Embed Size (px)

Citation preview

pestel

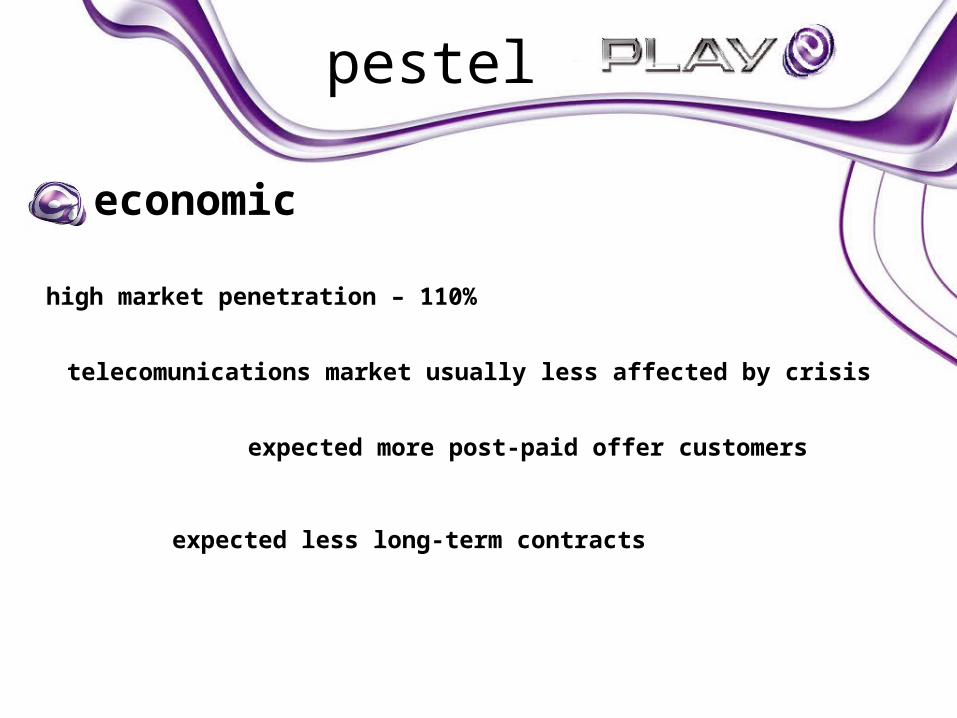

• economic

telecomunications market usually less affected by crisis

expected more post-paid offer customers

high market penetration – 110%

expected less long-term contracts

pestel

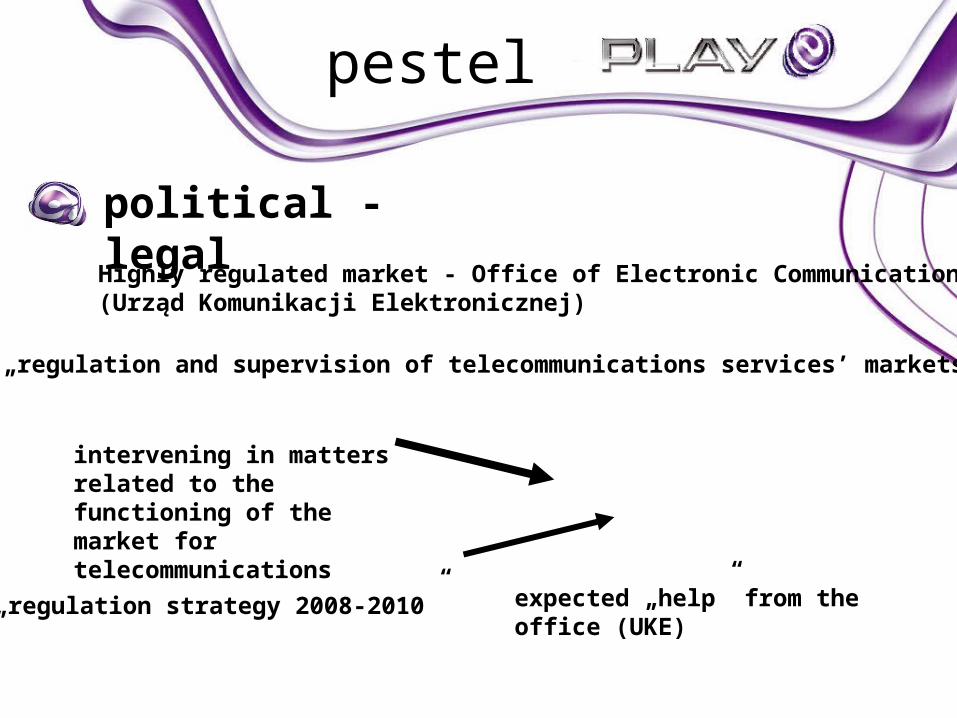

Highly regulated market - Office of Electronic Communications(Urząd Komunikacji Elektronicznej)

intervening in matters related to the functioning of the market for telecommunications

„regulation and supervision of telecommunications services’ markets”

„regulation strategy 2008-2010” expected „help” from the office (UKE)

political - legal

strategic analysis and strategy formulation

Karol Sudak

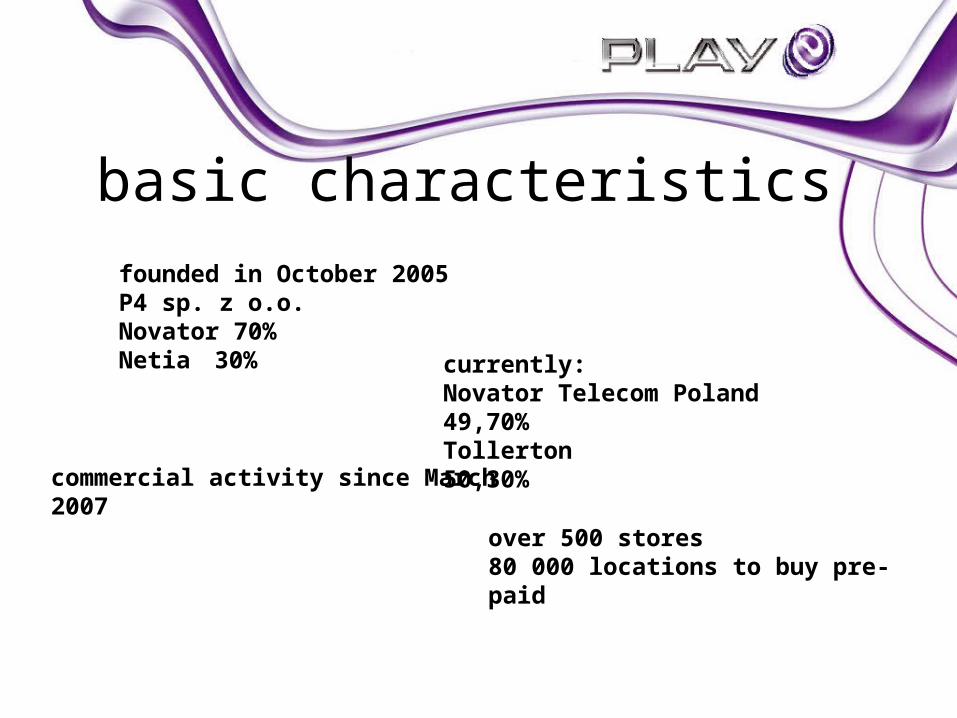

basic characteristics

commercial activity since March 2007

over 500 stores80 000 locations to buy pre-paid

founded in October 2005P4 sp. z o.o. Novator 70%Netia 30% currently:

Novator Telecom Poland 49,70%Tollerton 50,30%

offer

post-paid ONE PLAY 25, 45, 64, 95, 145

offers services for individuals and companies

e-shop + online multimedia center

pre- paid PLAY FRESH

mobile internet UMTS/3Gpost-paid & pre paid

pestel

Highly regulated market - Office of Electronic Communications(Urząd Komunikacji Elektronicznej)

intervening in matters related to the functioning of the market for telecommunications

„regulation and supervision of telecommunications services’ markets”

political - legal

„regulation strategy 2008-2010”

pestel

pace of growth relatively high („0” or small recession)

intrest rates relatively high – higher costs of capital

economic

financial crisis coming (or not)telecomunications market usually less affected by crisis

expected more post-paid offer customers

pestel

social

relatively young society

intrest rates relatively high – higher costs of capital

pestel

technological

increasing usage of high technologies

well developed online distribution channel

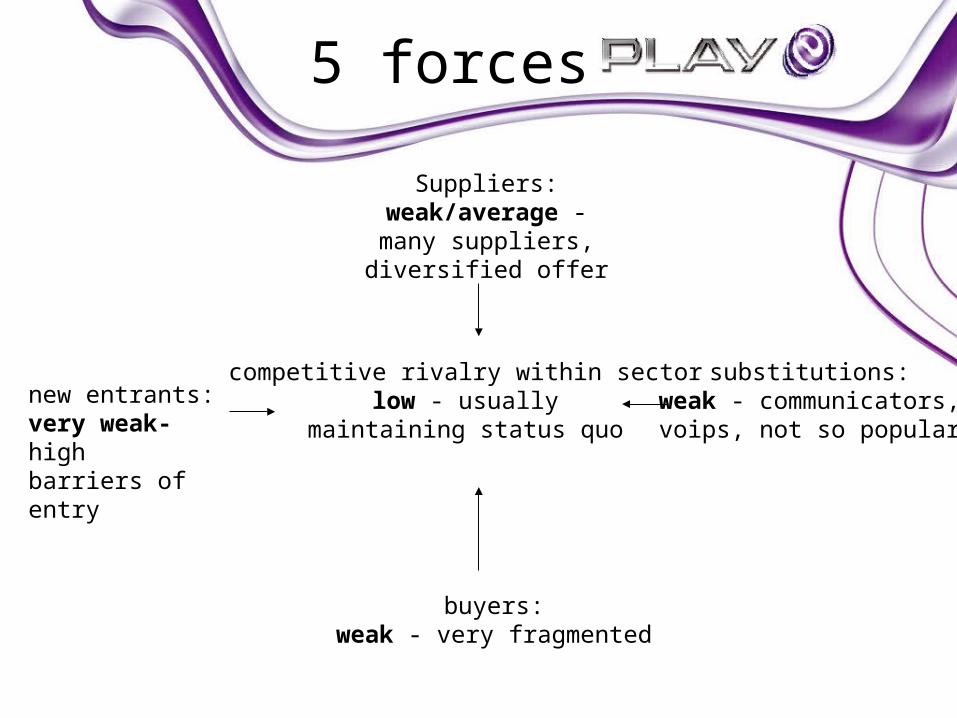

5 forces

Suppliers:weak/average - many suppliers, diversified

offer

buyers:weak - very fragmented

substitutions:weak - communicators,

voips, not so popular

competitive rivalry within sectorlow - usually

maintaining status quo

new entrants:very weak- high barriers of entry

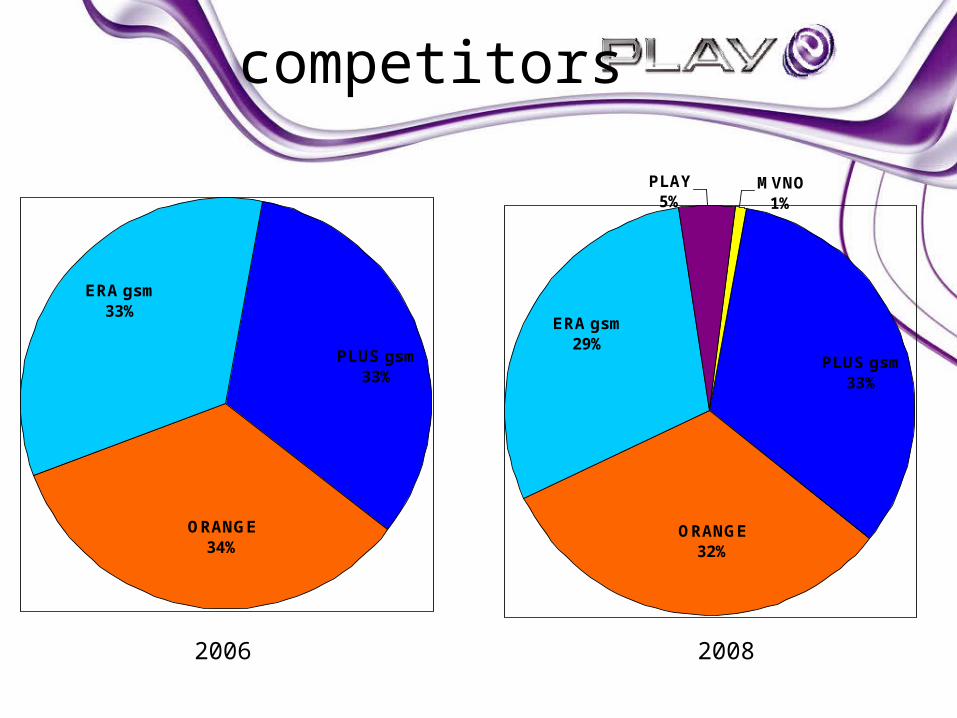

competitors

PLAY5%

MVNO1%

ERA gsm29%

PLUS gsm33%

ORANGE32%

ERA gsm33%

PLUS gsm33%

ORANGE34%

2006 2008

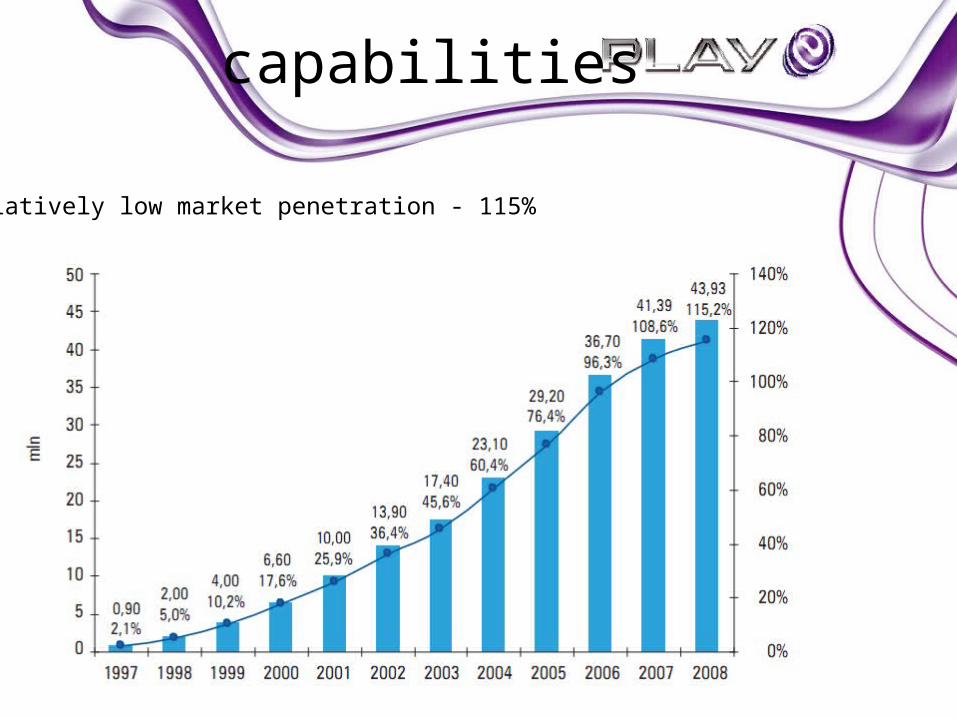

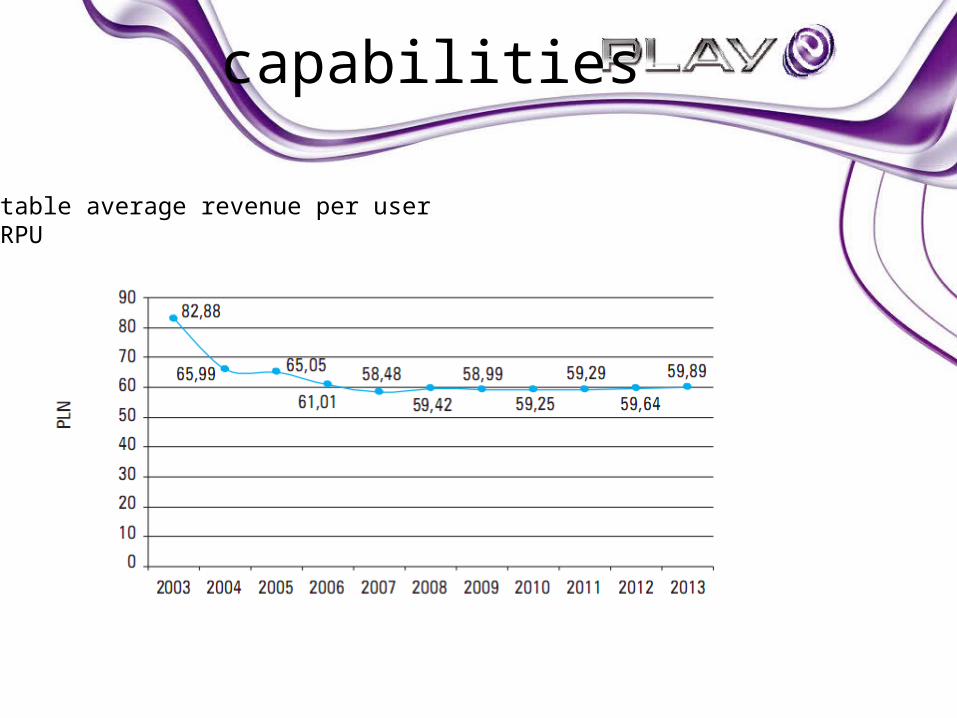

capabilities

relatively low market penetration - 115%

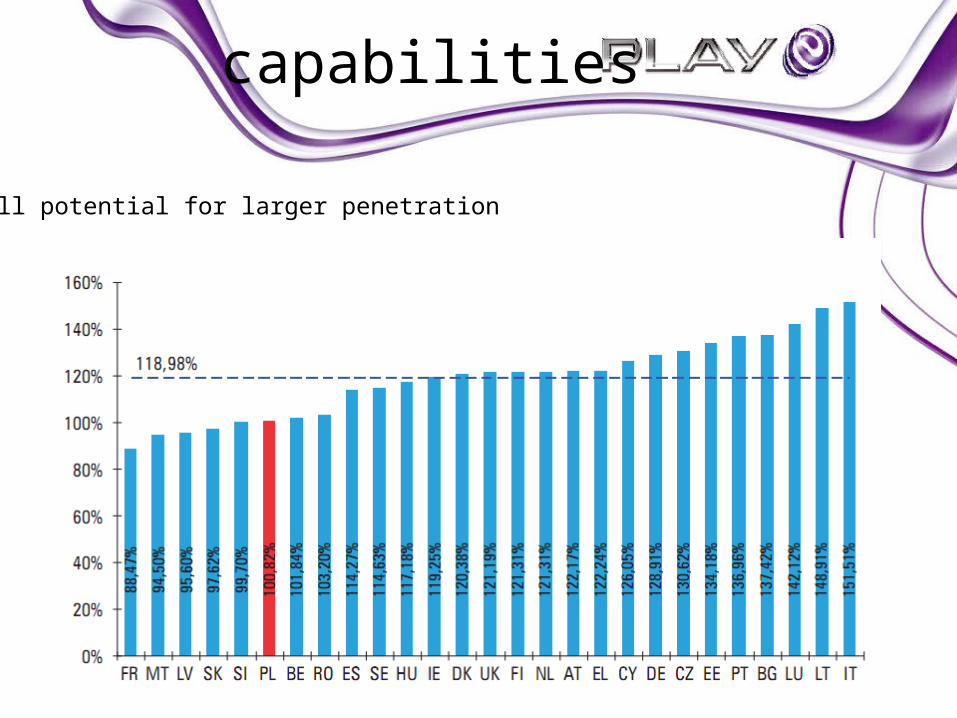

capabilities

small potential for larger penetration

capabilities

stable average revenue per userARPU

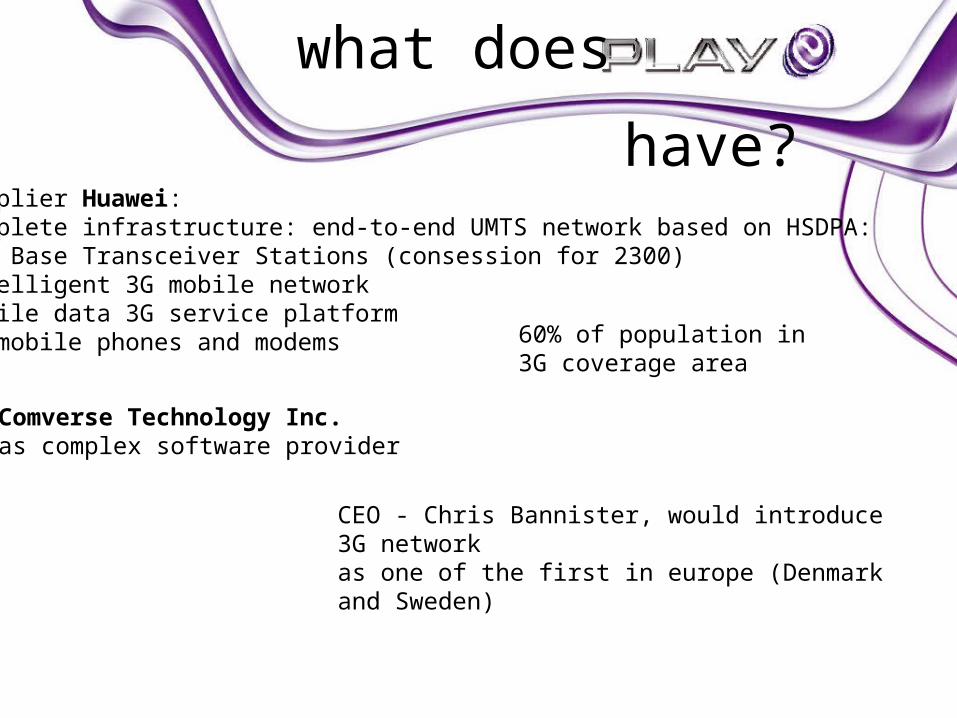

what does

supplier Huawei:complete infrastructure: end-to-end UMTS network based on HSDPA:500 Base Transceiver Stations (consession for 2300)intelligent 3G mobile networkmobile data 3G service platform3G mobile phones and modems

Comverse Technology Inc.as complex software provider

have?

60% of population in 3G coverage area

CEO - Chris Bannister, would introduce 3G networkas one of the first in europe (Denmark and Sweden)

what does

want to offer?

„PLAY - first multimedia mobile operator in Poland”

encouraging customers to use data transfer- related services

„there's more to life than talking”

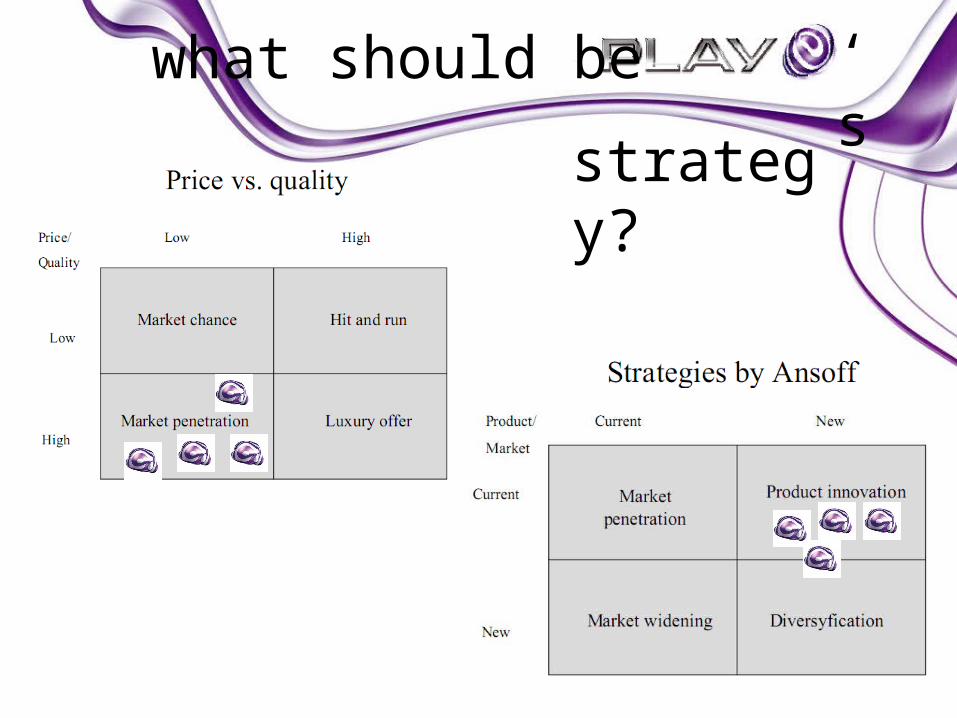

what should be ‘s

strategy?

why is it possible?

very high margins - possible lowering price AND implementing new high quality services

support from Office of Electronic Communications encouraging investments and new players

large potential market for mobile network services

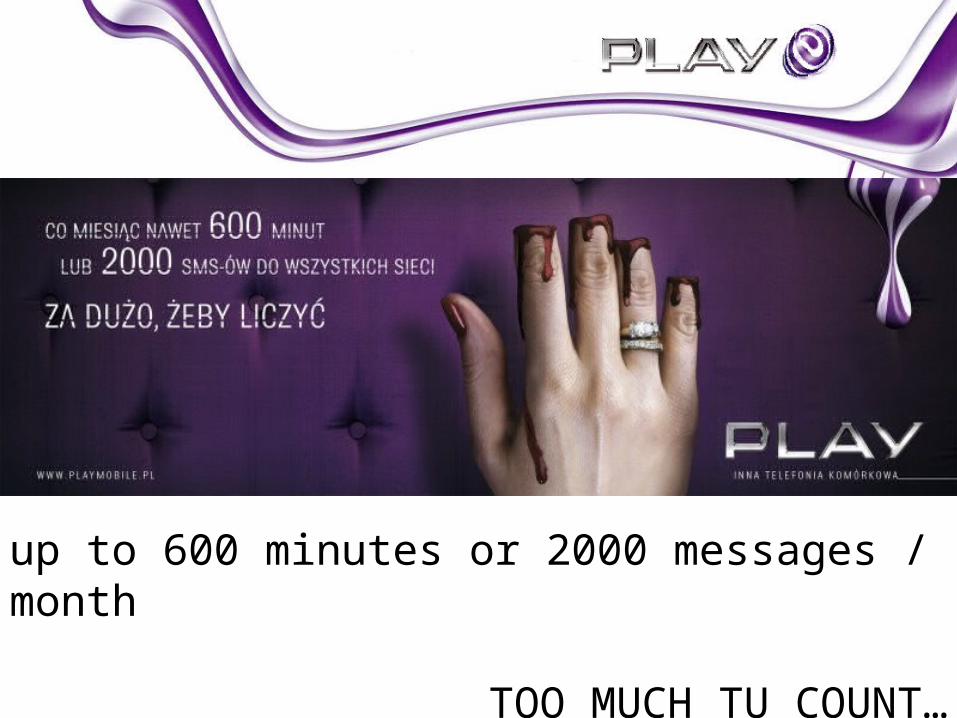

up to 600 minutes or 2000 messages / month

TOO MUCH TU COUNT…