Embed Size (px)

DESCRIPTION

Overview of angel and venture capital financing for Canadian technology entrepreneurs

Citation preview

Things to Know when Raising Angel and Venture Capital Financing

Contemporary Issues for Technology Entrepreneurs in Canada

Dave LitwillerExecutive-in-Residence

December 17, 2013

Copyright, David J. Litwiller 2013 2

Introduction

• Angel Investors• Venture Capital (VC) Investors• Timeline• Investment Structures• Due Diligence• Negotiating Tips• Factors with Greatest Influence Over Outcomes

Copyright, David J. Litwiller 2013 3

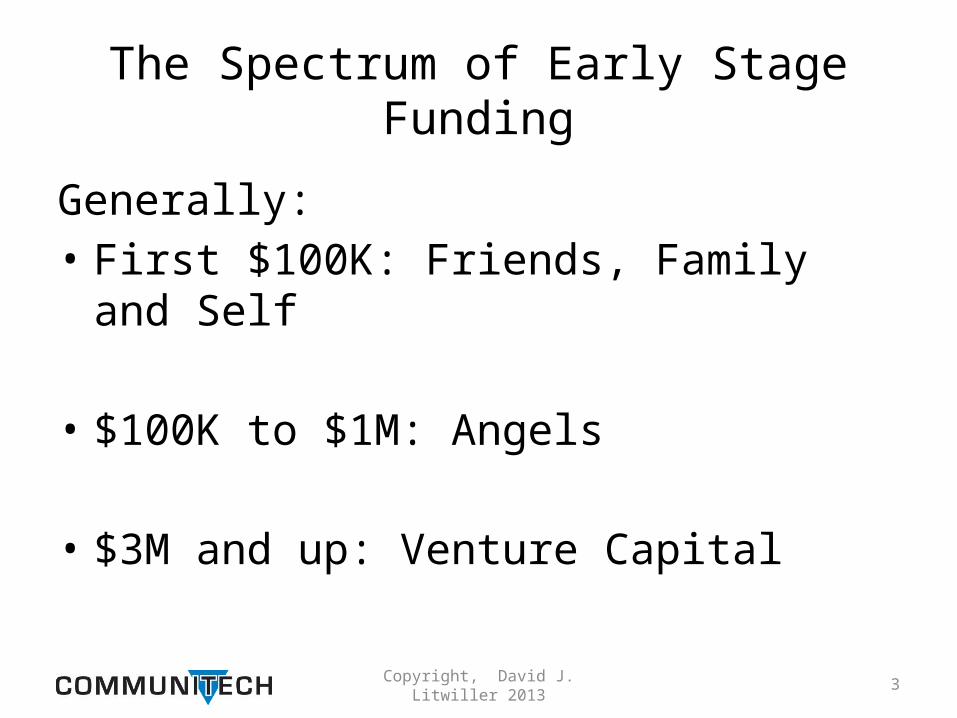

The Spectrum of Early Stage Funding

Generally:• First $100K: Friends, Family and Self

• $100K to $1M: Angels

• $3M and up: Venture Capital

Copyright, David J. Litwiller 2013 4

Angel Investing• 95% of returns come from 5% of investments

– Deals need potential to return 10*, not just 5* of later rounds

• Implication: Everything about your deal needs to indicate that it is one of the few, hottest deals of the year– Team, technology, market, timing, speed of execution, agility

• Further Implication: If your deal is not one of the stand-outs, even among investment-worthy opportunities– Less bargaining power– Slower funding cycles; more distraction from operations– Less influence over attaining high performance governance, appropriate

operational involvement and positive networking/referral impact from investors

Copyright, David J. Litwiller 2013 5

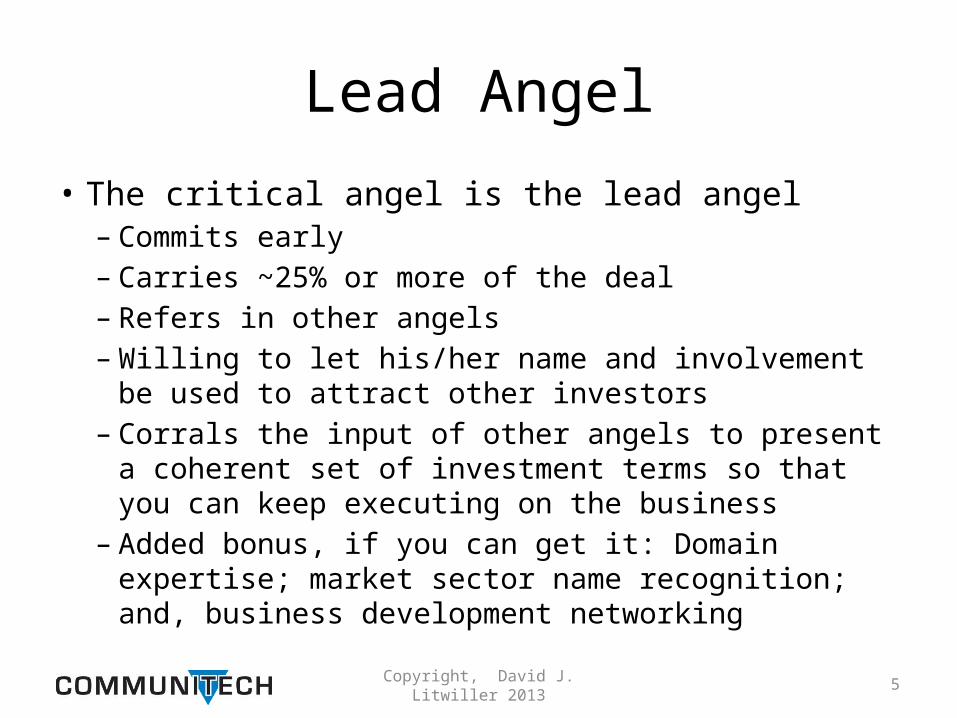

Lead Angel

• The critical angel is the lead angel– Commits early– Carries ~25% or more of the deal– Refers in other angels– Willing to let his/her name and involvement be used to attract

other investors– Corrals the input of other angels to present a coherent set of

investment terms so that you can keep executing on the business

– Added bonus, if you can get it: Domain expertise; market sector name recognition; and, business development networking

Copyright, David J. Litwiller 2013 6

Lead Angel

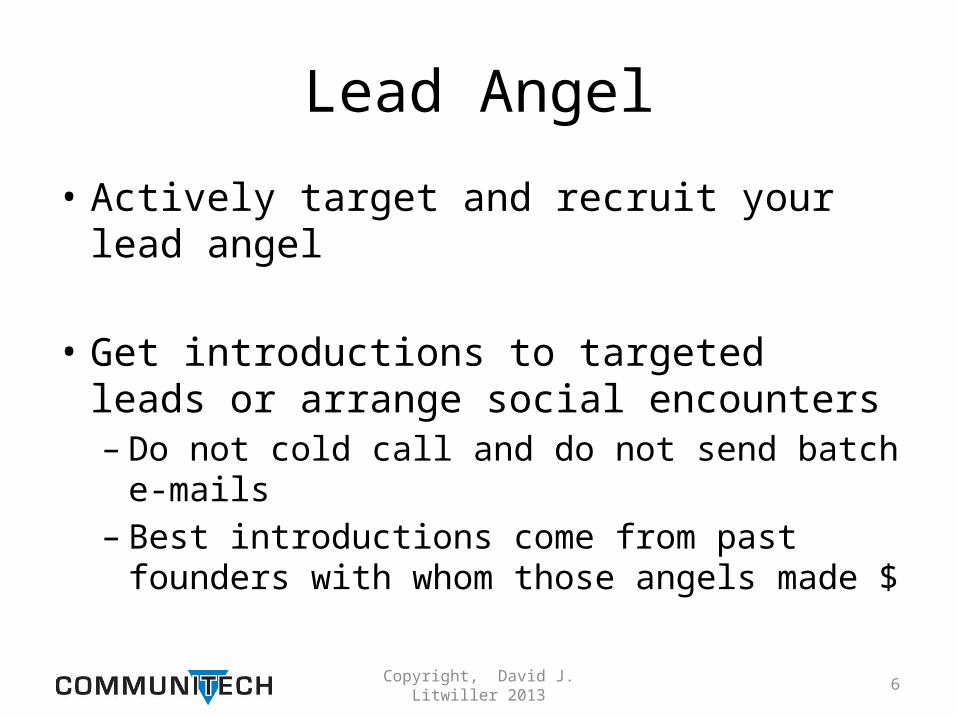

• Actively target and recruit your lead angel

• Get introductions to targeted leads or arrange social encounters– Do not cold call and do not send batch e-mails– Best introductions come from past founders with

whom those angels made $

Copyright, David J. Litwiller 2013 7

Lead Angel

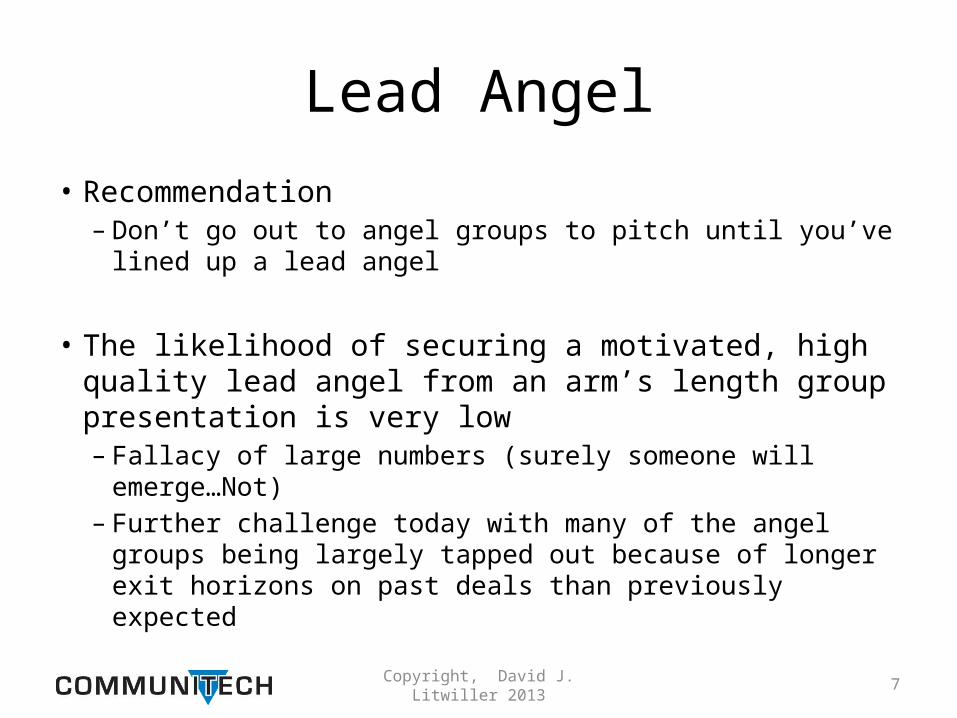

• Recommendation– Don’t go out to angel groups to pitch until you’ve lined up a

lead angel

• The likelihood of securing a motivated, high quality lead angel from an arm’s length group presentation is very low– Fallacy of large numbers (surely someone will emerge…Not)– Further challenge today with many of the angel groups

being largely tapped out because of longer exit horizons on past deals than previously expected

Copyright, David J. Litwiller 2013 8

Where Angel Investment Works Best

• Capital efficient businesses– Consumer web– Consumer-like B2B SaaS– Mobile– Software-in-plastic kinds of lower risk hardware– Other low barrier to entry, low regulation businesses

• Other fields require larger funding amounts, more funding rounds, and have more potential friction points before liquidity to harm the potential investment returns for early round investors

• Where an early exit is likely – Angels are generally much happier than VCs to take an early exit– VCs need to stay in and gamble for the biggest outcomes to make their business

model work

Copyright, David J. Litwiller 2013 9

Bimodal Angel Investing Success Models

• Small number of investments– In domains where the angel is an expert, and has a current network to make

privileged introductions to substantially lift the success trajectory for each investee

– Angel has time to dedicate to helping each investee, is supportive, but without excessive interference

– Typically five or fewer investments at any one time

• Large number of investments– At least 25, better yet is over 100 investments– Sometimes maligned as “spray and pray”– Little time for value add, but these angels typically don’t interfere much– Sometimes not even much due diligence– Strong statistical and empirical basis favouring this form of angel investing given

the natural volatility of such early stage participation

Copyright, David J. Litwiller 2013 10

Amount of Angel Funding To Raise

• Mode #1:– Enough to fund the next 12-18 months, as the

minimum increment of runway to justify the time and effort fundraising

• Mode #2:– Enough to reach the next major milestones or proof

points at which time the business will be much more valuable and able to attract larger funding amounts at higher valuation

Copyright, David J. Litwiller 2013 11

How Much Funding to Raise

• Know your number, and the use of proceeds– Nothing says indecision like waffling on the size of

the raise or the critical investments to be made

Copyright, David J. Litwiller 2013 12

Angel Due Diligence

• The lead angel will typical spend ten to twenty hours on due diligence

• Expect you will spend at least twice that amount of time with preparation, meetings, and follow-up actions

Copyright, David J. Litwiller 2013 13

Targeting VCs

• You need to start with: – Forty firms – Well selected as being top quartile in their field over the

past two years for investment returns – Deep, current domain expertise– Recent deal flow at the same stage of development– Several completed first time investments as lead in the past

18 months, and still in the first four years of their fund

• To get this number of firms requires going south of the border for some candidate funds

Copyright, David J. Litwiller 2013 14

Targeting VCs

• Do as much due diligence on any VC with which things start heating up as that VC will do on you– Integrity and communication style of the key people– In depth discussion with current and past investees

about how the VC behaved, particularly in challenging conditions

– Understanding from past associates and investees of how the individual VCs would game their own accounting and incentive structures and the implications for investee company deal structures

Copyright, David J. Litwiller 2013 15

Pre-Formation VCs• It is difficult to raise a new VC fund in Canada today• Manage your time carefully if a pre-formation fund is interested in

you• The likelihood they will receive funds to commence investment

operations is very low• Moreover, good VCs do not want to pre-identify their initial

portfolio of investments to their targeted limited partners – Those limited partners would then (understandably) want to condition

their investment in the VC fund on due diligence regarding the prospective investees

• If an interested VC has not yet secured their own funding, you are usually far better to diplomatically defer the conversation until if and when they have a first closing

Copyright, David J. Litwiller 2013 16

Caution about Growth Stage VCs as an Earlier Stage Company

• One of the few areas of VC strength as an asset class over the past decade has been growth stage funds

• Growth stage investee thumbnail:– $10M in annual sales– Product-market fit– Substantial, proven management team– Looking for growth capital to propel target to $30M sales and beyond

• These funds will spend time with you as an earlier stage company, but often it is more as a brain pick for ideas for their investment portfolio or to identify new sectors of interest than with a view to legitimate investment candidacy in your company – Don’t expect them to bend their investment parameters for you, despite any

intimations to the contrary

Copyright, David J. Litwiller 2013 17

How to Interpret Any VC Answer Other than Yes

• VCs are approached for 100 to 150 deals to yield each one that they complete

• One of the core competencies of any VC is knowing how to say no without having people hate them

• Common forms of a quasi-diplomatic No:– Buddy pass/referral to another firm– Rock fetch/if you can find someone else to lead… – Not now (but keep giving us information); too early– Exploding term sheet– Early term sheet with no real pace of follow-up activity

Copyright, David J. Litwiller 2013 18

How to Interpret Any Answer Other than Yes

• Takeaway:– With VCs, listen to the answer to your overture for investment, not the

reason

– Anything other than a clear Yes to proceed to the next step of investigation and negotiation is a No, no matter the more diminutive form of the words used

– Maxim for how to think about early VC approaches: Lead, follow, or get out of the way

– Once there is a high quality lead VC doing the heavy lifting of due diligence and negotiating, there will usually be many other funds that would like to jump on and help syndicate the round

Copyright, David J. Litwiller 2013 19

The Significance of a First Meeting

• It takes many potential deals to find a few good deals

• VC firm partners and associates are accountable to each other weekly to review deal pipelines, usually Monday mornings

• Each investment executive is obligated to report that they have looked at significant number of new deals, to show that they are broadly aware of interesting companies and ideas which might be developing, and larger trends which may be emerging across sectors of interest

Copyright, David J. Litwiller 2013 20

The Significance of a First Meeting

• A VC’s willingness to take a first private meeting shouldn’t be seen as anything more than them fulfilling their internal metrics for raw deal flow

• Far more significant is a second meeting and beyond when the VC is clearly investing significant time and opportunity cost pursuing your deal, and expressing an interest in leading an investment round, not just joining a syndicate

Copyright, David J. Litwiller 2013 21

At The First Meeting and After

• Lay out the roadmap of company objectives over the next two to four months

• Then,– Nail all of them (customers, tech, partnerships)– Hit a couple more you hadn’t promised

Copyright, David J. Litwiller 2013 22

At the Second Meeting and After

• Be prepared

• Have answers to all of the open questions from the first meeting

• Show that you can adapt very quickly based on events since you last met

Copyright, David J. Litwiller 2013 23

The Investor’s Acid Test

• Rising sense of momentum at each successive meeting

• Otherwise, deal is off

Copyright, David J. Litwiller 2013 24

VC Caution

• Stay away from discussing product roadmap specifics until you have a clear signal of investment likelihood– Often VCs have other investees to which they can feed

this information – Sometimes they are even incubating directly competitive

ventures

• Test question: How far into the 100 hours of typical due diligence for a lead VC is the prospective investor when precise roadmap questions start coming up?

Copyright, David J. Litwiller 2013 25

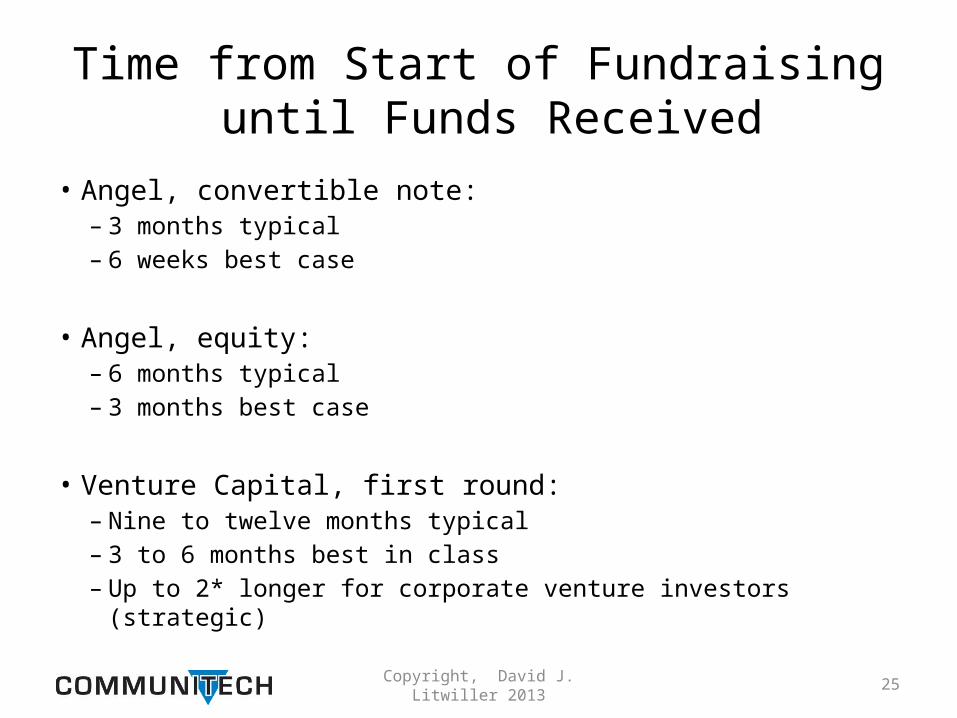

Time from Start of Fundraising until Funds Received

• Angel, convertible note:– 3 months typical– 6 weeks best case

• Angel, equity:– 6 months typical– 3 months best case

• Venture Capital, first round:– Nine to twelve months typical– 3 to 6 months best in class– Up to 2* longer for corporate venture investors (strategic)

Copyright, David J. Litwiller 2013 26

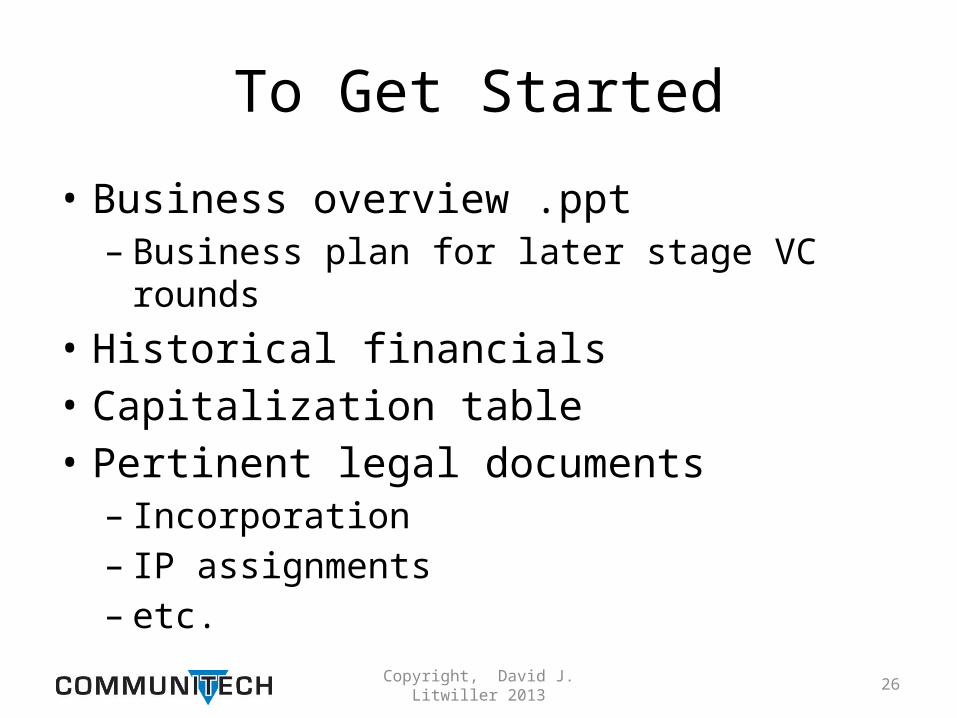

To Get Started

• Business overview .ppt– Business plan for later stage VC rounds

• Historical financials• Capitalization table• Pertinent legal documents– Incorporation– IP assignments– etc.

Copyright, David J. Litwiller 2013 27

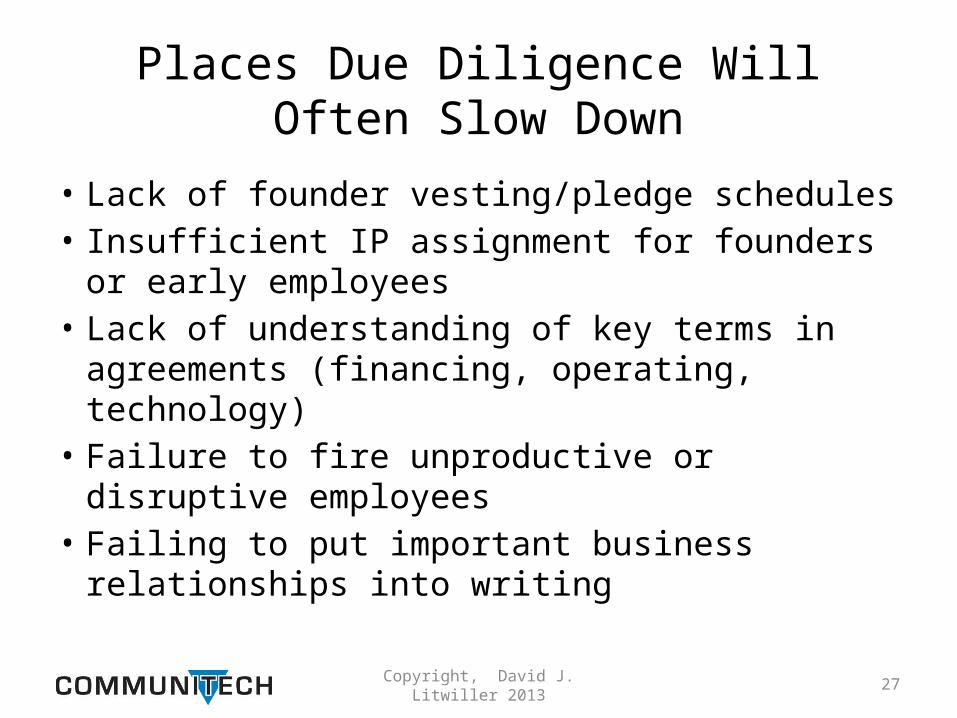

Places Due Diligence Will Often Slow Down

• Lack of founder vesting/pledge schedules• Insufficient IP assignment for founders or early

employees• Lack of understanding of key terms in

agreements (financing, operating, technology)• Failure to fire unproductive or disruptive

employees• Failing to put important business relationships

into writing

Copyright, David J. Litwiller 2013 28

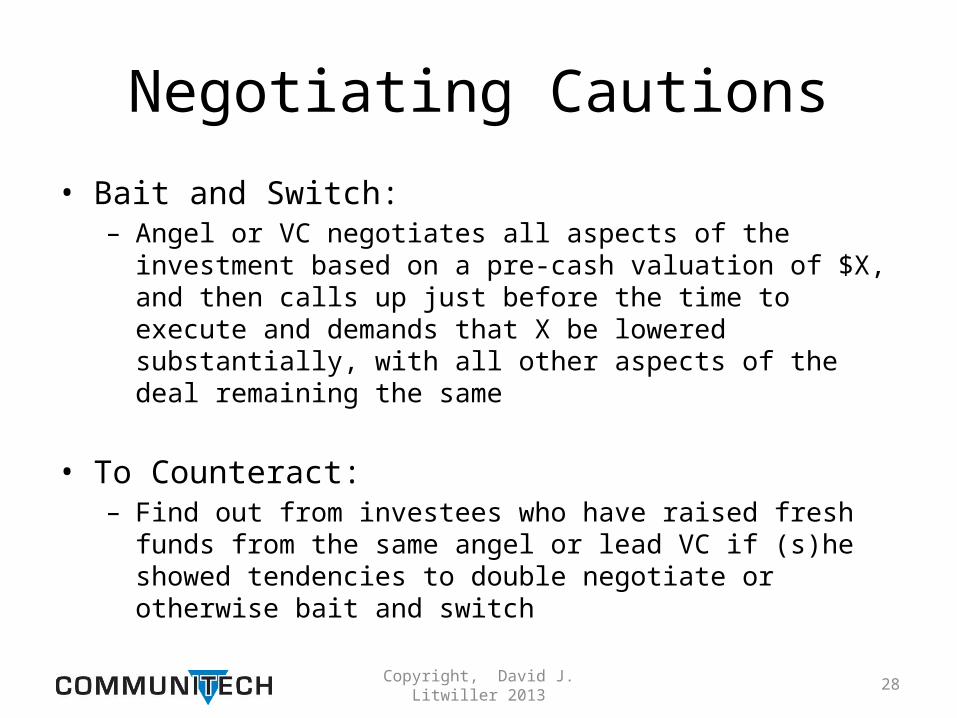

Negotiating Cautions

• Bait and Switch:– Angel or VC negotiates all aspects of the investment based on a pre-

cash valuation of $X, and then calls up just before the time to execute and demands that X be lowered substantially, with all other aspects of the deal remaining the same

• To Counteract:– Find out from investees who have raised fresh funds from the same

angel or lead VC if (s)he showed tendencies to double negotiate or otherwise bait and switch

Copyright, David J. Litwiller 2013 29

Negotiating Cautions

• Your Price (Sort Of), My Terms– Scenario: Entrepreneur desires an apparently higher pre-cash

valuation for the business than the Angel or VC initially offers– Angel or VC comes back with a higher nominal pre-cash valuation term

sheet, but with significant additional preference rights– The expected value of those preference rights typically lowers the

implied pre-cash valuation to less than the initial pre-cash valuation– Moreover, the addition of those further preference rights creates a

more complex baseline for subsequent investment rounds– Downstream investors will typically see the last investment round’s

rights as the starting point for what they will demand

Copyright, David J. Litwiller 2013 30

Picking Funding Partners

• Do as much due diligence on your prospective funders as they do on you– You will be joined at the hip for many years as the expected case– Spend the time getting to know who you will be doing business with

before the deal gets signed– Explore particularly how a candidate investor has reacted in the recent

past when investee companies hit a rough patch and plans needed to adjust

• For VCs, know how the carry is divided among the partners, because that allocation shows who really calls the shots

Copyright, David J. Litwiller 2013 31

Picking Funding Partners

• Test how actively and precisely the angel or VC has been able to network on behalf of recent past investee companies to boost prospects

• Be wary of VC generalists, which invest across many sectors – Ex: software, semis, cleantech, biotech…– Nearly impossible for a generalist to develop enough

expertise or credibility to add much value, especially at later stages of company development as contextualization demands increase

Copyright, David J. Litwiller 2013 32

Financing Agents

• Preferred practice: Never use them– Good management teams and good deals find their own investors and

introductions to investors

• Financing agents:– Signal desperation or lack of business savvy by entrepreneurs– Garnish the proceeds of the funding, usually 5% to 15%, effectively

taxing the investment returns for a prospective funder, making the likelihood of securing funding plummet

– Make high quality angels and VCs run away– Often are people trying to restart failed careers in other sectors of

finance, and taint the business in the eyes of candidate investors through their association

Copyright, David J. Litwiller 2013 33

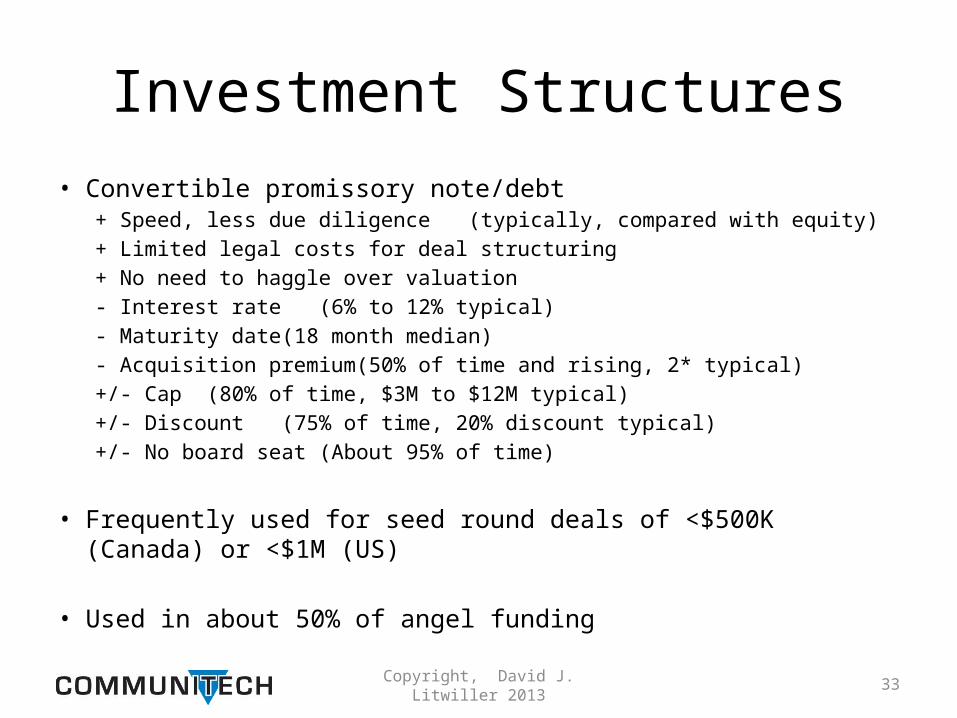

Investment Structures• Convertible promissory note/debt

+ Speed, less due diligence (typically, compared with equity)+ Limited legal costs for deal structuring+ No need to haggle over valuation- Interest rate (6% to 12% typical)- Maturity date (18 month median)- Acquisition premium (50% of time and rising, 2* typical)+/- Cap (80% of time, $3M to $12M typical)+/- Discount (75% of time, 20% discount typical)+/- No board seat (About 95% of time)

• Frequently used for seed round deals of <$500K (Canada) or <$1M (US)

• Used in about 50% of angel funding

Copyright, David J. Litwiller 2013 34

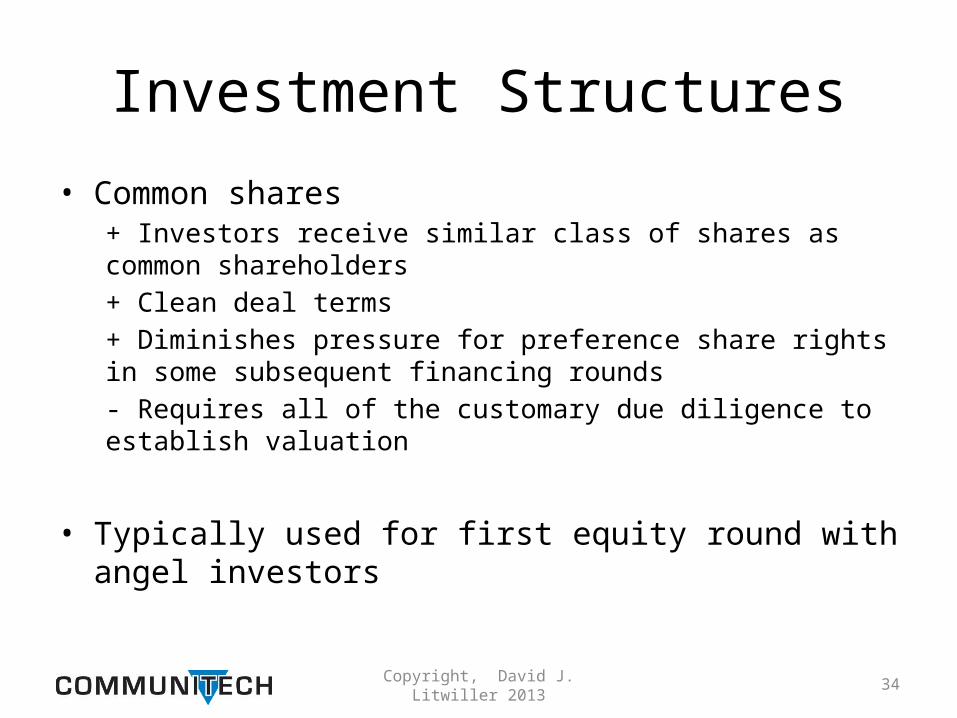

Investment Structures

• Common shares+ Investors receive similar class of shares as common shareholders+ Clean deal terms+ Diminishes pressure for preference share rights in some subsequent financing rounds- Requires all of the customary due diligence to establish valuation

• Typically used for first equity round with angel investors

Copyright, David J. Litwiller 2013 35

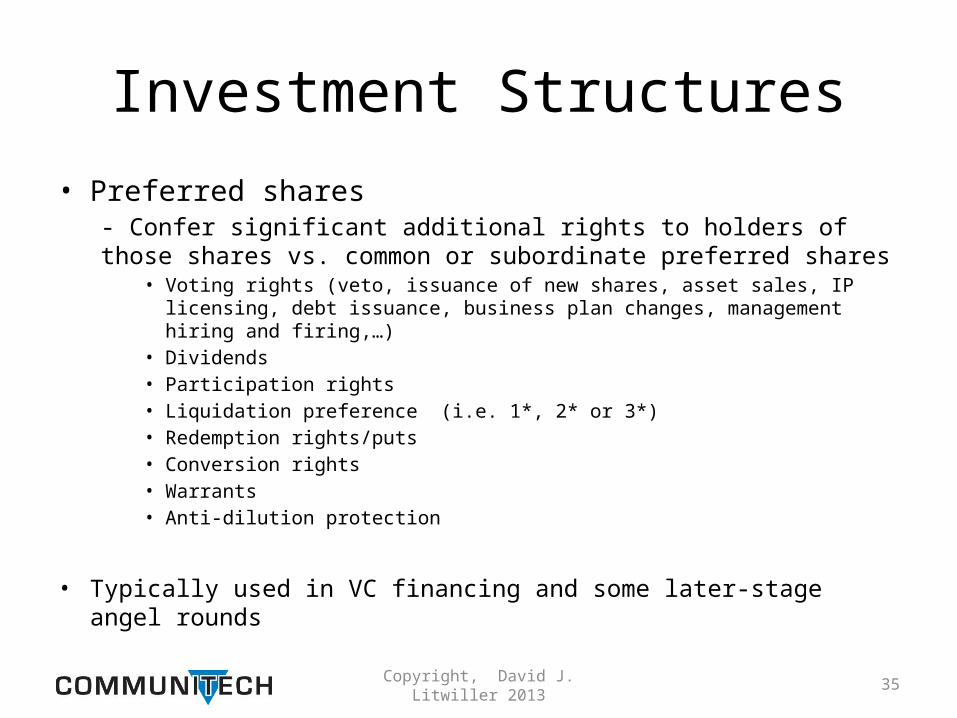

Investment Structures

• Preferred shares- Confer significant additional rights to holders of those shares vs. common or subordinate preferred shares

• Voting rights (veto, issuance of new shares, asset sales, IP licensing, debt issuance, business plan changes, management hiring and firing,…)

• Dividends• Participation rights• Liquidation preference (i.e. 1*, 2* or 3*)• Redemption rights/puts• Conversion rights• Warrants• Anti-dilution protection

• Typically used in VC financing and some later-stage angel rounds

Copyright, David J. Litwiller 2013 36

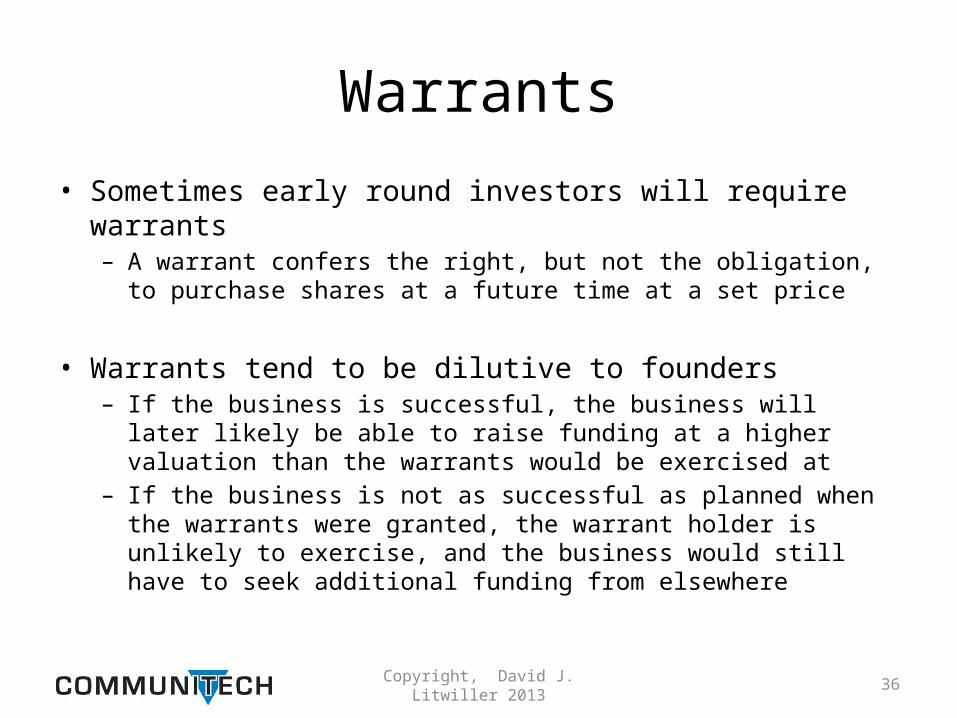

Warrants

• Sometimes early round investors will require warrants– A warrant confers the right, but not the obligation, to purchase shares

at a future time at a set price

• Warrants tend to be dilutive to founders– If the business is successful, the business will later likely be able to

raise funding at a higher valuation than the warrants would be exercised at

– If the business is not as successful as planned when the warrants were granted, the warrant holder is unlikely to exercise, and the business would still have to seek additional funding from elsewhere

Copyright, David J. Litwiller 2013 37

Deal Sweeteners

• Know what additional matching and non-dilutive funding is available, such as IRAP, OCE, FedDev, TecTerra, IDF, OPA, and SDTC

• Private investors generally like seeing that their investment will play somewhat bigger through these amplification instruments than the direct amount they invest

• But, be careful to preserve full access to SR&ED and Digital Media Tax Credits, as they are the cheapest form of capital

Copyright, David J. Litwiller 2013 38

Critical Term Sheet Mistakes to Avoid

• Granting early investors a rights of first refusal on future financing rounds– Scares away new downstream investors– They would face the prospect of doing all of the due diligence, and

then having the deal be scooped by the earlier round investors– Shows lack of deal savvy by the entrepreneur, and poor start-up

acumen generally

• Veto rights over future fundraising– Gives early investors de facto exclusivity for supplying future capital, if

they want it– Similar issues as the RoFR above

Copyright, David J. Litwiller 2013 39

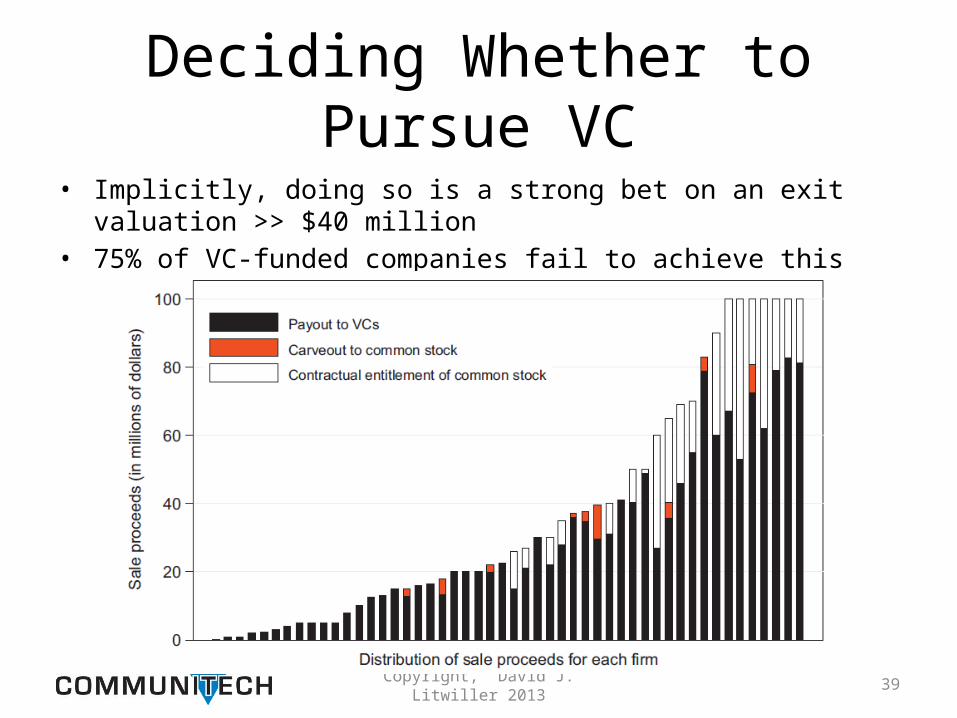

Deciding Whether to Pursue VC• Implicitly, doing so is a strong bet on an exit valuation >> $40 million• 75% of VC-funded companies fail to achieve this

Copyright, David J. Litwiller 2013 40

Your Best Tools

• Competition for the deal– Multiple, motivated investors, all independently interested in

investing– VC Q: Who else are you talking to? Ans: All the usual culprits. Period.

• A deadline driven by a likely near-term event which will further drive up valuation or investment interest

• Confidence, tempered by enough humility to learn very quickly

• High quality, larger in-sector partners with significant bilateral operational interaction

Copyright, David J. Litwiller 2013 41

Your Best Tools

• Salesmanship and negotiating skill– Leaving no one in doubt that you can do all the other

things needed to build a great business: attract customers, partners, key future hires, strategic suppliers, future funders, etc.

• Make investors feel smart, cool and sexy for getting into your deal

• Execute relentlessly

Copyright, David J. Litwiller 2013 42

In Closing

• One thing to remember:

– A funding model is not a business model

– Spend more time with customers and driving revenue than you do with candidate funders

Copyright, David J. Litwiller 2013 43

In Closing

• And a second thing:

– The way to attract the best funders is to show them that you don’t need them

– One way is through competition for the deal

– Others are through gross margin, working capital, non-dilutive funding, and resisting premature scaling to defer the need for equity or venture debt financing and improve your negotiating position

Copyright, David J. Litwiller 2013 44

References“Cash, Connections and Chemistry”, Litwiller, 2011http://www.slideshare.net/davidjl/cash-connections-and-chemistry-angel-investment-in-early-stage-technology-ventures-feb-2011-dave-litwiller-final

“High Tech Start Up”, Nesheim, Free Press, 2000 http://www.nesheimgroup.com/books

“Renegotiation of Cash Flow Rights in the Sale of VC-backed firms”, Broughman and Fried, Journal of Financial Economics, Elsevier, 2009http://leeds-faculty.colorado.edu/bhagat/RenegotiationCashFlowRightsVC.pdf

“Term Sheet Series”, Feld et al, 2005-2008http://www.feld.com/wp/archives/2008/06/revisiting-the-term-sheet.html

“Venture Capital and the Finance of Innovation”, 2nd Ed., Metrick et al, Wiley, 2010http://www.stpia.ir/files/Venture%20Capital%20and%20Finance%20of%20Innovatoin.pdf

Copyright, David J. Litwiller 2013 45

Questions?

© David J. Litwiller, 2013 46

Follow-up Discussion

Contact:

dave [dot] litwiller [at] communitech.ca

![[Preston, 2007] Angel Financing for Entrepreneurs - Early-Stage Funding for Long-Term Success](https://img.pdfslide.us/doc/110x75/55cf883f55034664618ee110/preston-2007-angel-financing-for-entrepreneurs-early-stage-funding-for.jpg)