Embed Size (px)

Citation preview

Operationalizing Customer Centricity: A Prescription for Building Brand Loyalty and Healthy Competitive Advantage Payers must refine processes across multiple channels to create a highly competitive brand based on consistently high-quality, member-centric experiences.

Executive SummaryThere is no question that the healthcare system is ailing. Costs are rising as customer satisfac-tion falters. New technologies, regulations and an increasingly competitive marketplace are forcing healthcare providers and payers to rethink how they operate. Customers are at the center of the tempest, and the industry must find new ways to engage with them.

According to a report by J. D. Power & Associates, many consumers are not satisfied with their health insurance provider interactions, whether paying a bill or inquiring about in-network physicians (see Figure 1). Common reasons for dis-satisfaction include unhelpful call center agents and cumbersome interactive voice response (IVR) systems. And when payers deny members’ claims, the result is anger and distrust.

Most consumers today hold payers to the same standards they experience with other business-to-consumer businesses, such as retailers, in terms of their ability to deliver highly personal-ized, high-value services. Their experience with online retail giants such as Amazon have taught consumers to expect high-touch interactions and a choice of channels, along with speedy

service and quality products. They want clear communications about benefits and coverage in plain language; caring and informed customer service; and efficiency and consistency at every touchpoint, from enrollment through billing, across every access platform.

Most healthcare payers fall far short of this ideal, leading to a general perception of poor service in the market. Even with the millions of new healthcare consumers entering the market under the Affordable Care Act, some payers may have a hard time attracting and retaining members. Consumers today also have more freedom and financial incentive to switch payers if they’re not happy.

The time has come for health insurers to change their approach to building customer relation-ships. They need to reevaluate each element of the interaction cycle, including awareness, con-sideration, enrollment, onboarding, service, billing and ongoing communication. Payers should also consider how new technologies are changing the determination of diagnoses, treatments and ongoing care, and redesign their processes to compete in this new context.

• Cognizant 20-20 Insights

cognizant 20-20 insights | april 2014

Source: J.D. Power & Associates, 2012Figure 1

0 5 10 15 20

Office closedCould not reach live person

System outageRouted incorrectly

Provider DB inaccuracyToo many transfers

Communicated timeline not metCall hold/wait time too long

Request can't be performedTransfer call disconnected

Content levelPlan design/provider network

Agent voice/volume/toneUnhelpful agent

Agent knowledge gapInconsistent communications

IVR too difficultMessage outcome

Top Reasons for Dissatisfaction Process knowledge 59%Communication 27%Call routing 22%Health plan operations 8%Staffing 4%

Reasons for Member Dissatisfaction

2

To turn the situation around, healthcare payers need to shift their focus from internal objectives to customers. Missing the chance to understand customer needs and failing to provide the consistent, quality experiences they seek will lead to irrelevance and insolvency.

This white paper probes how payers can meet these expectations and build a strong brand synonymous with service, quality and trustwor-thiness. The key to competitive branding will be “operationalizing” a member-centric vision. Payers must use multichannel capabilities and the data generated by members and providers to inform and realign business processes so they can deliver a consistent, rich experience for prospects and members across multiple channels.

This approach will also improve business perfor-mance and cost issues by creating a more virtual, efficient organization. Payers following this course will be positioned to build lifetime relation-ships with existing members and attract new ones for sustainable competitive advantage.

Engaging Healthcare Consumers Today’s consumers want more engagement with healthcare players through their preferred channels of interaction, especially when shopping for insurance, comparing benefits and assessing provider quality.1 Payers aren’t meeting expec-

tations; consumers give the health insurance industry low marks on its ability to communicate through multiple channels.2

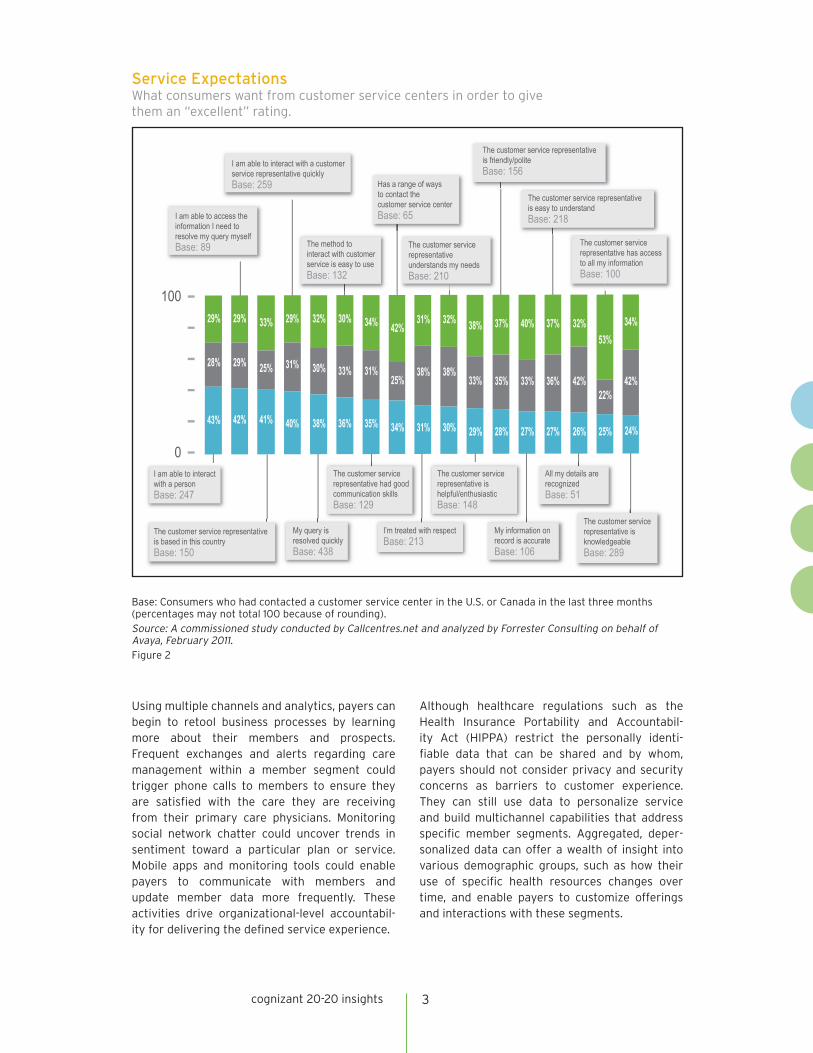

Consumer expectations for health insurance services are high (see Figure 2, next page), par-ticularly for consistent experiences at all touch-points and channels. Providing a consistent experience requires continuity of services, data access and “look and feel” across channels, whether by telephone, on the Web or via chat. Consistently high performance is a hallmark of strong brands, as is routine delivery of experi-ences that meet or exceed consumer expecta-tions. Healthcare consumers say brand strength is a strong influence on their healthcare purchase decisions. 3

’Operationalizing’ Member Centricity across Multiple Channels For payers, meeting the demands of healthcare consumers will require infusing member-centric-ity into business processes to deliver seamless service and rich experiences across multiple channels (see Figure 3, page 4). Proactively designing the customer experience will enable payers to make better business decisions; drive segmentation to individual member levels; and create customized, rich interactions with members that epitomize their branding.

cognizant 20-20 insights

cognizant 20-20 insights 3

Using multiple channels and analytics, payers can begin to retool business processes by learning more about their members and prospects. Frequent exchanges and alerts regarding care management within a member segment could trigger phone calls to members to ensure they are satisfied with the care they are receiving from their primary care physicians. Monitoring social network chatter could uncover trends in sentiment toward a particular plan or service. Mobile apps and monitoring tools could enable payers to communicate with members and update member data more frequently. These activities drive organizational-level accountabil-ity for delivering the defined service experience.

Although healthcare regulations such as the Health Insurance Portability and Accountabil-ity Act (HIPPA) restrict the personally identi-fiable data that can be shared and by whom, payers should not consider privacy and security concerns as barriers to customer experience. They can still use data to personalize service and build multichannel capabilities that address specific member segments. Aggregated, deper-sonalized data can offer a wealth of insight into various demographic groups, such as how their use of specific health resources changes over time, and enable payers to customize offerings and interactions with these segments.

Base: Consumers who had contacted a customer service center in the U.S. or Canada in the last three months (percentages may not total 100 because of rounding).Source: A commissioned study conducted by Callcentres.net and analyzed by Forrester Consulting on behalf of Avaya, February 2011.Figure 2

I am able to access the information I need to resolve my query myself

I am able to interact with a personBase: 247

I am able to interact with a customer service representative quicklyBase: 259

The method to interact with customer service is easy to useBase: 132

The customer service representative had good communication skillsBase: 129

Has a range of ways to contact the customer service centerBase: 65

I’m treated with respectBase: 213

My information on record is accurateBase: 106

100

0

Base: 89 The customer service representative understands my needsBase: 210

The customer service representative is friendly/politeBase: 156

The customer service representative is easy to understandBase: 218

The customer service representative has access to all my informationBase: 100

All my details are recognizedBase: 51

The customer service representative is knowledgeableBase: 289

The customer service representative is based in this countryBase: 150

The customer service representative is helpful/enthusiasticBase: 148

My query is resolved quicklyBase: 438

43%

28%

29%

42%

29%

29%

41%

25%

33%

40%

31%

29%

38%

30%

32%

36%

33%

30%

35%

31%

34%

34%

25%

42%

31%

38%

31%

30%

38%

32%

29%

33%

38%

28%

35%

37%

27%

33%

40%

27%

36%

37%

26%

42%

32%

25%

22%

53%

24%

42%

34%

Service ExpectationsWhat consumers want from customer service centers in order to give them an “excellent” rating.

cognizant 20-20 insights 4

Before embarking on process reconfiguration, payers must take the following three steps to ensure their process improvements support a strong, member-centric brand.

Step 1: Define the member experience.

• Proactively design the customer experience: Know your customers, their intents and how customers from each segment will satisfy those intents.

• Actions:

> Prioritize customer intentions.

> Define a customer experience blueprint.

> Implement a customer-oriented process de-sign.

> Assess customer communications and ex-pectations.

> Align training programs with customer expe-rience objectives.

Payers can analyze their existing member base from various perspectives to identify member segments or even individual member behavior. Segment data may include demographics, health conditions, utilization rates, lifetime value, preferred channels, etc.

Step 2: Deliver the service promise.

• Drive organizational (vendors, agents, opera-tions management) accountability for deliver-ing the defined service experience.

Align performance with experience objectives from top to bottom.

• Actions:

> Capture and evaluate every interaction.

> Hold vendors and agents accountable.

> Monitor customer engagement and satisfac-tion.

> Prioritize factors that drive customer satis-faction and net promoter scores (CSAT/NPS).

> Deliver more effective training to improve the customer experience.

Payers must map member experiences to existing processes to understand the member perspective, with special attention to where gaps exist between customer expectations and the payer’s ability to deliver. This will help identify pain points and highlight ways to improve the member experience.

Predictive analytics can offer insights into how the benefit needs and economic power of various segments will evolve over time and influence the service promise (see sidebar, next page).

Step 3: Create programs and offerings to expand customer relationships.

• Deepen customer relationships by increasing share of wallet and upselling the bundle.

> Monitor every customer against a common customer engagement index and actively work to extend each relationship.

Figure 3

Data and Analytics

Plan Offerings

Member Insights

Member Data

Personalized Communications

ConsistentMember

Experience

Mobile

, Texts

& A

pps Web & E-mail

SocialCall C

ente

r

Member CentricityInternal processes need to be aligned with member needs and expectations across multiple channels and access platforms.

• Actions:

> Collaborate on marketing campaigns.

> Leverage an average revenue per user (ARPU) increase framework.

> Implement an upsell and cross-sell engine and provide training.

> Develop contact center sales offerings.

> Develop more effective sales agents through improved training and faster time to profi-ciency.

With a granular understanding of member segments and individuals, payers can present new benefit options to members as their lifestyles and economic conditions change, whether the member is starting a family or nearing retirement. These options can be generated on-the-fly by smart algorithms and workflows, making them cost-effective to offer.

Payers should consider extending their offer-ings to complementary services, such as health club discounts, personal trainers following orthopedic rehabilitation, nutrition coaches, discounted monitoring devices and rewards programs that provide incentives for managing chronic health issues. With some of the newer sensor-based health monitoring devices, orga-nizations can also track adherence to wellness programs and provide virtual coaching to ensure that members follow treatments that lead to better health.

Focus on Member Centricity Improves Business ResultsWhen payer organizations put members at the center of their business processes, they stand to realize powerful business benefits, including:

• Additional value creation and business process improvement opportunities created

Quick Take

Retailers, especially those with online roots, are training consumers to expect their needs to be anticipated and for appropriate solutions and products to be offered before they ask for them. In healthcare, insight into members’ future needs may lead to wellness and lower costs, as well as greater member retention rates. Predictive analytics can help payers achieve such foresight.

Predictive analytics enables payers to anticipate issues that will arise within segments of the health populations they serve. The data feeding the analytics tools can come from multiple channels, from customer complaint logs to health resource use to demographic data. Algorithms parse these variables and more to predict which segments and members are likely to be:

• At risk for disenrollment.

• Considering transitioning between plans.

• Perceiving poor payer experiences.

• Lacking early disease detection.

• Struggling to manage chronic conditions.

• Overusing diagnostic procedures or drugs.

• Misusing provider resources due to lack of primary care access.

Predictive insights can also reveal factors contrib-uting to member dissatisfaction, as well as missed opportunities for member-centric offerings. Dis-connected processes, fragmented systems and data silos can prevent contact center representa-tives from seeing complete member interaction histories or failing to connect at-risk members with care management specialists. Analytics can also help determine where to focus on process optimization and new service development for the greatest return.

Optimizing the design and delivery of the member experience through predictive analytics also helps payers unlock value. Offering segment-driven, personalized benefits options to members at risk for disenrollment could lead to retained business; for example, providing coaching to help manage chronic conditions can reduce costs by slowing or preventing more expensive medical intervention. The success factor will hinge on using predictive analytics insights to design and provide these offerings before members ask for them.

Gaining a Deeper Understanding of Members’ Needs Through Predictive Analytics

5cognizant 20-20 insights

cognizant 20-20 insights 6

through improved customer insight utili-zation across the organization. The same insights that assist a customer service rep-resentative or prompt a Web server to offer help tools can be used by internal quality improvement, clinical, financial and marketing functions for better decision-making.

• Cost reduction achieved through improved integration of channels. A single view of the member that is visible across lines of business and multiple channels reduces contact center costs and overhead through shortened resolution times, resulting in a reduced cost structure. Similar cost cuts are possible through reduced duplication of effort, error elimination, etc.

• Greater member retention and sales oppor-tunities achieved through targeted com-munications and personalized relationships with customers. As payer organizations consolidate data to develop rich customer segments and use predictive analytics tools to anticipate future behavior, they can create detailed and granular member personas that reflect their many types of customers. These personas, created from segment transaction history, demographics and predictive models, make the potential life changes and resulting product needs of each segment more tangible. Creating finely detailed, insightful profiles can help payers further personalize their customer-centric offerings, such as knowing which communication channels each member type prefers and offering more personalized, targeted offerings to member segments.

Delivering Rich Member-Centric Experiences: A Checklist Providing members with personalized, stream-lined services, whether for initial enrollment or managing chronic conditions, requires the following capabilities:

• Collect and analyze digital data from a wide variety of member and prospect touchpoints as regulations permit, including monitoring of data generated by existing members as they interact with payer processes and provider networks.

• Develop granular segments for customers and prospects, based on demographics, utilization of services, etc., to understand member needs.

• Understand member perceptions and expe-riences with key business processes, from enrollment through billing.

• Enable member insights to flow through the organization to support business, financial and clinical functions.

• Create consistent experiences for members receiving services spanning several business units, such as Medicare, Medicaid and Tricare, ensure smooth coordination of benefits among the relevant plans and provide a single point of contact to these members.

• Offer self-service options across different access platforms.

• Support member preferences for using a variety of access platforms and communica-tions tools, from mobile texts to written com-munications.

• Use social network tools to communicate with members (e.g., distribute health and wellness messages or appointment alerts) and “listen” for aggregate health concerns.

This list is ambitious but reflects today’s competi-tive realities. Payers that execute on these capa-bilities will build stronger brands and retain and grow their member bases more effectively than those struggling with data silos and non-integrat-ed channels.

Looking AheadCreating value maps is one way that payers can identify the best opportunities for immediate cost savings and service improvements. Such maps put member-focused initiatives into financial terms to help drive decision-making about current and existing services. These maps can also provide insight into whether payers should attempt to invest in member-centric processes internally or work with experienced third-parties that can deliver the required functions as services, eliminating the need for capital investment and making operating costs scalable and predictable.

We’re still in the early days of the transition of healthcare to a retail-focused industry. This time advantage gives forward-thinking payers a window of opportunity to make effective decisions and build brands based on member-centric services, powered by multichannel capa-bilities with indicative and predictive analytics. The payers that accomplish this will create sus-tainable differentiation in the marketplace, a solid foundation for continued process improvement and a loyal, strong — and ultimately profitable — member base.

About CognizantCognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process out-sourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and approximately 171,400 employees as of December 31, 2013, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world. Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

World Headquarters500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 20 7297 7600Fax: +44 (0) 20 7121 0102Email: [email protected]

India Operations Headquarters#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2014, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About the AuthorKamesh Somanchi is a Healthcare Market Leader for business process services and global growth markets within Cognizant’s Business Process Services Practice. His experience spans both U.S. and international healthcare, as well as life sciences. During his career, Kamesh has assisted those industries in areas that include product filings, sales and marketing launch strategies, product launches and post-launch stabilization and performance improvement. He has helped clients set up shared service centers — consolidating and optimizing operations to improve the customer experience. His expertise includes management consulting, end-to-end process consulting, systems integration and business process out-sourcing. Kamesh can be reached at [email protected].

Footnotes1 Sherry Coughlin and Paul Kecklin, “2012 Survey of U.S. Health Care Consumers: Five-Year Look Back,”

Deloitte University Press, Dec. 14, 2012, http://dupress.com/articles/2012-survey-of-u-s-health-care-con-sumers-five-year-look-back/.

2 “ACSI Finance & Insurance Report 2013 Third Quarter Update On Overall U.S. Customer Satisfaction,” American Customer Satisfaction Index, Dec. 10, 2013, http://www.theacsi.org/news-and-resources/cus-tomer-satisfaction-reports/customer-satisfaction-reports-2013/acsi-finance-and-insurance-report-2013/acsi-finance-and-insurance-report-2013-download.

3 “More than Four in Five Americans Say Brand Is Important when Selecting a Health Insurance Plan,” Harris Interactive, June 20, 2013, http://www.harrisinteractive.com/NewsRoom/HarrisPolls/tabid/447/mid/1508/articleId/1217/ctl/ReadCustom%20Default/Default.aspx.