Embed Size (px)

Citation preview

p.3

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

CONTENTSINTRODUCTION

ABOUT CONFLICT MINERALS

DODD-FRANK SECTION 1502

THE COMPLIANCE PROCESS

THE DELIVERABLES

ON THE OECD DUE DILIGENCE GUIDANCE

HOW BUREAU VERITAS CAN HELP

ABOUT BUREAU VERITAS

ABOUT ESTELLE LEVIN LIMITED

5

7

9

13

15

19

21

22

23

chap. 1

chap. 2

chap. 3

chap. 4

chap. 5

chap. 6

chap. 7

BUREAU VERITAS & ESTELLE LEVIN LTD. ON CONFLICT MINERALS CHALLENGESAND MOVING BEYOND COMPLIANCE

p.5p.4

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

Certain minerals originating in the Democratic Republic of Congo (DRC) and adjoining countries have been a major source of international concern. Armed groups in the region are accused of severe human rights abuses and of using proceeds from the sales of these minerals to fuel regional conflicts. A broad range of public, private, and civil society groups have been working to bring light to this issue and, in recent years, legislation has been passed to address this problem.

In 2010, Section 1502 of the Dodd-Frank Wall Street Reform and Consumer Protection Act was put forth in the US Congress to address the problem of conflict minerals by requiring publicly listed companies to disclose their use of specific minerals originating in the DRC and adjoining countries. In 2012, the US Securities and Exchange Commission (SEC) issued its final rule to implement the requirements in the Dodd-Frank Act. This was the first legislation of its kind in the United States. Canada and the European Union are taking similar steps to address conflict minerals through legislation and it should be expected that many other countries will follow.

The legislative aim of the current conflict minerals regulation is to bring transparency to the supply chain so that financial links to armed groups can be identified. Indeed, with requirements for due diligence,

reporting, and public disclosure, the legislation has been designed to ensure accountability and discourage companies from doing business in ways that ultimately support exploitation and conflict.

There is also potential for unintended consequences to arise from this legislation. In aiming first and foremost to ensure conflict-free supply chains, many companies are deciding to source from outside of the DRC and its adjoining countries altogether. A mass disengagement from these economies is having clear impacts on local poverty and, as highlighted in comments to the SEC proposed rule, this could even create drivers for conflict. Thus, it is important to highlight that constructive engagement with mineral supply chains originating in conflict areas is the most effective solution to the difficult problem of conflict minerals.

INTRODUCTION

chap.1

INTRODUCTION

chap.1

tin tungsten

tantalum gold

p.7p.6

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

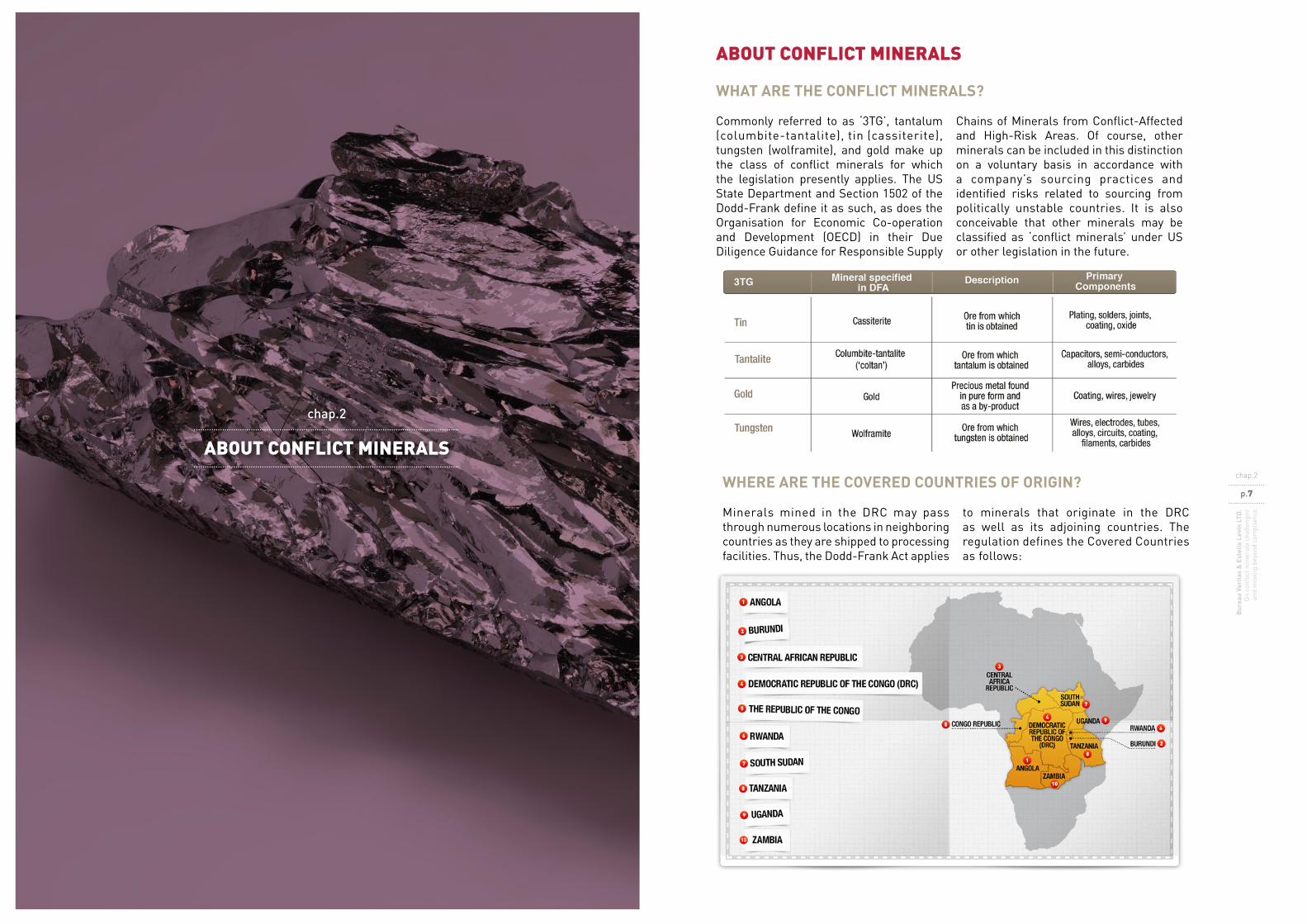

WHAT ARE THE CONFLICT MINERALS?

Commonly referred to as ‘3TG’, tantalum (columbite-tantalite), tin (cassiterite), tungsten (wolframite), and gold make up the class of conflict minerals for which the legislation presently applies. The US State Department and Section 1502 of the Dodd-Frank define it as such, as does the Organisation for Economic Co-operation and Development (OECD) in their Due Diligence Guidance for Responsible Supply

Chains of Minerals from Conflict-Affected and High-Risk Areas. Of course, other minerals can be included in this distinction on a voluntary basis in accordance with a company’s sourcing practices and identified risks related to sourcing from politically unstable countries. It is also conceivable that other minerals may be classified as ‘conflict minerals’ under US or other legislation in the future.

ABOUT CONFLICT MINERALS

chap.2

ABOUT CONFLICT MINERALS

chap.2

WHERE ARE THE COVERED COUNTRIES OF ORIGIN?

Minerals mined in the DRC may pass through numerous locations in neighboring countries as they are shipped to processing facilities. Thus, the Dodd-Frank Act applies

to minerals that originate in the DRC as well as its adjoining countries. The regulation defines the Covered Countries as follows:

p.9p.8

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e DODD-FRANK SECTION 1502

chap.3

DODD-FRANK SECTION 1502

chap.3

WHO IS AFFECTED?

All US-based and foreign issuers to the SEC under Sections 13(a) and 15(d) of the Exchange Act that manufacture or contract to manufacture products for which “conflict minerals are necessary to

the functionality or production ”fall under the scope of Section 1502 of the Dodd-Frank Act. An issuer that only services, maintains, or repairs a product containing conflict minerals is not affected.

Points to consider when determining if conflict minerals are necessary to “functionality or production” include the following:

• If it is intentionally added to the product or any component of the product

• If it is necessary to the product’s generally expected function, use, or purpose

• If it is incorporated for purposes of ornamentation, decoration or embellishment

p.10

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

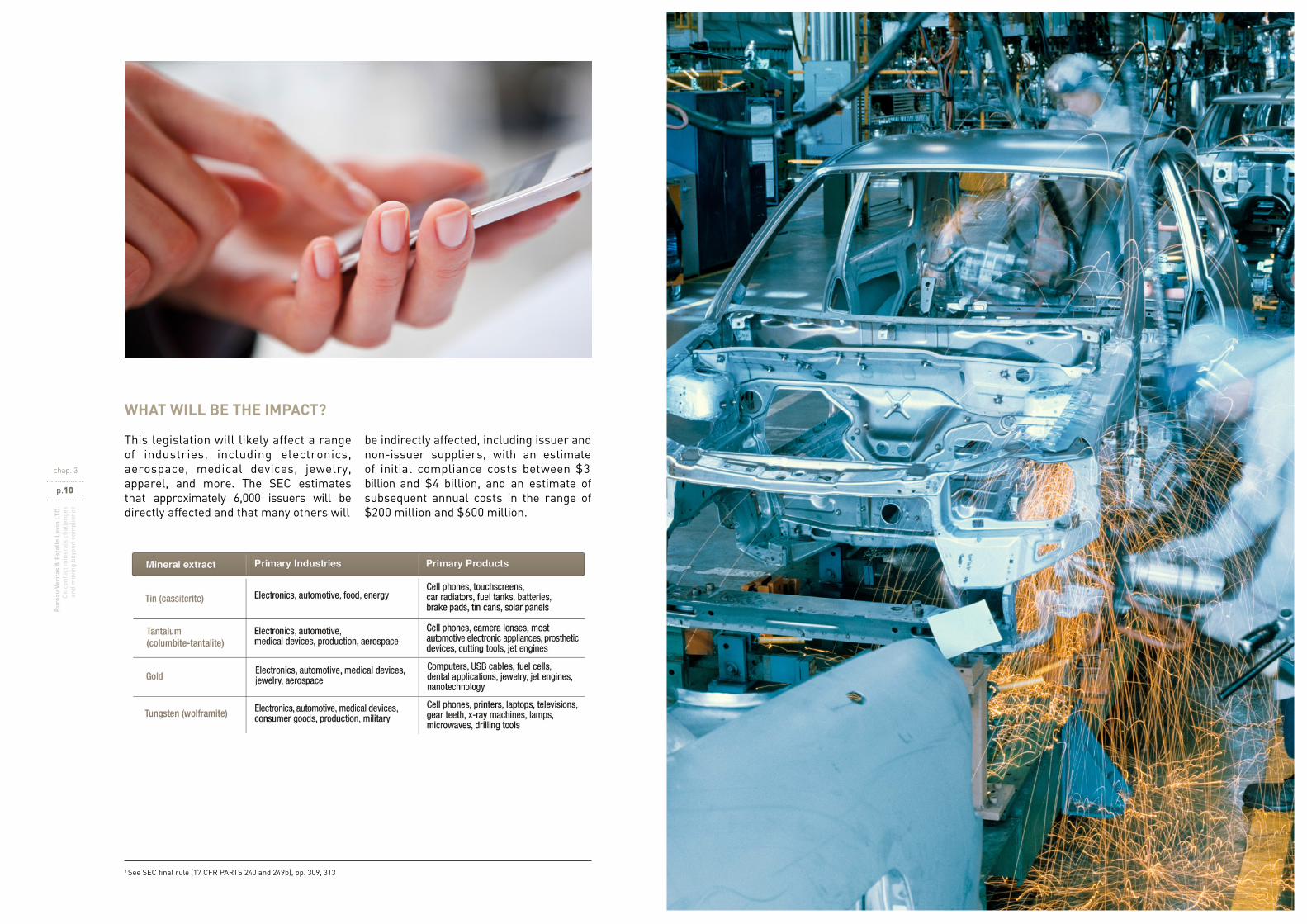

WHAT WILL BE THE IMPACT?

This legislation will likely affect a range of industries, including electronics, aerospace, medical devices, jewelry, apparel, and more. The SEC estimates that approximately 6,000 issuers will be directly affected and that many others will

be indirectly affected, including issuer and non-issuer suppliers, with an estimate of initial compliance costs between $3 billion and $4 billion, and an estimate of subsequent annual costs in the range of $200 million and $600 million.

chap. 3

1 See SEC final rule (17 CFR PARTS 240 and 249b), pp. 309, 313

p.13

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

The process for compliance can be broken down into three steps:

1. DETERMINE IF THE RULEAPPLIES TO YOUR COMPANY.

• An issuer needs to determine whetherits products contain minerals thatsubject it to Dodd–Frank Section 1502.

2. DETERMINE WHETHERCONFLICT MINERALS ARE FROM SCRAP OR RECYCLED SOURCES AND IF THEY ORIGINATE IN THE COVERED COUNTRIES.

• All affected issuers are required toconduct a ‘reasonable country of origininquiry’ (RCOI).

• An issuer that knows or reasonablybelieves that its conflict minerals didcome from scrap or recycled sourcesor did not originate in the CoveredCountries must briefly describetheir RCOI in a Form SD (SpecializedDisclosure Report) but does not needto move on to Step 3.

3. AN ISSUER WITH CONFLICTMINERALS THAT ARE POSSIBLY NOT FROM SCRAP OR RECYCLED SOURCES AND THAT POSSIBLY DID ORIGINATE IN THE COVERED COUNTRIES NEEDS TO EXERCISE DUE DILIGENCE.

• If an issuer believes that its conflictminerals possibly did not come fromscrap or recycled sources and possiblydid originate in the Covered Countries,it must exercise due diligence.

• If, after exercising due diligence, an issuer can determine that its conflict minerals did come from scrap or recycled sources or did not originate in the Covered Countries, it must describe its RCOI and due diligence measures in a Form SD, but the issuer is not required to submit a Conflict Minerals Report (CMR).

• If an issuer cannot determine that itsconflict minerals are not from scrapor recycled sources or that they didnot originate in the Covered Countries,it must submit a Conflict MineralsReport as an exhibit to the Form SD.

THE COMPLIANCE PROCESS

chap.4

THE COMPLIANCE PROCESS

chap.4

p.15

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

WHAT IS THE TIMELINE FOR DELIVERABLES?

All issuers that are subject to Dodd-Frank Section 1502 are required to file a Form SD, the Specialized Disclosure Report. It is thus important to understand what this form entails. Below is an overview of the elements that may need to be included in a Form SD.

Reasonable Country of Origin Inquiry (RCOI)The RCOI must be conducted in good faith and must be reasonably designed to determine country of origin.

All issuers are required to describe their RCOI and the results thereof in the Form SD. The issuer is also required to disclose this information on its publicly accessible website and provide a link to that website in the Form SD.

Due Diligence The due diligence process must conform to a nationally or internationally recognized framework if available.

Some issuers will need to exercise due diligence on the source and chain of custody of their conflict minerals. The due diligence process must be based on a nationally or internationally recognized framework. One example of such a framework is the OECD Due Diligence Guidance for Responsible

Supply Chains of Minerals from Conflict-Affected and High-Risk Areas (OECD Due Diligence Guidance). This framework has special supplements to ensure the particularities of the different supply chains for gold and the 3TGs are manageable.

An issuer required to exercise due diligence must describe its initial RCOI and subsequent due diligence process and the results thereof in the Form SD. The issuer is also required to disclose this information on its publicly accessible website and provide a link to that website in the Form SD.

Conflict Minerals Report (CMR)If an issuer cannot determine that its conflict minerals are not from scrap or recycled sources or that they are not from the Covered Countries, it must submit a Conflict Minerals Report as an exhibit to the Form SD. The report must describe the measures taken to exercise due diligence over the source and chain of custody of the conflict minerals.

THE DELIVERABLES

chap.5

THE DELIVERABLES

chap.5

p.17p.16

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e The Conflict Minerals Report should specify:• The country of origin of the conflict

minerals• Any efforts made to determine the

mine or location of origin with thegreatest possible specificity

• The facilities used for processing theconflict minerals, such as the smelteror refinery

• A description of any products that arenot “DRC conflict free”

An issuer must have an independent private sector audit (IPSA) of its Conflict Minerals Report. It is estimated that 6,000 issuers will be subject to Dodd-Frank Section 1502 and that 75% will need to file an independently audited Conflict Minerals Report.

TRANSITION PERIOD

Issuers submitting Conflict Minerals Reports that are unable to determine whether their products are “DRC conflict free” are allowed to describe their products as “DRC conflict undeterminable” during a transitional period.

In these cases, the Conflict Minerals Report shall include: • The country of origin of the minerals,

if known

• The facilities used to process theconflict minerals, if known

• Any efforts made to determinethe mine or location of origin withthe greatest possible specificity, ifapplicable

• The steps the issuer has taken, if any,since the period covered by its lastreport, or the steps that the issuerwill take to mitigate the risk that itsconflict minerals may benefit armedgroups

• The steps, if any, the issuer has takento improve its due diligence

If the issuer’s products are “DRC conflict undeterminable,” an independent private sector audit of the Conflict Minerals Report is not mandatory.

The “undeterminable” reporting option relates differently to smaller and larger issuers. For larger issuers, the option will be allowed only during the first two fiscal years (2014-2016). For smaller issuers, this alternative will be permitted during the first four fiscal years (2014-2018). At the first reporting deadlines after the transition periods (31 May 2016 for larger issuers, 31 May 2018 for smaller issuers), an issuer with “undeterminable” products will need to identify them as “not been found to be DRC conflict free” in the Conflict Minerals Report.

chap.5chap. 5

WHAT IS THE TIMELINE FOR DELIVERABLES?

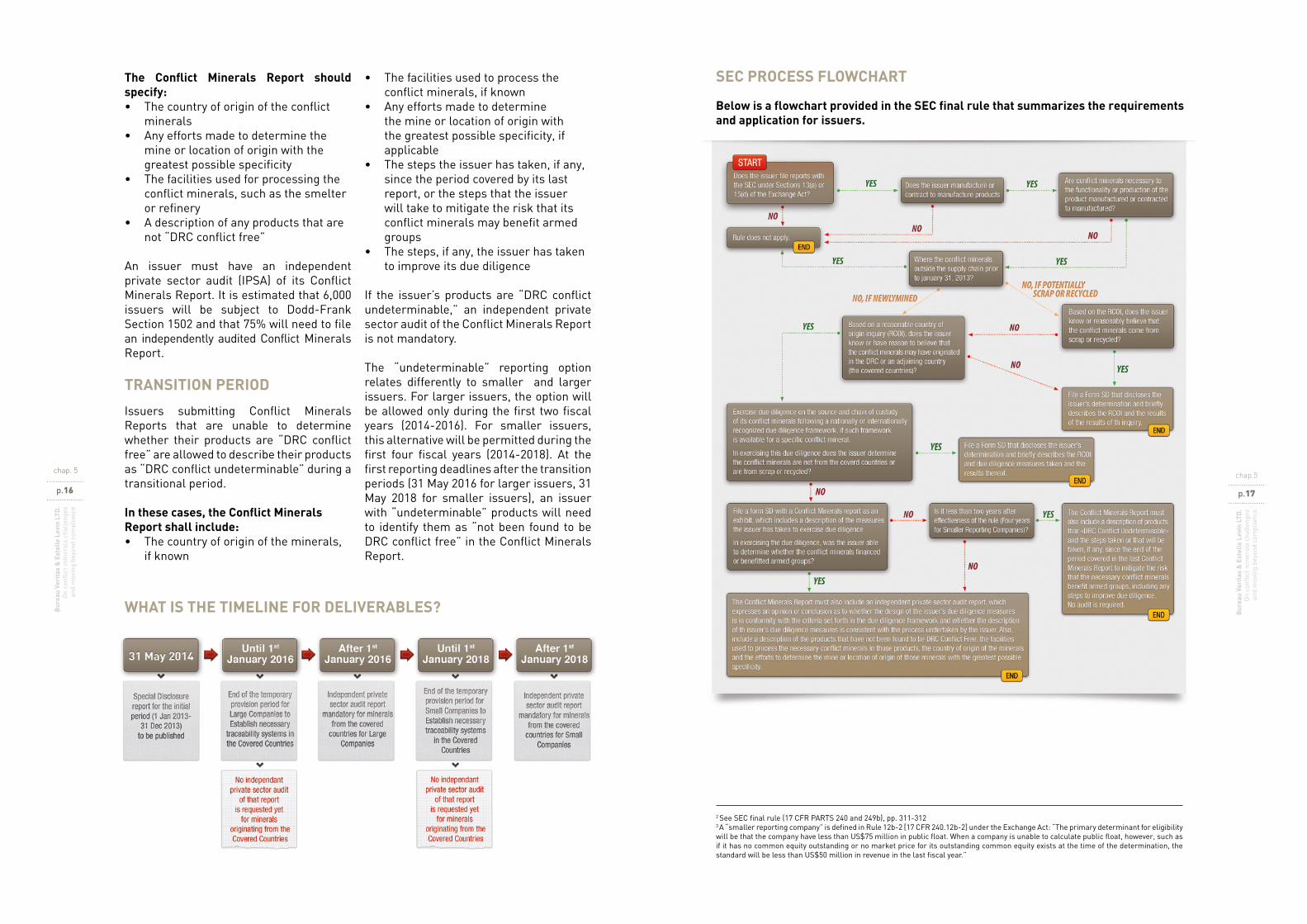

SEC PROCESS FLOWCHART

Below is a flowchart provided in the SEC final rule that summarizes the requirements and application for issuers.

2 See SEC final rule (17 CFR PARTS 240 and 249b), pp. 311-3123 A “smaller reporting company” is defined in Rule 12b-2 [17 CFR 240.12b-2] under the Exchange Act: “The primary determinant for eligibility will be that the company have less than US$75 million in public float. When a company is unable to calculate public float, however, such as if it has no common equity outstanding or no market price for its outstanding common equity exists at the time of the determination, the standard will be less than US$50 million in revenue in the last fiscal year.”

p.19

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

The OECD Due Diligence Guidance is the globally recognized foundation for conflict minerals due diligence and the keystone document from which all conflict minerals standards have been derived.

For a company using the OECD Due Diligence Guidance to comply with the Dodd-Frank Act, the first two steps would be mandatory to be judged to have done risk assessment satisfactorily wherever they are operating. Only if ‘red-flag’ issues are identified during the risk assessment process are steps three to five then triggered.

RED FLAGS THAT TRIGGER OECD GUIDANCE STEPS 3-5

Red flag locations of mineral origin and transit• Mineral is from, or has been

transported through, a conflict-affected or high-risk area.

• Mineral from recyclable/ scrap ormixed sources has been refined in a country where mineral from conflict-affected and high-risk areas transits.

Supplier red flags• Suppliers operate in a red flag

location.• Upstream companies have business

interests in mineral suppliers from a red flag location.

• Suppliers / upstream companieshave sourced mineral from a red flag location in the last 12 months.

Red flag circumstances• Step 1 indicates anomalies or unusual

circumstances that reasonably suggest that the mineral extraction, transport or trade may contribute to conflict or serious abuses.

• Sources where there are weakenforcement of anti-money laundering or anti-corruption laws, customs controls, or other relevant laws;

informal banking system; and/or the extensive use of cash (optional red-flag).

The OECD Due Diligence Guidance makes a distinction between due diligence activities for upstream (mine to smelter/refiner) and downstream (smelter/refiner to retailer) actors, with a greater onus of due diligence activities being placed on the smelter/refiner and upstream segment.

INITIATIVES DERIVED FROM THE OECD DUE DILIGENCE GUIDANCE

There are a number of responsible sourcing initiatives which ensure conformance with the due diligence recommendations of the OECD Due Diligence Guidance. These include the Responsible Jewellery Council’s Code of Practices and Chain of Custody Standard (RJC), the World Gold Council’s Conflict-free Gold Standard, the EICC’s Conflict Free Smelter Initiative, the London Bullion Market Association’s Responsible Gold Guidance, and the Dubai Multi Commodities Centre’s Responsible Sourcing Guidance. Not all will apply to your business, and some seek to assure more than the business practices and human rights issues prioritized by the OECD Due Diligence Guidance.

ON THE OECD DUE DILIGENCE GUIDANCE

chap.6

ON THE OECD DUE DILIGENCE GUIDANCE

chap.6

The OECD Due Diligence Guidance 5 Steps:

1. Establish strong company management systems

2. Identify and assess risks in the supply chain

3. Design and implement a strategy to respond to identified risks

4. Carry out independent third-party audit of supply chain due diligenceat identified points in the supply chain

5. Report on supply chain due diligence

p.21

Bur

eau

Veri

tas

& E

stel

le L

evin

LTD

. O

n co

nflic

t min

eral

s ch

alle

nges

and

mov

ing

beyo

nd c

ompl

ianc

e

TRAINING

Bureau Veritas, in partnership with Estelle Levin Ltd. (ELL), offers public training to issuer and non-issuer manufacturers, suppliers, and vendors to educate them on conflict minerals regulations and to present the solutions available to address their challenges and build capacity for action.

Two levels of training are offered:• Conflict Minerals - Executive Overview• Conflict Minerals - Understanding &

Implementing

SYSTEMS GAP ASSESSMENTSAs regulatory deadl ines approach, organizations need to ensure that their conflict minerals due diligence systems are effective and meet Dodd-Frank requirements. Bureau Veritas offers to review due diligence systems to identify any gaps between organizations’ existing systems and the recommendations outlined in the OECD Due Diligence Guidance or a specific industry framework.

THIRD-PARTY AUDITS AND CERTIFICATION

Once due diligence systems are in place, Bureau Veritas provides Conflict Minerals Chain of Custody Certification and Third-Party Audits against industry standards and the OECD Due Diligence Guidance, respectively. Bureau Veritas is an approved auditor for RJC, LBMA, and DMCC chain of custody standards.

Impartial audits ensure accuracy, and reliability, and demonstrate the highest level of commitment.

Benefits of certification and third-party audits:• Streamlined processes and

operational efficiency• Impartial verification of your

compliance• Increase organizational value,

customer perception, and stakeholder relationships

SEC REPORTING

All issuers that are subject to Dodd-Frank Section 1502 are required to file a Form SD, and depending on the origin of their conflict minerals or level of determination, issuers may need to submit a Conflict Minerals Report (CMR). This reporting can be a complementary output of the third-party audit process.The independent private sector audit (IPSA) of Conflict Minerals Reports must be conducted in accordance with the requirements of the Generally Accepted Government Auditing Standards (GAGAS) as established by the U.S. Government Accountability Office (GAO). With core values of integrity and ethics and an established history in impartial counsel, Bureau Veritas meets all GAGAS performance audit requirements and is fully prepared to provide independent private sector audits of Conflict Minerals Reports.

HOW BUREAU VERITAS CAN HELP

chap.6

HOW BUREAU VERITAS CAN HELP

chap.7

Bureau Veritas is a world leader in conformity assessment and certification services. Created in 1828, the Group has almost 59,000 employees in around 1,300 offices and laboratories located in 140 countries. Bureau Veritas helps its clients to improve their performances by offering services and innovative solutions in order to ensure that their assets, products, infrastructure and processes meet standards and regulations in terms of quality, health and safety, environmental protection and social responsibility. With proven experience and expertise in independent third-party auditing, due diligence systems, and chain of custody standards, and with resources around the world, Bureau Veritas is poised to be a leader in conflict minerals solutions. Learn more at www.bureauveritas.com.

ABOUT BUREAU VERITAS

ELL is a specialist consultancy dedicated to responsible mining and sourcing. Working from concept to implementation, we help our clients transform their ideas, businesses, and operations into something more sustainable not just for them, but for their stakeholders, too. We provide world-class research, advisory, and capacity-building services to businesses along the value chain (mining, trading, manufacture, retail), governments, aid agencies, and NGOs. We stand amongst the world’s foremost development consultancies with expertise in Artisanal and Small-scale Mining (ASM) and in the development of responsible sourcing and due diligence systems for minerals, especially from fragile economies. Conflict minerals have been a core specialism for ELL since 2003; we investigate the issues, design the initiatives addressing them, educate stakeholders, and support companies in supply chain due diligence and conflict minerals management. Learn more at www.estellelevin.com and www.asm-pace.org.

ABOUT ESTELLE LEVIN LIMITED

Credits :Contributors : François Heuzé, Estelle Levin, and Lucas Lopez-VidelaGraphic design and illustration : www.distillateurgraphik.comPhotos : cover © William Warby © Alchemist-hp / p4. © Carlos Aguilar / p5. © Alchemist-hp © Jurii © Paulrommer - Fotolia © Vitaly Korovin - Fotolia / p6. © Alchemist-hp / p8. © Vitaly Korovin - Fotolia / p9. © Africa Studio - fotolia © Laura Lartigue / p10. © webphotographeer - Istock / p11. © Fabio Filzi - IStock / p12. © Paulrommer / p13. © Djgunner - Istock / p14. © Brasil2 - Istock / p15. © Hidesy - Istock / p18. © Malajscy - Fotolia / p21. © Urbancow - Istock.

BUREAU VERITAS & ESTELLE LEVIN LTD. ON CONFLICT MINERALS CHALLENGES

AND MOVING BEYOND COMPLIANCE