Embed Size (px)

Citation preview

Saving people moneySarah Tavel

Saving people money has been the driving force behind many of the biggest consumer wins of the internet era.

Observation

For example…

Managing what you have

Getting more for less

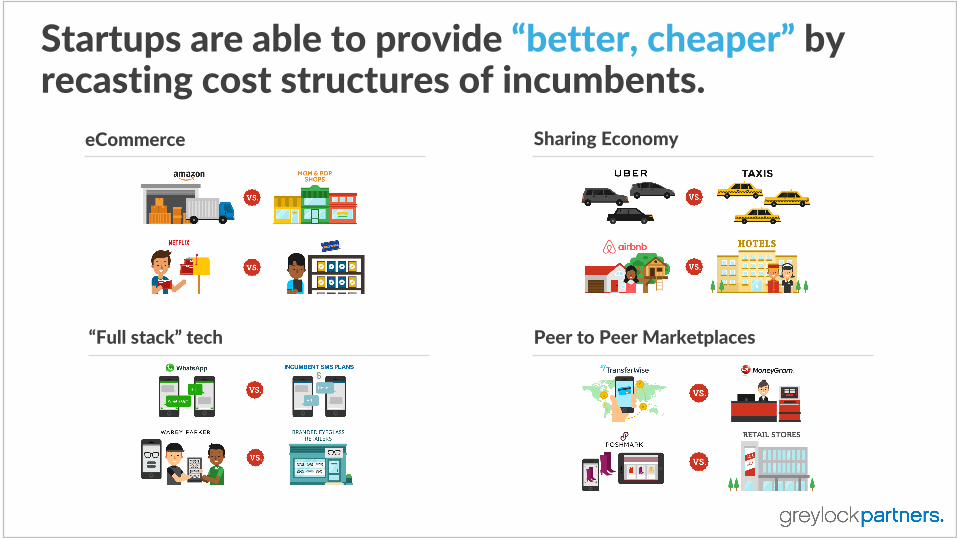

Startups are able to provide “better, cheaper” by recasting cost structures of incumbents.

eCommerce

“Full stack” tech

Sharing Economy

Peer to Peer Marketplaces

Why does saving money lead to such massive companies?

It’s the painkiller of the mass market.

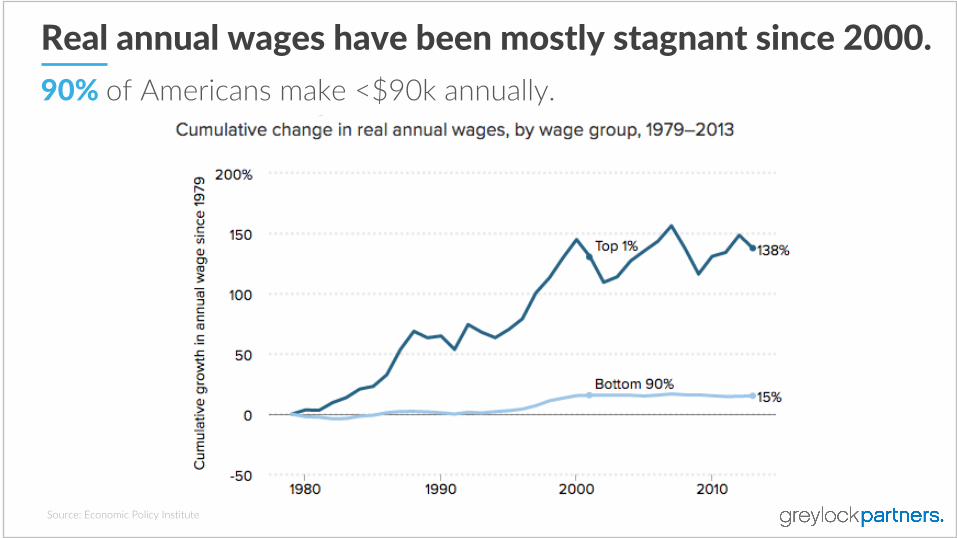

Real annual wages have been mostly stagnant since 2000.90% of Americans make <$90k annually.

Source: Economic Policy Institute

Millennials are now facing a new set of pains in need of a painkiller.

What we usually talk about with Millennials:

Largest generation: Born between ~1981-‐2004

• Digital natives -‐ trust and expect more from tech

• Generation of “early adopters”

• Check their phone 45x a day -‐more than they engage with people

• Spend 30hrs+/month on social media

Source: SDL, Millennial Disruption Index

Here’s another dimension…

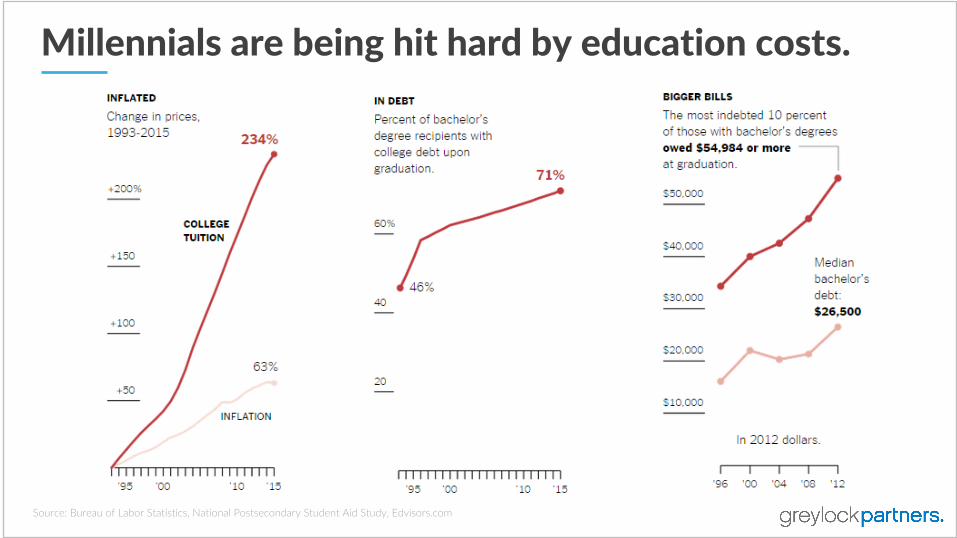

Millennials are being hit hard by education costs.

Source: Bureau of Labor Statistics, National Postsecondary Student Aid Study, Edvisors.com

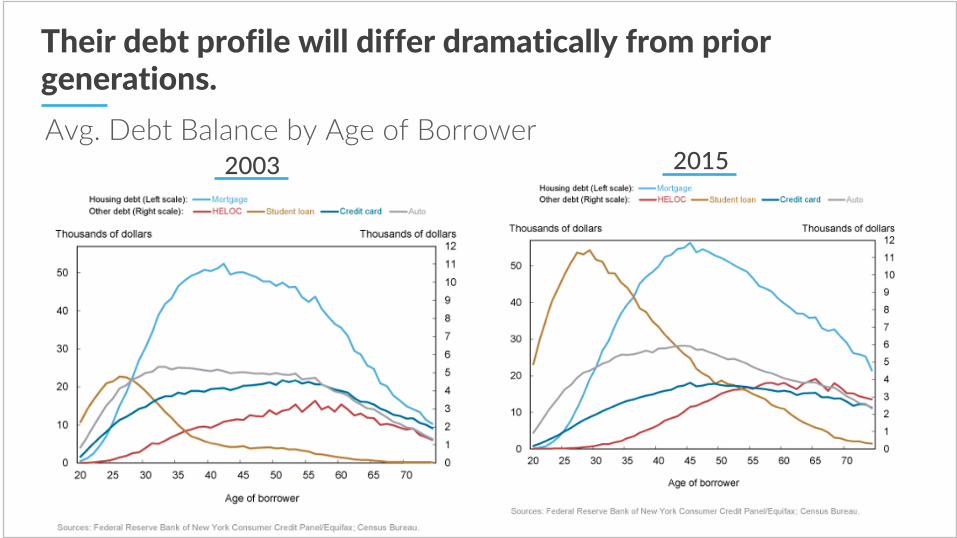

Their debt profile will differ dramatically from prior generations.

2003 2015Avg. Debt Balance by Age of Borrower

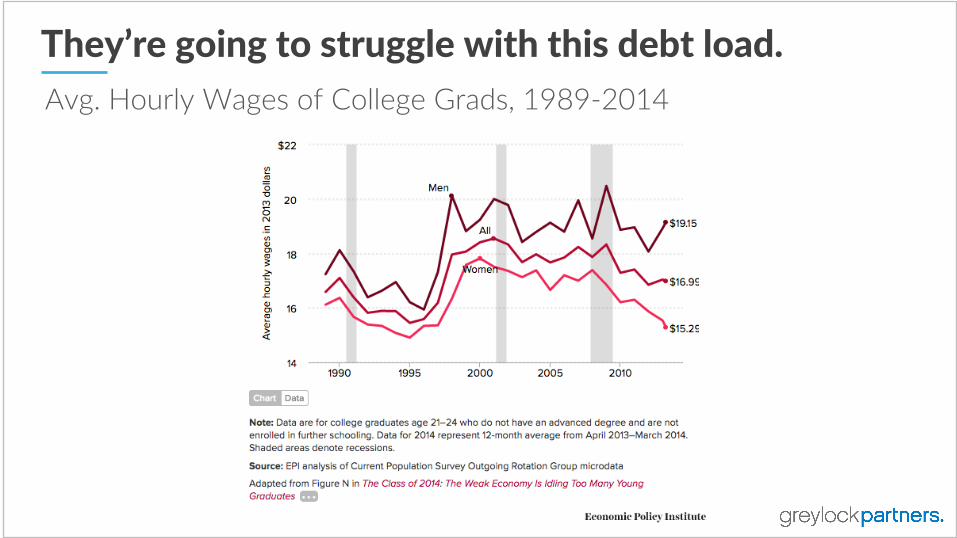

They’re going to struggle with this debt load.Avg. Hourly Wages of College Grads, 1989-‐2014

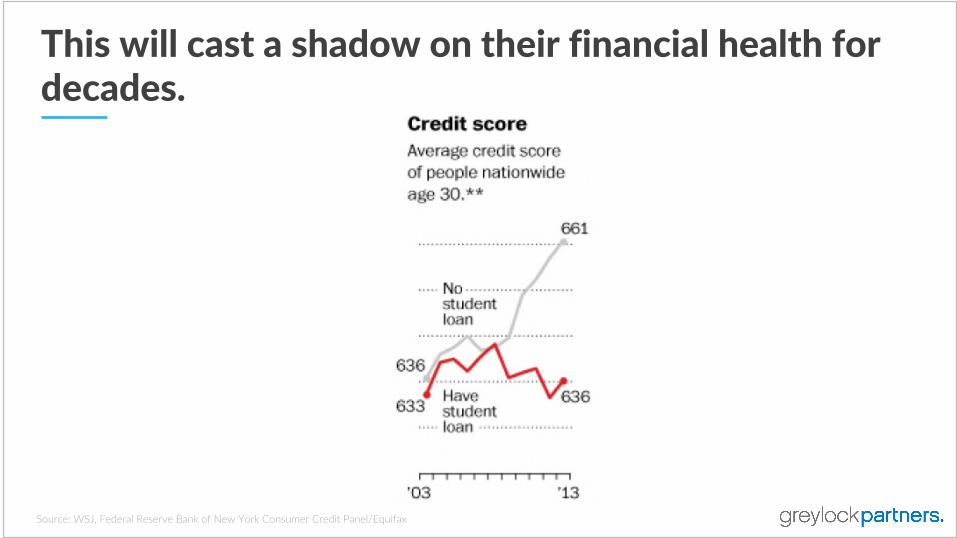

This will cast a shadow on their financial health for decades.

Source: WSJ, Federal Reserve Bank of New York Consumer Credit Panel/Equifax

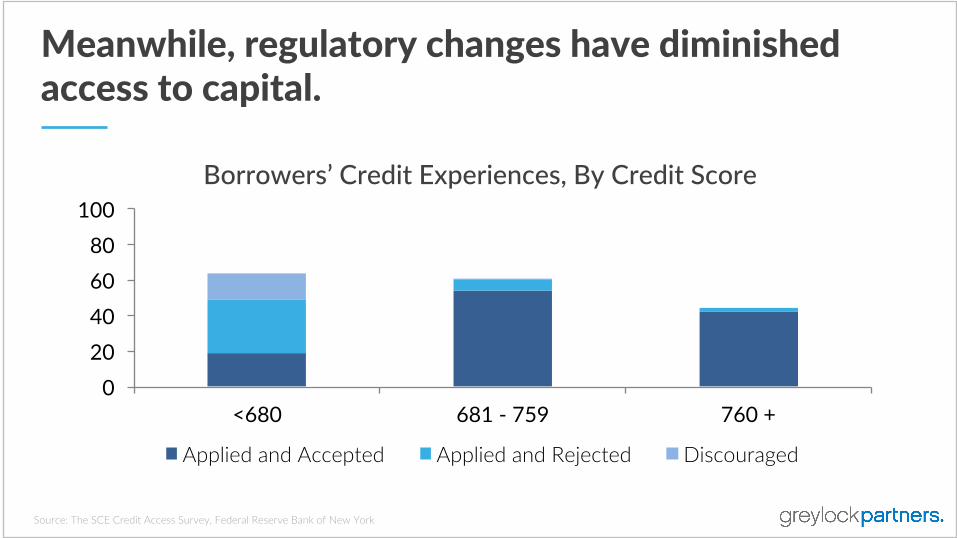

Meanwhile, regulatory changes have diminished access to capital.

Source: The SCE Credit Access Survey, Federal Reserve Bank of New York

020406080

100

<680 681 -‐ 759 760 +

Applied and Accepted Applied and Rejected Discouraged

Borrowers’ Credit Experiences, By Credit Score

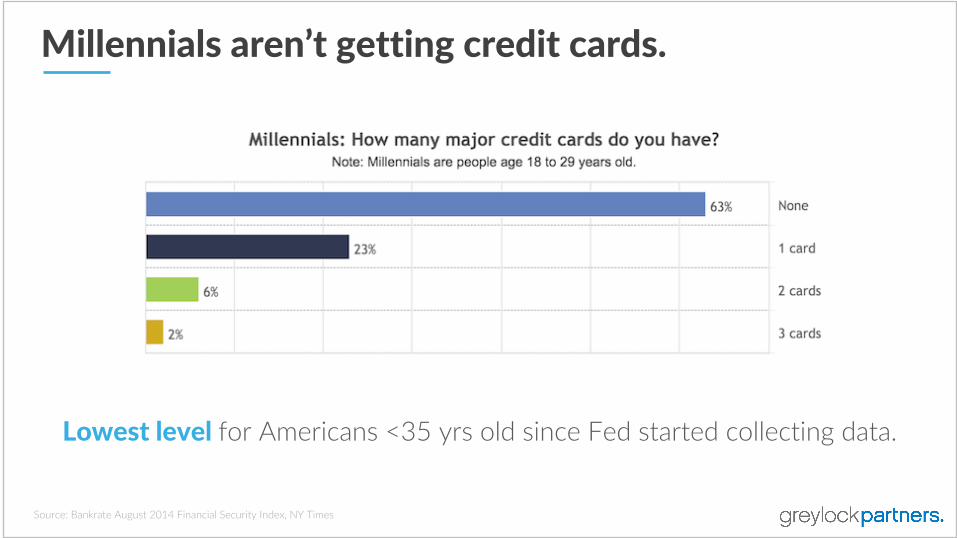

Millennials aren’t getting credit cards.

Source: Bankrate August 2014 Financial Security Index, NY Times

Lowest level for Americans <35 yrs old since Fed started collecting data.

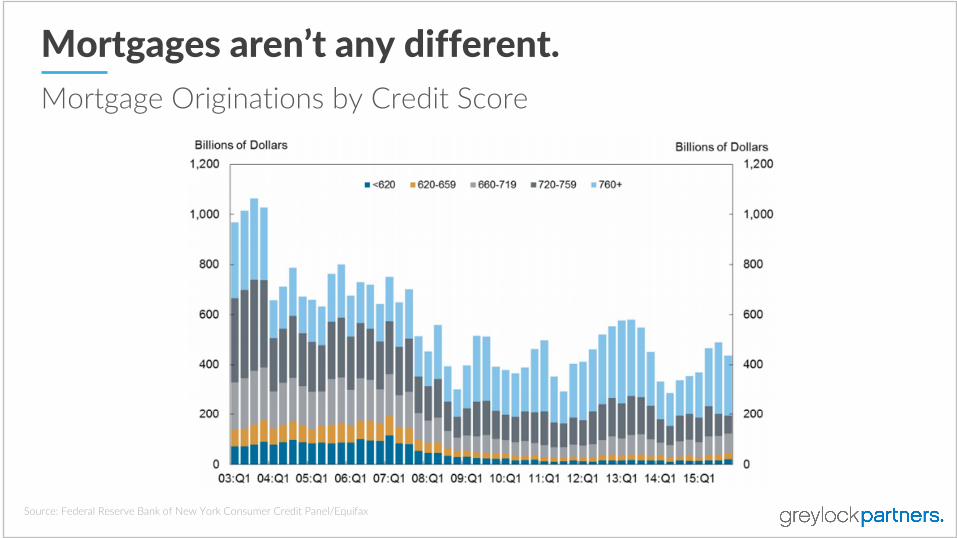

Mortgages aren’t any different.Mortgage Originations by Credit Score

Source: Federal Reserve Bank of New York Consumer Credit Panel/Equifax

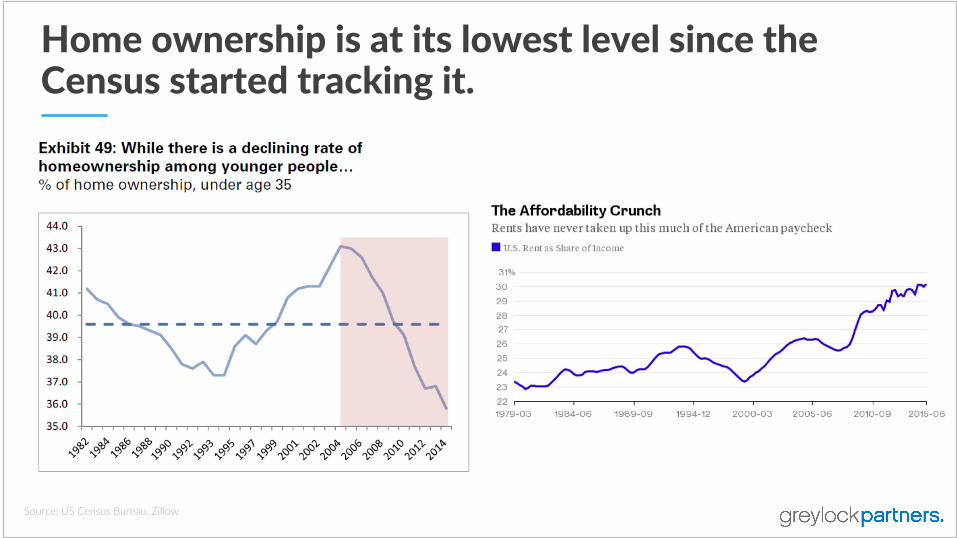

Home ownership is at its lowest level since the Census started tracking it.

Source: US Census Bureau, Zillow

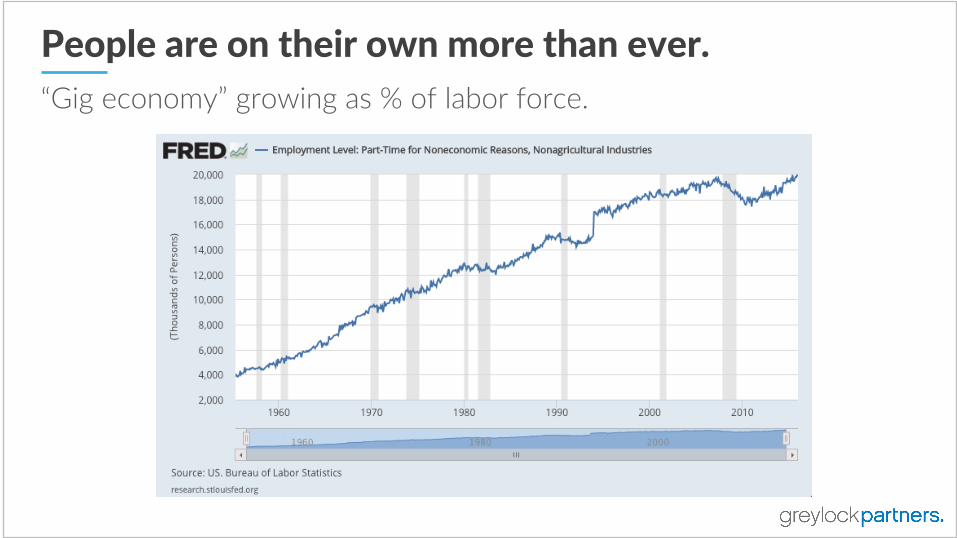

People are on their own more than ever.“Gig economy” growing as % of labor force.

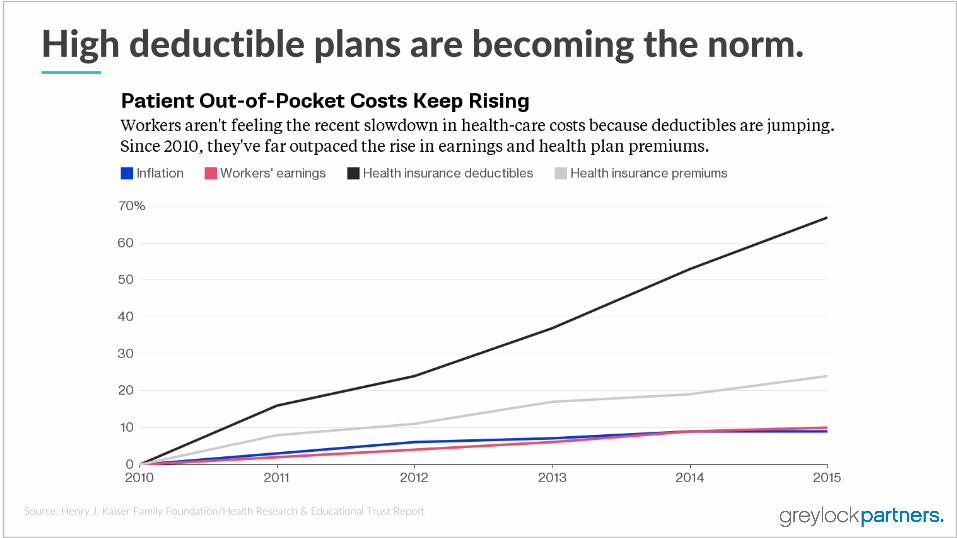

High deductible plans are becoming the norm.

Source: Henry J. Kaiser Family Foundation/Health Research & Educational Trust Report

Taken together, you have a generation juggling a new financial reality.

• Entering adulthood with a complex personal financial picture.

• Expenses going up (loan servicing, rent, health) while income is stagnant.

• Reduced access to and adoption of traditional forms of credit (credit card, mortgage)

Americans, particularly Millennials, need new ways to save money.

Getting more for less

Managing your financial health

Medical?Housing?Education?

Financial Advice?Access to credit?Resilience?

It’s time. Fintech is ripe for disruption:

Recent startup wins (Square, LendingClub, SoFi, Stripe) creating generation of founders who understand how to navigate the space.

Regulatory changes as result of Financial Crisis restricting ability of incumbents to innovate.

Classic consumer internet opportunities (“the next great photo app!”) have largely dried up, so talented consumer-‐oriented founders looking elsewhere.

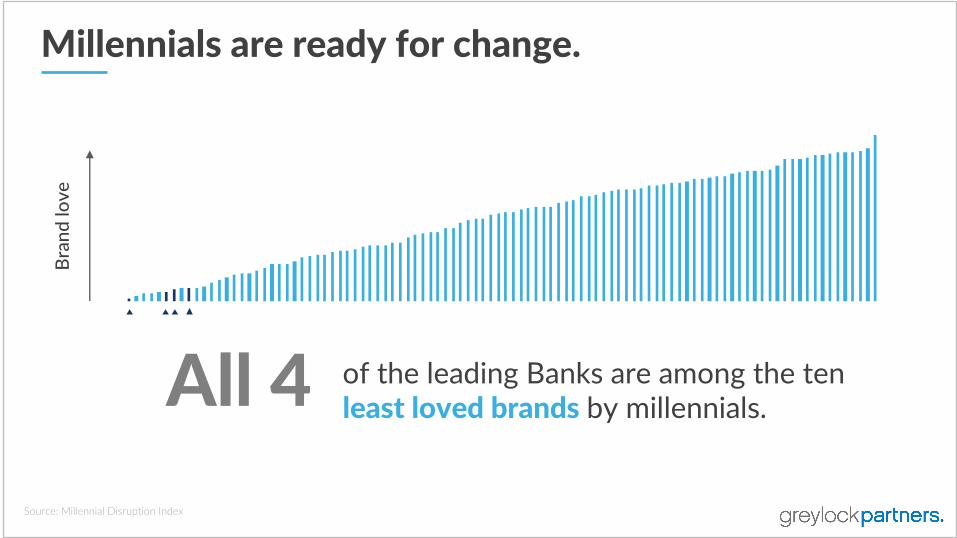

Millennials are ready for change.Brand love

of the leading Banks are among the ten least loved brands by millennials.All 4

Source: Millennial Disruption Index

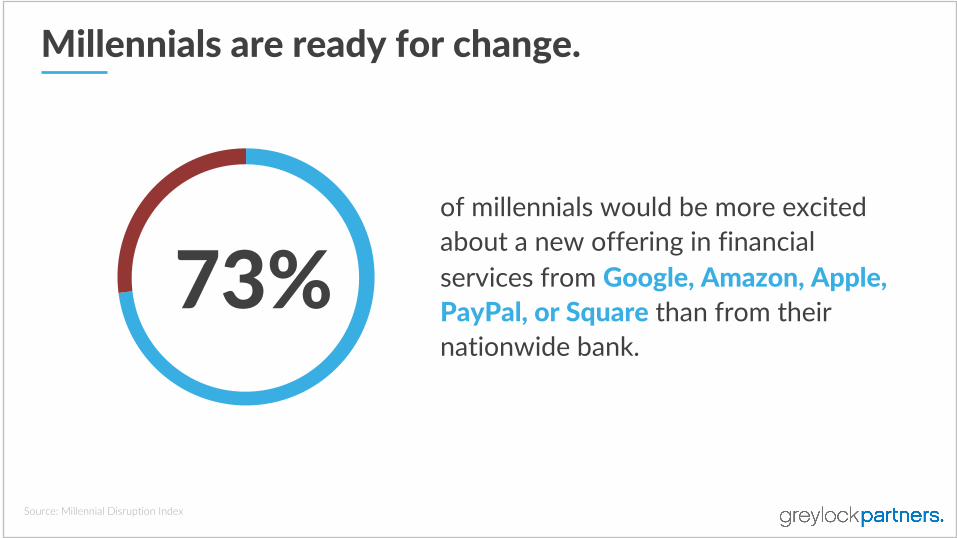

Millennials are ready for change.

73% of millennials would be more excited about a new offering in financial services from Google, Amazon, Apple, PayPal, or Square than from their nationwide bank.

Source: Millennial Disruption Index

Opportunities

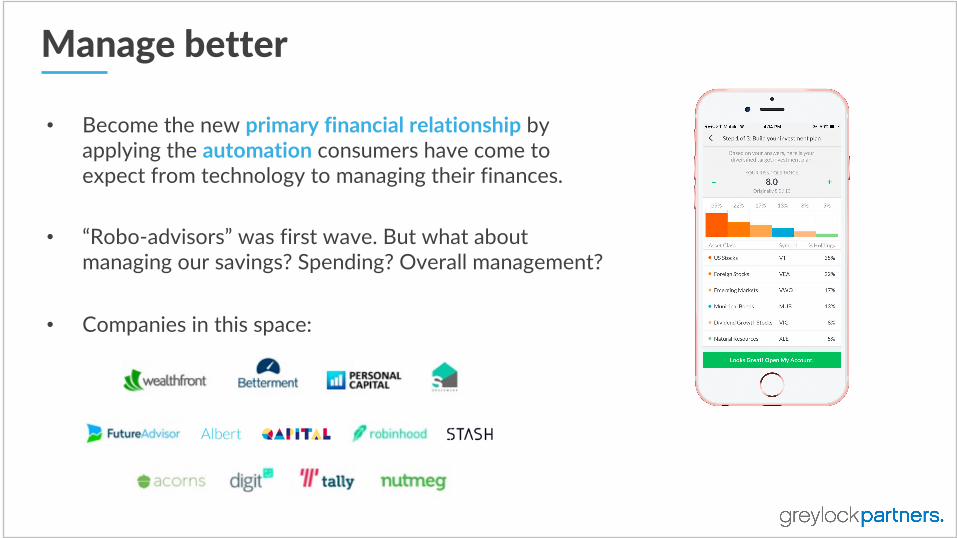

Manage better

• Become the new primary financial relationship by applying the automation consumers have come to expect from technology to managing their finances.

• “Robo-‐advisors” was first wave. But what about managing our savings? Spending? Overall management?

• Companies in this space:

Increase financial resilience: Borrow better

• Reimagining loan products to increase access to capital and/or reduce cost of capital:– New short-‐term credit instruments– Rethinking home ownership

• Must have differentiated user acquisition story and/or unique data advantage.

• Companies in this space:

Increase financial resilience: Insure better• Protection from the unexpected

– New insurance products for underserved needs or segments (e.g., freelancers)

– Recast cost structure of incumbents (by going direct to consumer, peer to peer, etc.) to provide existing products with better experience, cheaper.

• Companies in this space:

And of course…. Spend better

• Slow growth of healthcare, housing, and education costs• Telemedicine, price transparency• Work-‐based education programs, disrupt the

4-‐year college experience• Co-‐living

• “Renting” economy disrupts new verticals

• Companies in this space:

“ Silicon Valley is coming. There are hundreds of startups with a lot of brains and money working on various alternatives to traditional banking… Silicon Valley is good at getting rid of pain points. Banks are good at creating them ”

-‐ Jamie DimonCEO, JPMorgan Chase

Thank you.