Embed Size (px)

Citation preview

Persuasive Pitching

Matt RothmanHemisphere Capital

Techmeetups

2

Overview

• Hemisphere• The market• Funding strategy• Investor selection• Presentation• Terms• Timetable

3

Hemisphere

• Investment and advisory• Focus on platforms• Growth stage• International expansion• Portfolio of six companies• Raising capital in San Francisco, New York &

London over the past 13 years.

4

Game plan

• Funding strategy is as important as product or marketing strategy– “Rules of the Raise”• Raise more than you think you need• Raise it when you don’t need it • Raise it from people who bring more than

money–Friends, family, expertise

5Source: © DJX VentureSource

2009 2010 2011 2012 2013$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

$20.00

US: Average Deal Size (2009-2013) ($M)

Seed Round Linear (Seed Round) First Round Linear (First Round)Second Round Linear (Second Round) Later Stage Linear (Later Stage)

$3.71

$0.76

Fueled byUnicorn rounds

Market situation

6Source: © DJX VentureSource

2009 2010 2011 2012 2013$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

Europe: Average Deal Size (2009-2013) ($M)

Seed Round First Round Second Round Later StageSeed Round Linear (Seed Round) First Round Linear (First Round)Second Round Linear (Second Round) Later Stage Linear (Later Stage)

$2.26

$$0.34 44%

61%

7Source: © DJX VentureSource

Average deal size 2009-2013 (millions)

Europe US Difference

Seed Round $0.58 $0.82 -29.9%

First Round $2.79 $4.48 -37.7%

Second Round $5.63 $8.24 -31.6%

Later Stage $11.52 $15.19 -24.2%

8

Countries most active US VCsIn Q4 14, US VCs weremost active in UK deals.

And, were active in 20%of early and venture rounds, growing more active in later stages(more than 50%).

Naturally, valuations increase.

9

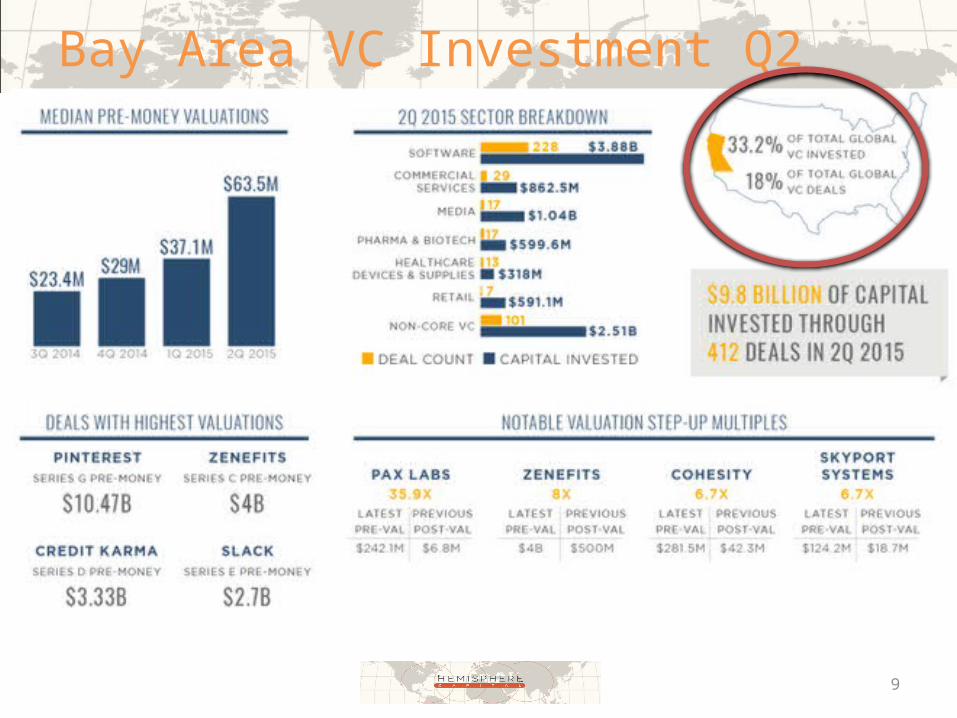

Bay Area VC Investment Q2

10

New York VC Investment Q2

22%

11

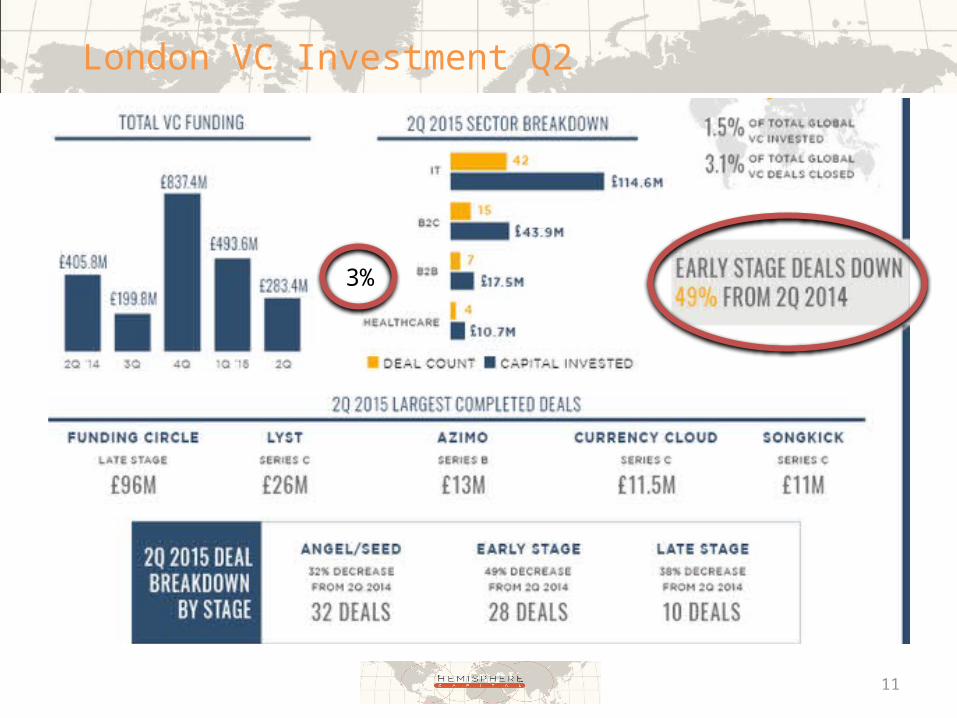

London VC Investment Q2

3%

12

London’s boom is US driven

• Q1 2015 £682 million, a 66% increase over the same period last year.

• In 2014, London-based companies received $1.4 billion, with $795.2 million coming from US based investors driven by the biggest rounds:

• Farfetch: $86 million raised at $1 billion valuation• Shazam: $30 million at $1 billion• Improbable: $20 million at $100 million• Blippar: $45 million

13

European Series A League Table

Total of 106 deals in 2014Six of 10 firms are London and/orUS

Venture ‘types’:Notion – solely B2BOctopus – VCT Northzone – solely ScandinaviaPoint Nine – Berlin Angels

14

Selecting Investors– Stage

• HNW (SEIS/EIS), VCT, strategic

– industry or sector knowledge– Round ‘sweet spot’– A network of customers and executives– Experience as entrepreneurs “Founders Funds”– Investment track record– Geography: UK, US, Europe– Participate in the next round – Who they co-invest with

• Advisors & Governance

15

Some perspective

16

Presentation– Focus on a single business line– Address business objections upfront• Revenues, marketing, opportunity size

– “Show don’t tell”– Pitch by analogy: examples that amplify/validate– Concept vs Data driven (vision vs numbers)– It will be all about execution risk– 10/20/30

17

StorytellingYou are ‘Chief Salesperson and Narrator’– Recruiting customers, employees, investors– Talking points, tempo, temperament

“If you’re lucky enough to grow your company from Series A to Series C, and on to hundreds of millions of dollars in revenue, and successful IPO, you will need to tell your company’s story in high-stakes situations over and over again. Because of this, VCs place huge positive weight on how good you are at this skill. Great storytellers have an unfair competitive advantage.” Bill Gurley, Benchmark

18

TAM, SAM, SOM• Opportunity size: TAM • How big is your dream: SAM• What can your pipeline: • Customers/users: how many, how long? Quotes

• Team: history, skills, talent• Risks• Competitive landscape: identify USP• Metrics: measure success– Users, partners, growth, revenues, profits– If you can’t measure it, you can’t manage it

19

Product is just the start• Product pipeline– Where is it now? Milestones

• GTM– Execution, experience, holes

• Financials: paperwork– Reasonable assumptions– Comparables

• Use of Funds• Recap the focus, forecast and funding needs

20

Terms• Valuation – the market decides• Series/round • Leaders & followers• Syndication• Convertible debt• Warrants/options• Founders shares

21

Timetable

• 90 days• Due diligence: legal and financial– Cap table– Customer contracts– Employees

• Legals• Closing• Next round – valuation appreciation

22

Questions• Venture backable business: Is it worthy of VC

investment?*• Warm intro to an investor• VCs want to date before committing • Lead partner• Funding process• Term sheet and DD

Alex Iskold