Embed Size (px)

Citation preview

Scientific Research and Experimental Development Tax Incentive Program

(SR&ED)

BUS 750 - INNOVATION TOOL-KIT

Canada has a rich history of innovation!

JUST THE TIP OF OUR ICEBERG!

AGENDA

● SR&ED program overview

● Who’s eligible

● What’s eligible & what’s not

● Example claim

● Tips to maximizing your returns

● Benefits & Limitations

SOME NEW TERMS

● SR&ED = Scientific Research & Experimental Development

● CCPC = Canadian-Controlled Private Corporation

● ITC = Investment Tax Credit

SR&ED = Incentivizing Risk!

FREE MONEY!!!

What is SR&ED?

● Economic incentive for investment in R&D and innovation in Canada

● Promotes corporate R&D as opposed to institutional R&D

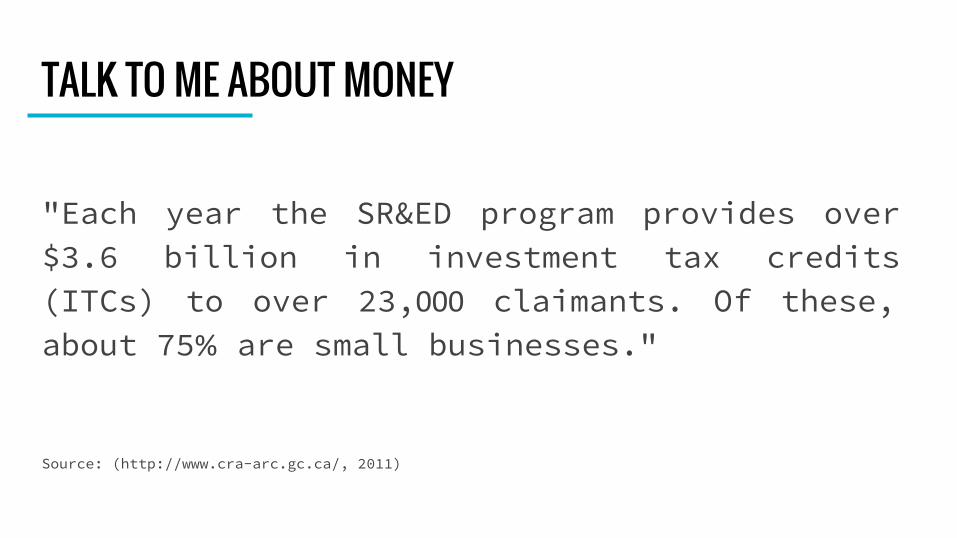

"Each year the SR&ED program provides over $3.6 billion in investment tax credits (ITCs) to over 23, claimants. Of these, about 75 are small businesses."

Source: (http://www.cra-arc.gc.ca/, 2011)

TALK TO ME ABOUT MONEY

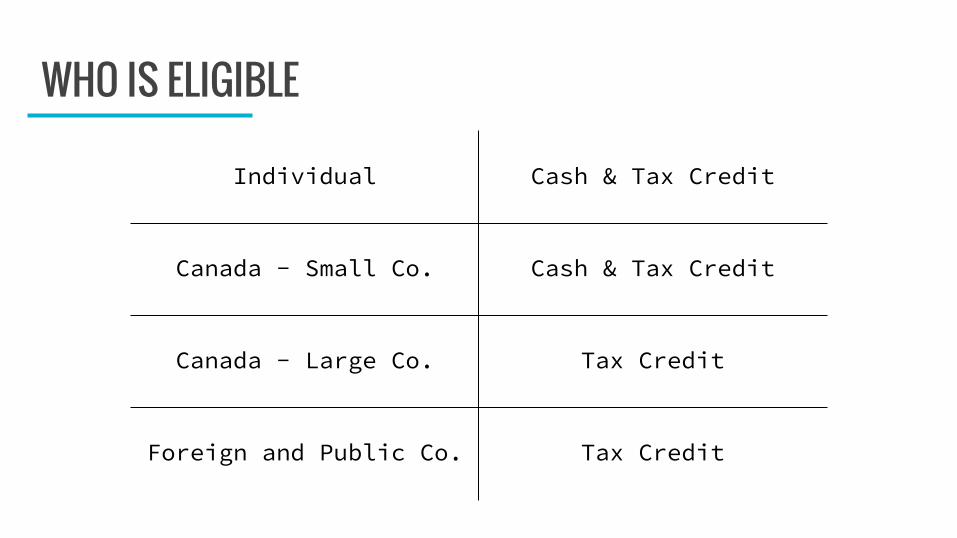

WHO IS ELIGIBLE

Individual Cash & Tax Credit

Canada - Small Co. Cash & Tax Credit

Canada - Large Co. Tax Credit

Foreign and Public Co. Tax Credit

what’s in what’s out?

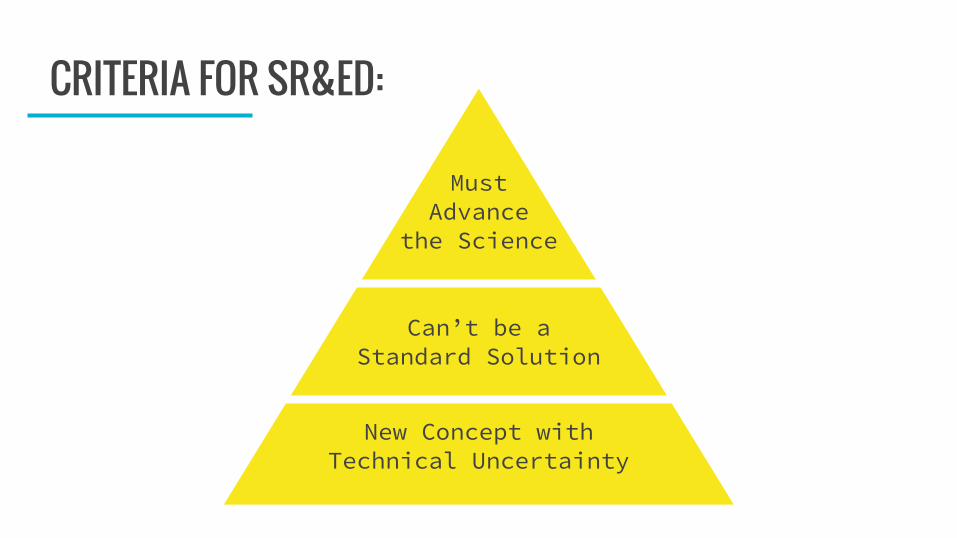

CRITERIA FOR SR&ED:

New Concept with Technical Uncertainty

Can’t be a Standard Solution

MustAdvance

the Science

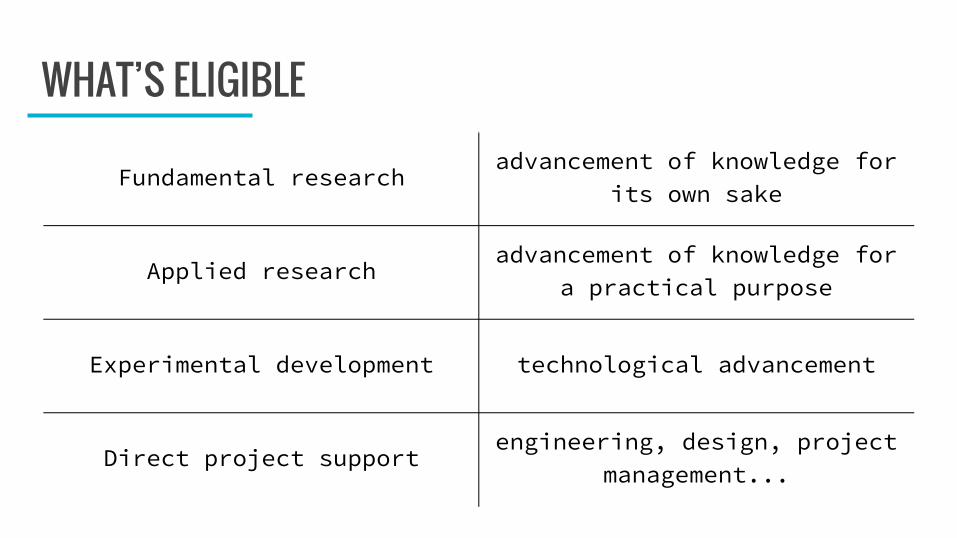

WHAT’S ELIGIBLE

Fundamental researchadvancement of knowledge for

its own sake

Applied researchadvancement of knowledge for

a practical purpose

Experimental development technological advancement

Direct project support engineering, design, project

management...

WHAT’S NOT ELIGIBLE

● Capital Equipment

● Travel & related expenses

● Intellectual property related expenses

● Legal and Accounting fees

● Real Estate

● Marketing/Sales

● Any work beyond Prototyping phase

HOW DOES IT BREAK DOWN

● Wages and Salaries

● Overhead

● Purchased Material

● Contracted Research

● Research Done Abroad ○ only if directly related and

vital to project

HOW YOU CLAIM YOUR MONEY

● Write 2 reports○ Justification of claim○ Description of claim

○ Financial details for audit

● Submit within 18 months of year-end (<6 months to fast-track)

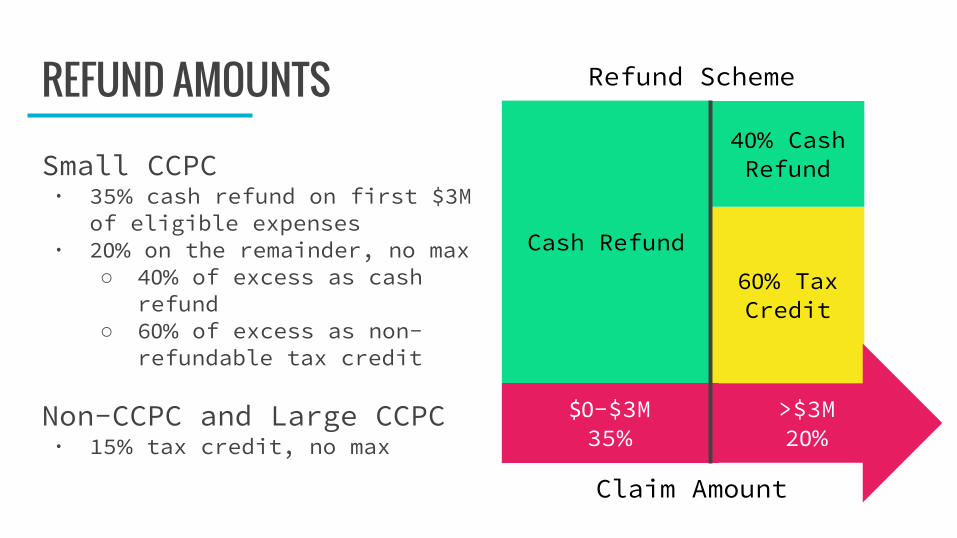

the bottom line

Small CCPC∙ 35 cash refund on first $3M

of eligible expenses∙ 2 on the remainder, no max

○ 4 of excess as cash refund

○ 6 of excess as non-refundable tax credit

Non-CCPC and Large CCPC∙ 15 tax credit, no max

REFUND AMOUNTS

Cash Refund6 Tax Credit

4 Cash Refund

-$3M35

>$3M2

Claim Amount

Refund Scheme

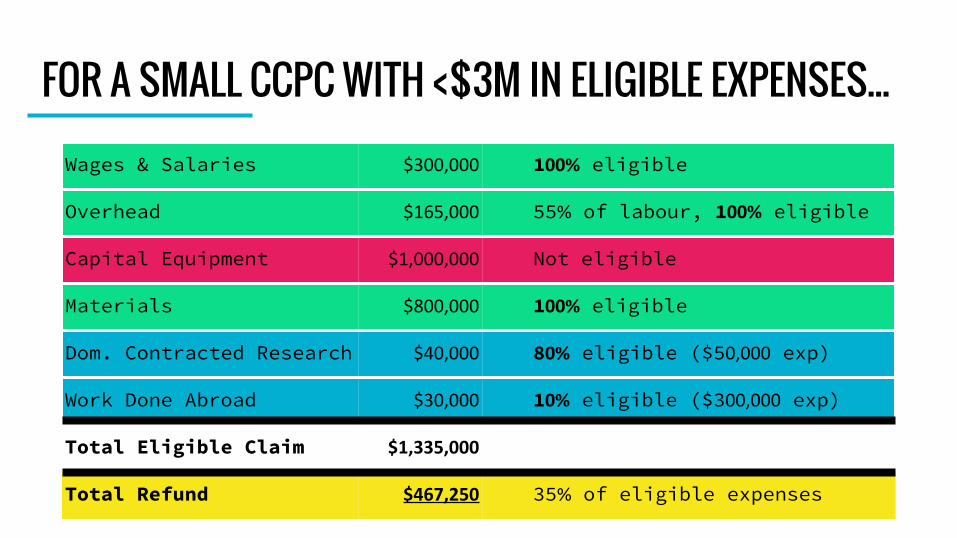

FOR A SMALL CCPC WITH <$3M IN ELIGIBLE EXPENSES...Wages & Salaries 1 eligible

Overhead 55 of labour, 1 eligible

Capital Equipment Not eligible

Materials 1 eligible

Dom. Contracted Research 8 eligible ($5 exp)

Work Done Abroad 1 eligible ($3 exp)

Total Eligible Claim

Total Refund 35 of eligible expenses

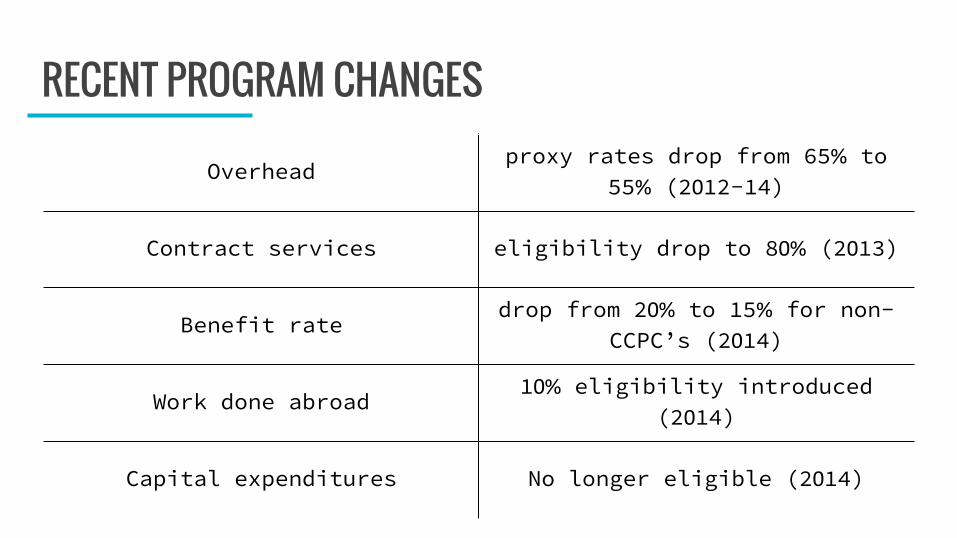

RECENT PROGRAM CHANGES

Overheadproxy rates drop from 65 to

55 (2 12-14)

Contract services eligibility drop to 8 (2 13)

Benefit ratedrop from 2 to 15 for non-

CCPC’s (2 14)

Work done abroad 1 eligibility introduced

(2 14)

Capital expenditures No longer eligible (2 14)

OK, where do I start?

COMMON PITFALLS

● Transition points are key○ i.e. From Prototype to Production

● In-house vs. Contracted Dev.○ Domestic vs. foreign contractors

○ Balance the salary & recruitment

cost of hiring specialists vs.

losses of claimable amount of overhead (OH as of wages)

COMMON PITFALLS (cont.)

● Total-cost of implementation○ Tracking and Reporting○ Training & incentives○ Project administration

○ Report writing & consultant fees

● Document, Document, Document○ Technical work○ Financial costs○ Daily tracking is recommended

● Individuals should incorporate○ Cap increased from 15 to 35

● Keep R&D in-house○ Claim overhead

○ Reduced to 8 (Canada) or 1 (Foreign)

● Pay a pro○ Fixed fee vs. variable

TIPS TO GET MORE $$$

TIPS TO GET MORE $$$ (cont.)

● Proxy vs. traditional overhead calculation○ 55 of all wages/salaries

○ Kill overhead - work from mom’s basement

● Leverage available CRA support○ Self assessment tool○ Account Executive Services○ Free first time review○ Pre-claim Project Review Services

● Capture○ Process for recording time○ Train employees○ Employee buy-in (KPI/bonus)

● Future○ Credits valid for up to 20 years

TIPS TO GET MORE $$$ (cont.)

Bringing it all together

SUMMARY -- BENEFITS -- COMPANY

● Funding - but DON’T give up equity!

● Able to bring new products to market quicker

● Shorter ROI cycles● Encouraged to grow companies and employee bases

SUMMARY -- BENEFITS -- COMMUNITY

● Keeping well paid jobs in Canada● Plugs holes to slow “brain drain”

● Supports a culture of experimentation and risk-taking

● Fostering communities of innovation (inventors, innovators & investors)

SUMMARY -- LIMITATIONS

● High cost to administer & report● May not incentivize the “right” type of innovation (i.e. ICT)

● Allocates resources away from direct funding & institutional innovation investments

● High burden to taxpayers

Is the SR&ED program good for Canadians?

4 billion times, YES!SR&ED enables Canadians to be bold, curious and courageous enough to research, innovate and grow businesses locally!

REFERENCESHearn, D. R. (2013). Introduction to R&D Tax Credits in Canada. Retrieved from http:

//www.scitax.com/:

http://www.scitax.com/pdf/Introduction.to.R&D.Tax.Credits.in.Canada.SCITAX.pdf

http://www.cra-arc.gc.ca/. (2009, 07). Overview of the Scientific Research and

Experimental

Development (SR&ED) Tax Incentive Program. Retrieved from http://www.cra-arc.gc.ca/:

http://www.cra-arc.gc.ca/E/pub/tg/rc4472/rc4472-e.html

Madore, O. (1998, August). SCIENTIFIC RESEARCH AND EXPERIMENTAL DEVELOPMENT: TAX

POLICY.

Retrieved from http://publications.gc.ca/: http://publications.gc.ca/Collection-

R/LoPBdP/CIR/899-e.htm

Wikipedia. (n.d.). Scientific Research and Experimental Development Tax Credit

Program. Retrieved from https://en.wikipedia.

org/wiki/Scientific_Research_and_Experimental_Development_Tax_Credit_Program

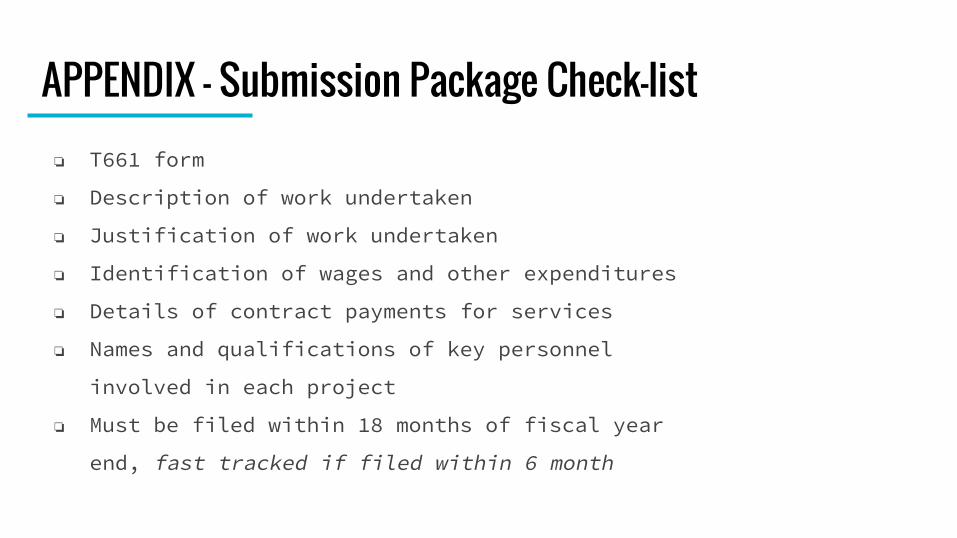

APPENDIX - Submission Package Check-list❏ T661 form

❏ Description of work undertaken

❏ Justification of work undertaken

❏ Identification of wages and other expenditures

❏ Details of contract payments for services

❏ Names and qualifications of key personnel

involved in each project

❏ Must be filed within 18 months of fiscal year

end, fast tracked if filed within 6 month

![Kimball & Ross - The Data Warehouse Toolkit 2nd Ed [Wiley 2002].pdf](https://img.pdfslide.us/doc/110x75/613cb86da3339922f86eeadf/kimball-amp-ross-the-data-warehouse-toolkit-2nd-ed-wiley-2002pdf.jpg)