Embed Size (px)

Citation preview

T.J. Orr, ERPA, QPA, QKA

Retirement Planning Questions You Will Surely Encounter in

2015

www.pinnacle-plan.com

2

The information contained in this presentation is accurate as of August 2015

3

Our Goal

Instill confidence in our clients when offering retirement planning

advice.

4

Agenda

“Owner-only” retirement planning issues1. SEP vs. 401(k)2. Source of compensation for different entities3. Optimal salary for small business owners4. In-plan Roth conversions5. Adding a defined benefit plan6. Best practices

Recent updates1. Electronic Form 5500 filings for owner-only plans2. Plan document restatements

Information to collect

5

SEP vs. 401(k)

Owner-Only Retirement Planning Issues

6

Common Scenario

Successful small business owner No employees Wants to decrease their current

income tax liability Wants to increase retirement

savings

What’s better, SEP or 401(k)?

7

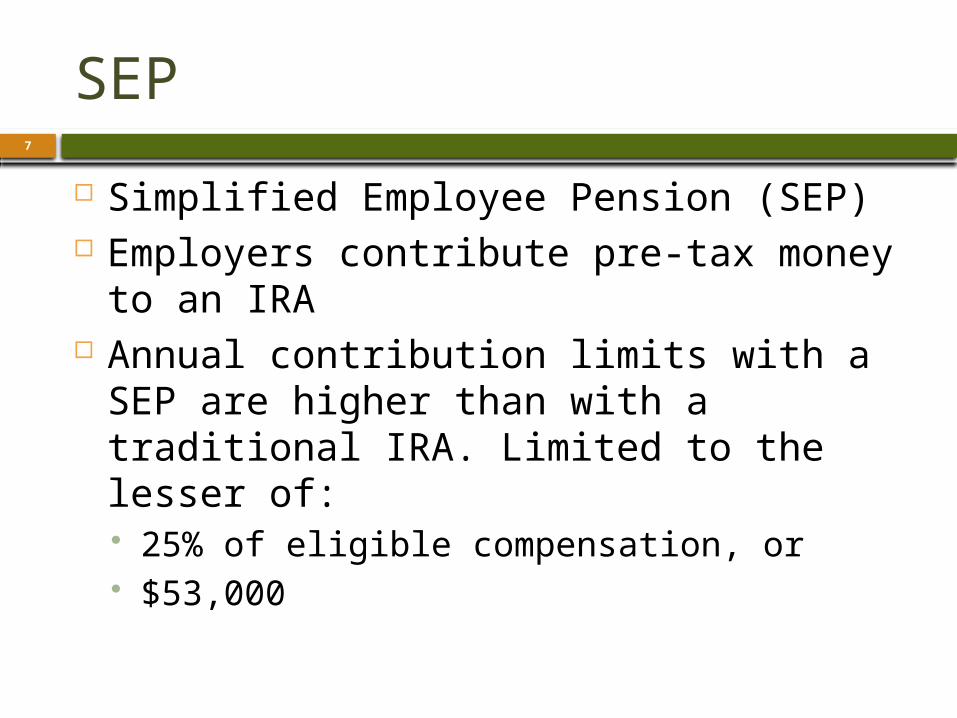

SEP

Simplified Employee Pension (SEP) Employers contribute pre-tax money to

an IRA Annual contribution limits with a SEP are

higher than with a traditional IRA. Limited to the lesser of: 25% of eligible compensation, or $53,000

8

Third-PartyAdministrat

or

SEP

SEPs do not require the services of a third-party administrator, such as Pinnacle Plan Design.

9

401(k) Plan

Myth: there is an inherent difference between a “401(k) Plan” and an “Owner-only 401(k) Plan”

Reality: False! An “Owner-only 401(k) Plan” is simply a 401(k) plan

with one participant

An owner-only plan does enjoy the benefits of a 401(k) without the concern for non-key and non-highly compensated employees. A plan design that anticipates the possibility of employees may be warranted.

10

401(k) Plan

Allows participants to make pre-tax elective deferrals or post-tax “Roth” contributions Maximum of $18,000 per year

Plan may also include discretionary employer profit sharing and/or matching contributions

Employer contributions are limited to the tax deduction limitation, which equals 25% of eligible compensation.

Maximum annual allocation is equal to the lesser of: 100% of the participant's eligible compensation, or 53,000

11

401(k) Plan: Catch-up Contributions

Participants age 50+ may defer an additional $6,000 to the 401(k) New Limits Become:

$24,000 for 401(k) elective deferrals $59,000 for annual allocations

Catch-up contributions are not available in a SEP

12

Third-PartyAdministrat

or

401(k) Plan

401(k) plans benefit from the services of a third-party administrator, such as Pinnacle Plan Design

13

Benefits of a Third-Party Administrator (TPA)

A TPA Engagement Typically Ensures Plan document and required amendments

are timely adopted Terms of plan document are followed All testing is passed Tracks assets held by money type Preps Form 5500 Prompts for required minimum distributions Is pro-active in adapting to changing

circumstances (e.g. sole proprietor move to S-Corp election)

14

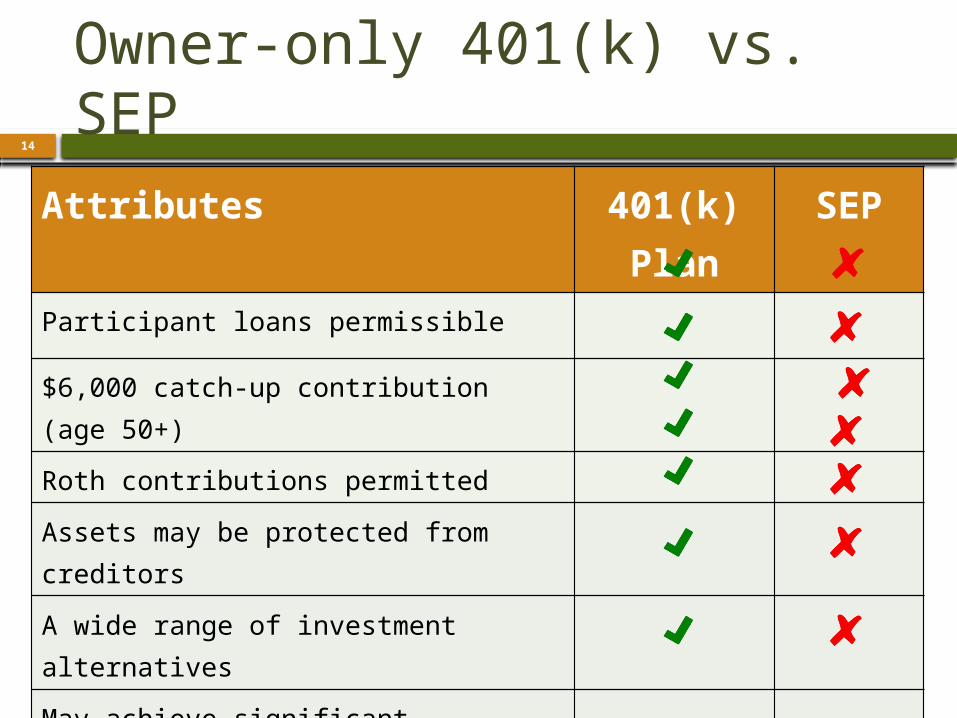

Owner-only 401(k) vs. SEP

Attributes 401(k) Plan SEPParticipant loans permissible

$6,000 catch-up contribution (age 50+)

Roth contributions permittedAssets may be protected from creditorsA wide range of investment alternativesMay achieve significant disparity in contributions when adding employeesVesting schedules permitted (relevant if any employees hired)

15

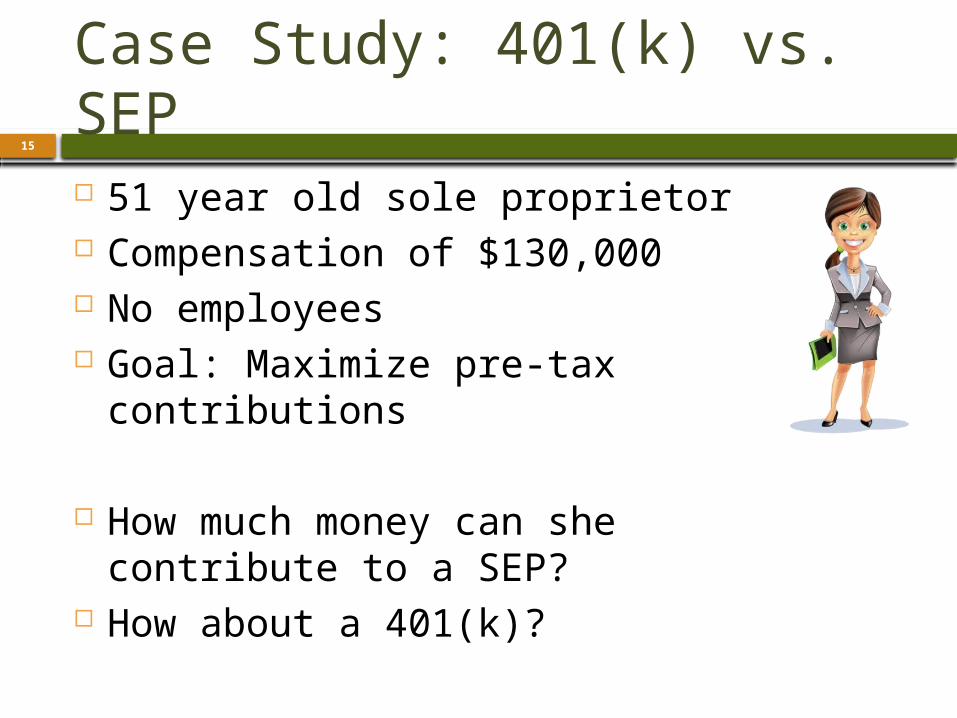

Case Study: 401(k) vs. SEP

51 year old sole proprietor Compensation of $130,000 No employees Goal: Maximize pre-tax

contributions

How much money can she contribute to a SEP?

How about a 401(k)?

16

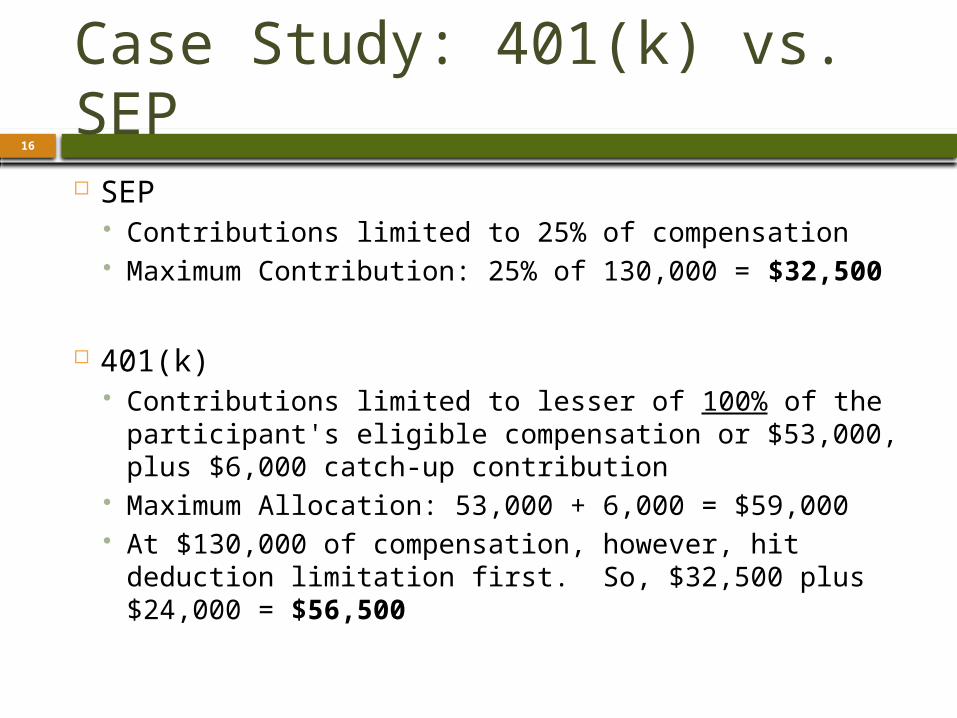

Case Study: 401(k) vs. SEP

SEP Contributions limited to 25% of compensation Maximum Contribution: 25% of 130,000 = $32,500

401(k) Contributions limited to lesser of 100% of the

participant's eligible compensation or $53,000, plus $6,000 catch-up contribution

Maximum Allocation: 53,000 + 6,000 = $59,000 At $130,000 of compensation, however, hit deduction

limitation first. So, $32,500 plus $24,000 = $56,500

17

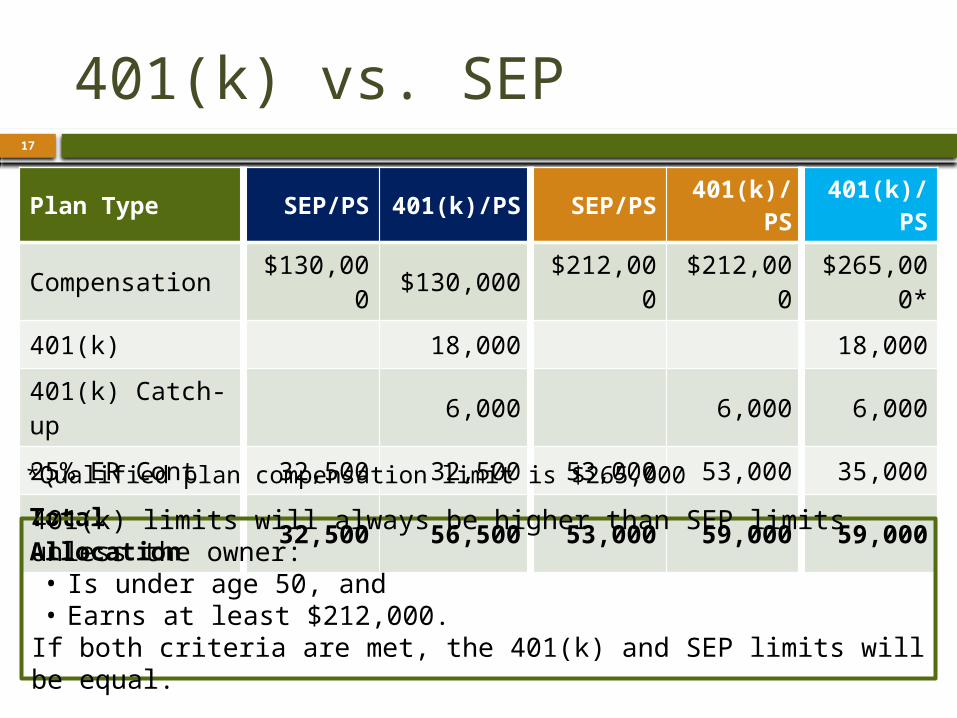

401(k) vs. SEP

Plan Type SEP/PS 401(k)/PS SEP/PS 401(k)/PS

401(k)/PS

Compensation$130,00

0 $130,000$212,00

0$212,00

0$265,00

0*

401(k) 18,000 18,000

401(k) Catch-up 6,000 6,000 6,000

25% ER Cont 32,500 32,500 53,000 53,000 35,000

Total Allocation 32,500 56,500 53,000 59,000 59,000*Qualified plan compensation limit is $265,000

401(k) limits will always be higher than SEP limits unless the owner:• Is under age 50, and • Earns at least $212,000.

If both criteria are met, the 401(k) and SEP limits will be equal.

18

Source of Compensation for Different Entities

Owner-Only Retirement Planning Issues

19

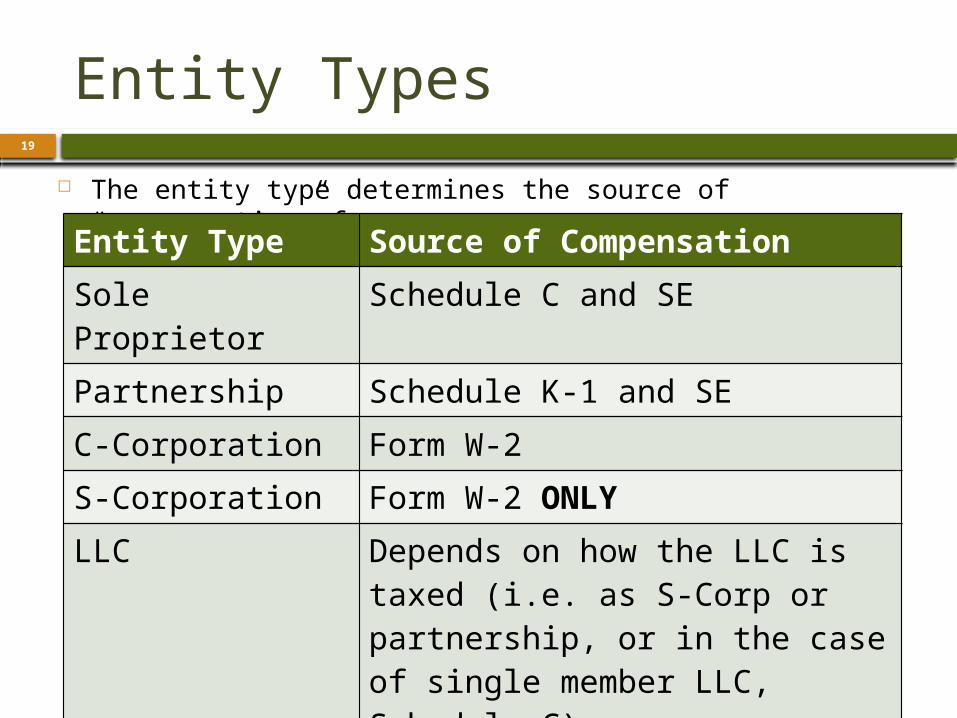

Entity Types

The entity type determines the source of “compensation” for ownerEntity Type Source of Compensation

Sole Proprietor Schedule C and SE

Partnership Schedule K-1 and SE

C-Corporation Form W-2

S-Corporation Form W-2 ONLY

LLC Depends on how the LLC is taxed (i.e. as S-Corp or partnership, or in the case of single member LLC, Schedule C)

Note: Maximum 2015 Considered Plan Compensation = $265,000.

20

Optimal Salary for Small Business Owners

Owner-Only Retirement Planning Issues

21

Common Scenario

Owner of an S-corp has been told to reduce his/her W-2 wages to minimize their payroll taxes

Same owner wants to maximize contributions to a retirement plan to maximize his/her tax deduction, which requires higher W-2 wages. Tax deduction is limited to 25% of the participants’

eligible compensation (W-2 wages)

W-2 Wages

MinimizePayrollTaxes

MaximizeTax

Deduction

22

Reducing W-2 Wages

Allows an S-Corp shareholder to have more of their income taxed as trade or business income on their personal tax return

Payroll taxes are then reduced because trade or business income is not subject to payroll tax

23

Reducing W-2 Wages

RISK! IRS frowns upon this IRS requires "reasonable compensation" for the industry

to be paid Result would be taxes up to 100% of the payroll taxes

not paid, plus penalties

MISSED OPPORTUNITY! Reduced W-2 wages limits an

owner’s tax deductible contribution to a qualified retirement plan

24

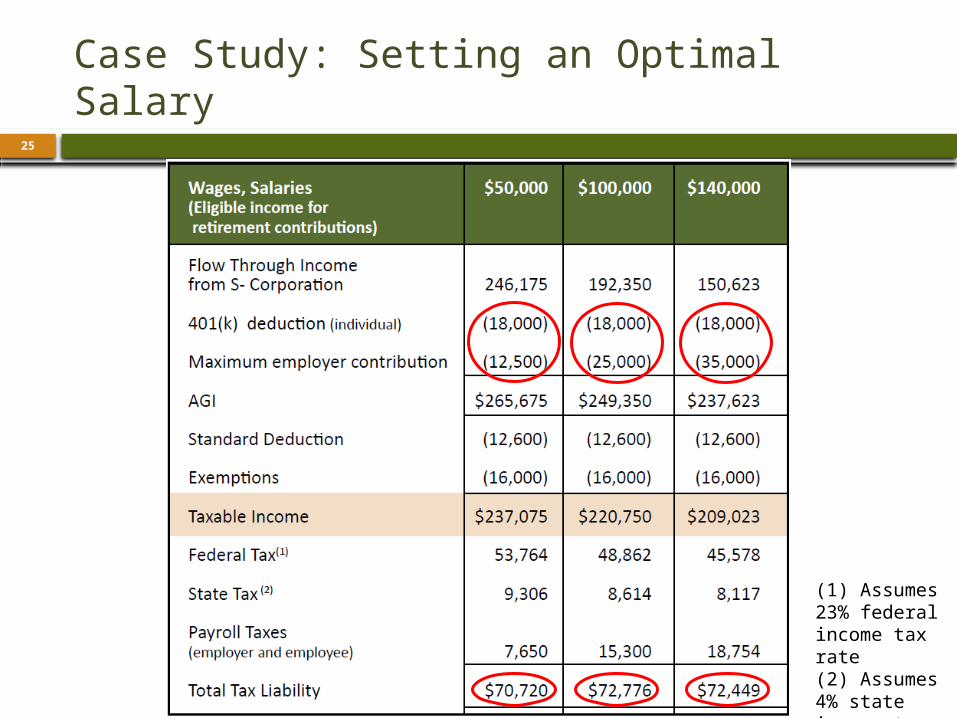

Case Study: Setting an Optimal Salary

Single owner/taxpayer of an S-corp earns $300,000 of income

She wants to contribute the maximum to the company retirement plan ($53,000 for 2015)

Uses the standard deduction only

25

Case Study: Setting an Optimal Salary

(1) Assumes 23% federal income tax rate(2) Assumes 4% state income tax rate

26

Takeaways

An increase in salary allows an owner to make the maximum permissible tax-deferred contribution to the retirement plan without significantly affecting their total tax liability.

An increased salary can potentially increase Social Security benefits

Additionally, the tax deferral allowed in a retirement plan offers a significant and powerful strategy for accumulating retirement assets and meeting retirement goals.

27

In-plan Roth Conversions

Owner-Only Retirement Planning Issues

28

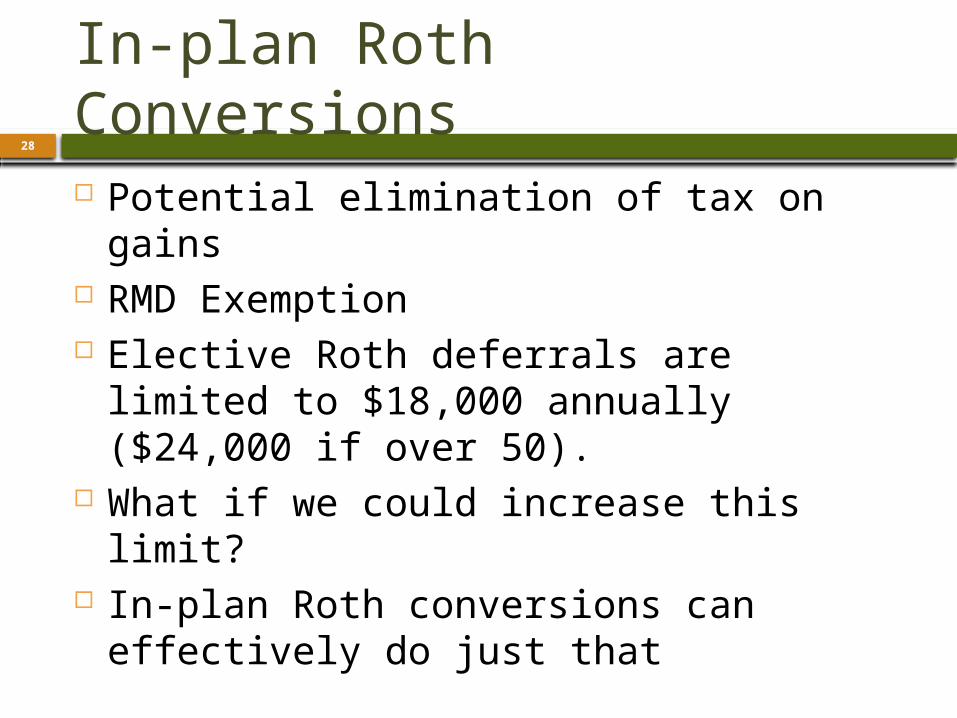

In-plan Roth Conversions

Potential elimination of tax on gains RMD Exemption Elective Roth deferrals are limited to

$18,000 annually ($24,000 if over 50). What if we could increase this limit? In-plan Roth conversions can effectively

do just that

29

In-plan Roth Conversions

A conversion of non-Roth monies within the plan into Roth monies

Can apply to: elective salary deferrals matching contributions non-elective contributions amounts rolled into the plan from another plan qualified matching contributions (QMACs) qualified non-elective contributions (QNECs) after-tax employee contributions

Source: irs.gov

30

Case Study: In-plan Roth Conversions

51 year old sole proprietor Compensation of $120,000 No employees Goal: Maximize Roth account

Q: What is the maximum amount he can add to his Roth account each year?

A: $59,000 How???

31

Case Study: In-plan Roth Conversions

The annual additions limit for a 51 year old is $59,000 Up to $24,000 in pre-tax or Roth elective deferrals The remainder can be comprised of profit sharing,

matching or after-tax employee contributions

Owner could make a $35,000 after-tax employee contribution to the plan, then convert it to Roth. Will never pay tax on the earnings Effectively increases his Roth limit from $24,000 to

$59,000

32

In-plan Roth Conversions

Plan document must permit Roth contributions AND Roth conversions

Participant election required Plan must issue Form 1099-R

Box 1 – Gross Distribution Box 2a – Taxable Amount Box 5 – Include any basis recovery Box 7 – Code G

No 945 tax withholding required Not subject to 72(t)’s early withdrawal penalty, unless

ultimately distributed to participant within the 5-year period beginning with the first day of the participant’s tax year in which the rollover was made.

33

Cautions

This strategy is only effective in owner-only plans After-tax voluntary contributions subject to ACP testing. The ACP test ensures that matching and after-tax employee contributions to

not discriminate in favor of HCEs NHCE participants would likely not contribute, causing the ACP test to fail

The plan document must allow for in-plan Roth conversions

Currently no IRS approved wording on In-Plan Roth Conversion amendments. Rather, currently operating under good-faith amendments.

Not a lot of record-keepers are ready to allow this, but 1 participant plans usually not on record-keeping platforms.

Segregated accounts recommended.

34

Adding a Defined Benefit Plan

Owner-Only Retirement Planning Issues

35

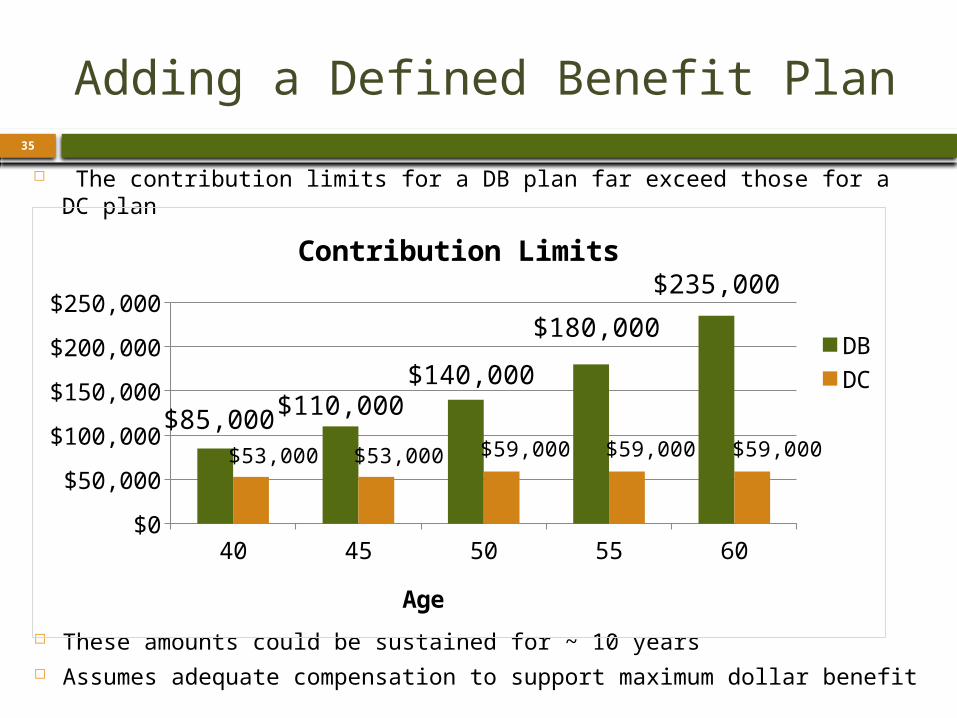

Adding a Defined Benefit Plan

These amounts could be sustained for ~ 10 years Assumes adequate compensation to support maximum dollar benefit

The contribution limits for a DB plan far exceed those for a DC plan

40 45 50 55 60$0

$50,000

$100,000

$150,000

$200,000

$250,000

$85,000$110,000

$140,000

$180,000

$235,000

$53,000 $53,000 $59,000 $59,000 $59,000

Contribution Limits

DBDC

Age

36

Tax Deduction Limits for Combo Plans (DB and DC)

Depends upon PBGC coverage and profit sharing Contribution1) If plan is exempt from PBGC coverage and profit

sharing exceeds 6% of total compensation: Deduction is limited to 31% of total eligible

compensation.

2) If plan is exempt from PBGC coverage and profit sharing is limited to 6% of total compensation

No deduction limit. May take tax deduction for full amount of employer contribution to DB and DC plans.

3) If plan is covered by PBGC No deduction limit. May take tax deduction for full

amount of employer contribution to DB and DC plans.

37

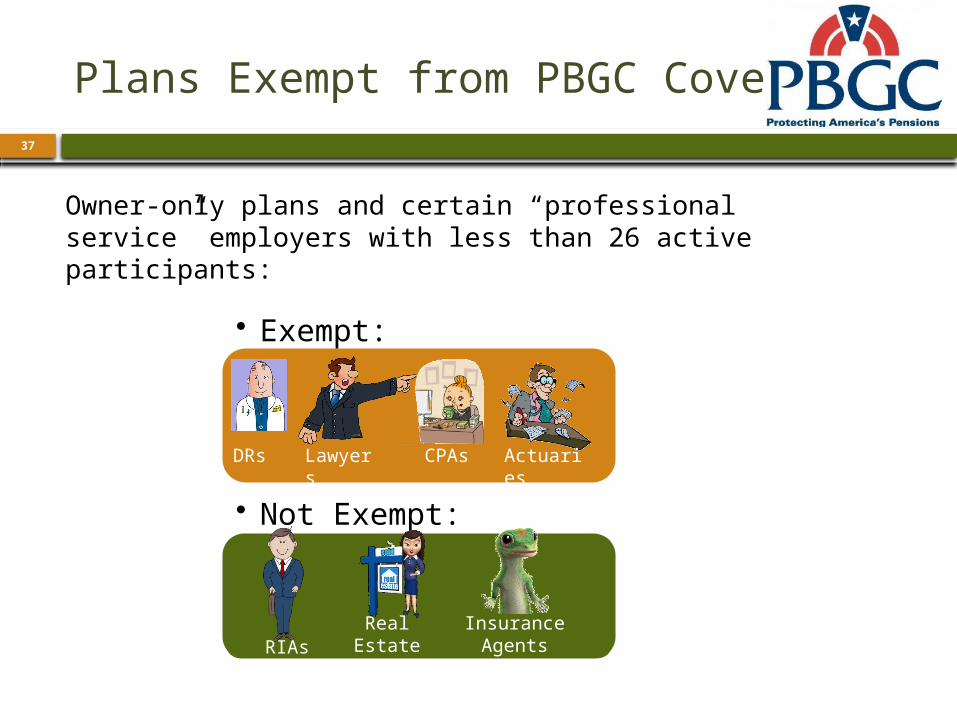

Plans Exempt from PBGC Coverage

Owner-only plans and certain “professional service” employers with less than 26 active participants:

• Exempt:

• Not Exempt:

DRs Lawyers

CPAs Actuaries

RIAsReal

EstateAgents

InsuranceAgents

38

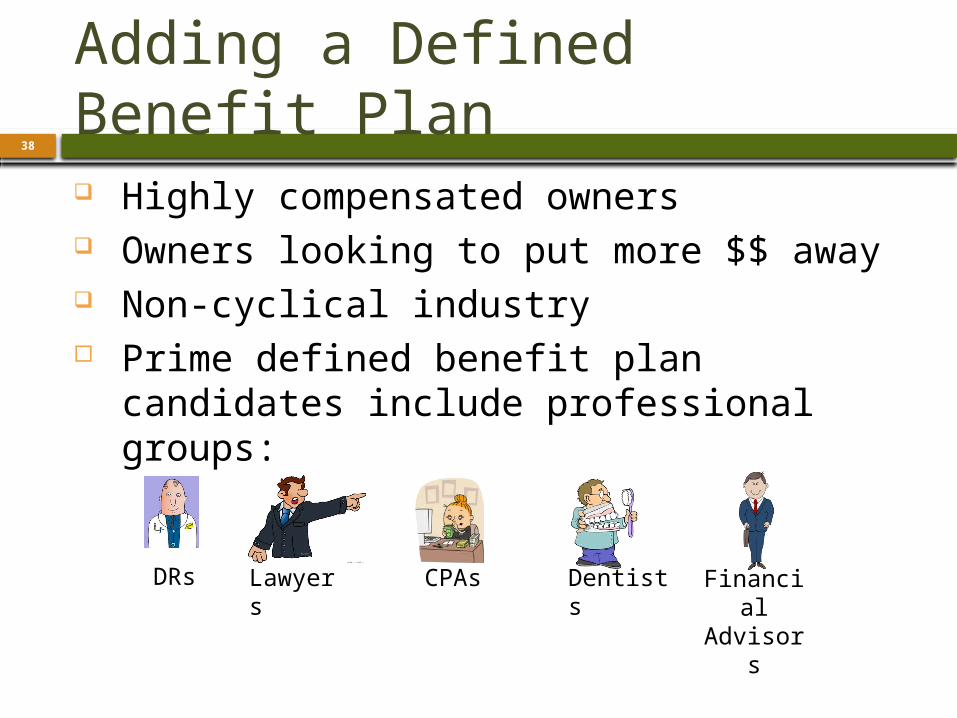

Adding a Defined Benefit Plan Highly compensated owners Owners looking to put more $$ away Non-cyclical industry Prime defined benefit plan candidates

include professional groups:

DRs Lawyers

CPAs Dentists Financial

Advisors

39

Best Practices

Owner-Only Retirement Planning Issues

40

Best Practices

Plan Design Use the most restrictive eligibility criteria to prevent entry by newly

hired employee Use a vesting schedule to prevent immediate vesting of a newly

hired employee

Be aware of potential related employers Always ask about ownership in other entities For a member of an LLC, note that the member is an employee of

the LLC, so only the LLC can adopt a plan. That is, the self-employed partner in an LLC taxed as a partnership cannot adopt a plan.

Tracking assets by money type is necessary Differing limitations Differing withdrawal restrictions Differing vesting for participant loan purposes

41

5500EZ 5500SF

Filing Update

42

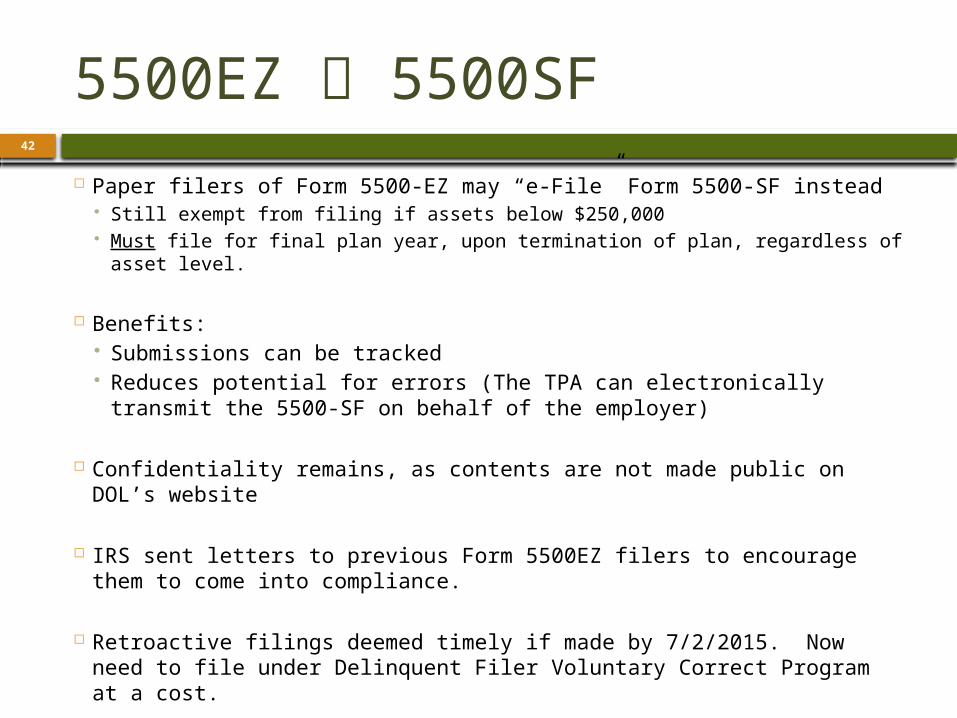

5500EZ 5500SF

Paper filers of Form 5500-EZ may “e-File” Form 5500-SF instead Still exempt from filing if assets below $250,000 Must file for final plan year, upon termination of plan, regardless of asset

level.

Benefits: Submissions can be tracked Reduces potential for errors (The TPA can electronically transmit

the 5500-SF on behalf of the employer)

Confidentiality remains, as contents are not made public on DOL’s website

IRS sent letters to previous Form 5500EZ filers to encourage them to come into compliance.

Retroactive filings deemed timely if made by 7/2/2015. Now need to file under Delinquent Filer Voluntary Correct Program at a cost.

43

PPA Plan Document Restatements

Document Restatement Update

44

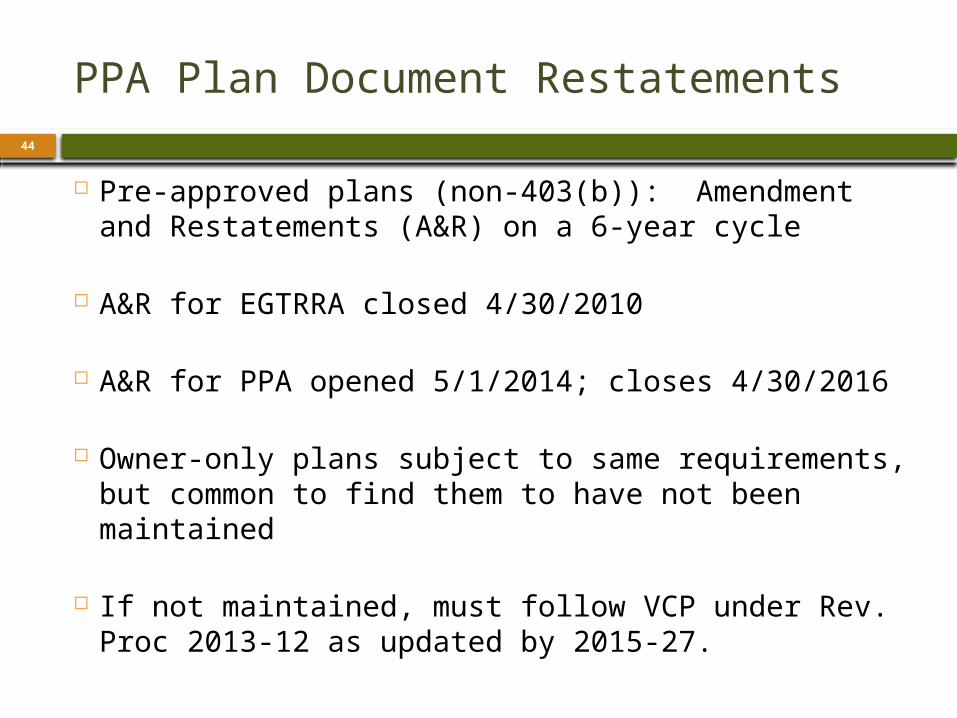

PPA Plan Document Restatements

Pre-approved plans (non-403(b)): Amendment and Restatements (A&R) on a 6-year cycle

A&R for EGTRRA closed 4/30/2010

A&R for PPA opened 5/1/2014; closes 4/30/2016

Owner-only plans subject to same requirements, but common to find them to have not been maintained

If not maintained, must follow VCP under Rev. Proc 2013-12 as updated by 2015-27.

45

PPA Plan Document Restatements

Evaluate before you restate!

46

When Assessing a Retirement Plan Opportunity

Information to Collect

47

Information to Collect

1. What is the goal of the plan? Do all owners wish to maximize contributions?

2. If there are profits for the year, is this typical and anticipated to continue?

3. Has the company ever sponsored another retirement plan?

4. How is the employer’s entity taxed?

48

Information to Collect

5. What is the ownership structure of the company? Other business interests?

6. Does the company employ any relatives of the owners?

7. Are there anticipated changes in the company structure or employee demographics in the next 2-3 years?

8. How does the employer want to manage the assets of the plan?

49

Collaboration With CPAs

We strongly value collaboration, which means…

We Are a Part of Your Team

We Are Committed to Your Continued

Success

We Listen and Offer Customized

Solutions

We Respond Quickly to Your Needs

50

Firm Facts

315years of related

experience

33pension-related

designations

845plans

administered

$1.3 Billion

plan assets

18,300participants

At Pinnacle Plan Design we design and administer retirement plans for self-employed individuals, for-profit businesses and non-profit organizations. Retirement plans offer business owners and executives the ability to reduce current tax liabilities, help ensure their personal retirement plans stay aligned with company needs, and provide a benefit to recruit and retain the talent needed to grow their business. Our superior technical expertise, combined with our unparalleled client service, makes us an industry leader in the retirement plan industry. Our highly credentialed professionals are committed to delivering outstanding client service. We provide accurate, comprehensive and timely work. Pinnacle Plan Design is an unbiased provider assisting CPAs in delivering personalized, consultative solutions to their clients. We build mutually successful partnerships with accountants across the country so that clients nationally receive a complete and exceptional plan experience.

Retirement Plan Design▲Administration▲Consulting▲Actuarial Services

www.pinnacle-plan.com

51

Beth A. Cooper, CRPS®Strategic Development [email protected](520) 906-4821