Embed Size (px)

Citation preview

Orchestrate the Balancebetween a Growth Strategy vs.Driving Cost EfficienciesBy Elmien Sambandan

Elmien is a manager in the Africa team for Supply Chain andOperations Advisory at EY. She holds a degree in IndustrialEngineering as well as an engineering honours degree inManagement of Technology, both from the University of Pretoria.Elmien is a certified project management professional (PMP®)and has more than 8 years’ experience in Supply Chainconsulting in various countries in Africa.

She has experience as a project manager for new productdevelopment, especially for African countries, at a large globalconsumer products manufacturer. Her supply chain expertisespans across supply chain strategy and design, supply chainnetwork optimisation, inventory management, integratedbusiness planning and new product development processes.Elmien is a member of the South African Institute for IndustrialEngineers.

Speaker Biography – Elmien Sambandan

• Nigeria Consumer Market Landscape

• Growth Enabler – Route to Market

• Emerging Market Strategy: Efficiency vs. Investment

• A Case Study – Multinational FMCG Company

• Conclusion

• Appendix

Elmien Sambandan

Agenda

1

4

3

2

5

6

Elmien Sambandan

►Mostly Christian►Higher income►Lower unemployment

rate►Southern residents are

more likely to try newthings

► Lagos residents aremore price conscious,with 55% favouring lowprices over a largeselection of products

►Mostly Muslim►Lower income►Higher unemployment

rate►Only 18% of Kano

residents are likely totry new things

►Northern Nigeriansseem less priceconscious

Northern NigeriaSouthern Nigeria

Source(s): Nielsen; Mckinsey; EY analysis

Nigeria’s consumer base is quite diverse with prominent differences betweenthe northern and southern regions.

Nigeria Consumer Market Landscape

Elmien Sambandan

0.00.51.01.52.02.53.0

2010 2015 2020 2025Algeria Egypt MoroccoTunisia Botswana GhanaKenya Namibia NigeriaSouth Africa

Source: IHS Global Insight

160

8141 50

24 2

240

10156 54 33

050

100150200250300

Nigeria

Egypt

Kenya

SouthAfrica

Algeria

Morocco

Ghana

Tunisia

Namibia

Botswana

2010 2025

Population growth (%) Population growth (million persons)

Nigeria’s consumer base is the largest and fastest growing in Africa, exceeding200 million by 2020.

Nigeria Consumer Market Landscape

►Nigeria has a growing middle income consumer and has one of the fastest growingconsumer-driven GDP’s in Africa

Elmien Sambandan Source(s): Santander; EY analysis

TheTraditionals

The Rising

The Thriving

►Consumers with low and irregular income►Very price sensitive, this segment depends on cheap

products mostly from informal markets►This is the largest group of consumers

►Middle class consumers with stable and rising income►Even though this segment bases their choices on

quality and practicality of products, the price remainsan important factor

►This segment relevancy is increasing

►Consumers with a higher income and high level ofeducation

►Mostly composed by cosmopolitan professionals; thissegment focuses on high quality, fashionable productspurchased in supermarkets or abroad.

►This segments represents a minority of the population

The consumers can be described in 3 distinct profiles: The Traditionals, theRising and the Thriving.

Nigeria Consumer Market Landscape

Elmien Sambandan

►Nigerian families focus their main expenditures in essential items as Food and Non-Alcoholic Beverages disregarding discretionary items such as leisure.

►Utilities expenditures are lower than in South Africa due to limited accessibility ofwater, electricity, gas and other fuels to organised entities.

Nigeria Consumer Market LandscapeIt is an attractive emerging market for consumer products companies, withfood being the major spend of households in Nigeria.

Sources: AfDB 2009 ; EY Analysis

US$ 127bn US$ 171bn

Growth Enabler – Route to Market

Elmien Sambandan

Maximising the growth opportunity in Nigeria, the products should be alignedto the targeted consumer base and enabled through the Route to Market.

ProductsConsumers

• Locally Relevant (unique)• Single use pack formats driving

complexity• Rising input costs

• Irregular or low income• 50% of population <15 years• Demand concentrated in Kano and

Lagos regions• Price sensitive; need low,

competitive price points

• > 900,000 outlets for sales; traditional trade >90%• Lack of control and visibility over route to market• Long lead times at the Lagos port, affecting shelf life and working capital• Logistics and distribution is a key differentiator given the infrastructure

Route to Market

Growth Enabler – Route to Market

Elmien Sambandan

1. Choosing which markets in which to compete

2. Shaping propositions for diverse consumers

3. Controlling the route to market

4. Innovating for local context

5. Being locally relevant…social license to operate

There are 5 Critical Success Factors for maximising the opportunity in Africa,one of them a competitive edge and impacting the Supply Chain significantly.

Elmien Sambandan

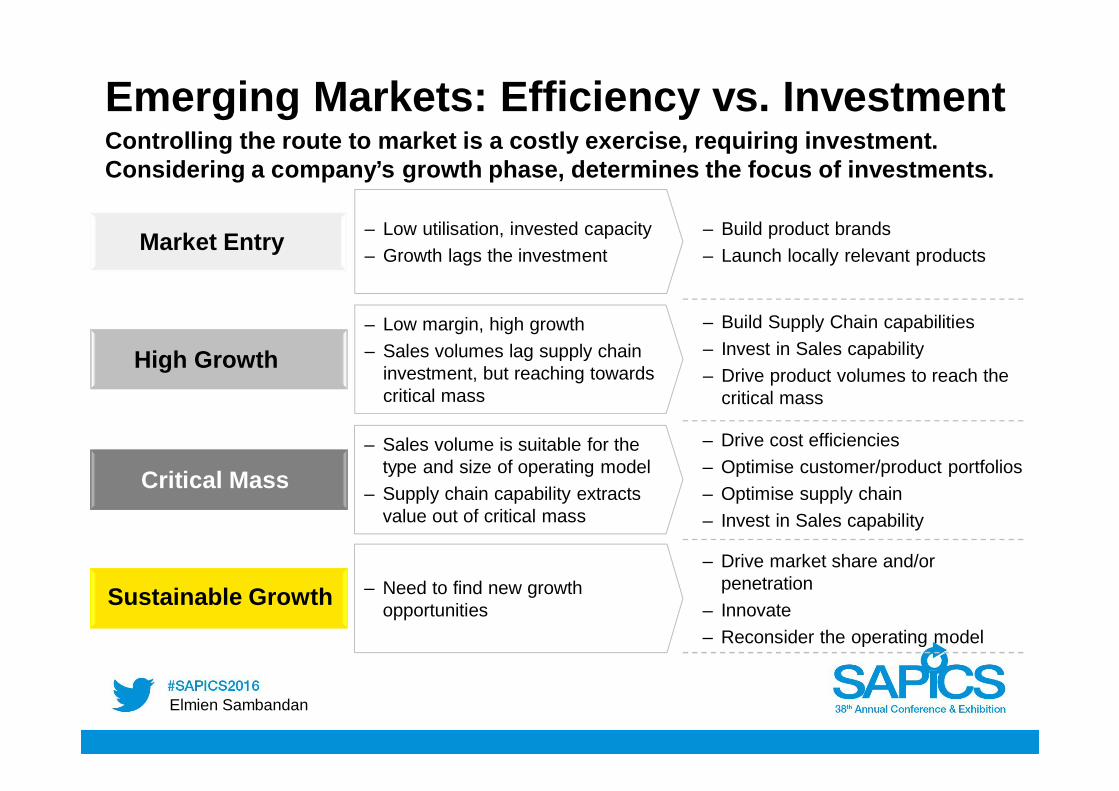

Controlling the route to market is a costly exercise, requiring investment.Considering a company’s growth phase, determines the focus of investments.

Emerging Markets: Efficiency vs. Investment

Market Entry

High Growth

Critical Mass

Sustainable Growth

– Low utilisation, invested capacity– Growth lags the investment

– Build product brands– Launch locally relevant products

– Low margin, high growth– Sales volumes lag supply chain

investment, but reaching towardscritical mass

– Build Supply Chain capabilities– Invest in Sales capability– Drive product volumes to reach the

critical mass

– Sales volume is suitable for thetype and size of operating model

– Supply chain capability extractsvalue out of critical mass

– Drive cost efficiencies– Optimise customer/product portfolios– Optimise supply chain– Invest in Sales capability

– Need to find new growthopportunities

– Drive market share and/orpenetration

– Innovate– Reconsider the operating model

A Case Study – Multinational FMCG

Elmien Sambandan

► Manufacturing plant► 2 warehouses, 14 depots► 500+ Distributors► ± 40 SKUs► Overall 60% utilisation of depots► Inventory: 7d fast moving; 78d tail end

An established consumer products manufacturer has reached critical salesvolumes to consider driving operational efficiencies whilst growing to the nextlevel.

Challenges:►No control or visibility over distributor order size/frequency.►No visibility of outlets penetration.►Product availability at distributors/outlets not controlled.►Distributors have limited and fluctuating cash flow.

Elmien Sambandan

A Case Study – Growth StrategyThe company invested in strategic growth initiatives that would increase theircontrol of the route to market from their own warehouses to include distributors.

► Build partnerships with keydistributors

► Allocate geographical locations todistributors

► Launch 3 new products► Deploy sales force at key distributors► Provide micro-financing to

distributors to relieve cash flowconstraints

► Launch mobile app for sales force totrack sales and inventory atdistributor, providing visibility

Growth Initiatives

► Increased visibility at distributors:– Inventory holding– Daily sales patterns– Promotions and pricing

► Increased control of inventory atdistributors:

– Cash flow enables purchases– Normalised order patterns– Reduced variance in supply chain

► Distributors take joint responsibilityfor geographical areas

► Innovation of new products createsconsumer excitement to drive growth

Impact

Elmien Sambandan

A Case Study – Cost OptimisationThe cost optimisation initiatives pursued by the company was not going to havea significant cost reduction impact, but rather risk additional loss of sales.

► Reduce transportation costs► Reduce costs of regional depots

through consolidation► Reduce overall inventory holding

Cost Optimisation Initiatives

► All warehousing and transport costswas only 5% of sales

► 2-7 months in a year, they are out ofstock on the top 4 fast moving SKUs.Inventory holding is too low

Cost Analysis

► Rationalised non-profitable products► Optimise inventory policies► Use key distributors for decentralised

“warehousing” space

These cost optimisation initiatives pursued will not have a significant impact on costs, but riskreducing product availability, negating all the investment created in the growth initiatives.

Revised Optimisation Initiatives

► Increased product availability frommanufacturing, in warehouses as wellas at distributors

► Create manufacturing capacity for fastmoving SKUs

Impact

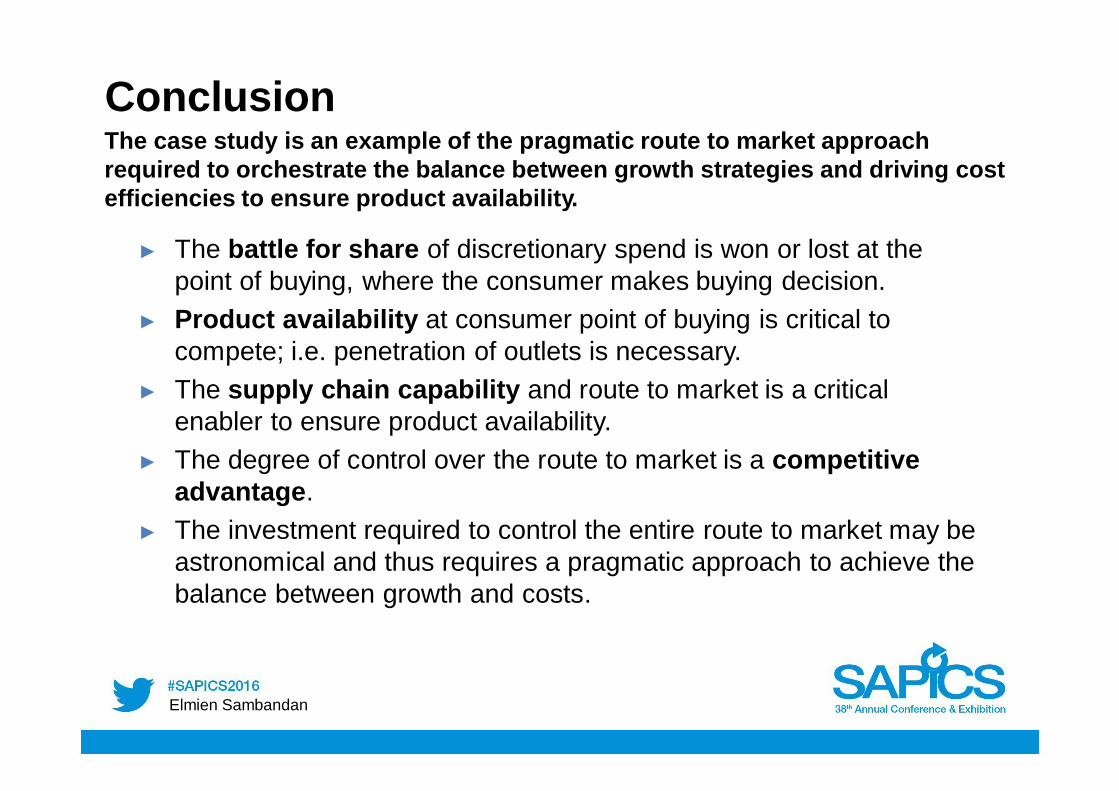

► The battle for share of discretionary spend is won or lost at thepoint of buying, where the consumer makes buying decision.

► Product availability at consumer point of buying is critical tocompete; i.e. penetration of outlets is necessary.

► The supply chain capability and route to market is a criticalenabler to ensure product availability.

► The degree of control over the route to market is a competitiveadvantage.

► The investment required to control the entire route to market may beastronomical and thus requires a pragmatic approach to achieve thebalance between growth and costs.

Elmien Sambandan

ConclusionThe case study is an example of the pragmatic route to market approachrequired to orchestrate the balance between growth strategies and driving costefficiencies to ensure product availability.

Appendix

Elmien Sambandan

• Route to Market Framework• Route to Market Distribution Model Alternatives

Elmien Sambandan

Assessing or designing an organisation’s route to market model can be done using thefollowing framework and maintaining the needs of the consumer at the centre of thesolution.

Route to Market Framework

Source: EY

Elmien Sambandan

Route-to-market Framework

A further breakdown of the framework provides key operating model components thatneed to be addressed to ensure a holistic route to market design.

Route to Market Framework

Source: EY

Elmien Sambandan

► Prime distributor(s)order(s) and import(s)the product

► Route to market maypass through otherdistribution tiers, e.g.sub distributors andwholesalers prior toreaching consumers,especially in traditionaltrade markets

► The distributor(s) areaccountable for supplychain, sales, customercontact and marketingactivities

As export except:► A subsidiary is created in

country to manage thesupply chain (includingimportation,warehousing andtransportation to thedistributor), manage thedistributor and supportlocal marketinginitiatives, e.g. materialslocalization

► The subsidiary receivesdemand plans from thedistributor andcalculates netrequirements

As import except► The subsidiary manages

all marketing andcustomer contactactivities, including keyaccounts, ordermanagement andcollections

► The distributor managesthe sales force only anddoes not take title to theproduct

► The subsidiary managesall in country activitiesincluding distribution toconsumers.

► Greater control of valuechain and accuracy indemand requirementsplanning.

Imports, manages logisticsand orders, invoices

Sales to customer

Manages logistics, salesand marketing

IMPORT2

Produces and delivers

Same as import plusmarketing

Sales to customer

Managessales force

AGENT3

Produces and delivers

Sales to customer

Same as Agent plussales

FULLYFLEDGED

4

Produces and delivers

EXPORT1

Produces, delivers andinvoices

Imports and distributes

Sales to customer

DIRECT TOCONSUMER

5

Produces and delivers

Sales to customer

3PL

► Head office ships directto consumer and savescosts

► 3PL provider could becontracted or employedto distribute withoutowning inventory

► Sub distributor utilizedto access rural marketsthat are too hard topenetrate. Typically usedwhen accessing marketsof traditional trade.

c

b

a

d

a Headquarters b Subsidiary c Prime Distributors d Sub distributors,wholesalers, retailers

Billing and collection

Purchase Order

Product delivery

Sales negotiation

Significant thought needs to go into what the “in-market” operating model needs to be,especially around the route to market and the degree of control required.

Route to Market Model Alternatives

Source: EY