Embed Size (px)

Citation preview

Frost & Sullivan

Overview of the General Insurance Industry

Malaysia

2

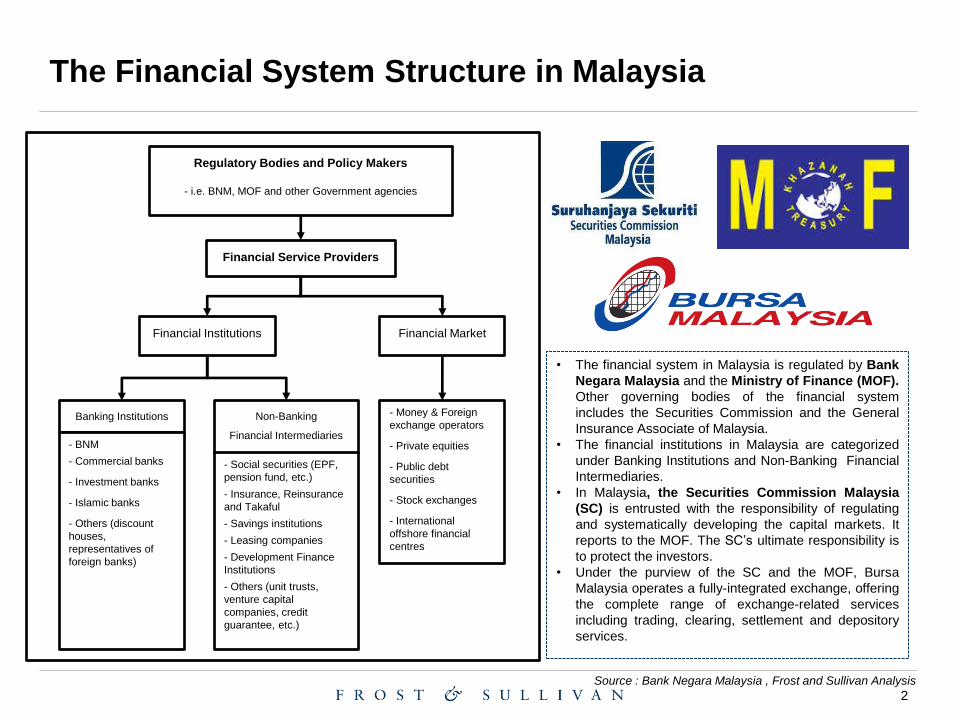

Financial Service Providers

Banking Institutions

Regulatory Bodies and Policy Makers

- i.e. BNM, MOF and other Government agencies

Financial Institutions Financial Market

Non-Banking

Financial Intermediaries - BNM

- Commercial banks

- Investment banks

- Islamic banks

- Others (discount

houses,

representatives of

foreign banks)

- Social securities (EPF,

pension fund, etc.)

- Insurance, Reinsurance

and Takaful

- Savings institutions

- Leasing companies

- Development Finance

Institutions

- Others (unit trusts,

venture capital

companies, credit

guarantee, etc.)

- Money & Foreign

exchange operators

- Private equities

- Public debt

securities

- Stock exchanges

- International

offshore financial

centres

• The financial system in Malaysia is regulated by Bank

Negara Malaysia and the Ministry of Finance (MOF).

Other governing bodies of the financial system

includes the Securities Commission and the General

Insurance Associate of Malaysia.

• The financial institutions in Malaysia are categorized

under Banking Institutions and Non-Banking Financial

Intermediaries.

• In Malaysia, the Securities Commission Malaysia

(SC) is entrusted with the responsibility of regulating

and systematically developing the capital markets. It

reports to the MOF. The SC’s ultimate responsibility is

to protect the investors.

• Under the purview of the SC and the MOF, Bursa

Malaysia operates a fully-integrated exchange, offering

the complete range of exchange-related services

including trading, clearing, settlement and depository

services.

The Financial System Structure in Malaysia

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

3

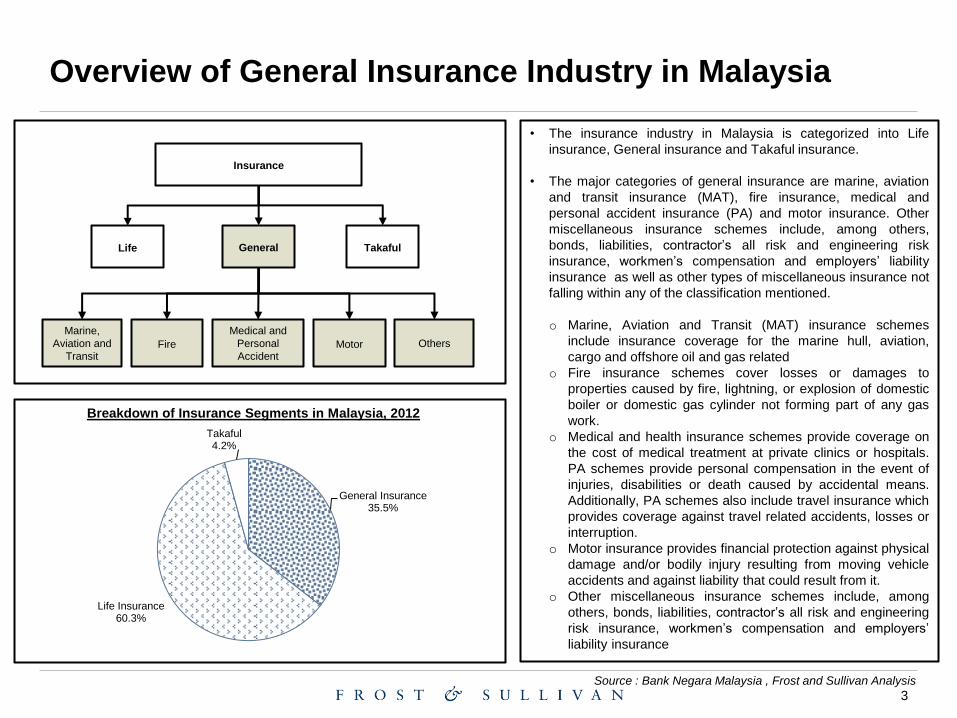

Insurance

Life General

Marine,

Aviation and

Transit

Medical and

Personal

Accident

Others Motor Fire

• The insurance industry in Malaysia is categorized into Life

insurance, General insurance and Takaful insurance.

• The major categories of general insurance are marine, aviation

and transit insurance (MAT), fire insurance, medical and

personal accident insurance (PA) and motor insurance. Other

miscellaneous insurance schemes include, among others,

bonds, liabilities, contractor’s all risk and engineering risk

insurance, workmen’s compensation and employers’ liability

insurance as well as other types of miscellaneous insurance not

falling within any of the classification mentioned.

o Marine, Aviation and Transit (MAT) insurance schemes

include insurance coverage for the marine hull, aviation,

cargo and offshore oil and gas related

o Fire insurance schemes cover losses or damages to

properties caused by fire, lightning, or explosion of domestic

boiler or domestic gas cylinder not forming part of any gas

work.

o Medical and health insurance schemes provide coverage on

the cost of medical treatment at private clinics or hospitals.

PA schemes provide personal compensation in the event of

injuries, disabilities or death caused by accidental means.

Additionally, PA schemes also include travel insurance which

provides coverage against travel related accidents, losses or

interruption.

o Motor insurance provides financial protection against physical

damage and/or bodily injury resulting from moving vehicle

accidents and against liability that could result from it.

o Other miscellaneous insurance schemes include, among

others, bonds, liabilities, contractor’s all risk and engineering

risk insurance, workmen’s compensation and employers’

liability insurance

Takaful

General Insurance 35.5%

Life Insurance 60.3%

Takaful 4.2%

Breakdown of Insurance Segments in Malaysia, 2012

Overview of General Insurance Industry in Malaysia

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

4

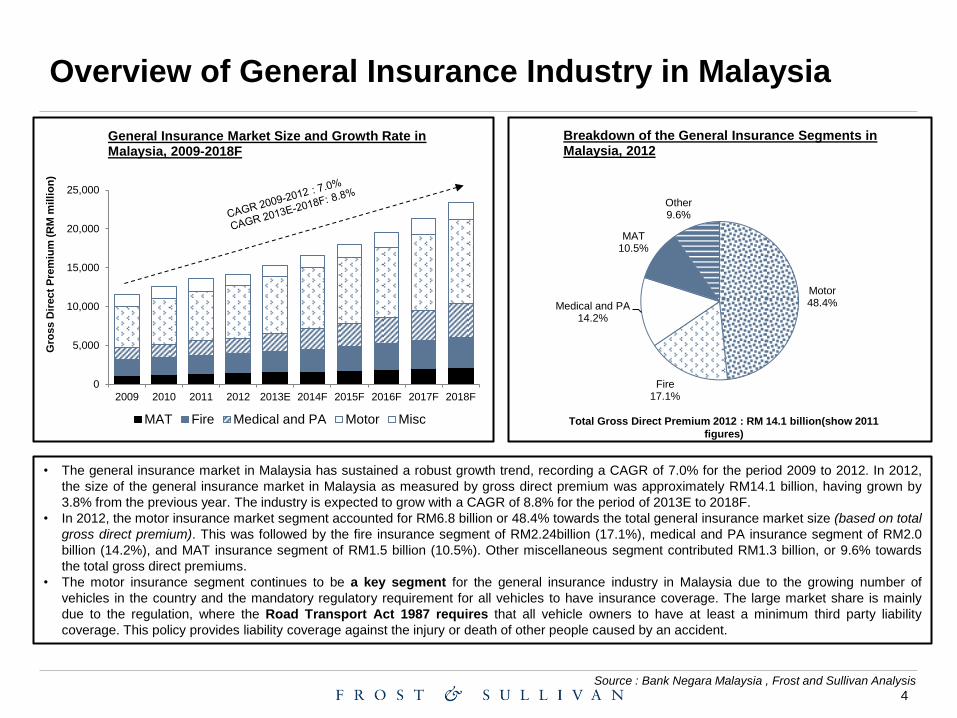

• The general insurance market in Malaysia has sustained a robust growth trend, recording a CAGR of 7.0% for the period 2009 to 2012. In 2012,

the size of the general insurance market in Malaysia as measured by gross direct premium was approximately RM14.1 billion, having grown by

3.8% from the previous year. The industry is expected to grow with a CAGR of 8.8% for the period of 2013E to 2018F.

• In 2012, the motor insurance market segment accounted for RM6.8 billion or 48.4% towards the total general insurance market size (based on total

gross direct premium). This was followed by the fire insurance segment of RM2.24billion (17.1%), medical and PA insurance segment of RM2.0

billion (14.2%), and MAT insurance segment of RM1.5 billion (10.5%). Other miscellaneous segment contributed RM1.3 billion, or 9.6% towards

the total gross direct premiums.

• The motor insurance segment continues to be a key segment for the general insurance industry in Malaysia due to the growing number of

vehicles in the country and the mandatory regulatory requirement for all vehicles to have insurance coverage. The large market share is mainly

due to the regulation, where the Road Transport Act 1987 requires that all vehicle owners to have at least a minimum third party liability

coverage. This policy provides liability coverage against the injury or death of other people caused by an accident.

Motor 48.4%

Fire 17.1%

Medical and PA 14.2%

MAT 10.5%

Other 9.6%

Breakdown of the General Insurance Segments in Malaysia, 2012

Total Gross Direct Premium 2012 : RM 14.1 billion(show 2011

figures)

Overview of General Insurance Industry in Malaysia

0

5,000

10,000

15,000

20,000

25,000

2009 2010 2011 2012 2013E 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

General Insurance Market Size and Growth Rate in Malaysia, 2009-2018F

MAT Fire Medical and PA Motor Misc

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

5

-8

-6

-4

-2

0

2

4

6

8

10

12

% C

hange

Year

Inflation Rate (%) Real GDP Growth (%) Real Interest Rate (%)

Asian Financial Crisis

US/Europe recession

Commodity Crisis Global Financial

Crisis

Dot-com Bubble,

9/11

Thai Flood, Japan Earthquake

US sub-prime mortgage crisis -7.4%

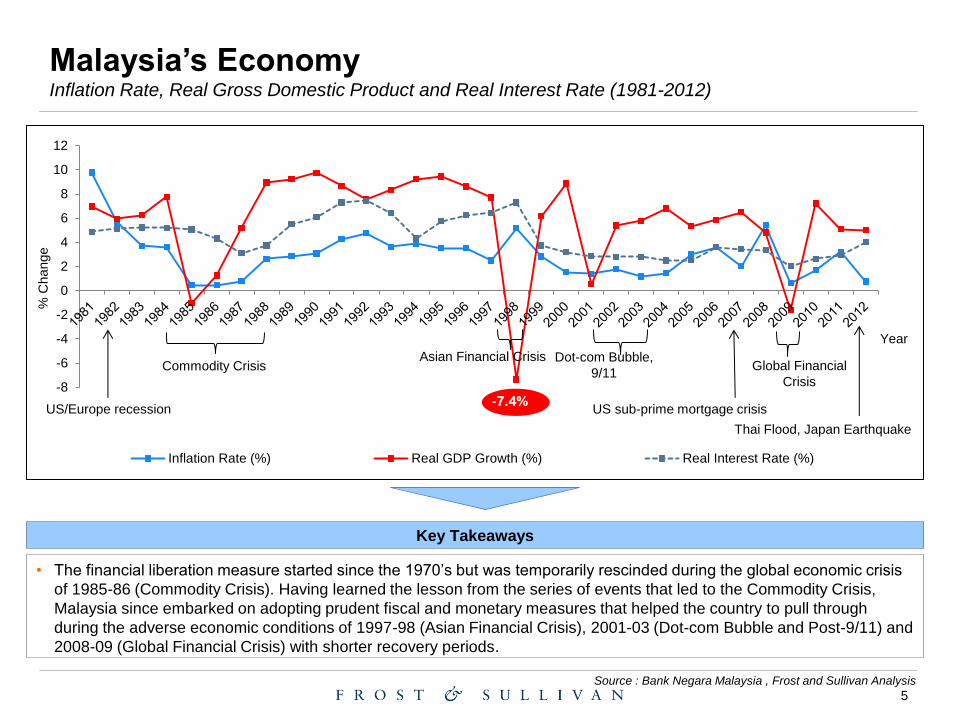

• The financial liberation measure started since the 1970’s but was temporarily rescinded during the global economic crisis

of 1985-86 (Commodity Crisis). Having learned the lesson from the series of events that led to the Commodity Crisis,

Malaysia since embarked on adopting prudent fiscal and monetary measures that helped the country to pull through

during the adverse economic conditions of 1997-98 (Asian Financial Crisis), 2001-03 (Dot-com Bubble and Post-9/11) and

2008-09 (Global Financial Crisis) with shorter recovery periods.

Key Takeaways

Malaysia’s Economy Inflation Rate, Real Gross Domestic Product and Real Interest Rate (1981-2012)

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

6

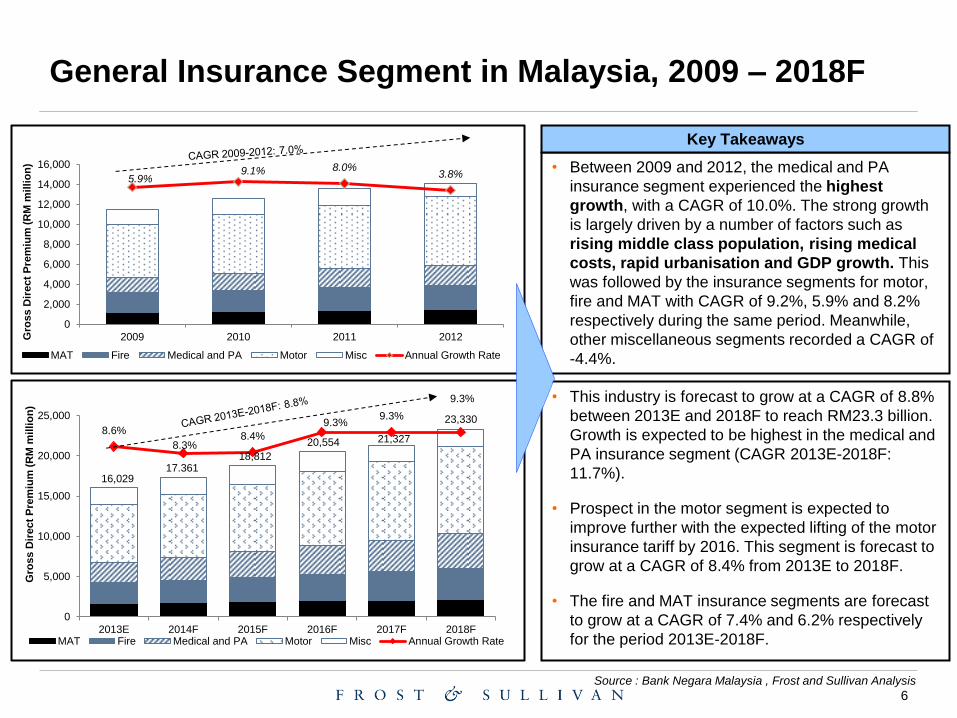

• Between 2009 and 2012, the medical and PA

insurance segment experienced the highest

growth, with a CAGR of 10.0%. The strong growth

is largely driven by a number of factors such as

rising middle class population, rising medical

costs, rapid urbanisation and GDP growth. This

was followed by the insurance segments for motor,

fire and MAT with CAGR of 9.2%, 5.9% and 8.2%

respectively during the same period. Meanwhile,

other miscellaneous segments recorded a CAGR of

-4.4%.

Key Takeaways

• This industry is forecast to grow at a CAGR of 8.8%

between 2013E and 2018F to reach RM23.3 billion.

Growth is expected to be highest in the medical and

PA insurance segment (CAGR 2013E-2018F:

11.7%).

• Prospect in the motor segment is expected to

improve further with the expected lifting of the motor

insurance tariff by 2016. This segment is forecast to

grow at a CAGR of 8.4% from 2013E to 2018F.

• The fire and MAT insurance segments are forecast

to grow at a CAGR of 7.4% and 6.2% respectively

for the period 2013E-2018F.

General Insurance Segment in Malaysia, 2009 – 2018F

5.9% 9.1% 8.0%

3.8%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2009 2010 2011 2012Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

MAT Fire Medical and PA Motor Misc Annual Growth Rate

16,029 17.361

18,812

20,554 21,327

23,330 8.6%

8.3% 8.4%

9.3% 9.3%

9.3%

0

5,000

10,000

15,000

20,000

25,000

2013E 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

MAT Fire Medical and PA Motor Misc Annual Growth Rate

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

7

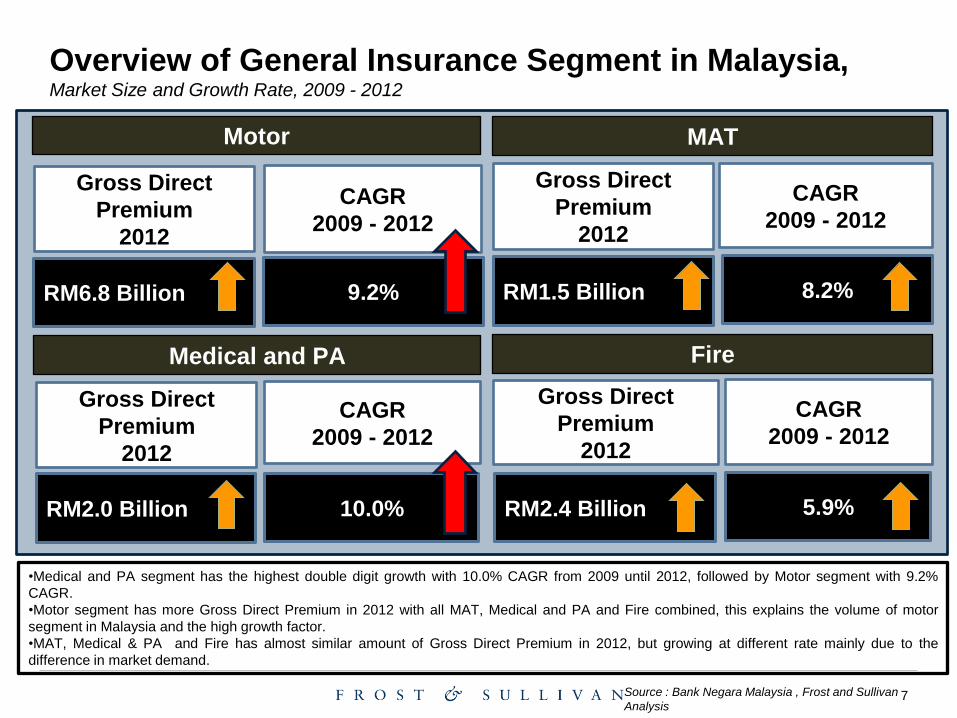

Overview of General Insurance Segment in Malaysia, Market Size and Growth Rate, 2009 - 2012

Gross Direct

Premium

2012

RM6.8 Billion

Motor

CAGR

2009 - 2012

9.2%

Gross Direct

Premium

2012

RM2.0 Billion

Medical and PA

CAGR

2009 - 2012

10.0%

Gross Direct

Premium

2012

RM1.5 Billion

MAT

CAGR

2009 - 2012

8.2%

Gross Direct

Premium

2012

RM2.4 Billion

Fire

CAGR

2009 - 2012

5.9%

•Medical and PA segment has the highest double digit growth with 10.0% CAGR from 2009 until 2012, followed by Motor segment with 9.2%

CAGR.

•Motor segment has more Gross Direct Premium in 2012 with all MAT, Medical and PA and Fire combined, this explains the volume of motor

segment in Malaysia and the high growth factor.

•MAT, Medical & PA and Fire has almost similar amount of Gross Direct Premium in 2012, but growing at different rate mainly due to the

difference in market demand.

Source : Bank Negara Malaysia , Frost and Sullivan

Analysis

8

0

2,000

4,000

6,000

8,000

10,000

12,000

2009 2010 2011 2012 2013E 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

Motor

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2009 2010 2011 2012 2013E 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

Medical and PA

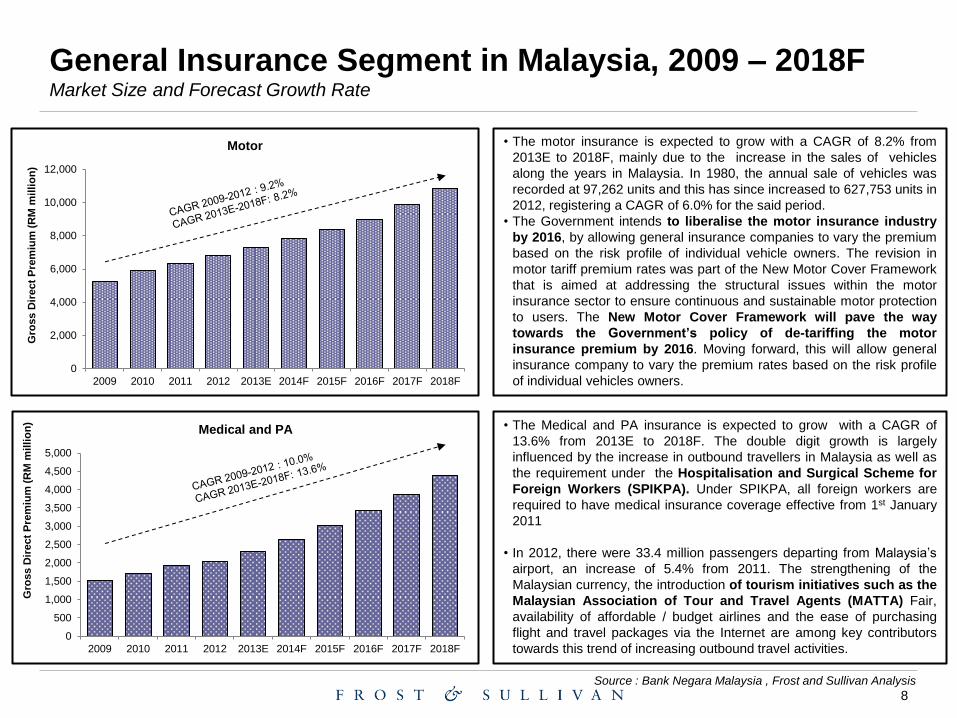

• The motor insurance is expected to grow with a CAGR of 8.2% from

2013E to 2018F, mainly due to the increase in the sales of vehicles

along the years in Malaysia. In 1980, the annual sale of vehicles was

recorded at 97,262 units and this has since increased to 627,753 units in

2012, registering a CAGR of 6.0% for the said period.

• The Government intends to liberalise the motor insurance industry

by 2016, by allowing general insurance companies to vary the premium

based on the risk profile of individual vehicle owners. The revision in

motor tariff premium rates was part of the New Motor Cover Framework

that is aimed at addressing the structural issues within the motor

insurance sector to ensure continuous and sustainable motor protection

to users. The New Motor Cover Framework will pave the way

towards the Government’s policy of de-tariffing the motor

insurance premium by 2016. Moving forward, this will allow general

insurance company to vary the premium rates based on the risk profile

of individual vehicles owners.

• The Medical and PA insurance is expected to grow with a CAGR of

13.6% from 2013E to 2018F. The double digit growth is largely

influenced by the increase in outbound travellers in Malaysia as well as

the requirement under the Hospitalisation and Surgical Scheme for

Foreign Workers (SPIKPA). Under SPIKPA, all foreign workers are

required to have medical insurance coverage effective from 1st January

2011

• In 2012, there were 33.4 million passengers departing from Malaysia’s

airport, an increase of 5.4% from 2011. The strengthening of the

Malaysian currency, the introduction of tourism initiatives such as the

Malaysian Association of Tour and Travel Agents (MATTA) Fair,

availability of affordable / budget airlines and the ease of purchasing

flight and travel packages via the Internet are among key contributors

towards this trend of increasing outbound travel activities.

General Insurance Segment in Malaysia, 2009 – 2018F Market Size and Forecast Growth Rate

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

9

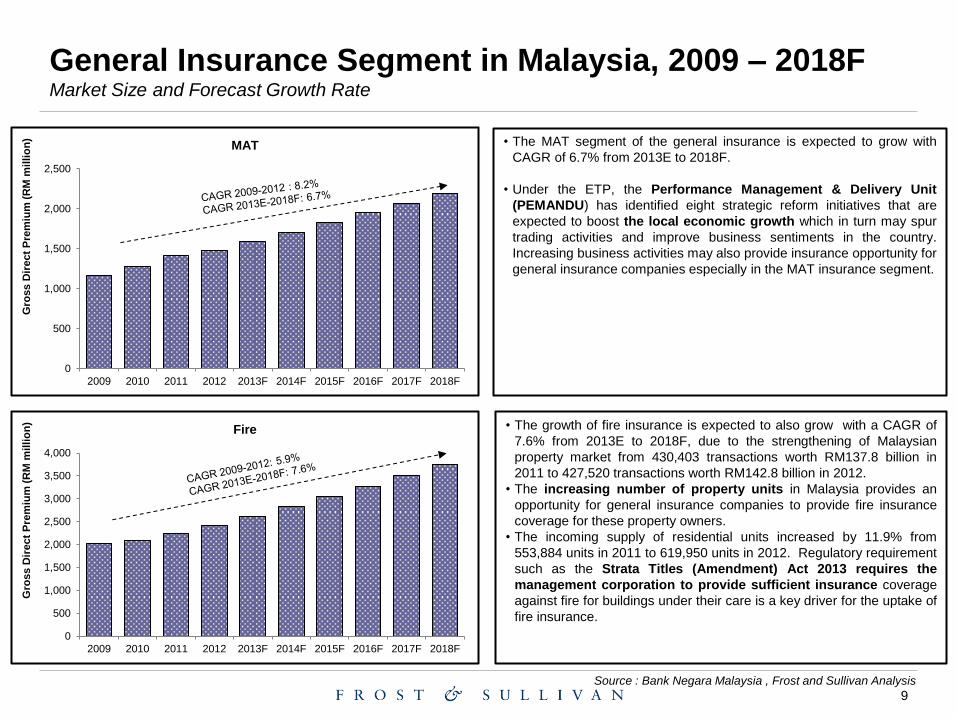

• The growth of fire insurance is expected to also grow with a CAGR of

7.6% from 2013E to 2018F, due to the strengthening of Malaysian

property market from 430,403 transactions worth RM137.8 billion in

2011 to 427,520 transactions worth RM142.8 billion in 2012.

• The increasing number of property units in Malaysia provides an

opportunity for general insurance companies to provide fire insurance

coverage for these property owners.

• The incoming supply of residential units increased by 11.9% from

553,884 units in 2011 to 619,950 units in 2012. Regulatory requirement

such as the Strata Titles (Amendment) Act 2013 requires the

management corporation to provide sufficient insurance coverage

against fire for buildings under their care is a key driver for the uptake of

fire insurance.

General Insurance Segment in Malaysia, 2009 – 2018F Market Size and Forecast Growth Rate

0

500

1,000

1,500

2,000

2,500

2009 2010 2011 2012 2013F 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

MAT

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2009 2010 2011 2012 2013F 2014F 2015F 2016F 2017F 2018F

Gro

ss D

irect

Pre

miu

m (

RM

mil

lio

n)

Fire

• The MAT segment of the general insurance is expected to grow with

CAGR of 6.7% from 2013E to 2018F.

• Under the ETP, the Performance Management & Delivery Unit

(PEMANDU) has identified eight strategic reform initiatives that are

expected to boost the local economic growth which in turn may spur

trading activities and improve business sentiments in the country.

Increasing business activities may also provide insurance opportunity for

general insurance companies especially in the MAT insurance segment.

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

10

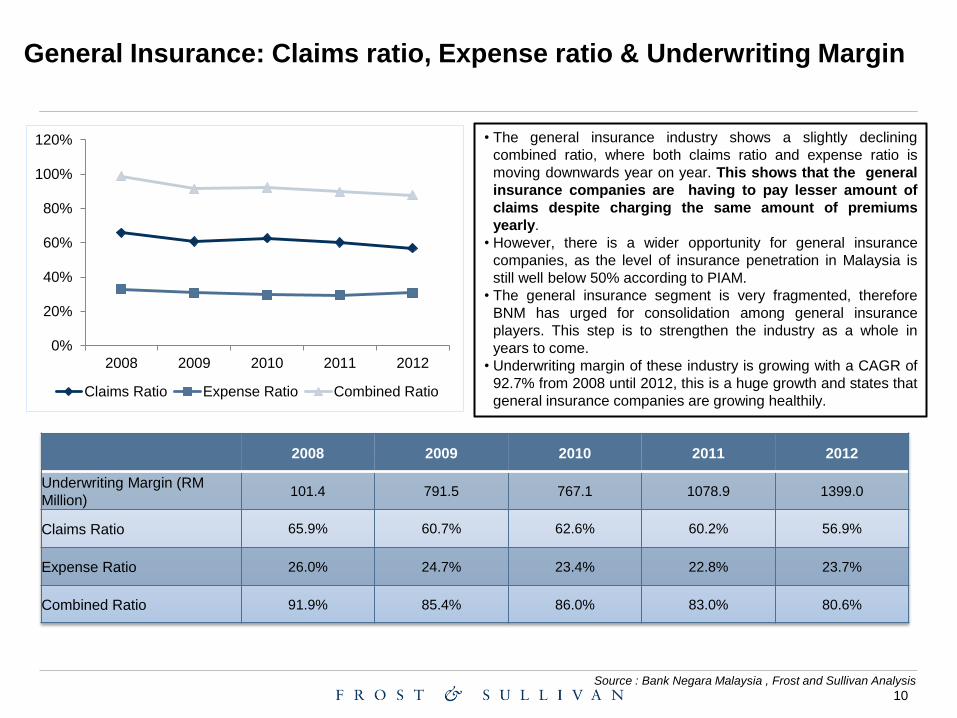

General Insurance: Claims ratio, Expense ratio & Underwriting Margin

2008 2009 2010 2011 2012

Underwriting Margin (RM

Million) 101.4 791.5 767.1 1078.9 1399.0

Claims Ratio 65.9% 60.7% 62.6% 60.2% 56.9%

Expense Ratio 26.0% 24.7% 23.4% 22.8% 23.7%

Combined Ratio 91.9% 85.4% 86.0% 83.0% 80.6%

0%

20%

40%

60%

80%

100%

120%

2008 2009 2010 2011 2012

Claims Ratio Expense Ratio Combined Ratio

• The general insurance industry shows a slightly declining

combined ratio, where both claims ratio and expense ratio is

moving downwards year on year. This shows that the general

insurance companies are having to pay lesser amount of

claims despite charging the same amount of premiums

yearly.

• However, there is a wider opportunity for general insurance

companies, as the level of insurance penetration in Malaysia is

still well below 50% according to PIAM.

• The general insurance segment is very fragmented, therefore

BNM has urged for consolidation among general insurance

players. This step is to strengthen the industry as a whole in

years to come.

• Underwriting margin of these industry is growing with a CAGR of

92.7% from 2008 until 2012, this is a huge growth and states that

general insurance companies are growing healthily.

Source : Bank Negara Malaysia , Frost and Sullivan Analysis

11

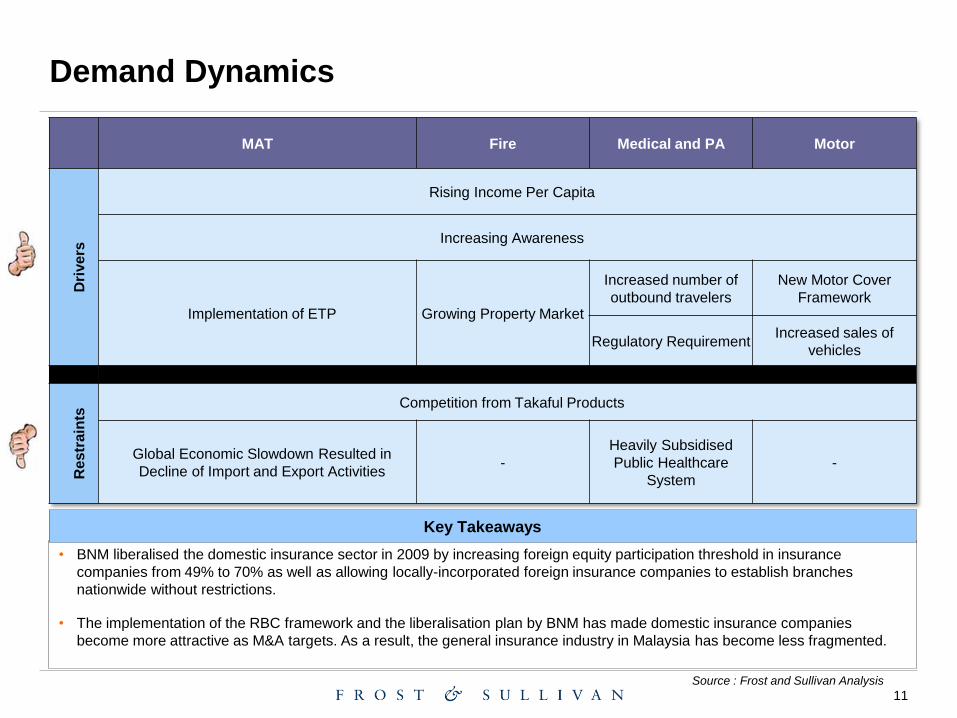

MAT Fire Medical and PA Motor

Dri

ve

rs

Rising Income Per Capita

Increasing Awareness

Implementation of ETP Growing Property Market

Increased number of

outbound travelers

New Motor Cover

Framework

Regulatory Requirement Increased sales of

vehicles

Re

str

ain

ts Competition from Takaful Products

Global Economic Slowdown Resulted in

Decline of Import and Export Activities -

Heavily Subsidised

Public Healthcare

System

-

• BNM liberalised the domestic insurance sector in 2009 by increasing foreign equity participation threshold in insurance

companies from 49% to 70% as well as allowing locally-incorporated foreign insurance companies to establish branches

nationwide without restrictions.

• The implementation of the RBC framework and the liberalisation plan by BNM has made domestic insurance companies

become more attractive as M&A targets. As a result, the general insurance industry in Malaysia has become less fragmented.

Key Takeaways

Demand Dynamics

Source : Frost and Sullivan Analysis

12

Source: Frost & Sullivan analysis.

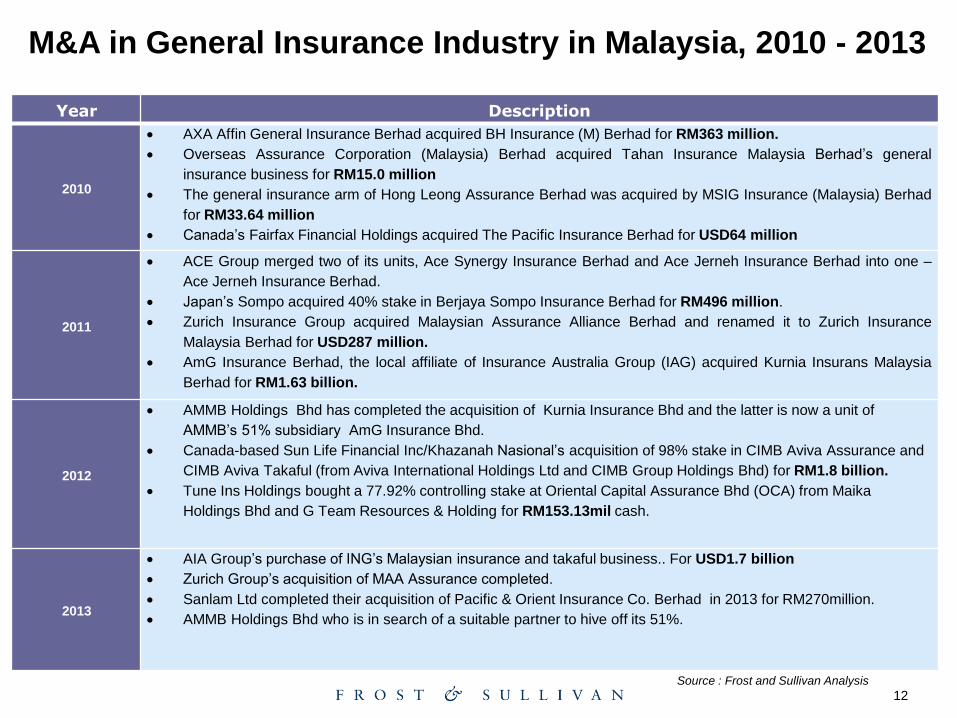

Year Description

2010

AXA Affin General Insurance Berhad acquired BH Insurance (M) Berhad for RM363 million.

Overseas Assurance Corporation (Malaysia) Berhad acquired Tahan Insurance Malaysia Berhad’s general

insurance business for RM15.0 million

The general insurance arm of Hong Leong Assurance Berhad was acquired by MSIG Insurance (Malaysia) Berhad

for RM33.64 million

Canada’s Fairfax Financial Holdings acquired The Pacific Insurance Berhad for USD64 million

2011

ACE Group merged two of its units, Ace Synergy Insurance Berhad and Ace Jerneh Insurance Berhad into one –

Ace Jerneh Insurance Berhad.

Japan’s Sompo acquired 40% stake in Berjaya Sompo Insurance Berhad for RM496 million.

Zurich Insurance Group acquired Malaysian Assurance Alliance Berhad and renamed it to Zurich Insurance

Malaysia Berhad for USD287 million.

AmG Insurance Berhad, the local affiliate of Insurance Australia Group (IAG) acquired Kurnia Insurans Malaysia

Berhad for RM1.63 billion.

2012

AMMB Holdings Bhd has completed the acquisition of Kurnia Insurance Bhd and the latter is now a unit of

AMMB’s 51% subsidiary AmG Insurance Bhd.

Canada-based Sun Life Financial Inc/Khazanah Nasional’s acquisition of 98% stake in CIMB Aviva Assurance and

CIMB Aviva Takaful (from Aviva International Holdings Ltd and CIMB Group Holdings Bhd) for RM1.8 billion.

Tune Ins Holdings bought a 77.92% controlling stake at Oriental Capital Assurance Bhd (OCA) from Maika

Holdings Bhd and G Team Resources & Holding for RM153.13mil cash.

2013

AIA Group’s purchase of ING’s Malaysian insurance and takaful business.. For USD1.7 billion

Zurich Group’s acquisition of MAA Assurance completed.

Sanlam Ltd completed their acquisition of Pacific & Orient Insurance Co. Berhad in 2013 for RM270million.

AMMB Holdings Bhd who is in search of a suitable partner to hive off its 51%.

M&A in General Insurance Industry in Malaysia, 2010 - 2013

Source : Frost and Sullivan Analysis

13

THANK YOU For Full Slide Deck please contact

Business & Financial Services Department

Malaysia