Embed Size (px)

DESCRIPTION

For the complete report, get in touch with us at : [email protected] The Sugar Industry in India is part of Netscribes’ Food & Beverage Series reports. The market will be boosted by the rapidly growing food and beverage industry with increasing production of confectionaries, resulting in increased demand for sugar. The report begins with the market overview section, providing details on the domestic sugar production and consumption. India is the world’s largest sugar consuming country and is also the second largest in terms of sugar production. The growth of sugar factories along with the sugar industry segments depicts the sugar industry scenario in India. The sugarcane overview section provides a clear idea about the linkage between the sugarcane farmers and millers, including growth of sugarcane production and cane acreage. This is followed by the sugar industry value chain, illustrating the structure and operational mechanism in the sugar plants and sugar refineries, including the distillery and cogeneration process. The regional distribution section provides a vivid description of the sugar industry in the largest sugar producing states across the country, including Maharashtra, Uttar Pradesh, Karnataka, Tamil Nadu, Andhra Pradesh, Gujarat, Haryana, Punjab and Bihar. This section provides state-wise information, such as no. of sugar factories, sugar production, average sugarcane production, sugarcane area and production. Factors driving the growth of sugar industry in India are also explained in detail. Growing population coupled with rising income is providing impetus to the growth in the country’s sugar consumption, benefiting the overall sugar industry. India is the world’s second largest populated country, representing about 17.31% of the global population. Aggressive growth in the food and beverage industries will lead to the increasing demand for sugar. High sugar content in confectionaries, including chocolates, pastries and ice-creams, will drive the domestic demand for sugar. By-products, such as ethanol and power via cogeneration provides cross functional and cross business opportunities. Growing pharmaceutical market and low per capita sugar consumption in India provide opportunities for the players to capitalize upon. The challenges hindering the market are illustrated. Oversupply situation coupled with higher cane prices results in declining profit margin for the players in the sugar industry. Cyclical nature of the crop results in volatility in sugar production leading to high cane arrears. The present pricing policy is highly government regulated resulting in limited bargaining power of the sugar millers. The government initiatives section provides a detailed description about the Pre-Budget Memorandum 2012-13, including removal of 10% levy sugar quota, implementation of tax incentives, Cenvat Credit on Bagasse, tax deduction under section 35 AD and exemption from both se

Citation preview

Insert Cover Image using Slide Master ViewDo not distort

Sugar Industry IndiaSugar Industry – India

June 2012

Executive Summary

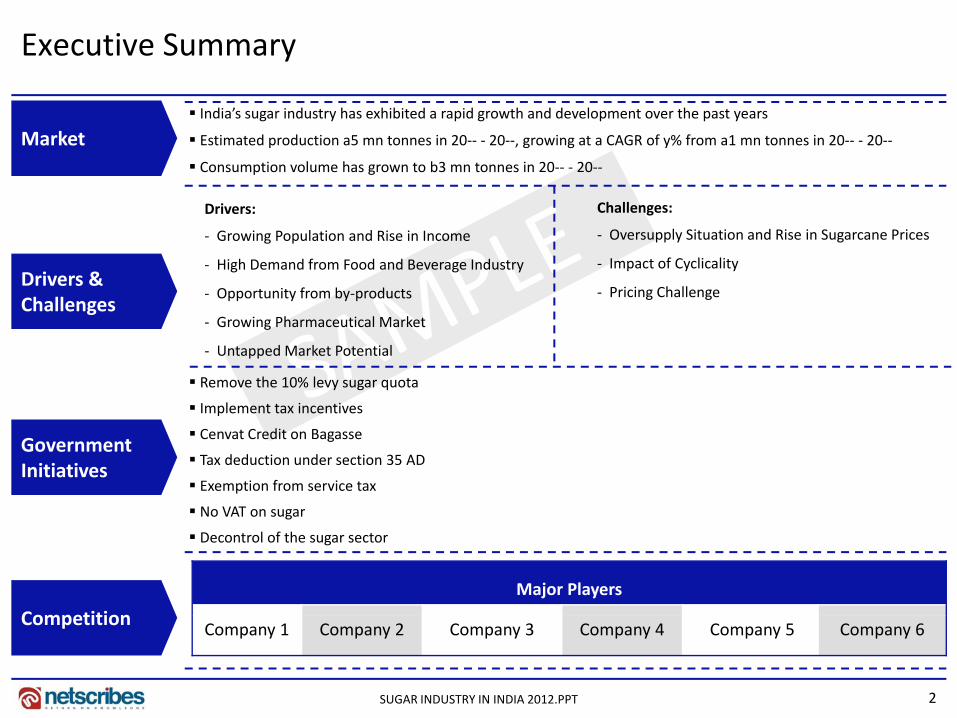

Market India’s sugar industry has exhibited a rapid growth and development over the past years

Estimated production a5 mn tonnes in 20‐‐ ‐ 20‐‐, growing at a CAGR of y% from a1 mn tonnes in 20‐‐ ‐ 20‐‐

Consumption volume has grown to b3 mn tonnes in 20‐‐ ‐ 20‐‐

D i Challenges

Drivers & Challenges

Drivers:

‐ Growing Population and Rise in Income

‐ High Demand from Food and Beverage Industry

‐ Opportunity from by‐products

Challenges:

‐ Oversupply Situation and Rise in Sugarcane Prices

‐ Impact of Cyclicality

‐ Pricing ChallengeChallenges

‐ Growing Pharmaceutical Market

‐ Untapped Market Potential

Remove the 10% levy sugar quota

Implement tax incentives

Government Initiatives

Implement tax incentives

Cenvat Credit on Bagasse

Tax deduction under section 35 AD

Exemption from service tax

No VAT on sugar

Competition

No VAT on sugar

Decontrol of the sugar sector

Major Players

2SUGAR INDUSTRY IN INDIA 2012.PPT

Competition Company 1 Company 2 Company 3 Company 4 Company 5 Company 6

•Market Overview

•Regional Distribution

•Export‐Import

•Drivers & Challengese s & a e ges

•Government Initiatives

•Competition•Competition

•Strategic Recommendations

3SUGAR INDUSTRY IN INDIA 2012.PPT

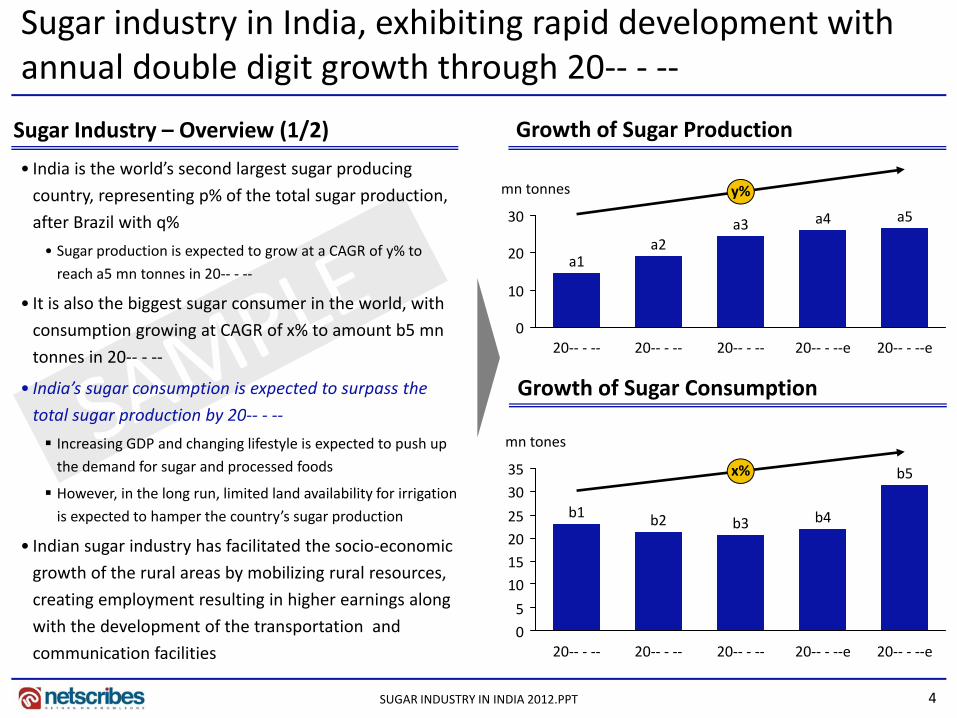

Sugar industry in India, exhibiting rapid development with annual double digit growth through 20‐‐ ‐ ‐‐

• India is the world’s second largest sugar producing

country, representing p% of the total sugar production,

Growth of Sugar ProductionSugar Industry – Overview (1/2)

mn tonnes y%

after Brazil with q%

• Sugar production is expected to grow at a CAGR of y% to

reach a5 mn tonnes in 20‐‐ ‐ ‐‐

• It is also the biggest sugar consumer in the world, with10

20

30 a5a4a3a2

a1

It is also the biggest sugar consumer in the world, with

consumption growing at CAGR of x% to amount b5 mn

tonnes in 20‐‐ ‐ ‐‐

• India’s sugar consumption is expected to surpass the

t t l d ti b 20

020‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

Growth of Sugar Consumptiontotal sugar production by 20‐‐ ‐ ‐‐

Increasing GDP and changing lifestyle is expected to push up

the demand for sugar and processed foods

However, in the long run, limited land availability for irrigation

i t d t h th t ’ d ti 25

30

35

mn tones

x% b5

b4b1is expected to hamper the country’s sugar production

• Indian sugar industry has facilitated the socio‐economic

growth of the rural areas by mobilizing rural resources,

creating employment resulting in higher earnings along 5

10

15

20

25 b4b3b2b1

4SUGAR INDUSTRY IN INDIA 2012.PPT

with the development of the transportation and

communication facilities0

20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

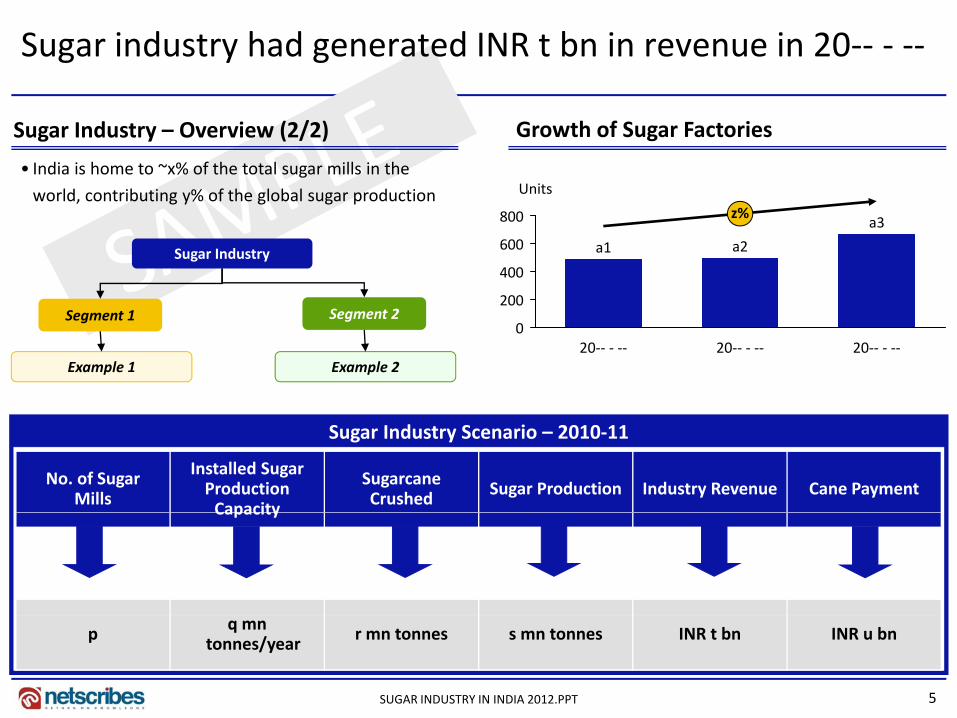

Sugar industry had generated INR t bn in revenue in 20‐‐ ‐ ‐‐

Sugar Industry – Overview (2/2)

• India is home to ~x% of the total sugar mills in the

world, contributing y% of the global sugar production

Growth of Sugar Factories

Units

200

400

600

800 a3z%

a2a1Sugar Industry

020‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

Segment 1 Segment 2

Example 1 Example 2

No. of Sugar Mills

Installed Sugar Production Capacity

Sugarcane Crushed Sugar Production Industry Revenue Cane Payment

Sugar Industry Scenario – 2010‐11

Capacity

5SUGAR INDUSTRY IN INDIA 2012.PPT

p q mn tonnes/year r mn tonnes s mn tonnes INR t bn INR u bn

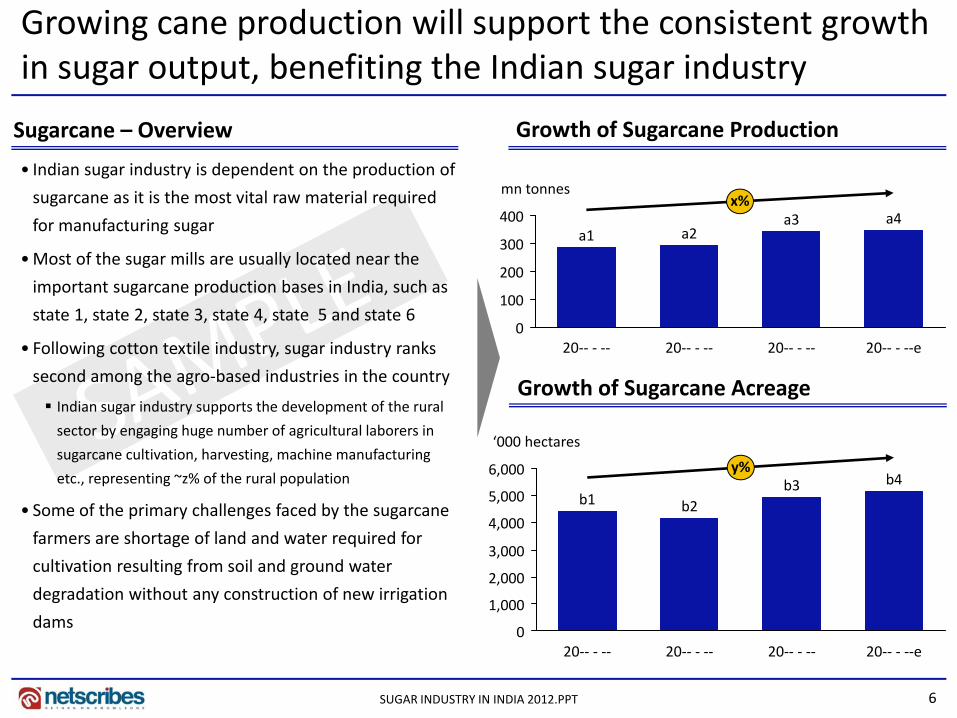

Growing cane production will support the consistent growth in sugar output, benefiting the Indian sugar industry

• Indian sugar industry is dependent on the production of

sugarcane as it is the most vital raw material required

Growth of Sugarcane ProductionSugarcane – Overview

mn tonnesx%g q

for manufacturing sugar

•Most of the sugar mills are usually located near the

important sugarcane production bases in India, such as 100

200

300

400x%

a4a3a2a1

state 1, state 2, state 3, state 4, state 5 and state 6

• Following cotton textile industry, sugar industry ranks

second among the agro‐based industries in the country

Indian sugar industry supports the development of the rural

020‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

Growth of Sugarcane AcreageIndian sugar industry supports the development of the rural

sector by engaging huge number of agricultural laborers in

sugarcane cultivation, harvesting, machine manufacturing

etc., representing ~z% of the rural population

• Some of the primary challenges faced by the sugarcane5,000

6,000

‘000 hectares

b1

y%b4b3

b2• Some of the primary challenges faced by the sugarcane

farmers are shortage of land and water required for

cultivation resulting from soil and ground water

degradation without any construction of new irrigation

d1,000

2,000

3,000

4,000

6SUGAR INDUSTRY IN INDIA 2012.PPT

dams0

20‐‐ ‐ ‐‐ 20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

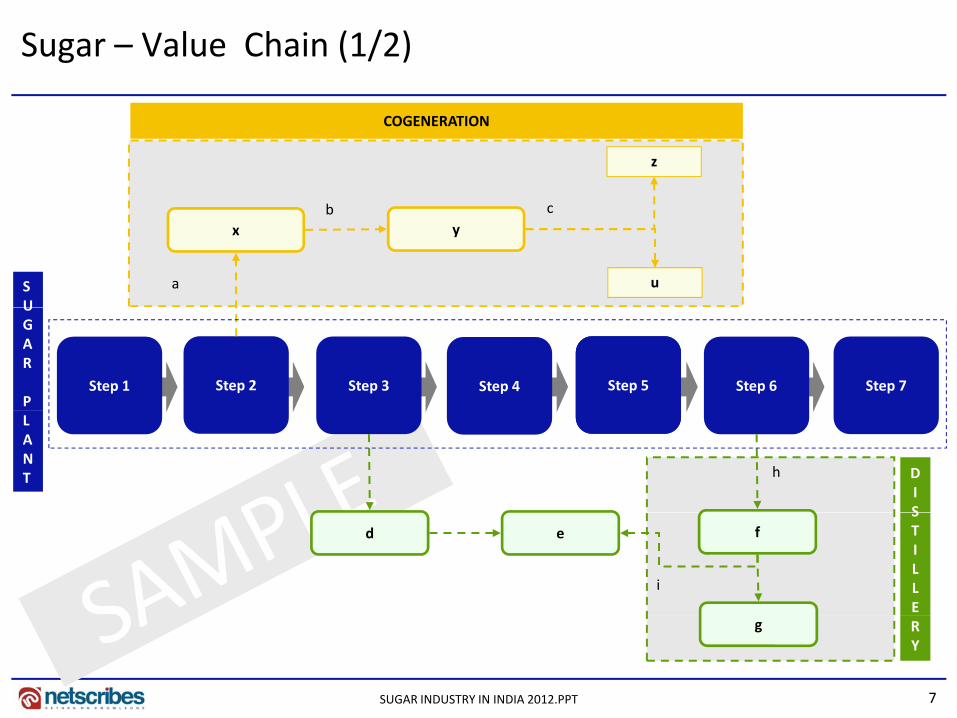

Sugar – Value Chain (1/2)

z

b

COGENERATION

x y

ua

b c

SU

Step 1 Step 2 Step 3 Step 4Syrup Boiling Step 6 Step 7Step 5

UGAR

P

h DIS

LANT

d e f

i

STILLE

7SUGAR INDUSTRY IN INDIA 2012.PPT

g RY

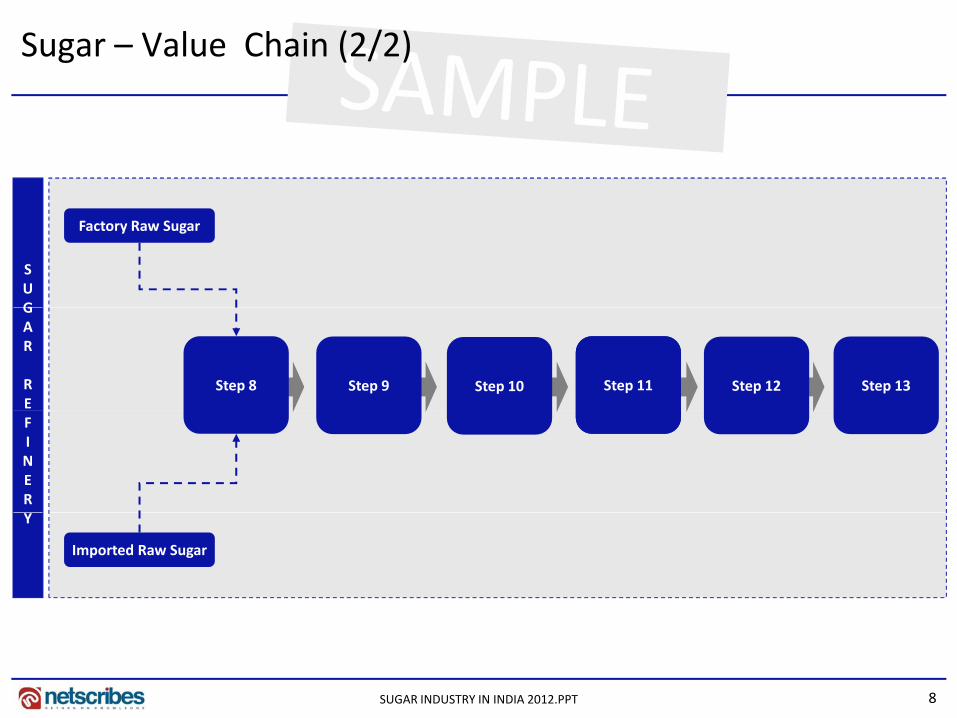

Sugar – Value Chain (2/2)

SUG

Factory Raw Sugar

Step 8 Step 9 Step 10Syrup Boiling Step 12 Step 13Step 11

GAR

REFINERY

Imported Raw Sugar

8SUGAR INDUSTRY IN INDIA 2012.PPT

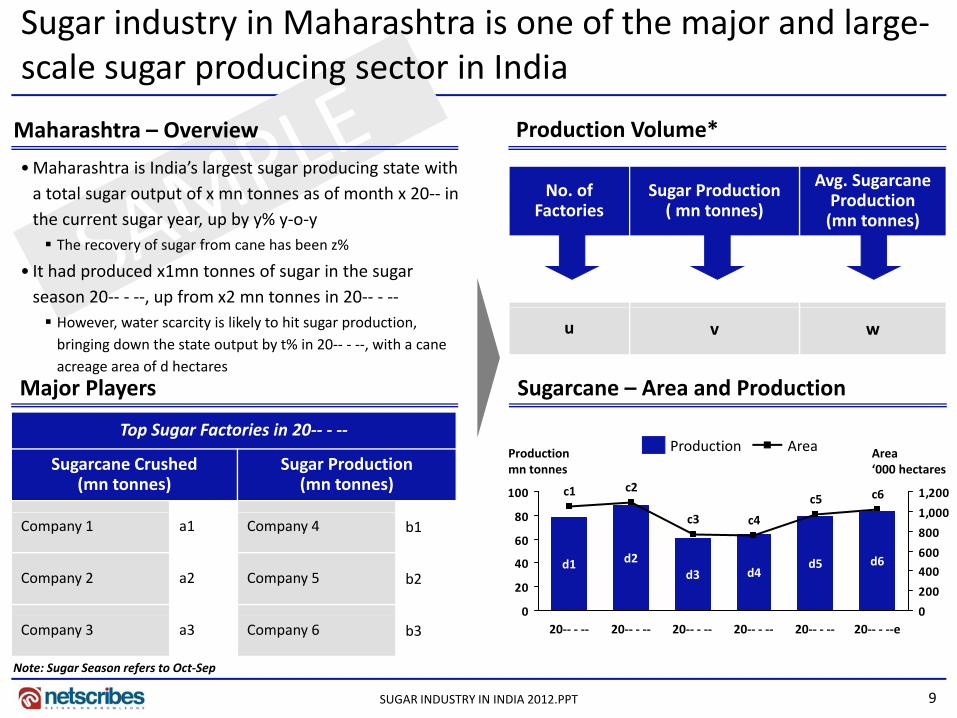

Sugar industry in Maharashtra is one of the major and large‐scale sugar producing sector in India

•Maharashtra is India’s largest sugar producing state with a total sugar output of x mn tonnes as of month x 20‐‐ in

Production Volume*Maharashtra – Overview

No. of F i

Sugar Production( )

Avg. Sugarcane Production

the current sugar year, up by y% y‐o‐y The recovery of sugar from cane has been z%

• It had produced x1mn tonnes of sugar in the sugar season 20‐‐ ‐ ‐‐, up from x2 mn tonnes in 20‐‐ ‐ ‐‐

Factories ( mn tonnes) Production(mn tonnes)

However, water scarcity is likely to hit sugar production, bringing down the state output by t% in 20‐‐ ‐ ‐‐, with a cane acreage area of d hectares

Sugarcane – Area and ProductionMajor Players

u v w

Top Sugar Factories in 20‐‐ ‐ ‐‐

Sugarcane Crushed (mn tonnes)

Sugar Production (mn tonnes)

80

100

1 000

1,200

Area‘000 hectares

Productionmn tonnes

c6c5c2c1

AreaProduction

Company 1 a1 Company 4 b1

Company 2 a2 Company 5 b2

0

20

40

60

80

0

200

400

600

800

1,000

d6d5

c4

d4

c3

d3d2d1

9SUGAR INDUSTRY IN INDIA 2012.PPT

Note: Sugar Season refers to Oct‐Sep

Company 3 a3 Company 6 b30 0

20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

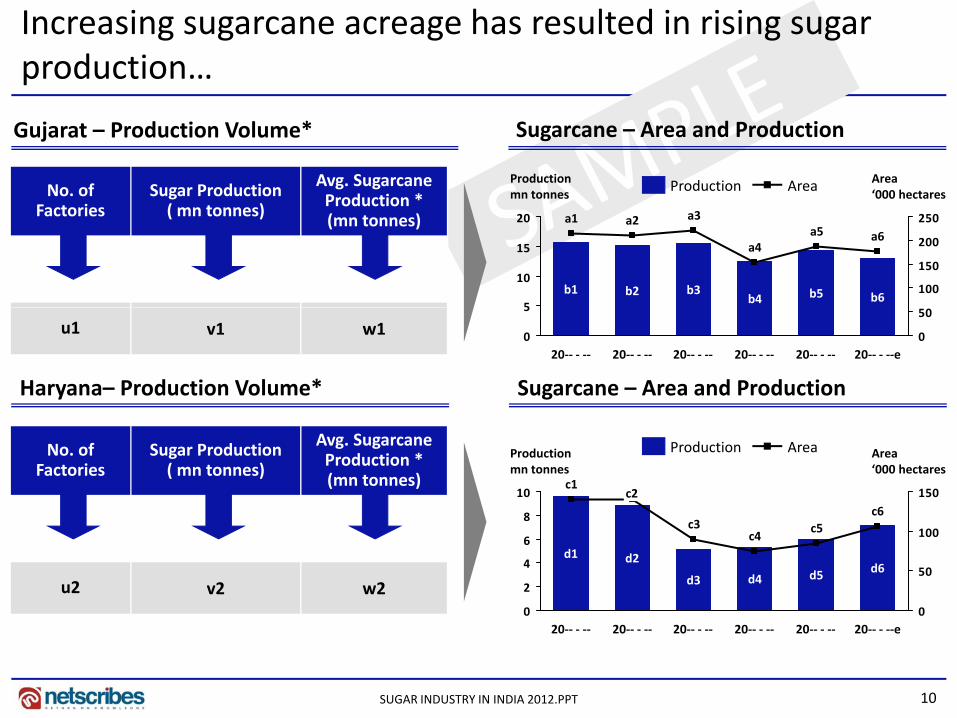

Increasing sugarcane acreage has resulted in rising sugar production…

Sugarcane – Area and ProductionGujarat – Production Volume*

No. of F i

Sugar Production( )

Avg. Sugarcane Production *

Area‘000 hectares

Productionmn tonnes

AreaProduction

Factories ( mn tonnes) Production (mn tonnes)

5

10

15

20

100

150

200

250a6

b6

a5

b5

a4

b4

a3

b3

a2

b2

a1

b1

Haryana– Production Volume*

u1 v1 w1 0

5

0

50

20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

Sugarcane – Area and Production

No. of Factories

Sugar Production( mn tonnes)

Avg. Sugarcane Production *(mn tonnes)

8

10 150c2c1

c6

Productionmn tonnes

Area‘000 hectares

AreaProduction

u2 v2 w20

2

4

6

8

0

50

100

d4

c3

d3

d2d1

c5

d5

c6

d6

c4

10SUGAR INDUSTRY IN INDIA 2012.PPT

0 020‐‐ ‐ ‐‐20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐ 20‐‐ ‐ ‐‐ 20‐‐ ‐ ‐‐e20‐‐ ‐ ‐‐

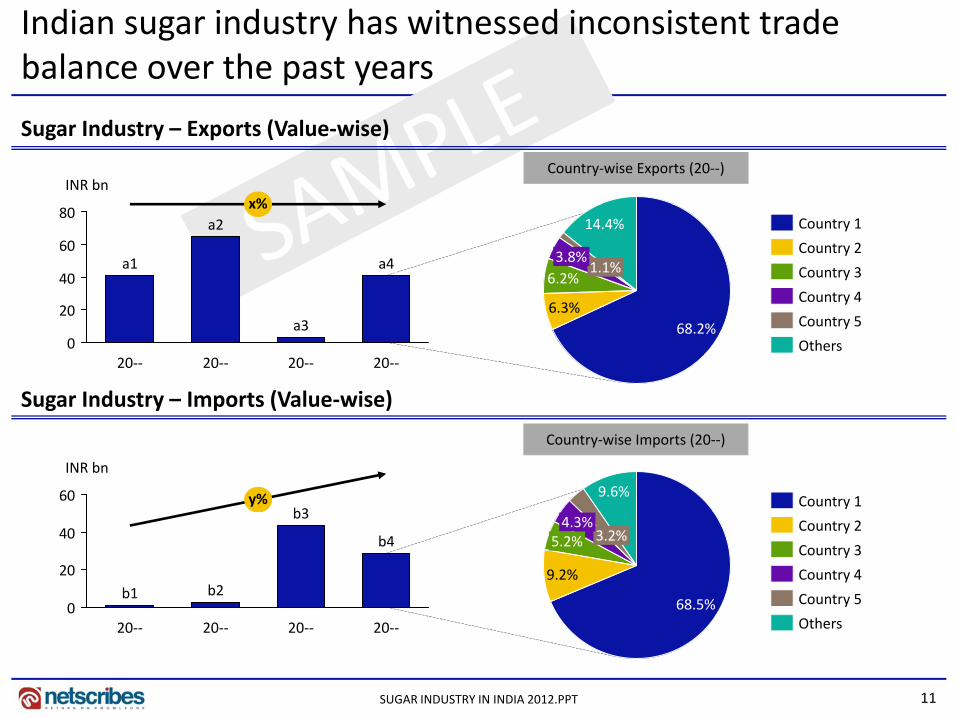

Indian sugar industry has witnessed inconsistent trade balance over the past years

Sugar Industry – Exports (Value‐wise)

x%INR bn

Country‐wise Exports (20‐‐)

20

40

60

80x%

a4

a2

a1 1.1%3.8%

6.2%

6 3%

14.4%

Country 4

Country 3

Country 2

Country 1

Sugar Industry – Imports (Value‐wise)

0

20

20‐‐20‐‐

a3

20‐‐20‐‐

6.3%68.2% Country 5

Others

g y p ( )

Country‐wise Imports (20‐‐)

60 y%

INR bn

b39.6%

Country 1

0

20

40 b4

b3

b2b1

3.2%4.3%

5.2%

9.2%

68.5% Country 5

Country 4

Country 3

Country 2

11SUGAR INDUSTRY IN INDIA 2012.PPT

20‐‐20‐‐20‐‐20‐‐ Others

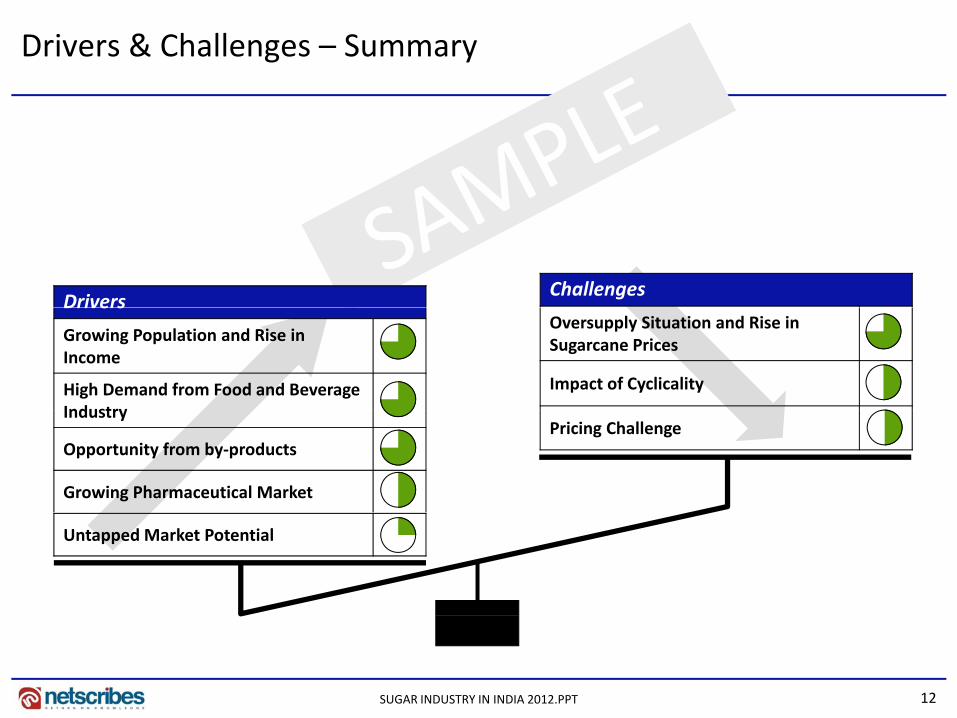

Drivers & Challenges – Summary

DriversChallenges

Drivers

Growing Population and Rise in Income

High Demand from Food and Beverage Industry

Oversupply Situation and Rise in Sugarcane Prices

Impact of Cyclicality

Industry

Opportunity from by‐products

Growing Pharmaceutical Market

Pricing Challenge

Untapped Market Potential

12SUGAR INDUSTRY IN INDIA 2012.PPT

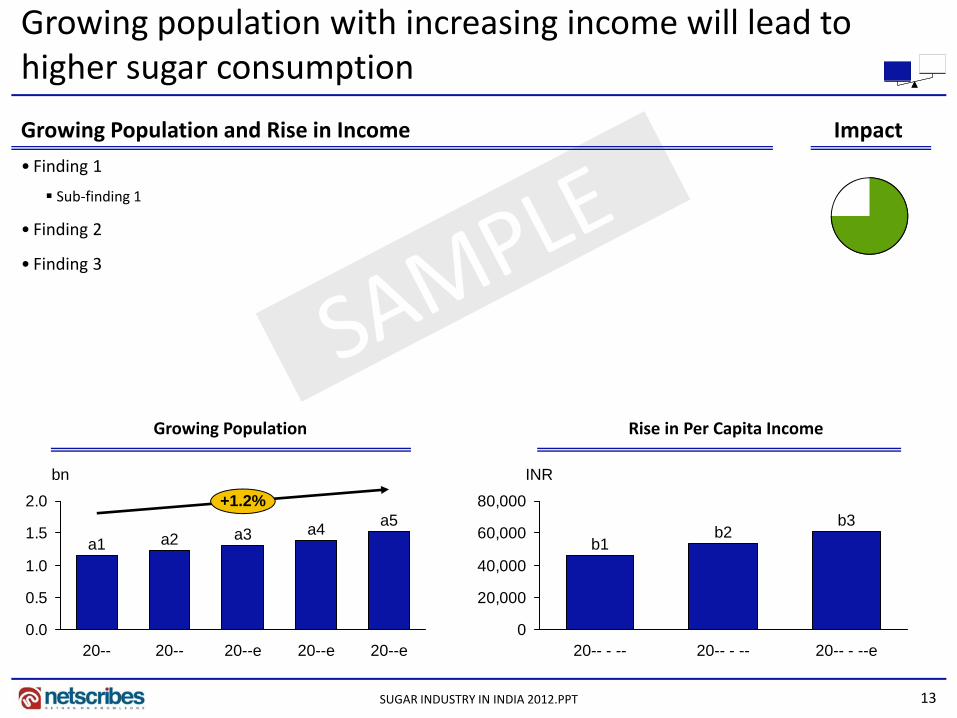

Growing population with increasing income will lead to higher sugar consumption

ImpactGrowing Population and Rise in Income

• Finding 1

Sub‐finding 1

• Finding 2

• Finding 3

Growing Population Rise in Per Capita Income

2.0bn

+1.2% 80,000INR

0.5

1.0

1.5a5a4a3a2a1

20,000

40,000

60,000b3

b2b1

13SUGAR INDUSTRY IN INDIA 2012.PPT

0.020--e20--e20--e20--20--

020-- - --e20-- - --20-- - --

…rapidly growing confectionary market leads to rise in sugar demand, boosting the Indian sugar industry

High Demand from Food and Beverage Industry (2/2)

Sugar content in Popular Chocolates

Chocolate Sugar Content per 100 gm

Sugar content in Ice‐cream

Mars a1 gm

Cadbury Dairy Milk a2 gm

Cadbury 5 Star a3 gm

M h 4

• Finding 1

• Finding 2

Sub‐finding 2Munch a4 gm

Gems a5 gm

Ice‐cream MarketChocolate MarketConfectionary Market

60

80

INR bnx% a4

a3a2

a120

30

INR bn

y% b4b3

b2 30

40 c4c3

c2c1

INR bn

z%

0

20

40

20‐‐e20‐‐e20‐‐e20‐‐0

10

20

20‐‐e20‐‐e20‐‐e20‐‐

b1

0

10

20

20‐‐e20‐‐e20‐‐e20‐‐

14SUGAR INDUSTRY IN INDIA 2012.PPT

Result 1Result 1

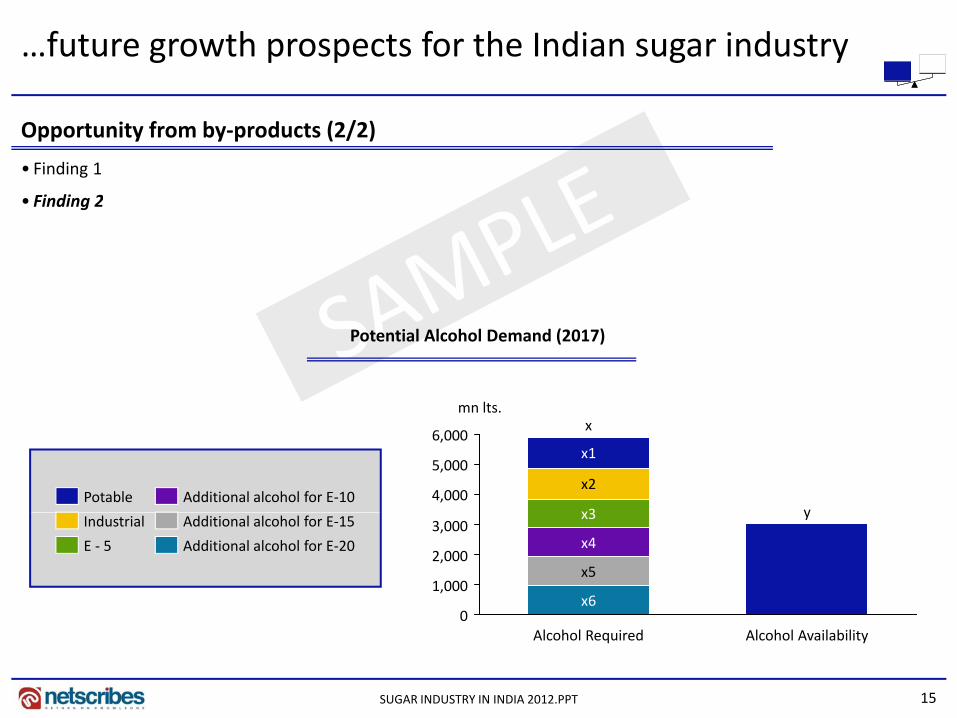

…future growth prospects for the Indian sugar industry

Opportunity from by‐products (2/2)

• Finding 1

• Finding 2Finding 2

mn lts

Potential Alcohol Demand (2017)

4,000

5,000

6,000

y

x

x3

x2

x1

mn lts.

Additional alcohol for E‐10Potable

0

1,000

2,000

3,000y

x6

x5

x4

x3

Additional alcohol for E‐20

Additional alcohol for E‐15

E ‐ 5

Industrial

15SUGAR INDUSTRY IN INDIA 2012.PPT

0Alcohol AvailabilityAlcohol Required

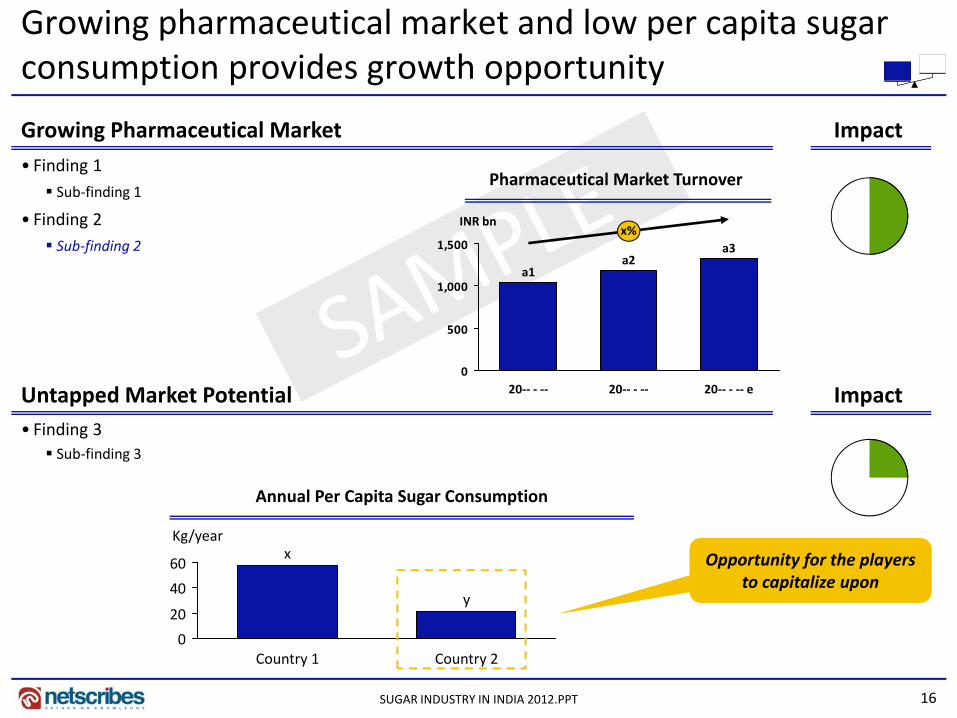

Growing pharmaceutical market and low per capita sugar consumption provides growth opportunity

•Finding 1 Sub‐finding 1

Growing Pharmaceutical Market Impact

Pharmaceutical Market Turnover

• Finding 2 Sub‐finding 2

1,000

1,500

INR bn

a3a2

a1

x%

Untapped Market Potential Impact0

500

20‐‐ ‐ ‐‐ e20‐‐ ‐ ‐‐20‐‐ ‐ ‐‐

• Finding 3 Sub‐finding 3

Annual Per Capita Sugar Consumption

20

40

60

y

xKg/year

Opportunity for the players to capitalize upon

16SUGAR INDUSTRY IN INDIA 2012.PPT

0

20

Country 2Country 1

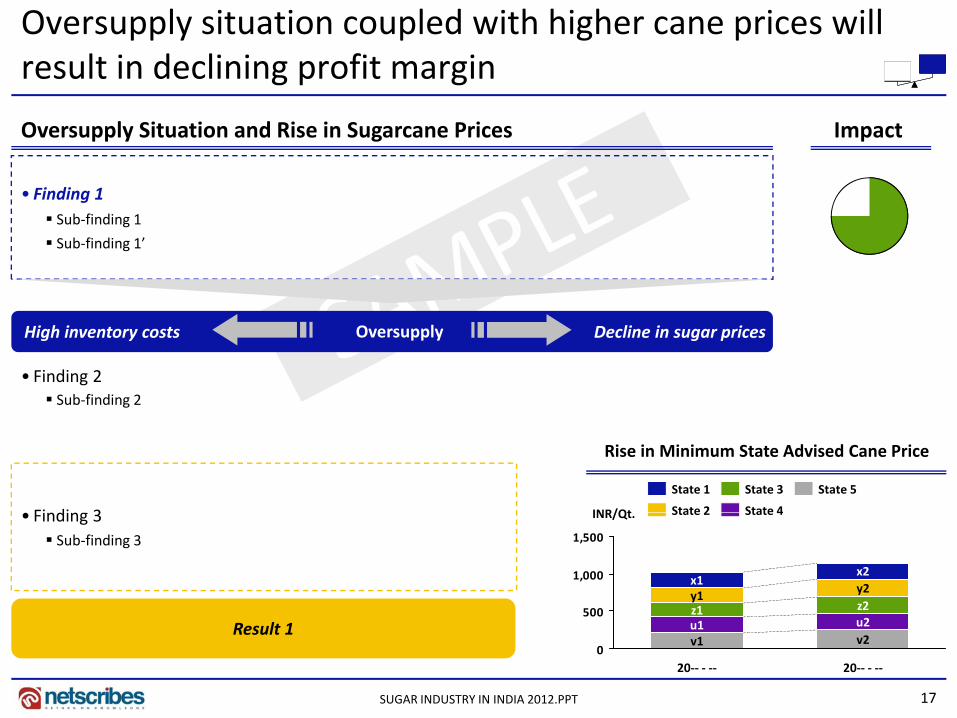

Oversupply situation coupled with higher cane prices will result in declining profit margin

Oversupply Situation and Rise in Sugarcane Prices Impact

• Finding 1 Sub‐finding 1

Sub‐finding 1’

High inventory costs Decline in sugar pricesOversupply

• Finding 2 Sub‐finding 2

Rise in Minimum State Advised Cane Price

Finding 3 INR/Qt

State 5

State 4

State 3

State 2

State 1

• Finding 3 Sub‐finding 3

500

1,000

1,500

INR/Qt.

z2y2x2

z1y1x1

State 4State 2

17SUGAR INDUSTRY IN INDIA 2012.PPT

Result 10

500

20‐‐ ‐ ‐‐

v2u2

20‐‐ ‐ ‐‐

v1u1

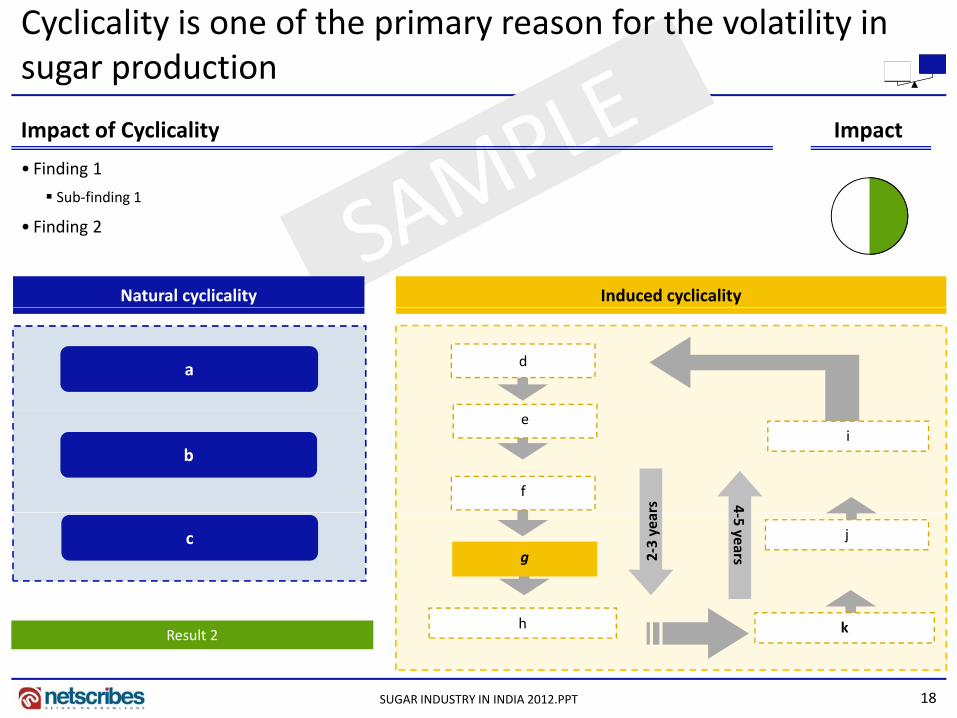

Cyclicality is one of the primary reason for the volatility in sugar production

ImpactImpact of Cyclicality

• Finding 1

Sub‐finding 1

• Finding 2

Induced cyclicalityNatural cyclicality

da

e

f

i

4rs

b

gj

4‐5 years2‐3 yea

c

18SUGAR INDUSTRY IN INDIA 2012.PPT

h kResult 2

Pre‐Budget Memorandum 2012‐13 (1/3)

Sugar Sector’s Budget 2012‐13 wish‐list

• Finding 1

Remove the 10% levy sugar

quota

• Finding 2

• Finding 3

• Finding 4

Implement tax i i

• Finding 1

• Finding 2

incentives• Finding 3

• Finding 4

19SUGAR INDUSTRY IN INDIA 2012.PPT

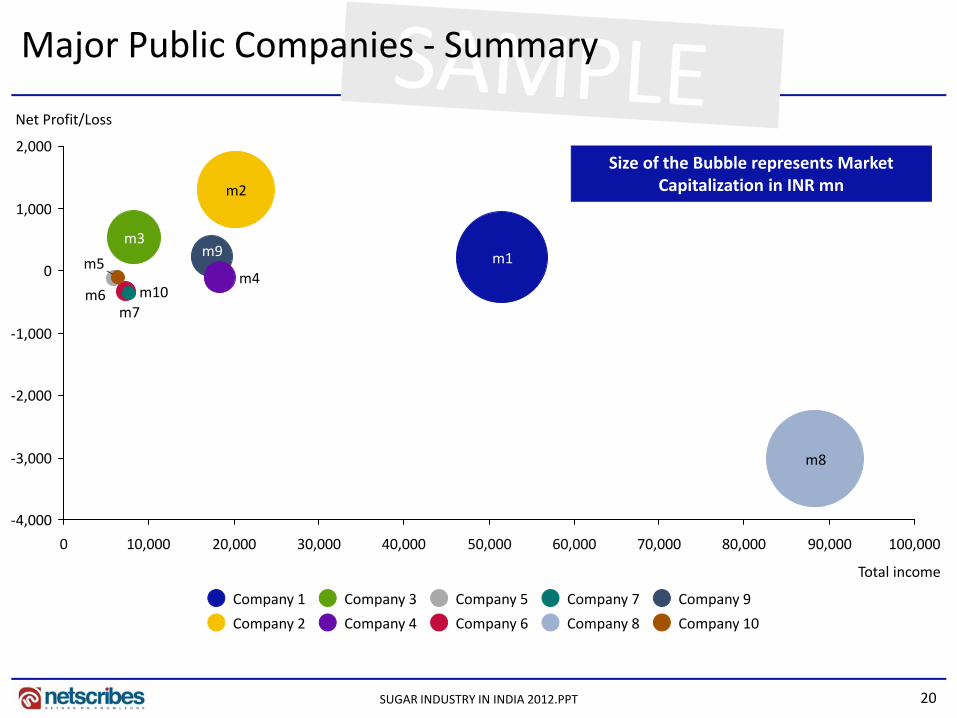

Major Public Companies ‐ Summary

1 000

2,000

m2

Net Profit/Loss

Size of the Bubble represents Market Capitalization in INR mn

0

1,000

m5m9

7m10m6

m4

m3m1

‐2,000

‐1,000m7

‐3,000 m8

‐4,000

0 10,000 20,000 30,000 40,000 50,000 60,000 70,000 80,000 90,000 100,000

Total income

Company 9Company 7Company 5Company 3Company 1

20SUGAR INDUSTRY IN INDIA 2012.PPT

Company 10Company 8Company 6Company 4Company 2

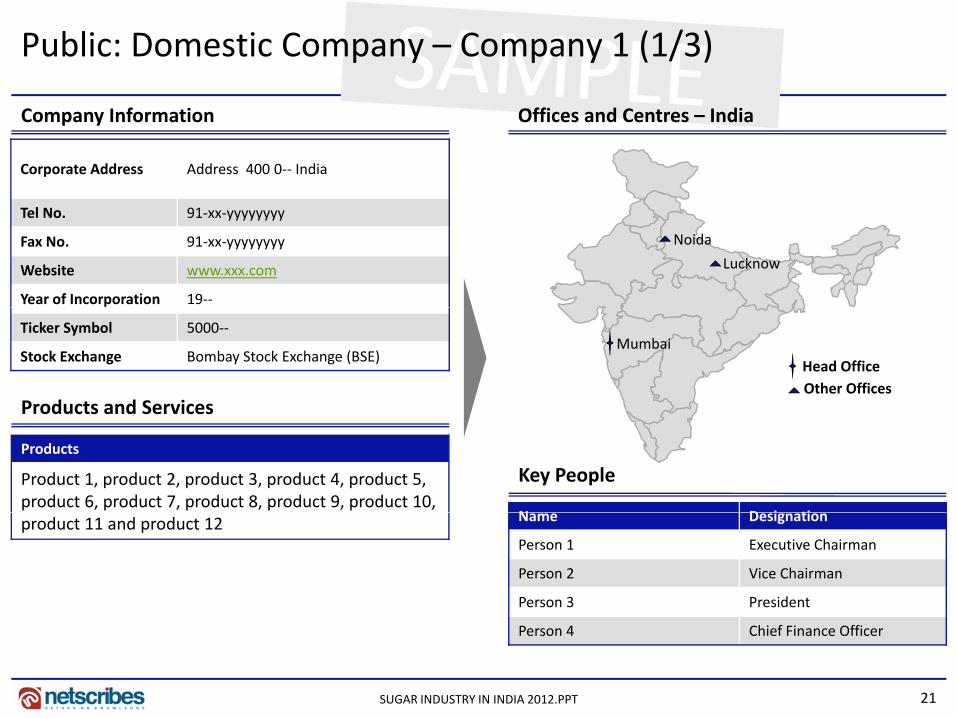

Public: Domestic Company – Company 1 (1/3)

Company Information Offices and Centres – India

Corporate Address Address 400 0‐‐ India

Tel No. 91‐xx‐yyyyyyyy

Fax No. 91‐xx‐yyyyyyyy

Website www.xxx.com

Year of Incorporation 19‐‐

Noida

Lucknow

Products and Services

Ticker Symbol 5000‐‐

Stock Exchange Bombay Stock Exchange (BSE)Head Office

Mumbai

Other Offices

Key People

Products and Services

Products

Product 1, product 2, product 3, product 4, product 5, product 6, product 7, product 8, product 9, product 10,

N D i tiproduct 11 and product 12 Name Designation

Person 1 Executive Chairman

Person 2 Vice Chairman

Person 3 President

21SUGAR INDUSTRY IN INDIA 2012.PPT

Person 4 Chief Finance Officer

i i l S h K i

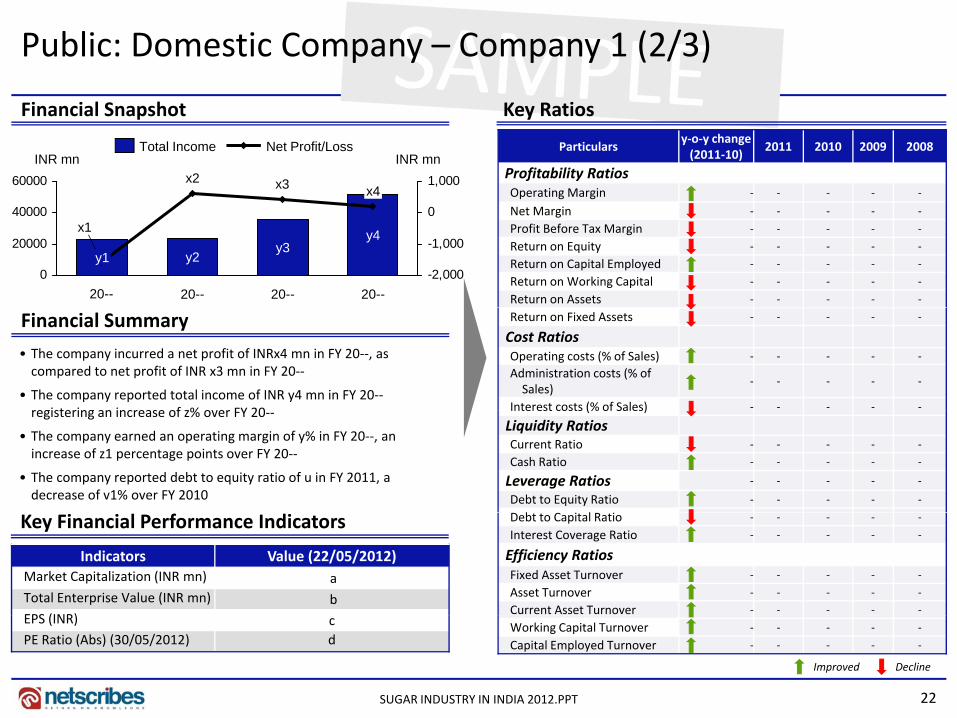

Public: Domestic Company – Company 1 (2/3)

Financial Snapshot Key Ratios

Particulars y‐o‐y change (2011‐10)

2011 2010 2009 2008

Profitability RatiosOperating Margin ‐ ‐ ‐ ‐ ‐

Net Profit/LossTotal Income

60000 1,000INR mn INR mn

x4x3x2

Net Margin ‐ ‐ ‐ ‐ ‐

Profit Before Tax Margin ‐ ‐ ‐ ‐ ‐

Return on Equity ‐ ‐ ‐ ‐ ‐

Return on Capital Employed ‐ ‐ ‐ ‐ ‐

Return on Working Capital ‐ ‐ ‐ ‐ ‐

Return on Assets ‐ ‐ ‐ ‐ ‐

0

20000

40000

-2,000

-1,000

0

20--

y4

20--

y3

20--

y2

x1

y1

20--

Financial Summary

• The company incurred a net profit of INRx4 mn in FY 20‐‐, as compared to net profit of INR x3 mn in FY 20‐‐

• The company reported total income of INR y4 mn in FY 20‐‐registering an increase of % over FY 20

Return on Fixed Assets ‐ ‐ ‐ ‐ ‐

Cost RatiosOperating costs (% of Sales) ‐ ‐ ‐ ‐ ‐

Administration costs (% of Sales)

‐ ‐ ‐ ‐ ‐

Interest costs (% of Sales) ‐ ‐ ‐ ‐ ‐registering an increase of z% over FY 20‐‐

• The company earned an operating margin of y% in FY 20‐‐, an increase of z1 percentage points over FY 20‐‐

• The company reported debt to equity ratio of u in FY 2011, a decrease of v1% over FY 2010

Interest costs (% of Sales)

Liquidity RatiosCurrent Ratio ‐ ‐ ‐ ‐ ‐

Cash Ratio ‐ ‐ ‐ ‐ ‐

Leverage Ratios ‐ ‐ ‐ ‐ ‐

Debt to Equity Ratio ‐ ‐ ‐ ‐ ‐

b i l iKey Financial Performance Indicators

Indicators Value (22/05/2012)Market Capitalization (INR mn) aTotal Enterprise Value (INR mn) bEPS (INR)

Debt to Capital Ratio ‐ ‐ ‐ ‐ ‐

Interest Coverage Ratio ‐ ‐ ‐ ‐ ‐

Efficiency RatiosFixed Asset Turnover ‐ ‐ ‐ ‐ ‐

Asset Turnover ‐ ‐ ‐ ‐ ‐

Current Asset Turnover ‐ ‐ ‐ ‐ ‐

22SUGAR INDUSTRY IN INDIA 2012.PPT

EPS (INR) cPE Ratio (Abs) (30/05/2012) d

Working Capital Turnover ‐ ‐ ‐ ‐ ‐

Capital Employed Turnover ‐ ‐ ‐ ‐ ‐

Improved Decline

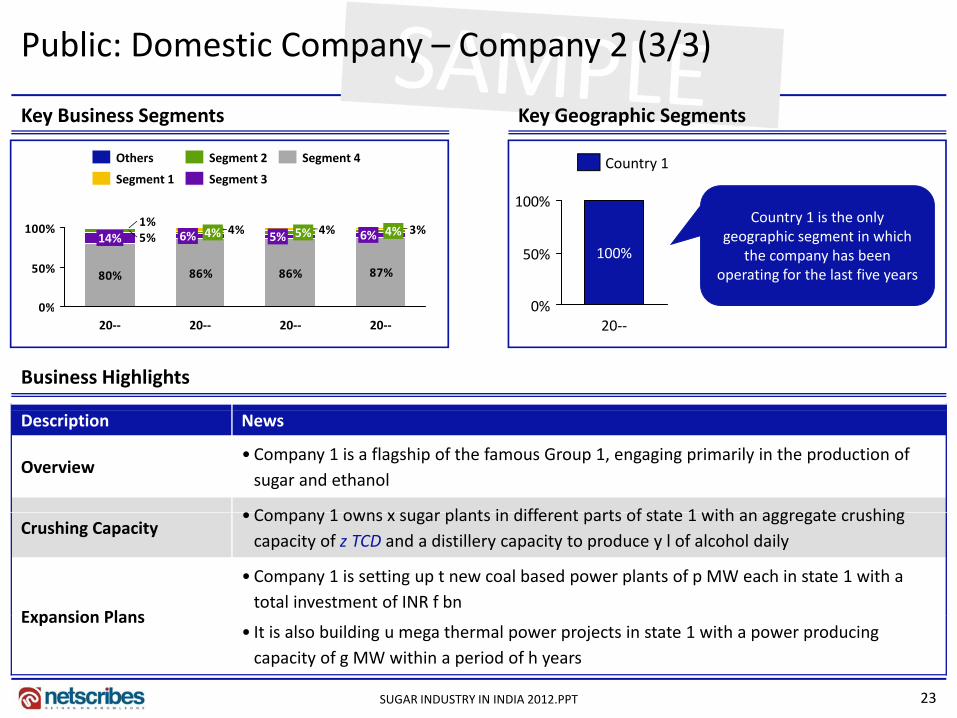

Public: Domestic Company – Company 2 (3/3)

Key Business Segments Key Geographic Segments

Segment 4

Segment 3

Segment 2

Segment 1

Others

100%

Country 1

80% 86% 86% 87%

5%3%4%4%

1%

0%

50%

100% 6% 4%5% 5%6% 4%14%

0%

50%

100%

100%

Country 1 is the only geographic segment in which

the company has been operating for the last five years

Business Highlights

0%20‐‐20‐‐20‐‐20‐‐

0%20‐‐

Description News

Overview• Company 1 is a flagship of the famous Group 1, engaging primarily in the production of sugar and ethanol

• Company 1 owns x sugar plants in different parts of state 1 with an aggregate crushingCrushing Capacity

• Company 1 owns x sugar plants in different parts of state 1 with an aggregate crushing capacity of z TCD and a distillery capacity to produce y l of alcohol daily

Expansion Plans

• Company 1 is setting up t new coal based power plants of p MW each in state 1 with a total investment of INR f bn

23SUGAR INDUSTRY IN INDIA 2012.PPT

Expansion Plans• It is also building u mega thermal power projects in state 1 with a power producing capacity of g MW within a period of h years

Thank you for the attentionThe Sugar Industry – India report is part of Research on India’s Food & Beverage Series.For more detailed information or customized research requirements please contact:

Phone: +91 33 4064 6214Phone: 91 33 4064 6214E‐Mail: [email protected]

Follow us on:

About NetscribesNetscribes is a knowledge‐consulting and solutions firm with clientele across the globe. The company’s expertise spans areas of investment & g g f g p y p p fbusiness research, business & corporate intelligence, content‐management services, and knowledge‐software services. At its core lies a true value proposition that draws upon a vast knowledge base. Netscribes is a one‐stop shop designed to fulfil clients’ profitability and growth objectives.

Disclaimer: This report is published for general information only Although high standards have been used in the preparation “Netscribes” is

24SUGAR INDUSTRY IN INDIA 2012.PPT

Disclaimer: This report is published for general information only. Although high standards have been used in the preparation, Netscribes is not responsible for any loss or damage arising from use of this document. This document is the sole property of Netscribes and prior permission is required for guidelines on reproduction.