Embed Size (px)

Citation preview

Fall Conference – Kona, HI October 22nd -25th, 2014

Relation of Firm Size to Long-Term Viability

Study Of Engineering News Record (ENR) Data

2

PHASE #1 – Analyze ENR 500 data for industry trends & changes to learn…

PHASE #2 – Dig deeper into Phase #1 findings to learn…

Why Did We Do This?

3

We were hearing… Mid-sized firms saying:

“We feel squeezed and threatened.”

Experts touting: “The death of the

mid-size firm.”

Mega firms suggesting: “Mid-sized firms should give up and sell to

me”

Why Did We Do This?

4

We were hearing…

Our experience was different… Thriving

Nimble

Vital

Purpose-driven

Why Did We Do This?

5

We were hearing…

Our experience was different…

We wanted facts…

Should mid-sized firms be confident or concerned?

6

Phase #1 – What We Did

7

Phase #1 – What We Did

How Did We Do Phase #1?

8

• Research done by the University of Colorado

• Four independent sponsors

• Goal – Maintain independence of the findings

Who

What Data came from public information: • Engineering News-Record • US Economic Census Data • US Bureau of Labor

Phase #1 Fun Research Facts

9

Used 37 years of overall data from 1977 to

2014

Encompassed multiple economic

cycles

Entered 400,000+ data points into

database

Over 1500 firms of ENR data

included in the study

116,000 engineering

firms in census data

…with sector diversification data in the last 25 years

In Phase #1 We Analyzed These Aspects Of The Data

10

• Does Size Matter? Industry trends & characteristics

• Are Mid-Sized Firms in Danger? Volatility of the firms on the list

• Does Size Matter For Market Sectors? Sectors where firms worked and role of diversification

• Are You On The Menu? Influence of industry consolidation

• How Do The Megas Grow? Influence of international work

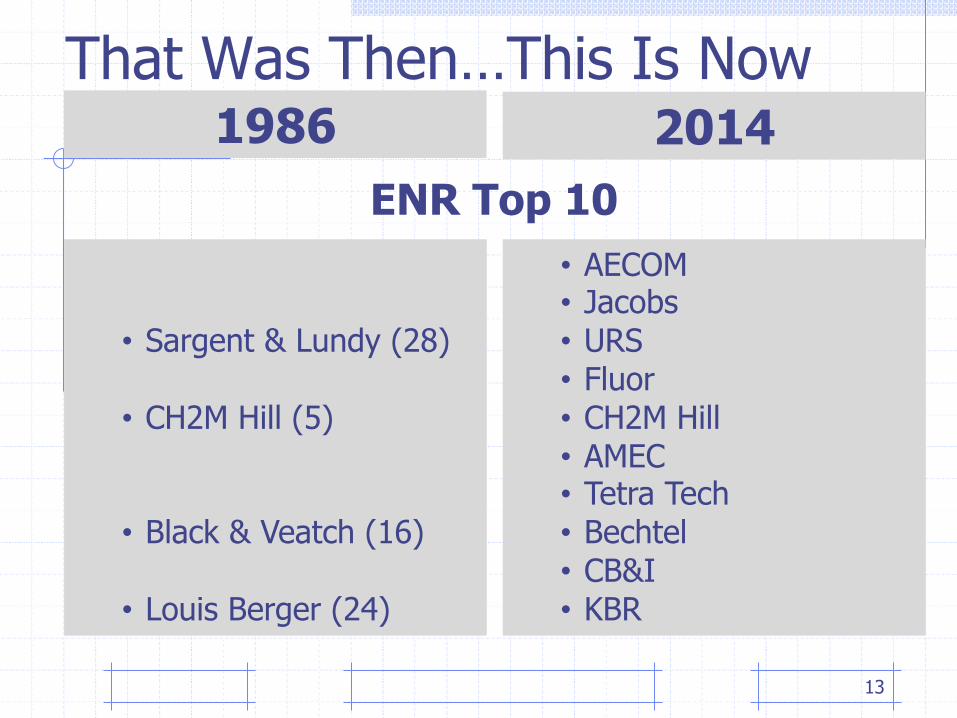

ENR Top 10

That Was Then…This Is Now 1986 2014

• AECOM • Jacobs • URS • Fluor • CH2M Hill • AMEC • Tetra Tech • Bechtel • CB&I • KBR

• Morrison-Knudsen • CRS Sirrine • Sargent & Lundy • Gibbs & Hill • CH2M Hill • Gilbert/Commonwealth • Holmes & Narver • Black & Veatch • Sverdrup • Louis Berger

11

ENR Top 10

That Was Then…This Is Now 1986 2014

• AECOM • Jacobs • URS • Fluor • CH2M Hill • AMEC • Tetra Tech • Bechtel • CB&I • KBR

12

• Sargent & Lundy • CH2M Hill • Black & Veatch • Louis Berger

ENR Top 10

That Was Then…This Is Now 1986 2014

• AECOM • Jacobs • URS • Fluor • CH2M Hill • AMEC • Tetra Tech • Bechtel • CB&I • KBR

13

• Sargent & Lundy (28) • CH2M Hill (5) • Black & Veatch (16) • Louis Berger (24)

Does Size Matter? (industry trends & characteristics)

15

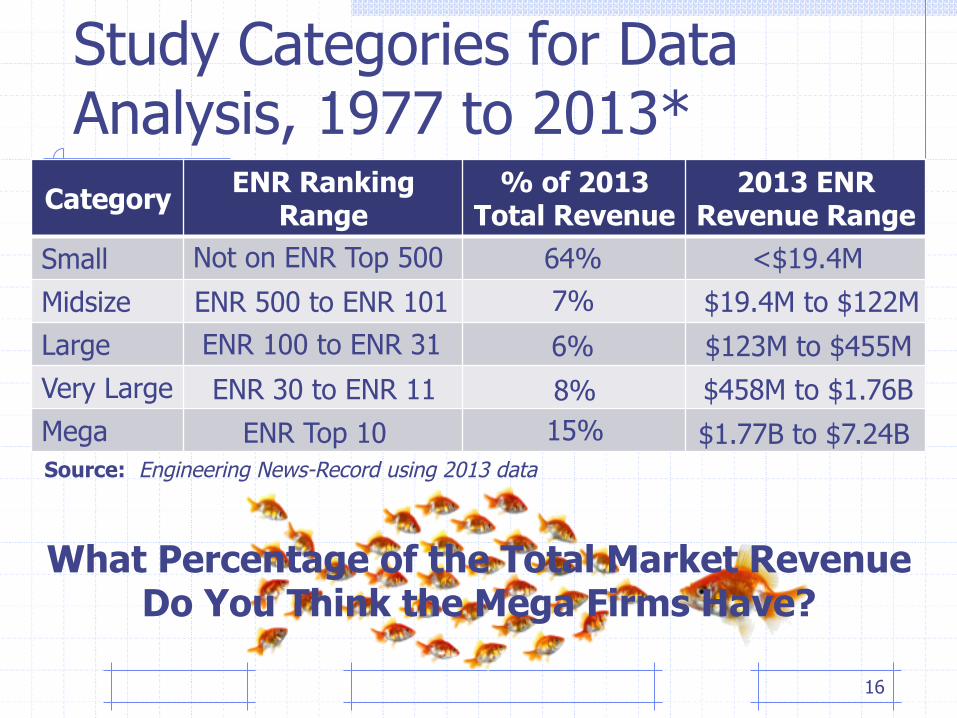

Study Categories for Data Analysis, 1977 to 2013*

Category ENR Ranking Range

% of 2013 Total Revenue

2013 ENR Revenue Range

Small Midsize Large Very Large Mega Source: Engineering News-Record using 2013 data

What Percentage of the Total Market Revenue Do You Think the Mega Firms Have?

Not on ENR Top 500

ENR 500 to ENR 101 ENR 100 to ENR 31

ENR 30 to ENR 11 ENR Top 10

<$19.4M $19.4M to $122M

$123M to $455M $458M to $1.76B

$1.77B to $7.24B

16

Study Categories for Data Analysis, 1977 to 2013*

Category ENR Ranking Range

% of 2013 Total Revenue

2013 ENR Revenue Range

Small Midsize Large Very Large Mega

Not on ENR Top 500

ENR 500 to ENR 101 ENR 100 to ENR 31

ENR 30 to ENR 11 ENR Top 10

<$19.4M $19.4M to $122M

$123M to $455M $458M to $1.76B

$1.77B to $7.24B

64% 7%

6%

8% 15%

What Percentage of the Total Market Revenue Do You Think the Mega Firms Have?

Source: Engineering News-Record using 2013 data

Page 17

Are Mid-Sized Firms In Danger? (volatility of ENR firms)

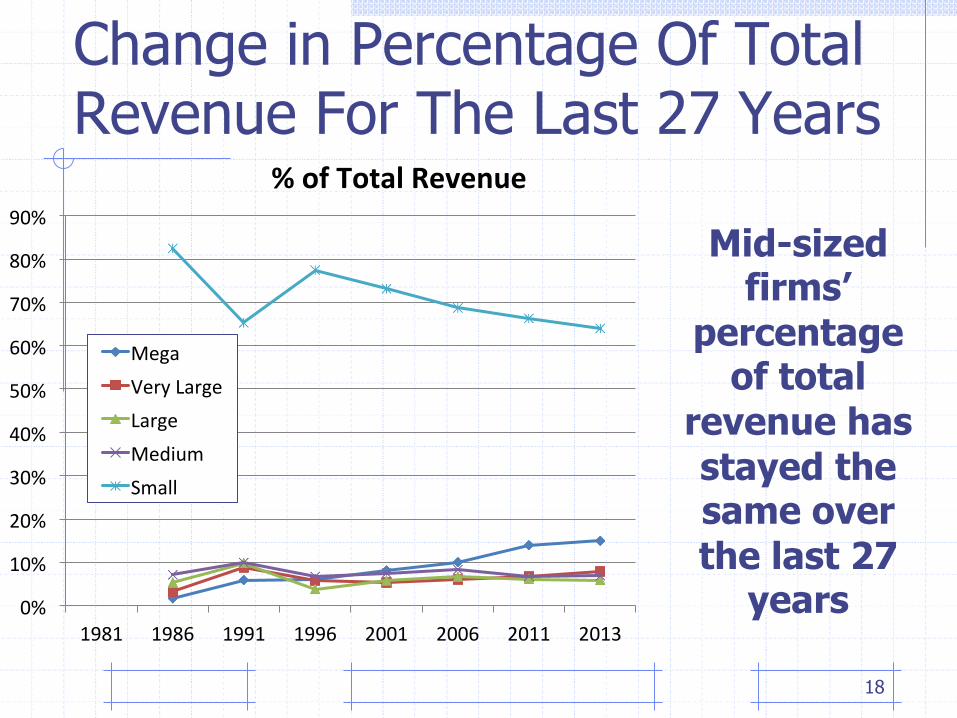

Change in Percentage Of Total Revenue For The Last 27 Years

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1981 1986 1991 1996 2001 2006 2011 2013

% of Total Revenue

Mega Very Large Large Medium Small

Mid-sized firms’

percentage of total

revenue has stayed the same over the last 27

years

18

And The Data Also Says… 1550 firms have been on ENR since 1977

58 stayed throughout the 37 years (29 mid-sized)

32 positively increased their rankings (14 mid-sized)

16 outperformed their peers in growth rates (9 mid-sized)

of those

Many midsized firms have endured and

performed!

of those

of those

19

Does Size Matter For Market Sectors?

20

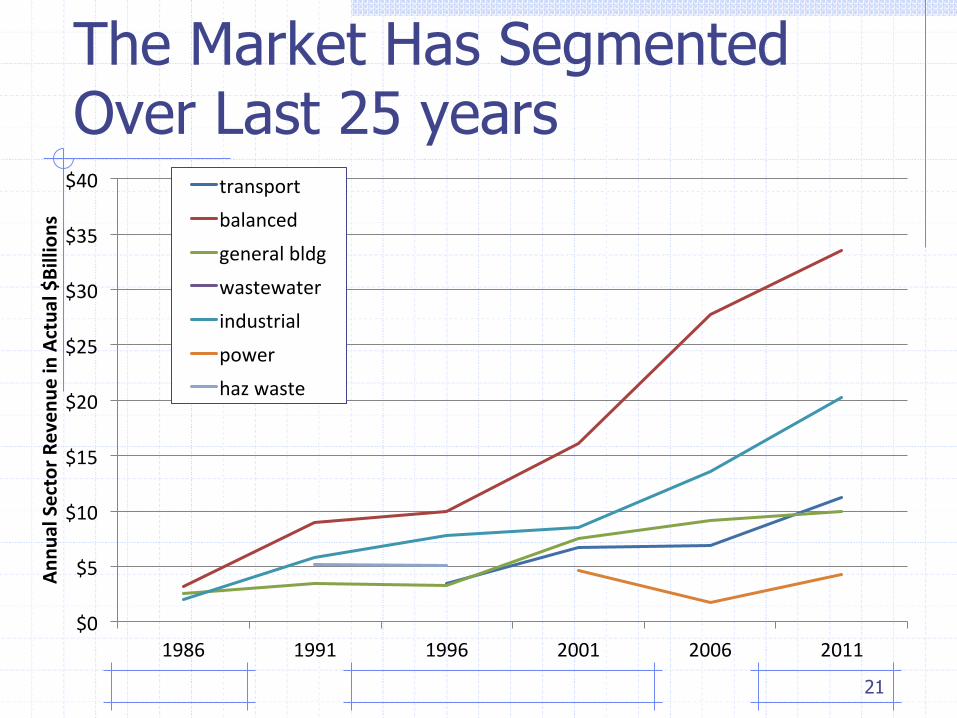

The Market Has Segmented Over Last 25 years

$0

$5

$10

$15

$20

$25

$30

$35

$40

1986 1991 1996 2001 2006 2011

Annu

al Sector R

even

ue in Actua

l $Billion

s

transport

balanced

general bldg

wastewater

industrial

power

haz waste

21

Different Size Firms Dominate Different Market Segments

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

transport balanced general bldg power industrial

% Revenue per Sector -‐ 2011 Mega

Very Large

Large

Medium

22

Are You On The Menu? (merger and acquisition activity)

M & A Activity and Market Consolidation of ENR 500 Firms

Since 2005, has been a shift from acquiring firms in the same sector to

acquiring a diversity of firms (especially for Mega Firms)

0

5

10

15

20

25

30

1985-‐1994 1995-‐2004 2005-‐2012

Same Sector versus Different Sector Purchases

same sector

different sector

24

How Do The Megas Grow? (versus everyone else)

25

Role of International – Factor In Recent Growth Of The Megas

0%

10%

20%

30%

40%

50%

60%

1981 1986 1991 1996 2001 2006 2007 2008 2009 2010 2011 2012 2013

InternaAonal Billings as Percent of Gross Billings Mega

Very Large

Large

Medium

% of 500 revenue

26

ENR Study Phase #2 - Why?

27

• What does it takes to prosper?

• What does it take to sustain success?

• What might have contributed to firms who are no longer around?

Phase #2 – Our Research

28

• The “Sweet 16” firms that stayed on the list and outperformed their peers

• Selected “sustaining” firms (out of the other 42 who stayed on the list)

• Other firms who are “living company” examples • Post mortems on firms not around today

Research Focus: Included and compared…

(> 50 firms represented in the study)

Phase #2 – Our Questions

29

Internal Strategy Cultural/philosophical business characteristics

External Strategy Impact of mix of business services and

geographic diversification

Financial Drivers and Performance Management Key financial practices and performance drivers

Succession Level of leadership/management/ownership

planning & development

Significant Events Triggering events that set the stage for long-term success

How We Organized Our Major Findings On Firms That Prosper

30

• 5 Key Success Factors

• Observations & best practices of Success Drivers

• Fatal Flaws – Counter characteristics of comparison firms no longer on the list

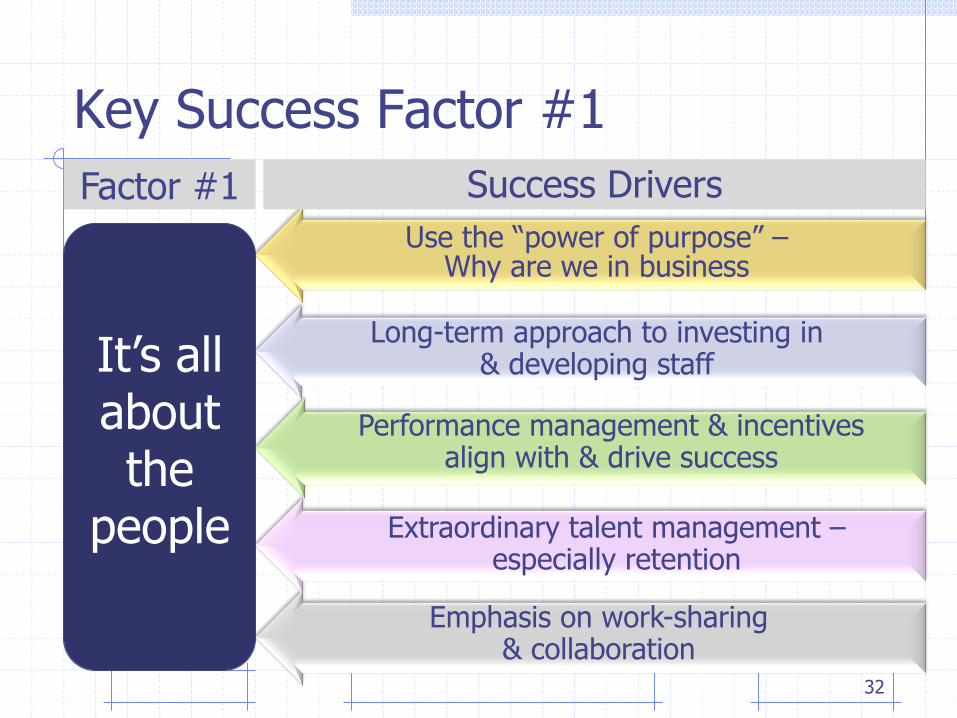

Key Success Factor #1

31

It’s all about the

people

Factor #1

Key Success Factor #1

32

Use the “power of purpose” – Why are we in business

Long-term approach to investing in & developing staff

Extraordinary talent management – especially retention

Performance management & incentives align with & drive success

Success Drivers

It’s all about the

people

Factor #1

Emphasis on work-sharing & collaboration

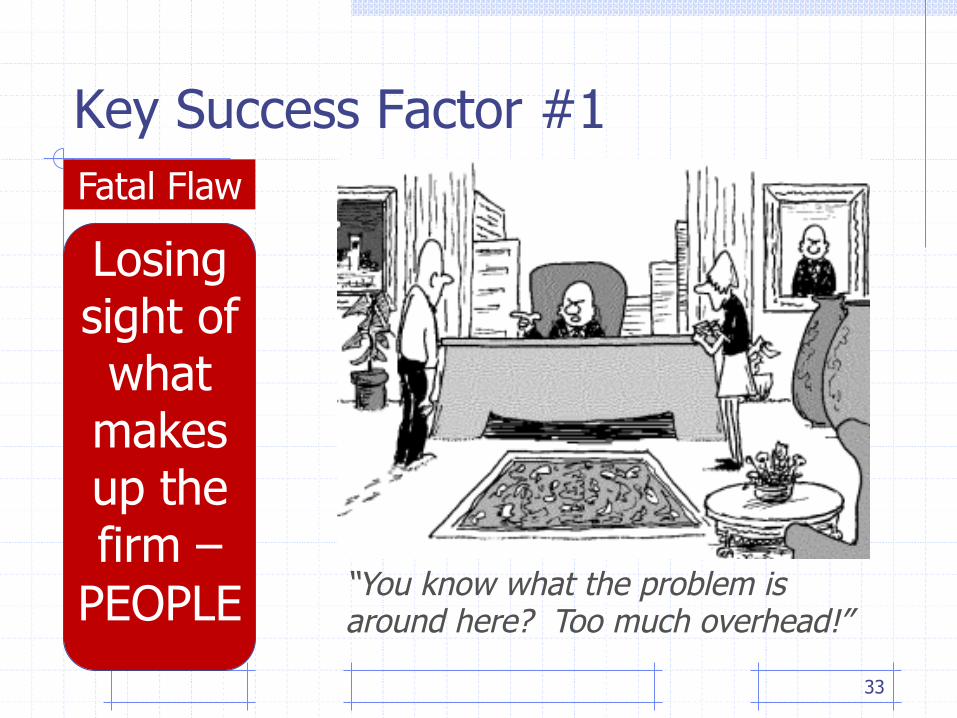

Key Success Factor #1

33

Losing sight of what

makes up the firm –

PEOPLE

Fatal Flaw

07/31/1996

“You know what the problem is around here? Too much overhead!”

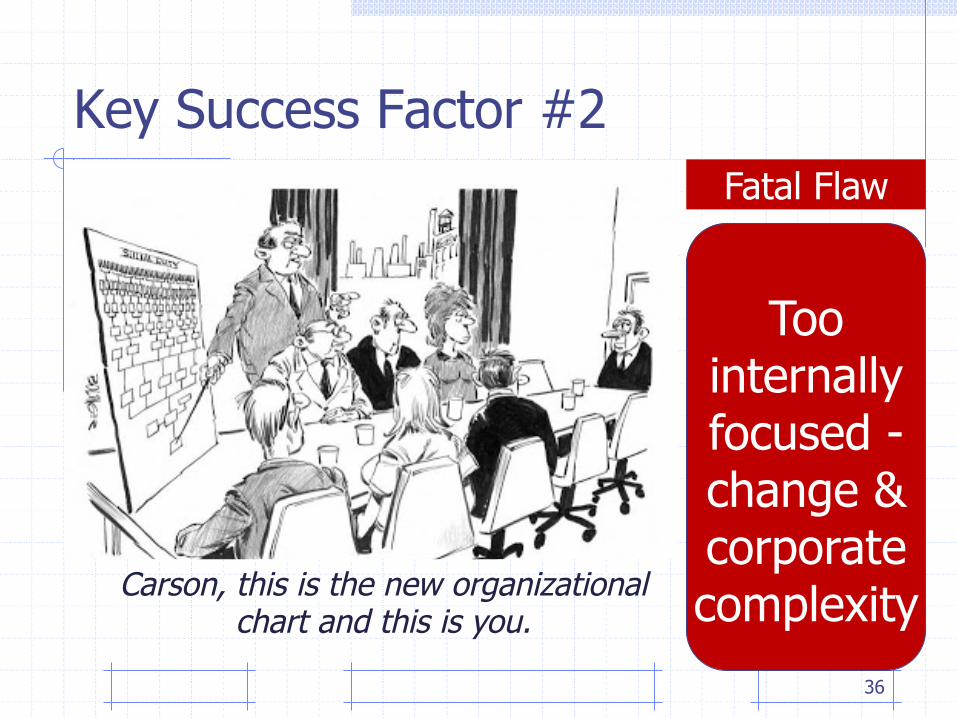

Key Success Factor #2

34

Have a clear client focus

strategy

Factor #2

Key Success Factor #2

35

Use a “customer intimacy” approach – Extra effort to understand clients & “their” business

Continually measure client satisfaction & performance

Have “agility” – Actively look for ways to provide more capability, service & value

Remove internal obstacles so staff can better focus on clients

Success Drivers

Have a clear client focus

strategy

Factor #2

Promote entrepreneurial spirit to better serve and add value

Key Success Factor #2

36

Too internally focused - change & corporate complexity

Fatal Flaw

Carson, this is the new organizational chart and this is you.

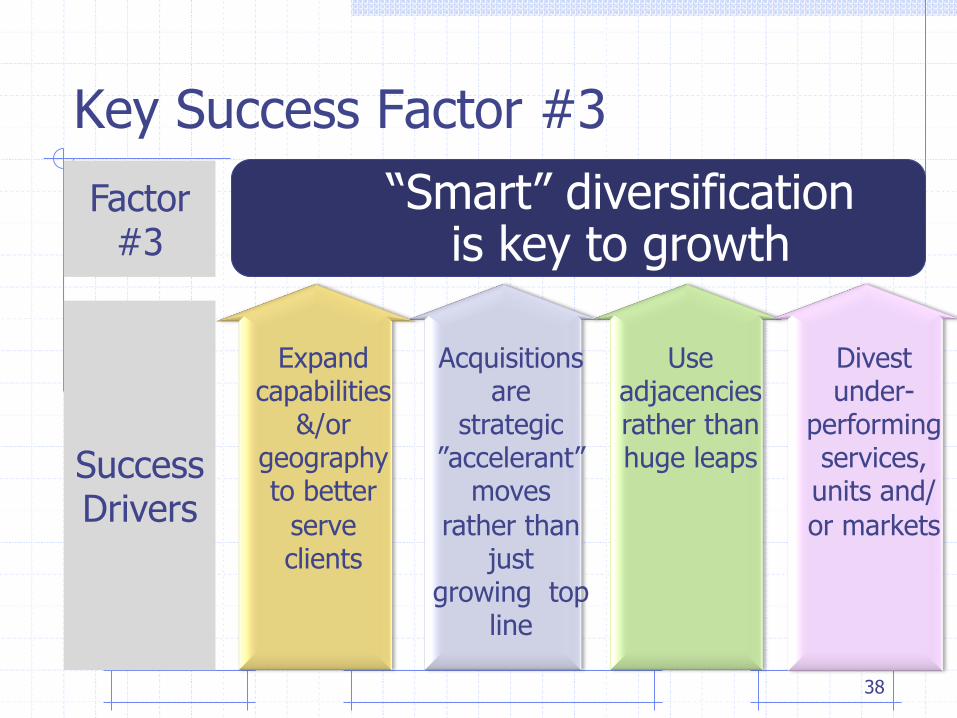

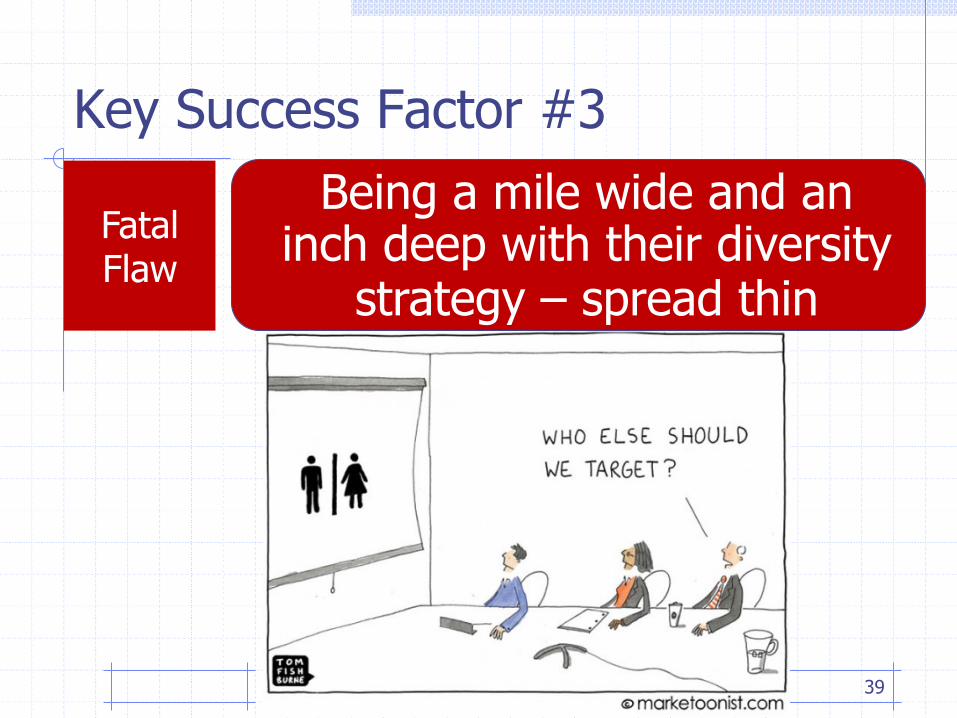

Key Success Factor #3

37

“Smart” diversification is key to growth

Factor #3

Success Drivers

Key Success Factor #3

38

Expand capabilities

&/or geography to better

serve clients

Acquisitions are

strategic ”accelerant”

moves rather than

just growing top

line

“Smart” diversification is key to growth

Factor #3

Use adjacencies rather than huge leaps

Divest under-

performing services,

units and/or markets

Key Success Factor #3

39

Being a mile wide and an inch deep with their diversity

strategy – spread thin

Fatal Flaw

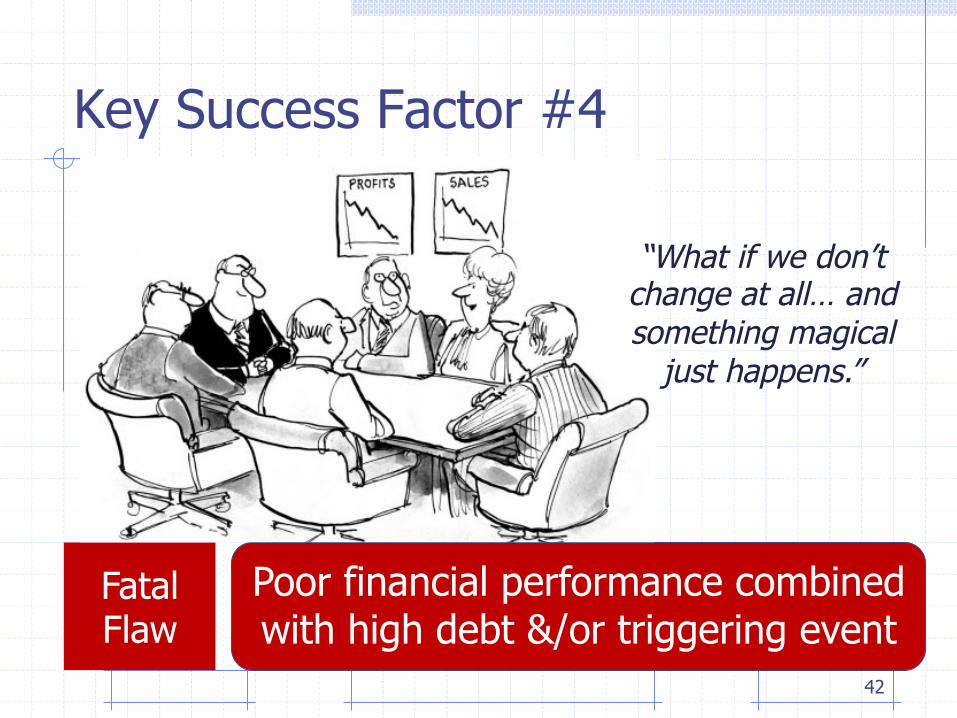

Key Success Factor #4

40

You gotta deliver financial performance

Factor #4

Key Success Factor #4

41

Success Drivers

Consistent above-

median to upper-quartile

profitability

Results driven – use goal setting/

metrics to drive clear

expect-ations & account-ability

Promote innovation

& continuous improve-ment to

get better

Capital strategy balances

short/long-term with little or no

debt

You gotta deliver financial performance

Factor #4

Key Success Factor #4

42

Poor financial performance combined with high debt &/or triggering event

Fatal Flaw

“What if we don’t change at all… and something magical

just happens.”

Key Success Factor #5

43

Ownership/ leadership succession taken very seriously

Factor #5

Key Success Factor #5

44

Ownership/ leadership succession taken very seriously

Factor #5

Broadening the ownership group is

a priority

Conservative capital structure &

long-range planning ensures

transition

Retain earnings & convert bonuses to capitalize the firm

Leaders are developed at multiple levels

Key Success Factor #5

45

No preparation for the future,

especially ownership & leadership

transition (I will live to

100!)

Fatal Flaw

Eventually son, you’ll be in charge of this – assuming of course that I

can’t come up with any better alternative.

Regarding The Key Success Factors, Some Of You May Be Thinking…

46

Well…duh! However, in the words

of a wise man….

“Greatness is not a function of circumstance

but of conscious choice & discipline.” -- Jim Collins

Questions?

47

Our Conclusion – Should Mid-Sized Firms Be Confident or Concerned?

48

Mid-sized firms are thriving, in some

ways, doing better than their larger

counterparts.

And if anyone tells you any differently,

tell them…