Embed Size (px)

Citation preview

1

Concept of control

• Ensuring that implementation is done as per plans.

Steps :1. Set standards2. Communicate standards3. Compare standards with actual performance4. Report deviations5. Take corrective actions.

2

Control Process in General

• Four basic elements –– Detector (actual measurement)– Assessor (comparison with standard)– Effector (alteration of behavior, if required)– Communication network (transmission of

information)

3

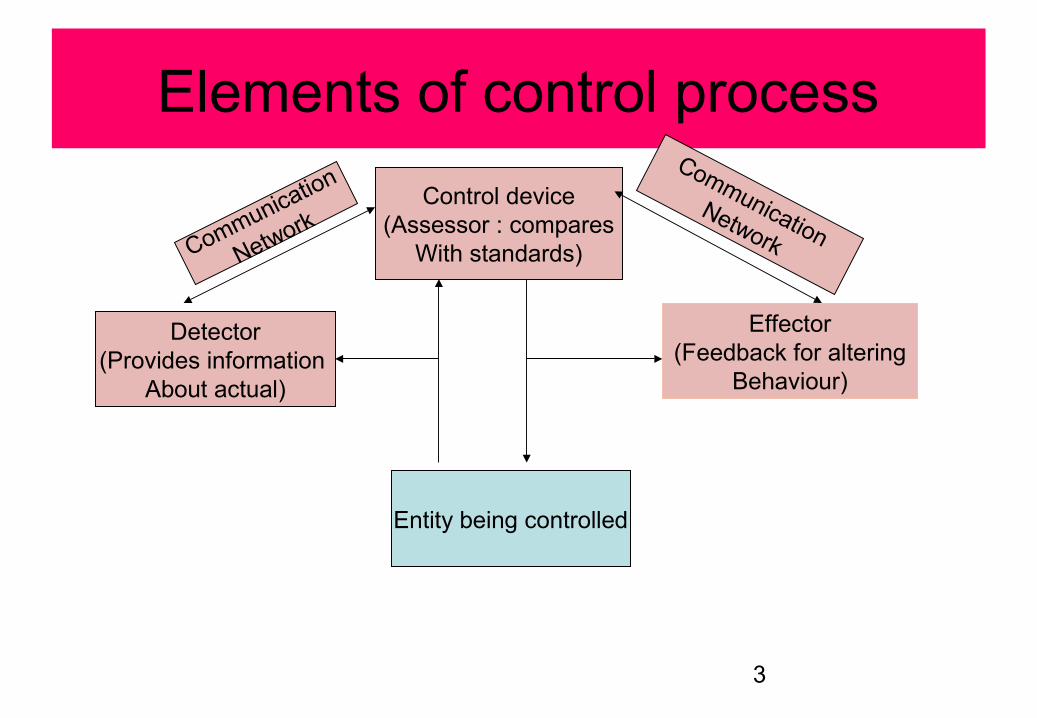

Elements of control process

Control device(Assessor : compares

With standards)

Detector(Provides information

About actual)

Effector(Feedback for altering

Behaviour)

Entity being controlled

Communication

Network

Communication Network

4

Concept of MCS• Management Control :

“Mgt control is the process by which managers assure that the resources obtained are used efficiently and effectively in the accomplishment of organizational goals” : Anthony

Efficiency : doing the things right ie. Relationship between input and output

I/P efficiency O/P

Effectiveness : doing the right things ie. Relationship between output and objectives

O/P effectiveness OBJECTIVES

System is a prescribed way or a systematic way of carrying out a set of activities which are usually repetitive in nature

5

MCS

• “MCS is a total system i.e. it covers all aspects of the firms’ operations to assure that all parts of the operations are in balance with each other”: Anthony

• “MCS refers to a framework or a set up by which the managers can ensure control over the actions of the actions of his subordinates as well as control over entire operations in the organization.” : Saravanavel

6

Characteristics of MCS

• Systematic method• Result oriented• Covers all operations• Based on the concept of Responsibility Centres

• Covers both efficiency and effectiveness

• Control of managerial performance• Regular process• Ensures goal congruence

7

Designing MCS for an organization

• Pre – requisites1. Control requires plans2. Clear org structure3. Active top mgt involvement4. Participation and motivation of employees5. Proper MIS6. Proper accounting system ( responsibility

accounting)

8

……………..Designing

• Steps

1. Classifying org into responsibility centres(RC)

2. Fixing responsibility of each RC

3. Deciding key variables for performance assessment

4. Developing MIS

5. Finding deviations and relating it to individual responsibility

6. Performance reporting to top mgt

7. Short term remedial actions and long term measures for controlling deviation

9

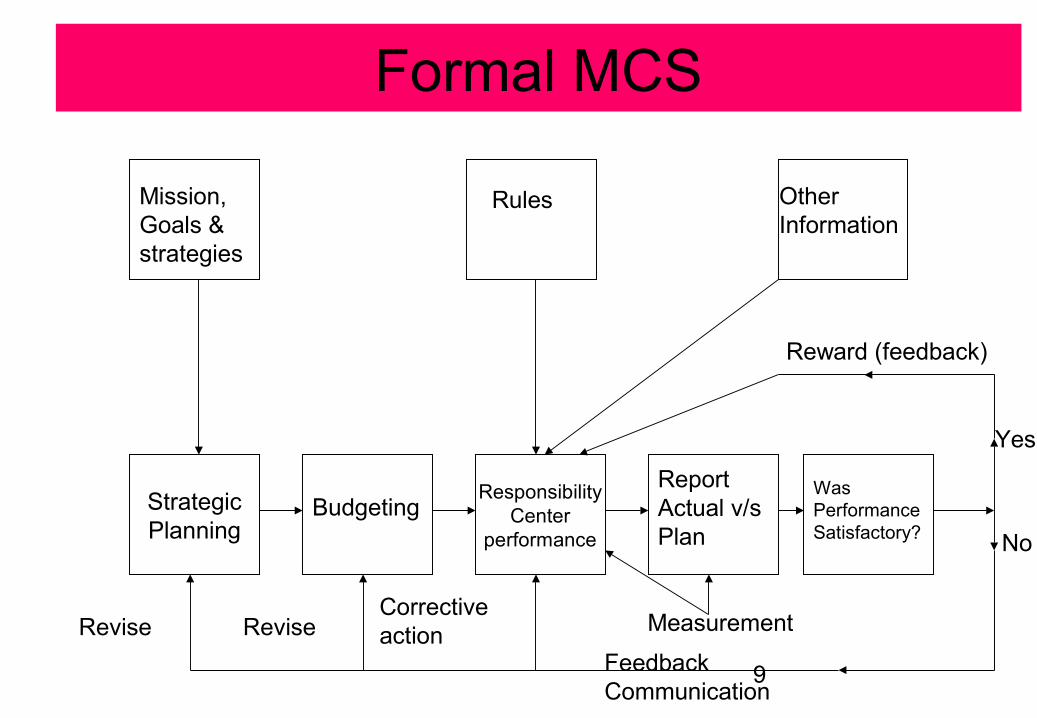

Formal MCS

ResponsibilityCenter

performance

StrategicPlanning

Mission,Goals & strategies

Rules OtherInformation

BudgetingReportActual v/sPlan

WasPerformanceSatisfactory?

Revise ReviseCorrectiveaction Measurement

FeedbackCommunication

Reward (feedback)

Yes

No

10

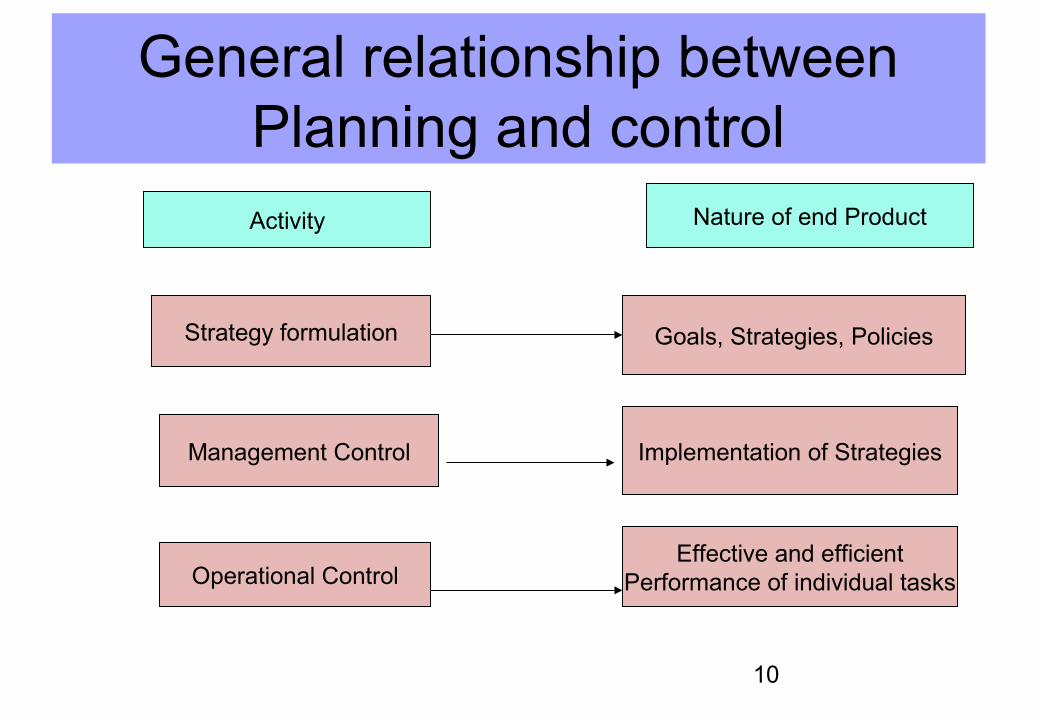

General relationship between Planning and control

Activity Nature of end Product

Strategy formulation

Management Control

Operational Control

Goals, Strategies, Policies

Implementation of Strategies

Effective and efficientPerformance of individual tasks

11

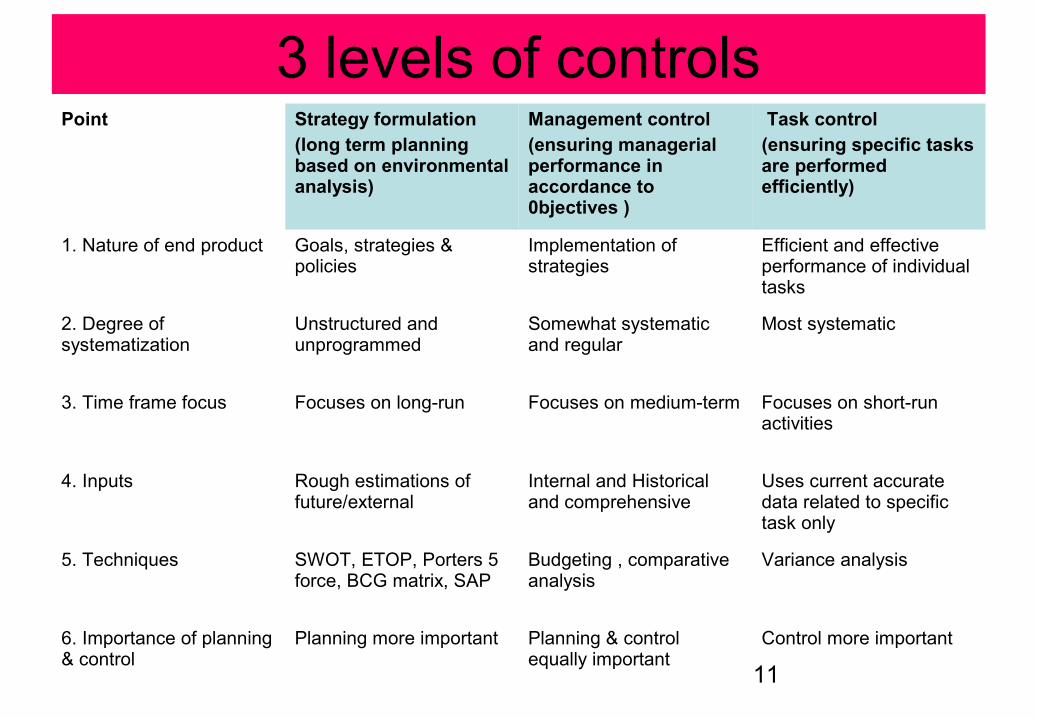

3 levels of controlsPoint Strategy formulation

(long term planning based on environmental analysis)

Management control(ensuring managerial performance in accordance to 0bjectives )

Task control(ensuring specific tasks are performed efficiently)

1. Nature of end product Goals, strategies & policies

Implementation of strategies

Efficient and effective performance of individual tasks

2. Degree of systematization

Unstructured and unprogrammed

Somewhat systematic and regular

Most systematic

3. Time frame focus Focuses on long-run Focuses on medium-term Focuses on short-run activities

4. Inputs Rough estimations of future/external

Internal and Historical and comprehensive

Uses current accurate data related to specific task only

5. Techniques SWOT, ETOP, Porters 5 force, BCG matrix, SAP

Budgeting , comparative analysis

Variance analysis

6. Importance of planning & control

Planning more important Planning & control equally important

Control more important

12

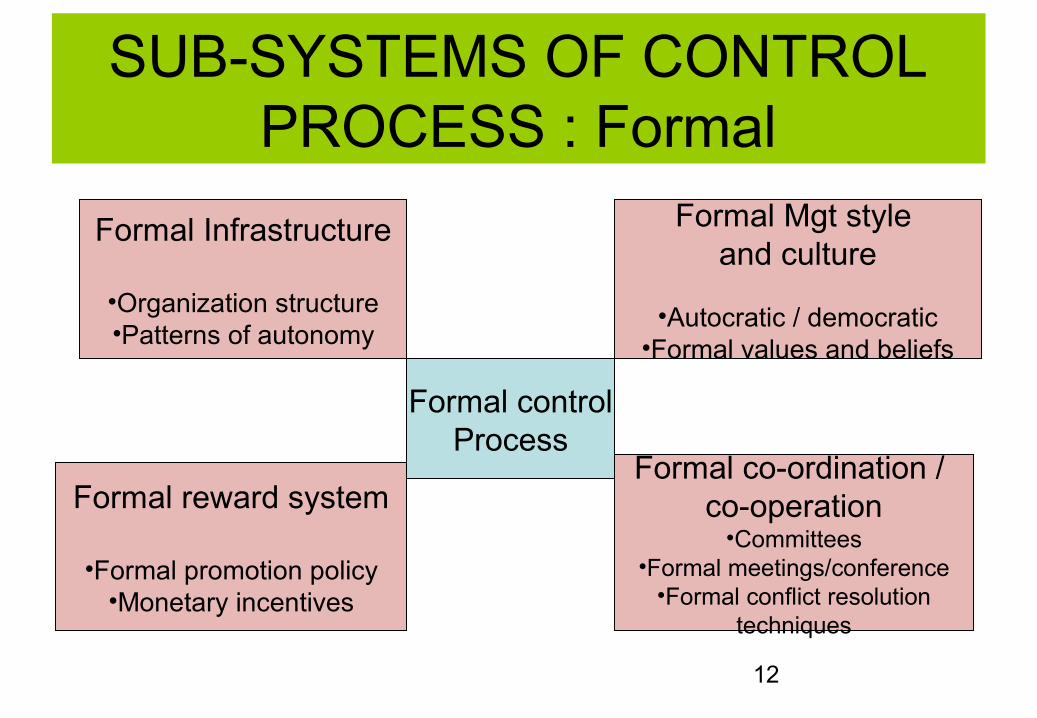

SUB-SYSTEMS OF CONTROL PROCESS : Formal

Formal Infrastructure

•Organization structure•Patterns of autonomy

Formal Mgt style and culture

•Autocratic / democratic•Formal values and beliefs

Formal reward system

•Formal promotion policy•Monetary incentives

Formal co-ordination / co-operation

•Committees•Formal meetings/conference

•Formal conflict resolutiontechniques

Formal controlProcess

13

SUB-SYSTEMS OF CONTROL PROCESS : Informal

• Informal control is :

1. Ad- hoc ( as and when required)

2. Based on intuition, experience, rationalization

3. No specific procedure.

14

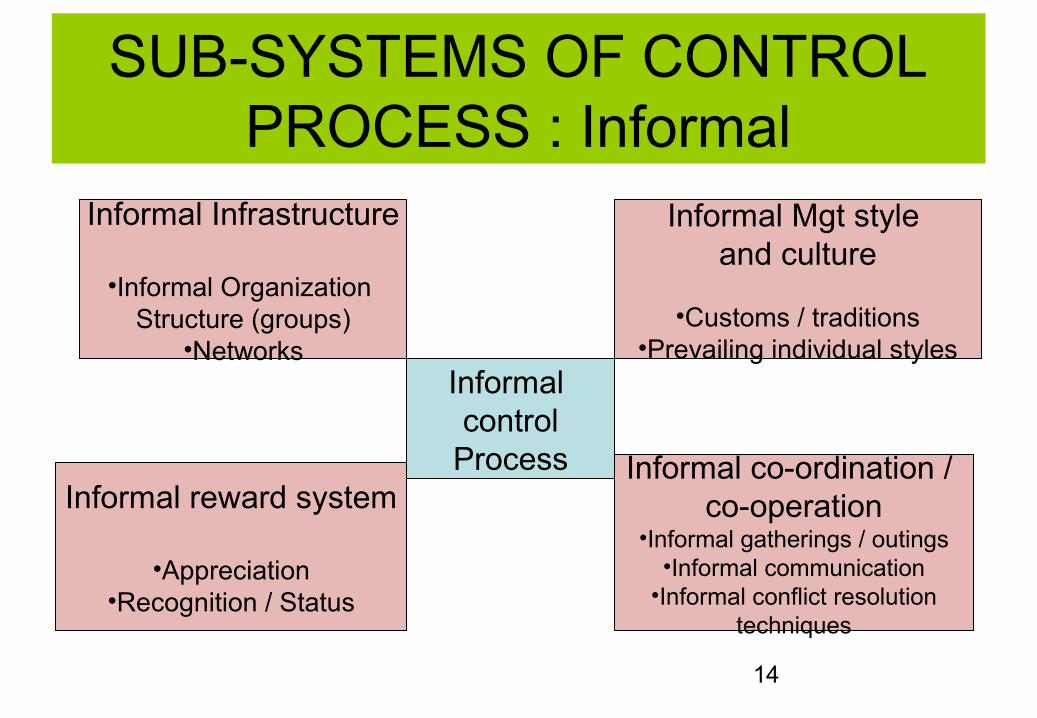

SUB-SYSTEMS OF CONTROL PROCESS : Informal

Informal Infrastructure

•Informal Organization Structure (groups)

•Networks

Informal Mgt style and culture

•Customs / traditions•Prevailing individual styles

Informal reward system

•Appreciation•Recognition / Status

Informal co-ordination / co-operation

•Informal gatherings / outings•Informal communication

•Informal conflict resolutiontechniques

Informal control

Process

15

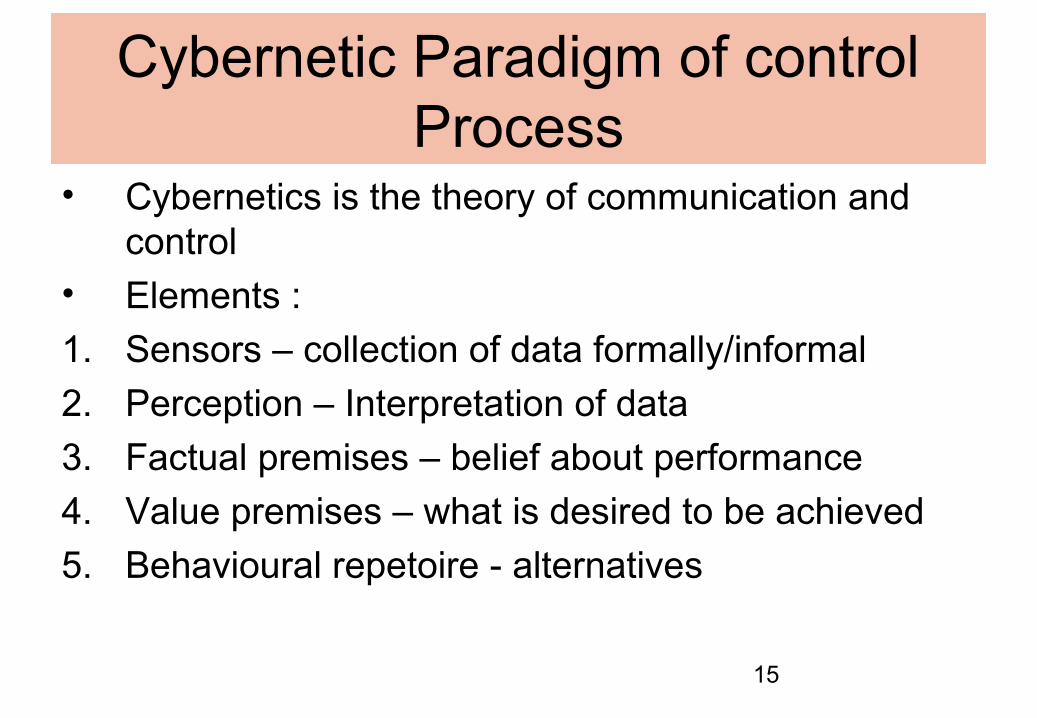

Cybernetic Paradigm of control Process

• Cybernetics is the theory of communication and control

• Elements :

1. Sensors – collection of data formally/informal

2. Perception – Interpretation of data

3. Factual premises – belief about performance

4. Value premises – what is desired to be achieved

5. Behavioural repetoire - alternatives

16

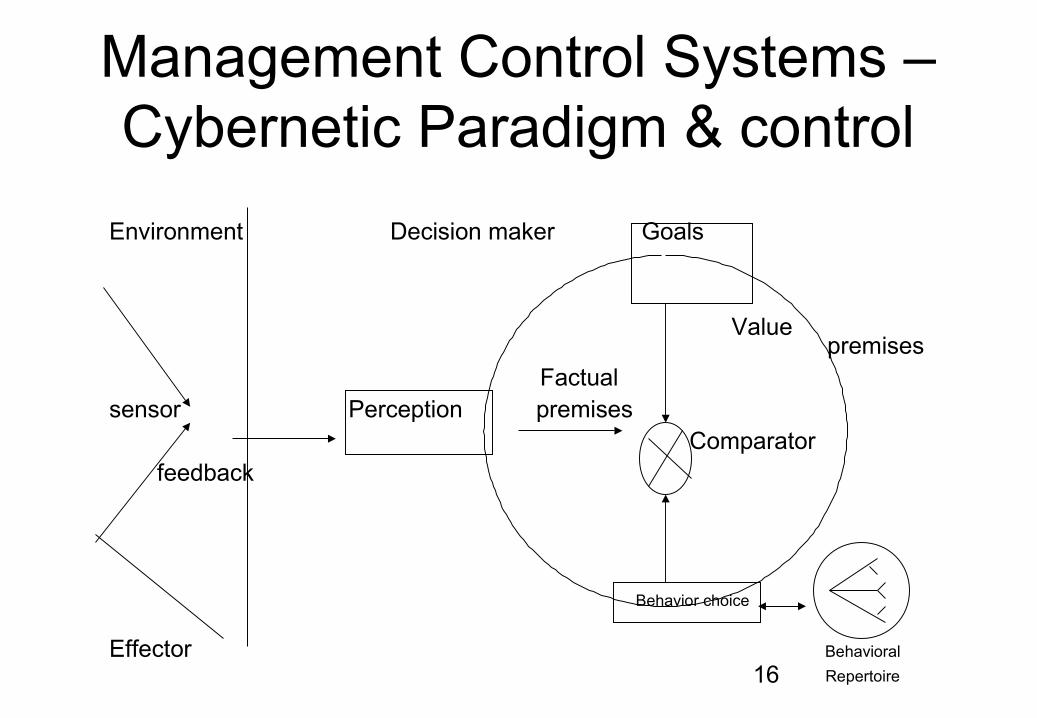

Management Control Systems – Cybernetic Paradigm & control

Environment Decision maker Goals

Value premises

Factualsensor Perception premises Comparator

feedback

Behavior choice

Effector Behavioral

Repertoire

17

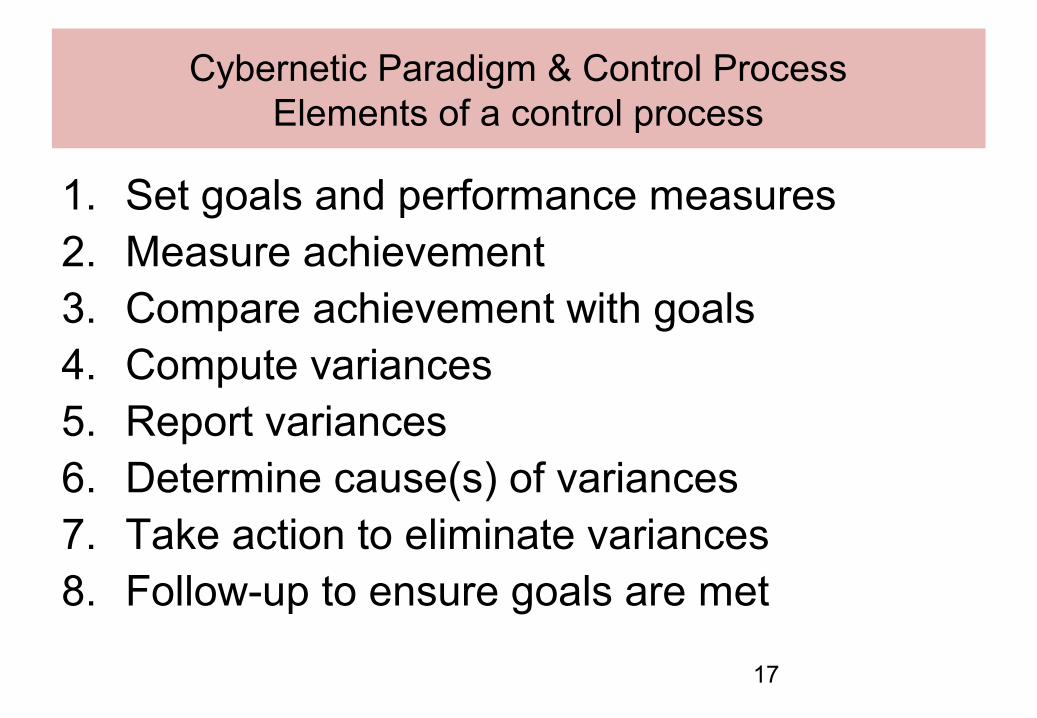

Cybernetic Paradigm & Control ProcessElements of a control process

1. Set goals and performance measures2. Measure achievement3. Compare achievement with goals4. Compute variances5. Report variances6. Determine cause(s) of variances7. Take action to eliminate variances8. Follow-up to ensure goals are met

18

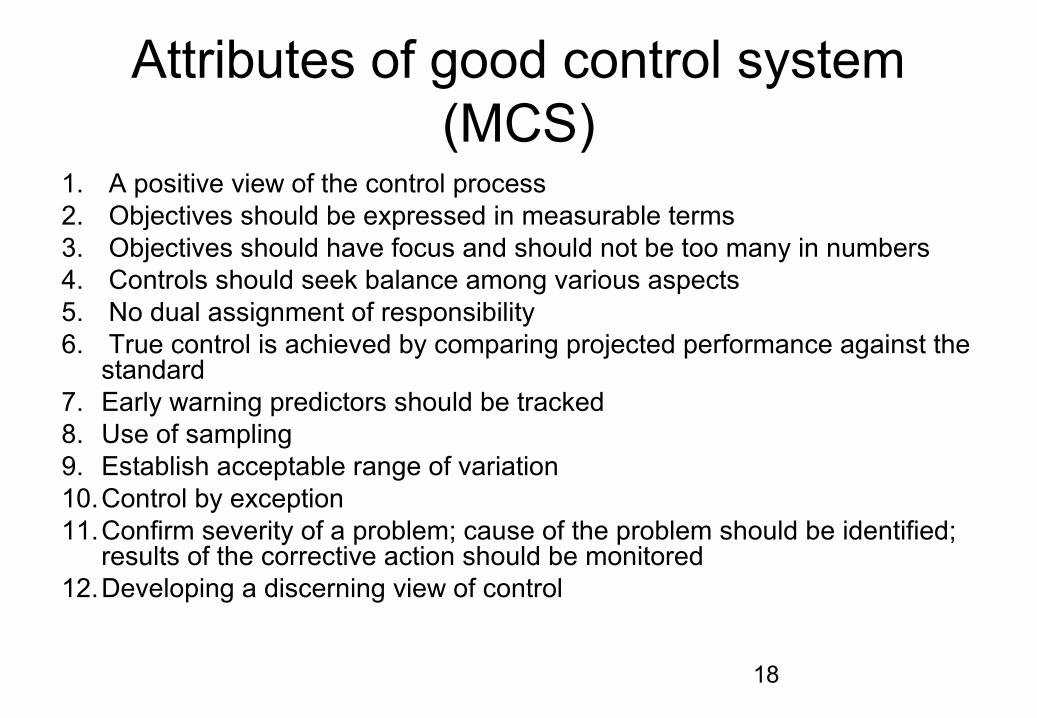

Attributes of good control system (MCS)

1. A positive view of the control process2. Objectives should be expressed in measurable terms3. Objectives should have focus and should not be too many in numbers4. Controls should seek balance among various aspects5. No dual assignment of responsibility6. True control is achieved by comparing projected performance against the

standard7. Early warning predictors should be tracked8. Use of sampling9. Establish acceptable range of variation10.Control by exception11.Confirm severity of a problem; cause of the problem should be identified;

results of the corrective action should be monitored12.Developing a discerning view of control

19

Understanding strategies – Concept of strategy

• Strategy describes the general direction in which an organization plans to move to attain its goals

• Strategy formulation – Environmental analysis pointing out opportunities and threats, simultaneous internal analysis revealing strengths and weaknesses, matching core competencies with external opportunities and deciding a strategy

20

Understanding strategies – Corporate and unit-level strategies

• Corporate strategy is concerned more with where to compete than how to compete; the latter is a matter of unit level strategy

• Classification into 3 types for corporate level – Single industry– Related diversification– Unrelated diversification

• Research has shown that, on average, related diversified firms perform the best, single industry perform next best, and unrelated diversified firms do not perform well over the long run. This is because Corporate HQ, in the related diversified firm, has the ability to transfer core competencies from one business unit to another.

21

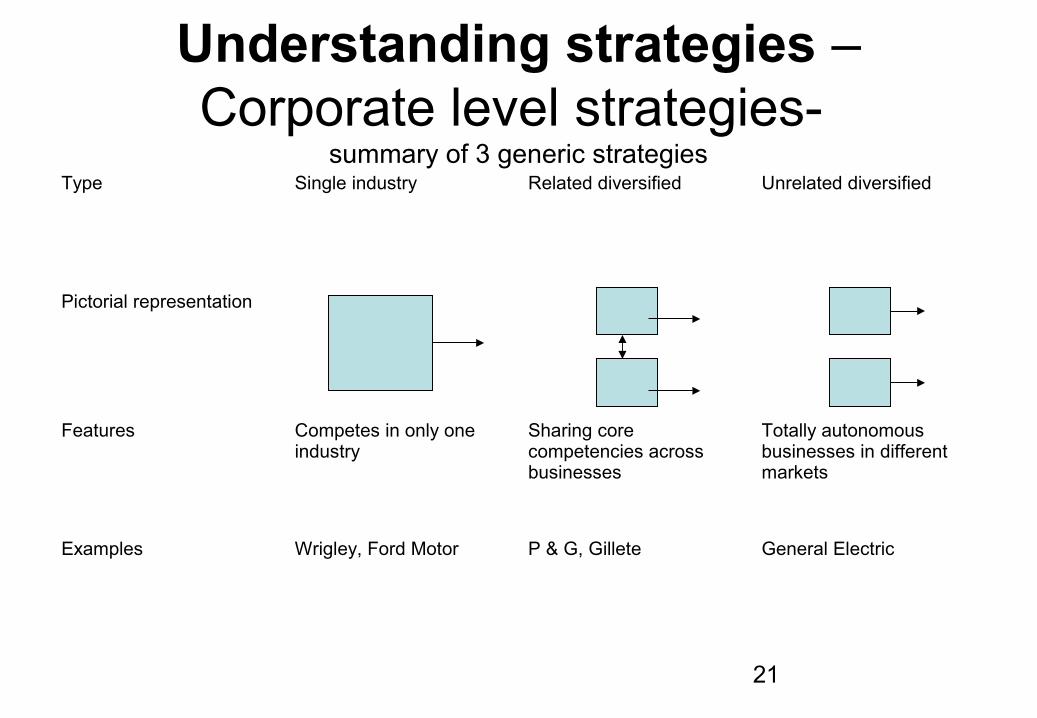

Understanding strategies – Corporate level strategies-

summary of 3 generic strategiesType Single industry Related diversified Unrelated diversified

Pictorial representation

Features Competes in only one industry

Sharing core competencies across businesses

Totally autonomous businesses in different markets

Examples Wrigley, Ford Motor P & G, Gillete General Electric

22

Understanding strategies –Unit-level strategies

• Business unit strategies depend on two interrelated aspects 1) its mission & 2)its competitive advantage

• There are a couple of famous models to fix the BU mission• One is the BCG Model and the other one is the GE Planning

Model• These models basically try to match the industry and the unit

in terms of opportunities/threats and strengths/weaknesses• Control system designers need to know what is the BU

mission but not necessarily why the BU has chosen that mission

23

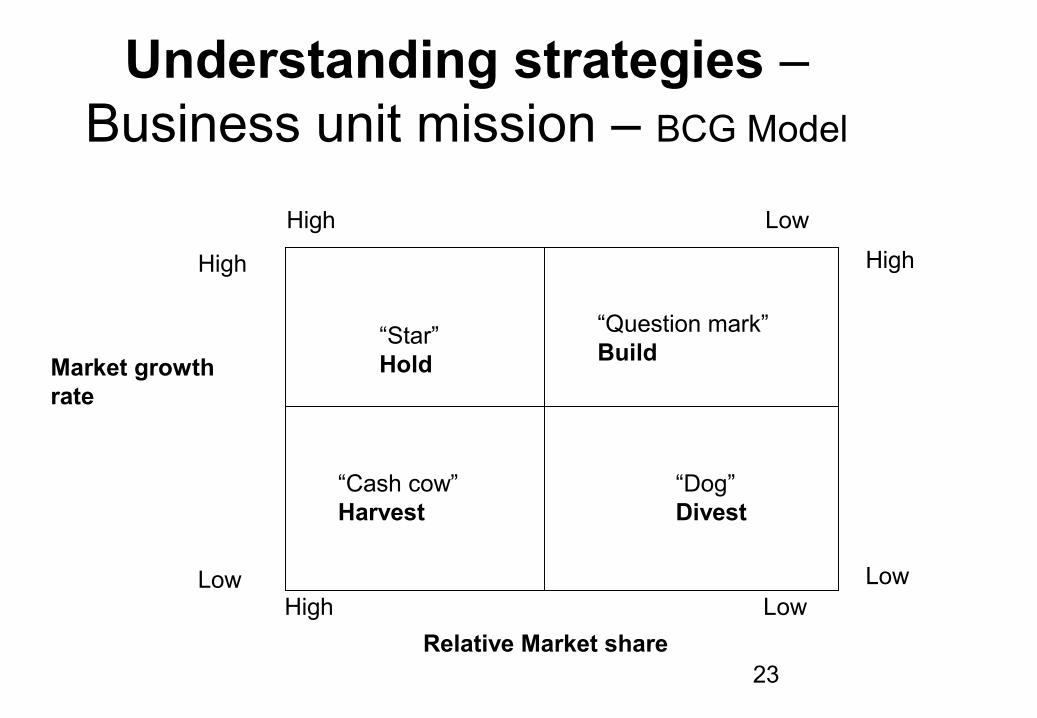

Understanding strategies – Business unit mission – BCG Model

“Star”Hold

“Question mark”Build

“Cash cow”Harvest

“Dog”Divest

Market growthrate

Relative Market share

High Low

High Low

High

Low

High

Low

24

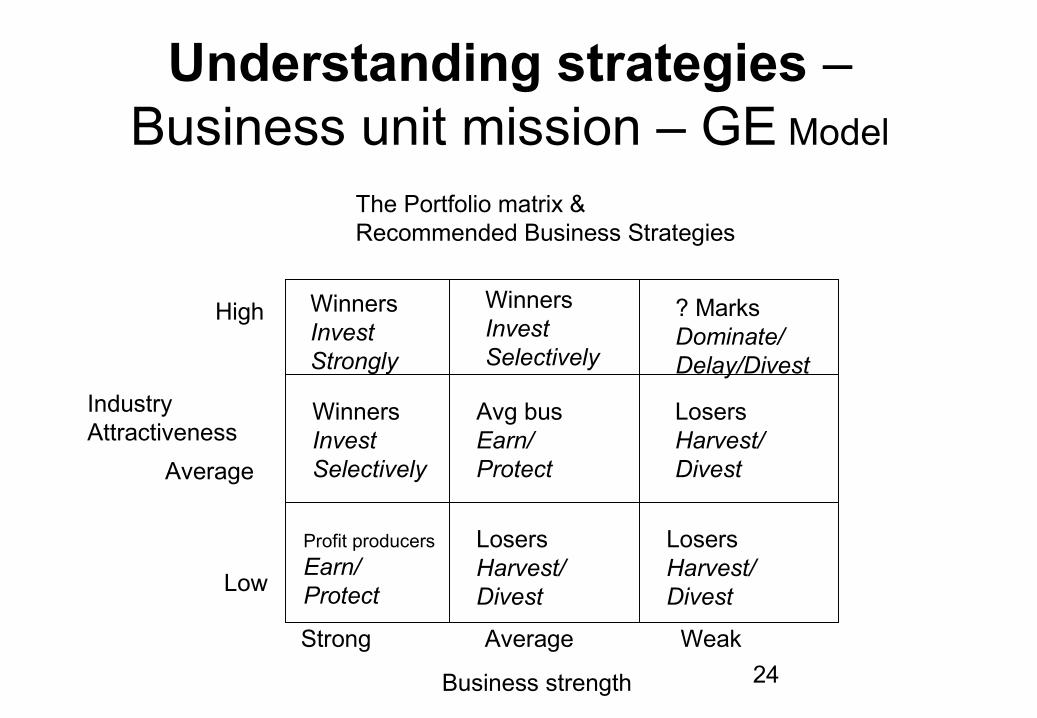

Understanding strategies – Business unit mission – GE Model

IndustryAttractiveness

Business strength

High

Average

Low

Strong Average Weak

WinnersInvest Strongly

WinnersInvest Selectively

Profit producers

Earn/Protect

WinnersInvest Selectively

Avg busEarn/Protect

LosersHarvest/Divest

? MarksDominate/Delay/Divest

LosersHarvest/Divest

LosersHarvest/Divest

The Portfolio matrix & Recommended Business Strategies

25

Understanding strategies – Gaining competitive advantage

• 3 interrelated questions should be considered – – What is the industry structure?– How should the BU exploit it?– What will be the basis of the BU’s competitive advantage?

• Michael Porter has suggested 2 analytical approaches to develop & sustain competitive advantage –

Industry analysis & Value chain analysis

26

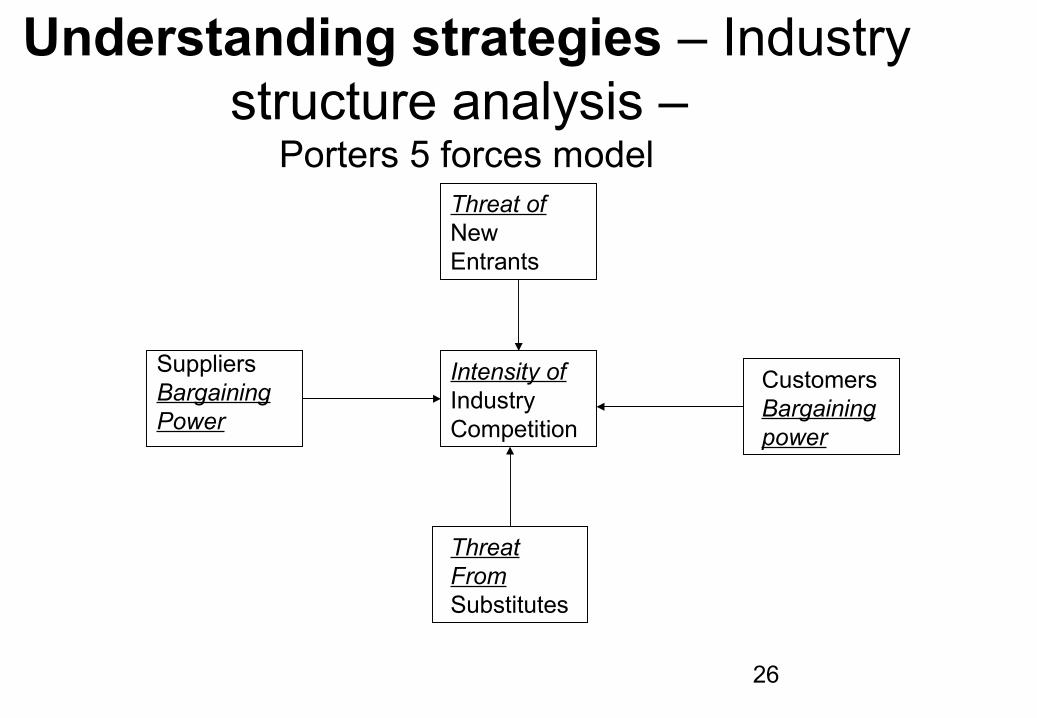

Understanding strategies – Industry structure analysis –

Porters 5 forces modelThreat of NewEntrants

Intensity ofIndustryCompetition

ThreatFromSubstitutes

Suppliers BargainingPower

CustomersBargainingpower

27

Understanding strategies – Industry structure analysis –

Porters 5 forces model• 3 observations with regard to industry analysis

– More powerful the 5 forces less profitable an industry is likely to be; conversely in high profitable industries these 5 forces are not strong

– Depending on relative strength of the 5 forces the strategic issues would emerge and would differ from industry to industry

– Understanding the nature of each force helps the firm to formulate effective strategies

28

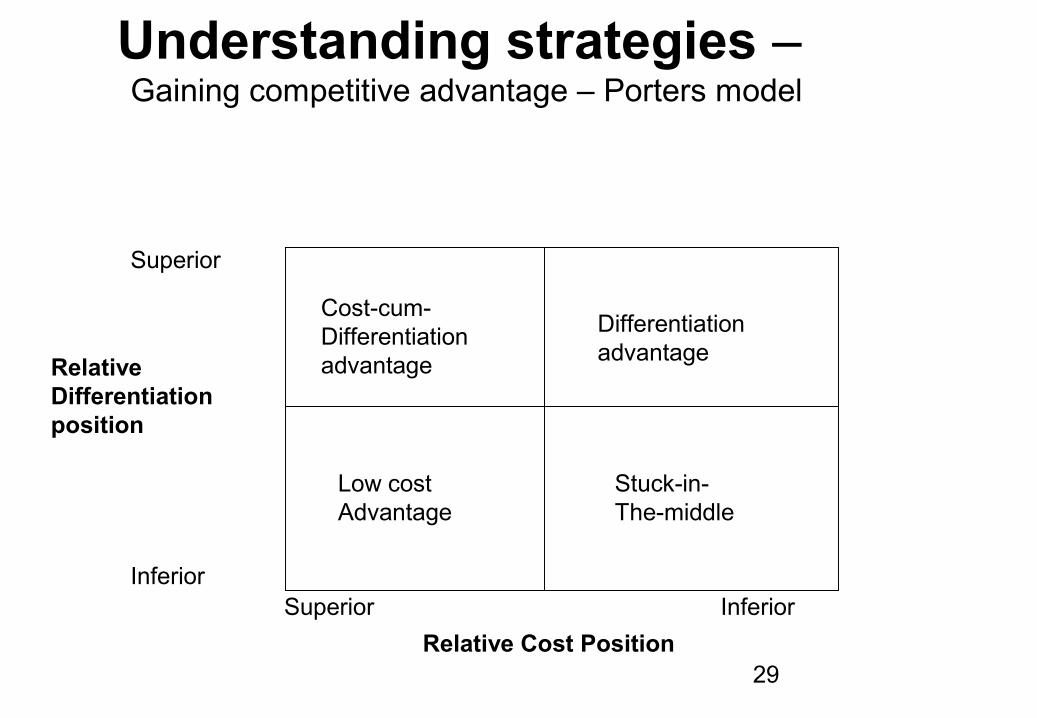

Understanding strategies – Gaining competitive advantage – Porters model

• The 5 force analysis is starting point to develop competitive advantage as it helps understanding external environment

• Response from the firm can be on two fronts – low cost & differentiation

• A firm should strive to achieve cost leadership and/or product differentiation to gain competitive advantage

29

Understanding strategies – Gaining competitive advantage – Porters model

Cost-cum-Differentiationadvantage

Differentiationadvantage

Low cost Advantage

Stuck-in-The-middle

RelativeDifferentiationposition

Relative Cost Position

Superior Inferior

Superior

Inferior

30

Understanding strategies – Gaining competitive advantage –

Value chain analysis

• Value chain disaggregates the firm into its distinct strategic activities

• It is a complete set of activities involved in a product beginning with extraction of raw material and ending with after sales service

• The VC framework is a method of breaking down the chain into specific activities in order to understand behavior of costs and sources of differentiation.

31

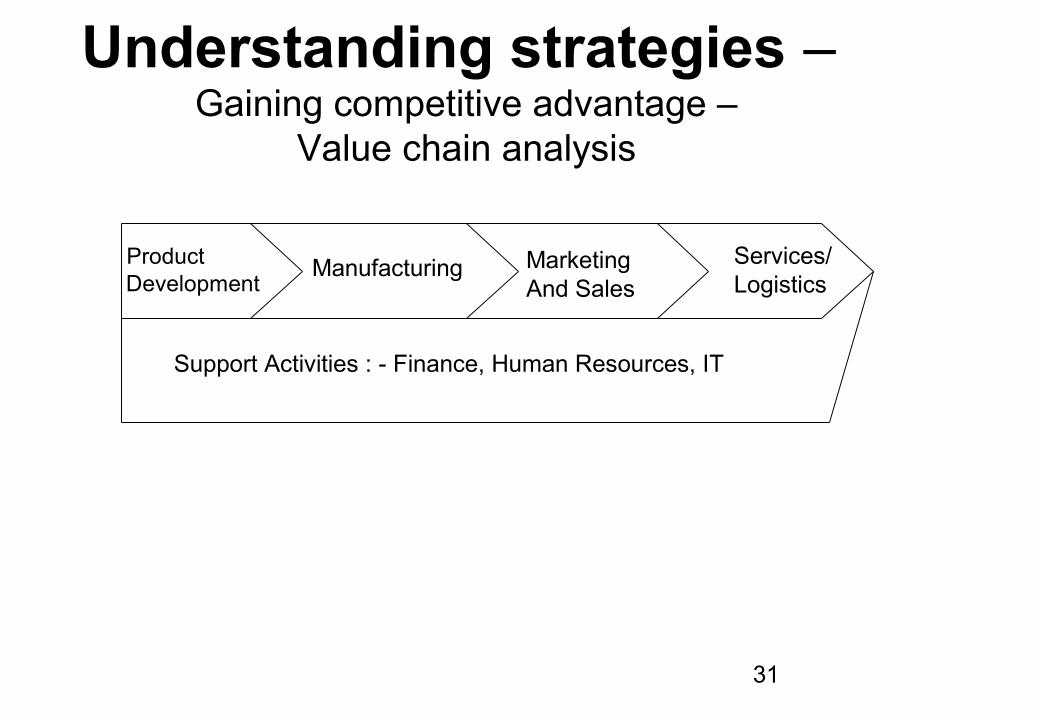

Understanding strategies – Gaining competitive advantage –

Value chain analysis

Product Development

Manufacturing MarketingAnd Sales

Services/Logistics

Support Activities : - Finance, Human Resources, IT

32

Understanding strategies – Gaining competitive advantage –

Value chain analysis

• For each value added activity, key questions are –1. Can we reduce costs in this activity, holding value (revenues)?

2. Can we increase value (revenues) in this activity holding costs constant?

3. Can we reduce assets in this activity holding costs and value (revenues) constant?

4. Most importantly can we do 1, 2 & 3 simultaneously?

• By systematically analyzing costs, revenues and assets in each activity, BU can achieve cost-cum-differentiation advantage.

33

Goal Congruence

• Central purpose of a MCS is to ensure a high level of goal congruence

• In a goal congruent process actions people are led to take in accordance with their perceived self-interest are also in the best interest of the organization

• In evaluating any management control practice, 2 most important questions are –

• What actions does it motivate people to take in their own self-interest?

• Are these actions in the best interest of the organization?

34

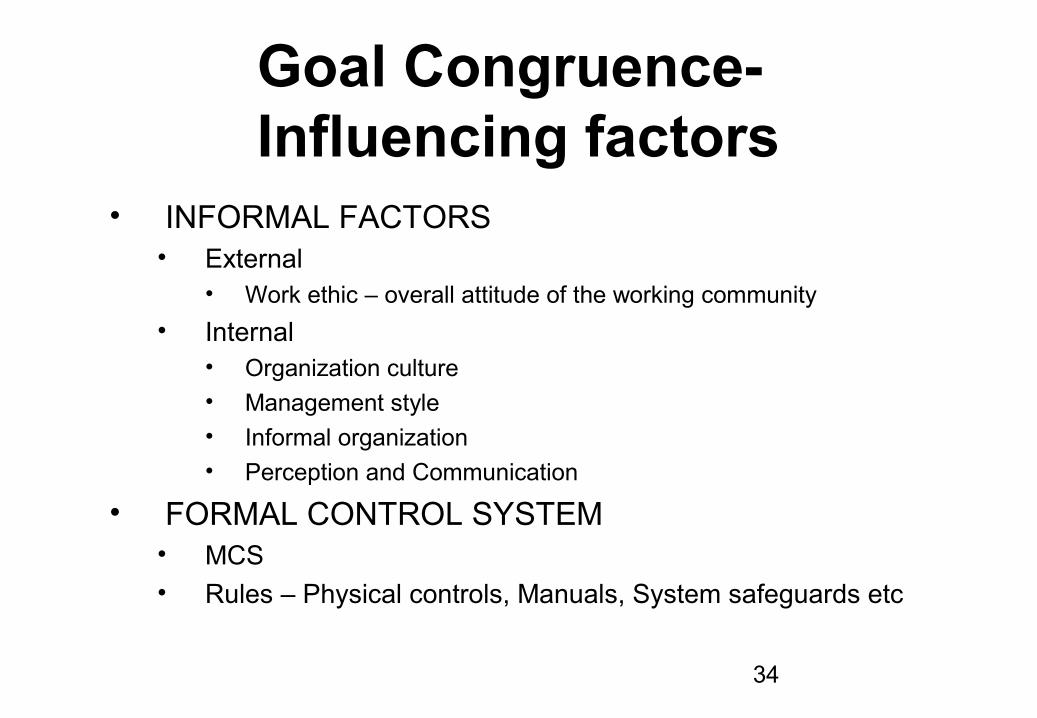

Goal Congruence- Influencing factors

• INFORMAL FACTORS• External

• Work ethic – overall attitude of the working community

• Internal• Organization culture• Management style• Informal organization• Perception and Communication

• FORMAL CONTROL SYSTEM• MCS• Rules – Physical controls, Manuals, System safeguards etc

35

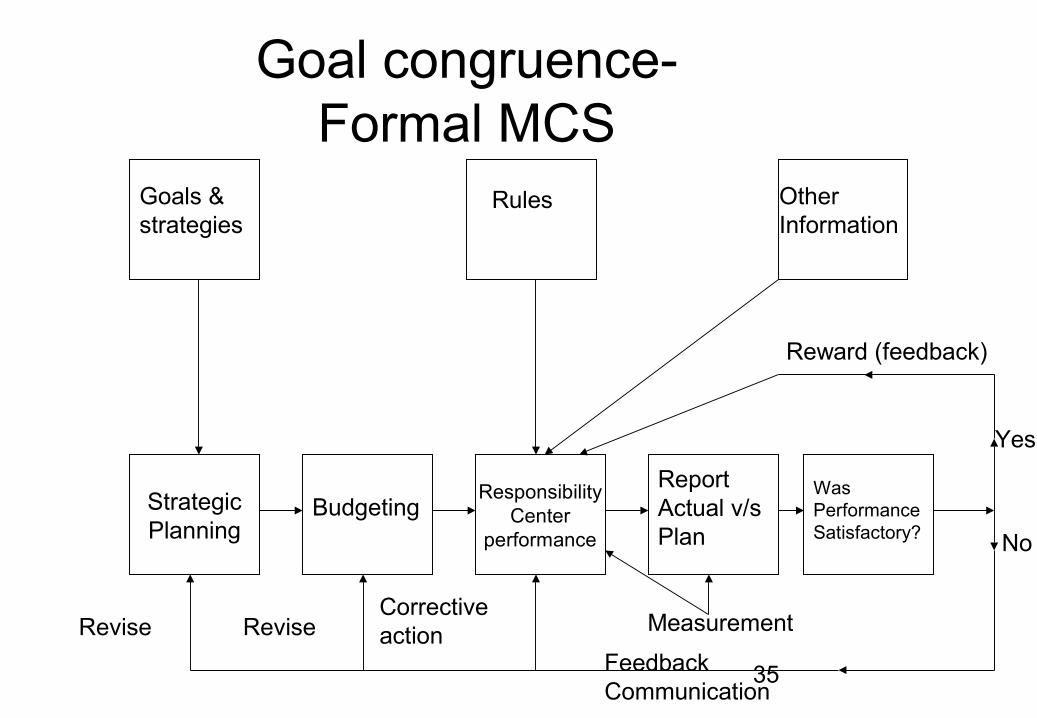

Goal congruence-Formal MCS

ResponsibilityCenter

performance

StrategicPlanning

Goals & strategies

Rules OtherInformation

BudgetingReportActual v/sPlan

WasPerformanceSatisfactory?

Revise ReviseCorrectiveaction Measurement

FeedbackCommunication

Reward (feedback)

Yes

No

36

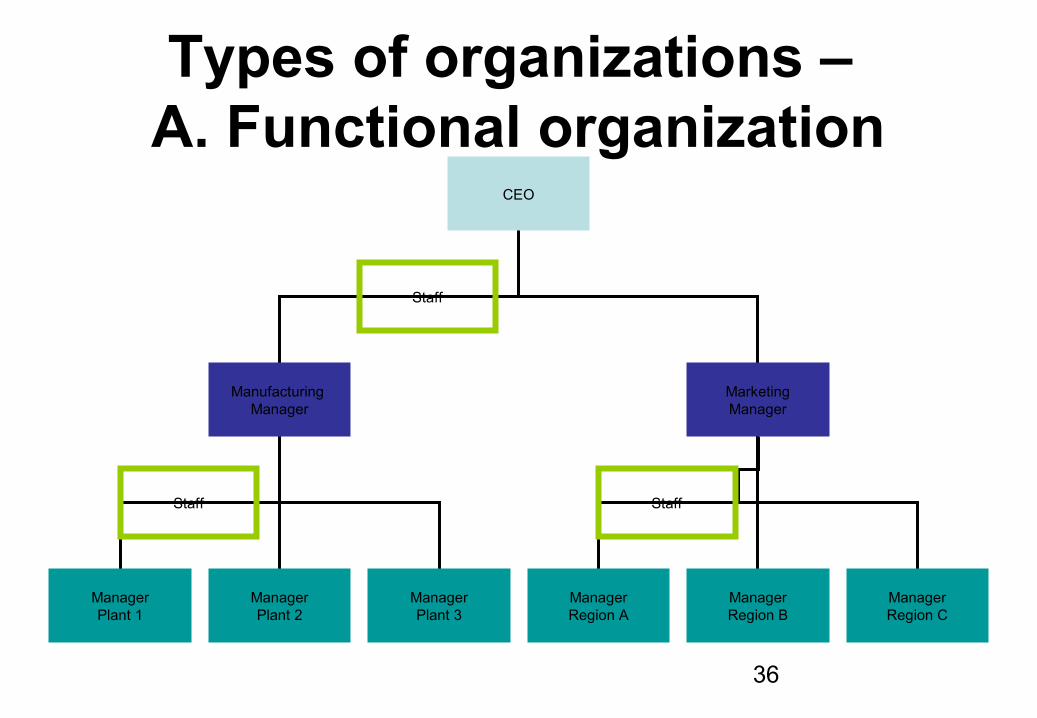

Types of organizations – A. Functional organization

CEO

Manufacturing Manager

MarketingManager

Staff

ManagerPlant 1

ManagerPlant 2

ManagerPlant 3

ManagerRegion A

ManagerRegion B

ManagerRegion C

Staff Staff

37

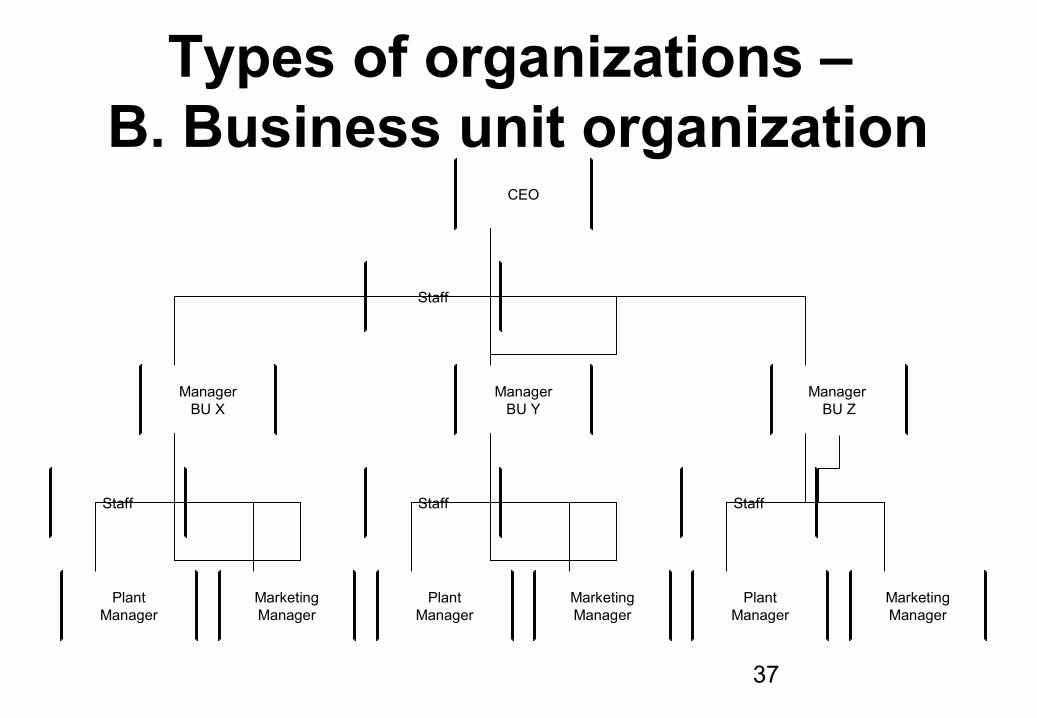

Types of organizations – B. Business unit organization

CEO

ManagerBU X

ManagerBU Y

Staff

PlantManager

MarketingManager

PlantManager

MarketingManager

Staff Staff

Manager BU Z

PlantManager

MarketingManager

Staff

38

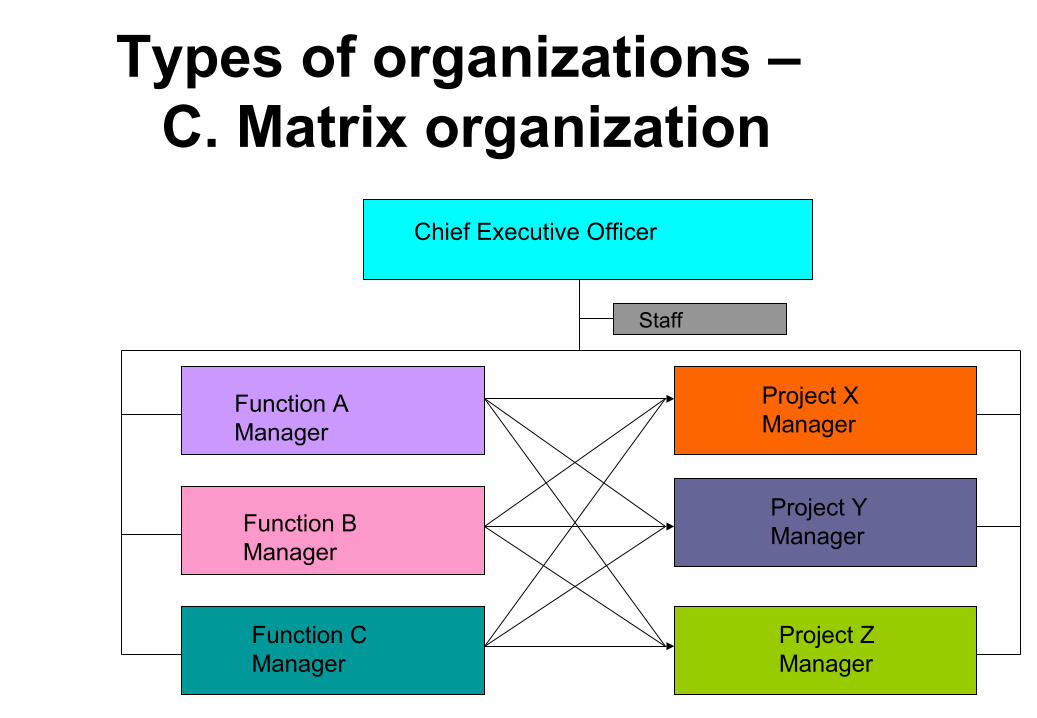

Types of organizations – C. Matrix organization

Chief Executive Officer

Staff

Function AManager

Function BManager

Function CManager

Project XManager

Project YManager

Project ZManager

39

Organization Structure & implications for system design

• Designers might be tempted to recommend the BU structure because of the apparently clear-cut profit responsibility. However they should not forget other considerations.

• The system designer must always fit the system to the organization rather than the other way around

40

Functions of the Controller

• Design and operate information and control systems• Preparing financial statements and reports• Preparing and analyzing performance reports

• Compiling the annual operating plan (budget)

• Supervising internal audit and accounting control procedures

• Developing subordinates

41

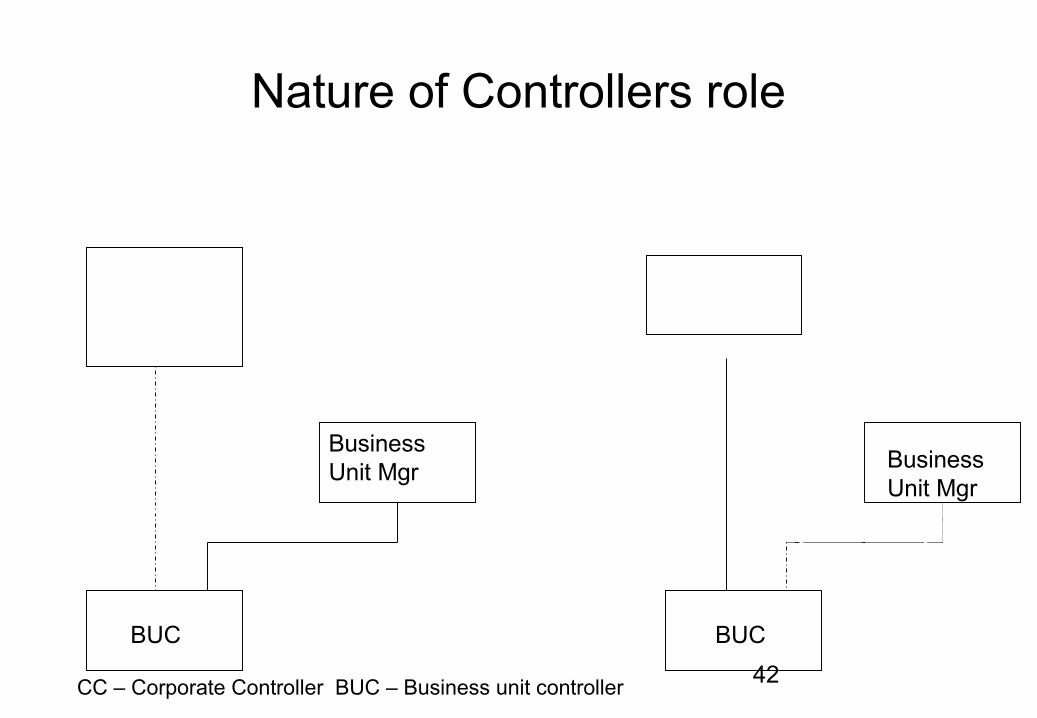

Nature of Controllers role

• Relation to line organization• Controllership is a staff function• Controller designs system, its use is done by line

managers• Decisions made by controllers are primarily those that

implement policies decided by line management• Controllers play important role in preparation of

strategic plans and budgets. • They are also called to scrutinize reports prepared by

line managers

42

Nature of Controllers role

Business Unit Mgr

BUC BUC

CC – Corporate Controller BUC – Business unit controller

Business Unit Mgr

43

Responsibility Centers - Basic

• Responsibility Centers (RC) constitute the structure of a control system and the assignment of responsibility to organizational units must reflect the organizations strategy.

• RC is an organization unit that is headed by a manager who is responsible for its activities

• RC exists to accomplish some purpose that are called as its objectives

44

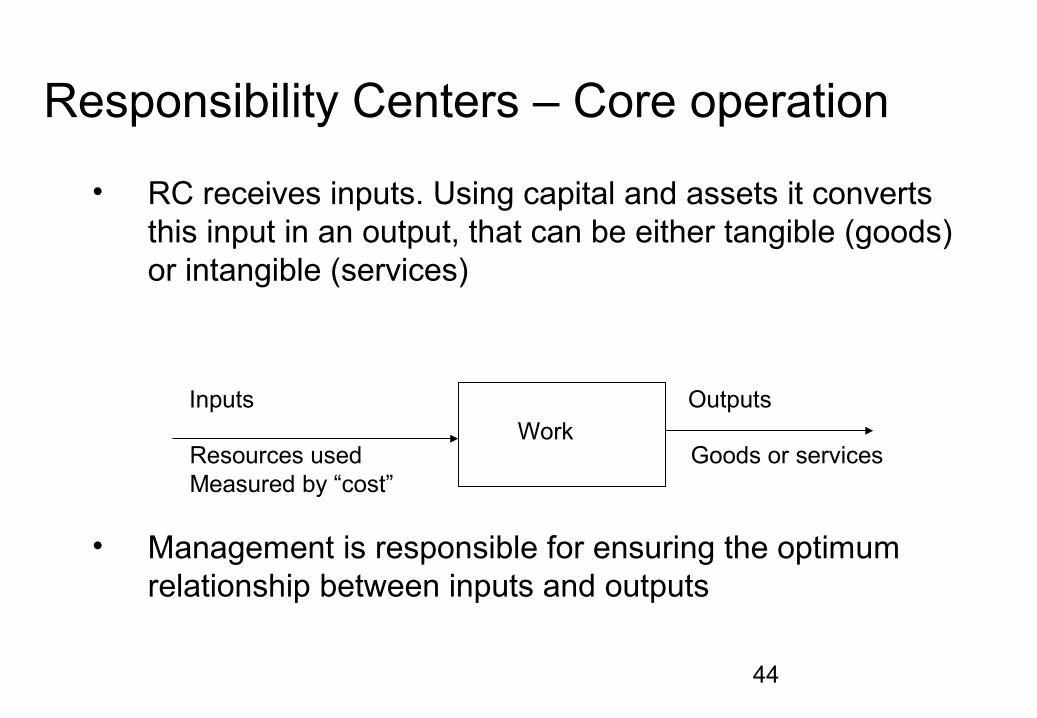

Responsibility Centers – Core operation

• RC receives inputs. Using capital and assets it converts this input in an output, that can be either tangible (goods) or intangible (services)

• Management is responsible for ensuring the optimum relationship between inputs and outputs

WorkInputs Outputs

Resources usedMeasured by “cost”

Goods or services

45

Responsibility Centers – Measuring inputs and outputs

• Cost is a monetary measure of the amount of resources used by a RC

• It is much easier to measure the cost of input than to calculate the value of outputs. For example, a college can easily measure how many students have passed but it is difficult to measure how much education each of them acquired

46

Responsibility Centers – Measuring inputs and outputs – Efficiency and Effectiveness

• Efficiency and effectiveness are the 2 performance measurement criteria for RC

• Efficiency is a ratio of input to output (doing things right)• Effectiveness is determined by the relationship between

a RC’s output and its objectives (doing right things)• These 2 e’s are not mutually exclusive; each RC has to

be efficient and effective as well• Profit as a measure of performance measures both

efficiency and effectiveness because profit is the major objective (effectiveness) and it is also the difference between output and input (efficiency)

47

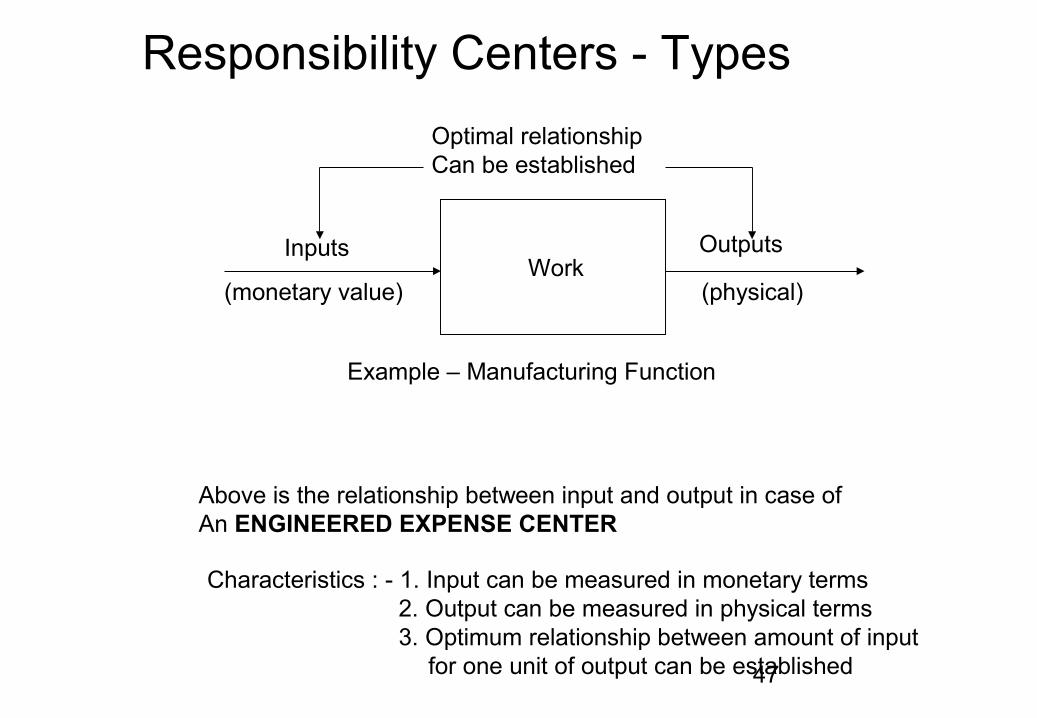

Responsibility Centers - Types

InputsWork

Outputs

(monetary value) (physical)

Optimal relationshipCan be established

Example – Manufacturing Function

Above is the relationship between input and output in case ofAn ENGINEERED EXPENSE CENTER

Characteristics : - 1. Input can be measured in monetary terms2. Output can be measured in physical terms3. Optimum relationship between amount of input

for one unit of output can be established

48

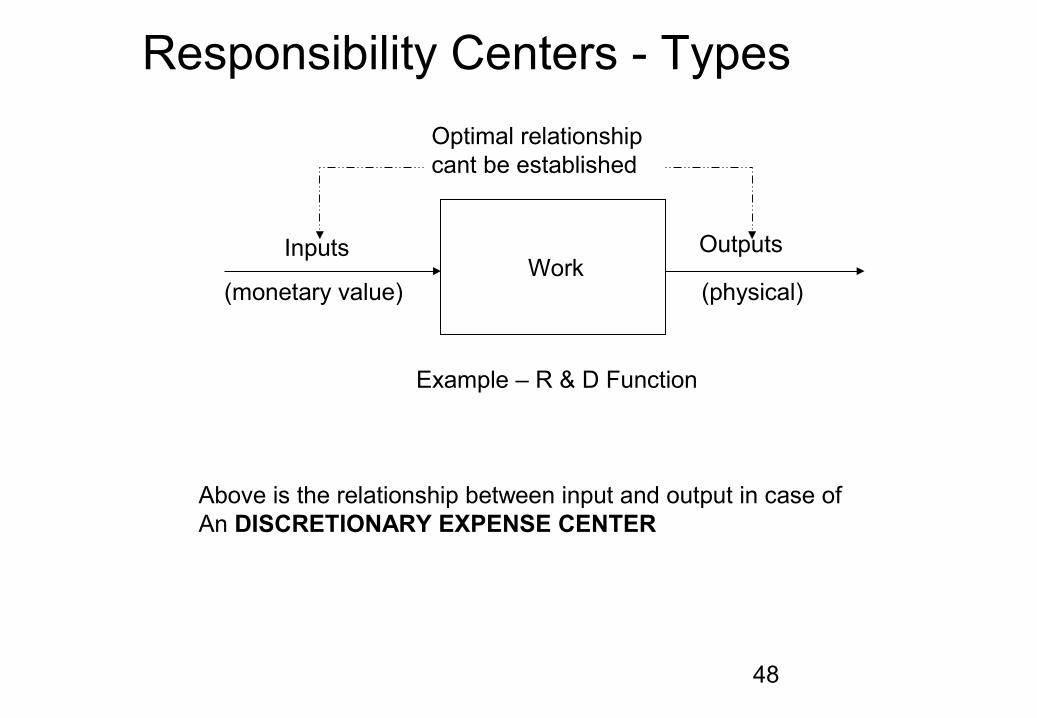

Responsibility Centers - Types

InputsWork

Outputs

(monetary value) (physical)

Optimal relationshipcant be established

Example – R & D Function

Above is the relationship between input and output in case ofAn DISCRETIONARY EXPENSE CENTER

49

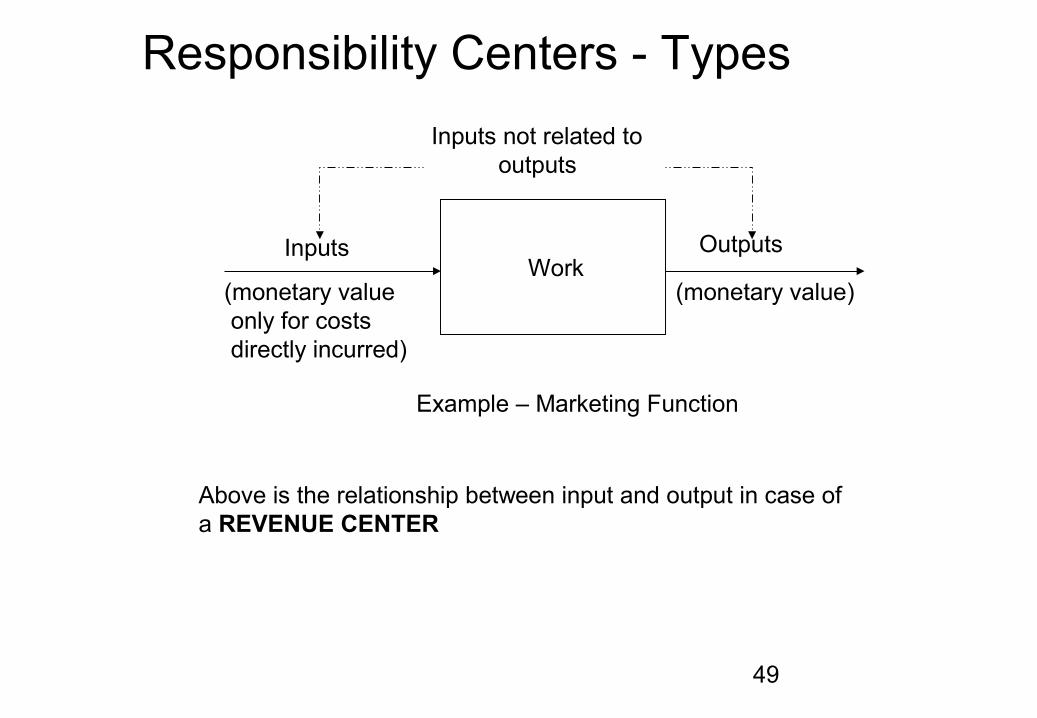

Responsibility Centers - Types

InputsWork

Outputs

(monetary value only for costs directly incurred)

(monetary value)

Inputs not related to outputs

Example – Marketing Function

Above is the relationship between input and output in case ofa REVENUE CENTER

50

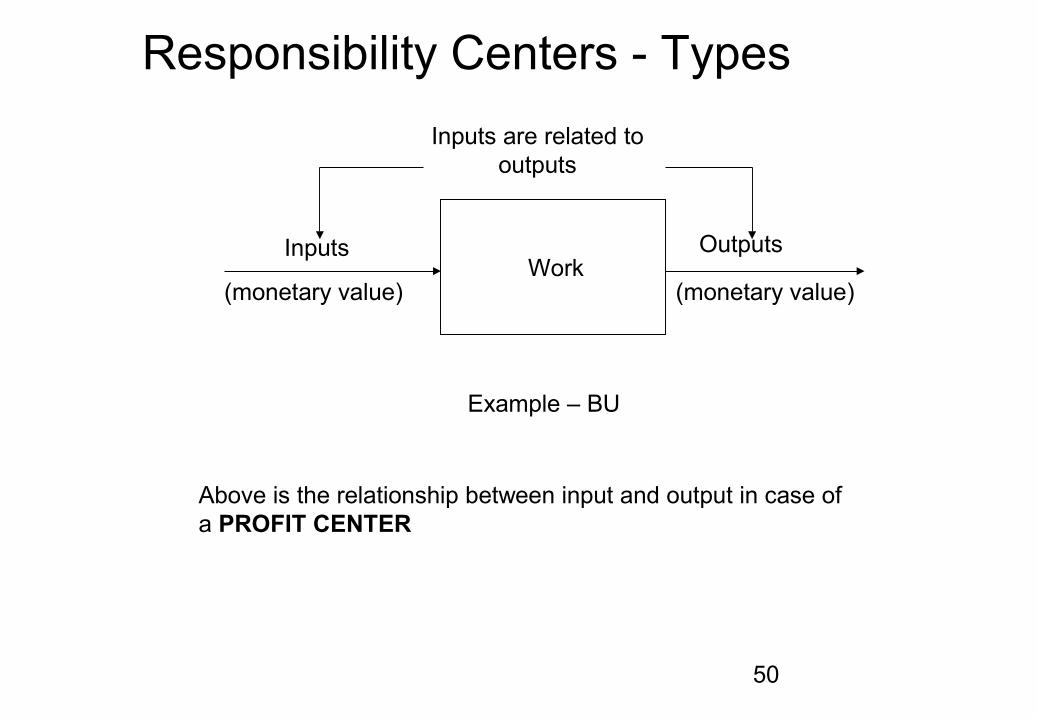

Responsibility Centers - Types

InputsWork

Outputs

(monetary value) (monetary value)

Inputs are related to outputs

Example – BU

Above is the relationship between input and output in case ofa PROFIT CENTER

51

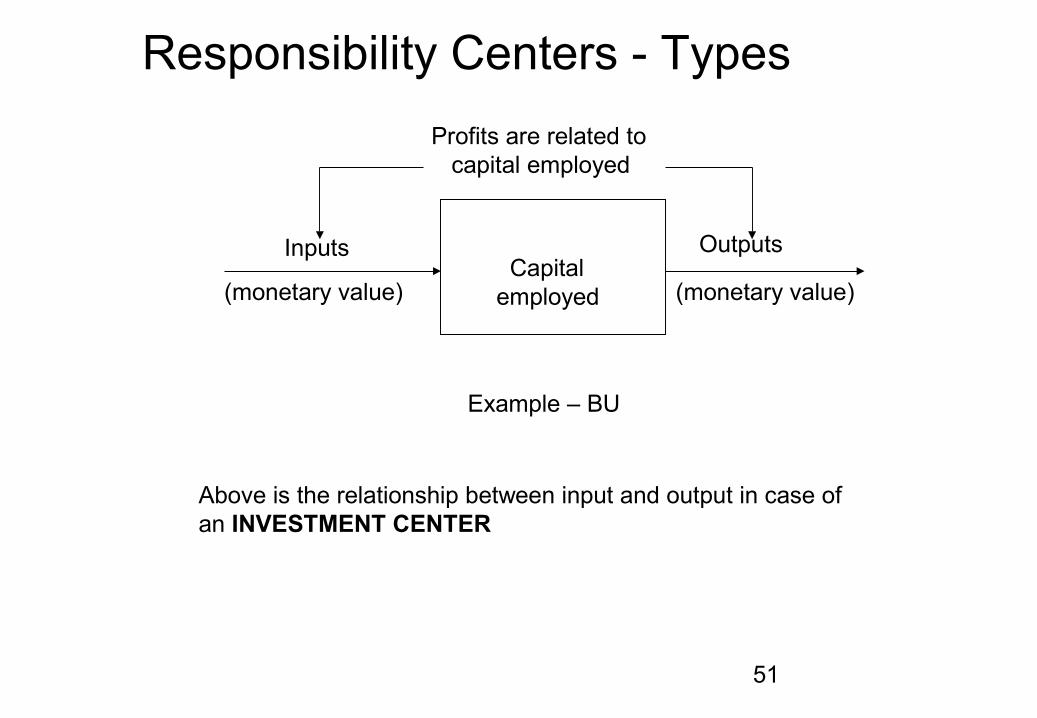

Responsibility Centers - Types

Inputs Capital employed

Outputs

(monetary value) (monetary value)

Profits are related to capital employed

Example – BU

Above is the relationship between input and output in case ofan INVESTMENT CENTER

52

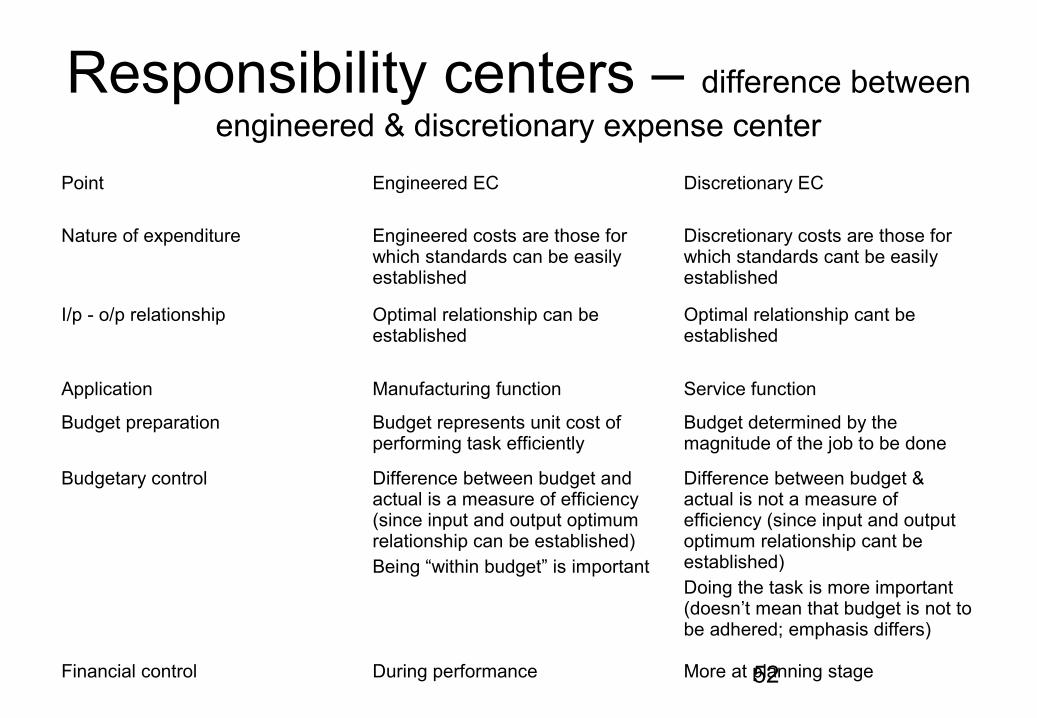

Responsibility centers – difference between engineered & discretionary expense center

Point Engineered EC Discretionary EC

Nature of expenditure Engineered costs are those for which standards can be easily established

Discretionary costs are those for which standards cant be easily established

I/p - o/p relationship Optimal relationship can be established

Optimal relationship cant be established

Application Manufacturing function Service function

Budget preparation Budget represents unit cost of performing task efficiently

Budget determined by the magnitude of the job to be done

Budgetary control Difference between budget and actual is a measure of efficiency (since input and output optimum relationship can be established)Being “within budget” is important

Difference between budget & actual is not a measure of efficiency (since input and output optimum relationship cant be established)Doing the task is more important (doesn’t mean that budget is not to be adhered; emphasis differs)

Financial control During performance More at planning stage

53

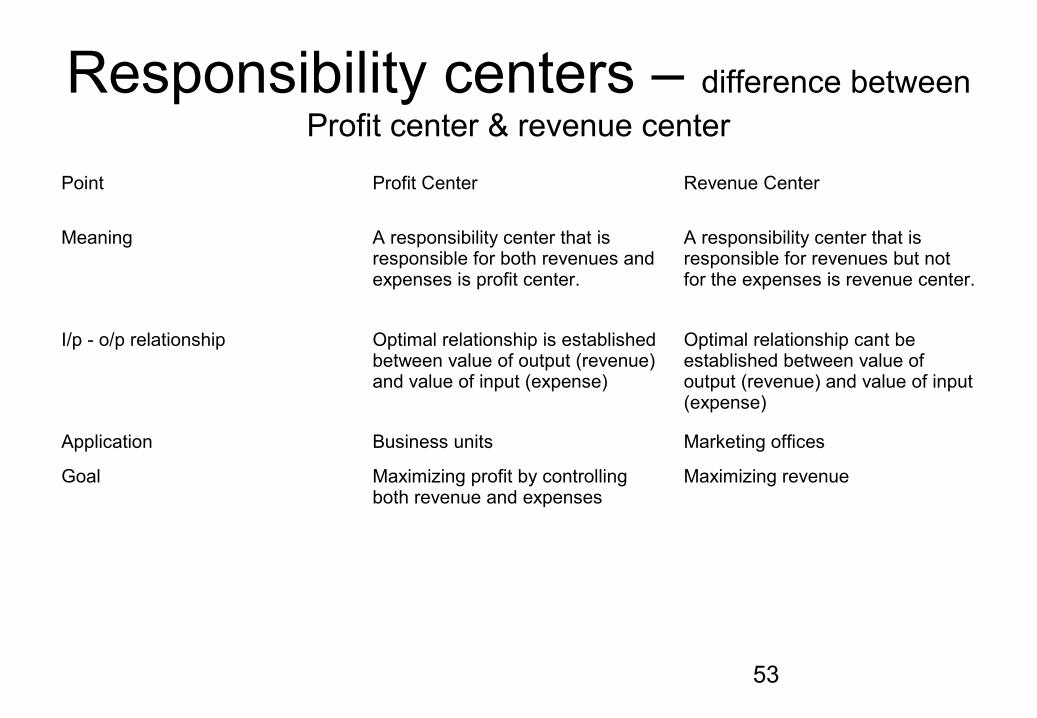

Responsibility centers – difference between Profit center & revenue center

Point Profit Center Revenue Center

Meaning A responsibility center that is responsible for both revenues and expenses is profit center.

A responsibility center that is responsible for revenues but not for the expenses is revenue center.

I/p - o/p relationship Optimal relationship is established between value of output (revenue) and value of input (expense)

Optimal relationship cant be established between value of output (revenue) and value of input (expense)

Application Business units Marketing offices

Goal Maximizing profit by controlling both revenue and expenses

Maximizing revenue

54

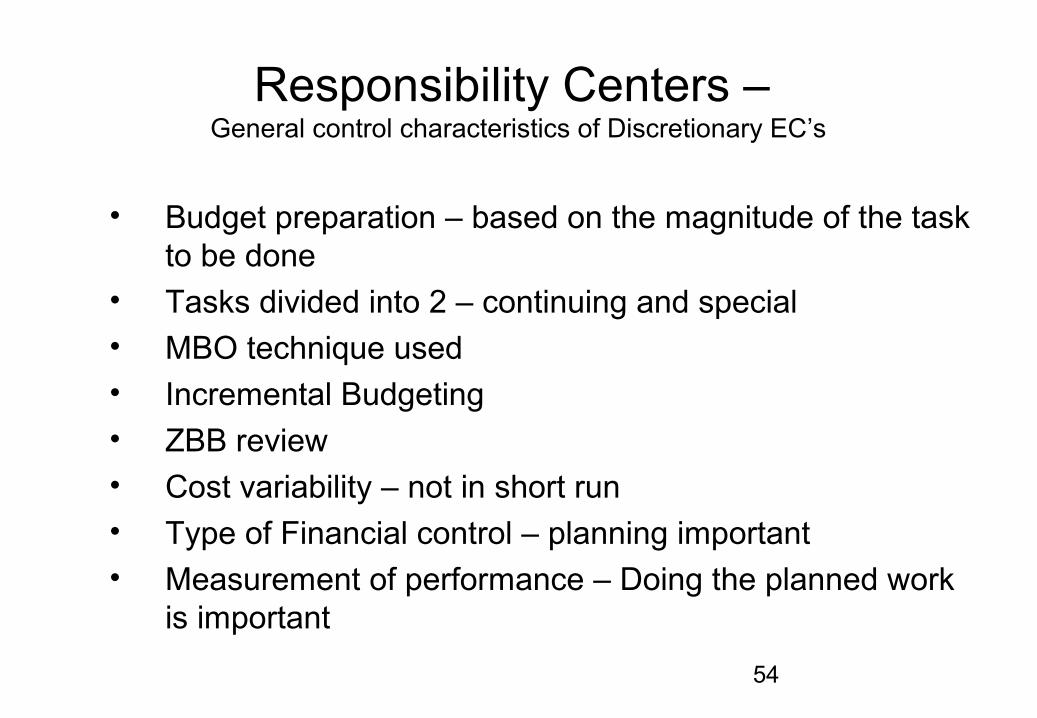

Responsibility Centers – General control characteristics of Discretionary EC’s

• Budget preparation – based on the magnitude of the task to be done

• Tasks divided into 2 – continuing and special• MBO technique used

• Incremental Budgeting

• ZBB review

• Cost variability – not in short run• Type of Financial control – planning important• Measurement of performance – Doing the planned work

is important

55

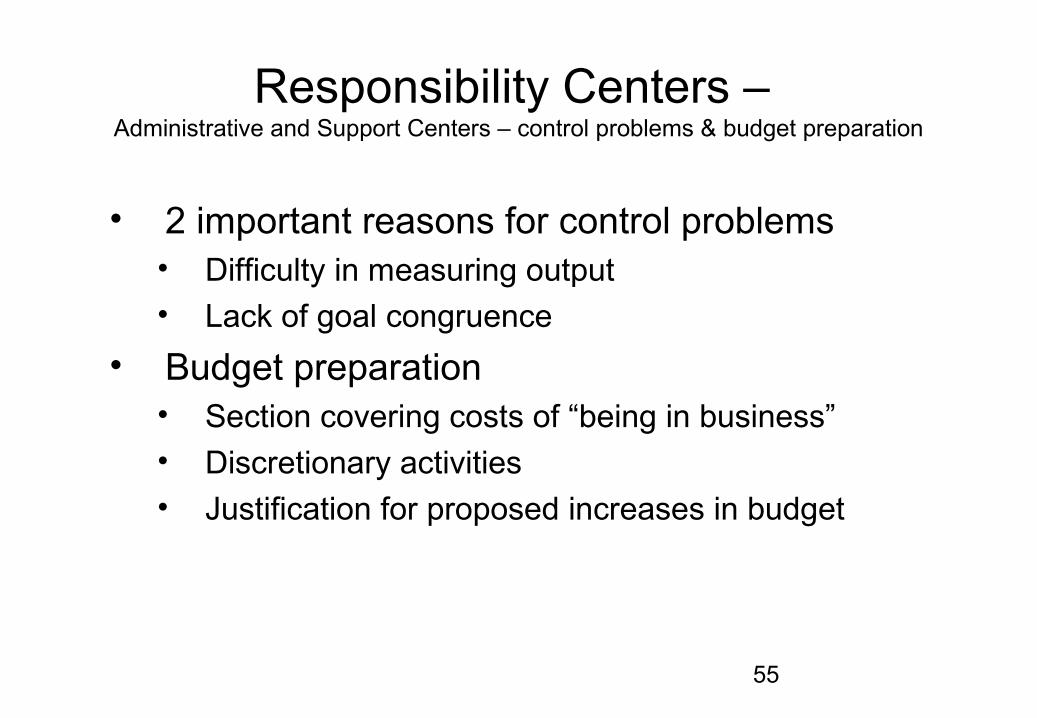

Responsibility Centers – Administrative and Support Centers – control problems & budget preparation

• 2 important reasons for control problems• Difficulty in measuring output• Lack of goal congruence

• Budget preparation• Section covering costs of “being in business”• Discretionary activities• Justification for proposed increases in budget

56

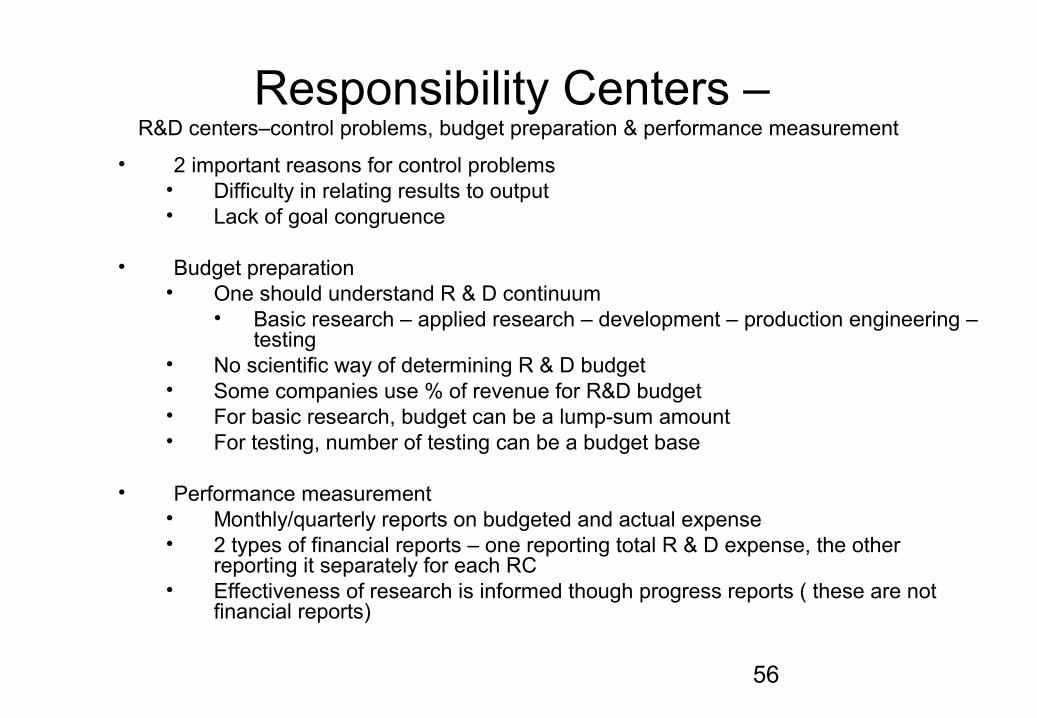

Responsibility Centers – R&D centers–control problems, budget preparation & performance measurement

• 2 important reasons for control problems• Difficulty in relating results to output• Lack of goal congruence

• Budget preparation• One should understand R & D continuum

• Basic research – applied research – development – production engineering – testing

• No scientific way of determining R & D budget• Some companies use % of revenue for R&D budget• For basic research, budget can be a lump-sum amount• For testing, number of testing can be a budget base

• Performance measurement• Monthly/quarterly reports on budgeted and actual expense• 2 types of financial reports – one reporting total R & D expense, the other

reporting it separately for each RC• Effectiveness of research is informed though progress reports ( these are not

financial reports)

57

Responsibility Centers – Marketing Centers – activities and related controls

• Logistic Activities• These RCs are similar to expense centers in

manufacturing plants and can be safely called as engineered expense centers

• Marketing activities – control problems• Measuring output is easy, evaluating effectiveness is difficult

because of influence of “other” factors on sales• Marketing expenses are often budgeted at % of sales not

because sales volume cause marketing expenses but because it gives larger affordability

• “Order-getting costs” are that way discretionary and controls cannot be easily standardized

58

Responsibility Centers – Profit Centers

• 2 conditions for delegating profit responsibility• Access to relevant information needed for decision

making• Measurement of effectiveness of the trade-offs made

by managers should be possible

59

Responsibility Centers – Profit Centers

• Advantages of profit centers• Improved quality of decisions• Quick decisions• HQ relieved from day-to-day decision making• Effective use of imagination and initiative• Training ground for managers• Enhanced profit consciousness• Information on profitability of individual units• They respond well to improvement initiatives since

their output is so readily measurable

60

Responsibility Centers – Profit Centers

• Difficulties with profit centers• Loss of control• Reduced quality of decisions

• Increased friction amongst units and HQ

• In-house competition may get substituted for cooperation

• Additional costs• Non-availability of competent GMs• Too much emphasis on short-run profitability

61

Responsibility Centers – Profit Centers

• Measurement of performance – Management performance and economic performance

• Measures of economic performance – measures of profitability• Contribution margin• Direct profit• Controllable profit• PBT• PAT

62

Responsibility Centers – Investment centers

• Difficulties in measuring assets employed• Cash- actual cash held at HQ much less than that would have been required as

an independent company• Receivables – whether to include at SP or COGS?• Inventories – how to deal with creditors?• Working Capital in general – treatment of current liabilities – 2 extreme treatments• Fixed Assets – which value to consider? Problems with depreciation• Leased assets – preference for leased assets over owned assets so as to reduce

capital charge• Idle assets – exclusion from computation of assets employed• Intangible assets – Capitalization of items like R & D and its repercussion on EVA

– if capitalized, very less incentive to cut such expenditure as it would only reduce a part of if by way of capital charge

63

Responsibility centers – Performance measures of an Investment center – ROI v/s EVA

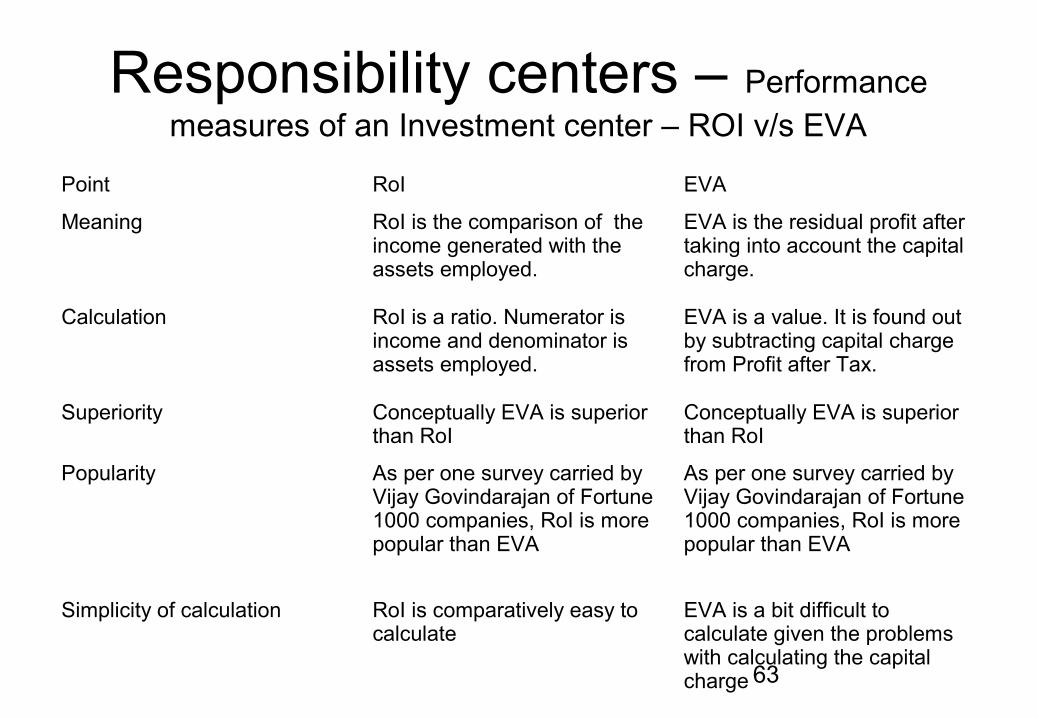

Point RoI EVA

Meaning RoI is the comparison of the income generated with the assets employed.

EVA is the residual profit after taking into account the capital charge.

Calculation RoI is a ratio. Numerator is income and denominator is assets employed.

EVA is a value. It is found out by subtracting capital charge from Profit after Tax.

Superiority Conceptually EVA is superior than RoI

Conceptually EVA is superior than RoI

Popularity As per one survey carried by Vijay Govindarajan of Fortune 1000 companies, RoI is more popular than EVA

As per one survey carried by Vijay Govindarajan of Fortune 1000 companies, RoI is more popular than EVA

Simplicity of calculation RoI is comparatively easy to calculate

EVA is a bit difficult to calculate given the problems with calculating the capital charge

64

Responsibility centers – Performance measures of an Investment center – RoI

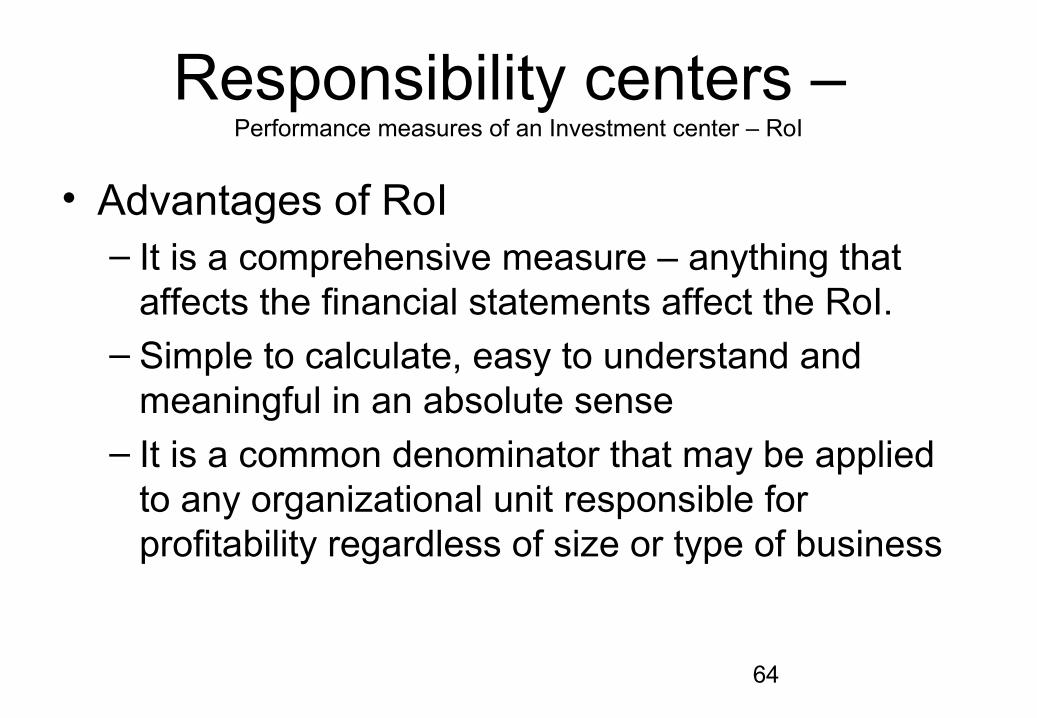

• Advantages of RoI– It is a comprehensive measure – anything that

affects the financial statements affect the RoI.– Simple to calculate, easy to understand and

meaningful in an absolute sense– It is a common denominator that may be applied

to any organizational unit responsible for profitability regardless of size or type of business

65

Responsibility centers – Performance measures of an Investment center – Superiority of EVA over RoI

• 4 points– EVA offer same profit objective for comparable investments, unlike RoI which may make

a manager reluctant to accept lower RoI (20%) opportunities than the current RoI (30%) levels despite being more than CoC (10%). RoI creates a bias towards little or no expansion in high-profit business units while at the same time low-profit units are making

investments at rates of returns well below those rejected by high-profit units.– Units can increase RoI by actually decreasing its overall profits. This thing will not

happen if EVA is measured.– Different interest rates can be used for different types of assets. For more riskier assets,

higher rates of costs of capital can be used. With RoI this is not possible.– EVA as compared to RoI has a stronger positive correlation with changes in a

company’s market value. To induce managers at the BU level to enhance shareholders value, managers can be told to create and grow EVA.

66

Strategic Planning Process

1. Reviewing and updating the strategic plan from last year

2. Deciding on assumptions and guidelines

3. First iteration of the new strategic plan

4. Analysis

5. Second iteration of the new strategic plan

6. Final review and approval

67

Budgetary control – Budget preparation process

• Organization• Budget Department• Budget Committee

• Issuance of guidelines• Initial budget proposal• Negotiation

• Review and approval

• Budget revisions• Procedures that provide for systematic updation

• Procedures that allow revisions under special circumstances

68

Budgetary control – Types of budgets & importance

– Types• Fixed and flexible budgets• Functional budgets• Incremental & Zero Base budgets• Annual, quarterly, monthly and weekly budgets

• Importance– It translates the strategic plan into an annual operating plan with

reasonable details– It provides a basis for translating the strategic decisions into actions

during the forthcoming year– It provides a good basis for controlling the actuals. Variances can be

analyzed and corrective actions can be taken.– It relieves the top management from day-to-day intervention and

botheration as it can look only into activities that are outside the budget

69

Budgetary control – Zero based budgeting

• In contrast to incremental budgeting, ZBB starts the budget from the scratch (de novo)

• Managers are required to justify the items with proper bases

• Thus ZBB is an intensive review of the budgetary allocations

• Certain basic questions are asked like – should the activity under review be performed at all? What should the quality level be?

• It is a good way of doing budgeting and can eliminate a lot of waste. However it demands some time and energy.

70

Transfer Pricing - basics

• If 2 or more profit centers are jointly responsible for developing, manufacturing and marketing of a product they should share the revenue when the product is finally sold. The transfer price is the mechanism for distributing this revenue.

• Objective of TP – • To provide each BU with information to determine optimum

tradeoffs between company costs and revenues• To induce goal congruent decisions• To measure economic performance of BU’s• It should be simple to understand and easy to administer

71

Transfer Pricing - methods

• Fundamental principle is that the TP should be similar to the price that would have been if the product was sold in outside market.

• Methods –

• Cost based• Marginal Costs plus markup• Standard cost plus mark up• Actual cost plus mark up• Full cost plus mark up

72

Transfer Pricing - methods

• Market price based– Equal to market price– Less than the market price– More than the market price

• Profit sharing : Profit of company distributed between the departments

• Negotiated price

73

Transfer Pricing - methods

• Two-step pricing

• Instead of building the fixed cost and profit element on a unit level as a part of the TP, the same is charged to the transferee unit on a periodical basis

• Thus the two-step pricing would mean – the first step to charge the variable cost as the TP and in the second step a lump-sum charging of the fixed cost and the profit.

• This method helps the transferee division to make appropriate short-term marketing decisions

74

Transfer Pricing - methods

• Dual Pricing (2 sets of prices)• Crediting transferor with outside sales price• But charging the transferee with total standard costs• Difference to be charged to a HQ account that will get

eliminated at the time of consolidation• This method is used when there are conflicts between the

transferor and transferee division and any other method is not working

75

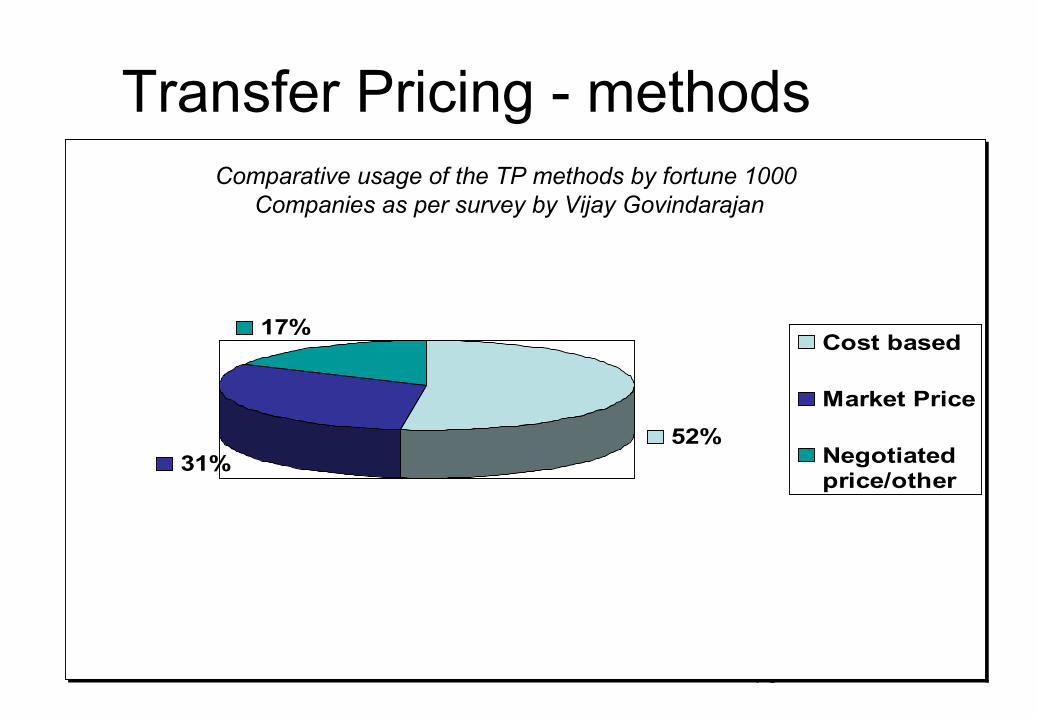

52%31%

17%Cost based

Market Price

Negotiatedprice/other

Transfer Pricing - methodsComparative usage of the TP methods by fortune 1000

Companies as per survey by Vijay Govindarajan

76

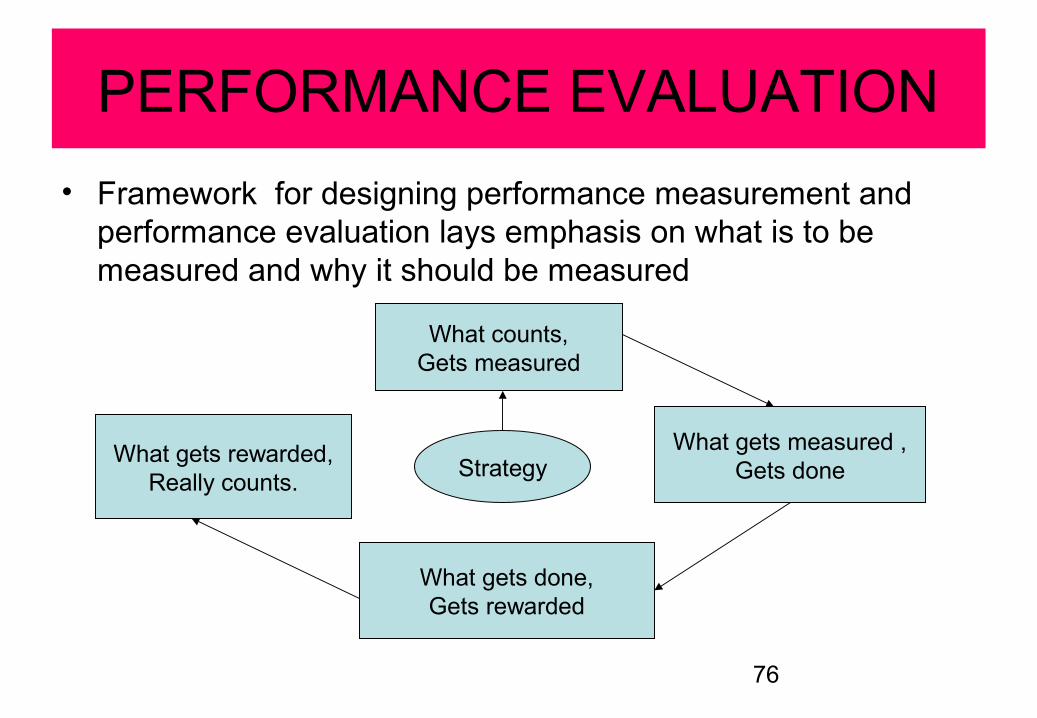

PERFORMANCE EVALUATION

• Framework for designing performance measurement and performance evaluation lays emphasis on what is to be measured and why it should be measured

What counts,Gets measured

What gets measured ,Gets done

What gets done,Gets rewarded

What gets rewarded,Really counts.

Strategy

77

Multiple criteria for performance evaluation

• Financial and Non financial variables

• Internal and External measures

• Long term and short term indicators

• Separate controllable and uncontrollable variables

78

Performance indicators

• Performance indicators can be:-

1.Results achieved : e.g. sales, profit

2.Efforts taken :- e.g. numbers of tests undertaken, number of new customers contacted

3.Costs incurred : e.g. cost of production

4.Resources employed : e.g. human resource, capital resources.

79

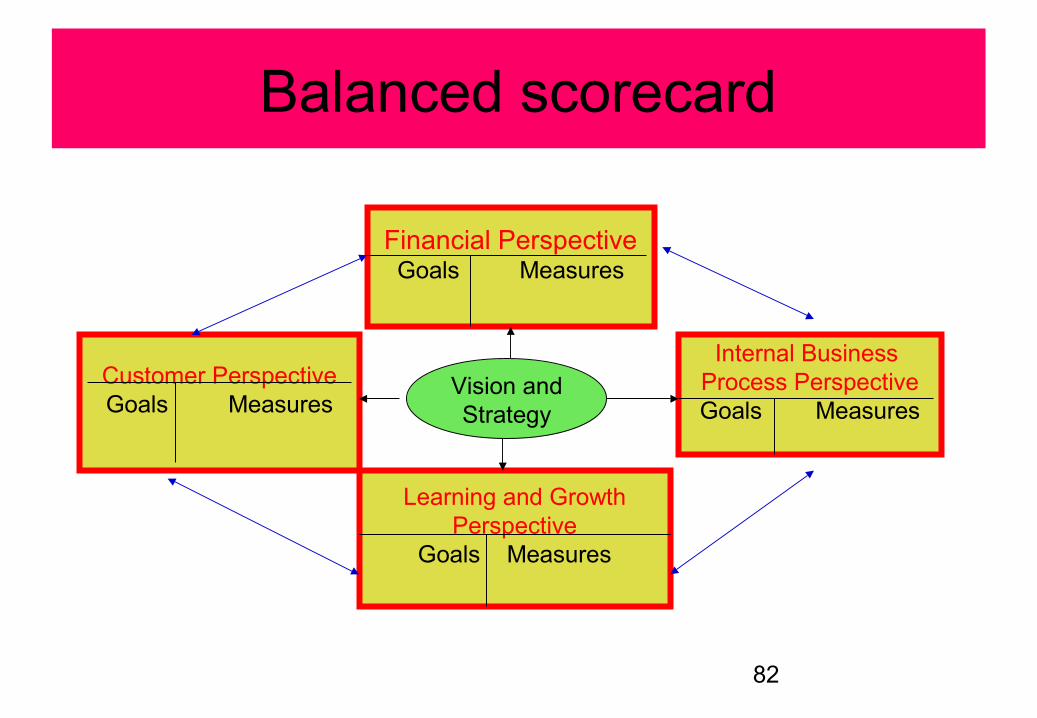

Performance Measurement – Balanced Score Card

• Developed by Kaplan and Norton

• Provides a mechanism for linking strategy to action

• Translates strategy into measurable parameters

80

Performance Measurement – Balanced Score Card

• Four perspectives to measure performance• Customer : How do customers see us?• Internal Business : What most we excel at ?• Innovation and learning: Can we continue to create

value?

• Financial: How do we look to shareholders?

• For each of this perspective appropriate performance measures should be developed

81

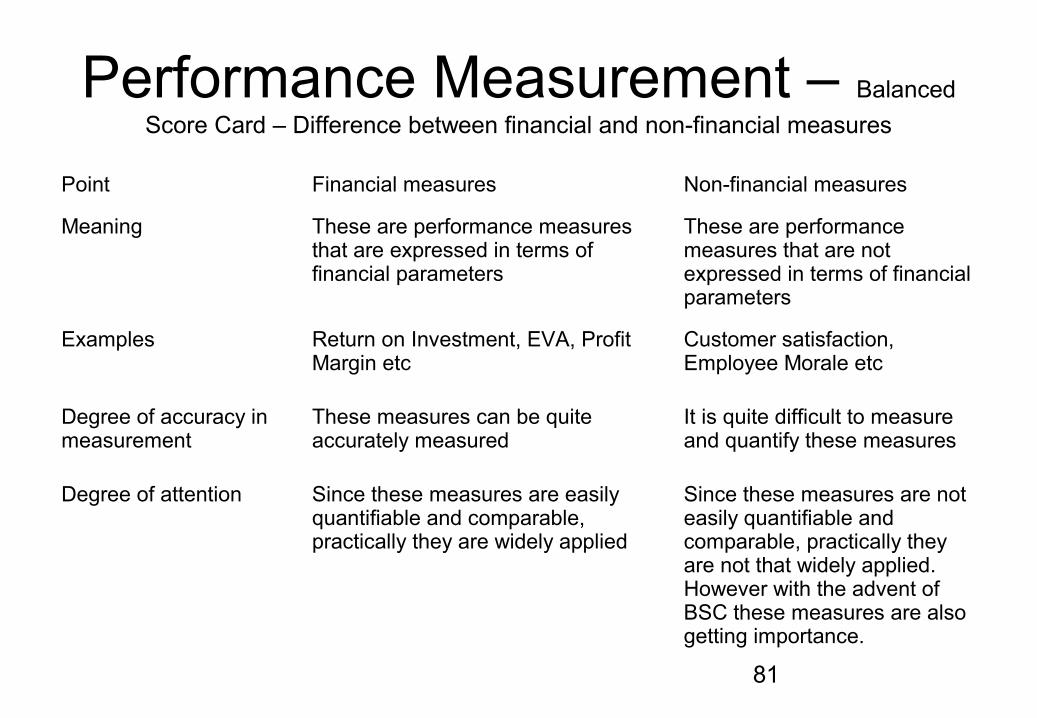

Performance Measurement – Balanced

Score Card – Difference between financial and non-financial measures

Point Financial measures Non-financial measures

Meaning These are performance measures that are expressed in terms of financial parameters

These are performance measures that are not expressed in terms of financial parameters

Examples Return on Investment, EVA, Profit Margin etc

Customer satisfaction, Employee Morale etc

Degree of accuracy in measurement

These measures can be quite accurately measured

It is quite difficult to measure and quantify these measures

Degree of attention Since these measures are easily quantifiable and comparable, practically they are widely applied

Since these measures are not easily quantifiable and comparable, practically they are not that widely applied. However with the advent of BSC these measures are also getting importance.

82

Balanced scorecard

Financial PerspectiveGoals Measures

Learning and GrowthPerspective

Goals Measures

Internal Business Process PerspectiveGoals Measures

Customer PerspectiveGoals Measures

Vision andStrategy

83

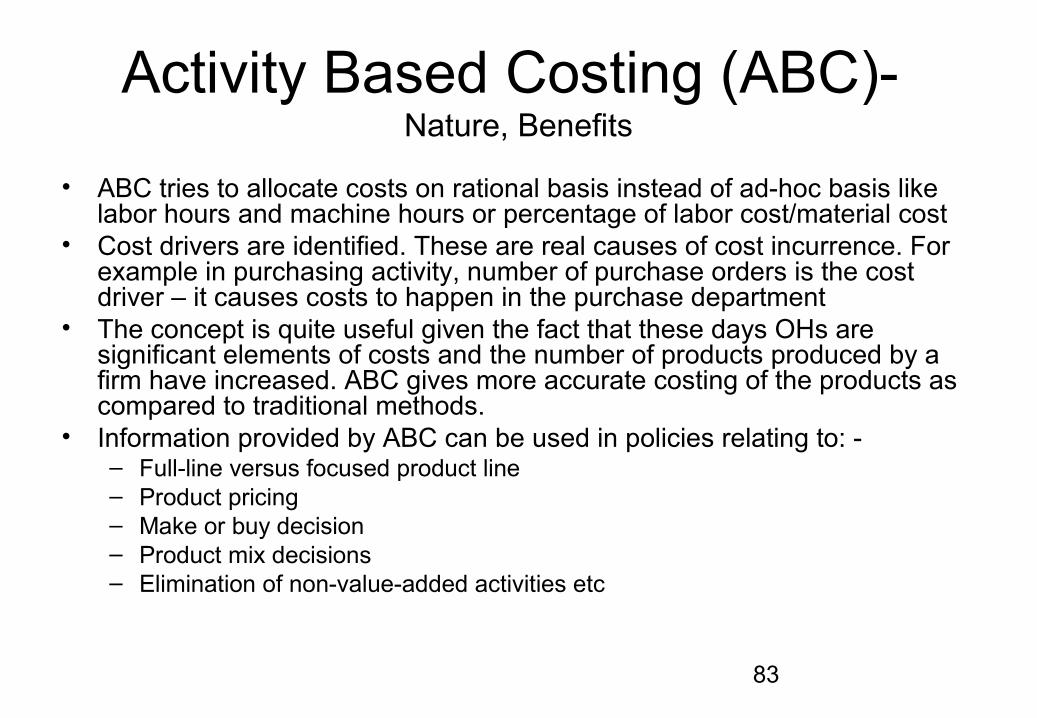

Activity Based Costing (ABC)- Nature, Benefits

• ABC tries to allocate costs on rational basis instead of ad-hoc basis like labor hours and machine hours or percentage of labor cost/material cost

• Cost drivers are identified. These are real causes of cost incurrence. For example in purchasing activity, number of purchase orders is the cost driver – it causes costs to happen in the purchase department

• The concept is quite useful given the fact that these days OHs are significant elements of costs and the number of products produced by a firm have increased. ABC gives more accurate costing of the products as compared to traditional methods.

• Information provided by ABC can be used in policies relating to: - – Full-line versus focused product line– Product pricing– Make or buy decision– Product mix decisions– Elimination of non-value-added activities etc

84

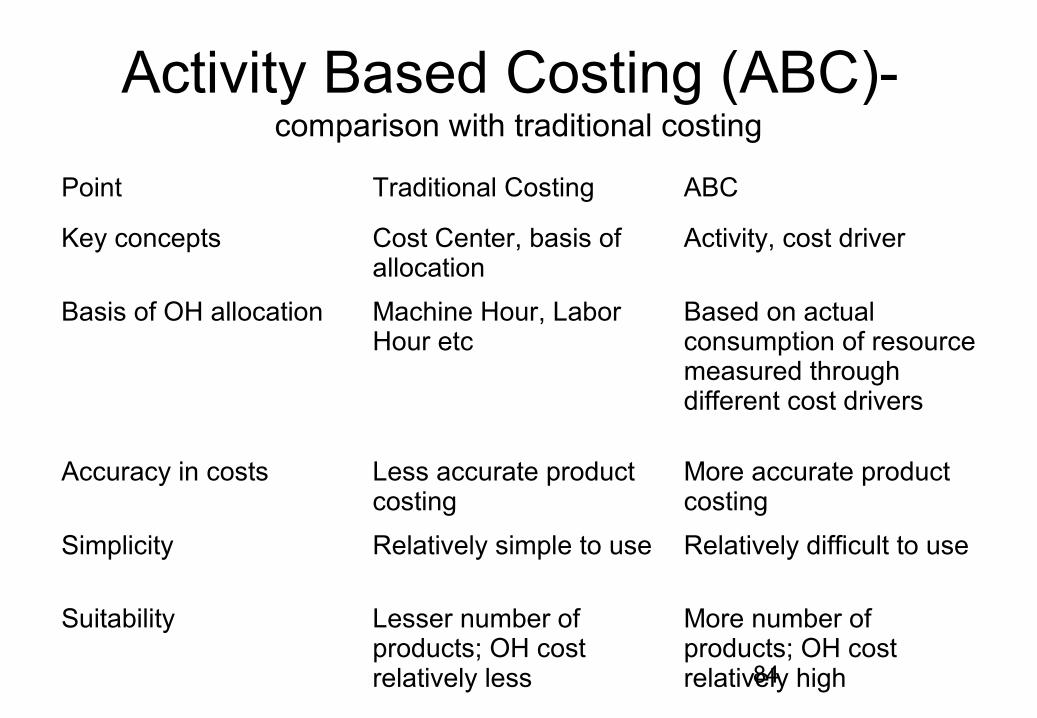

Activity Based Costing (ABC)- comparison with traditional costing

Point Traditional Costing ABC

Key concepts Cost Center, basis of allocation

Activity, cost driver

Basis of OH allocation Machine Hour, Labor Hour etc

Based on actual consumption of resource measured through different cost drivers

Accuracy in costs Less accurate product costing

More accurate product costing

Simplicity Relatively simple to use Relatively difficult to use

Suitability Lesser number of products; OH cost relatively less

More number of products; OH cost relatively high

85

MCS in service sector

• Characteristics of service organizations in general• Absence of inventory buffer• Difficulty in controlling quality• Labor intensive

• Multi-unit organizations

– The above characteristics peculiar to service sector are the causes of differences in the nature of MCS that is used in the Manufacturing Sector

86

MCS in service sector – Professional service organizations

• Special Characteristics• Goals• Professionals• Output and input measurement• Small size• Marketing

• MCS• Pricing• Profit Centers and TP• Strategic planning and budgeting• Control of operations• Performance measurement and appraisal

87

MCS in service sector – Financial service organizations

• Special Characteristics• Monetary assets• Time period for transactions• Risk and reward

• Technology

• MCS• General principles of MCS apply but they need to be

adapted to the above mentioned special characteristics

88

MCS in service sector – Health Care Organizations

• Special Characteristics• Difficult social problem• Change in mix of providers• Third-party payers• Professionals• Importance of quality control

• MCS• General principles of MCS apply• Because of high cost of equipments, strategic planning process is

important• Annual budget preparation is conventional• Huge quantity of information are available quickly for controlling of

operating activities• Financial performance is analyzed by comparison of revenues and

expenses with budgets

89

MCS in service sector – Nonprofit Organizations

• Special Characteristics• Absence of the profit measure• Contributed Capital• Fund Accounting

• Governance

• MCS• Product pricing• Strategic planning and budget preparation• Operation and evaluation

90

Auditing as a control tool • Auditing is a control tool that ensures through checking,

verification of documents and evidence that the plans/policies of the management are implemented as desired

• Many big organizations have a special internal audit department that carries internal audit to see to it that the internal controls and checks as set by the management are being adhered to

• There are different types of audits like financial audit, internal audit, cost audit, management audit etc. Purpose of these audits are different.

• An audit system makes the staff more vigilant. Audits like concurrent audit in banks actually act a continuous control system. Findings from an audit can help strengthen future controls.

91

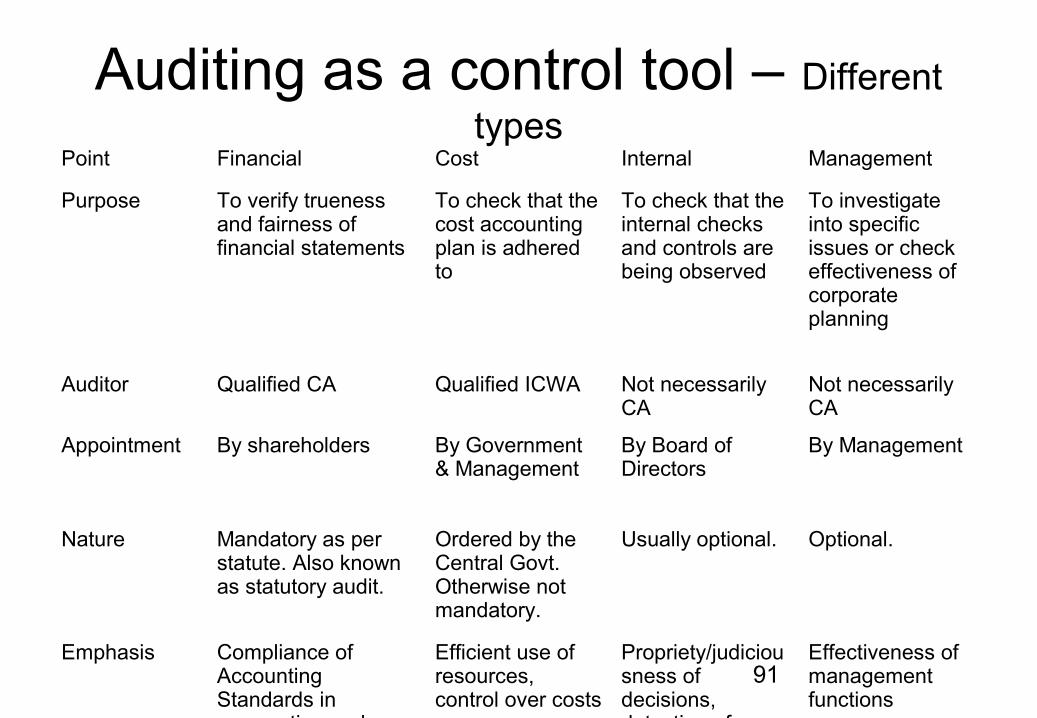

Auditing as a control tool – Different types

Point Financial Cost Internal Management

Purpose To verify trueness and fairness of financial statements

To check that the cost accounting plan is adhered to

To check that the internal checks and controls are being observed

To investigate into specific issues or check effectiveness of corporate planning

Auditor Qualified CA Qualified ICWA Not necessarily CA

Not necessarily CA

Appointment By shareholders By Government & Management

By Board of Directors

By Management

Nature Mandatory as per statute. Also known as statutory audit.

Ordered by the Central Govt. Otherwise not mandatory.

Usually optional. Optional.

Emphasis Compliance of Accounting Standards in preparation and disclosure

Efficient use of resources, control over costs

Propriety/judiciousness of decisions, detection of frauds

Effectiveness of management functions

92

Management Audit• Management Audit as the name suggests is the audit of the

management itself, that is, the management auditor judges the effectiveness of the functions performed by the management.

• The Management Auditor will check the planning, decision making, controlling and other such functions performed by the management.

• Management Auditor generally is a senior person with good all-round knowledge and experience.

• He uses tools like questionnaire to gather audit evidence. • If used properly Management Audit can be a good control tool to

provide feedback to the management about its own effectiveness.