Embed Size (px)

DESCRIPTION

Malayan Banking Berhad (Maybank) - Invest Malaysia 2010 Presentation

Citation preview

Invest Malaysia 2010 Dato’ Sri Abdul Wahid OmarPresident & CEO

Shangri-La Hotel, Kuala Lumpur30-31 March 2010

Maybank

Ridha WirakusumahPresident DirectorPresident DirectorPT Bank Internasional Indonesia Tbk

Introduction

L di b ki f hi i M l i ith k t l d hi l t

Recap from Invest Malaysia 2009:

Leading banking franchise in Malaysia with market leadership across almost all key business sectors.

Stronger footing after recent RM6 billion rights iss e hich has enabledStronger footing after recent RM6 billion rights issue which has enabled Maybank to maintain its credit rating, weather the current economic downturn, and capture growth opportunities.

Presence in key markets in the South East Asia and South Asia and is now strengthening its regional presence by capturing value from recent investments i.e. Bank Internasional Indonesia, MCB Bank and An Binh Bank.

Well positioned to capture growth opportunities and we have embarked on our Strategic Transformation Plan with the vision of becoming one of the top 5 banks in South and South East Asia by 2015.

2

Leading Banking Franchise

Stronger Financial Footing

St th i R i l PStrengthening Regional Presence

Strategy 2010 and beyond

3

Malaysia’s Leading Banking Franchise

Total assets: RM331 billionLargest market capitalisation of RM52 billion.

Largest bank in Malaysia

Largest branch network in Malaysia

386 branches, 2,800 ATMs, 9 million customers.

No.1 Internet banking with a dominant market share of 55%

Over 1,700 branches and offices in 14 countries.

16 million customers in the South East Asia region

Presence in key growth markets in South &South East Asia with GDP of 5.3% for 2011South East Asia

Strong credit rating,on par with sovereign

S&P : A-Fitch : A-

Moody’s: A3RAM: AAAon par with sovereign Fitch : A

Complete financial services provider

Extensive range of products and services covering Consumer, Corporate & SME, Islamic banking, Investment banking and Insurance.

RAM: AAA

p

Strong momentum in revenue and profitability.1H10 revenue grew 35.5% YoY, PATAMI rose 43.5% YoYMargins stable at 2 8% improving asset quality with Net NPL at 1 43%

Two strong quarters of performance for 1H10

Margins stable at 2.8%, improving asset quality with Net NPL at 1.43%.

4

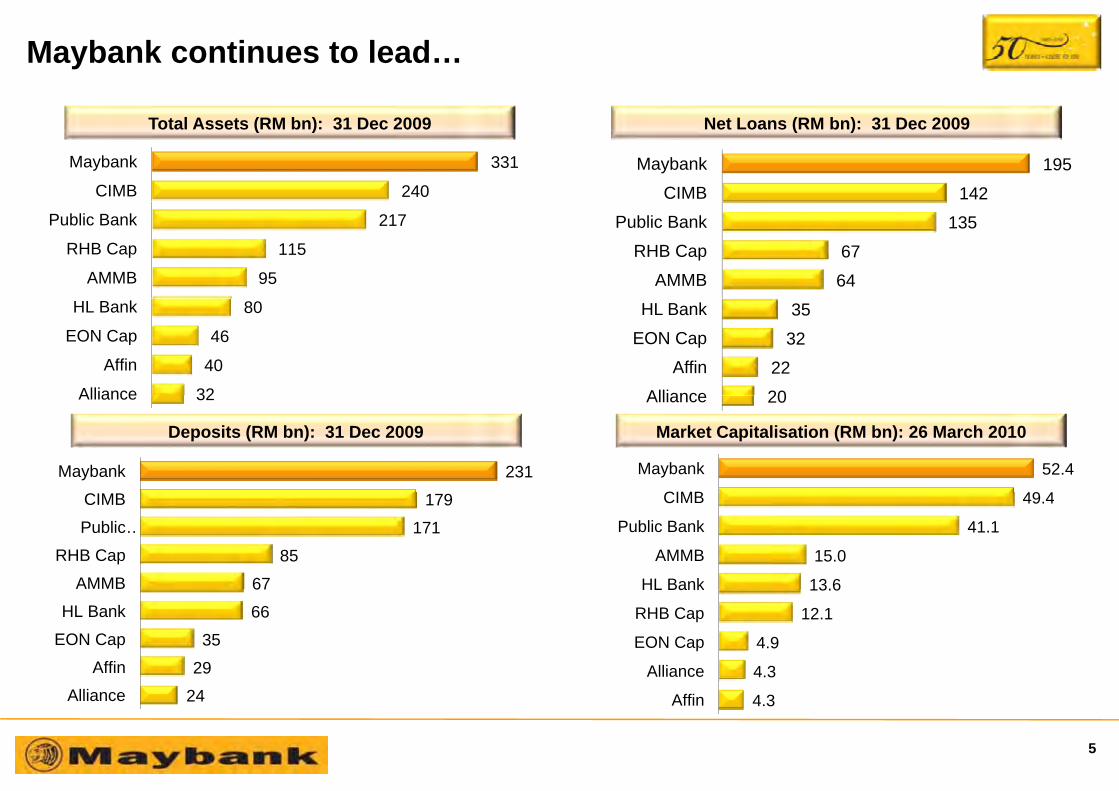

Maybank continues to lead…

240

331

CIMB

Maybank

Total Assets (RM bn): 31 Dec 2009 Net Loans (RM bn): 31 Dec 2009

142

195 CIMB

Maybank

95

115

217

AMMB

RHB Cap

Public Bank

64

67

135

AMMB

RHB Cap

Public Bank

32

40

46

80

Alliance

Affin

EON Cap

HL Bank

20

22

32

35

Alliance

Affin

EON Cap

HL Bank

32 Alliance

231Maybank

20 Alliance

Deposits (RM bn): 31 Dec 2009

49 4

52.4

CIMB

Maybank

Market Capitalisation (RM bn): 26 March 2010

67

85

171

179

AMMB

RHB Cap

Public …

CIMB

13.6

15.0

41.1

49.4

HL Bank

AMMB

Public Bank

CIMB

29

35

66

67

Affin

EON Cap

HL Bank

4.3

4.9

12.1

13.6

Alliance

EON Cap

RHB Cap

HL Bank

5

24Alliance 4.3Affin

Domestic Market: Leading market position in most sectors

Diversified across all financial products and services

Within the top 3 in almost all key business sectors

55%%)

Network Consumer Corporate Islamic Deposit Cards Insurance & Asset Mgmt

Investment Banking

30%

55%

Mar

ket S

hare

(%

New BusinessPremium

19%

30%

16%14%17% 17%17%

22% 24%21%

14%

27%21%23%

16%

29%

15%

8%

15%20%

10%14%

y n 8% 7%

anch

ATM

king

oans

oans

oans oan

oan

ance

cing

osits

osits

osits

osits

ASA

ase

ales

ance

M&A iting

ities

amily

eral

gmt

11 1 1 1

Indu

stry

Posi

tion

1 2 1 11 1

2 2 2 123 1 34 2 4

1 1

Bra A

Inte

rnet

Ban

k

Con

sum

er L

o

Hou

sing

Lo

Auto

Lo

Cor

pora

te L

SME

L

Trad

e Fi

na

Fina

nc

Dep

o

Fixe

d D

epo

Savi

ng D

epo

Dem

and

Dep

o CA

Cre

dit C

ard

B

Mer

chan

t Sa

Deb

t Iss

ua M

Und

erw

ri

Equi

Life

/Fa

ombi

ned

Gen

Asse

t Und

er M

D Co A* As at Dec 2009, except for Insurance & Asset Mgt (Sep 09)

6

Leading Banking Franchise

Stronger Financial Footing

St th i R i l PStrengthening Regional Presence

Strategy 2010 and beyond

7

Strong Performance in 1H 2010

RM

Net Income grew 35% YoY PATAMI grew 44% YoY

1875.3RM

million7,500

21.3%6408.2 Net

Income: +35%

1,5001306.72,360.1

5,000

YoY

54.1%YoY

4729.9 Non-InterestIncome: +78%

1,000590.3

737.5

832 21,142.0 1,218.1

1,327.2

2,500 2045 2

2684.7

3151.1 3257.1 Islamic BankingIncome: +25%

500

265.

0

1,54

7.4

1,62

7.6

1,68

3.1

2,81

2.4

3,31

0.7

285.2 305.1 381.6 355.9 495.0

832.2 2045.2Net-InterestIncome: +18%

01H 09 1H 10

1, 1 1 1

01Q09 2Q09 1Q10 2Q10 1H09 1H10

8

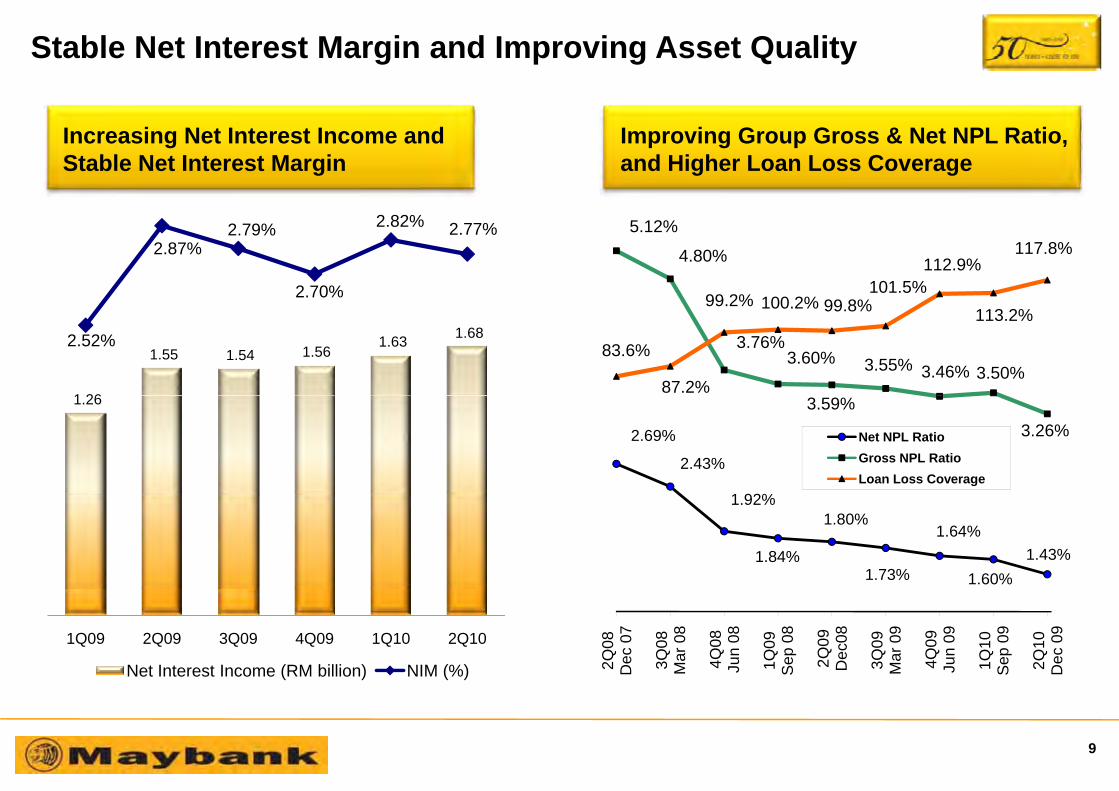

Stable Net Interest Margin and Improving Asset Quality

Improving Group Gross & Net NPL Ratio, and Higher Loan Loss Coverage

Increasing Net Interest Income and Stable Net Interest Margin

2.87%2.79%

2.70%

2.82% 2.77% 5.12%

4.80%

99 2% 100 2%101.5%

112.9%117.8%

1 26

1.55 1.54 1.56 1.63 1.68 2.52% 3.76%

3.60% 3.55% 3.46% 3.50%83.6%

87.2%

99.2% 100.2% 99.8% 113.2%

1.26

2.69%

2.43%

3.59%3.26%Net NPL Ratio

Gross NPL Ratio Loan Loss Coverage

1.92%

1.84%

1.80%

1.73%

1.64%

1.60%1.43%

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

Net Interest Income (RM billion) NIM (%) 2Q08

Dec

07

3Q08

Mar

08

4Q08

Jun

08

1Q09

Sep

08

2Q09

Dec

08

3Q09

Mar

09

4Q09

Jun

09

1Q10

Sep

09

2Q10

Dec

09

9

Robust loans growth in key business segments particularly in the consumer segment

Robust loans and business growth

800Maybank Industry *

Housing Loan Growth Cards Growth 1H FY10 YoY

Market share: 14%

Robust loans growth in key business segments, particularly in the consumer segment

400

600

RM

mill

ion Maybank Industry

Card base 4.4% - 0.2%

Billings 12.2% 6.9%

% %

Market share: 14%

0

200

2Q09 3Q09 4Q09 1Q10 2Q10

Receivables 8.3% 5.3%

Merchant Sales 23.9% 4.9%

* Industry figures for cards includes commercial banks and non FI players2Q09 3Q09 4Q09 1Q10 2Q10

800

commercial banks and non-FI players

Auto Loan Growth Corporate & Business Loans Growth

Market share: 17%

400

600

RM

mill

ion

STRC

Trade bills

Dec 09

Total Loans grew 5.6% annualised

0

200

2Q09 3Q09 4Q09 1Q10 2Q10

Term Loans

OD June 09

RM 2Q09 3Q09 4Q09 1Q10 2Q10 0 20 40 billion

10

Leading Banking Franchise

St th i R i l P

Stronger Financial Footing

Strengthening Regional Presence

Strategy 2010 and beyond

11

Our International PresenceOther Markets

China Papua New Guinea BruneiBahrain Pakistan

Other Markets

An Binh Bank(91 branches). To increase branches to

Treasury Centres

TreasuryCentresGrowth in selected assets

New York Vietnam (2 branches) Exploring to open 1 additional

increase branches to 150

Hong Kong

assets and Treasury activities

Londonbranch.

ASEAN Cambodia(7 branches) To(7 branches). To increase branches to 11 by FY2011

BII (250 branches). To add 200 branches by 2011 & Double ATMs to 1,500 by 2011.Possible conversion of Bank MaybankIndocorp into Syariah Bank

Singapore (22 branches) to focus on building strength in key products such as Auto & Housing LoanFor Corporate/SMEs, to selectively grow customer base

Philippines(45 branches).Further expansion of operations in Philippines

12

Indocorp into Syariah Bankgrow customer base

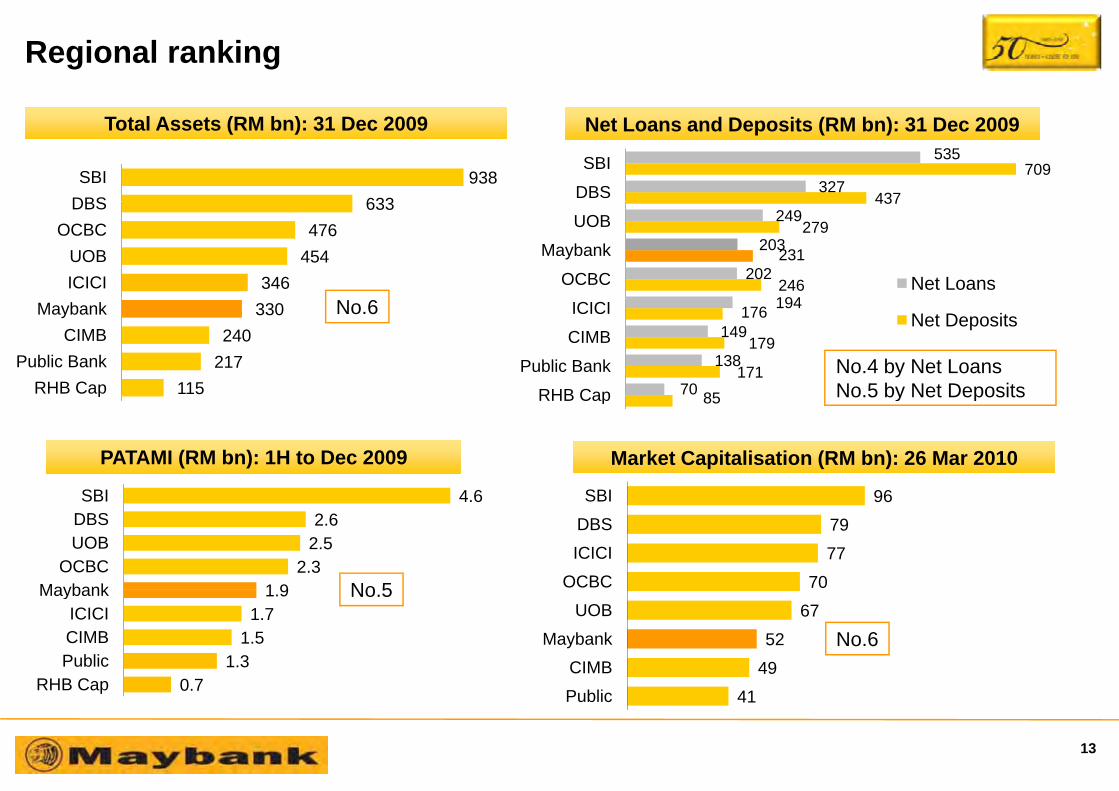

Regional ranking

Total Assets (RM bn): 31 Dec 2009 Net Loans and Deposits (RM bn): 31 Dec 2009

633938

DBSSBI

437

709327

535

DBS

SBI

346 454 476

633

ICICIUOB

OCBCDBS

246

231

279

437

194

202

203

249

OCBC

Maybank

UOB

Net Loans

115 217 240

330

RHB CapPublic Bank

CIMBMaybank

85171

179

176

70

138

149

194

RHB Cap

Public Bank

CIMB

ICICINet DepositsNo.6

No.4 by Net LoansNo.5 by Net Deposits

PATAMI (RM bn): 1H to Dec 2009

96SBI

Market Capitalisation (RM bn): 26 Mar 2010

p

4 6SBI

85RHB Cap No.5 by Net Deposits

707779

96

OCBCICICIDBSSBI

1 92.3

2.52.6

4.6

MaybankOCBC

UOBDBSSBI

No 5

4952

67

CIMBMaybank

UOB

0 71.3

1.51.7

1.9

RHB CapPublicCIMBICICI

Maybank No.5

No.6

41Public0.7RHB Cap

13

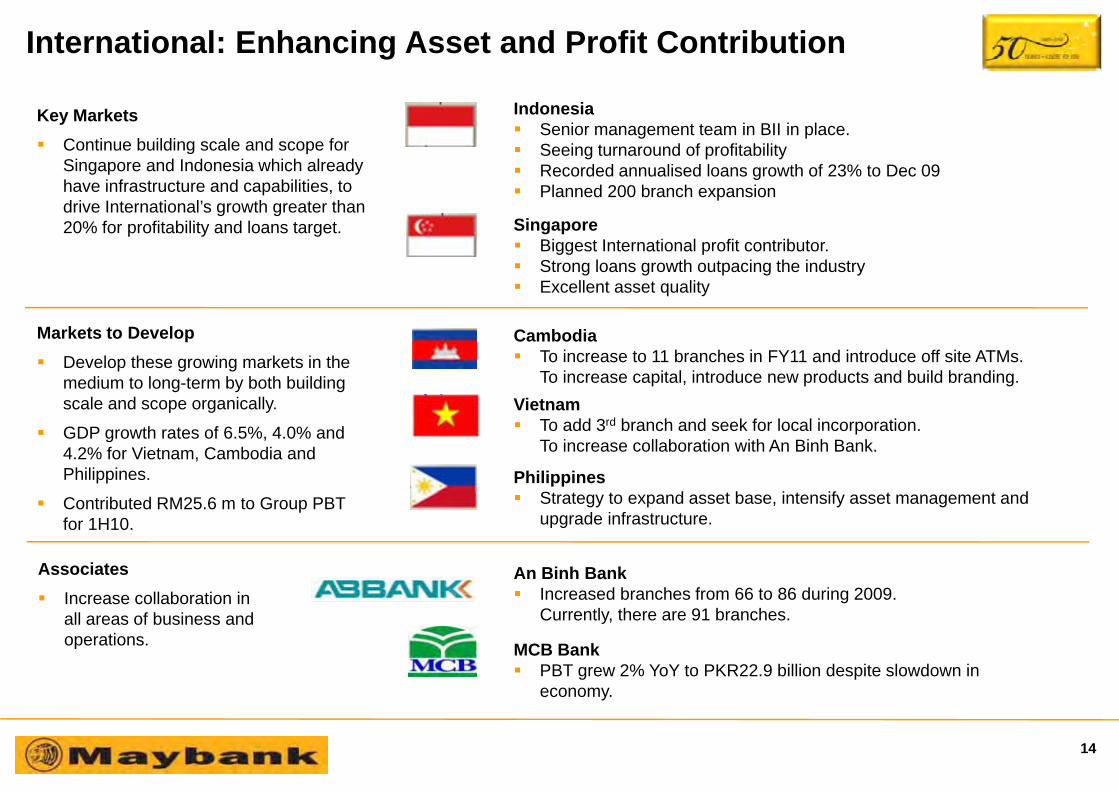

International: Enhancing Asset and Profit Contribution

I d iKey MarketsContinue building scale and scope for Singapore and Indonesia which already have infrastructure and capabilities, to d i I t ti l’ th t th

IndonesiaSenior management team in BII in place.Seeing turnaround of profitabilityRecorded annualised loans growth of 23% to Dec 09Planned 200 branch expansion

drive International’s growth greater than 20% for profitability and loans target. Singapore

Biggest International profit contributor.Strong loans growth outpacing the industryExcellent asset quality

Markets to DevelopDevelop these growing markets in the medium to long-term by both building

CambodiaTo increase to 11 branches in FY11 and introduce off site ATMs.To increase capital, introduce new products and build branding.

scale and scope organically.

GDP growth rates of 6.5%, 4.0% and 4.2% for Vietnam, Cambodia and Philippines.

VietnamTo add 3rd branch and seek for local incorporation.To increase collaboration with An Binh Bank.

PhilippinesSt t t d t b i t if t t d

Associates

Contributed RM25.6 m to Group PBT for 1H10.

Strategy to expand asset base, intensify asset management and upgrade infrastructure.

An Binh BankI d b h f 66 t 86 d i 2009Increase collaboration in

all areas of business and operations.

Increased branches from 66 to 86 during 2009. Currently, there are 91 branches.

MCB BankPBT grew 2% YoY to PKR22.9 billion despite slowdown in economy.

14

International: Assets and profits contribution

International targeted to contribute 40% of loans and profits by 2015

As at 31 December 2009 1H 10

14.611.1

759

Others: 5%Indonesia: 7%

atio

nal

3%

Singapore: 15%Indonesia: 5%Oth 7%

Loans(RM b)

PBT(RM m)

natio

nal

27%

41.6

103 175

Singapore: 21%

Inte

rna

33

InvestmentInsurance: 6%

Others: 7%

Inte

r 2

69.0 688 Business &Corporate: 34% Global

Markets: 24%

InvestmentBanking: 4%

c stic

%

464 Business &Corporate: 16%D

omes

tic67

%

Dom

es73

%

66.7665

Consumer: 33%Consumer: 23%

15

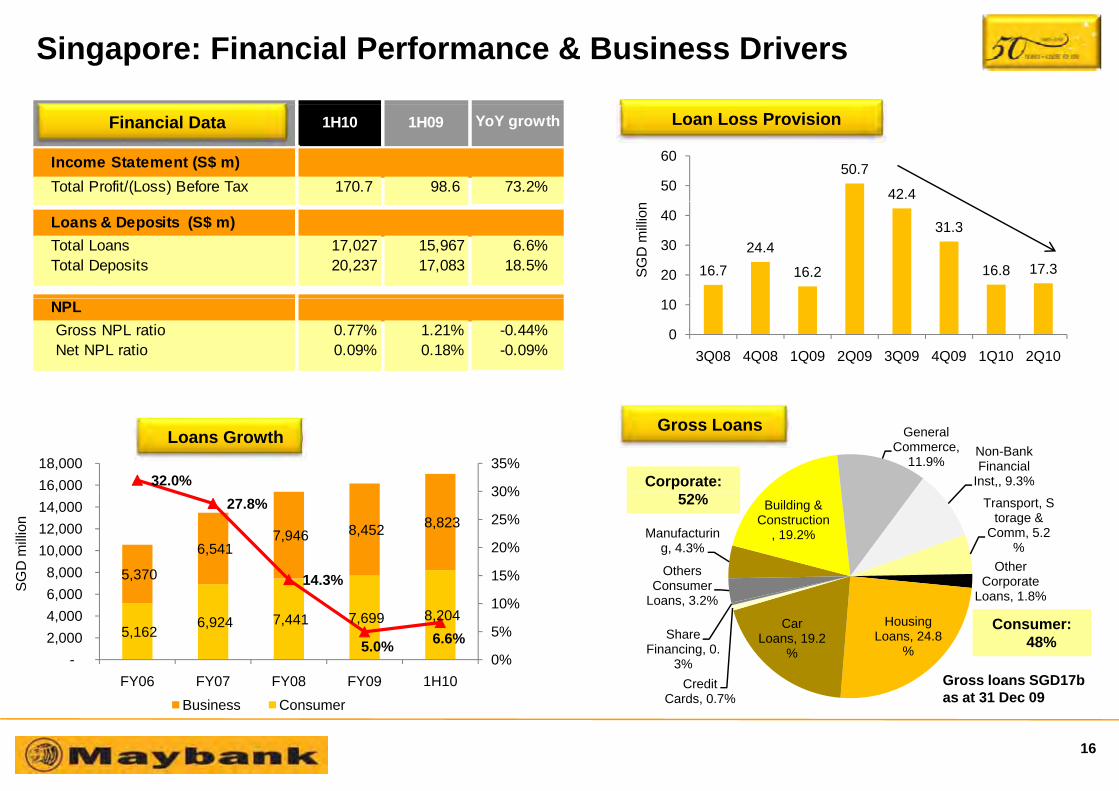

Singapore: Financial Performance & Business Drivers

50.7

42.450

60

1H10 1H09

Income Statement (S$ m)Total Profit/(Loss) Before Tax 170.7 98.6 73.2%

YoY growth Loan Loss ProvisionFinancial Data

16.724.4

16.2

31.3

16.8 17.320

30

40

SG

D m

illio

n

Loans & Deposits (S$ m)Total Loans 17,027 15,967 6.6%Total Deposits 20,237 17,083 18.5%

0

10

3Q08 4Q08 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10

NPLGross NPL ratio 0.77% 1.21% -0.44%Net NPL ratio 0.09% 0.18% -0.09%

General Commerce,

11.9%Non-Bank Financial

Inst,, 9.3%Corporate:

Gross LoansLoans Growth

32.0%30%

35%16,000 18,000

Manufacturing, 4.3%

Building & Construction

, 19.2%

Transport, Storage &

Comm, 5.2%

Other Corporate

Others Consumer

52%

5,370

6,541 7,946 8,452 8,823

27.8%

14.3% 15%

20%

25%

30%

6 0008,000

10,000 12,000 14,000

SG

D m

illio

n

Loans, 1.8%

Housing Loans, 24.8

%

Car Loans, 19.2

%

Credit

Share Financing, 0.

3%

Consumer Loans, 3.2%

Consumer:48%

Gross loans SGD17b

5,162 6,924 7,441 7,699 8,204

5.0% 6.6%0%

5%

10%

-2,000 4,000 6,000

FY06 FY07 FY08 FY09 1H10

S

Credit Cards, 0.7% as at 31 Dec 09

06 0 08 09 0Business Consumer

16

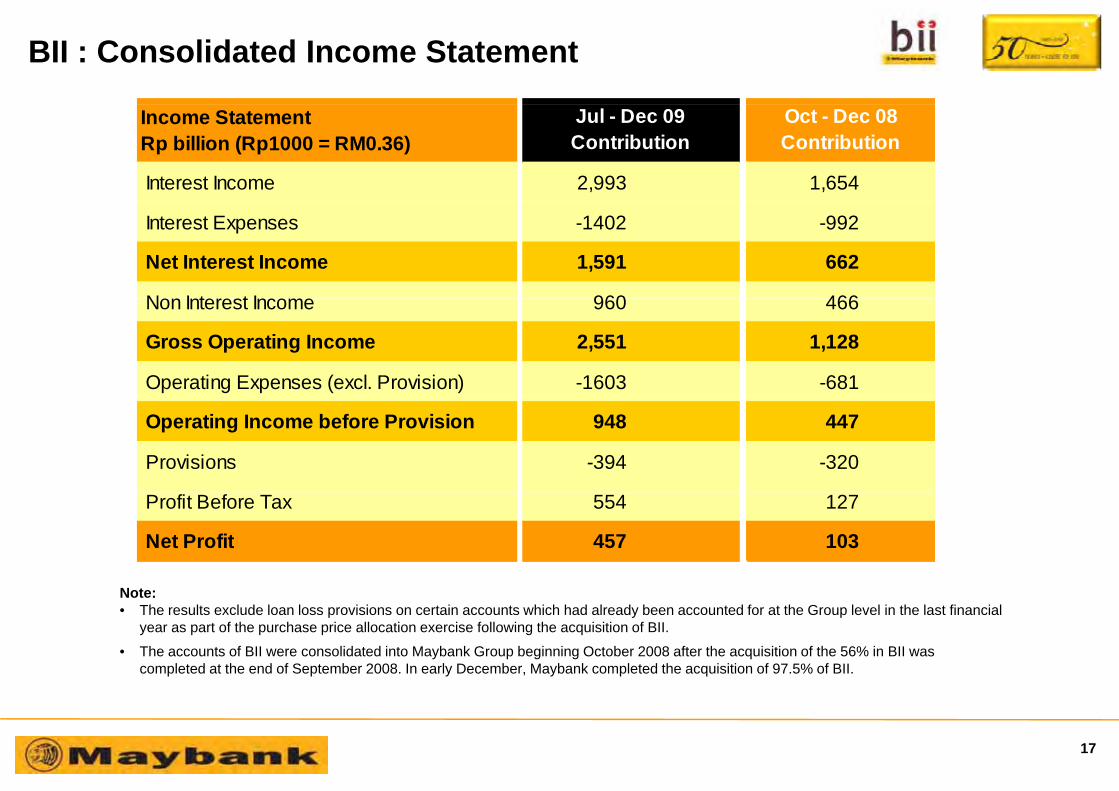

BII : Consolidated Income Statement

Income StatementRp billion (Rp1000 = RM0.36)

Interest Income 2,993 1,654

Jul - Dec 09Contribution

Oct - Dec 08Contribution

Interest Expenses -1402 -992

Net Interest Income 1,591 662

N I t t I 960 466 Non Interest Income 960 466

Gross Operating Income 2,551 1,128

Operating Expenses (excl. Provision) -1603 -681

Operating Income before Provision 948 447

Provisions -394 -320

Profit Before Tax 554 127

Net Profit 457 103

N tNote:• The results exclude loan loss provisions on certain accounts which had already been accounted for at the Group level in the last financial

year as part of the purchase price allocation exercise following the acquisition of BII.

• The accounts of BII were consolidated into Maybank Group beginning October 2008 after the acquisition of the 56% in BII was completed at the end of September 2008. In early December, Maybank completed the acquisition of 97.5% of BII.

17

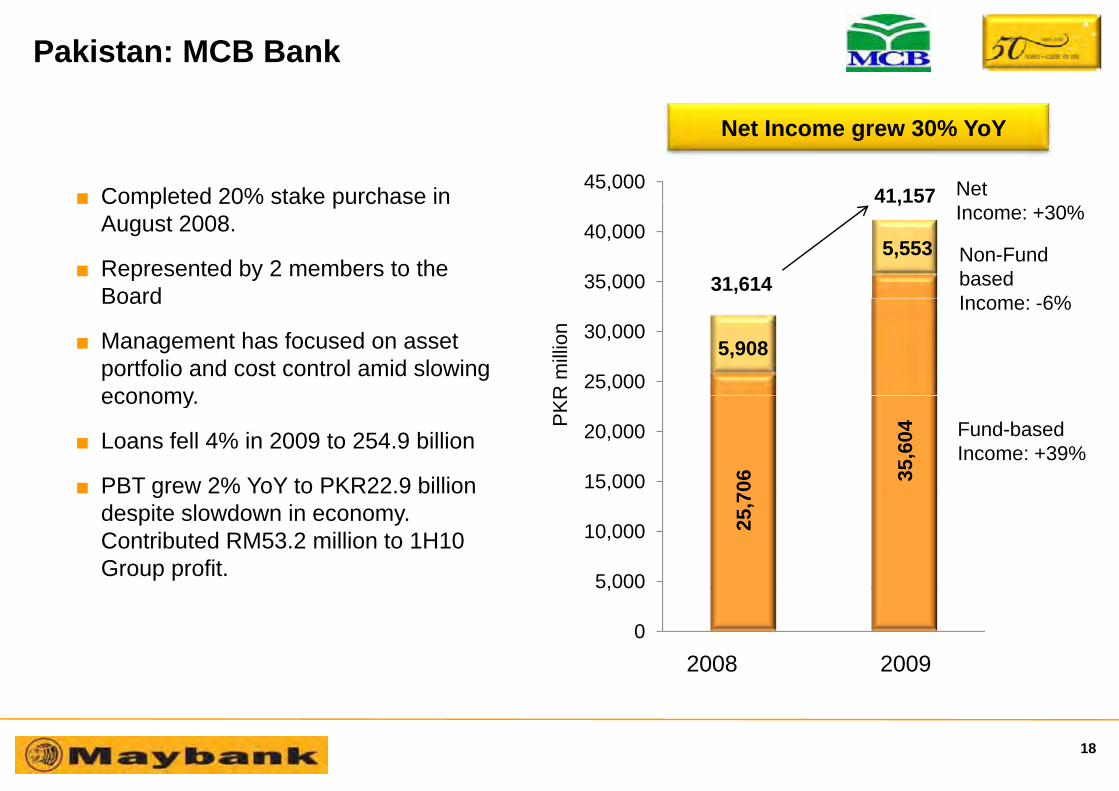

Pakistan: MCB Bank

■ Completed 20% stake purchase in45,000

41,157 Net

Net Income grew 30% YoY

■ Completed 20% stake purchase in August 2008.

■ Represented by 2 members to the Board

5,553 35,000

40,000

31,614

41,157

Non-FundbasedI 6%

Income: +30%

Board

■ Management has focused on asset portfolio and cost control amid slowing economy

5,908 25,000

30,000Income: -6%

R m

illio

n

economy.

■ Loans fell 4% in 2009 to 254.9 billion

■ PBT grew 2% YoY to PKR22.9 billion 06 35,6

04

15,000

20,000 Fund-basedIncome: +39%

PK

R

■ PBT grew 2% YoY to PKR22.9 billion despite slowdown in economy. Contributed RM53.2 million to 1H10 Group profit.

25,7

5,000

10,000

0

,

2008 20092008 2009

18

Vietnam: An Binh Bank

■ Completed initial 15% stake in Sept 2008 and additional 5% stake in Dec 2009.

■ Appointed 1 member to the Supervisory900 Net

Net Income grew 166% YoY

■ Appointed 1 member to the Supervisory Committee and 1 to Board of Directors.

■ Seconded a Chief Risk Officer 87.9 700

800778.2

Non-FundbasedI +304%

Income: +166%

■ Increased branches from 66 to 86 during 2009. Currently, there are 91 branches.

■ Business cooperation in the areas of 500

600Income: +304%

D m

illio

n

Consumer banking (credit cards, remittances), trade finance, sharing risk management framework 69

0.3

21 8300

400292.6

Fund-basedIncome: +155%

VN

D

■ Improving economic sentiment in the country even as VND faces devaluation pressure.

L 93% VND12 6 billi

270.

8

21.8

100

200

■ Loans grew 93% to VND12.6 billion.

■ PBT grew 535% in 2009 to VND415.5 m. Contributed RM4.5 million to 1H10 Group

fit

01H 09 1H 102008 2009

profit.

19

Bank Internasional Indonesia (BII)

20

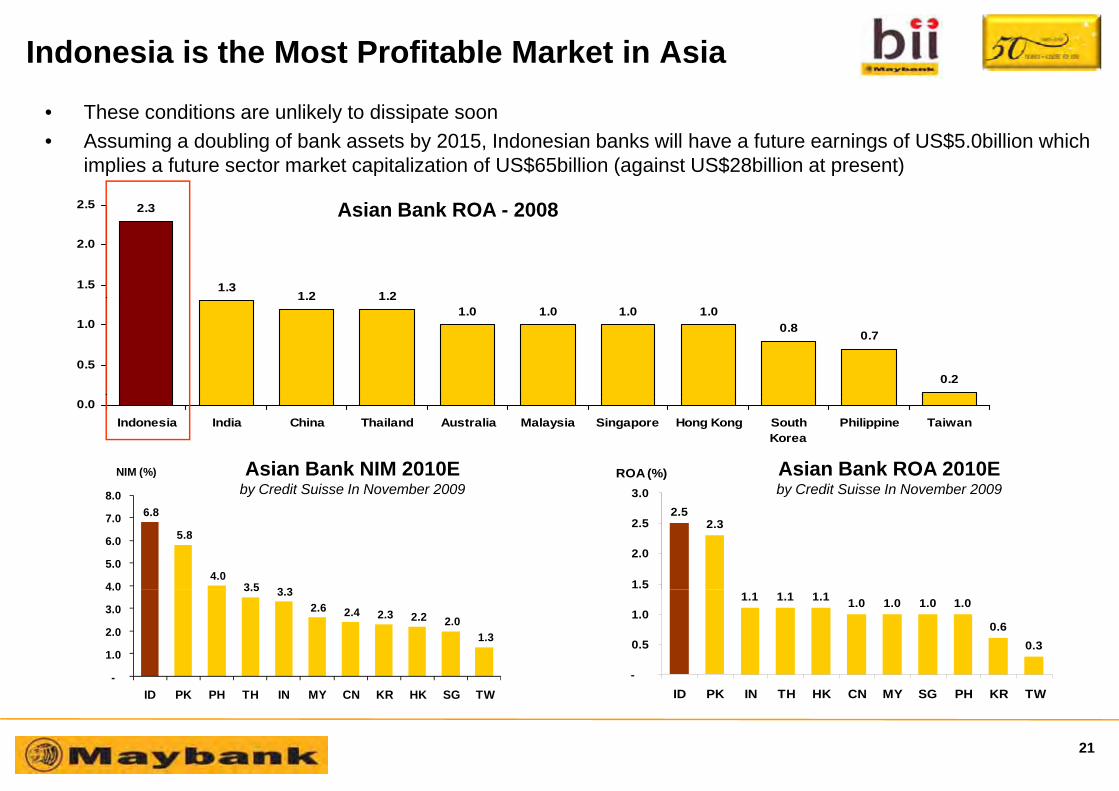

Indonesia is the Most Profitable Market in Asia

Th diti lik l t di i t

2 5

• These conditions are unlikely to dissipate soon• Assuming a doubling of bank assets by 2015, Indonesian banks will have a future earnings of US$5.0billion which

implies a future sector market capitalization of US$65billion (against US$28billion at present)

2.3

1.31.2 1.2

1.5

2.0

2.5 Asian Bank ROA - 2008

1.2 1.21.0 1.0 1.0 1.0

0.8 0.7

0.20.5

1.0

0.0Indonesia India China Thailand Australia Malaysia Singapore Hong Kong South

KoreaPhilippine Taiwan

3 0ROA (%)

8 0

NIM (%) Asian Bank NIM 2010Eby Credit Suisse In November 2009

Asian Bank ROA 2010Eby Credit Suisse In November 2009

2.52.3

1.5

2.0

2.5

3.06.8

5.8

4.0 3 5 3 34.0

5.0

6.0

7.0

8.0 by Credit Suisse In November 2009 by Credit Suisse In November 2009

1.1 1.1 1.0 1.0 1.0

0.60.3

1.1 1.0

-

0.5

1.0

3.5 3.3 2.6 2.4 2.3 2.2 2.0

1.3

-

1.0

2.0

3.0

4.0

21

ID PK IN TH HK CN MY SG PH KR TWID PK PH TH IN MY CN KR HK SG TW

Our Aspirations

5 x 5 x 5

T 5 B k bTop 5 Banks by Assets & Returns

Leading in 5 Areas

By 2015

In line with Maybank’s aspiration to be One of SEA & South Asia Top 5 Banks by 2015

22

Rationale to be in the areas we choose (1/2)

1. Leading banker for transportation industry• One of the banks that own motorcycle financing companies, both 2 wheelers and 4 wheelers• One of the banks that lend to shipping industry• Have a good base for airline business by partnering with Lion Air

2. USD Payment Bank• BII has a strong customer base with USD transactions• BII has a strong USD funding, with a composition FCY funding 26% compared to average industry of 17%• 65% of the FCY funding is in CASA (while industry average is 51%), indicating the heavy usage for

transactionsBII i th l ti l i USD t ti d ll k f• BII is the long time player in USD transactions and well known of :

• Offering competitive FX rate amongst other peer banks• Having flexibility to accept USD notes with substandard conditions while other banks would not

acceptaccept

3. SME/Commercial: No. 1 in Supply Chain Financing• Multiplier effect, i.e. end to end financial solution start collection to payment in each flow of business

creationcreation • Powerful cross sell engine, i.e. funding, lending and transaction • Unique positioning, with limited competition and relatively low risk• Economic of scale and time to market

23

Rationale to be in the areas we choose (2/2)

4. Corporate: No. 1 in Structured Trade Financing & Resource Based Industry• Lucrative business given limited players in the market, very structured (minimize credit risk), short tenor

and self liquidatingand self liquidating • Indonesia is a resource based (commodity) country, be it soft (sugar, rice, coffee, etc) and hard

(coal, tin, iron, oil n gas, etc) commodities. Normally in sourcing and transporting these commodities are not straight forward given limited working capital; and we are as bank sees this opportunity to finance this g g g p pp ybusiness and to move the products either locally or globally

5. No. 1 in Credit Card

• High margin business and provide entrance to other cross selling opportunities for deepening relationship• High margin business and provide entrance to other cross selling opportunities for deepening relationship • Card represent consumer lifestyle and behavior. Being number 1 in cards means most consumers /

population will use Bii credit card and Bii is on top of everyone's mind• By having credit card customer, it is a lifetime relationship as it is an open ended product y g , p p p

24

Leverage Synergy Opportunities With Maybank

Nascent syariah banking operations 5 branches, USD35 million loansDefine business model and alignment with Bank Maybank Indocorp

Syariah Banking

I t tReplicate Maybank-IB in Indonesia

Investment Banking

Create a program to allow Singapore accounts to be opened Maybank

NIA

GA

Maybank

p g g p pfrom Jakarta (Priority and Private banking)Singapore domiciled companies belonging to Indonesians

Corporate

Maybank Singapore

CIM

B-NMaybank Continue existing cross referrals of customers

Corporatebanking

Increasing trade business between Malaysia and IndonesiaN d t d f t d d t t f iliti

TradeNeed to ensure adequacy of trade and counterparty facilities

InsuranceSignificant potential to captureImprove bancassurance relationships

OthersAlign development of BII’s future IT architecture with MaybankInternet bankingSh i f t l t i l t d i l l d

p p

Sharing of talent as a regional expert and regional program leader

25

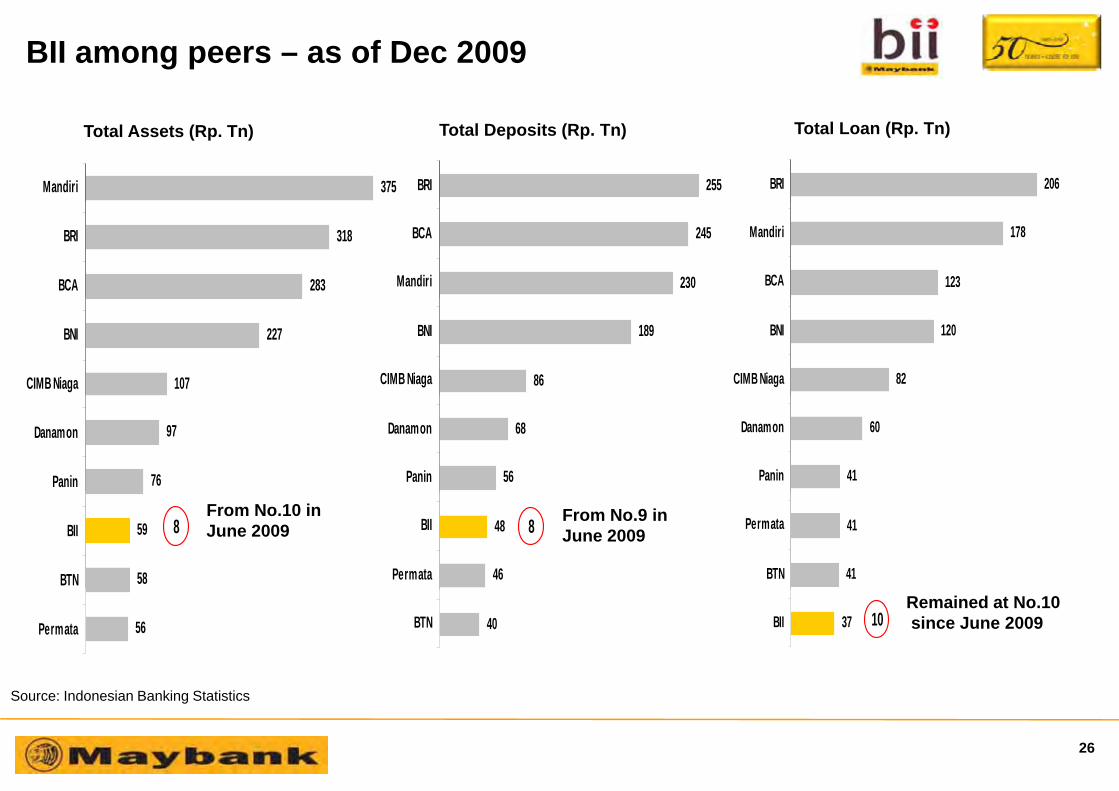

BII among peers – as of Dec 2009

375Mandiri 255BRI 206BRI

Total Assets (Rp. Tn) Total Deposits (Rp. Tn) Total Loan (Rp. Tn)

283

318

BCA

BRI

230

245

Mandiri

BCA

123

178

BCA

Mandiri

107

227

CIMB Niaga

BNI

86

189

CIMB Niaga

BNI

82

120

CIMB Niaga

BNI

76

97

Panin

Danamon

56

68

Panin

Danamon

41

60

Panin

Danamon

58

59

BTN

BII 8

46

48

Permata

BII 8

41

41

BTN

PermataFrom No.10 inJune 2009

From No.9 inJune 2009

56Permata 40BTN 37BII 10Remained at No.10since June 2009

Source: Indonesian Banking Statistics

26

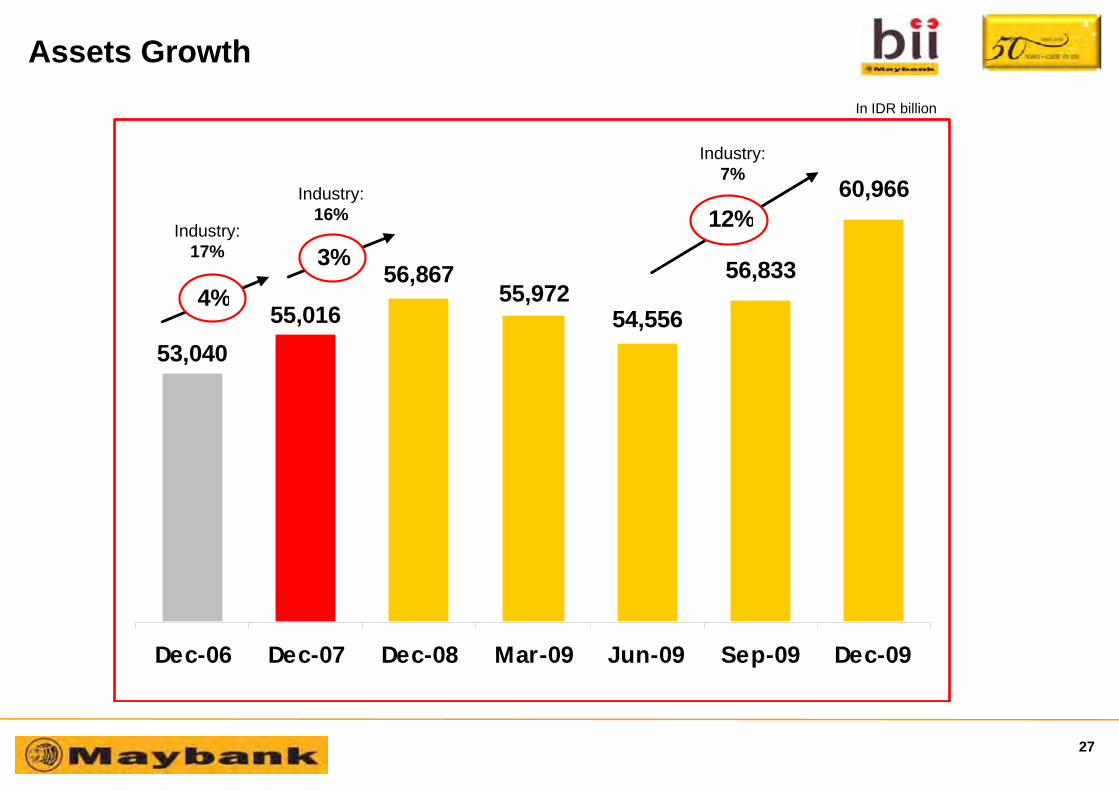

Assets Growth I IDR billi

60,966Industry:

Industry:7%

In IDR billion

56,83355,972

56,8674%

3%12%Industry:

17%

y16%

54,55655,972

55,01653,040

4%

Dec-06 Dec-07 Dec-08 Mar-09 Jun-09 Sep-09 Dec-09

27

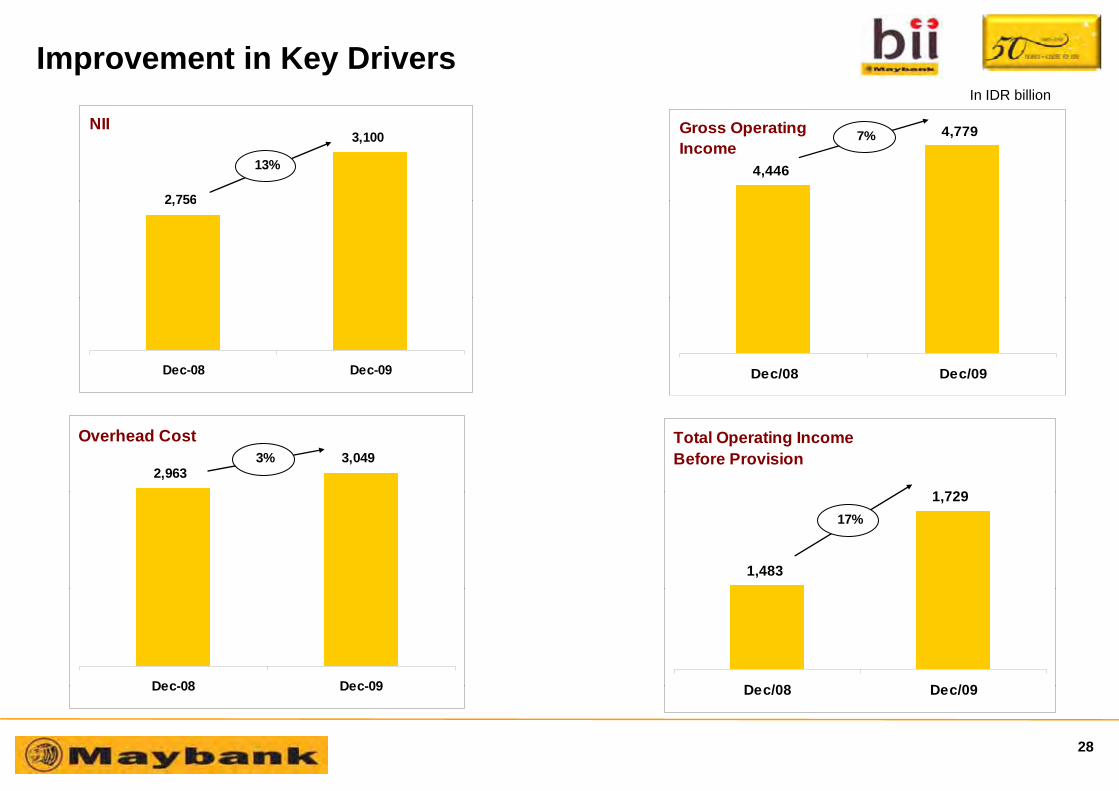

Improvement in Key DriversIn IDR billion

2 756

3,100

13%

NII

4,446

4,7797%Gross Operating Income

2,756

Dec-08 Dec-09 Dec/08 Dec/09

2,9633,049

Overhead Cost3%

1 729

Total Operating Income Before Provision

1,483

1,72917%

Dec-08 Dec-09 D /08 D /09Dec-08 Dec-09 Dec/08 Dec/09

28

WOM: Improvement in Risk Area

P i i ( thl ) f WOM tf li All the work is paying off at the bottom line

Monthly Profit (Net Profit, Rp. billion)

Provision expense (monthly) for WOM portfolio in BII(Rp. Billion)

8 23 8 16 8.54

10.17

8 37

9.9876

8.23 8.16

5.79

8.3765

5856

51

1.21 1.04

3.04

1.16

4045

3531 29

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

15

29

23

-5.02Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09

29

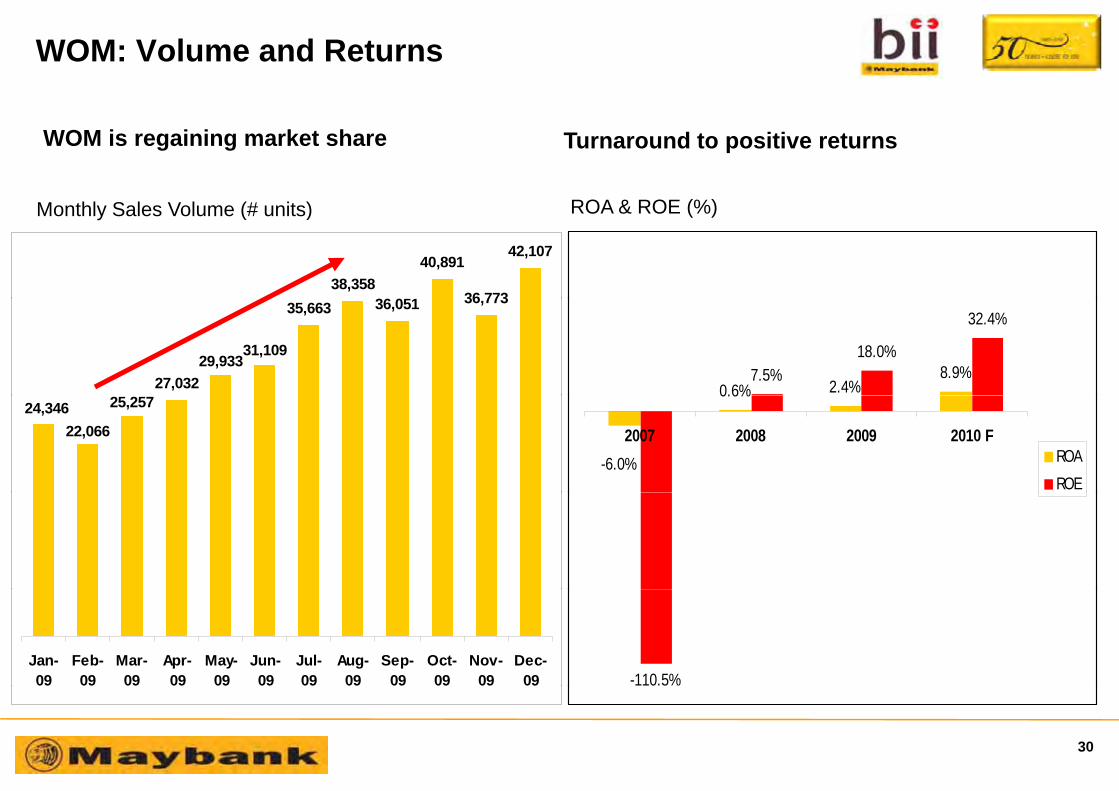

WOM: Volume and Returns

Turnaround to positive returnsWOM is regaining market share

M hl S l V l (# i ) ROA & ROE (%)

38,35836 051

40,891

36 773

42,107

Monthly Sales Volume (# units) ROA & ROE (%)

27,032

35,663 36,051 36,773

29,93331,109

0.6% 2.4%8.9%7.5%

18.0%

32.4%

25,25724,34622,066

0.6%

-6.0%

2007 2008 2009 2010 FROAROE

Jan-09

Feb-09

Mar-09

Apr-09

May-09

Jun-09

Jul-09

Aug-09

Sep-09

Oct-09

Nov-09

Dec-09 -110.5%

30

Summary and Prospects

Indonesian macroeconomic outlook is positive on the back of infrastructure development, recovery in consumer spending, domestic investment and FDI, as well as stable IDRas stab e

2009 was a year of consolidation in Bii, 2010-11 will be concentration on strengthening the infrastructure (IT and network) in order to build a sustainable g g ( )foundation for exceptional growth and in order to compete effectively in an ever tightening market

One of two top ten banks that has dedicated two wheelers subsidiary. Our prospect is to strengthen this and to expand it into a full fledge consumer financing business

Leverage our subsidiaries and increase cross-sell

Continue to maintain and strengthen our service differentiationg

Develop winning businesses in key areas and utilize synergy with Maybank to the fullest

31

Leading Banking Franchise

Stronger Financial Footing

St th i R i l PStrengthening Regional Presence

Strategy 2010 and beyond

32

Strategy 2010 and beyond

Focus on 3 key business pillars:y p

Community Financial Services

Wholesale BankingWholesale Banking

Insurance & Takaful

Supported by strong Enterprise Transformation Services,covering Operations and IT

33

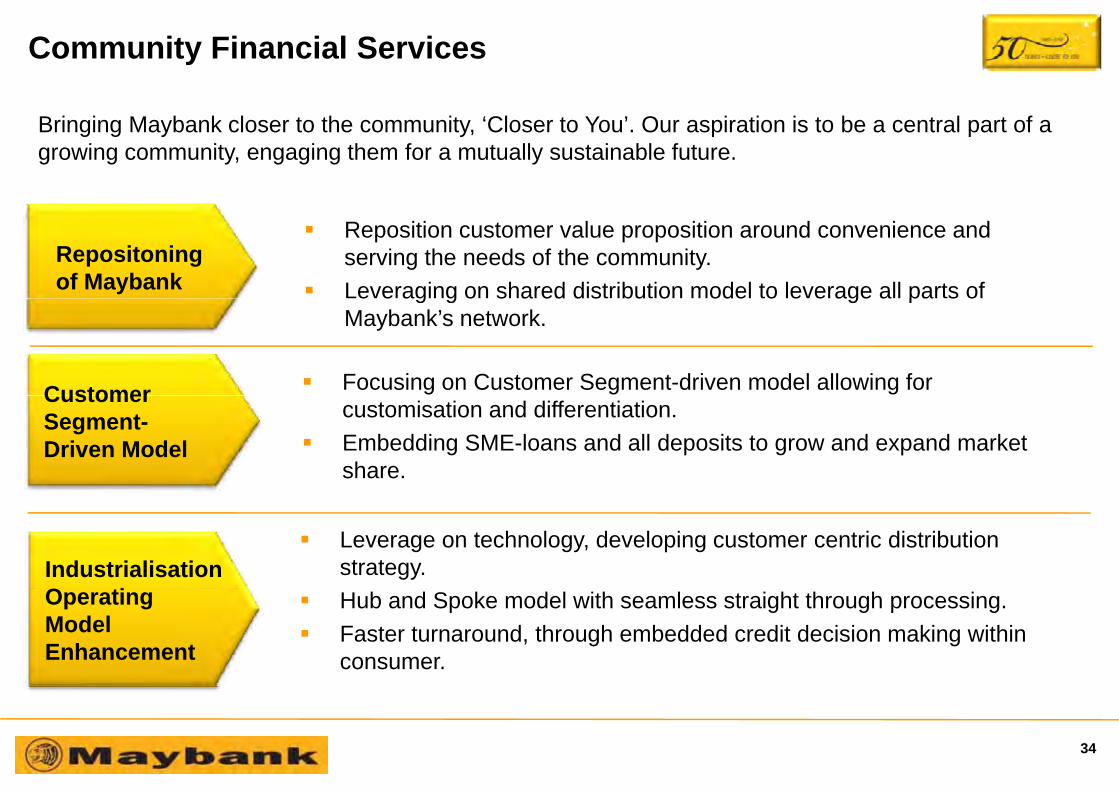

Community Financial Services

Bringing Maybank closer to the community, ‘Closer to You’. Our aspiration is to be a central part of a growing community, engaging them for a mutually sustainable future.

Reposition customer value proposition around convenience and serving the needs of the community.Leveraging on shared distribution model to leverage all parts of

Repositoningof Maybank

Focusing on Customer Segment-driven model allowing for

e e ag g o s a ed d s bu o ode o e e age a pa s oMaybank’s network.

Customercustomisation and differentiation.Embedding SME-loans and all deposits to grow and expand market share.

Customer Segment-Driven Model

Leverage on technology, developing customer centric distribution strategy.Industrialisation

O ti Hub and Spoke model with seamless straight through processing.Faster turnaround, through embedded credit decision making within consumer.

Operating ModelEnhancement

34

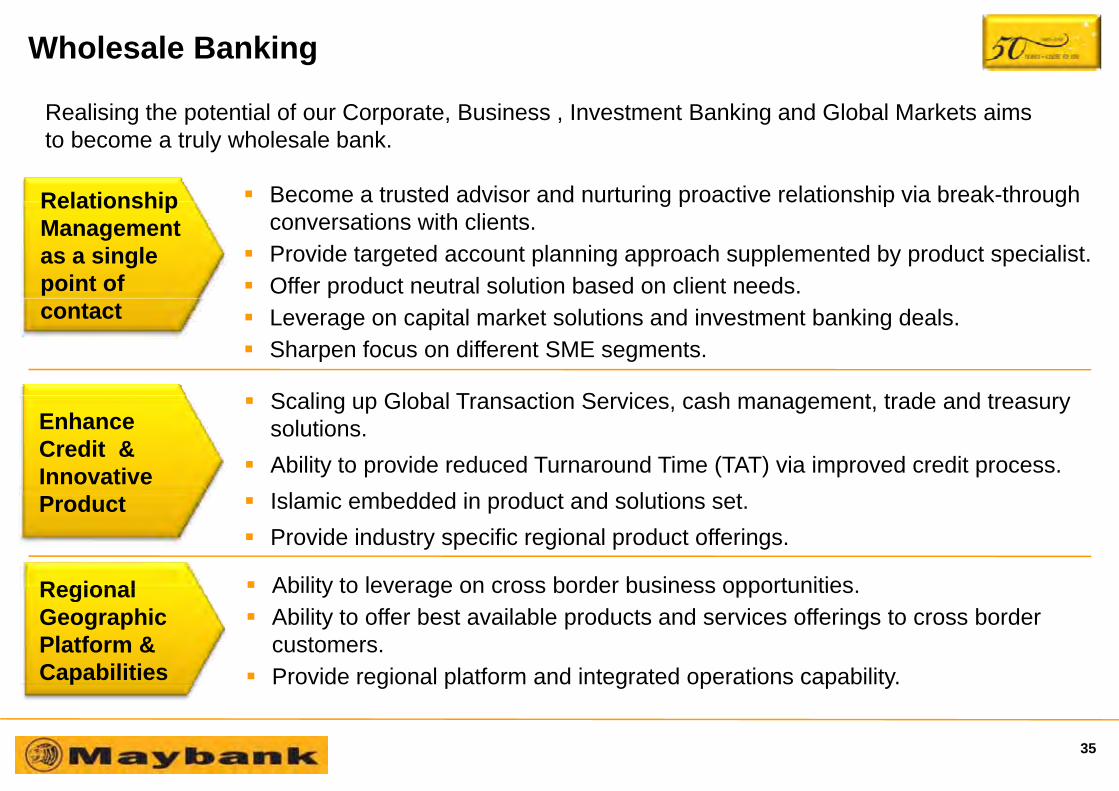

Wholesale BankingEnhanceCredit & Innovative ProductR li i th t ti l f C t B i I t t B ki d Gl b l M k t i

Become a trusted advisor and nurturing proactive relationship via break-through

ProductRealising the potential of our Corporate, Business , Investment Banking and Global Markets aims to become a truly wholesale bank.

Relationship Become a trusted advisor and nurturing proactive relationship via break through conversations with clients.Provide targeted account planning approach supplemented by product specialist.Offer product neutral solution based on client needs.

RelationshipManagement as a single point of

Leverage on capital market solutions and investment banking deals.Sharpen focus on different SME segments.

S li Gl b l T ti S i h t t d d t

contact

Scaling up Global Transaction Services, cash management, trade and treasury solutions. Ability to provide reduced Turnaround Time (TAT) via improved credit process.I l i b dd d i d d l i

EnhanceCredit & Innovative

Ability to leverage on cross border business opportunities

Islamic embedded in product and solutions set.Provide industry specific regional product offerings.

Product

Regional Ability to leverage on cross border business opportunities.Ability to offer best available products and services offerings to cross border customers.Provide regional platform and integrated operations capability.

RegionalGeographic Platform &Capabilities g p g p p y

35

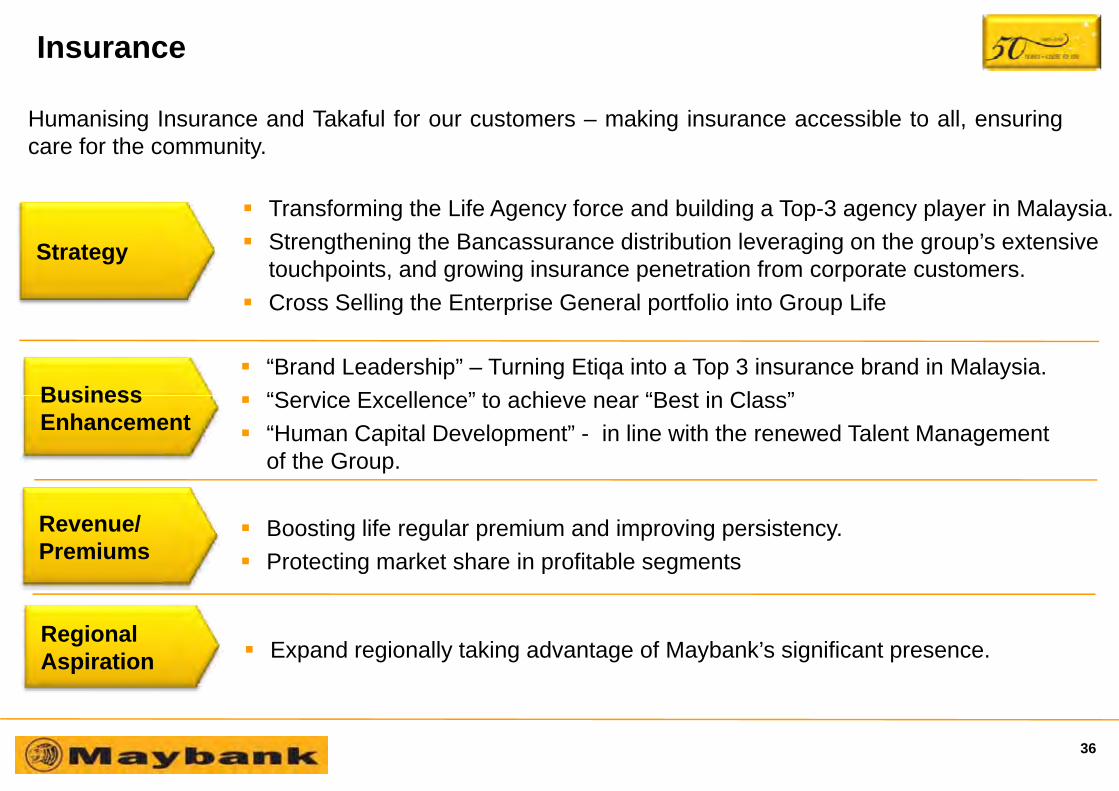

Insurance

T f i th Lif A f d b ildi T 3 l i M l i

Humanising Insurance and Takaful for our customers – making insurance accessible to all, ensuringcare for the community.

Transforming the Life Agency force and building a Top-3 agency player in Malaysia.Strengthening the Bancassurance distribution leveraging on the group’s extensive touchpoints, and growing insurance penetration from corporate customers.Cross Selling the Enterprise General portfolio into Group Life

Strategy

“Brand Leadership” – Turning Etiqa into a Top 3 insurance brand in Malaysia.“S i E ll ” t hi “B t i Cl ”

Cross Selling the Enterprise General portfolio into Group Life

Business “Service Excellence” to achieve near “Best in Class” “Human Capital Development” - in line with the renewed Talent Management of the Group.

Business Enhancement

Boosting life regular premium and improving persistency.Protecting market share in profitable segments

Revenue/Premiums

Expand regionally taking advantage of Maybank’s significant presence.Regional Aspiration

36

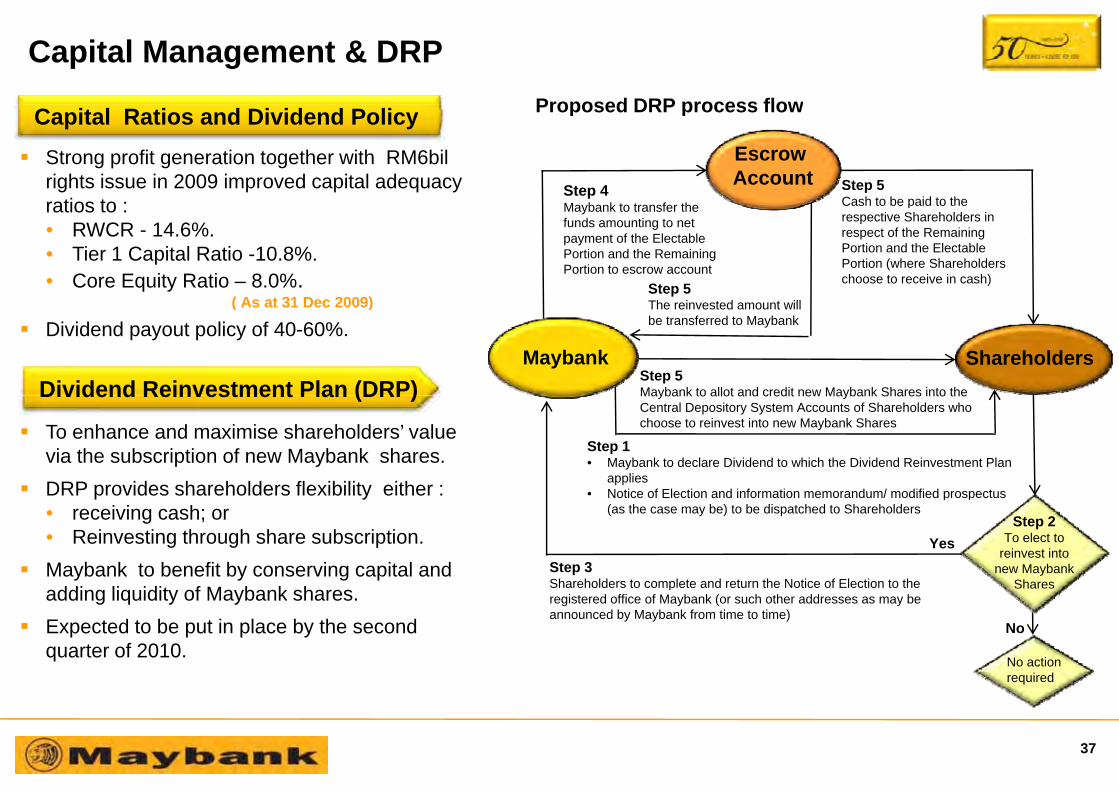

Capital Management & DRPProposed DRP process flow

Step 4 Step 5Cash to be paid to the

Escrow Account

Proposed DRP process flow

Strong profit generation together with RM6bil rights issue in 2009 improved capital adequacy ratios to

Capital Ratios and Dividend Policy

Maybank to transfer the funds amounting to net payment of the Electable Portion and the Remaining Portion to escrow account

Cash to be paid to the respective Shareholders in respect of the Remaining Portion and the Electable Portion (where Shareholders choose to receive in cash)

Step 5

ratios to :• RWCR - 14.6%.• Tier 1 Capital Ratio -10.8%.• Core Equity Ratio – 8.0%.

( A t 31 D 2009)

Step 5Maybank to allot and credit new Maybank Shares into the

The reinvested amount will be transferred to Maybank

Shareholders

( As at 31 Dec 2009)

Dividend payout policy of 40-60%.Maybank

Dividend Reinvestment Plan (DRP)

To enhance and maximise shareholders’ value via the subscription of new Maybank shares.DRP provides shareholders flexibility either :

Step 1• Maybank to declare Dividend to which the Dividend Reinvestment Plan

applies• Notice of Election and information memorandum/ modified prospectus

Maybank to allot and credit new Maybank Shares into the Central Depository System Accounts of Shareholders who choose to reinvest into new Maybank Shares

Dividend Reinvestment Plan (DRP)

DRP provides shareholders flexibility either :• receiving cash; or• Reinvesting through share subscription.Maybank to benefit by conserving capital and ddi li idit f M b k h

• Notice of Election and information memorandum/ modified prospectus (as the case may be) to be dispatched to Shareholders

Step 3Shareholders to complete and return the Notice of Election to the

Step 2To elect to

reinvest into new Maybank

Shares

Yes

adding liquidity of Maybank shares.Expected to be put in place by the second quarter of 2010.

No

pregistered office of Maybank (or such other addresses as may be announced by Maybank from time to time)

No action required

37

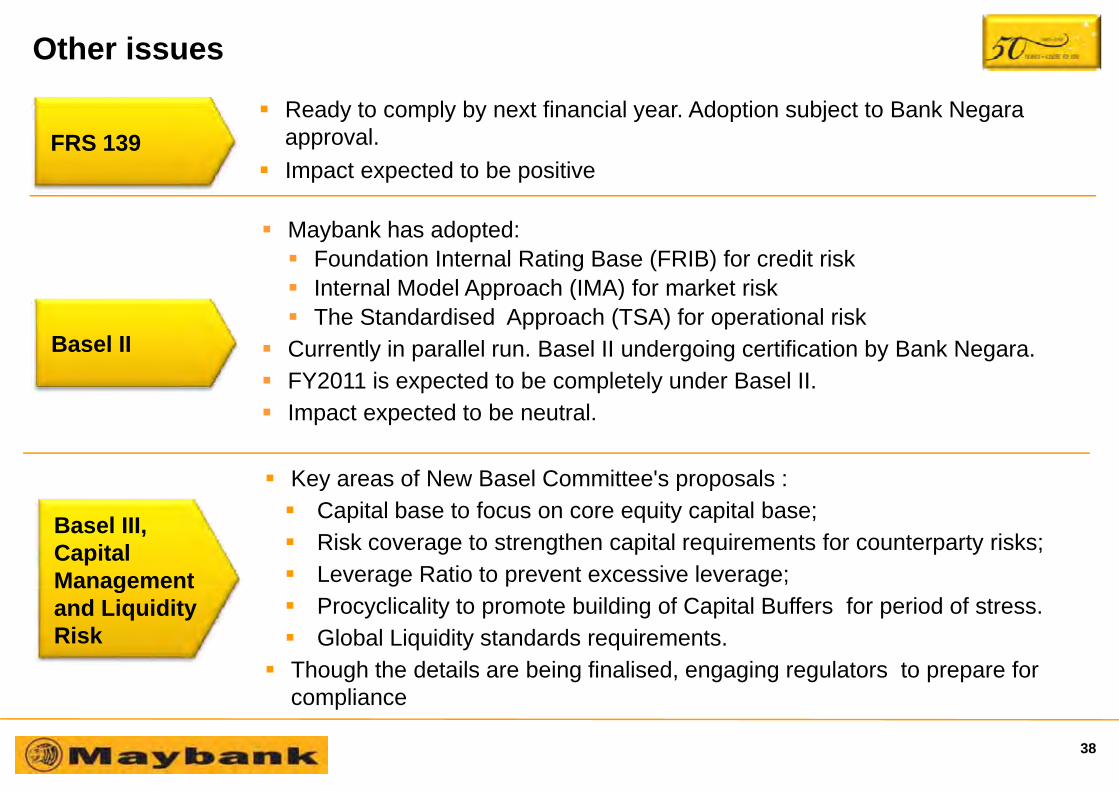

Other issues

R d t l b t fi i l Ad ti bj t t B k NReady to comply by next financial year. Adoption subject to Bank Negara approval.Impact expected to be positive

FRS 139

Maybank has adopted:Foundation Internal Rating Base (FRIB) for credit riskInternal Model Approach (IMA) for market riskpp ( )The Standardised Approach (TSA) for operational risk

Currently in parallel run. Basel II undergoing certification by Bank Negara.FY2011 is expected to be completely under Basel II.

Basel II

Impact expected to be neutral.

Key areas of New Basel Committee's proposals :Capital base to focus on core equity capital base;Risk coverage to strengthen capital requirements for counterparty risks;Leverage Ratio to prevent excessive leverage;

Basel III,Capital Management

Procyclicality to promote building of Capital Buffers for period of stress.Global Liquidity standards requirements.

Though the details are being finalised, engaging regulators to prepare for

gand Liquidity Risk

compliance

38

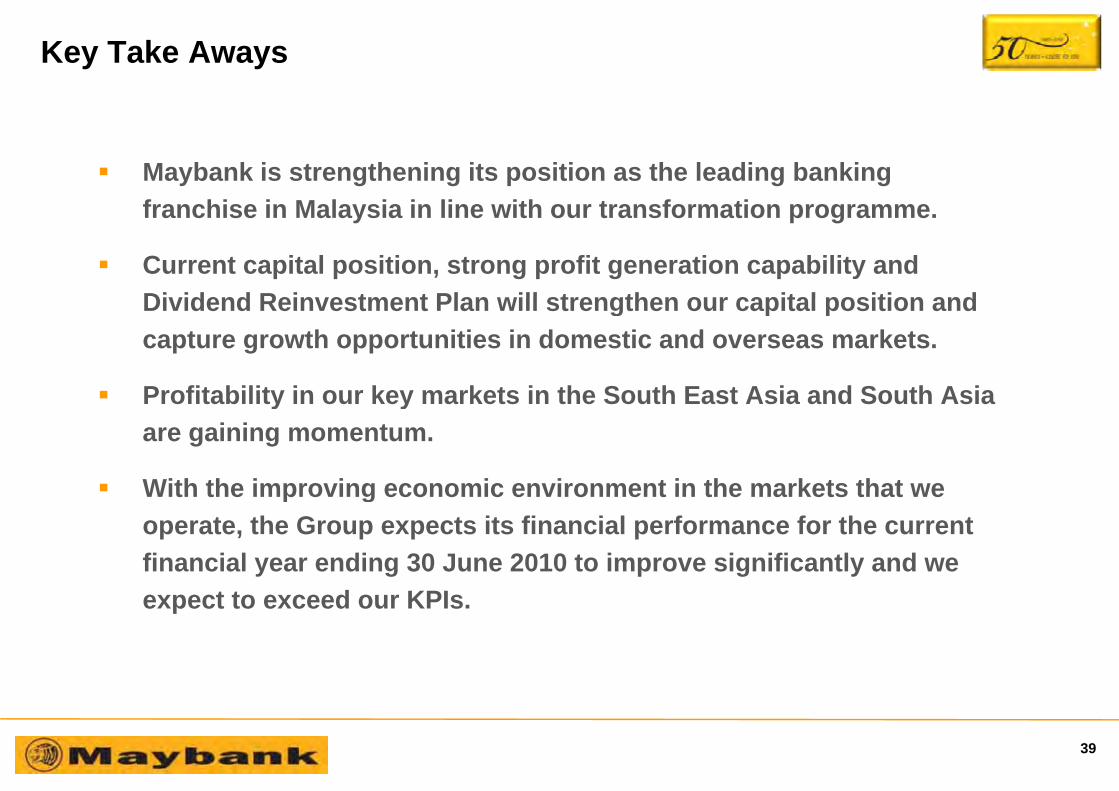

Key Take Aways

Maybank is strengthening its position as the leading banking f hi i M l i i li ith t f tifranchise in Malaysia in line with our transformation programme.

Current capital position, strong profit generation capability and Dividend Reinvestment Plan will strengthen our capital position andDividend Reinvestment Plan will strengthen our capital position and capture growth opportunities in domestic and overseas markets.

Profitability in our key markets in the South East Asia and South AsiaProfitability in our key markets in the South East Asia and South Asia are gaining momentum.

With the improving economic environment in the markets that weWith the improving economic environment in the markets that we operate, the Group expects its financial performance for the current financial year ending 30 June 2010 to improve significantly and we expect to exceed our KPIs.

39

Thank You

Khairussaleh RamliChief Financial OfficerContact: (6)03-2074 4288

MALAYAN BANKING BERHAD14th Floor, Menara Maybank100 Jalan Tun Perak

Hazimi KassimHead, Strategy and Corporate FinanceContact: (6)03-2074 8101

Raja Indra Putra Raja IsmailHead, Investor RelationsContact: (6)03-2074 8582Contact: (6)03 2074 4288

Email: [email protected], Jalan Tun Perak50050 Kuala Lumpur, MalaysiaTel : (6)03-2070 8833

www.maybank.com

Contact: (6)03 2074 8101Email: [email protected]

Contact: (6)03 2074 8582Email: [email protected]

40