Embed Size (px)

Citation preview

www.taxquotient.com

Indirect Tax Risk Management

An effective Enterprise Tax Risk Management (TRM)

13th October, 2015

Anthony Fernandes

Founder

Tax Quotient

Tax Risks

Tax risks are potential outcomes that arise from activities or events which could lead to tax adversities throughout the life of an enterprise.

www.taxquotient.com

Tax Risks – The Indian Context

• Tax Risks are currently one of the most significant risks faced by businesses and they are not “insurable”. Biggest business risks – Lloyd’s survey 2013

• The Indian tax system, particularly the indirect tax system is still evolving.

• There are 3 levels of indirect taxes, some over-lapping. The tax system is complex, dynamic and overseen by an aggressive tax administration. All these factors creates scope for tax risks/difficulties.

• So how does one recognize the risks, assess and mitigate them?

www.taxquotient.com

Tax Risks & Tax Opportunities

The nature of the activity determines the type of risks involved

www.taxquotient.com

The key therefore is to understand the activity

and risks involved.

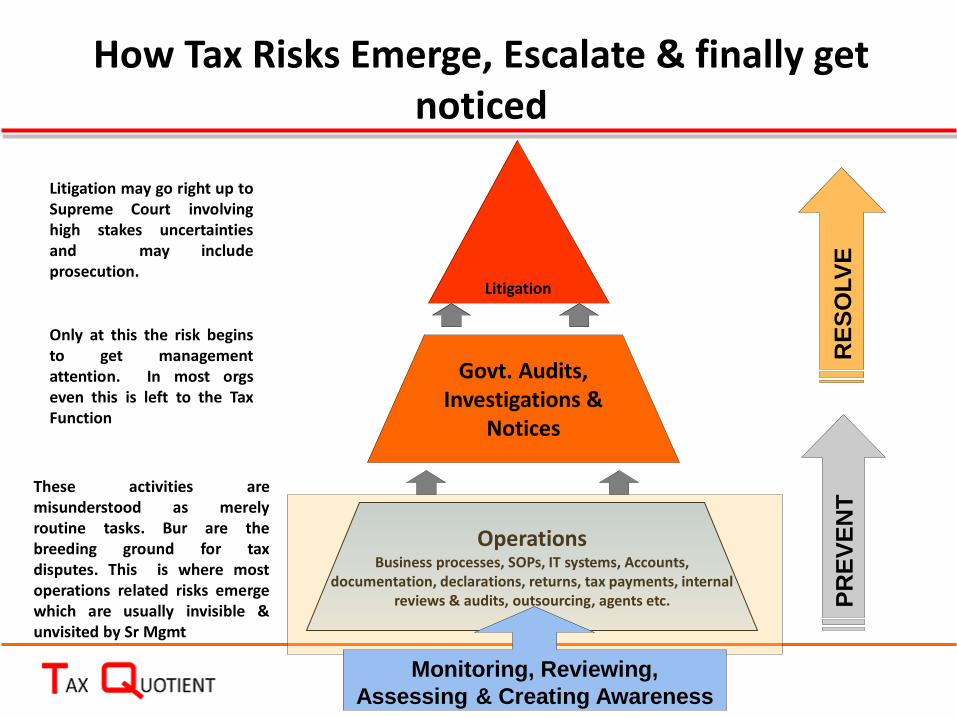

Litigation

Govt. Audits, Investigations &

Notices

These activities are misunderstood as merely routine tasks. Bur are the breeding ground for tax disputes. This is where most operations related risks emerge which are usually invisible & unvisited by Sr Mgmt

P

RE

VE

NT

RE

SO

LV

E

Only at this the risk begins to get management attention. In most orgs even this is left to the Tax Function

Litigation may go right up to Supreme Court involving high stakes uncertainties and may include prosecution.

How Tax Risks Emerge, Escalate & finally get noticed

Operations Business processes, SOPs, IT systems, Accounts,

documentation, declarations, returns, tax payments, internal reviews & audits, outsourcing, agents etc.

Monitoring, Reviewing,

Assessing & Creating Awareness

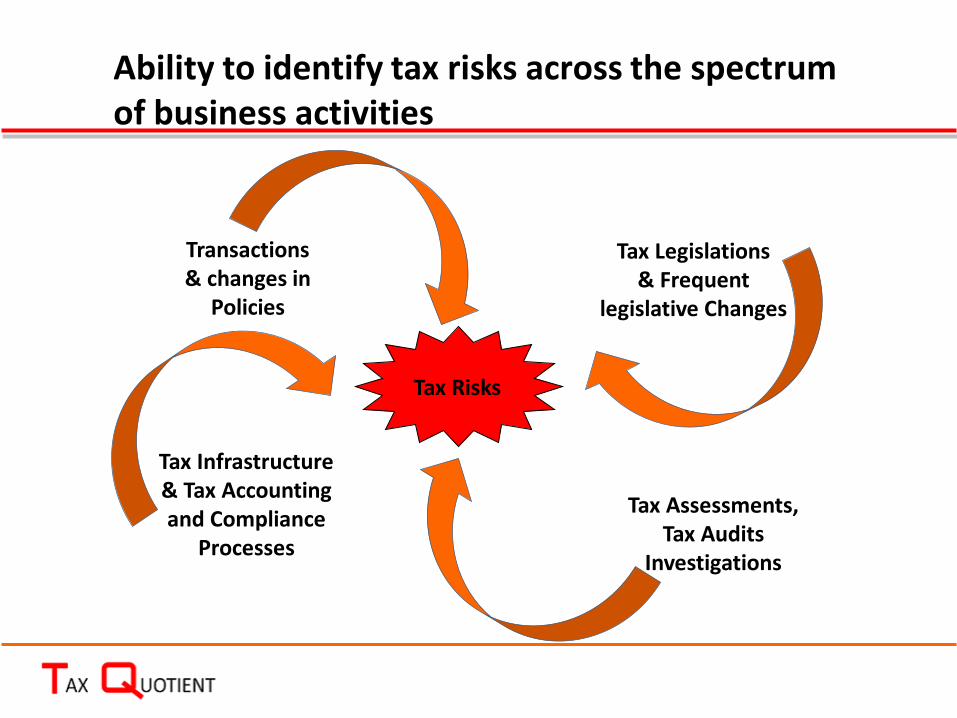

Tax Legislations & Frequent

legislative Changes

Transactions & changes in

Policies

Tax Infrastructure & Tax Accounting and Compliance

Processes

Tax Assessments, Tax Audits

Investigations

Tax Risks

Ability to identify tax risks across the spectrum of business activities

Tax Risk Management (TRM)

• TRM is NOT about becoming RISK AVERSE. Its about :

– Risk awareness. Its not about avoiding all risks nor about grabbing every tax

opportunity blindly.

– Its about creating a risk conscious infrastructure with continuous risk identification, assessment and mitigation

– Its about placing the right systems, processes & procedures in place to rein-in risks within acceptable levels

– Its about being proactive. Preventing not resolving risks after they emerge

– Opportunity to consciously calibrate risks to match with risk appetite of an enterprise.

– Avoiding all surprises! A known tax risk will never surprise!

• Not leaving it to chance! No surprises! Surprises are usually caused by “flawed” behaviour.

www.taxquotient.com

BLIPS – Context & Contributory factors for tax risks

• Behaviour – Risk appetite, attitude, conduct, focus, documentation and priorities

• Legislations – The operations an enterprise is engaged with determines the tax laws applicable

• Infrastructure for tax – Internal & External including CHA legal counsels, tax authorities and communication channels

• Policy – companies policies on risks, disclosures and risk mitigation

• Systems including IT systems for compliance

www.taxquotient.com

An ideal tax risk management system will work in tax

areas like the autonomous or involuntary nervous

system in a human body. A system which controls vital

life functions continuously, very silently without any

fuss.

The idea is to institutionalize it. Make it involuntary!

An Ideal Tax Risk Management

www.taxquotient.com

Types of Tax Risks

Transactional Risk

Operational Risk

Compliance Risk

Financial Risk

Reputational Risk

Litigation Risk

www.taxquotient.com

Types of Controls

Tax Control

Environment

Risk Assessment &

Mitigation

Standard Operating

Procedures

Financial Reports

Periodical monitoring

& Review

Review by Board &

Audit Committee

www.taxquotient.com

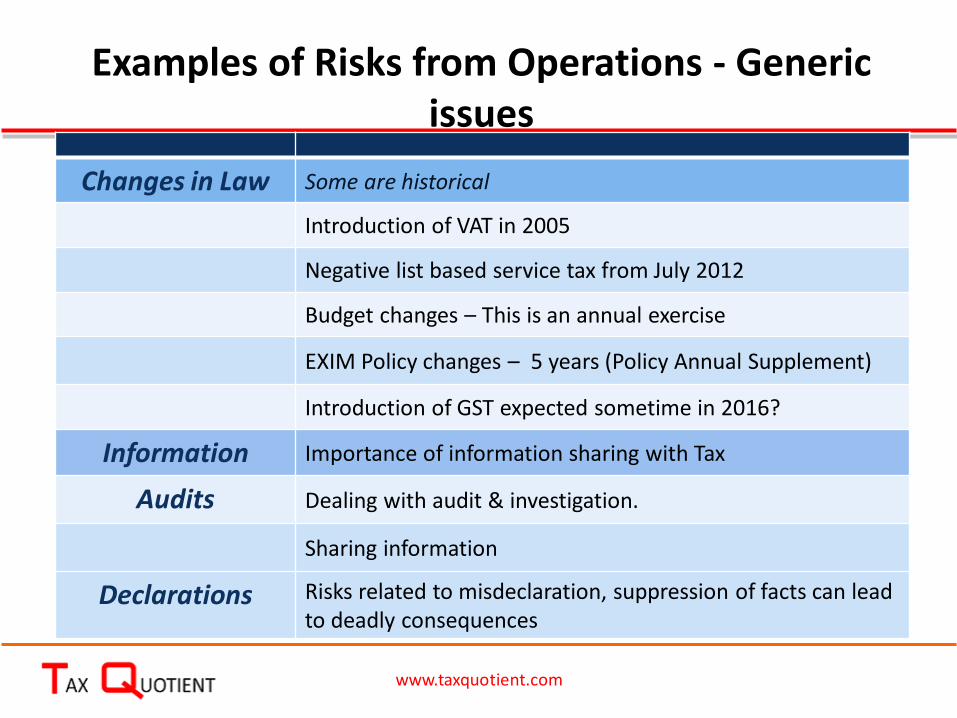

Changes in Law Some are historical

Introduction of VAT in 2005

Negative list based service tax from July 2012

Budget changes – This is an annual exercise

EXIM Policy changes – 5 years (Policy Annual Supplement)

Introduction of GST expected sometime in 2016?

Information Importance of information sharing with Tax

Audits Dealing with audit & investigation.

Sharing information

Declarations Risks related to misdeclaration, suppression of facts can lead to deadly consequences

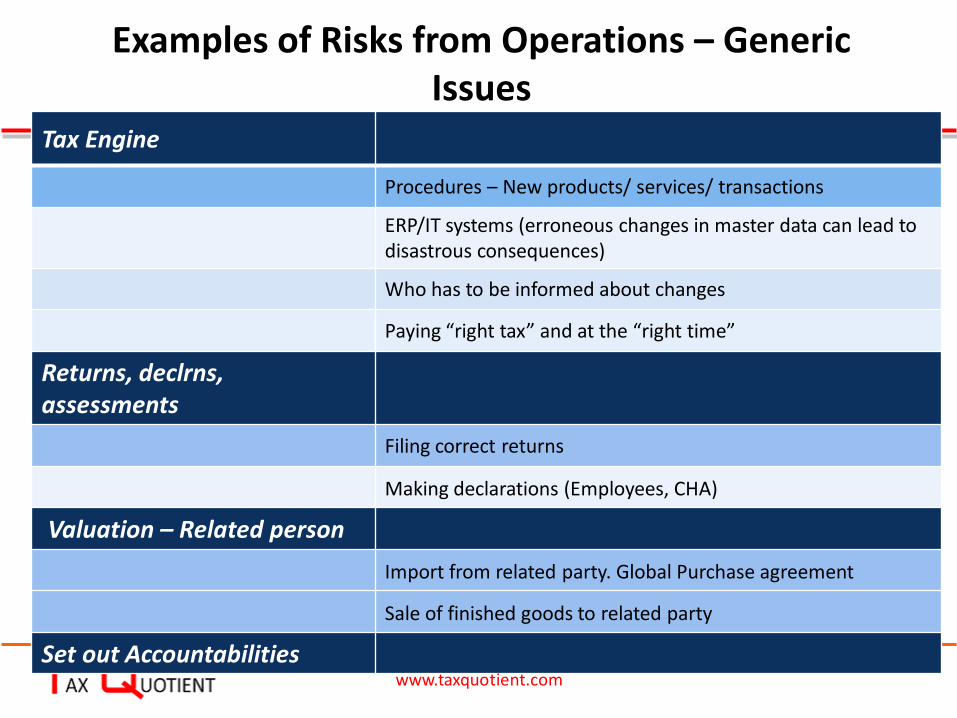

Examples of Risks from Operations - Generic issues

www.taxquotient.com

Tax Engine

Procedures – New products/ services/ transactions

ERP/IT systems (erroneous changes in master data can lead to disastrous consequences)

Who has to be informed about changes

Paying “right tax” and at the “right time”

Returns, declrns, assessments

Filing correct returns

Making declarations (Employees, CHA)

Valuation – Related person

Import from related party. Global Purchase agreement

Sale of finished goods to related party

Set out Accountabilities

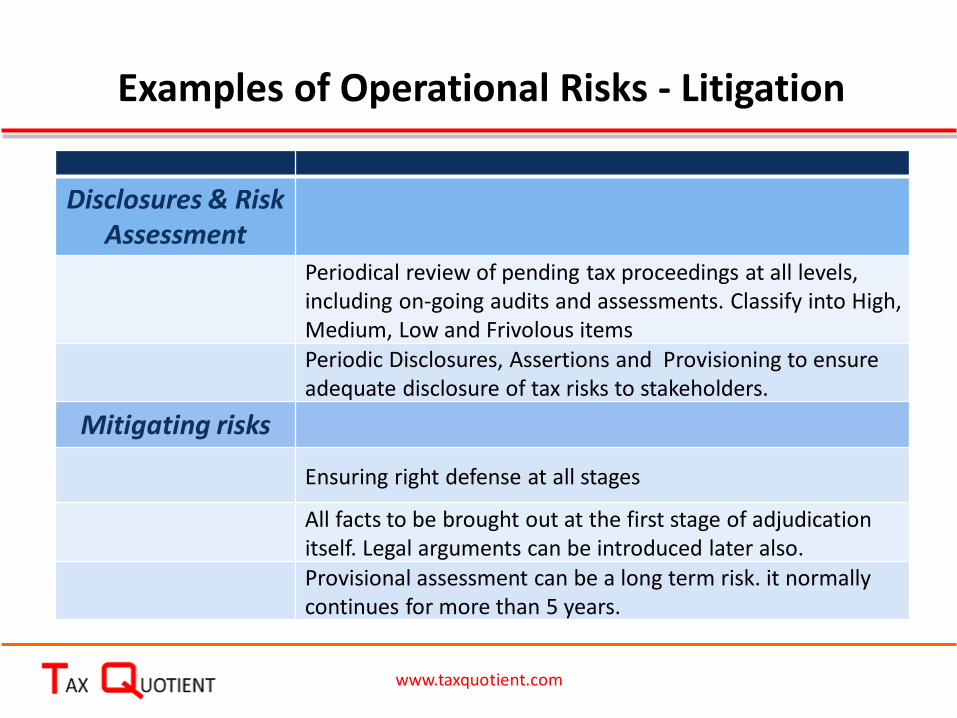

Examples of Risks from Operations – Generic Issues

www.taxquotient.com

Disclosures & Risk Assessment

Periodical review of pending tax proceedings at all levels, including on-going audits and assessments. Classify into High, Medium, Low and Frivolous items Periodic Disclosures, Assertions and Provisioning to ensure adequate disclosure of tax risks to stakeholders.

Mitigating risks

Ensuring right defense at all stages

All facts to be brought out at the first stage of adjudication itself. Legal arguments can be introduced later also. Provisional assessment can be a long term risk. it normally continues for more than 5 years.

Examples of Operational Risks - Litigation

www.taxquotient.com

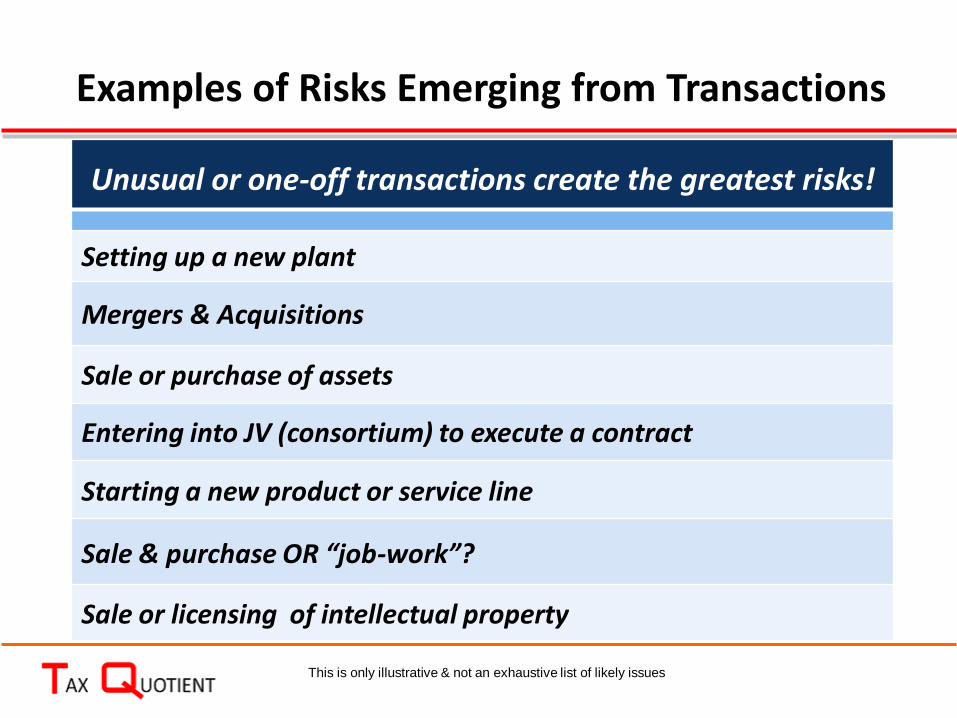

Unusual or one-off transactions create the greatest risks!

Setting up a new plant

Mergers & Acquisitions

Sale or purchase of assets

Entering into JV (consortium) to execute a contract

Starting a new product or service line

Sale & purchase OR “job-work”?

Sale or licensing of intellectual property

Examples of Risks Emerging from Transactions

This is only illustrative & not an exhaustive list of likely issues

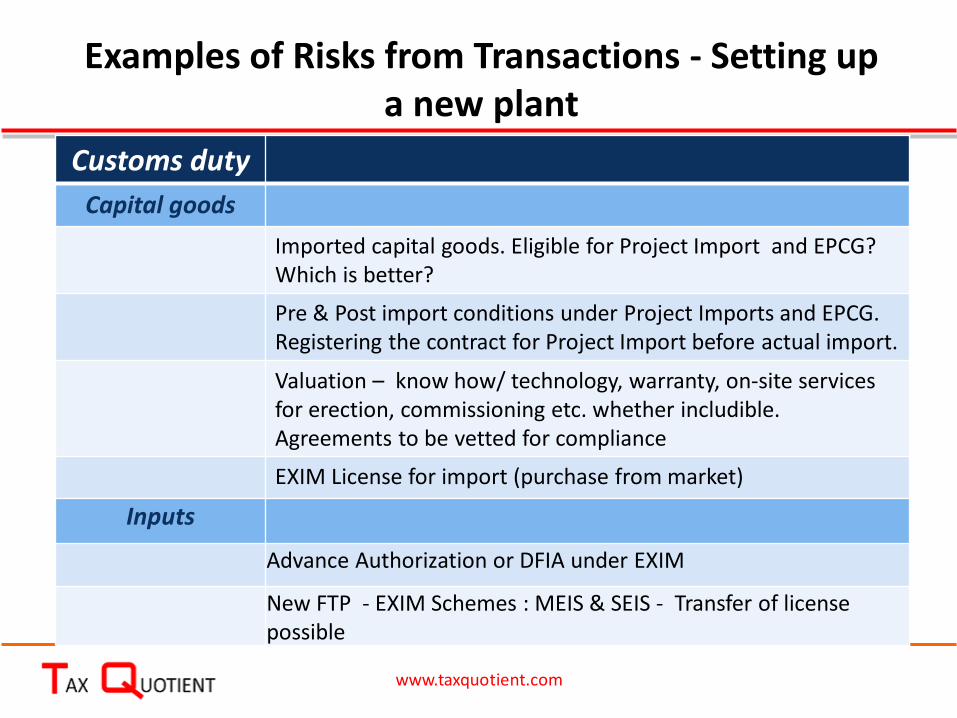

Customs duty

Capital goods

Imported capital goods. Eligible for Project Import and EPCG? Which is better?

Pre & Post import conditions under Project Imports and EPCG. Registering the contract for Project Import before actual import.

Valuation – know how/ technology, warranty, on-site services for erection, commissioning etc. whether includible. Agreements to be vetted for compliance

EXIM License for import (purchase from market)

Inputs

Advance Authorization or DFIA under EXIM

New FTP - EXIM Schemes : MEIS & SEIS - Transfer of license possible

Examples of Risks from Transactions - Setting up a new plant

www.taxquotient.com

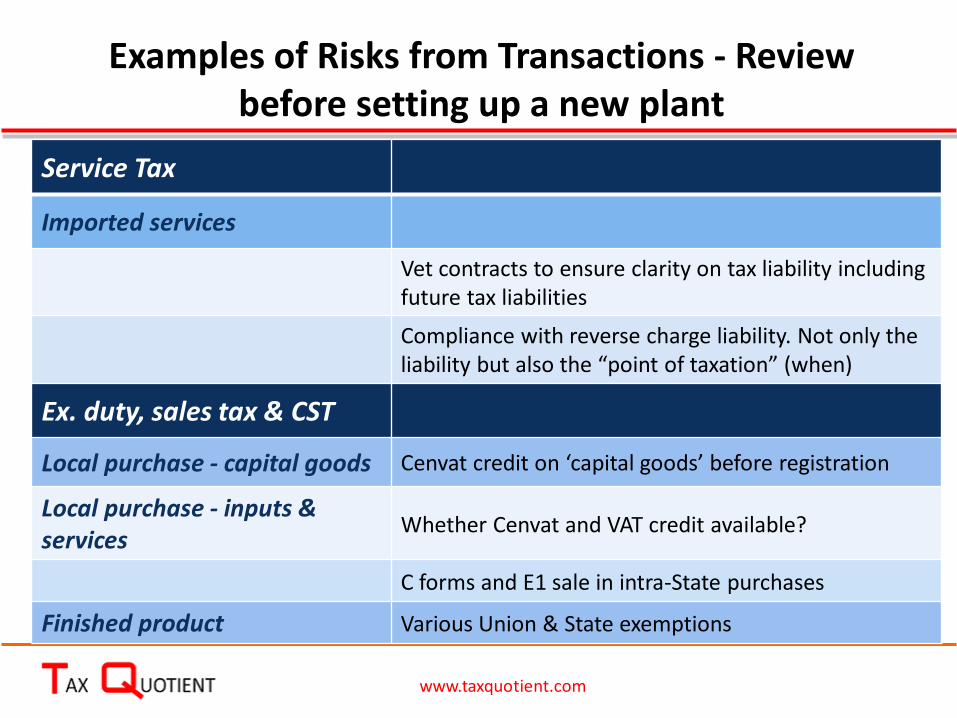

Service Tax

Imported services

Vet contracts to ensure clarity on tax liability including future tax liabilities

Compliance with reverse charge liability. Not only the liability but also the “point of taxation” (when)

Ex. duty, sales tax & CST

Local purchase - capital goods Cenvat credit on ‘capital goods’ before registration

Local purchase - inputs & services

Whether Cenvat and VAT credit available?

C forms and E1 sale in intra-State purchases

Finished product Various Union & State exemptions

Examples of Risks from Transactions - Review before setting up a new plant

www.taxquotient.com

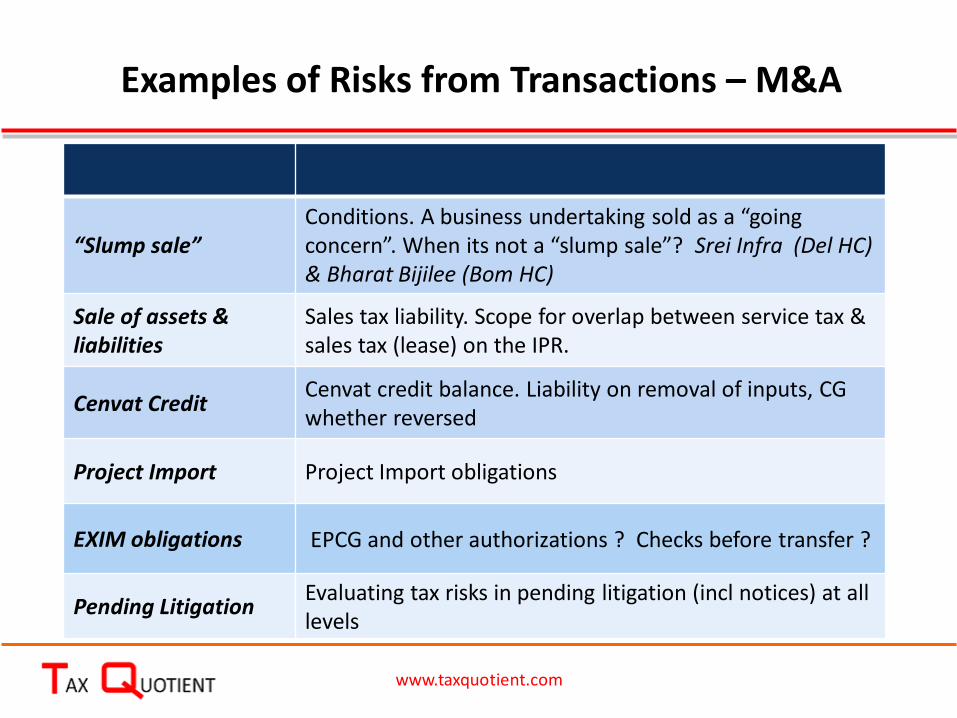

“Slump sale” Conditions. A business undertaking sold as a “going concern”. When its not a “slump sale”? Srei Infra (Del HC) & Bharat Bijilee (Bom HC)

Sale of assets & liabilities

Sales tax liability. Scope for overlap between service tax & sales tax (lease) on the IPR.

Cenvat Credit Cenvat credit balance. Liability on removal of inputs, CG whether reversed

Project Import Project Import obligations

EXIM obligations EPCG and other authorizations ? Checks before transfer ?

Pending Litigation Evaluating tax risks in pending litigation (incl notices) at all levels

Examples of Risks from Transactions – M&A

www.taxquotient.com

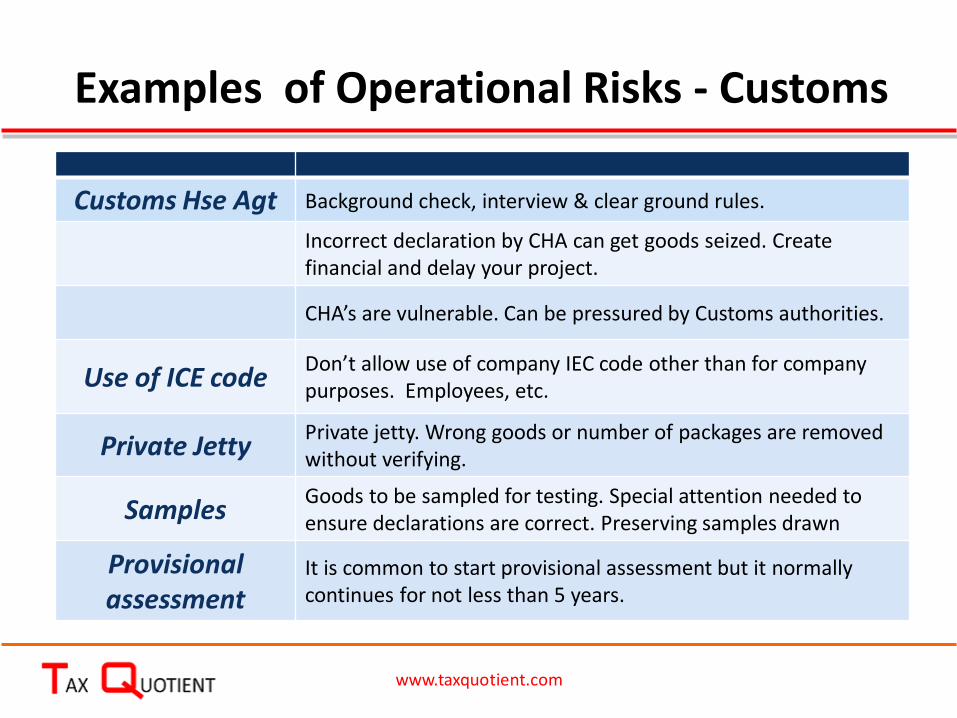

Customs Hse Agt Background check, interview & clear ground rules.

Incorrect declaration by CHA can get goods seized. Create financial and delay your project.

CHA’s are vulnerable. Can be pressured by Customs authorities.

Use of ICE code Don’t allow use of company IEC code other than for company purposes. Employees, etc.

Private Jetty Private jetty. Wrong goods or number of packages are removed without verifying.

Samples Goods to be sampled for testing. Special attention needed to ensure declarations are correct. Preserving samples drawn

Provisional assessment

It is common to start provisional assessment but it normally continues for not less than 5 years.

Examples of Operational Risks - Customs

www.taxquotient.com

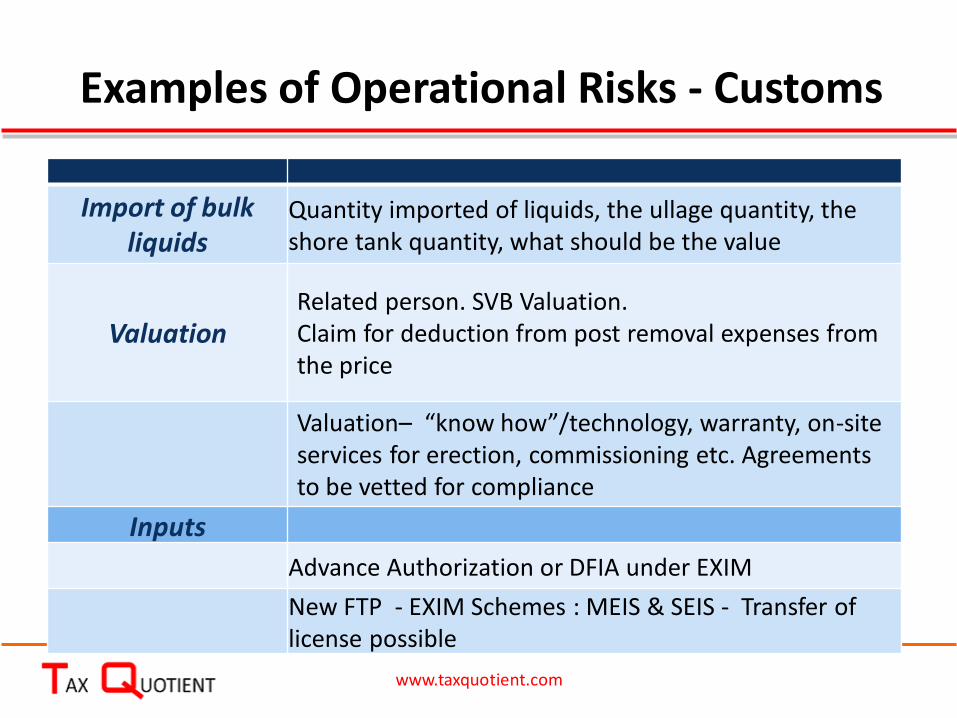

Import of bulk liquids

Quantity imported of liquids, the ullage quantity, the shore tank quantity, what should be the value

Valuation Related person. SVB Valuation. Claim for deduction from post removal expenses from the price

Valuation– “know how”/technology, warranty, on-site services for erection, commissioning etc. Agreements to be vetted for compliance

Inputs

Advance Authorization or DFIA under EXIM

New FTP - EXIM Schemes : MEIS & SEIS - Transfer of license possible

Examples of Operational Risks - Customs

www.taxquotient.com

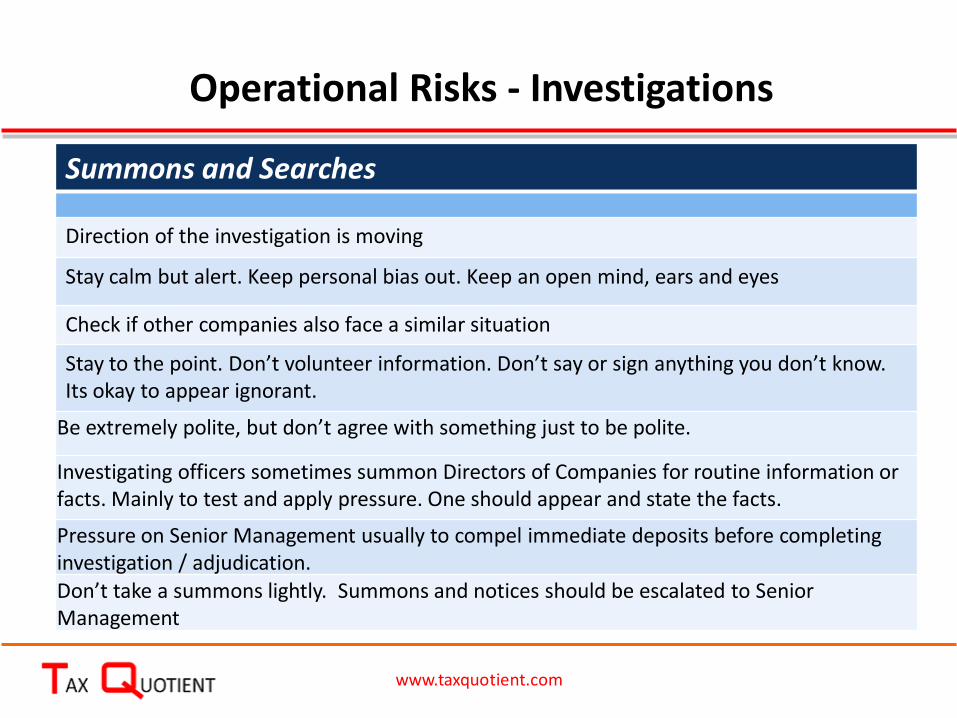

Summons and Searches

Direction of the investigation is moving

Stay calm but alert. Keep personal bias out. Keep an open mind, ears and eyes

Check if other companies also face a similar situation

Stay to the point. Don’t volunteer information. Don’t say or sign anything you don’t know. Its okay to appear ignorant.

Be extremely polite, but don’t agree with something just to be polite.

Investigating officers sometimes summon Directors of Companies for routine information or facts. Mainly to test and apply pressure. One should appear and state the facts.

Pressure on Senior Management usually to compel immediate deposits before completing investigation / adjudication. Don’t take a summons lightly. Summons and notices should be escalated to Senior Management

Operational Risks - Investigations

www.taxquotient.com

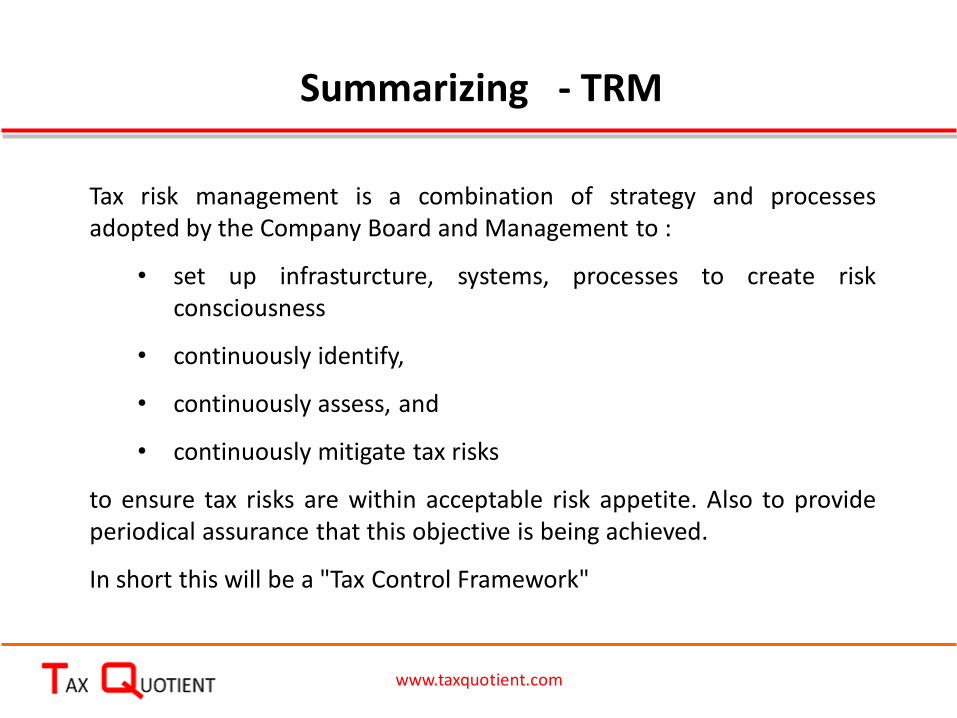

Tax risk management is a combination of strategy and processes adopted by the Company Board and Management to :

• set up infrasturcture, systems, processes to create risk consciousness

• continuously identify,

• continuously assess, and

• continuously mitigate tax risks

to ensure tax risks are within acceptable risk appetite. Also to provide periodical assurance that this objective is being achieved.

In short this will be a "Tax Control Framework"

www.taxquotient.com

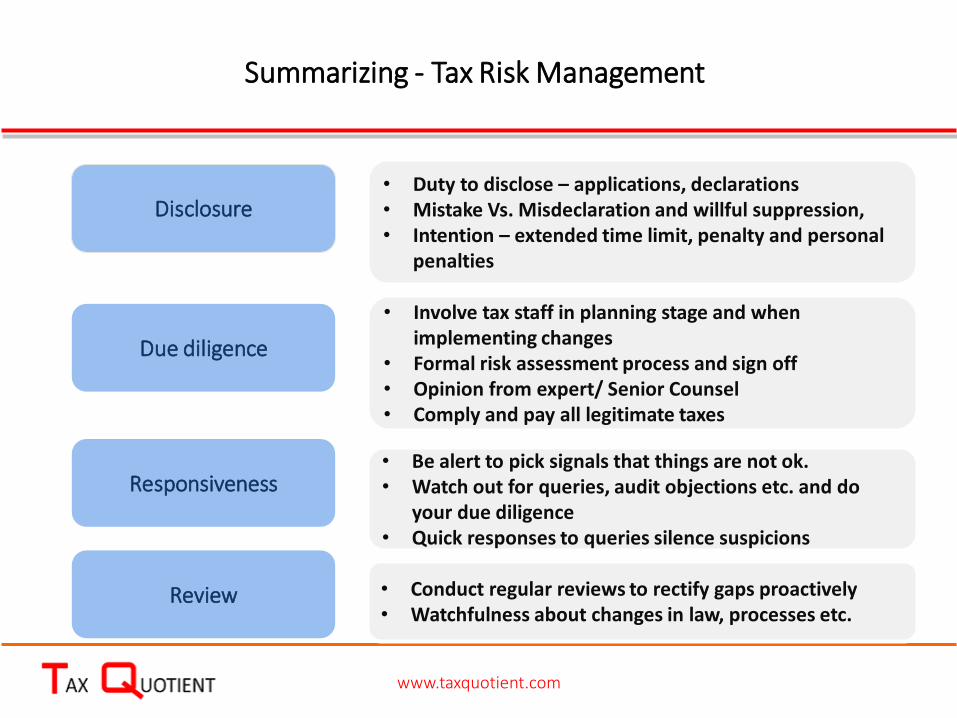

Summarizing - TRM

Disclosure • Duty to disclose – applications, declarations • Mistake Vs. Misdeclaration and willful suppression, • Intention – extended time limit, penalty and personal

penalties

Due diligence

• Involve tax staff in planning stage and when implementing changes

• Formal risk assessment process and sign off • Opinion from expert/ Senior Counsel • Comply and pay all legitimate taxes

Responsiveness • Be alert to pick signals that things are not ok. • Watch out for queries, audit objections etc. and do

your due diligence • Quick responses to queries silence suspicions

Summarizing - Tax Risk Management

Review • Conduct regular reviews to rectify gaps proactively • Watchfulness about changes in law, processes etc.

www.taxquotient.com

24

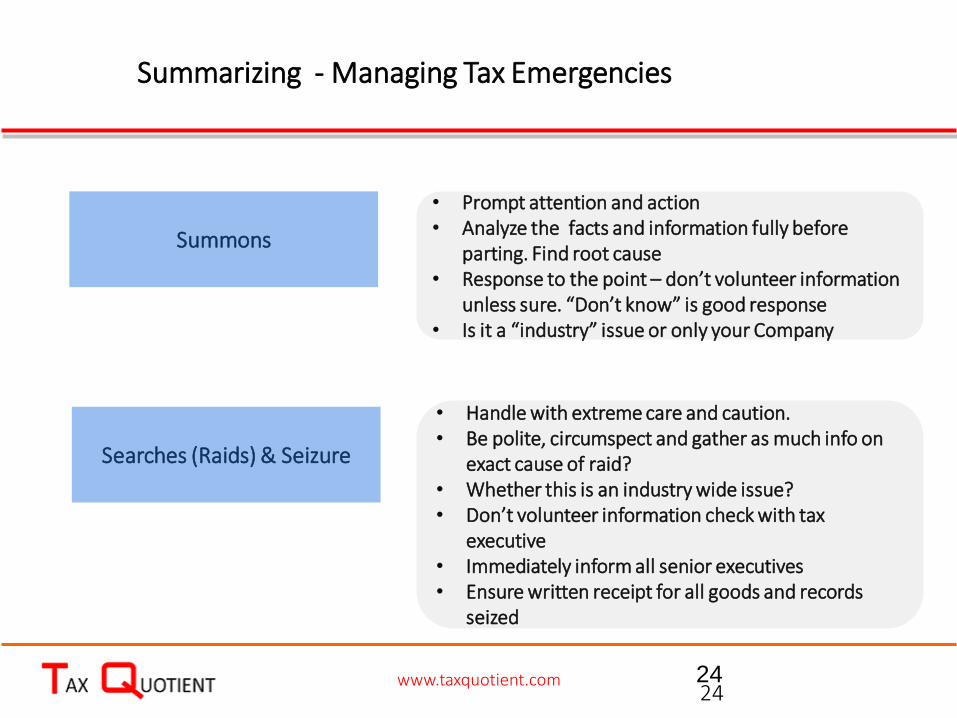

Searches (Raids) & Seizure

Summons

Summarizing - Managing Tax Emergencies

• Prompt attention and action • Analyze the facts and information fully before

parting. Find root cause • Response to the point – don’t volunteer information

unless sure. “Don’t know” is good response • Is it a “industry” issue or only your Company

• Handle with extreme care and caution. • Be polite, circumspect and gather as much info on

exact cause of raid? • Whether this is an industry wide issue? • Don’t volunteer information check with tax

executive • Immediately inform all senior executives • Ensure written receipt for all goods and records

seized

24 www.taxquotient.com