Embed Size (px)

DESCRIPTION

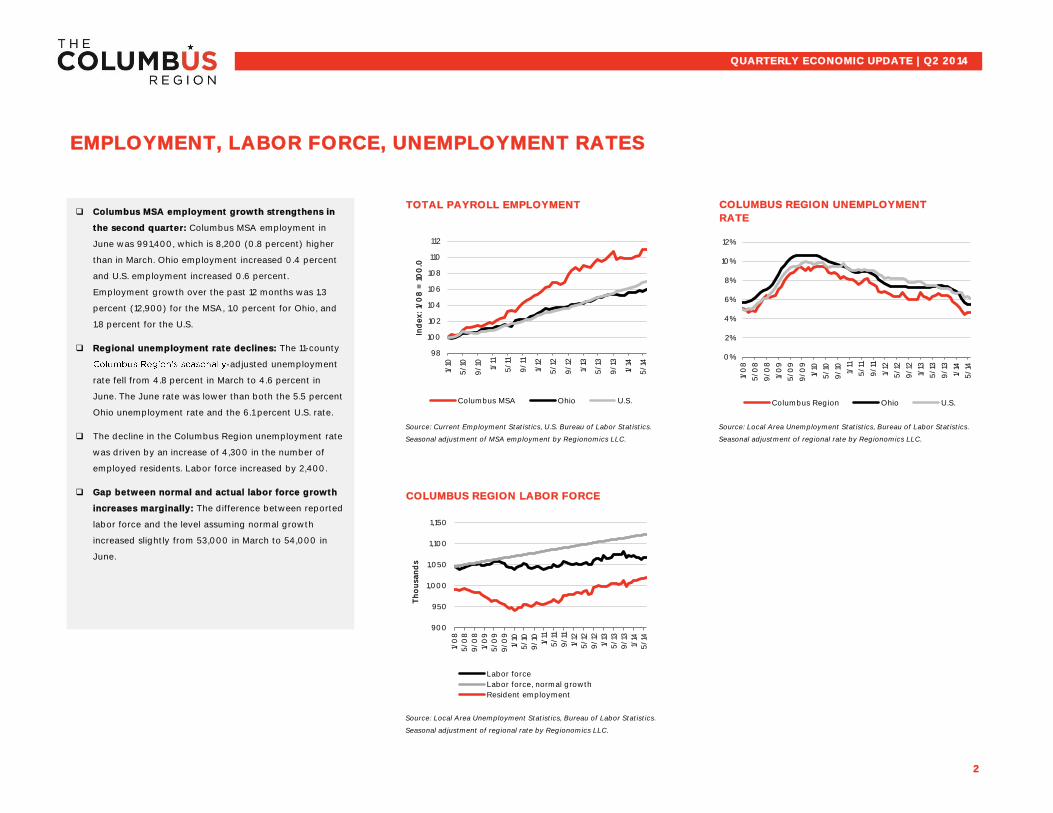

Columbus MSA employment was up 8,200 (0.8 percent) from March to June, ahead of Ohio’s increase of 0.4 percent and the U.S. increase of 0.6 percent, according to the Q2 economic update report produced by Columbus 2020. Going into the second half of the year, unemployment in the Columbus Region continued to decline at 4.6 percent, compared to June state and national rates of 5.5 and 6.1, respectively.

Citation preview

QUARTERLY ECONOMIC

UPDATEQ2 2014

columbusregion.com 614-225-6063

TABLE OF CONTENTS

Employment, labor force and unemployment . . . . . . . . . . . .2

Employment by industry. . . . . . . . . . . . . . . . . . . . . . . . . 3

County employment . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Commercial real estate . . . . . . . . . . . . . . . . . . . . . . . . . . . . .7

Airport passengers and cargo . . . . . . . . . . . . . . . . . . . . . 7

Housing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

GDP and inflation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Columbus 2020 performance. . . . . . . . . . . . . . . . . . . . . . 11

Notable expansions and locations . . . . . . . . . . . . . . . . . . 13

1

QUARTERLY ECONOMIC UPDATE | Q2 2014

The Columbus 2020 economic update for the

second quarter of 2014 covers regional

economic data and economic development

activities from April to June. The analysis of the

regional economy (pages 2 to 10) was prepared

by Bill LaFayette, Ph.D., RegionomicsTM LLC.

FOREWORD By G. Scott McComb President and CEO, Heartland Bank

The Columbus Region did very well in the second quarter of 2014 and continues to lead much of the nation into the economic recovery. Reasons for this economic improvement are multi-fold: The Columbus Region has a diverse employment base consisting of government,

financial, insurance, and private enterprises. These employers have been able to recover more quickly from the recession, although growth in the coming quarters will most likely be in the manufacturing sector.

The Columbus Region is home to more than 60 college and university campuses, and the emphasis on getting a college education is more prevalent than ever. Due to

staying after graduation to call Central Ohio home.

Services continue to expand across the Region commensurate with job growth, out of market investment, and spin-off income from mineral rights due to the hydraulic fracturing in eastern Ohio.

Government gets things done in Ohio, and our state is among the most financially well managed in the union. While a good deal of the country is in gridlock, Ohio has once again opened the door to business. Ohio has made major investments in infrastructure that will benefit the state and the Columbus Region in the future.

Regional efforts like Columbus 2020 have performed "gap closing" techniques to get projects across the finish line, and to showcase the viability and desirability of the Region to the world.

The Columbus Region has a propensity to buy local. The expansion of many Central Ohio based companies across several industries is evidence that keeping dollars circulating within the same economy is a core strength of our region. Every dollar spent with a locally based company is the equivalent of $8 spent with national firms not based in the Region.

The second quarter was strong for the Columbus Region and I remain bullish on our prospects for the rest of 2014 and beyond.

TOTAL PAYROLL EMPLOYMENT

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics. Source: Local Area Unemployment Statistics, Bureau of Labor Statistics.

Seasonal adjustment of MSA employment by Regionomics LLC. Seasonal adjustment of regional rate by Regionomics LLC.

COLUMBUS REGION LABOR FORCE

Source: Local Area Unemployment Statistics, Bureau of Labor Statistics.

Seasonal adjustment of regional rate by Regionomics LLC.

2

QUARTERLY ECONOMIC UPDATE | Q2 2014

EMPLOYMENT, LABOR FORCE, UNEMPLOYMENT RATES

COLUMBUS REGION UNEMPLOYMENT

RATE Columbus MSA employment growth strengthens in

the second quarter: Columbus MSA employment in

June was 991,400, which is 8,200 (0.8 percent) higher

than in March. Ohio employment increased 0.4 percent

and U.S. employment increased 0.6 percent.

Employment growth over the past 12 months was 1.3

percent (12,900) for the MSA, 1.0 percent for Ohio, and

1.8 percent for the U.S.

Regional unemployment rate declines: The 11-county

-adjusted unemployment

rate fell from 4.8 percent in March to 4.6 percent in

June. The June rate was lower than both the 5.5 percent

Ohio unemployment rate and the 6.1 percent U.S. rate.

The decline in the Columbus Region unemployment rate

was driven by an increase of 4,300 in the number of

employed residents. Labor force increased by 2,400.

Gap between normal and actual labor force growth

increases marginally: The difference between reported

labor force and the level assuming normal growth

increased slightly from 53,000 in March to 54,000 in

June.

98

100

102

104

106

108

110

112

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

0%

2%

4%

6%

8%

10%

12%

1/0

8

5/0

8

9/0

8

1/0

9

5/0

9

9/0

9

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Columbus Region Ohio U.S.

900

950

1,000

1,050

1,100

1,150

1/0

8

5/0

8

9/0

8

1/0

9

5/0

9

9/0

9

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Th

ou

san

ds

Labor force

Labor force, normal growth

Resident employment

MANUFACTURING

*Excluding computer design and related services.

PROFESSIONAL & BUSINESS SERVICES COMPUTER DESIGN & RELATED SERVICES FINANCE & INSURANCE

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics.

Seasonal adjustment of MSA employment by Regionomics LLC.

3

QUARTERLY ECONOMIC UPDATE | Q2 2014

EMPLOYMENT BY INDUSTRY

LOGISTICS: TRANSPORTATION,

WAREHOUSING & WHOLESALE

MSA SHARE OF EMPLOYMENT BY INDUSTRY, JUNE

2014

Logistics 8.5% Manufacturing

7.0%

Professional & business svcs*

15.1%

Computer design &

related svcs 1.8%

Finance & insurance

6.1% Healthcare & social

assistance 12.3%

Leisure & hospitality

10.1%

Government 16.4%

Retail trade 10.2%

Other 12.6%

96

98

100

102

104

106

108

110

112

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

98

100

102

104

106

108

110

112

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

95

100

105

110

115

120

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex:

1/0

8 =

10

0.0

Columbus MSA Ohio U.S.

98

100

102

104

106

108

110

112

114

116

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

95

100

105

110

115

120

125

130

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

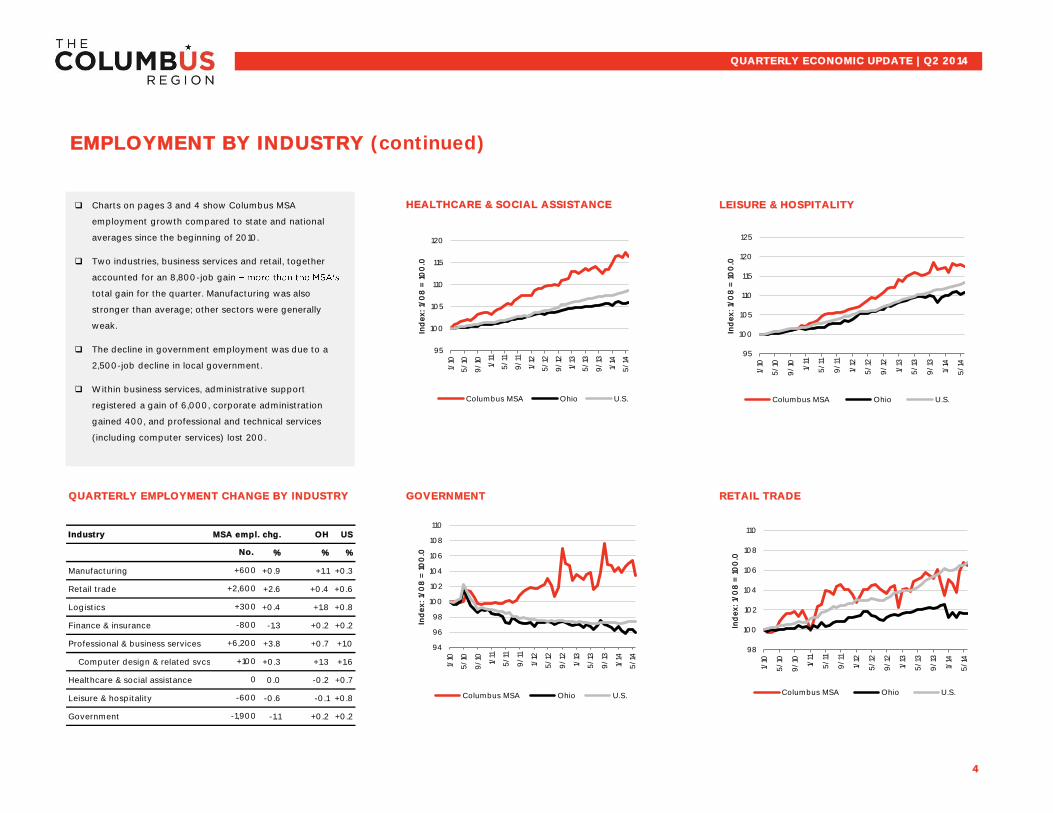

LEISURE & HOSPITALITY

QUARTERLY EMPLOYMENT CHANGE BY INDUSTRY GOVERNMENT RETAIL TRADE

Industry MSA empl. chg. OH US

% % %

Manufacturing +0.9 +1.1 +0.3

Retail trade +2.6 +0.4 +0.6

Logistics +0.4 +1.8 +0.8

Finance & insurance -1.3 +0.2 +0.2

Professional & business services +3.8 +0.7 +1.0

Computer design & related svcs. +0.3 +1.3 +1.6

Healthcare & social assistance 0.0 -0.2 +0.7

Leisure & hospitality -0.6 -0.1 +0.8

Government -1.1 +0.2 +0.2

4

-1,900

0

+6,200

-600

HEALTHCARE & SOCIAL ASSISTANCE

QUARTERLY ECONOMIC UPDATE | Q2 2014

EMPLOYMENT BY INDUSTRY (continued)

+100

-800

+2,600

No.

+300

+600

Charts on pages 3 and 4 show Columbus MSA

employment growth compared to state and national

averages since the beginning of 2010.

Two industries, business services and retail, together

accounted for an 8,800-job gain

total gain for the quarter. Manufacturing was also

stronger than average; other sectors were generally

weak.

The decline in government employment was due to a

2,500-job decline in local government.

Within business services, administrative support

registered a gain of 6,000, corporate administration

gained 400, and professional and technical services

(including computer services) lost 200.

95

100

105

110

115

120

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

95

100

105

110

115

120

125

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex:

1/0

8 =

10

0.0

Columbus MSA Ohio U.S.

94

96

98

100

102

104

106

108

110

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex:

1/0

8 =

10

0.0

Columbus MSA Ohio U.S.

98

100

102

104

106

108

110

1/10

5/1

0

9/10

1/11

5/1

1

9/11

1/12

5/1

2

9/12

1/13

5/1

3

9/13

1/14

5/1

4

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio U.S.

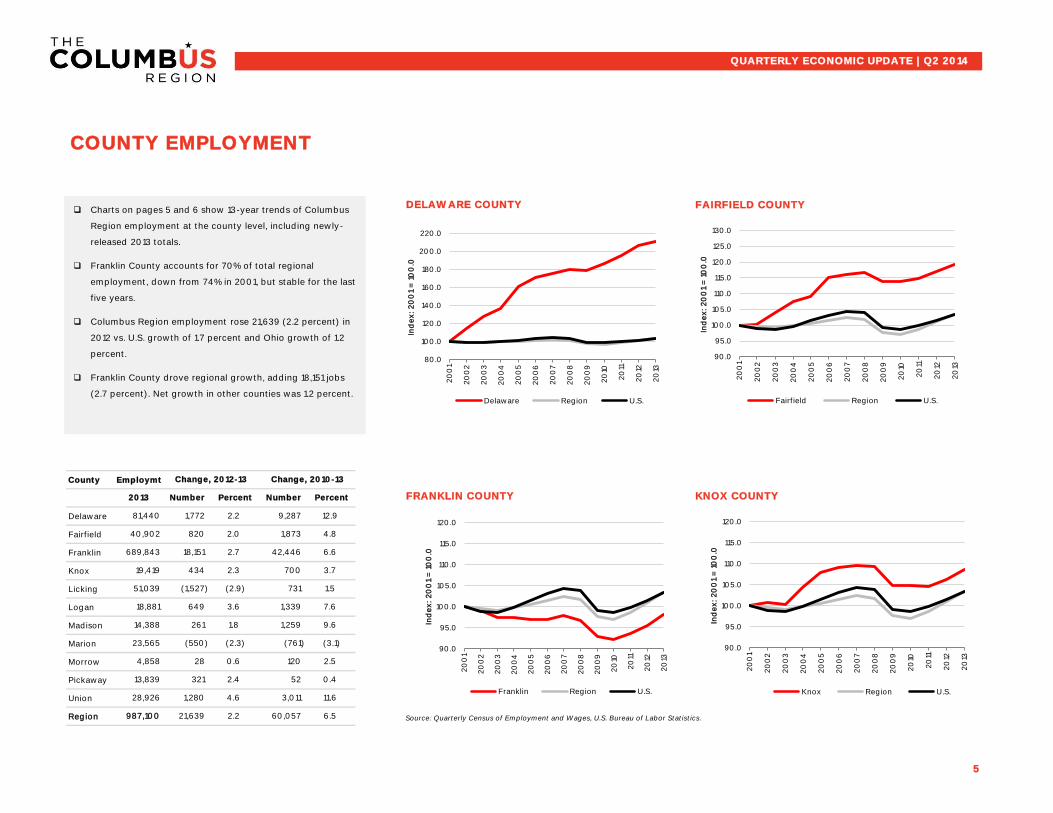

FAIRFIELD COUNTY

County Employmt.

FRANKLIN COUNTY KNOX COUNTY

Delaware

Fairfield

Franklin

Knox

Licking

Logan

Madison

Marion

Morrow

Pickaway

Union

Region Source: Quarterly Census of Employment and Wages, U.S. Bureau of Labor Statistics.

5

Change, 2010-13Change, 2012-13

Percent

12.9

4.8

6.6

3.7

(2.3)

2013 Number

81,440 1,772 9,287

40,902 820 1,873

Number

2.0

2.7

2.3

(2.9)

3.6

13,839 321 52

261 1,259

1,339

1.8

51,039 (1,527) 731

18,881 649

1.5

28,926 1,280 3,011

987,100 21,639 60,057

23,565

9.6

Percent

2.2

42,446

14,388

4,858 28 1200.6

2.2 6.5

(550) (761)

2.4

4.6

(3.1)

2.5

0.4

11.6

7.6

COUNTY EMPLOYMENT

DELAWARE COUNTY

QUARTERLY ECONOMIC UPDATE | Q2 2014

689,843 18,151

19,419 434 700

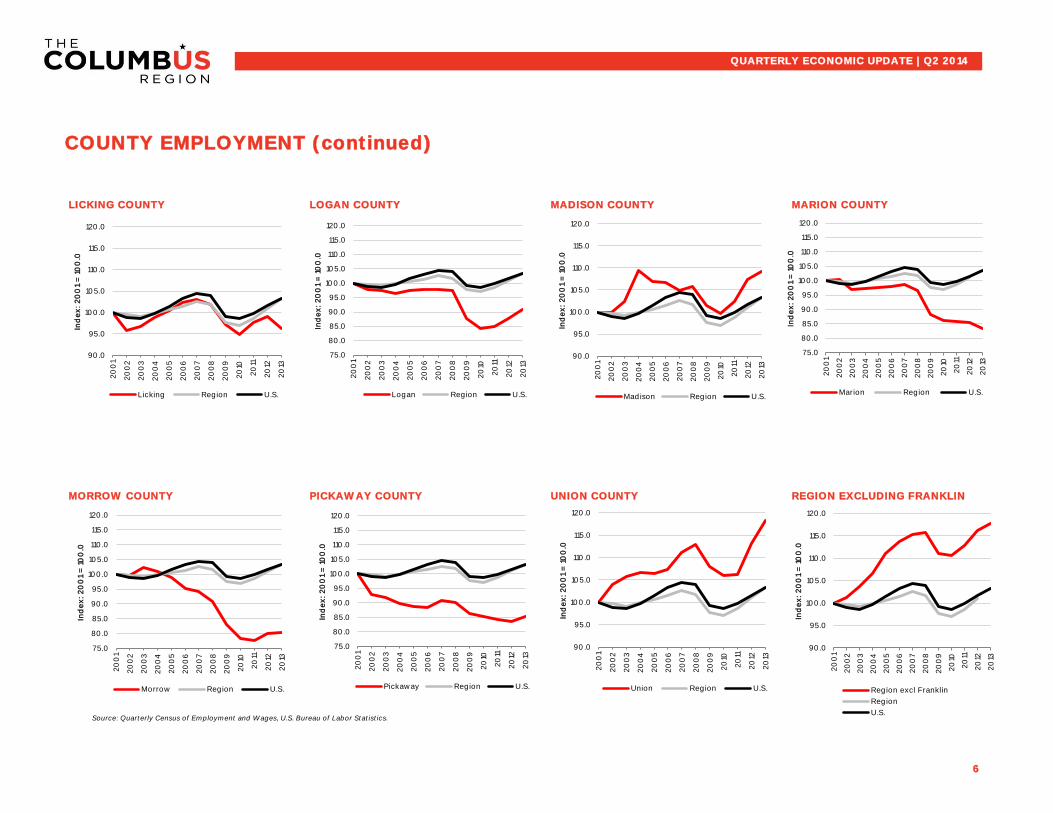

Charts on pages 5 and 6 show 13-year trends of Columbus

Region employment at the county level, including newly-

released 2013 totals.

Franklin County accounts for 70% of total regional

employment, down from 74% in 2001, but stable for the last

five years.

Columbus Region employment rose 21,639 (2.2 percent) in

2012 vs. U.S. growth of 1.7 percent and Ohio growth of 1.2

percent.

Franklin County drove regional growth, adding 18,151 jobs

(2.7 percent). Net growth in other counties was 1.2 percent.

80.0

100.0

120.0

140.0

160.0

180.0

200.0

220.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Delaware Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0

130.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Fairfield Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Franklin Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Knox Region U.S.

LICKING COUNTY LOGAN COUNTY MADISON COUNTY MARION COUNTY

EDUCATION & HEALTH SERVICESMORROW COUNTY PICKAWAY COUNTY UNION COUNTY REGION EXCLUDING FRANKLIN

Source: Quarterly Census of Employment and Wages, U.S. Bureau of Labor Statistics.

6

QUARTERLY ECONOMIC UPDATE | Q2 2014

COUNTY EMPLOYMENT (continued)

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Licking Region U.S.

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Logan Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex:

20

01

= 1

00

.0

Madison Region U.S.

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Marion Region U.S.

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Morrow Region U.S.

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Pickaway Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex: 2

00

1 =

10

0.0

Union Region U.S.

90.0

95.0

100.0

105.0

110.0

115.0

120.0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

Ind

ex:

20

01

= 1

00

.0

Region excl Franklin

Region

U.S.

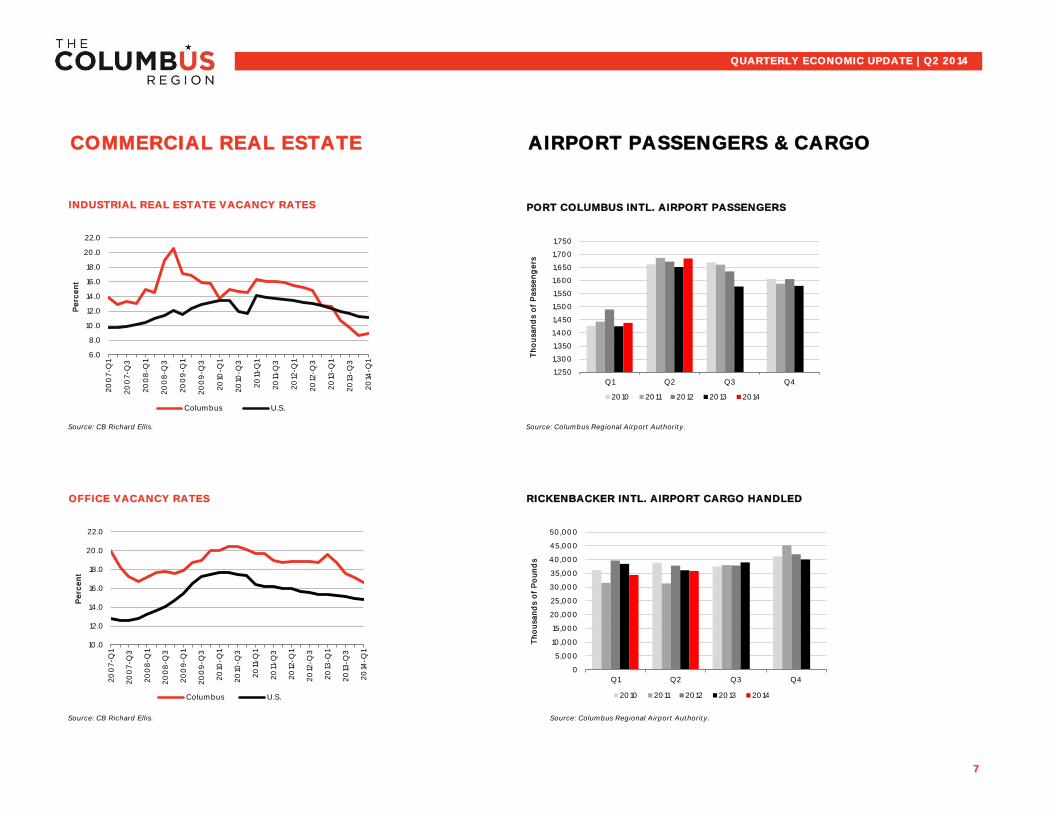

INDUSTRIAL REAL ESTATE VACANCY RATES PORT COLUMBUS INTL. AIRPORT PASSENGERS

Source: CB Richard Ellis. Source: Columbus Regional Airport Authority.

OFFICE VACANCY RATES RICKENBACKER INTL. AIRPORT CARGO HANDLED

Source: CB Richard Ellis. Source: Columbus Regional Airport Authority.

7

AIRPORT PASSENGERS & CARGOCOMMERCIAL REAL ESTATE

QUARTERLY ECONOMIC UPDATE | Q2 2014

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

22.0

20

07-Q

1

20

07-Q

3

20

08

-Q1

20

08

-Q3

20

09

-Q1

20

09

-Q3

20

10-Q

1

20

10-Q

3

20

11-Q

1

20

11-Q

3

20

12-Q

1

20

12-Q

3

20

13-Q

1

20

13-Q

3

20

14-Q

1

Pe

rce

nt

Columbus U.S.

1,250

1,300

1,350

1,400

1,450

1,500

1,550

1,600

1,650

1,700

1,750

Q1 Q2 Q3 Q4

Th

ou

san

ds o

f P

asse

ng

ers

2010 2011 2012 2013 2014

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

Q1 Q2 Q3 Q4

Th

ou

san

ds o

f P

ou

nd

s

2010 2011 2012 2013 2014

10.0

12.0

14.0

16.0

18.0

20.0

22.0

20

07-Q

1

20

07-Q

3

20

08

-Q1

20

08

-Q3

20

09

-Q1

20

09

-Q3

20

10-Q

1

20

10-Q

3

20

11-Q

1

20

11-Q

3

20

12-Q

1

20

12-Q

3

20

13-Q

1

20

13-Q

3

20

14-Q

1

Pe

rce

nt

Columbus U.S.

Source: U.S. Census Bureau. Source: Columbus Board of Realtors.

CHANGE IN RESIDENTIAL SALES FROM SAME QUARTER PREVIOUS YEAR

Source: Columbus Board of Realtors, National Association of Realtors.

8

RESIDENTIAL SALES, COLUMBUS MLS

AREA

RESIDENTIAL BUILDING PERMITS,

COLUMBUS MSA

QUARTERLY ECONOMIC UPDATE | Q2 2014

HOUSING

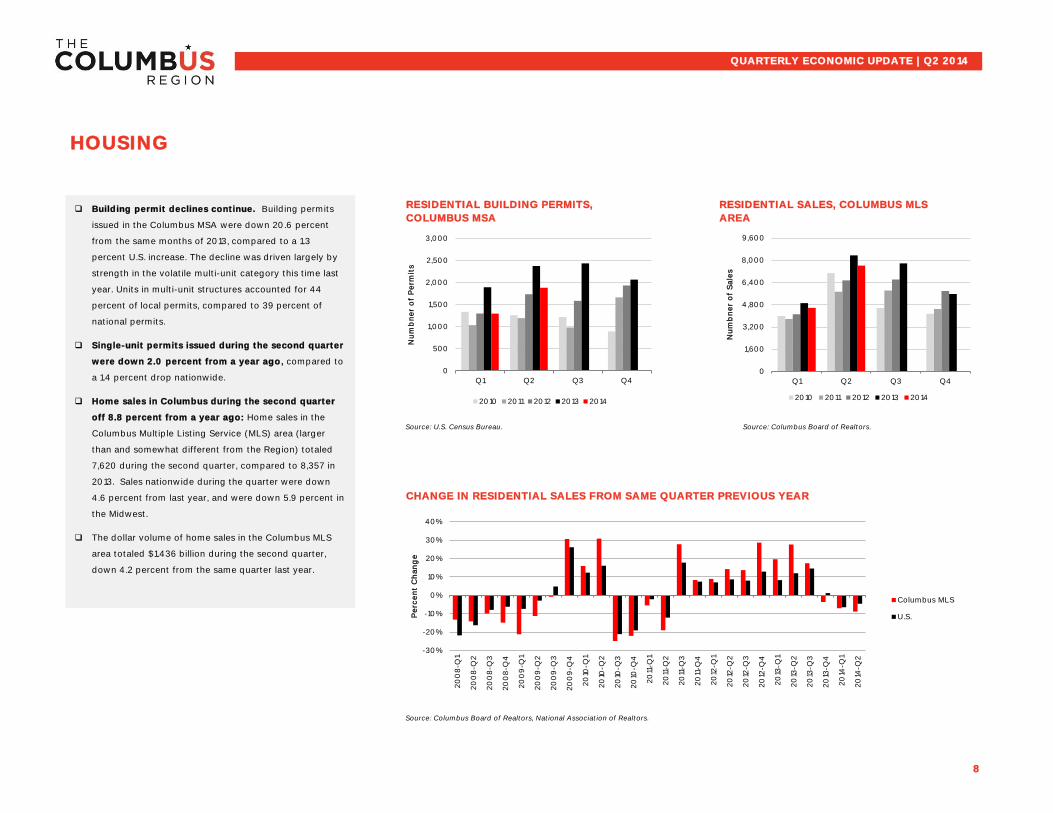

Building permit declines continue. Building permits

issued in the Columbus MSA were down 20.6 percent

from the same months of 2013, compared to a 1.3

percent U.S. increase. The decline was driven largely by

strength in the volatile multi-unit category this time last

year. Units in multi-unit structures accounted for 44

percent of local permits, compared to 39 percent of

national permits.

Single-unit permits issued during the second quarter

were down 2.0 percent from a year ago, compared to

a 1.4 percent drop nationwide.

Home sales in Columbus during the second quarter

off 8.8 percent from a year ago: Home sales in the

Columbus Multiple Listing Service (MLS) area (larger

than and somewhat different from the Region) totaled

7,620 during the second quarter, compared to 8,357 in

2013. Sales nationwide during the quarter were down

4.6 percent from last year, and were down 5.9 percent in

the Midwest.

The dollar volume of home sales in the Columbus MLS

area totaled $1.436 billion during the second quarter,

down 4.2 percent from the same quarter last year.

0

500

1,000

1,500

2,000

2,500

3,000

Q1 Q2 Q3 Q4

Nu

mb

ne

r o

f P

erm

its

2010 2011 2012 2013 2014

0

1,600

3,200

4,800

6,400

8,000

9,600

Q1 Q2 Q3 Q4

Nu

mb

ne

r o

f S

ale

s

2010 2011 2012 2013 2014

-30%

-20%

-10%

0%

10%

20%

30%

40%

20

08

-Q1

20

08

-Q2

20

08

-Q3

20

08

-Q4

20

09

-Q1

20

09

-Q2

20

09

-Q3

20

09

-Q4

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

20

12-Q

2

20

12-Q

3

20

12-Q

4

20

13-Q

1

20

13-Q

2

20

13-Q

3

20

13-Q

4

20

14-Q

1

20

14-Q

2

Pe

rce

nt

Ch

an

ge

Columbus MLS

U.S.

MSA HOUSE PRICE CHANGE, 1ST QUARTER 2007 TO 1ST QUARTER 2014

MSA HOUSE PRICE CHANGE, 2ND QUARTER 2011 TO 1ST QUARTER 2014

Source: Federal Housing Finance Agency House Price Index.

9

QUARTERLY ECONOMIC UPDATE | Q2 2014

HOUSING (continued)

FHFA HOUSE PRICE INDEX, 1ST QUARTER 2007 -

1ST QUARTER 2014

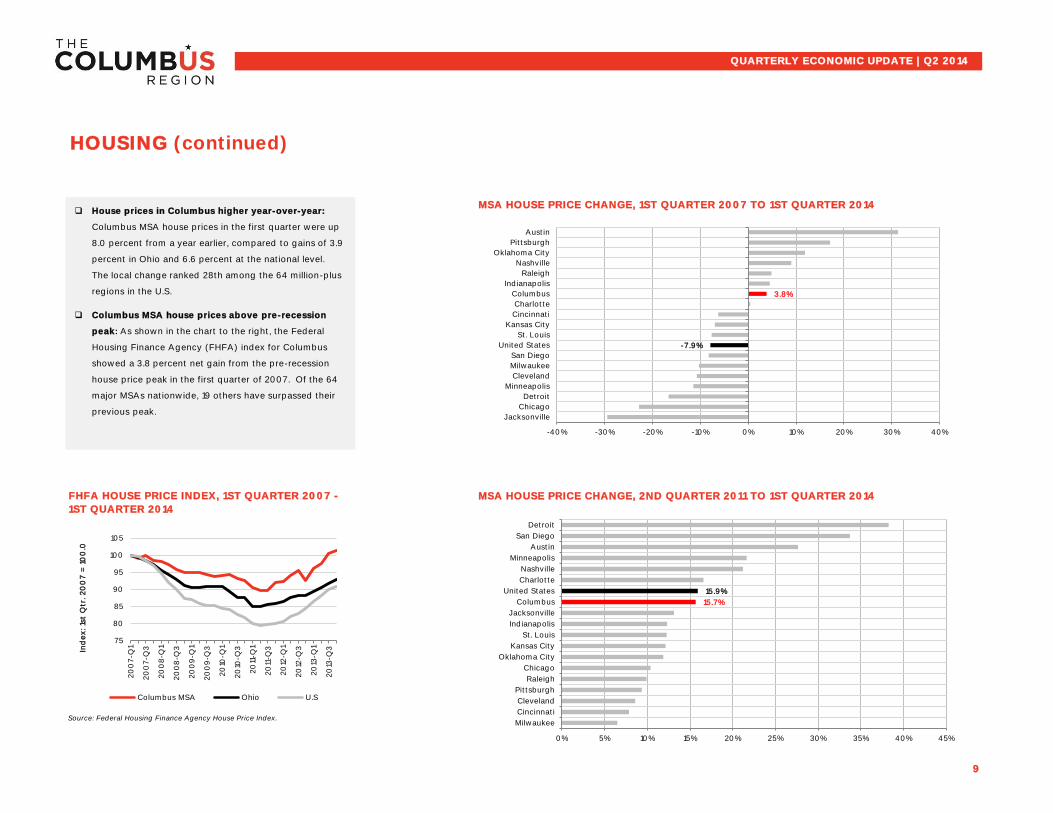

House prices in Columbus higher year-over-year:

Columbus MSA house prices in the first quarter were up

8.0 percent from a year earlier, compared to gains of 3.9

percent in Ohio and 6.6 percent at the national level.

The local change ranked 28th among the 64 million-plus

regions in the U.S.

Columbus MSA house prices above pre-recession

peak: As shown in the chart to the right, the Federal

Housing Finance Agency (FHFA) index for Columbus

showed a 3.8 percent net gain from the pre-recession

house price peak in the first quarter of 2007. Of the 64

major MSAs nationwide, 19 others have surpassed their

previous peak.

-7.9%

3.8%

-40% -30% -20% -10% 0% 10% 20% 30% 40%

Jacksonville

Chicago

Detroit

Minneapolis

Cleveland

Milwaukee

San Diego

United States

St. Louis

Kansas City

Cincinnati

Charlotte

Columbus

Indianapolis

Raleigh

Nashville

Oklahoma City

Pittsburgh

Austin

15.7%

15.9%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Milwaukee

Cincinnati

Cleveland

Pittsburgh

Raleigh

Chicago

Oklahoma City

Kansas City

St. Louis

Indianapolis

Jacksonville

Columbus

United States

Charlotte

Nashville

Minneapolis

Austin

San Diego

Detroit

75

80

85

90

95

100

105

20

07-Q

1

20

07-Q

3

20

08

-Q1

20

08

-Q3

20

09

-Q1

20

09

-Q3

20

10-Q

1

20

10-Q

3

20

11-Q

1

20

11-Q

3

20

12-Q

1

20

12-Q

3

20

13-Q

1

20

13-Q

3Ind

ex: 1s

t Q

tr. 2

00

7 =

10

0.0

Columbus MSA Ohio U.S

HISTORIC AND FORECAST U.S. GDP; HISTORIC PERSONAL CONSUMPTION

Source: U.S. Bureau of Economic Analysis, Wall Street Journal Economic Forecasting Survey.

CPI INFLATION, LARGE MIDWEST CITIES

Source: Consumer Price Index (CPI-U), U.S. Bureau of Labor Statistics

10

QUARTERLY ECONOMIC UPDATE | Q2 2014

GDP AND INFLATION

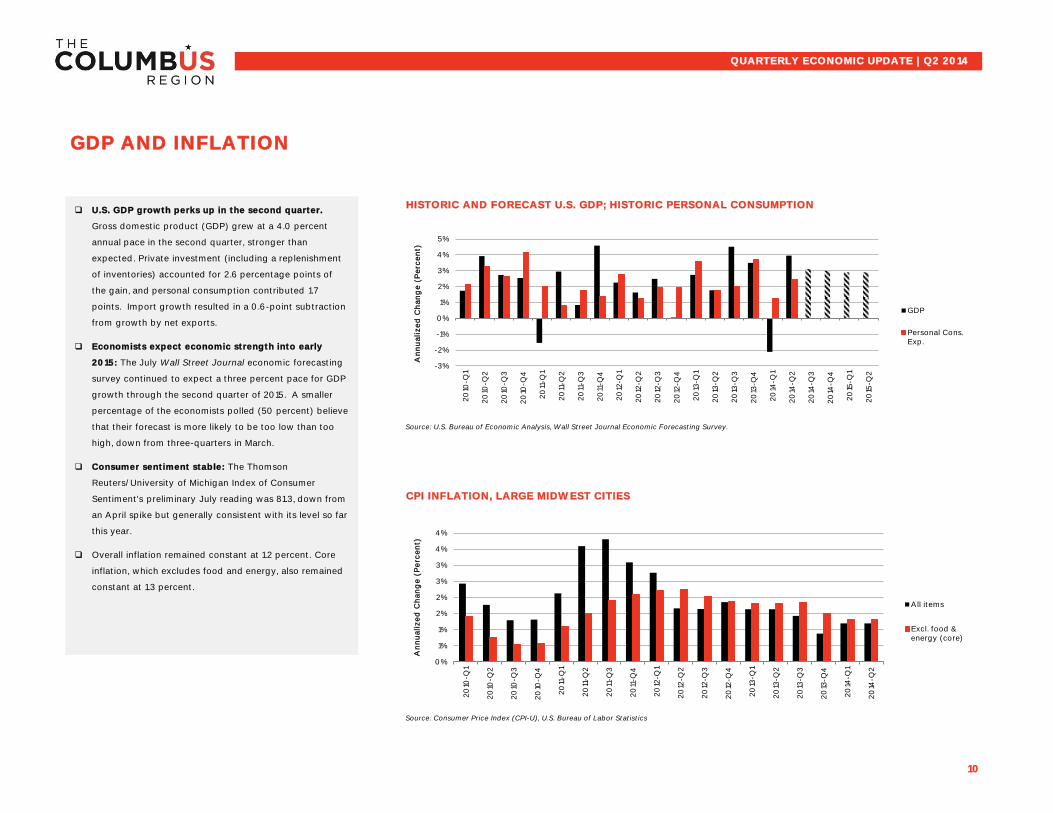

U.S. GDP growth perks up in the second quarter.

Gross domestic product (GDP) grew at a 4.0 percent

annual pace in the second quarter, stronger than

expected. Private investment (including a replenishment

of inventories) accounted for 2.6 percentage points of

the gain, and personal consumption contributed 1.7

points. Import growth resulted in a 0.6-point subtraction

from growth by net exports.

Economists expect economic strength into early

2015: The July Wall Street Journal economic forecasting

survey continued to expect a three percent pace for GDP

growth through the second quarter of 2015. A smaller

percentage of the economists polled (50 percent) believe

that their forecast is more likely to be too low than too

high, down from three-quarters in March.

Consumer sentiment stable: The Thomson

Reuters/University of Michigan Index of Consumer

Sentiment's preliminary July reading was 81.3, down from

an April spike but generally consistent with its level so far

this year.

Overall inflation remained constant at 1.2 percent. Core

inflation, which excludes food and energy, also remained

constant at 1.3 percent.

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

20

12-Q

2

20

12-Q

3

20

12-Q

4

20

13-Q

1

20

13-Q

2

20

13-Q

3

20

13-Q

4

20

14-Q

1

20

14-Q

2

20

14-Q

3

20

14-Q

4

20

15-Q

1

20

15-Q

2

An

nu

alize

d C

han

ge

(P

erc

en

t)

GDP

Personal Cons.Exp.

0%

1%

1%

2%

2%

3%

3%

4%

4%

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

20

12-Q

2

20

12-Q

3

20

12-Q

4

20

13-Q

1

20

13-Q

2

20

13-Q

3

20

13-Q

4

20

14-Q

1

20

14-Q

2

An

nu

alize

d C

han

ge

(P

erc

en

t)

All items

Excl. food &energy (core)

PROJECTS ACTIVE AT END OF EACH MONTH

11

PROJECTS ACTIVE AT END OF EACH MONTH

BY SECTOR

NUMBER OF PROJECTS STARTED

(2013 v. 2014)

FIRST-TIME VISITS (2013 v. 2014)

QUARTERLY ECONOMIC UPDATE | Q2 2014

COLUMBUS 2020 PERFORMANCE | PROJECTS JAN-JUN 2014

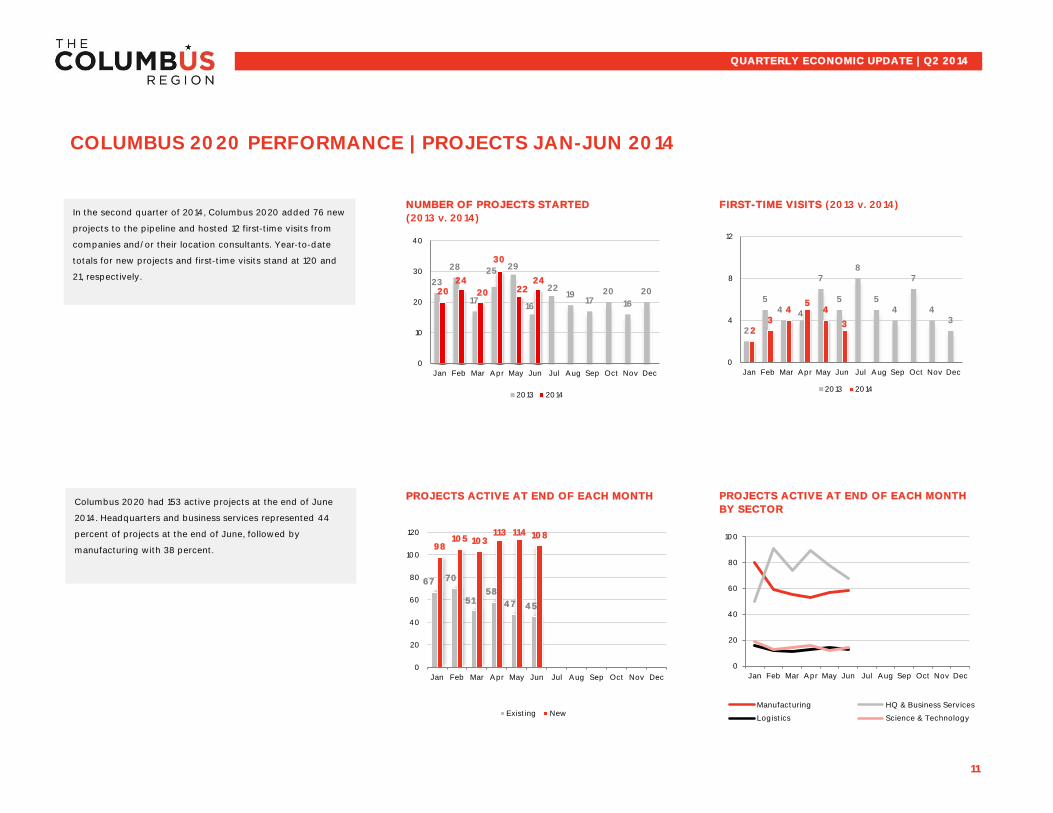

In the second quarter of 2014, Columbus 2020 added 76 new

projects to the pipeline and hosted 12 first-time visits from

companies and/or their location consultants. Year-to-date

totals for new projects and first-time visits stand at 120 and

21, respectively.

Columbus 2020 had 153 active projects at the end of June

2014. Headquarters and business services represented 44

percent of projects at the end of June, followed by

manufacturing with 38 percent.

67 70

51 58

47 45

98 105 103

113 114 108

0

20

40

60

80

100

120

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Existing New

0

20

40

60

80

100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Manufacturing HQ & Business Services

Logistics Science & Technology

23

28

17

25 29

16

22 19

17 20

16

20 20 24

20

30

22 24

0

10

20

30

40

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2

5 4 4

7

5

8

5 4

7

4 3

2 3

4 5

4

3

0

4

8

12

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014

2014 Q3 PLANNED ACTIVITIES

12

EXISTING BUSINESS VISITS CONDUCTED BY

SECTOR

EXISTING BUSINESS VISITS CONDUCTED BY PLACE

QUARTERLY ECONOMIC UPDATE | Q2 2014

2014 Q2 COMPLETED ACTIVITIES

COLUMBUS 2020 PERFORMANCE | DEVELOPMENT ACTIVITIES JAN-JUN 2014

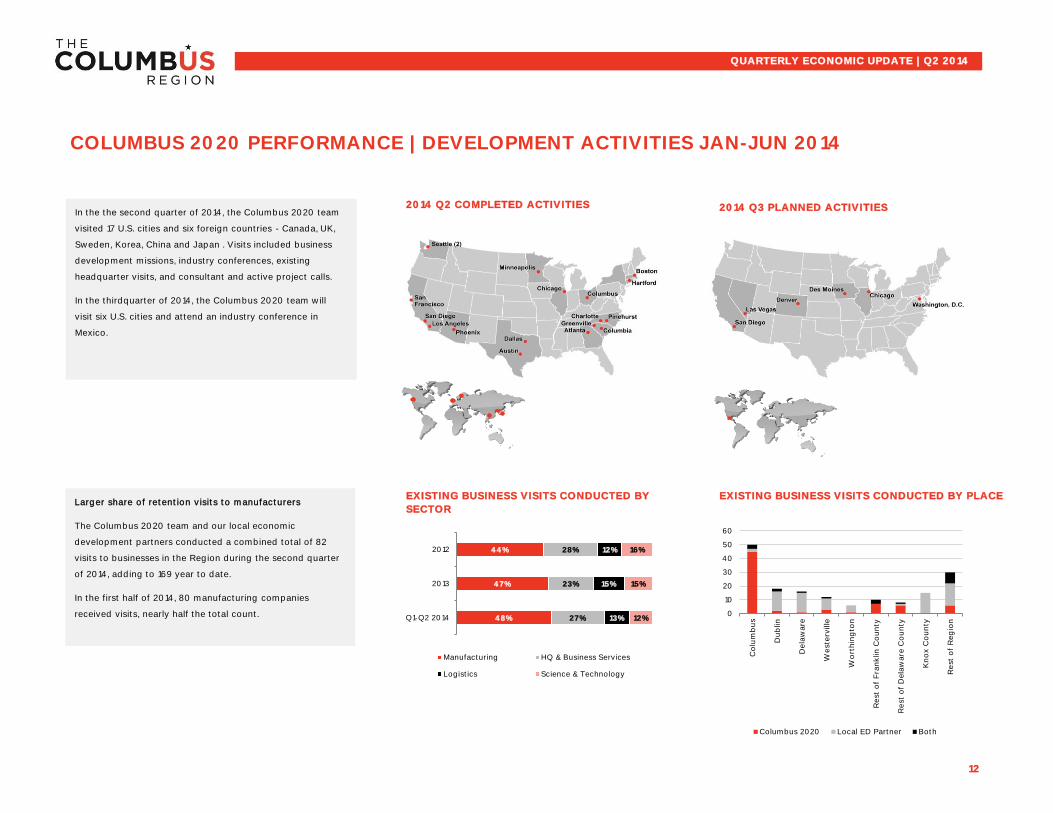

In the the second quarter of 2014, the Columbus 2020 team

visited 17 U.S. cities and six foreign countries - Canada, UK,

Sweden, Korea, China and Japan . Visits included business

development missions, industry conferences, existing

headquarter visits, and consultant and active project calls.

In the thirdquarter of 2014, the Columbus 2020 team will

visit six U.S. cities and attend an industry conference in

Mexico.

Larger share of retention visits to manufacturers

The Columbus 2020 team and our local economic

development partners conducted a combined total of 82

visits to businesses in the Region during the second quarter

of 2014, adding to 169 year to date.

In the first half of 2014, 80 manufacturing companies

received visits, nearly half the total count. 0

10

20

30

40

50

60

Co

lum

bu

s

Du

blin

De

law

are

West

erv

ille

Wo

rth

ing

ton

Rest

of

Fra

nklin

Co

un

ty

Rest

of

Dela

ware

Co

un

ty

Kn

ox C

ou

nty

Rest

of

Reg

ion

Columbus 2020 Local ED Partner Both

44%

47%

48%

28%

23%

27%

12%

15%

13%

16%

15%

12%

2012

2013

Q1-Q2 2014

Manufacturing HQ & Business Services

Logistics Science & Technology

13

ED PROJECT ANNOUNCEMENTS - JOB

CREATION

QUARTERLY ECONOMIC UPDATE | Q2 2014

ED PROJECT ANNOUNCEMENTS BY

SECTOR

NOTABLE EXPANSIONS & LOCATIONS | JAN-JUN 2014

ED PROJECT ANNOUNCEMENTS, COUNT

BY MUNICIPALITY

ED PROJECT ANNOUNCEMENTS, COUNT

BY PLACE

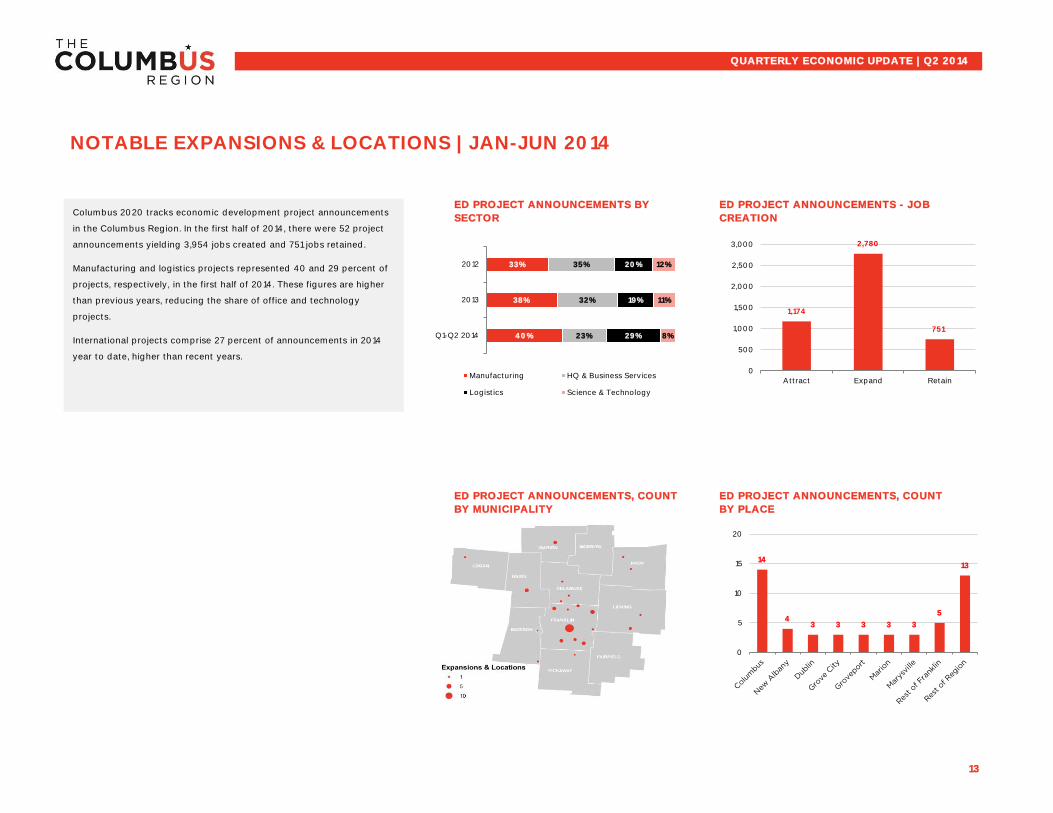

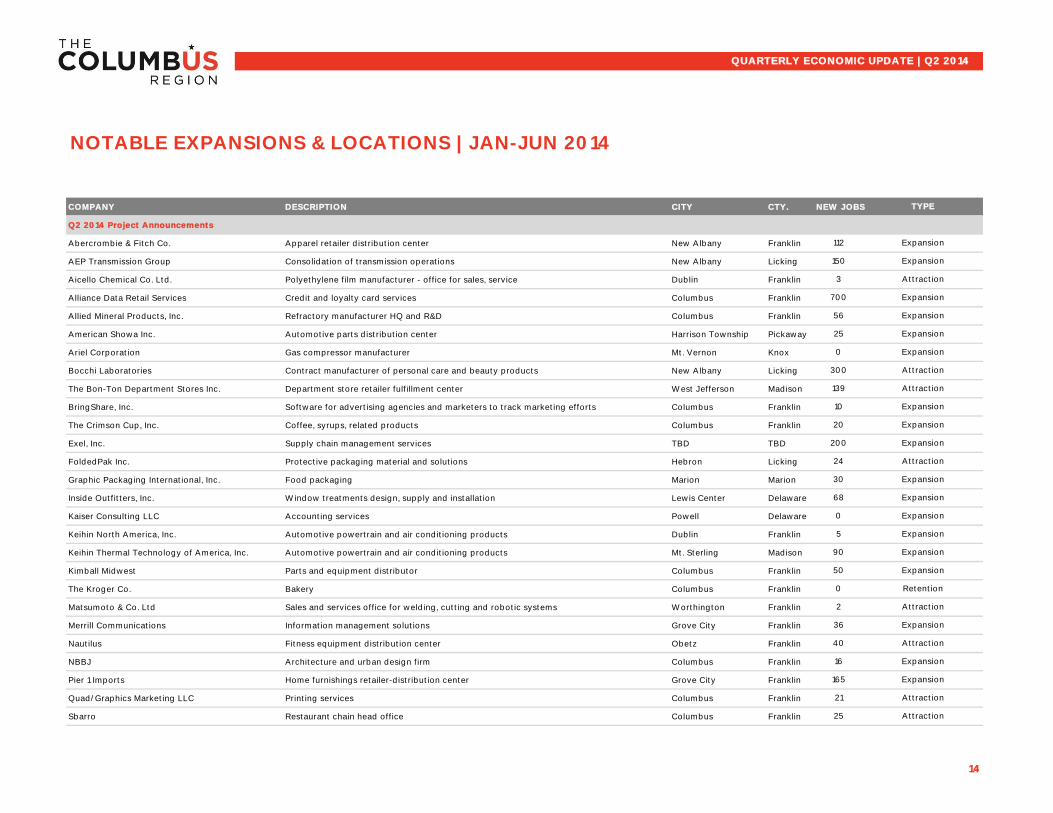

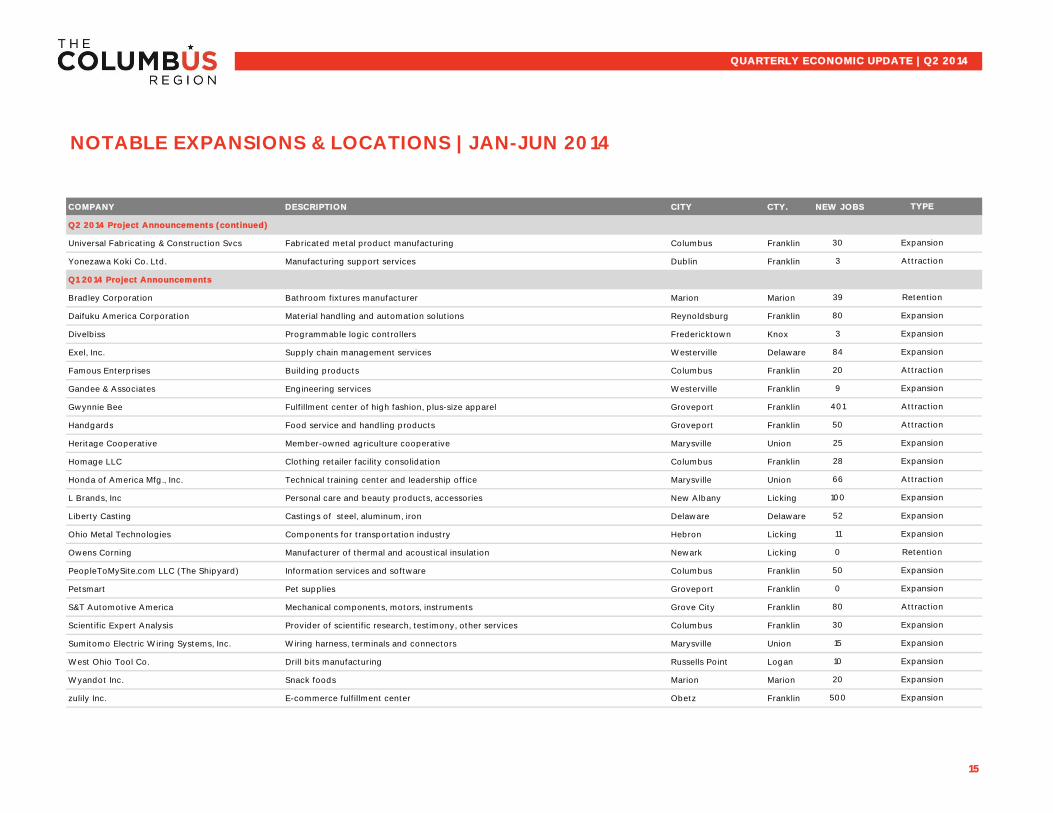

Columbus 2020 tracks economic development project announcements

in the Columbus Region. In the first half of 2014, there were 52 project

announcements yielding 3,954 jobs created and 751 jobs retained.

Manufacturing and logistics projects represented 40 and 29 percent of

projects, respectively, in the first half of 2014. These figures are higher

than previous years, reducing the share of office and technology

projects.

International projects comprise 27 percent of announcements in 2014

year to date, higher than recent years.

1,174

2,780

751

0

500

1,000

1,500

2,000

2,500

3,000

Attract Expand Retain

14

4 3 3 3 3 3

5

13

0

5

10

15

20

33%

38%

40%

35%

32%

23%

20%

19%

29%

12%

11%

8%

2012

2013

Q1-Q2 2014

Manufacturing HQ & Business Services

Logistics Science & Technology

COMPANY DESCRIPTION CITY CTY. NEW JOBS

Q2 2014 Project Announcements

Abercrombie & Fitch Co. Apparel retailer distribution center New Albany Franklin

AEP Transmission Group Consolidation of transmission operations New Albany Licking

Aicello Chemical Co. Ltd. Polyethylene film manufacturer - office for sales, service Dublin Franklin

Alliance Data Retail Services Credit and loyalty card services Columbus Franklin

Allied Mineral Products, Inc. Refractory manufacturer HQ and R&D Columbus Franklin

American Showa Inc. Automotive parts distribution center Harrison Township Pickaway

Ariel Corporation Gas compressor manufacturer Mt. Vernon Knox

Bocchi Laboratories Contract manufacturer of personal care and beauty products New Albany Licking

The Bon-Ton Department Stores Inc. Department store retailer fulfillment center West Jefferson Madison

BringShare, Inc. Software for advertising agencies and marketers to track marketing efforts Columbus Franklin

The Crimson Cup, Inc. Coffee, syrups, related products Columbus Franklin

Exel, Inc. Supply chain management services TBD TBD

FoldedPak Inc. Protective packaging material and solutions Hebron Licking

Graphic Packaging International, Inc. Food packaging Marion Marion

Inside Outfitters, Inc. Window treatments design, supply and installation Lewis Center Delaware

Kaiser Consulting LLC Accounting services Powell Delaware

Keihin North America, Inc. Automotive powertrain and air conditioning products Dublin Franklin

Keihin Thermal Technology of America, Inc. Automotive powertrain and air conditioning products Mt. Sterling Madison

Kimball Midwest Parts and equipment distributor Columbus Franklin

The Kroger Co. Bakery Columbus Franklin

Matsumoto & Co. Ltd Sales and services office for welding, cutting and robotic systems Worthington Franklin

Merrill Communications Information management solutions Grove City Franklin

Nautilus Fitness equipment distribution center Obetz Franklin

NBBJ Architecture and urban design firm Columbus Franklin

Pier 1 Imports Home furnishings retailer-distribution center Grove City Franklin

Quad/Graphics Marketing LLC Printing services Columbus Franklin

Sbarro Restaurant chain head office Columbus Franklin

14

Retention

Expansion

Expansion

25 Expansion

139

50

Expansion

40

36 Expansion

Attraction

2 Attraction

165 Expansion

21 Attraction

25 Attraction

Expansion

30 Expansion

68 Expansion

20 Expansion

300

10

0

Expansion

Attraction

700 Expansion

Attraction

Attraction

Expansion

Expansion

0

56

Attraction

QUARTERLY ECONOMIC UPDATE | Q2 2014

NOTABLE EXPANSIONS & LOCATIONS | JAN-JUN 2014

TYPE

112 Expansion

150 Expansion

3

Expansion

0

Expansion

200

24

5

90

16

COMPANY DESCRIPTION CITY CTY. NEW JOBS

Q2 2014 Project Announcements (continued)

Universal Fabricating & Construction Svcs Fabricated metal product manufacturing Columbus Franklin

Yonezawa Koki Co. Ltd. Manufacturing support services Dublin Franklin

Q1 2014 Project Announcements

Bradley Corporation Bathroom fixtures manufacturer Marion Marion

Daifuku America Corporation Material handling and automation solutions Reynoldsburg Franklin

Divelbiss Programmable logic controllers Fredericktown Knox

Exel, Inc. Supply chain management services Westerville Delaware

Famous Enterprises Building products Columbus Franklin

Gandee & Associates Engineering services Westerville Franklin

Gwynnie Bee Fulfillment center of high fashion, plus-size apparel Groveport Franklin

Handgards Food service and handling products Groveport Franklin

Heritage Cooperative Member-owned agriculture cooperative Marysville Union

Homage LLC Clothing retailer facility consolidation Columbus Franklin

Honda of America Mfg., Inc. Technical training center and leadership office Marysville Union

L Brands, Inc Personal care and beauty products, accessories New Albany Licking

Liberty Casting Castings of steel, aluminum, iron Delaware Delaware

Ohio Metal Technologies Components for transportation industry Hebron Licking

Owens Corning Manufacturer of thermal and acoustical insulation Newark Licking

PeopleToMySite.com LLC (The Shipyard) Information services and software Columbus Franklin

Petsmart Pet supplies Groveport Franklin

S&T Automotive America Mechanical components, motors, instruments Grove City Franklin

Scientific Expert Analysis Provider of scientific research, testimony, other services Columbus Franklin

Sumitomo Electric Wiring Systems, Inc. Wiring harness, terminals and connectors Marysville Union

West Ohio Tool Co. Drill bits manufacturing Russells Point Logan

Wyandot Inc. Snack foods Marion Marion

zulily Inc. E-commerce fulfillment center Obetz Franklin

15

80 Attraction

52 Expansion

39 Retention

11 Expansion

0 Retention

50 Expansion

0

30 Expansion

15 Expansion

10 Expansion

20 Expansion

500 Expansion

Expansion

28 Expansion

66 Attraction

100 Expansion

QUARTERLY ECONOMIC UPDATE | Q2 2014

NOTABLE EXPANSIONS & LOCATIONS | JAN-JUN 2014

TYPE

80 Expansion

3 Expansion

Attraction

9 Expansion

401 Attraction

50 Attraction

25 Expansion

30 Expansion

3 Attraction

84 Expansion

20