Embed Size (px)

DESCRIPTION

A quantitative look at the risk in budgeting cost, taking into account discounted cash flows for cost and benefits.

Citation preview

Square Peg ConsultingCopyright 2001, all rights reserved

Quantitative Risk Analysis in Budgeting and Cost Analysis

John C. GoodpastureSquare Peg Consulting

Square Peg ConsultingCopyright 2001, all rights reserved

Budgets are estimates

There are no facts about the future, only estimatesSimple budget estimates do not account for riskRisk is handled by estimating the impact of uncertainties on future cash flows (uses of funds and sources of funds)

Square Peg ConsultingCopyright 2001, all rights reserved

Terms in risk-managed budgeting

Discounting – takes into account the risks of receiving or paying funds in the future

Expected Value – takes into account the uncertainty of estimate

Net Present Value – cash value at time zero (now)

Internal Rate of Return – discount required for NPV = 0

Economic Value Add (EVA) – profit-based calculation of discounted value

Square Peg ConsultingCopyright 2001, all rights reserved

Capital budgeting*Present value (PV) = Value at future date * Discount factorDiscount factor = 1/(1-k)n where n is the number of accounting periods between the present and the future and k is the cost of capital factor

Net Present Value (NPV) = Σ PV of cash inflows - Σ PV of cash outflows

$ Inflows

$ OutflowsTime

Economic Value Add = After-tax operating income - k (Capital invested)where k is the cost of capital rate, %

Expected Monetary Value = Σ $OutcomeNth * ProbabilityNthfor all possible outcomes

*The flow of cash and not expenses

Square Peg ConsultingCopyright 2001, all rights reserved

PM influences NPV via the project timeline

First, the value of money decays over time. This decay is due to the effects of inflation, the uncertainty that future flows will continue or begin, and the uncertainty that a better investment is available elsewhere. In all cases, the “present value” is more than the “future value.”

Second, the value of the project is the net of the present value of all the cash outlays for investment and inflows from operations and salvage.

Square Peg ConsultingCopyright 2001, all rights reserved

NPV

Future benefits are “discounted” to the present to account for RISK in the future.

Time

$ Benefits, Expected Value

NPV is the Σ benefits + investment in the present value.IRR is the discount rate that makes NPV equal to $0.

$ Investment

Σ {present values}

Square Peg ConsultingCopyright 2001, all rights reserved

Two-dimensional risks

Present Time

Future Time

Estimate Uncertainty

Discount for•Inflation•Risk of getting paid•Capital cost•Denied opportunity•Market uncertainty

Distribution of estimate

EV

Square Peg ConsultingCopyright 2001, all rights reserved

PV tableYear 0 1 2 3 4

5% 1.0 0.952 0.907 0.864 0.823

8% 1.0 0.926 0.857 0.794 0.735

12% 1.0 0.893 0.797 0.712 0.636

13% 1.0 0.885 0.783 0.693 0.613

14% 1.0 0.877 0.769 0.675 0.592

Discount

PV = Value before discount * factor at intersection of Discount and Year

Square Peg ConsultingCopyright 2001, all rights reserved

NPV example$500 investment made now, that yields a $1000 benefit 2 years from now, at a discount factor of 12%, has an NPV of $?.

Answer: From the table of present values, find the factor for 12% 2 years from now; multiply the FV by the factor to get the PV; net with the investment-$500 + 1000 * 0.797 = $297

Square Peg ConsultingCopyright 2001, all rights reserved

NPV example

Mathematically: $297 = -$500/(1 + 12%)0 +$1000/(1 + 12%)2

$297 = -$500 + $797

Square Peg ConsultingCopyright 2001, all rights reserved

NPV and EVA in project selection

A valuable project has positive, or at worst $0, NPVA valuable project must earn back more than, or at worst equal, the cost of the capital invested: EVA > $0Discount rate used in NPV and EVA for project approval is the “hurdle rate”IRR is the maximum discount rate for EVA or NPV = $0

Square Peg ConsultingCopyright 2001, all rights reserved

Paul’s project

$500K investment required12.8% hurdle rate$700K+ benefit stream estimated over 5 yearsIs this a good deal?

Square Peg ConsultingCopyright 2001, all rights reserved

Paul’s project, NPVPaul's Project

$000

Year Cash Investment

Benefits Face Value

Benefits Present Value @ 12.8% PV Cash Flow

0 ($500.00) ($500.00)

1 $141.46 $125.41 ($374.59)

2 $141.46 $111.18 ($263.42)

3 $141.46 $98.56 ($164.85)

4 $141.46 $87.38 ($77.48)

5 $141.46 $77.46 ($0.01)

Totals ($500.00) $707.30 $499.99 ($0.01)

NPV = $0; IRR is 12.8%–A-risk-neutral investor would take $0 or the project opportunity indifferently–Spreadsheet “add-in” Resolver will iteratively solve for benefits given the investment and hurdle rate.

Square Peg ConsultingCopyright 2001, all rights reserved

EVA

Alternative Competing for Capital

Alternative Competing for Capital

EVANet Cash

Benefits from Project

Opportunity Cost of Capital Employed

After-Tax Earnings

$0

CE x discount rate = CCECapital Employed to Execute a Project

EVA = (Present value of after-tax earnings) – (Benefits from the next best competing opportunity)

Square Peg ConsultingCopyright 2001, all rights reserved

Paul’s project EVADepreciate $500K annually at $100K per year, discount rate 12.8%

Depreciation Schedule for Paul's Project $000

Year 1 Year 2 Year 3 Year 4 Year 5 Total

$100.00 $100.00 $100.00 $100.00 $100.00 $500.00 Depreciation

$500.00 $400.00 $300.00 $200.00 $100.00 Capital employed

(CE)

12.80% 12.80% 12.80% 12.80% 12.80% Cost of capital rate (CCR)

$64.00 $51.20 $38.40 $25.60 $12.80 $192.00Cost of capital employed (CCE) =

CE x CCR

$56.74 $40.24 $26.75 $15.81 $7.01 $146.55 PV CCE

Square Peg ConsultingCopyright 2001, all rights reserved

Paul's Project Plan with EVA = $0 $000

Outlays shown as ($000), Discount factor 12.8%

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 TOTAL

($500.00) Investment

$56.74 $40.24 $26.75 $15.81 $7.01 $146.55 PV CCE

$29.31 $29.31 $29.31 $29.31 $29.31 $146.55 PV after-tax earnings

($27.43) ($10.93) $2.56 $13.50 $22.50 $0.00 PV EVA

$33.06 $37.29 $42.07 $47.45 $53.53 $213.40 FV after-tax earnings

$100.00 $100.00 $100.00 $100.00 $100.00 $500.00 FV depreciation

$133.06 $137.29 $142.07 $147.45 $153.53 $713.40 FV cash benefits

($500.00) $117.96 $107.90 $98.99 $91.08 $84.07 $0.00 NPV cash benefits

Project goal

NPV of Net Cash Flow = EVA of after-tax earnings

Square Peg ConsultingCopyright 2001, all rights reserved

Present value of EVA of cash earnings and NPV of cash flow are equal!

Square Peg ConsultingCopyright 2001, all rights reserved

Risk analysis in expense (cost) estimating

1. Begin with WBS2. Use decision trees to evaluate EMV of

alternatives in each WBS, as appropriate

3. For uncertain cost elements, estimate a distribution

4. Obtain PV of all EVs5. Sum EVs and deterministic costs for

project estimate

Square Peg ConsultingCopyright 2001, all rights reserved

Project WBS

Project NEW PRODUCT

Product Design2

PM Office1 Software

Development3

Integration and Test

4

Deployment6

Training and Support

5

Square Peg ConsultingCopyright 2001, all rights reserved

“3-point estimate” and the error of “Most Likely”

$41Total WBS 2,3,4

$23$15$114. Integration & Test

$35$20$163. SW Design

$10$6$42. Product Design

PessimisticMost LikelyOptimisticWBS Element

Project Cost Estimates and Ranges$000

All WBS cost estimates are PV

Square Peg ConsultingCopyright 2001, all rights reserved

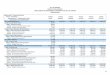

EV is a better estimate

$46.67(14% greater than Most Likely)

$41Total WBS 2,3,4

$16.33$154. Integration & Test

$23.67$203. SW Design

$6.67$62. Product Design

Expected Value*Most LikelyWBS Element

Project Cost Estimates and Ranges$000

•Triangular distribution assumed*The EMV from a decision tree outcome for a WBS element would go in this column

Square Peg ConsultingCopyright 2001, all rights reserved

What’s been learned?

Capital budgeting is about cash flowNPV and EVA are equivalentGood projects have positive NPV and EVAEV math reduces risk of WBS cost estimates