Embed Size (px)

Citation preview

Role of HR after Discovering an Employee Fraud

Sanjay Kaushik

2

Fraud

INCREASING

Why fraud happens?

3

TRUST

GREED

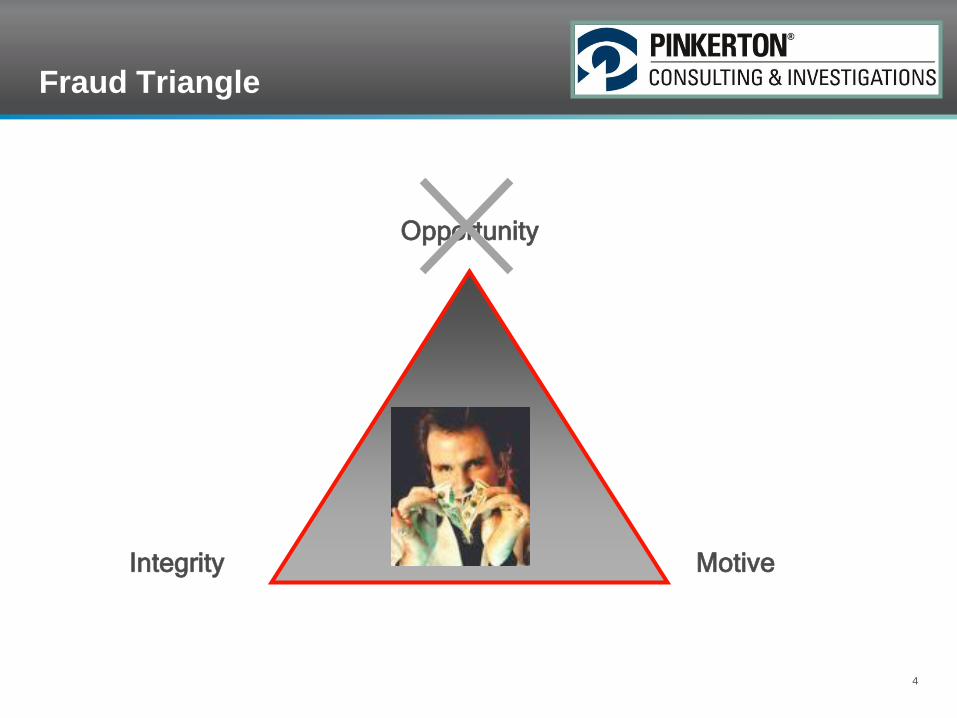

Fraud Triangle

4

Motive Integrity

Opportunity

5

Impact on the Organization

• Financial loses

• Reputation damage

• Crisis of confidence – internal / external impact

• Liability – civil and criminal

After Fraud

6

• Steps to mitigate extent of loss

• Immediate consultation with an expert

• Investigation

• Action without delay

When all else fails –Conducting

Investigations that

Work

Who Should be Involved In the

Investigation

8

• Human Resource Department

• Legal Department

• Security

• Management – If their knowledge will be helpful in conducting the

investigation

Effectively handling identified fraud

9

Internal investigations

Identifying the suspect - Confession/admission

- Direct evidence – eyewitness

- Circumstantial evidence

• Motive

• Opportunity – access/physically possible to commit the crime

• Associate evidence – physical evidence/clues

Tracing and locating the suspect

Gather facts proving guilt for court (establish elements of the

offence)

Investigation methodology

10

• Document the allegation – identify all possible indicators of fraud

• Determine potential loss – determine if error or mistake made?

• Review internal controls

• Determine the type of evidence needed to pursue – identify indicators

showing intent

• Review records – chain of custody

• Determine who should be interviewed - Develop interview approach

• Perform forensic analysis

• Complete interviews – signed statements

• Report

Follow-On To Investigation

• Management has to make decisions on disciplinary actions

• Investigators need to remain fact gatherers and not get directly involved in the specific disciplinary actions

• Can be referred for criminal prosecution, restitution, termination, reprimands; but know the positives and negatives of all of these options

• Don’t forget -- If there were vulnerabilities identified in policies, procedures or security measures – take corrective actions to close those gaps

• Investigations should lead to refinement of Threats and Vulnerabilities – linked to Risk

Analysis & deterrents

12

• Learning lessons

• A joined-up approach to

intelligence- and data-sharing

• How will dishonesty be handled?

Reporting cases to the police?

• Deterrents

Staff Fraud Prevention areas

13

• Staff vetting

• Promoting an anti fraud culture

• Monitoring of staff

• Effectively responding to identified staff fraud

• Analysis and deterrents

Staff Vetting

14

• Organizations First line of defense

• Check, double check & then re – check

• Maximum possible accuracy of

information

• Understand the databases

• Know the strengths & weaknesses of

your vendor

Anti fraud culture

15

• Promoting a culture of honesty and ethics

• New & Existing staff training and awareness

• Anonymous reporting mechanism

• Engage in regular dialogue with staff to improve systems

and identify potential problems

• Controls

Monitoring staff

16

• Risk assessments - assess organization specific risks

• Monitoring at work – Information Risk controls, requisite levels of controls

• Covert monitoring – e mail monitoring, internet activity

• Risk-based approach

• Internal monitoring systems – early warning signs, exception reports

Challenges

17

• Many organizations are anxious to play down the threat from within

and have been reluctant to admit to the scale of the problem or the

associated financial losses.

• Incidences of fraud may go unreported or getting mis - assigned as

credit losses/bad debts or operational losses

• Increased targeting by organized crime through infiltration and by

attempting to corrupt staff

• Employing credible deterrents

THANK YOU!!

QUESTIONS?