAL PERFORMANCE

BENCHMARKING

EDUCATION

RESEARCH

1,801

#RIC164

#RIC16

THE DEATH OF PUREPLAYRETAIL

INTRODUCTION

6

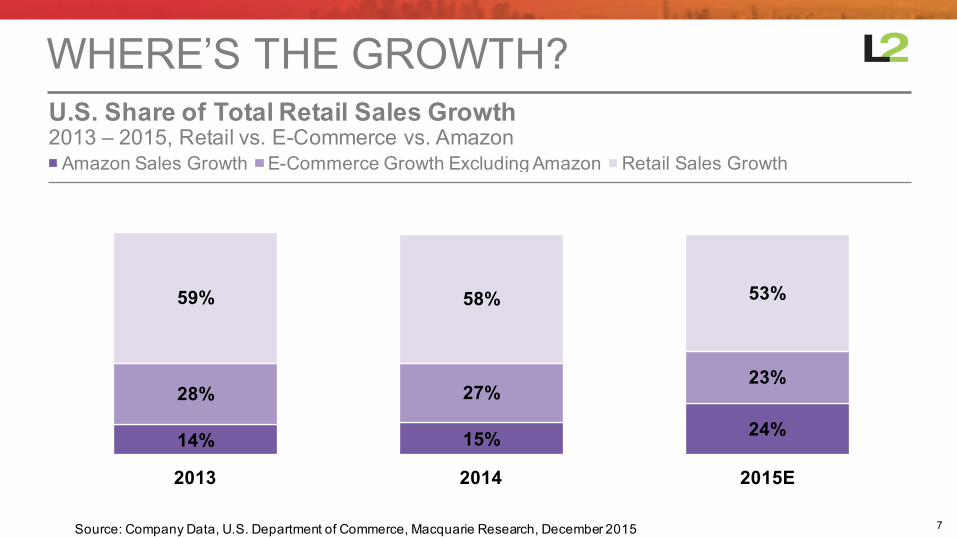

November 2015, N=1,006By DemographicChannel Where U.S. Internet Users Planned to Shop on Black Friday

ONLINE SHOPPING SURGES

Source: “Holiday Shopping Survey 2015,” conducted by Ipsos, November 6, 2015

YOUNGAges 18 - 34

AFFLUENTHHI = $50K+

Online Only30%

Online & In-Store26%

In-Store Only22%

Don't Plan to Shop21%

Online Only24%

Online & In-Store17%In-Store

Only18%

Don't Plan to Shop41%

7

2013 – 2015, Retail vs. E-Commerce vs. AmazonU.S. Share of Total Retail Sales Growth

WHERE’S THE GROWTH?

14% 15% 24%

28% 27%23%

59% 58% 53%

2013 2014 2015E

Amazon Sales Growth E-Commerce Growth Excluding Amazon Retail Sales Growth

Source: Company Data, U.S. Department of Commerce, Macquarie Research, December 2015

8

2015Share of Online Sales: Top-50 U.S. E-Commerce Retailers

NOT THE FULL STORY

Source: Internet Retailer, L2 Analysis

Other E-Commerce Pureplays8%

Other Retailers

41%

Amazon36%10%

Walmart5%

9

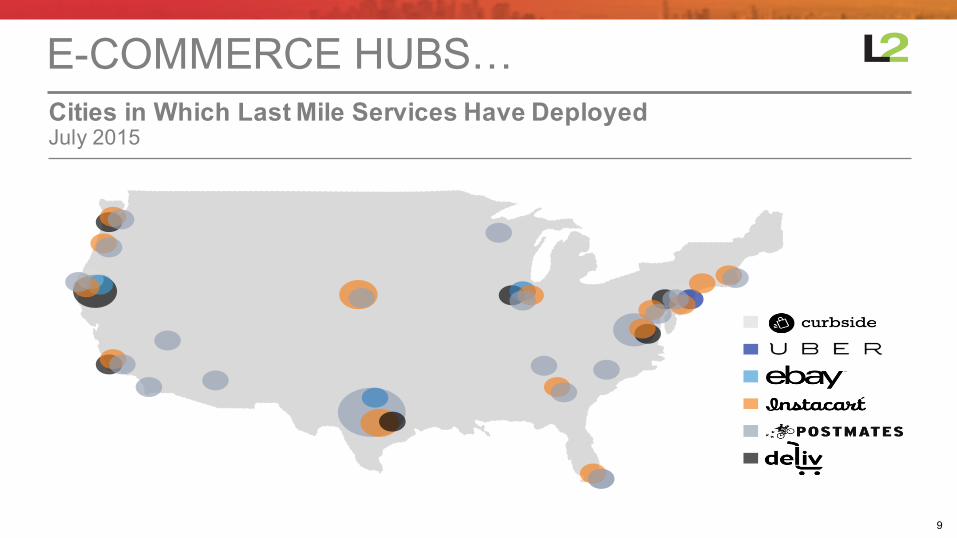

July 2015Cities in Which Last Mile Services Have Deployed

E-COMMERCE HUBS…

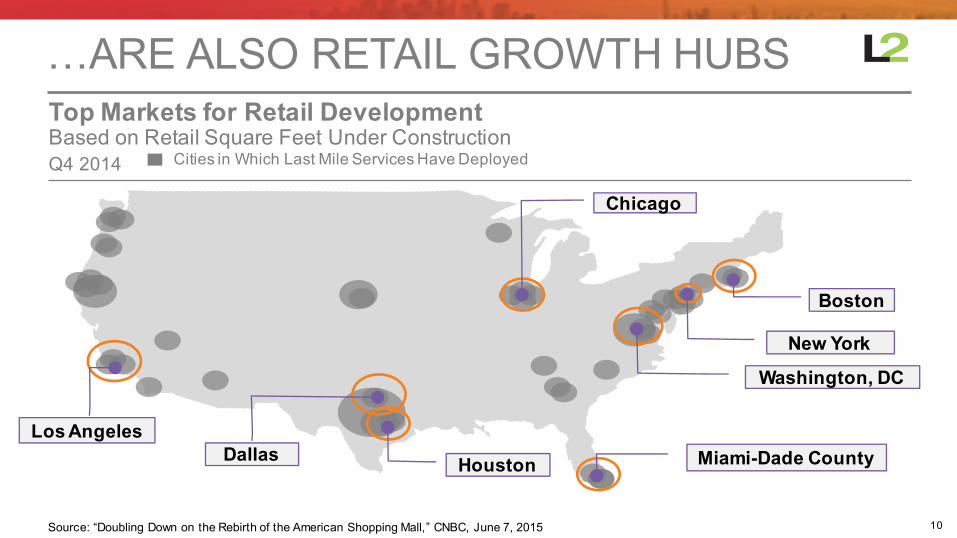

10

Q4 2014Based on Retail Square Feet Under ConstructionTop Markets for Retail Development

…ARE ALSO RETAIL GROWTH HUBS

Boston

New York

Washington, DC

Miami-Dade CountyHoustonDallasLos Angeles

Chicago

Source: “Doubling Down on the Rebirth of the American Shopping Mall,” CNBC, June 7, 2015

Cities in Which Last Mile Services Have Deployed

11

December 2015Manhattan: New or Future Mall Locations

HIGH-END RETAIL IS THRIVING

March 2015Brookfield Place

Expected 2016WTC Mall

Expected 2019Hudson Yards

Sales are up $45 per square foot year-on-year at high-end (A++) malls.**Source: Fortune, March 2015

12

U.S., 2015 n E-Commerce Pureplay RetailerFastest Growing E-Commerce Players Among Top-500

PUREPLAY GROWING FAST, BUT…

Brand 2015 E-CommerceSales 2015 E-Commerce Sales Growth

1 Leesa Sleep LLC $28,500,000 20257.1%

2 Harry’s Grooming $30,000,000 400.0%

3 Petco Animal Supplies Inc. $319,000,000 283.7%

4 Touch of Modern Inc. $100,000,000 233.3%

5 Saatva Inc. $81,000,000 200.0%

6 Casper Sleep $85,000,000 183.3%

7 FitBit Inc. $75,000,000 150.0%

8 rue21 Inc. $35,000,000 150.0%

9 Shoes.com $222,992,939 149.9%

10 Pharmapacks LLC $69,000,000 119.0%

Source: Internet Retailer

13

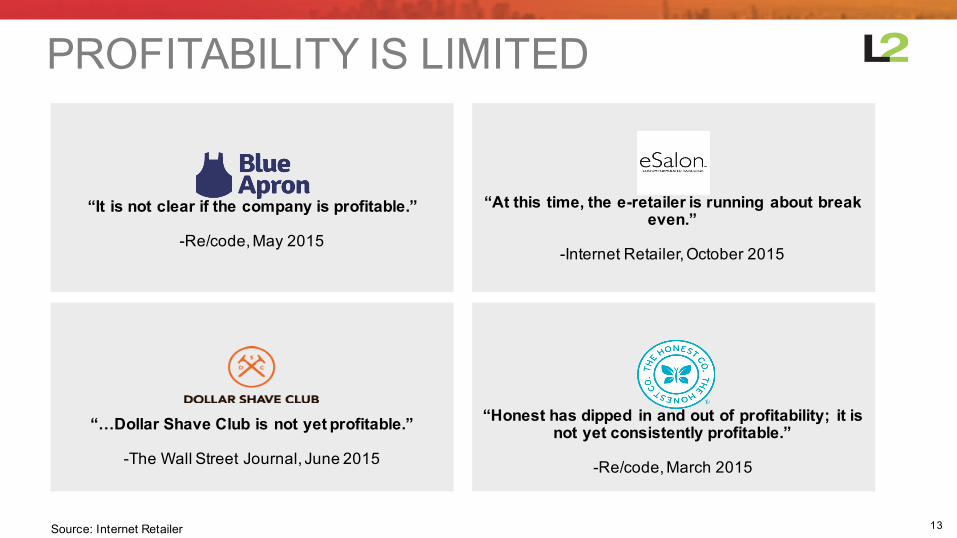

PROFITABILITY IS LIMITED

“At this time, the e-retailer is running about break even.”

-Internet Retailer, October 2015

“It is not clear if the company is profitable.”

-Re/code, May 2015

“…Dollar Shave Club is not yet profitable.”

-The Wall Street Journal, June 2015

“Honest has dipped in and out of profitability;; it is not yet consistently profitable.”

-Re/code, March 2015

Source: Internet Retailer

14

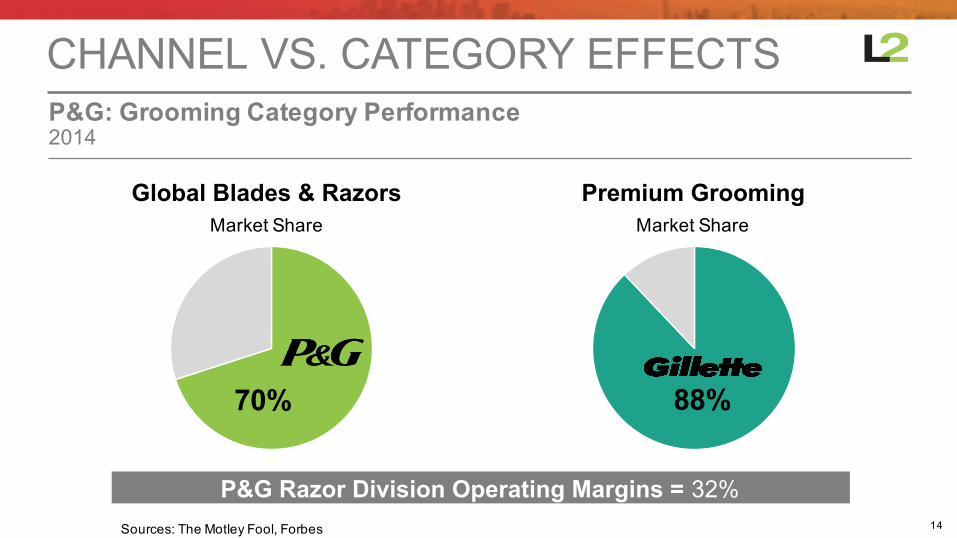

2014P&G: Grooming Category Performance

CHANNEL VS. CATEGORY EFFECTS

Global Blades & RazorsMarket Share

Premium GroomingMarket Share

70% 88%

P&G Razor Division Operating Margins = 32%Sources: The Motley Fool, Forbes

15

The 4XFusion ProGlide

RIPE FOR DISRUPTION

Number of Cartridges 4 4

Blades per Cartridge 5 4

Price $18.47 $6 + Free Shipping

16

Q1 2015 – Q3 2015 Millions of Dollars, 2015Amazon YoYSales Growth Amazon Operating Income

AMAZON: POWERED BY AWS

Source: SEC Filings;; “Amazon’s $160 billion business you’ve never heard of,” CNN Money, November 4, 2015

49%

81% 78%

13% 17% 20%

Q1 2015 Q2 2015 Q3 2015

Amazon Web Services Amazon Retail

38%

62%

Q1 2015

Amazon Web Services Amazon Retail

36%

64%

Q2 2015

52%

48%

Q3 2015

$706M

$1,705M$993M

17

49%

16%

73%

22%

Prime Non-Prime

Spent $200+ Over the Last 90 Days Shop on Amazon 2+ Times per Monthn=647 Prime Members, 970 Non-Prime MembersSelf-Reported Spend and Usage of Amazon.com

PRIME DRIVES LOYALTY…

Sources: RBC Capital Markets Proprietary Survey, Macquarie Research

18

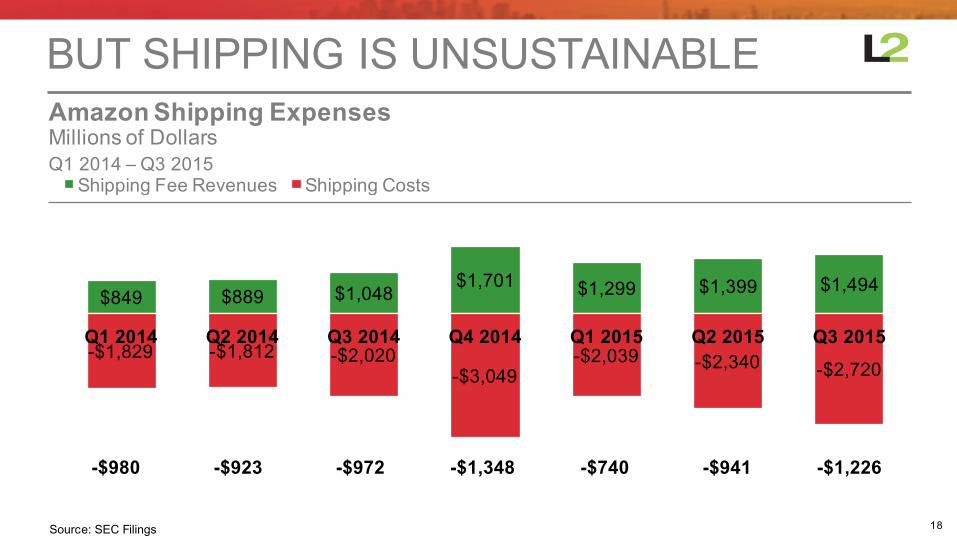

Q1 2014 – Q3 2015Millions of DollarsAmazon Shipping Expenses

BUT SHIPPING IS UNSUSTAINABLE

$849 $889 $1,048$1,701 $1,299 $1,399 $1,494

-$1,829 -$1,812 -$2,020-$3,049

-$2,039 -$2,340 -$2,720

Q1 2014 Q2 2014 Q3 2014 Q4 2014 Q1 2015 Q2 2015 Q3 2015

Shipping Fee Revenues Shipping Costs

-$980 -$923 -$972 -$1,348 -$740 -$941 -$1,226

Source: SEC Filings

19

Q1 2013 – Q2 2015Millions of DollarsAmazon Quarterly Net Income

VISION TRUMPS PROFITS

$482

$79$92

-$57

$214

-$437

-$126

$108

$239

-$41-$7

$82

Q4 2015Q3 2015Q2 2015Q1 2015Q4 2014Q3 2014Q2 2014Q1 2014Q4 2013Q3 2013Q2 2013Q1 2013

Source: SEC Filings

Amazon did not turn its first profit until Q4 2001 — seven years after its founding — and has ducked in and out of profitability ever since.

20

1997–2015, in USD Billions nAmazon ◼ Walmart Annual Net Income: Amazon vs. Walmart

IN A CORNER

Source: Quartz.com;; Data from FactSet

21

October 14, 2015Walmart Stock Price Following Annual Investor Day Earnings Call

…NOT AFFORDED TO ALL RETAILERS

Source: Quartz.com;; Data from FactSet

Walmart lost $20 billion in market value in 20 minutes – the entire market value of Macy’s – after it forecasted depressed earnings per share until 2019 due to increases in

employee wages and investments in e-commerce.

#RIC16

THE DEATH OF PUREPLAYRETAIL

STUDY OVERVIEW

23

L2 Intelligence Report: Death of Pureplay Retail 2016

STUDY OVERVIEW

Contrasts digital and retail KPIs for pureplay, evolved pureplay and omnichannel retailers to illustrate how companies can benefit from operating and investing across channels.

RETURN ON INVESTMENTCONSUMER EXPERIENCE

CUSTOMER ACQUISITION THE LAST MILE

24

BRAND LIST

Online-only retailers that may have experimented with a popup shop, but have not opened a permanent retail location

Companies that began as online-only but have opened a permanent retail location in the last five years

Retailers that have effectively linked their in-store and online businesses to leverage their status as omnichannel retailers

25

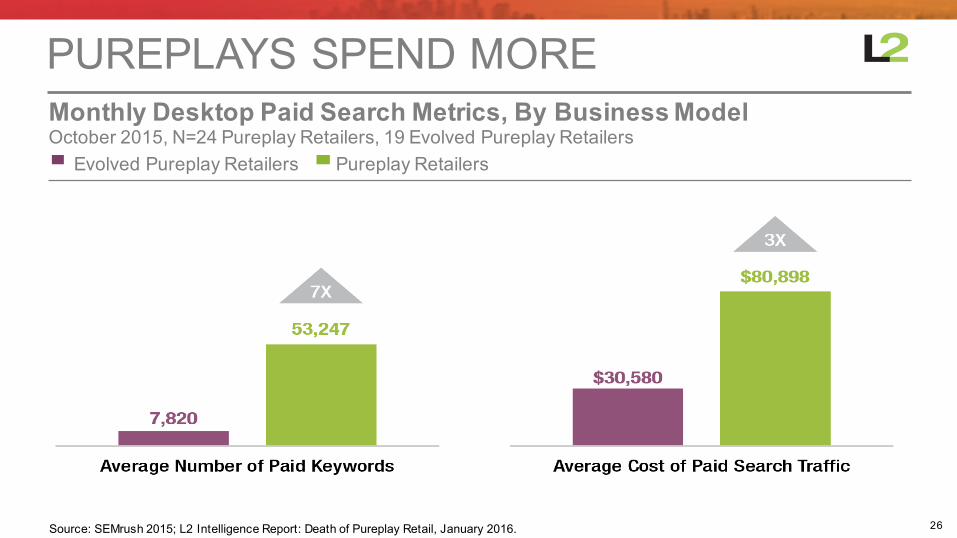

August 2015, N=24 Pureplay Retailers, 19 Evolved Pureplay Retailers, 20 Omnichannel LeadersBy Operating ModelDesktop Paid Search Traffic as a Percentage of Overall Search

TRAFFIC MUST BE BOUGHT

Source: Similar Web, August 2015

26

Evolved Pureplay Retailers Pureplay RetailersOctober 2015, N=24 Pureplay Retailers, 19 Evolved Pureplay RetailersMonthly Desktop Paid Search Metrics, By Business Model

PUREPLAYS SPEND MORE

Source: SEMrush 2015;; L2 Intelligence Report: Death of Pureplay Retail, January 2016.

27

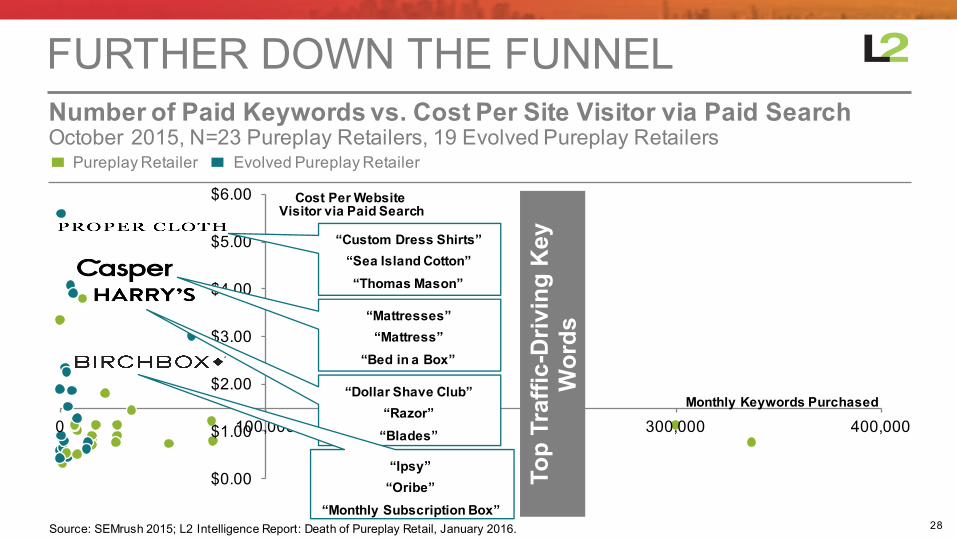

October 2015, N=23 Pureplay Retailers*Number of Paid Keywords vs. Cost Per Site Visitor via Paid Search

AND CAST A WIDER NET

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

0 100,000 200,000 300,000 400,000

Cost Per Website Visitor via Paid Search

Monthly Keywords Purchased

Source: SEMrush 2015;; L2 Intelligence Report: Death of Pureplay Retail, January 2016. *Note: Excluding The Clymb (no paid keywords)

Top Traffic-Driving Key Words“Lingerie”

“Red Dresses”“Dr Martens”

“Wedding Dresses”

“iPhone 6 Cases”“Dog Collars”

“Jewelry”

“Bar Stools”“Shopping”

“Maternity Clothes”

“Lingerie”“Umbrella”

28

October 2015, N=23 Pureplay Retailers, 19 Evolved Pureplay RetailersNumber of Paid Keywords vs. Cost Per Site Visitor via Paid Search

FURTHER DOWN THE FUNNEL

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

0 100,000 200,000 300,000 400,000

Cost Per Website Visitor via Paid Search

Monthly Keywords Purchased

PureplayRetailer Evolved PureplayRetailer

Source: SEMrush 2015;; L2 Intelligence Report: Death of Pureplay Retail, January 2016.Top Traffic-Driving Key

Words

“Custom Dress Shirts”“Sea Island Cotton”“Thomas Mason”

“Mattresses”“Mattress”

“Bed in a Box”

“Dollar Shave Club”“Razor”“Blades”

“Ipsy”“Oribe”

“Monthly Subscription Box”

29

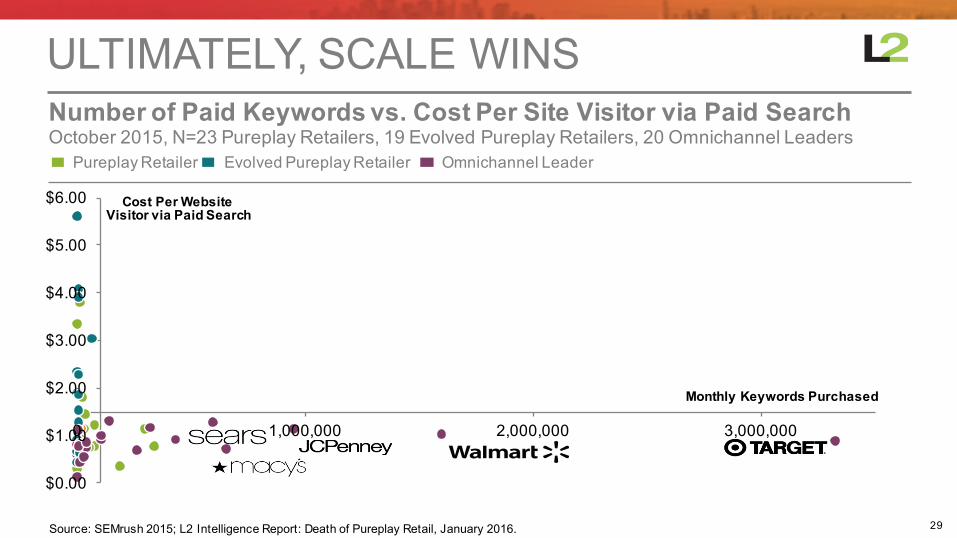

October 2015, N=23 Pureplay Retailers, 19 Evolved Pureplay Retailers, 20 Omnichannel LeadersNumber of Paid Keywords vs. Cost Per Site Visitor via Paid Search

ULTIMATELY, SCALE WINS

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

0 1,000,000 2,000,000 3,000,000

Cost Per Website Visitor via Paid Search

Monthly Keywords Purchased

PureplayRetailer Evolved PureplayRetailer Omnichannel Leader

Source: SEMrush 2015;; L2 Intelligence Report: Death of Pureplay Retail, January 2016.

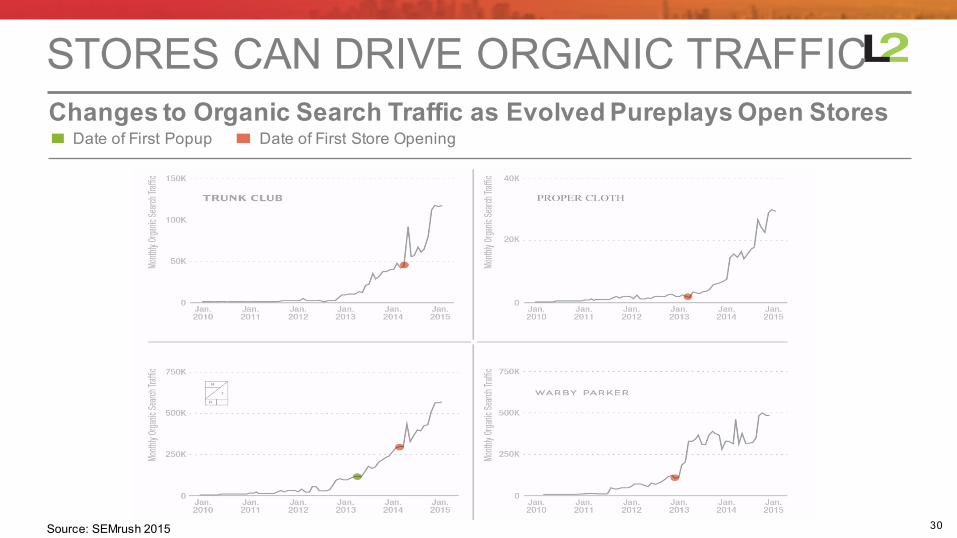

30

Changes to Organic Search Traffic as Evolved PureplaysOpen Stores

STORES CAN DRIVE ORGANIC TRAFFIC

Source: SEMrush 2015

Date of First Popup Date of First Store Opening

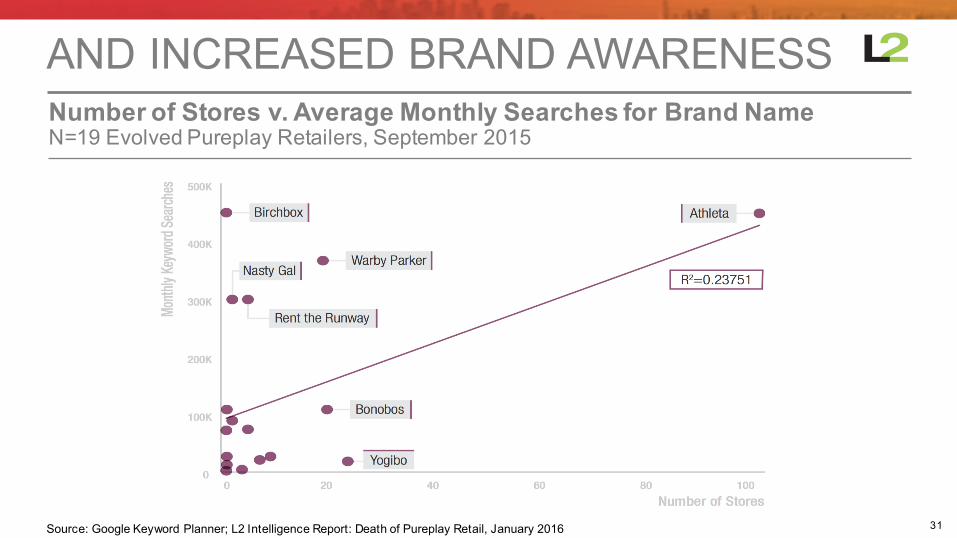

31

N=19 Evolved Pureplay Retailers, September 2015Number of Stores v. Average Monthly Searches for Brand Name

AND INCREASED BRAND AWARENESS

Source: Google Keyword Planner;; L2 Intelligence Report: Death of Pureplay Retail, January 2016

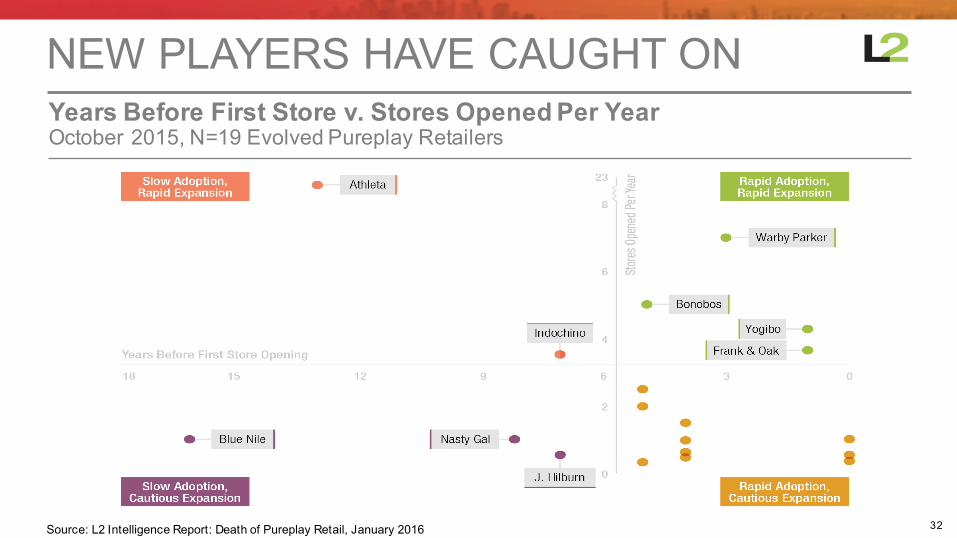

32Source: L2 Intelligence Report: Death of Pureplay Retail, January 2016

October 2015, N=19 Evolved Pureplay RetailersYears Before First Store v. Stores Opened Per Year

NEW PLAYERS HAVE CAUGHT ON

33

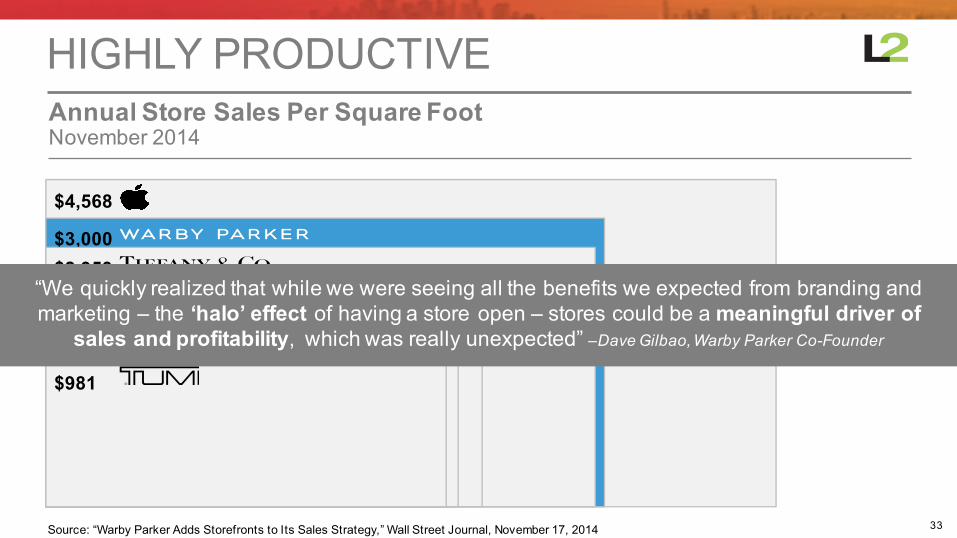

$4,568

$3,000$2,953

$1,192$1,061

November 2014Annual Store Sales Per Square Foot

HIGHLY PRODUCTIVE

Source: “Warby Parker Adds Storefronts to Its Sales Strategy,” Wall Street Journal, November 17, 2014

$981

“We quickly realized that while we were seeing all the benefits we expected from branding and marketing – the ‘halo’ effect of having a store open – stores could be a meaningful driver of

sales and profitability, which was really unexpected” –Dave Gilbao, Warby Parker Co-Founder

34

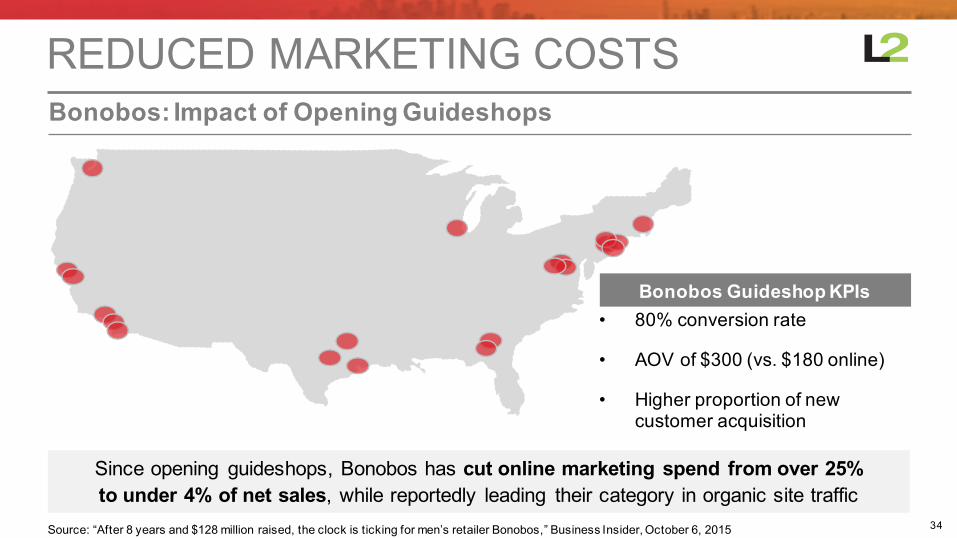

Bonobos: Impact of Opening Guideshops

REDUCED MARKETING COSTS

Source: “After 8 years and $128 million raised, the clock is ticking for men’s retailer Bonobos,” Business Insider, October 6, 2015

Bonobos GuideshopKPIs• 80% conversion rate

• AOV of $300 (vs. $180 online)

• Higher proportion of new customer acquisition

Since opening guideshops, Bonobos has cut online marketing spend from over 25% to under 4% of net sales, while reportedly leading their category in organic site traffic

35

$0

$10

$20

$30

$40

$50

$60

$70

$0$20$40$60$80$100$120$140$160

1/1/02 1/1/04 1/1/06 1/1/08 1/1/10 1/1/12 1/1/14

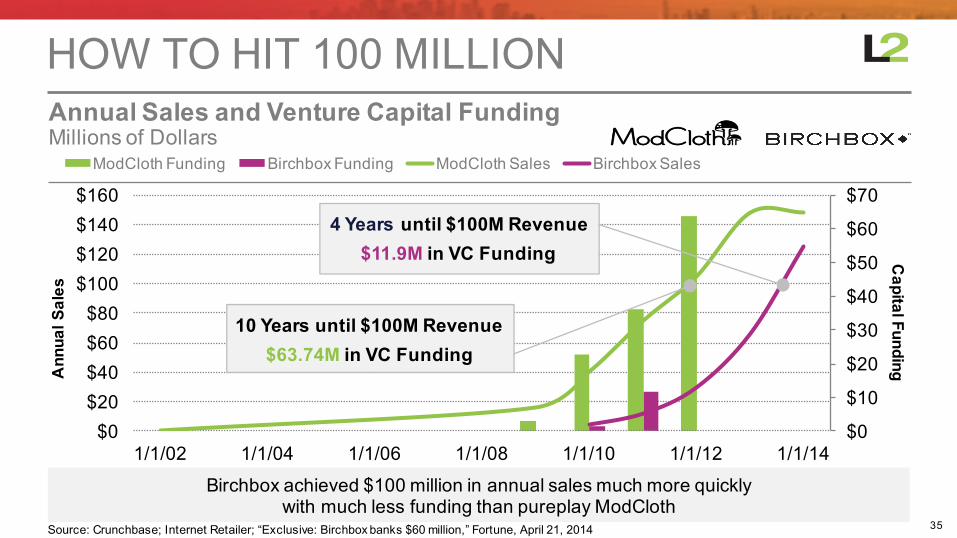

ModCloth Funding Birchbox Funding ModCloth Sales Birchbox SalesMillions of DollarsAnnual Sales and Venture Capital Funding

HOW TO HIT 100 MILLIONCapital FundingA

nnual Sales

Birchbox achieved $100 million in annual sales much more quickly with much less funding than pureplay ModCloth

Source: Crunchbase;; Internet Retailer;; “Exclusive: Birchbox banks $60 million,” Fortune, April 21, 2014

10 Years until $100M Revenue$63.74M in VC Funding

4 Years until $100M Revenue$11.9M in VC Funding

36

$0$10$20$30$40$50$60$70$80

$0$20$40$60$80$100$120$140$160

1/1/02 1/1/04 1/1/06 1/1/08 1/1/10 1/1/12 1/1/14

ModCloth Funding Birchbox Funding ModCloth Sales Birchbox SalesMillions of DollarsAnnual Sales and Venture Capital Funding

WHAT WAS THE DIFFERENCE?Capital FundingA

nnual Sales

From August 2013 to July 2014, Birchbox opened a popup shop, announced funding for a new store, and opened a flagship

Opens popup

Announces $60M funding for permanent store

Opens Flagship

Source: Crunchbase;; Internet Retailer;; “Exclusive: Birchbox banks $60 million,” Fortune, April 21, 2014

37

ModCloth: Brick-and-Mortar Initiatives

MODCLOTH TURNS TO BRICKS

Hires former Chief Strategy Officer at Urban Outfitters

Opens its first pop-up shop in two years in LA

Launches a “Fit Shop” in San Francisco

“…as we look to 2016, we can start to think about when and where to launch our first permanent fit shop.”

— Matthew Kaness, CEO & Board Director

January 2015 April 2015 June 2015

38

October 2015, N=6 Pureplay Retailers, 7 Evolved Pureplay RetailersAverage Threshold for Free Shipping

PRESSURE

*Excluding retailers without free shipping threshold.Source: L2 Intelligence Report: Death of Pureplay Retail, January 2016.

39

October 2015, N=23 Pureplay Retailers, 19 Evolved Pureplay RetailersPercent of RetailersExpedited Delivery Options Offered, By Business Model

PUREPLAYS PRIORITIZE SPEED

87% of pureplay retailers offer expedited shipping options,compared with just two thirds of evolved pureplays.

Source: L2 Intelligence Report: Death of Pureplay Retail, January 2016.

PureplayRetailer Evolved PureplayRetailer

40

Shipping Subscription Programs

REASONABLE EXPECTATIONS?

Retailer

Revenues $89 billion $486 billion $440million

Shipping Program $99 / year $50 / year $50 / year

41

October 2015, N=19 Evolved Pureplay Retailers, 20 Omnichannel Leaders % of RetailersBuy Online, Return In-Store, By Business Model

INVENTORY CAPABILITIES STILL LAG

Source: L2 Intelligence Report: Death of Pureplay Retail, January 2016.

42

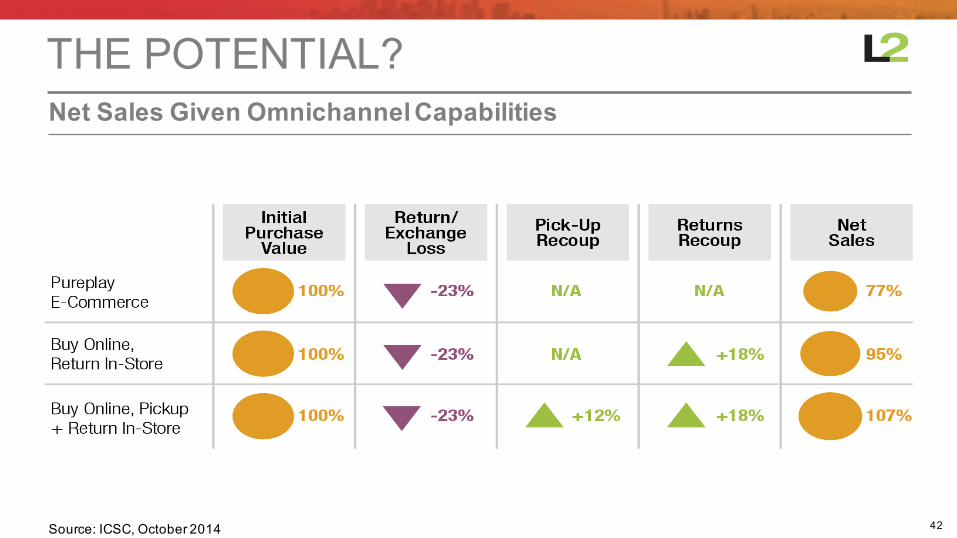

Net Sales Given OmnichannelCapabilities

THE POTENTIAL?

Source: ICSC, October 2014

43

Macy’s Ship from Store Locations vs. Amazon’s U.S. FC’s

SHIP-FROM-STORE IS WINNING

§ n 2012 n 2013 n 2014 n 2015 Macy’s SFS Locations nAmazon Distribution Centers

292 SFS Locations

500 SFS Locations

775 SFS Locations

886 SFS Locations

68 FC’s

Source: “Macy’s battle for the ‘last mile’ leads to Amazon,” NYPost.com, July 2015;; “Amazon Global Fulfillment Center Network,” MWPVL, October 2015

44

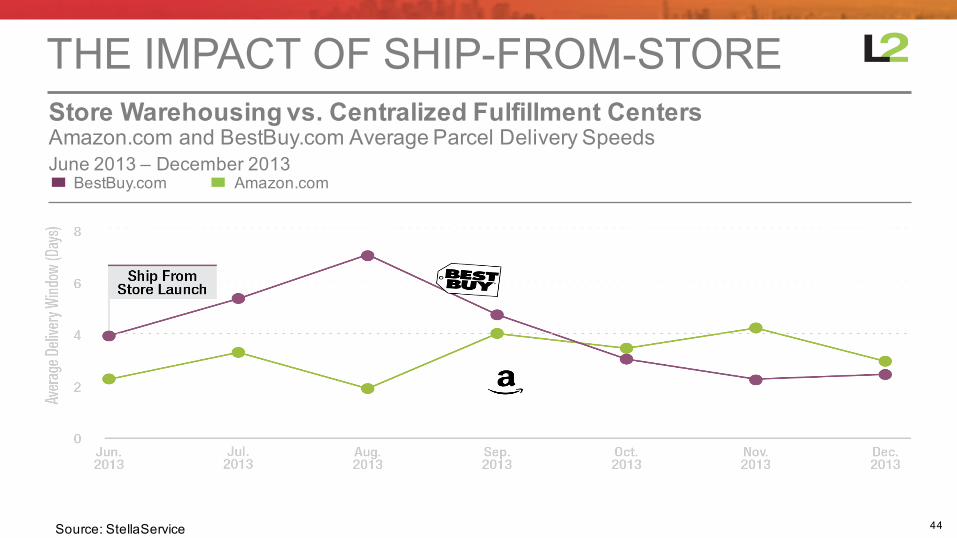

June 2013 – December 2013Amazon.com and BestBuy.com Average Parcel Delivery SpeedsStore Warehousing vs. Centralized Fulfillment Centers

THE IMPACT OF SHIP-FROM-STORE

BestBuy.com Amazon.com

Source: StellaService

45

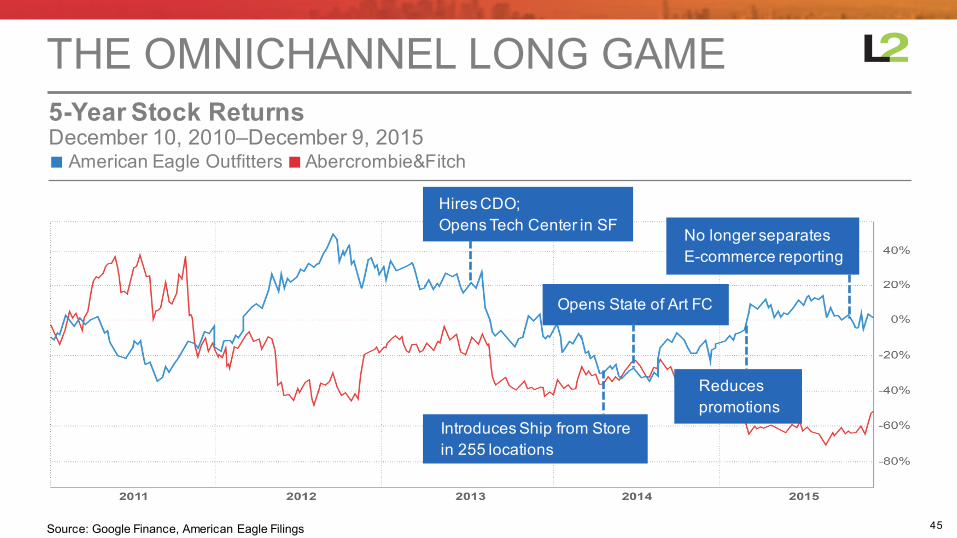

◼ American Eagle Outfitters ◼Abercrombie&FitchDecember 10, 2010–December 9, 20155-Year Stock Returns

THE OMNICHANNEL LONG GAME

Source: Google Finance, American Eagle Filings

No longer separates E-commerce reporting

Hires CDO;;Opens Tech Center in SF

Introduces Ship from Storein 255 locations

Opens State of Art FC

Reduces promotions

46

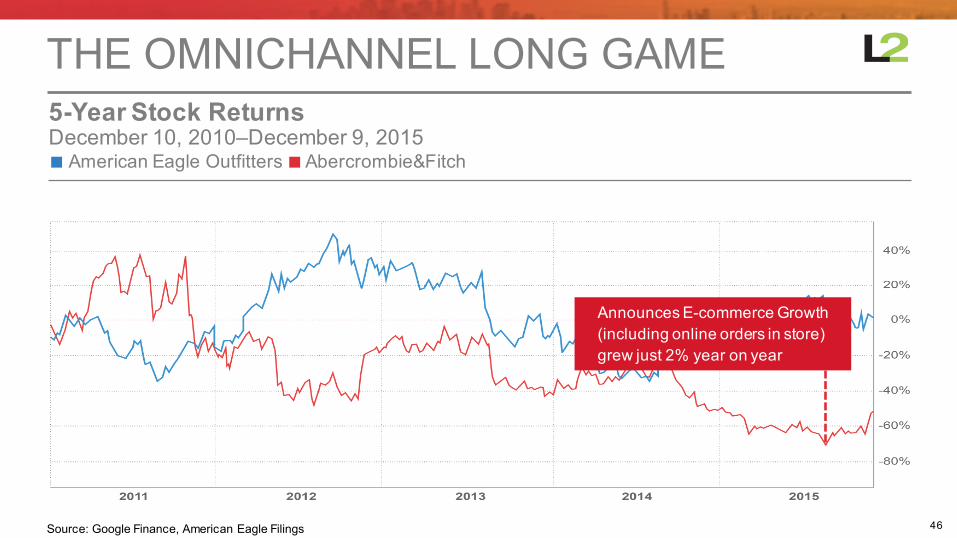

◼ American Eagle Outfitters ◼Abercrombie&FitchDecember 10, 2010–December 9, 20155-Year Stock Returns

THE OMNICHANNEL LONG GAME

Source: Google Finance, American Eagle Filings

Announces E-commerce Growth (including online orders in store) grew just 2% year on year

47

CONNECTIVE TISSUE

Reserve Items In-Store Only via App

Personalized “My AEO” Offers Inbox

AERewards Card Links to Passbook

Push Notifications for Timely Offers

Halfway through 2015, American Eagle returned to positive sales growth (+11%)

Source: L2 Inc.

48

October 2015, N=19 Evolved Pureplay Retailers, 20 Omnichannel Leaders% of RetailersIn-Store Event & Appointment Promotion, By Business Model

NEXT-GEN SERVICE

Source: L2 Intelligence Report: Death of Pureplay Retail, January 2016.

Omnichannel Leaders Evolved PureplayRetailers

49

Indochino: Online Appointment Booking for Bespoke Suits

BESPOKE APPOINTMENT SERVICES

“Anytime we open a store in a city, we see awareness and sales in that city grow four times compared to what it was previously, as online-only.”

— Drew GreenIndochino CEO

50

Rent the Runway: In-Store Fit Consultations

INCREASED CONSUMER CONFIDENCE

“A lot of the in-store customers are members on our site whohaven’t transacted yet. They’re intrigued but they haven’t gotten over the hump of being concerned over fit or getting the item on time.”

— Jennifer HymanRTR Co-Founder & CEO

Source: “Bonobos, Rent the runway Navigate Clicks-to-Bricks Evolution,” Apparel, November 1, 2014

51

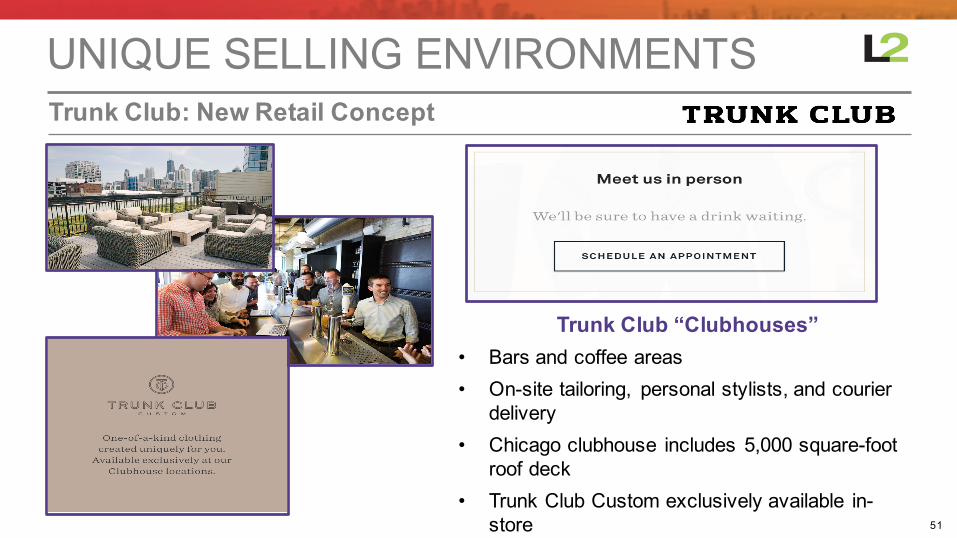

Trunk Club: New Retail Concept

UNIQUE SELLING ENVIRONMENTS

Trunk Club “Clubhouses”• Bars and coffee areas• On-site tailoring, personal stylists, and courier

delivery• Chicago clubhouse includes 5,000 square-foot

roof deck• Trunk Club Custom exclusively available in-

store

52

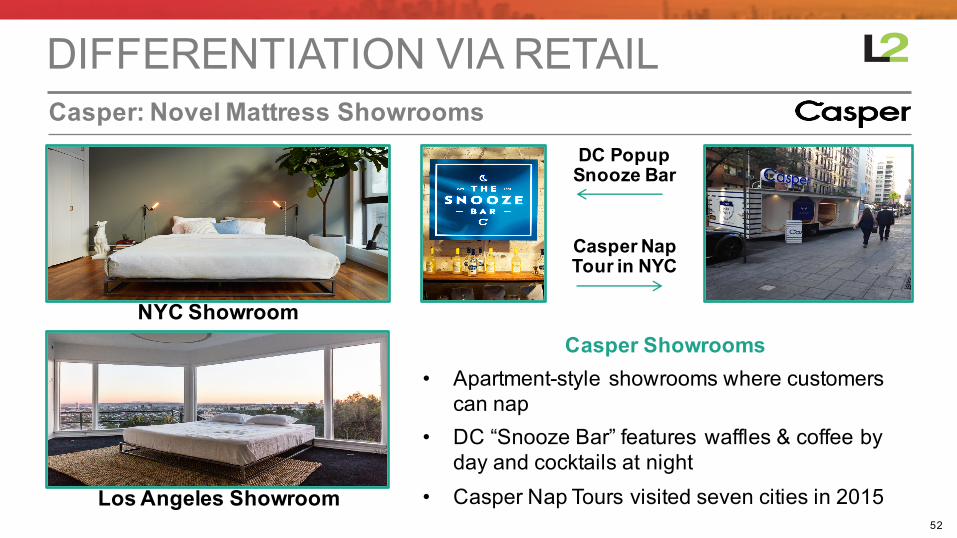

Casper: Novel Mattress Showrooms

DIFFERENTIATION VIA RETAIL

Casper Showrooms• Apartment-style showrooms where customers can nap

• DC “Snooze Bar” features waffles & coffee by day and cocktails at night

• Casper Nap Tours visited seven cities in 2015

NYC Showroom

Los Angeles Showroom

DC Popup Snooze Bar

Casper Nap Tour in NYC

53

Percentage of Non-Entry Level Team Hired from Select Retail OrganizationTop Companies Represented in Evolved Retailer Management Teams

DRAFTING RETAIL DREAM TEAMS

Douglas SimpsonVP of RetailPreviously VP of Operations,Juicy Couture

Andrew Lande-ShannonDesign Director, Offline RetailPreviously VP of Stores, Joe Fresh

Philippe PinatelPresident and COOPreviously SVP and GM,Sephora Canada

Benjamin FayVP of Retail Development and Customer ExperiencePreviously EVP of Store Design, JCPenney

Birchbox Senior Retail Hires

#RIC16

THE DEATH OF PUREPLAYRETAIL

CONCLUSIONS

55

CONCLUSIONS

E-COMMERCE CONSOLIDATION: WINNER TAKES ALL

SIREN SONG OF PUREPLAY RETAIL

THE MYTH OF ORGANIC REACH ONLINE

VC SUBSIDIES: WHEN DOES THE MUSIC END?

TWO FOR ONE: ONLINE TRAFFIC + OFFLINE PROFITS

#RIC16

THE DEATH OF PUREPLAYRETAIL

Maureen Mullen, L2 Inc.

#RIC16