Embed Size (px)

Citation preview

MBA MondaysFred Wilson

This is a Leanpub book which is for sale at http://leanpub.com. Leanpubhelps you connect with readers and sell your ebook, while you’re writing itand after it’s done.

T A B L E O F C O N T E N T S

1Preface

3ROI and Net Present Value

3How to Calculate a Return on Investment

5The Present Value of Future Cash Flows

7The Time Value of Money

11Compounding Interest

15Corporate Entities

15Corporate Entities

19Piercing the Corporate Veil

21Accounting

21Accounting

24The Profit and Loss Statement

28The Balance Sheet

34Cash Flow

38Analyzing Financial Statements

43Business, Metrics and Pricing

43Key Business Metrics

45Price: Why Lower Isn't Always Better

47Projections, Budgeting and Forecasting

47Projections, Budgeting and Forecasting

49Scenarios

52Budgeting in a Small Early Stage Company

55Budgeting in a Growing Company

58Budgeting in a Large Company

60Forecasting

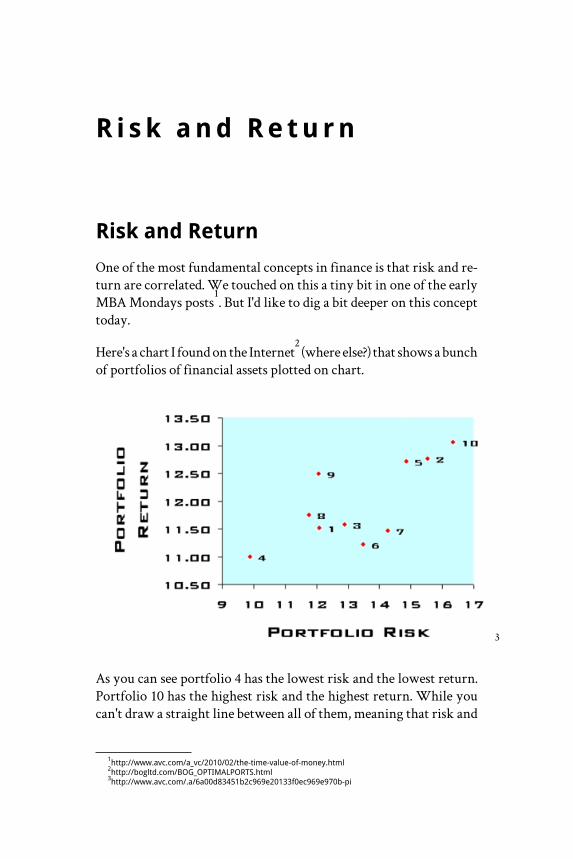

63Risk and Return

63Risk and Return

65Diversification

68Hedging

70Currency Risk in a Business

73Purchasing Power Parity

77Business Costs

77Opportunity Costs

78Sunk Costs

80Off Balance Sheet Liabilities

83Valuation

83Enterprise Value and Market Value

85Bookings Vs. Revenues Vs. Collections

87Commission Plans

87Commission Plans

91What a CEO Does

91What a CEO Does

92What a CEO Does, Continued

95Outsourcing

95Outsourcing

97Outsourcing Vs. Offshoring

101Employee Equity

101Employee Equity

103Employee Equity: Dilution

106Employee Equity: Appreciation

107Employee Equity: Options

111Employee Equity: The Liquidation Overhang

114Employee Equity: The Option Strike Price

117Employee Equity: Restricted Stock and RSUs

119Employee Equity: Vesting

122Employee Equity: How Much?

127Mergers and Acquisitions

127Acquisition Finance

128M&A Fundamentals

130Buying and Selling Assets

Pre face

MBA Mondays is written by Fred Wilson1, and licensed under the

Creative Commons Attribution 3.0 license. For details, see this post2.

1http://www.avc.com/a_vc/about.html2http://www.avc.com/a_vc/2011/02/mba-mondays-everywhere.html

ROI and Net P resentVa lue

How to Calculate a Return onInvestment

The Gotham Gal1 and I make a fair number of non-tech angel invest-

ments. Things like media, food products, restaurants, music, local realestate, local businesses. In these investments we are usually backingan entrepreneur we've gotten to know who delivers products to themarket that we use and love. The Gotham Gal runs this part of ourinvestment portfolio with some involvement by me.

As I look over the business plans and projections that these entrepren-eurs share with us, one thing I constantly see is a lack of sophisticationin calculating the investor's return.

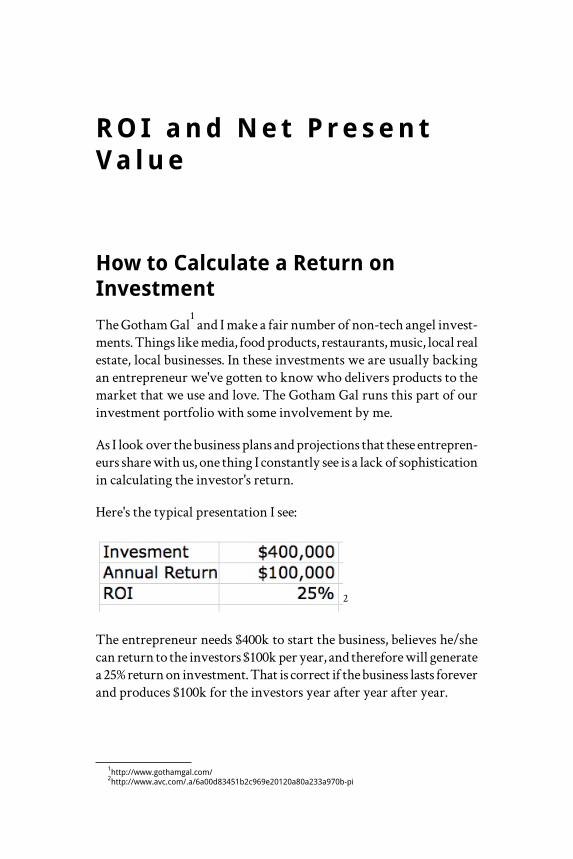

Here's the typical presentation I see:

2

The entrepreneur needs $400k to start the business, believes he/shecan return to the investors $100k per year, and therefore will generatea 25% return on investment. That is correct if the business lasts foreverand produces $100k for the investors year after year after year.

1http://www.gothamgal.com/2http://www.avc.com/.a/6a00d83451b2c969e20120a80a233a970b-pi

But many businesses, probably most businesses, have a finite life. Arestaurant may have a few good years but then lose its clientele andgo out of business. A media product might do well for a decade butthen lose its way and fold.

And most businesses are unlikely to produce exactly $100k every yearto the investors. Some businesses will grow the profits year after year.Others might see the profits decline as the business matures and headsout of business.

So the proper way to calculate a return is using the "cash flow method".Here's how you do it.

1) Get a spreadsheet, excel will do, although increasingly I recommendgoogle docs spreadsheet

3 because it's simpler to share with others.

2) Lay out along a single row a number of years. I would suggest tenyears to start.

3) In the first year show the total investment required as a negativenumber (because the investors are sending their money to you).

4) In the first through tenth years, show the returns to the investors(after your share). This should be a positive number.

5) Then add those two rows together to get a "net cash flow" number.

6) Sum up the totals of all ten years to get total money in, total moneyback, and net profit.

7) Then calculate two numbers. The "multiple" is the total moneyback divided by the total money in. And then using the "IRR" function,calculate an annual return number.

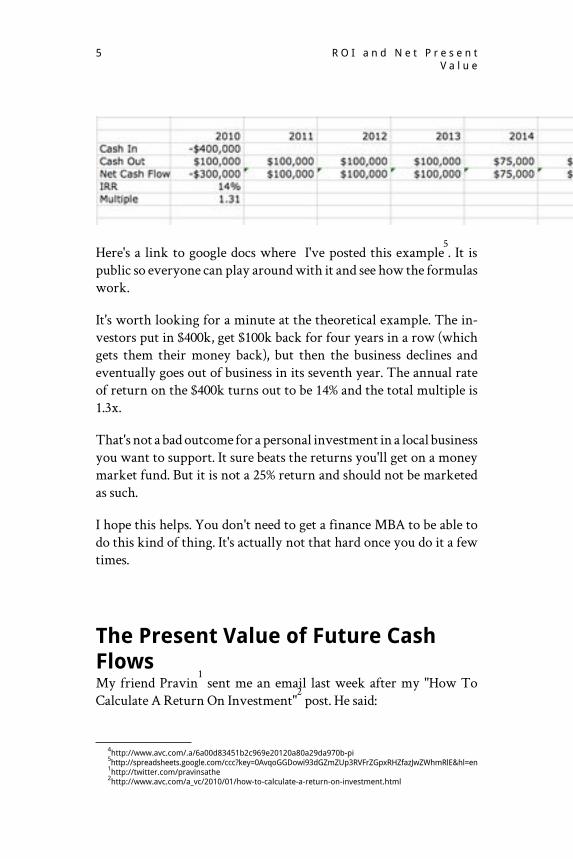

Here's what it should look like:

3http://docs.google.com

4R O I a n d N e t P r e s e n tV a l u e

4

Here's a link to google docs where I've posted this example5. It is

public so everyone can play around with it and see how the formulaswork.

It's worth looking for a minute at the theoretical example. The in-vestors put in $400k, get $100k back for four years in a row (whichgets them their money back), but then the business declines andeventually goes out of business in its seventh year. The annual rateof return on the $400k turns out to be 14% and the total multiple is1.3x.

That's not a bad outcome for a personal investment in a local businessyou want to support. It sure beats the returns you'll get on a moneymarket fund. But it is not a 25% return and should not be marketedas such.

I hope this helps. You don't need to get a finance MBA to be able todo this kind of thing. It's actually not that hard once you do it a fewtimes.

The Present Value of Future CashFlowsMy friend Pravin

1 sent me an email last week after my "How To

Calculate A Return On Investment"2 post. He said:

4http://www.avc.com/.a/6a00d83451b2c969e20120a80a29da970b-pi5http://spreadsheets.google.com/ccc?key=0AvqoGGDowi93dGZmZUp3RVFrZGpxRHZfazJwZWhmRlE&hl=en1http://twitter.com/pravinsathe2http://www.avc.com/a_vc/2010/01/how-to-calculate-a-return-on-investment.html

R O I a n d N e t P r e s e n tV a l u e

5

I wish there was a class that I could take that would teachme how to properly research stocks/companies for invest-ment purposes and how that could be made into a privatetutoring business. It'd be for people like me, people whodidn't go to school for business but still are interested inunderstanding all the jargon, methods of investing, etcand how to apply it to a buy and hold strategy.

Pravin then went on to say that the post I wrote was exactly the kindof thing he was looking for and that he'd like to see me do more of it.So with that preface, I'd like to announce a new series here at AVC.I'm calling it "MBA Mondays". Every monday I'll write a post that isabout a topic I learned in business school. I'll keep it dead simple (manypeople thought my ROI post last week was too simple). And I'll tryto connect it to some real world experience.

I'll start with the topic Pravin wanted some help with: how to valuestocks, what they are worth today, and what they could be worth inthe future. This topic will take weeks of MBA Mondays to workthrough but we'll start with a fundamental concept, the present valueof future cash flows.

I was taught, and I believe with all my head and heart, that companiesare worth the "present value" of "future cash flows". What that meansis if you could know with certainty the exact amount of cash earningsthat the company will produce from now until eternity, you couldlay those cash flows out and then using some interest rate that reflectsthe time value of money, you could calculate what you'd pay todayfor those future cash flows.

Let's make it really simple. You want to buy the apartment next toyou for investment purposes. It rents for $1000/month. It costs$200/month to maintain. So it produces $800/month of "cash flow".Let's leave aside inflation, rent increases, cost increases, etc and assumefor this post that it will always produce $800/month of cash flow.

6R O I a n d N e t P r e s e n tV a l u e

And let's say that you will accept a 10% annual return on your invest-ment. There are a multitude of reasons why you'll accept differentinterest rates for different investments, but we'll just use 10% for thisone.

Once you know the cash flow ($800/month) and the interest rate (alsocalled the "discount rate"), you can calculate present value. And thisexample is as easy as it gets because the cash flow doesn't change andthe interest rate is 10%.

The annual cash flow is $9,600 (12 x $800) and if you want to earn 10%on your money every year, you can pay $96,000 for the apartment.In order to check the math, let's calculate 10% of $96,000. That's $9,600per year.

In practice, it is never this simple. Cash flows will vary year after year.You'll have to lay them out in a spreadsheet and do a present valueanalysis. We'll do that next week.

But it is the principle here that is important. Companies (and otherinvestments) are worth the "present value" of all the cash you'll earnfrom them in the future. You can't just add up all that cash because adollar tomorrow (or ten years from now) is worth less than a dollaryou have in your pocket. So you need to "discount" the future cashflows by an acceptable rate of interest.

That basic concept is the bedrock of all valuation concepts in finance.It can get incredibly complex, way beyond my ability to calculate oreven explain. But you have to understand this concept before you cango further. I hope you do. Next week we'll look at using spreadsheetsto calculate present values.

The Time Value of MoneyIt's Monday, time for MBA Mondays.

R O I a n d N e t P r e s e n tV a l u e

7

Last week, I posted about The Present Value Of Future CashFlows

1 and in the comments Pascal-Emmanuel Gobry

2 wrote

3:

That being said, before even covering NPV, I would have first talked aboutthe time value of money. To me, time value of money is one of the top 3concepts that blew my mind in business school and that should be commonknowledge. When you think about it, all of finance, but also much of business,is underpinned by that. Once you understand time value of money, you un-derstand opportunity costs, you understand sunk costs, you just view theworld in a whole different light.

PEG is right. We have to talk about the Time Value Of Money andit was a mistake to dive into concepts like Present Value and DiscountRates before doing that. So we'll hit the rewind button and go backto the start. Here it goes.

Money today is generally worth more than money tomorrow.As another commenter to last week's post put it "you can't buy beertonight with next year's earnings". Money in your pocket, cash inhand, is worth more than cash that you don't actually have in hand.If you think about it that simply, everyone can agree that they'd ratherhave the cash in hand than the promise of the same amount at somelater day.

And interest rates are used to calculate exactly how much more themoney is worth today than tomorrow. Let's say that you'd take $900today instead of $1000 exactly a year from now. That means you'daccept a 11.1% "discount rate" on that transaction. I calculated that asfollows:

1) I calculated how much of a "discount" you would take in order toget the money today versus next year. That is $1000 less $900, or $100

1http://www.avc.com/a_vc/2010/01/valuing-stocks-today-and-tomorrow.html2http://twitter.com/pegobry3http://www.avc.com/a_vc/2010/01/valuing-stocks-today-and-tomorrow.html#comment-32276641

8R O I a n d N e t P r e s e n tV a l u e

2) I then divided the discount by the amount you'd take today. Thatis $100/$900, which is 11.1%.

This transaction could be modeled out the other way. Let's say youare willing to loan a friend $900 and you agree that he'll pay you aninterest rate of 11.1%. You multiply $900 times 11.1%, you get $100 oftotal interest, and add that to the $900 and calculate that he'll pay youback $1000 a year from now.

As you can tell from the way I talked about them, interest rates anddiscount rates are generally the same thing. There are technical differ-ences, but both represent a rate of increase in the time value of money.

So if the interest rate describes the time value of money, then thehigher it is, the more valuable money is in your hands and the lessvaluable money is down the road.

There are multiple reasons that money can be more valuable todaythan tomorrow. Let's talk about two of them.

1) Inflation - This is a complicated topic that we are not going to getinto in detail here. But I need to at least mention it. When prices ofthings rise faster than they should, we call that inflation. It can becaused by a number of things, most often when the supply of moneyis rising faster than is sustainable. But the important thing to note isthat if a house that costs $100,000 today is going to cost $120,000 nextyear, that represents 20% inflation and you'd want to earn 20% onyour money every year to compensate you for that inflation. You'dwant a 20% interest rate on your cash to be compensated for that in-flation.

2) Risk - If your money is in a federally guaranteed bank deposit fora year, you might accept 2% interest on it. If it is invested in yourfriend's startup, you might want a double on your money in a year.Why the difference between a 2% interest rate and a 100% interestrate? Risk. You know you are getting the money in the bank back.You are pretty sure you aren't getting the money back that you inves-ted in your friend's startup and want to get a lot back if it works out.

R O I a n d N e t P r e s e n tV a l u e

9

So let's deconstruct interest rates a bit to parse these different reasonsout of them.

Let's say the current rate of interest on a one year treasury bill (a notesold by the US Gov't that is federally guaranteed) is paying a rate ofinterest of 3%. That is an important rate to pay attention to. Becauseit is a one year interest rate on a risk free instrument (assuming thatthe US Gov't is solvent and always will be). We will assume for nowthat is true. So the "risk free rate" is 3%. That is the rate that the"market" says we should be accepting for a one year instrument withno risk.

Now let's take inflation into account. If the Consumer Price Index(the CPI) says that costs are rising 2.5% year over year, then we cansay that the one year inflation rate is 2.5%. It can get a lot more com-plicated than this, but many real estate leases use the CPI so we canuse it too. If you subtract the inflation rate from the risk free rate, youget something called the "real interest rate". In our example, thatwould be 0.5% (3% minus 2.5%). And we call the 3% rate, the "nominalrate".

Now let's take risk into account. Let's say you can find a corporatebond in the bond market that is coming due next year and will pay$1000 and it is trading for $900 right now. We know from the examplethat we started with that it is "paying" a discount rate of 11.1% for thenext year. If we subtract the 3% risk free rate of interest from the11.1%, we can determine that market is demanding a "risk premium"of 8.1% over the risk free rate for this bond. That means that noteveryone thinks that this company is going to be able to pay back thebond in full, but most people do.

Ok, so hopefully you'll see that interest rates and discount rates havecomponents to them. In its simplest form, and interest rate is com-posed of the risk free rate plus an inflation premium plus a riskpremium. In our examples, the risk free "real" interest rate is 0.5%,the inflation premium is 2.5%, and the risk premium on the corporatebond is 8.1%. Add all of those together, and you get the 11.1% rate thatis the discount rate the corporate bond trades at in the markets.

10R O I a n d N e t P r e s e n tV a l u e

Which leads me to my final point. Markets set rates. Banks don't andgovernments don't. Banks and governments certainly impact ratesand governments can do a lot to impact rates and they do all the time.But at the end of the day it is you and me and it is the traders, bothspeculators and hedgers, who determine how much of a discount we'llaccept to get our money now and how much interest we'll want towait another year. It is the sum total of all of these transactions thatcreate the market and the market sets rates and they change everysecond and always will (at least in a capitalist system).

That was tough to do in a blog post. It's a very simple concept butvery powerful and as Pascal-Emmanuel said, it is fundamental to allof finance. I hope I explained it well. It's important to understand thisone.

Compounding Interest

It's time for MBA Mondays again. For the third week in a row, thetopic of the post has been suggested by a reader. Last week, EliaFreedman wrote:

"A suggestion for your next post. The logical follow-onis to explain the second half of the TVM (time value ofmoney), which is compounding interest."

Before I address the issue of compounding interest, I'd like to recognizetwo things about the MBA Monday series. The first is that each posthas a very rich comment thread attached to it. If you are seriouslyinterested in learning this stuff, you would be well served to take thetime to read the comments and the replies to them, including mine.The second is that the readers are building the curriculum for me.Each post has resulted in at least one suggestion for the next week's

R O I a n d N e t P r e s e n tV a l u e

11

post. I dove into MBA Mondays without thinking through the logicalprogression of topics. At this point, I'm just going to run withwhatever people suggest and try to assemble it on the fly. It's workingwell so far. So if you have a suggestion for next week's topic, or anytopic, please leave a comment.

Last week, I described interest as the rate of change in the time valueof money. And we broke interest rates down into the real rate, theinflation factor, and the risk factor. And we calculated that if you in-vested $900 today at an 11.1% rate of interest, you'd end up with $1000a year from now.

But what happens if you wait a few years to get your money back andreceive annual interest payments along the way? Let's say you investthe same $900, receive $100 each year for four years, and then in thelast year, you receive $1000 (your $900 back plus the final year's $100interest payment).

There are two scenarios here and they depend on what you do withthe annual interest payments.

In the first scenario, you pocket the cash and do something else withit. In that scenario, you will realize the 11.1% rate of interest that youwould have realized had you taken the $1000 one year later. It's basic-ally the same deal, just with a longer time horizon. And your totalproceeds on your $900 investment are $1400 (your $900 return of"principal" plus five $100 interest payments).

In the second scenario, you reinvest the interest payments at 11.1%each year and take a final payment in year five. If you reinvest eachinterest payment at 11.1% interest, at the end of year five, you willreceive $1524 as your final payment. Notice that the total proceedsin this scenario are $124 higher than in the other scenario. That isbecause you reinvested the interest payments instead of pocketingthem.

12R O I a n d N e t P r e s e n tV a l u e

Both scenarios produce a "rate of return" of 11.1%. If you look at thisgoogle spreadsheet

1, you can see how these two scenarios map out.

And you can see the calculation of total profit and "internal rate ofreturn".

The fact that you make a larger profit on one versus the other at thesame "rate of interest" shows the power of compounding interest. Itreally helps if you reinvest your interest payments instead of pocket-ing them. While $124 over five years doesn't seem like much, let'slook at the power of compounding interest over a longer horizon.

Let's say you inherit $100,000 around the time you graduate fromcollege. Instead of spending it on something, you decide to invest itfor your retirement 45 years later. If you invest it at the 11.1% rate ofinterest that we've been using, the differences between pocketing the$11,100 you'd get each year and reinvesting it are HUGE.

If you pocket the $11,000 of interest each year, you will receive$599,500 on your $100,000 investment over 45 years.

But if you reinvest the $11,000 of interest each year at 11.1% interest,you will receive $11.4 million dollars when you retire. That's right.$11.4 million dollars versus $599,500. That is the power of compound-ing interest over a long period of time.

You can see how this models out in this google spreadsheet (sheetstwo and three)

2.

Now let's tie this issue to startups and venture capital. Venture capitalinvestments are often held for a fairly long time. I am currentlyserving on several boards of companies that my prior firm, FlatironPartners, invested in during 1999 and 2000. Our hold periods for theseinvestments are into their second decade. Of course not every venturecapital investment lasts a decade or more. But the average hold periodfor a venture capital investment tends to be about seven or eight years.

1http://spreadsheets.google.com/ccc?key=0AvqoGGDowi93dDdFc0dCRGlBc0FFSV9zb3dYZllpSFE&hl=en2http://spreadsheets.google.com/ccc?key=0AvqoGGDowi93dDdFc0dCRGlBc0FFSV9zb3dYZllpSFE&hl=en

R O I a n d N e t P r e s e n tV a l u e

13

And during those seven to eight years, there are no annual interestpayments. So when you calculate the rate of return on the investment,the spreadsheet looks like this. It's a compound interest situation.

If you go back to the $100,000 over 45 years example, you'll see thata return of 114x your money over 45 years produces the same "return"as 6x your money with annual interest payments.

The differences are not as great over seven or eight years but they aremade greater by virtue of the fact that VCs seek to make 40-50% an-nual rates of return on their capital. If you read last week's post, you'llknow that comes from the risk factor involved. The more risk aninvestment has, the higher rate of return an investor will require ontheir money in a successful outcome.

If you want to generate a 50% rate of return compounded over eightyears on $100,000, you will need to return $2.562 million, or 25.6xyour investment. See this google spreadsheet (sheet 4)

3 for the details.

The good news is that most venture capital investments are madeover time, not all at once in the first year. So the "hold periods" on thelater rounds are not as long and make this math a bit easier oneveryone involved (maybe a topic for next week or some other time?).

But as you can see, compounding interest over any length of time in-creases significantly the amount of money you need to return in orderto pay the same rate of return as a security with annual interest pay-ments. There are two big takeaways here. The first is if you are aninvestor, you should reinvest your interest payments instead ofspending them. It makes a huge difference on the outcome of yourinvestment. The second is if you are an entrepreneur, you should takeas little money as you can at the start and always understand that yourinvestors are seeking a return and that the time value of moneycompounds and makes your job as the producer of that return partic-ularly hard.

3http://spreadsheets.google.com/ccc?key=0AvqoGGDowi93dDdFc0dCRGlBc0FFSV9zb3dYZllpSFE&hl=en

14R O I a n d N e t P r e s e n tV a l u e

Corpora te En t i t i e s

Corporate Entities

I'm taking a turn on MBA Mondays today. We are moving past theconcepts of interest and time value of money and moving into theworld of corporations. Today, I'd like to talk about what kinds ofentities you might encounter in the world of business.

First off, you don't have to incorporate to be in business. There aremany people who run a business and don't incorporate. A good ex-ample of this are many of the sellers on Etsy

1. They make things, sell

them, receive the income, and pay the taxes as part of their personalreturns.

But there are three big reasons you'll want to consider incorporating;liability, taxes, and investment. And the kind of corporate entity youcreate depends on where you want to come out on all three of thosefactors.

I'd like to say at this point that I am not a lawyer or a tax advisor andthat if you are planning on incorporating, I would recommend con-sulting both before making any decisions. I hope that we'll get bothlawyers and tax advisors commenting on this post and adding to thediscussion of these issues. I'll also say that this post is entirely basedon US law and that it does not attempt to discuss international law.

With that said, here goes.

When you start a business, it is important to recognize that it willeventually be something entirely different than you. You won't ownall of it. You won't want to be liable for everything that the companydoes. And you won't want to pay taxes on its profits.

1http://www.etsy.com/

Creating a company is implicitly recognizing those things. It is puttinga buffer between you and the business in some important ways.

Let's talk first about liability. When you create a company, you canlimit your liability for actions of the corporation. Those actions canbe for things like bills (called accounts payable in accounting parlance),promises made (like services to be rendered), and lawsuits. This is anincredibly important concept and the reason that most lawyers advisetheir clients to incorporate as soon as possible. You don't want to putyourself and your family at personal risk for the activities you under-take in your business. It's not prudent or expected in our society.

Taxes are the next thing most people think about when incorporating.There are two basic kinds of corporate entities for taxes; "flow throughentities" and "tax paying entities." Here is the difference. Flow throughcorporate entities don't pay taxes, they pass the income (and tax payingobligation) through to the owners of the business. Tax paying entitiespay the taxes at the corporate level and the owners have no obligationfor the taxes owed. Your neighborhood restaurant is probably a "flowthrough entity." Google is a tax paying entity. When you buy 100shares of Google, you are not going to get a tax bill for your share oftheir earnings at the end of the year.

And then there is investment/ownership. Even before we talk aboutinvestment, there is the issue of business partners. Let's say you wantto split the ownership of your business 50/50 with someone else. Youhave to incorporate to create the entity that you can co-own. Andwhen you want to take investment, you'll need to have a corporateentity that can issue shares or membership interests in return for thecapital that others invest in your business.

So now that we've talked about the three major considerations, let'stalk about the different kinds of entities you will come across.

For many new startups, the form of corporate entity they choose iscalled the LLC. It stands for Limited Liability Company

2. This form

of business has been around for a long time in some countries but be-

2http://en.wikipedia.org/wiki/Limited_liability_company

16C o r p o r a t e E n t i t i e s

came recognized and popular in the US sometime in the past 25 years.The key distinguishing characteristics of a LLC is that you get thelimitation of liability of a corporation, you can take investment cap-ital (with restrictions that we'll talk about next), but the taxes are"flow through". Most companies, including tech startups, start out asLLCs these days. Owners in LLC are most commonly called "members"and investments or ownership splits are structured in "membershipinterests."

As the business grows and takes on more sophisticated investors (likeventure funds), it will most often convert into something called a CCorporation

3. Most of the companies you would buy stock in on the

public markets (Google, Apple, GE, etc) are C Corporations. Mostventure backed companies are C Corporations. C Corporationsprovide the limitation of liability, provide even more sophisticatedways to split ownership and raise capital, and most importantly are"tax paying entities." Once you convert from a LLC to a C corporation,you as the founder or owner no longer are responsible for paying thetaxes on your share of the income. The company pays those taxes atthe corporate level.

There are many reasons why a venture fund or other "sophisticatedinvestors" prefer to invest in a C corporation over a LLC. Most ven-ture funds require conversion when they invest. The flow throughof taxes in the LLC can cause venture funds and their investors allsorts of tax issues. This is particularly true of venture funds withforeign investors. And the governance and ownership structures ofan LLC are not nearly as developed as a C corporation. This stuff canget really complicated quickly, but the important thing to know isthat when your business is small and "closely held" a LLC works well.When it gets bigger and the ownership gets more complicated, you'llwant to move to a C corporation.

A nice hybrid between the C corporation and the LLC is the S corpor-ation

4. It requires a simpler ownership structure, basically one class

of stock and less than 100 shareholders. It is a "flow through entity"

3http://en.wikipedia.org/wiki/C_corporation4http://en.wikipedia.org/wiki/S_corporation

C o r p o r a t e E n t i t i e s17

and is simple to set up. You cannot do as much with the ownershipstructure with an S corporation as you can with a LLC so if you planto stay a flow through entity for a long period of time and raise signi-ficant capital, an LLC is probably better.

Another entity you might come across is the Limited Partnership5.

The funds our firm manages are Limited Partnerships. And some bigcompanies, like Bloomberg LP, are limited partnerships. The keydifferences between a Limited Partnership and LLCs and C corpora-tions are around liabilities. In the limited partnership, the investorshave limited liability (like a LLC or C corporation) but the managers(called General Partners) do not. Limited Partnerships are set up totake in outside investment and split ownership. And they are flowthrough entities.

There are many other forms of corporate ownership but these threeare among the most common and show how the three big issues ofliability, ownership, and taxes are handled differently in each.

The important thing to remember about all of this is that if you arestarting a business, you should create a corporate entity to managethe risk and protect you and your family from it. You should startwith something simple and evolve it as the business needs grow anddevelop.

As an investor, you should make sure you know what kind of corpor-ation you are investing in, you should know what kind of liabilityyou are exposing yourself to, and what the tax obligations will be asa result.

And most of all, get a good lawyer and tax advisor. Though they areexpensive, over time the best ones are worth their weight in gold.

5http://en.wikipedia.org/wiki/Limited_partnership

18C o r p o r a t e E n t i t i e s

Piercing the Corporate Veil

Yet another MBA Monday topic comes from the comments of lastweek's post

1. This series is turning into a conversation which makes

me very pleased.

Mr Shawn Yeager said2:

As a recovering lawyer, and a serial entrepreneur, I con-stantly have associates, friends, and family coming tome for advice on formation issues (amongst other things).I think your high level overview leaves out something thatalways comes as a surprise to these people: the concept of"Piercing the Corporate Veil" of liability protection.

I said last week that forming a company is the best way to "putting abuffer between you and the business." But as Shawn and others pointout in last week's comment thread, you can't just pretend to be abusiness, you have to be a business.

"Being a business" means separating your personal and business re-cords, separating your personal and business bank accounts, treatingthe business as a real entity, having board meetings, taking boardminutes, doing major activities via board resolutions, following "dueprocess."

If you don't behave as a real business, you could find yourself in asituation where someone, most commonly someone who is suingyour business, can come after you (and your business partners) per-sonally. And then you are going to say "but what about the liabilitylimitation the business provides?" It may not be there for you.

1http://www.avc.com/a_vc/2010/02/corporate-entity.html2http://www.avc.com/a_vc/2010/02/corporate-entity.html#comment-36092343

C o r p o r a t e E n t i t i e s19

That's called "piercing the corporate veil". And you should take thatthreat seriously. So once you create a company, treat it seriously, fol-low the rules, and do it right. Once again, if you have a good lawyer,he or she will lay this all out for you and even give you many of thetools to do this stuff right.

20C o r p o r a t e E n t i t i e s

Account ing

Accounting

I'm making up the curriculum for MBA Mondays on the fly. The endgame is to lay out how to look a businesses, value it, and invest in it.We started with the time value of money and interest rates, we thentalked about the corporate entity. Now I want to talk about how tokeep track of the money in a company. That is called accounting. Thiswill be a multi-post effort and will include posts on cash flow, profitand loss, balance sheets, GAAP accounting, audits, and financialstatement analysis. But before we can get to those issues, we need tostart with the basics of accounting.

Accounting is keeping track of the money in a company. It's criticalto keep good books and records for a business, no matter how smallit is. I'm not going to lay out exactly how to do that, but I am goingto discuss a few important principals.

The first important principal is every financial transaction of acompany needs to be recorded. This process has been made mucheasier with the advent of accounting software. For most startups,Quickbooks

1 will do in the beginning. As the company grows, the

choice of accounting software will become more complicated, but bythen you will have hired a financial team that can make those choices.

The recording of financial transactions is not an art. It is a science anda well understood science. It revolves around the twin concepts of a"chart of accounts" and "double entry accounting." Let's start with thechart of accounts.

The accounting books of a company start with a chart of accounts.There are two kinds of accounts; income/expense accounts and as-

1http://quickbooks.intuit.com/

set/liability accounts. The chart of accounts includes all of them. In-come and expense accounts represent money coming into and out ofa business. Asset and liability accounts represent money that is con-tained in the business or owed by the business.

Advertising revenue that you receive from Google Adsense would bean income account. The salary expense of a developer you hire wouldbe an expense account. Your cash in your bank account would be anasset account. The money you owe on your company credit cardwould be called "accounts payable" and would be a liability.

When you initially set up your chart of accounts, the balance in eachand every account is zero. As you start entering financial transactionsin your accounting software, the balances of the accounts goes up orpossibly down.

The concept of double entry accounting is important to understand.Each financial transaction has two sides to it and you need both ofthem to record the transaction. Let's go back to that Adsense revenueexample. You receive a check in the mail from Google. You depositthe check at the bank. The accounting double entry is you record anincrease in the cash asset account on the balance sheet and a corres-ponding equal increase in the advertising revenue account. Whenyou pay the credit card bill, you would record a decrease in the cashasset account on the balance sheet and a decrease in the "accountspayable" account on the balance sheet.

These accounting entries can get very complicated with many ac-counts involved in a single recorded transaction, but no matter howcomplicated the entries get the two sides of the financial transactionalways have to add up to the same amount. The entry must balanceout. That is the science of accounting.

Since the objective of MBA Mondays is not to turn you all into ac-countants, I'll stop there, but I hope everyone understands what achart of accounts and an accounting entry is now.

Once you have a chart of accounts and have recorded financialtransactions in it, you can produce reports. These reports are simply

22A c c o u n t i n g

the balances in various accounts or alternatively the changes in thebalances over a period of time.

The next three posts are going to be about the three most commonreports;

• the profit and loss statement which is a report of the changes inthe income and expense accounts over a certain period of time(month and year being the most common)

• the balance sheet which is a report of the balances all all asset andliability accounts at a certain point in time

• the cash flow statement which is report of the changes in all of theaccounts (income/expense and asset/liability) in order to determinehow much cash the business is producing or consuming over acertain period of time (month and year being the most common)

If you have a company, you must have financial records for it. Andthey must be accurate and up to date. I do not recommend doing thisyourself. I recommend hiring a part-time bookkeeper to maintainyour financial records at the start. A good one will save you all sortsof headaches. As your company grows, eventually you will need a fulltime accounting person, then several, and at some point your financeorganization could be quite large.

There is always a temptation to skimp on this part of the business.It's not a core part of most businesses and is often not valued by techentrepreneurs. But please don't skimp on this. Do it right and well.And hire good people to do the accounting work for your company.It will pay huge dividends in the long run.

A c c o u n t i n g23

The Profit and Loss Statement

Today on MBA Mondays we are going to talk about one of the mostimportant things in business, the profit and loss statement (also knownas the P&L).

Picking up from the accounting post1 last week, there are two kinds

of accounting entries; those that describe money coming into and outof your business, and money that is contained in your business. TheP&L deals with the first category.

A profit and loss statement is a report of the changes in the incomeand expense accounts over a set period of time. The most commonperiods of time are months, quarters, and years, although you canproduce a P&L report for any period.

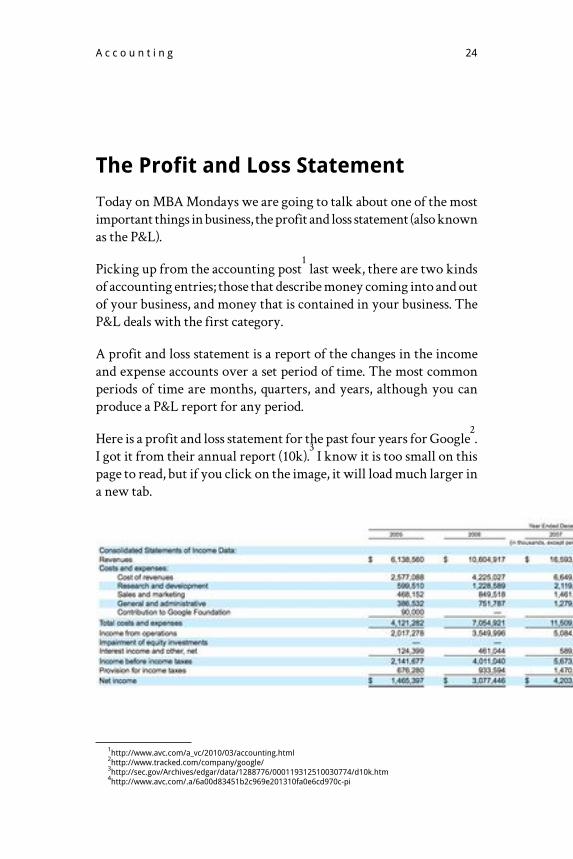

Here is a profit and loss statement for the past four years for Google2.

I got it from their annual report (10k).3 I know it is too small on this

page to read, but if you click on the image, it will load much larger ina new tab.

4

1http://www.avc.com/a_vc/2010/03/accounting.html2http://www.tracked.com/company/google/3http://sec.gov/Archives/edgar/data/1288776/000119312510030774/d10k.htm4http://www.avc.com/.a/6a00d83451b2c969e201310fa0e6cd970c-pi

24A c c o u n t i n g

The top line of profit and loss statements is revenue (that's why you'lloften hear revenue referred to as "the top line"). Revenue is the totalamount of money you've earned coming into your business over a setperiod of time. It is NOT the total amount of cash coming into yourbusiness. Cash can come into your business for a variety of reasons,like financings, advance payments for services to be rendered in thefuture, payments of invoices sent months ago.

There is a very important, but highly technical, concept called revenuerecognition. Revenue recognition determines how much revenueyou will put on your accounting statements in a specific time period.For a startup company, revenue recognition is not normally difficult.If you sell something, your revenue is the price at which you sold theitem and it is recognized in the period in which the item was sold. Ifyou sell advertising, revenue is the price at which you sold the advert-ising and it is recognized in the period in which the advertising actu-ally ran on your media property. If you provide a subscription service,your revenue in any period will be the amount of the subscriptionthat was provided in that period.

This leads to another important concept called "accrual accounting."When many people start keeping books, they simply record cash re-ceived for services rendered as revenue. And they record the bills theypay as expenses. This is called "cash accounting" and is the way mostof us keep our personal books and records. But a business is not sup-posed to keep books this way. It is supposed to use the concept of ac-crual accounting.

Let's say you hire a contract developer to build your iPhone app. Andyour deal with him is you'll pay him $30,000 to deliver it to you. Andlet's say it takes him three months to build it. At the end of the threemonths you pay him the $30,000. In cash accounting, in month threeyou would record an expense of $30,000. But in accrual accounting,each month you'd record an expense of $10,000 and because you aren'tactually paying the developer the cash yet, you charge the $10,000each month to a balance sheet account called Accrued Expenses. Thenwhen you pay the bill, you don't touch the P&L, its simply a balance

A c c o u n t i n g25

sheet entry that reduces Cash and reduces Accrued Expenses by$30,000.

The point of accrual accounting is to perfectly match the revenuesand expenses to the time period in which they actually happen, notwhen the payments are made or received.

With that in mind, let's look at the second part of the P&L, the expensesection. In the Google P&L above, expenses are broken out into severalcategories; cost of revenues, R&D, sales and marketing, and generaland administration. You'll note that in 2005, there was also a contri-bution to the Google Foundation, but that only happened once, in2005.

The presentation Google uses is quite common. One difference youwill often see is the cost of revenues applied directly against the rev-enues and a calculation of a net amount of revenues minus cost ofrevenues, which is called gross margin. I prefer that gross margin bebroken out as it is a really important number. Some businesses havevery high costs of revenue and very low gross margins. And examplewould be a retailer, particularly a low price retailer. The gross marginsof a discount retailer could be as low as 25%.

Google's gross margin in 2009 was roughly $14.9bn (revenue of $23.7bnminus cost of revenues of $8.8bn). The way gross margin is most oftenshown is as a percent of revenues so in 2009 Google's gross marginwas 63% (14.9bn divided by 23.7). I prefer to invest in high gross marginbusinesses because they have a lot of money left after making a saleto pay for the other costs of the business, thereby providing resourcesto grow the business without needing more financing. It is also mucheasier to get a high gross margin business profitable.

The other reason to break out "cost of revenues" is that it will mostlikely increase with revenues whereas the other expenses may not.The non cost of revenues expenses are sometimes referred to as"overhead". They are the costs of operating the business even if youhave no revenue. They are also sometimes referred to as the "fixedcosts" of the business. But in a startup, they are hardly fixed. Theseexpenses, in Google's categorization scheme, are R&D, sales and

26A c c o u n t i n g

marketing, and general/admin. In layman's terms, they are the costsof making the product, the costs of selling the product, and the costof running the business.

The most interesting line in the P&L to me is the next one, "IncomeFrom Operations" also known as "Operating Income." Income FromOperations is equal to revenue minus expenses. If "Income From Op-erations" is a positive number, then your base business is profitable.If it is a negative number, you are losing money. This is a criticalnumber because if you are making money, you can grow your businesswithout needing help from anyone else. Your business is sustainable.If you are not making money, you will need to finance your businessin some way to keep it going. Your business is unsustainable on itsown.

The line items after "Income From Operations" are the additionalexpenses that aren't directly related to your core business. They in-clude interest income (from your cash balances), interest expense(from any debt the business has), and taxes owed (federal, state, local,and possibly international). These expenses are important becausethey are real costs of the business. But I don't pay as much attentionto them because interest income and expense can be changed bymaking changes to the balance sheet and taxes are generally only paidwhen a business is profitable. When you deduct the interest and taxesfrom Income From Operations, you get to the final number on theP&L, called Net Income.

I started this post off by saying that the P&L is "one of the most im-portant things in business." I am serious about that. Every businessneeds to look at its P&L regularly and I am a big fan of sharing theP&L with the entire company. It is a simple snapshot of the health ofa business.

I like to look at a "trended P&L" most of all. The Google P&L that Ishowed above is a "trended P&L" in that it shows the trends in reven-ues, expenses, and profits over five years. For startup companies, Iprefer to look at a trended P&L of monthly statements, usually overa twelve month period. That presentation shows how revenues are

A c c o u n t i n g27

increasing (hopefully) and how expenses are increasing (hopefullyless than revenues). The trended monthly P&L is a great way to lookat a business and see what is going on financially.

I'll end this post with a nod to everyone who commented last weekthat numbers don't tell you everything about a business. That is verytrue. A P&L can only tell you so much about a business. It won't tellyou if the product is good and getting better. It won't tell you howthe morale of the company is. It won't tell you if the managementteam is executing well. And it won't tell you if the company has theright long term strategy. Actually it will tell you all of that but afterit is too late to do anything about it. So as important as the P&L is, itis only one data point you can use in analyzing a business. It's a goodplace to start. But you have to get beyond the numbers if you reallywant to know what is going on.

The Balance Sheet

Today on MBA Mondays we are going to talk about the Balance Sheet.

The Balance Sheet shows how much capital you have built up in yourbusiness.

If you go back to my post on Accounting1, you will recall that there

are two kinds of accounts in a company's chart of accounts; revenueand expense accounts and asset and liability accounts.

Last week we talked about the Profit and Loss statement2 which is a

report of the revenue and expense accounts.

The Balance Sheet is a report of the asset and liability accounts. Assetsare things you own in your business, like cash, capital equipment, andmoney that is owed to you for products and services you have de-

1http://www.avc.com/a_vc/2010/03/accounting.html2http://www.avc.com/a_vc/2010/03/the-profit-and-loss-statement.html

28A c c o u n t i n g

livered to customers. Liabilities are obligations of the business, likebills you have yet to pay, money you have borrowed from a bank orinvestors.

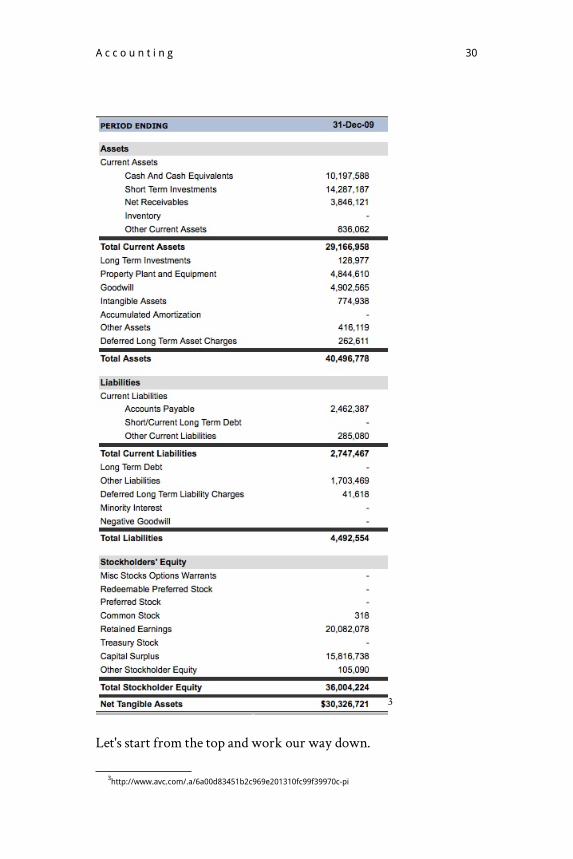

Here is Google's balance sheet as of 12/31/2009:

A c c o u n t i n g29

3

Let's start from the top and work our way down.

3http://www.avc.com/.a/6a00d83451b2c969e201310fc99f39970c-pi

30A c c o u n t i n g

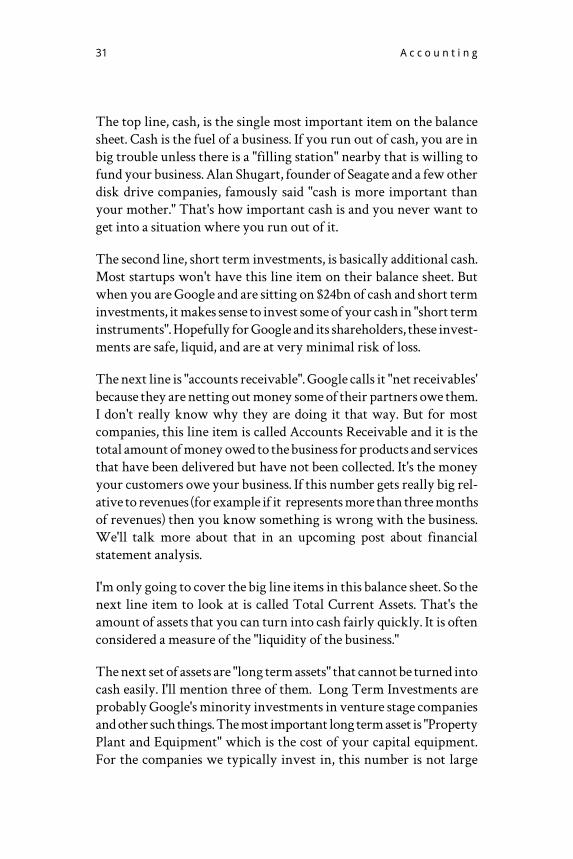

The top line, cash, is the single most important item on the balancesheet. Cash is the fuel of a business. If you run out of cash, you are inbig trouble unless there is a "filling station" nearby that is willing tofund your business. Alan Shugart, founder of Seagate and a few otherdisk drive companies, famously said "cash is more important thanyour mother." That's how important cash is and you never want toget into a situation where you run out of it.

The second line, short term investments, is basically additional cash.Most startups won't have this line item on their balance sheet. Butwhen you are Google and are sitting on $24bn of cash and short terminvestments, it makes sense to invest some of your cash in "short terminstruments". Hopefully for Google and its shareholders, these invest-ments are safe, liquid, and are at very minimal risk of loss.

The next line is "accounts receivable". Google calls it "net receivables'because they are netting out money some of their partners owe them.I don't really know why they are doing it that way. But for mostcompanies, this line item is called Accounts Receivable and it is thetotal amount of money owed to the business for products and servicesthat have been delivered but have not been collected. It's the moneyyour customers owe your business. If this number gets really big rel-ative to revenues (for example if it represents more than three monthsof revenues) then you know something is wrong with the business.We'll talk more about that in an upcoming post about financialstatement analysis.

I'm only going to cover the big line items in this balance sheet. So thenext line item to look at is called Total Current Assets. That's theamount of assets that you can turn into cash fairly quickly. It is oftenconsidered a measure of the "liquidity of the business."

The next set of assets are "long term assets" that cannot be turned intocash easily. I'll mention three of them. Long Term Investments areprobably Google's minority investments in venture stage companiesand other such things. The most important long term asset is "PropertyPlant and Equipment" which is the cost of your capital equipment.For the companies we typically invest in, this number is not large

A c c o u n t i n g31

unless they rack their own servers. Google of course does just thatand has spent $4.8bn to date (net of depreciation) on its "factory". De-preciation is the annual cost of writing down the value of yourproperty plant and equipment. It appears as a line in the profit andloss statement. The final long term asset I'll mention is Goodwill. Thisis a hard one to explain. But I'll try. When you purchase a business,like YouTube, for more than it's "book value" you must record thedifference as Goodwill. Google has paid up for a bunch of businesses,like YouTube and Doubleclick, and it's Goodwill is a large number,currently $4.9bn. If you think that the value of any of the businessesyou have acquired has gone down, you can write off some or all ofthat Goodwill. That will create a large one time expense on yourprofit and loss statement.

After cash, I believe the liability section of the balance sheet is themost important section. It shows the businesses' debts. And the otherthing that can put you out of business aside from running out of cashis inability to pay your debts. That is called bankruptcy. Of course,running out of cash is one reason you may not be able to pay yourdebts. But many companies go bankrupt with huge amounts of cashon their books. So it is critical to understand a company's debts.

The main current liabilities are accounts payable and accrued expenses.Since we don't see any accrued expenses on Google's balance sheet Iassume they are lumping the two together under accounts payable.They are closely related. Both represent expenses of the business thathave yet to be paid. The difference is that accounts payable are forbills the company receives from other businesses. And accrued ex-penses are accounting entries a company makes in anticipation ofbeing billed. A good example of an accounts payable is a legal bill youhave not paid. A good example of an accrued expense is employeebenefits that you have not yet been billed for that you accrue for eachmonth.

If you compare Current Liabilities to Current Assets, you'll get a senseof how tight a company is operating. Google's current assets are $29bnand its current liabilities are $2.7bn. It's good to be Google, they are

32A c c o u n t i n g

not sweating it. Many of our portfolio companies operate with thesenumbers close to equal. They are sweating it.

Non current liabilities are mostly long term debt of the business. Theamount of debt is interesting for sure. If it is very large compared tothe total assets of the business its a reason to be concerned. But itseven more important to dig into the term of the long term debt andfind out when it is coming due and other important factors. You won'tfind that on the balance sheet. You'll need to get the footnotes of thefinancial statements to do that. Again, we'll talk more about that in afuture post on financial statement analysis.

The next section of the balance sheet is called Stockholders Equity.This includes two categories of "equity". The first is the amount thatequity investors, from VCs to public shareholders, have invested inthe business. The second is the amount of earnings that have beenretained in the business over the years. I'm not entirely sure howGoogle breaks out the two on it's balance sheet so we'll just talk aboutthe total for now. Google's total stockholders equity is $36bn. That isalso called the "book value" of the business.

The cool thing about a balance sheet is it has to balance out. TotalAssets must equal Total Liabilities plus Stockholders Equity. InGoogle's case, total assets are $40.5bn. Total Liabilities are $4.5bn. Ifyou subtract the liabilities from the assets, you get $36bn, which isthe amount of stockholders equity.

We'll talk about cash flow statements next week and the fact that abalance sheet has to balance can be very helpful in analyzing andprojecting out the cash flow of a business.

In summary, the Balance Sheet shows the value of all the capital thata business has built up over the years. The most important numbersin it are cash and liabilities. Always pay attention to those numbers.I almost never look at a profit and loss statement without also lookingat a balance sheet. They really should be considered together as theyare two sides of the same coin.

A c c o u n t i n g33

Cash Flow

This week on MBA Mondays1 we are going to talk about cash flow.

A few weeks ago, in my post on Accounting2, I said there were three

major accounting statements. We’ve talked about the Income State-ment

3 and the Balance Sheet

4. The third is the Cash Flow Statement.

I’ve never been that interested in the Cash Flow Statement per se. Thestandard form of a cash flow statement is a bit hard to comprehendin my opinion and I don’t think it does a very good job of describingthe various aspects of cash flow in a business.

That said, let’s start with the concept of cash flow and we’ll come backto the accounting treatment.

Cash flow is the amount of cash your business either produces orconsumes in a given period, typically a month, quarter, or year. Youmight think that is the same as the profit of the business, but that isnot correct for a bunch of reasons.

The profit of a business is the difference between revenues and ex-penses. If revenues are greater than expenses, your business is produ-cing a profit. If expenses are greater than revenues, your business isproducing a loss.

But there are many examples of profitable businesses that consumecash. And there are also examples of unprofitable businesses thatproduce cash, at least for a period of time.

Here’s why.

As I explained in the Income Statement post5, revenues are recognized

as they are earned, not necessarily when they are collected. And ex-

1http://www.avc.com/a_vc/mba-mondays/2http://www.avc.com/a_vc/2010/03/accounting.html3http://www.avc.com/a_vc/2010/03/the-profit-and-loss-statement.html4http://www.avc.com/a_vc/2010/03/the-balance-sheet.html5http://www.avc.com/a_vc/2010/03/the-profit-and-loss-statement.html

34A c c o u n t i n g

penses are recognized as they are incurred, not necessarily when theyare paid for. Also, some things you might think of as expenses of abusiness, like buying servers, are actually posted to the Balance Sheetas property of the business and then depreciated (ie expensed) overtime.

So if you have a business with significant hardware requirements,like a hosting business for example, you might be generating a profiton paper but the cash outlays you are making to buy servers maymean your business is cash flow negative.

Another example in the opposite direction would be a software as aservice business where your company gets paid a year in advance foryour software subscription revenues. You collect the revenue upfrontbut recognize it over the course of the year. So in the month you col-lect the revenue from a big customer, you might be cash flow positive,but your Income Statement would show the business operating at aloss.

Cash flow is really easy to calculate. It’s the difference between yourcash balance at the start of whatever period you are measuring andthe end of that period. Let’s say you start the year with $1mm in cashand end the year with $2mm in cash. Your cash flow for the year ispositive by $1mm. If you start the year with $1mm in cash and endthe year with no cash, your cash flow for the year is negative by $1mm.

But as you might imagine the accounting version of the cash flowstatement is not that simple. Instead of getting into the standard form,which as I said I don’t really like, let’s talk about a simpler form thatgets you to mostly the same place.

Let’s say you want to do a cash flow statement for the past year. Youstart with your Net Income number from your Income Statement forthe year. Let’s say that number is $1mm of positive net income.

Then you look at your Balance Sheet from the prior year and thecurrent year. Look at the Current Assets (less cash) at the start of theyear and the Current Assets (less cash) at the end of the year. If theyhave gone up, let’s say by $500,000, then you subtract that number

A c c o u n t i n g35

from your Net Income. The reason you subtract the number is yourbusiness used some of your cash to increase its current assets. Onetypical reason for that is your Accounts Receivable went up becauseyour customers are taking longer to pay you.

Then look at your Non-Current Assets at the start of the year and theend of the year. If they have gone up, let’s say by $500k, then you alsosubtract that number from your Net Income. The reason is yourbusiness used some of your cash to increase its Non-Current Assets,most likely Property, Plant, and Equipment (like servers).

At this point, halfway through this simplified cash flow statement,your business that had a Net Income of $1mm produced no cash be-cause $500k of it went to current assets and $500k of it went to non-current assets.

Liabilities work the other way. If they go up, you add the number toNet Income. Let’s start with Current Liabilities such as AccountsPayable (money you owe your suppliers, etc). If that number goes upby $250k over the course of the year, you are effectively using yoursuppliers to finance your business. Another reason current liabilitiescould go up is Deferred Revenue went up. That would mean you areeffectively using your customers to finance your business (like thatsoftware as a service example earlier on in this post).

Then look at Long Term Liabilities. Let’s say they went up by $500kbecause you borrowed $500k from the bank to purchase the serversthat caused your Non-Current Assets to go up by $500k. So add that$500k to Net Income as well.

Now, the simplified cash flow statement is showing $750k of positivecash flow. But we have one more section of the Balance Sheet to dealwith, Stockholders Equity. For Stockholders Equity, you need to backout the current year’s net income because we started with that. Onceyou do that, the main reason Stockholders Equity would go up wouldbe an equity raise. Let’s say you raised $1mm of venture capital duringthe year and so Stockholder’s Equity went up by $1mm. You’d addthat $1mm to Net Income as well.

36A c c o u n t i n g

So, that’s basically it. You start with $1mm of Net Income, subtract$500k of increased current assets, subtract $500k of increased non-current assets, add $250k of increased current liabilities, add $500k ofincreased long-term liabilities, and add $1mm of increased stockhold-ers equity, and you get positive cash flow of $1.75mm.

Of course, you’ll want to check this against the cash balance at thestart of the year and the end of the year to make sure that in fact cashdid go up by $1.75mm. If it didn’t, then you have to go back and checkyour math.

So why would anyone want to do the cash flow statement the longway if you can simply compare cash at the start of the year and theend of the year? The answer is that doing a full-blown cash flowstatement tells you a lot about where you are consuming or producingcash. And you can use that information to do something about it.

Let’s say that your cash flow is weak because your accounts receivableare way too high. You can hire a dedicated collections person. Youcan start cutting off customers who are paying you too late. Or youcan do a combination of both. Bringing down accounts receivable isa great way to improve a business’ cash flow.

Let’s say you are spending a boatload on hardware to ramp up yourweb service’s capacity. And it is bringing your cash flow down. If youare profitable or have good financial backers, you can go to a bankand borrow against those servers. You can match non-current assetsto long-term liabilities so that together they don’t impact the cashflow of your business.

Let’s say your current liabilities went down over the past year by$500k. That’s a $500k reduction in your cash flow. Maybe you arepaying your bills much more quickly than you did when you startedthe business and had no cash. You might instruct your accountingteam to slow down bill payment a bit and bring it back in line withprior practices. That could help produce better cash flow.

These are but a few examples of the kinds of things you can learn bydoing a cash flow statement. It’s simply not enough to look at the In-

A c c o u n t i n g37

come Statement and the Balance Sheet. You need to understand thethird piece of the puzzle to see the business in its entirety.

One last point and I am done with this week’s post. When you aredoing projections for future years, I encourage management teamsto project the income statement first, then the cash flow statement,and then end up with the balance sheet. You can make assumptionsabout how the line items in the Income Statement will cause thevarious Balance Sheet items to change (like Accounts Receivableshould be equal to the past three months of revenue) and then lay allthat out as a cash flow statement and then take the changes in thevarious items in the cash flow statement to build the Balance Sheet.I like to do that in monthly form. We’ll talk more about projectionsnext week because I think this is a very important subject for startupsand entrepreneurial management teams to wrap their heads around.

Analyzing Financial Statements

This topic could be and is a full semester course at some businessschools. It is a deep and rich topic that I can’t cover in one single blogpost. But it is also a relatively narrow skill set at its most developedlevels. If you are going to be a public equity analyst, you need to un-derstand this stuff cold and this post will not get you there.

But if you are an entrepreneur being handed financial statementsfrom your bookkeeper or accountant or controller, then you need tobe able to understand them and I’d like this post to help you do that.I’d also like this post help those of you who want to be more confidentbuying, holding, and selling public stocks. So that’s the perspective Iwill bring to this topic.

In the past three weeks, we talked about the three main financialstatements, the Income Statement

1, the Balance Sheet

2, and the Cash

1http://www.avc.com/a_vc/2010/03/the-profit-and-loss-statement.html2http://www.avc.com/a_vc/2010/03/the-balance-sheet.html

38A c c o u n t i n g

Flow Statement3. This post is going to attempt to help you figure out

how to analyze them, at least at a cursory level.

In general, I like to start with cash. It’s the first line item on the BalanceSheet (it could be the first several lines if you want to combine it withshort term investments). Note how much cash you have or how muchcash the company you are analyzing has. Remember that number. Ifsomeone asks you how much cash you have in your business, or abusiness you are analyzing, and you can’t answer that to the last ac-counting period (at least), then you failed. There is no middle ground.Cash is that important.

Then look at how much cash the business had in a prior period. Lastmonth is a good place to start but don’t end there. Look at how muchcash went up or down in the past month. Then look much fartherback, at least a quarter, and ideally six months and/or a year. Calculatehow much cash went up or down over the period and then divide bythe number of months in the period. That’s the average cash flow (orcash burn) per month. Remember that number.

But that number can be misleading, particularly if you did any debtor equity financings during that period (or if you paid off any debtfacilities during that period). Back out the debt and equity financingsand do the same calculations of average cash flow per month. Hope-fully the monthly number, the quarterly average, the six-month av-erage, and the annual average are in the same ballpark. If they are not,something is changing in the business, either for the good or the badand you need to dig deeper to find out what. We’ll get to that.

If cash flow is positive for all periods, then you are done with cash. Ifit is negative, do one more thing. Divide your cash balance by the av-erage monthly burn rate and figure out how many months of cashyou have left. If you are burning cash, you need to know this numberby heart as well. It is the length of your runway. For all you entrepren-eurs out there, the three cash related numbers you need to be on topof are current cash balance, cash burn rate, and months of runway.

3http://www.avc.com/a_vc/2010/03/cash-flow.html

A c c o u n t i n g39

I generally like to go to the income statement next. And I like to layout a few periods next to each other, ideally chronologically fromoldest on the left to the newest on the right. For startups and earlystage companies, a 12 month trended monthly presentation of theincome statement is ideal. For more mature companies, includingpublic companies, the current quarter and the four previous quartersare best.Some people like to graph the key line items in the income statement(revenue, gross margin, operating costs, operating income) over time. That’s good if you are a visual person. I find looking at the hardnumbers works better for me. Note how things are moving in thebusiness. In a perfect world, revenues and gross margins are growingfaster than operating costs, and operating income (or losses) are in-creasing (or decreasing) faster than both of them. That is a demonstra-tion of the operating leverage in the business.

But some early stage companies either have no revenue or are invest-ing in the business faster than they are growing revenue. That is asound strategy if the investments they are making are solid ones andif they have a timeline laid out during which they’ll do this. You can’tdo that forever. You’ll run out of cash and go out of business.

From this analysis, you may see why the business is burning cash orburning cash more quickly or less quickly. You may see why thebusiness is growing its cash flow rapidly. I am most comfortable whenthe monthly operating income (or losses) of a business are roughlyequal to its cash flow (or cash burn). This does not have to be the casefor the business to be healthy but it means the business has a relativelysimple economic architecture, which is always comforting. FromEnron to Lehman Brothers, we’ve learned that complex business ar-chitectures are hard to analyze and easy to manipulate.

One thing that bears mentioning here are “one time items” on the In-come Statement. They make your life harder. If you go back to theIncome Statement post

4 and look at Google’s statement, you’ll see that

in the first year of their presentation Google made a one-time contri-bution to the Google Foundation. That depressed earnings in that

4http://www.avc.com/a_vc/2010/03/the-profit-and-loss-statement.html

40A c c o u n t i n g

period. You need to back that one time charge out for a consistentpresentation, but you also need to be somewhat suspicious of one-time charges. Companies can try to bury ongoing expenses in one-time charges and inflate their earnings. You don’t see that much instartups but you do in public companies and it’s a “red flag” if a com-pany does it too often.

If the monthly operating income (after backing out one-time charges)doesn’t come close to the monthly cash burn rates, then something isgoing on with the balance sheet of the business. Many of these differ-ences are normal for certain businesses. My friend Ron Schreiber toldme about a software distribution business he and his partner JordanLevy ran in the mid 80s. They would buy software from Microsoft,Lotus, and others in bulk and sell it in small quantities to mom andpop businesses. Microsoft and Lotus wanted to be paid upfront whenthe shipped the software but the mom and pop businesses were run-ning on fumes and could not pay until they sold the software. So Ron’sbusiness, called Software Distribution Services (of course), was alwaysout of cash. In Ron’s words, they were a bank and a distributioncompany and weren’t getting paid for the banking part of their busi-ness. All during this time the revenue line and the operating incomeline was growing fast and furious as desktop software went from aniche business to a mainstream business. Eventually Ron and Jordanhad to sell their business to Ingram, a large book distributor who hadthe financial resources to provide the “banking services”. They madea nice hit on that company, but not anything like what Microsoft andLotus did even though they grew their topline just as fast as theirsuppliers.Ron and Jordan’s business was “working capital intensive.” Workingcapital is the non cash current assets and liabilities of the business.When they grow rapidly in relation to revenues, it means you arefinancing other parts of the food chain in your industry and that’s agreat way to run out of cash.

So if monthly income and monthly cash flow aren’t in the same ball-park, look at the changes in working capital month over month. Wewent over this a bit last week in preparing the cash flow statement.

A c c o u n t i n g41

If working capital is the culprit soaking up the cash, you need to lookat two things.The first is if the revenues are real. A great way to inflate revenues isto “ship product” to people who aren’t going to pay you. A companythat is doing that is operating fraudently so you don’t see it very often.But if someone is doing this, cash will be going down while profitsare steady and accounts receivable are growing rapidly. I always lookfor that in a company that is supposed to be profitable but is suckingcash.

The second is the availability of working capital financing. If a busi-ness can finance its working capital needs inexpensively, then it canoperate successfully with this business model. In times when debt isflowing freely, these can be good businesses to operate. When cash istight, they are not.

The final thing to look for on the balance sheet is capex. If a businessis operating profitably, and growing profits, but its capex line isgrowing faster than profits, it’s got the potential for problems. Hostingcompanies are an example of a set of companies that might be in thissituation. Again, the availability of financing is the key. Local cableoperators operated profitably for years with big negative cash flowsbecause of capex. The fiancial markets like the monopolies thesebusineses were granted and consistently provided them with financingto buy more capex. But if that party ends, it can be painful.This post is three pages long in my editor so it’s time to stop. Thereis more to discuss on this topic so I’d like to know if I did this topicjustice for most of you or if you’d like another post that digs a littledeeper. My preference is to move on because I’m getting a bit tired ofwriting about accounting every Monday, but most of all I want tocover the stuff you want to learn or freshen up on. So let me know.

42A c c o u n t i n g

Bus ines s , Met r i c s andPr i c ing

Key Business MetricsThe past five MBA Mondays posts have been about accounting con-cepts, financial statements, and related issues. I don't know about allof you, but I'm a bit tired of that stuff. So I'm moving on to somethinga bit different.

Every business should have a set of metrics that it tracks on a regularbasis. These metrics could include some of the accounting stuff we'vebeen talking about like cash, revenues, profits, etc but it should notbe limited to those kinds of metrics.

Early on when the company is developing its first product or service,those metrics might be related to product development like develop-ment resources, features completed, known bugs, etc. Once the productor service is launched, the metrics might shift to include customers,daily active users, churn, conversions from free trial to paid customer,etc.

As the business grows and develops, the amount of data you can collectand publish to your team grows. If you aren't careful, you can over-whelm your team with data.

It becomes very important to distill the business down to a handfulof key business metrics. There are usually four to six metrics that willbe sufficient to determine the overall health and growth trajectoryof the business and it is best to focus the team on them.

Our portfolio company Meetup 1has learned to focus on successful

Meetup groups. Those are Meetup groups that are active, meetingregularly, have growing memberships, and are paying fees to Meetup.Meetup could focus on other data sets like monthly unique visitors,new Meetup groups, total registered users, revenues, profits, cash.They collect that data and share it with the team. But the number onething they look at it successful Meetup groups and that has workedwell for them. It is their key business metric.

Sometimes the most important data on your business is the hardestto collect. Twitter

2 knows that the total number of times all tweets

have been viewed each day, month, or year is a critical measure of theoverall reach of the network. But because so many of those tweets areviewed on third party services, web pages, apps, etc, it is very hard tocollect that data. The Company is only now starting to measure them.

Most key business metrics will be drivers of revenues and growthbut not all of them. Etsy

3 is focusing a lot of effort on its customer

service metrics, which are a cost center not a revenue driver. But theCompany knows that customer service is critical to the health of themarketplace, so customer service metrics are key business metricsfor them.

The management team should spend time talking about and selectingthe key business metrics to focus on. They should collect the data ona regular basis, the more real-time the better in my opinion, and theyshould publish the key business metrics to the entire team.

I do not believe it makes any sense to segment who gets to see whatbusiness metrics in a company. Sales metrics should be shared withdevelopment. Customer service metrics should be shared with finance.And so on and so forth.

Some companies buy big screens and mount them on the walls aroundthe office and publish the key business metrics on them so everyonecan see them. I like that approach. But I also like sending out a regular

1http://www.meetup.com/2http://twitter.com/3http://www.etsy.com

44B u s i n e s s , M e t r i c s a n dP r i c i n g

email to the entire company with the key business metrics and howthey are trending. And of course, I think these metrics should be sharedwith the Board and key investors.

When you publish financial projections (a topic for the coming weeks),you should include your projections or assumptions for key businessmetrics in the periods for which you are projection financial perform-ance. Many of these metrics will be drivers of your projections butthey are also helpful to establish the overall progress of the businessover time.

It is a good idea to evaluate what your company's key business metricsshould be from time to time. I like to suggest at least once a year,probably around the annual budgeting exercise (another topic for thecoming week). It is expected that you will change some of these metricsevery year as the business grows and develops. Don't just keep addingnew ones, you should also subtract old ones that don't seem as usefulanymore. Keep the total number of key business metrics you aretracking to a small enough number that most people on the teamcould recite them from memory. Less is more when it comes to keybusiness metrics.