Embed Size (px)

Citation preview

Un

sa

ve

d D

ocu

me

nt / 7

/11

/20

13

/ 2

2:5

5

Essar – Lets Begin

Madhu Vuppuluri, CEO, Essar Americas

IMM Conference, November 11, 2013

Un

sa

ve

d D

ocu

me

nt / 7

/11

/20

13

/ 2

2:5

5

Essar Global Overview

PRIVATE & CONFIDENTIAL

Leading Business Group with Globally Diversified Operations

Oil & Gas

2,034 MMBOE reserves

36 MMTPA refineries

1,400 retail outlets

Power

455 MT coal reserves

3,910 MW operational capacity

Going up to 6,700 MW by 2014

Shipping***26 ships, 15 rigs incl. semisubmersible and 4,200 chartered trucks

BPO55 global Aegis locations

Real Estate~16 Mn Sq ft. Portfolio in residential, commercial and mixed use projects

Telecom ServicesGSM services in Kenya 900 branded retail outlets

Projects

Engineering, Procurement & Construction

2nd largest equipment bank in India

Ports***

104 MTPA operational capacity

181 MTPA planned capacity

Resources

2 Bn tonnes of reserves

27 MTPA pellet capacity

172 MT coal reserves

Steel Making & Marketing

14 MTPA steel-making capacity

5 MTPA processing and distribution capacity

350 retail outlets

Energy ** Infrastructure ServicesSteel

2

73000 Employees, Presence in 25 countries with Revenues of US$ 35 Bn

** Listed on LSE ***Listed on BSE & NSE

PRIVATE & CONFIDENTIAL

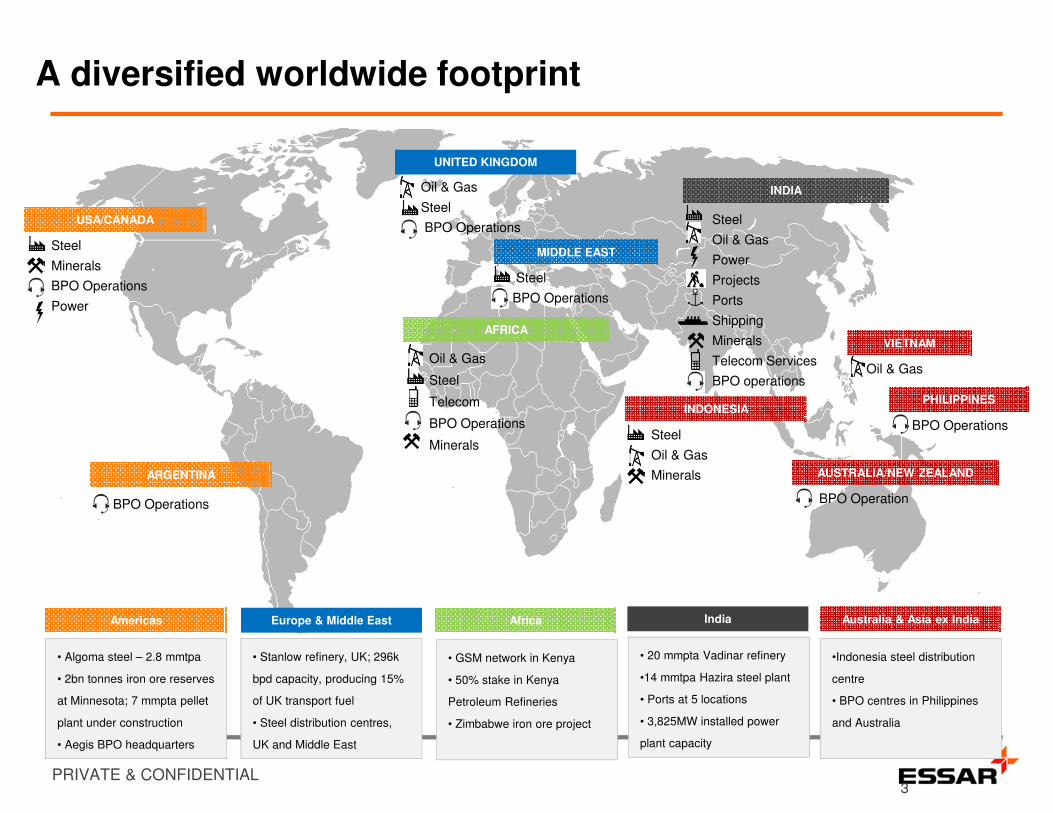

A diversified worldwide footprint

USA/CANADA

Steel

Minerals

BPO Operations

Power

AFRICA

Oil & Gas

Steel

Telecom

BPO Operations

Minerals

INDONESIA

Steel

Oil & Gas

Minerals

INDIA

Steel

Oil & Gas

Power

Projects

Ports

Shipping

Minerals

Telecom Services

BPO operations

UNITED KINGDOM

Oil & Gas

Steel

BPO Operations

AUSTRALIA/NEW ZEALAND

BPO Operation

MIDDLE EAST

Steel

BPO Operations

VIETNAM

Oil & Gas

PHILIPPINES

BPO Operations

ARGENTINA

BPO Operations

Americas Europe & Middle East IndiaAfrica Australia & Asia ex India

• Algoma steel – 2.8 mmtpa

• 2bn tonnes iron ore reserves

at Minnesota; 7 mmpta pellet

plant under construction

• Aegis BPO headquarters

• Stanlow refinery, UK; 296k

bpd capacity, producing 15%

of UK transport fuel

• Steel distribution centres,

UK and Middle East

• 20 mmpta Vadinar refinery

•14 mmtpa Hazira steel plant

• Ports at 5 locations

• 3,825MW installed power

plant capacity

• GSM network in Kenya

• 50% stake in Kenya

Petroleum Refineries

• Zimbabwe iron ore project

•Indonesia steel distribution

centre

• BPO centres in Philippines

and Australia

3

Un

sa

ve

d D

ocu

me

nt / 7

/11

/20

13

/ 2

2:5

5

Addressing global overcapacity challenges

PRIVATE & CONFIDENTIAL

Global Steel Market Outlook

� Global capacity utilization increased from 75% in August’13 to 79% in September’13. The increase

is significantly higher than the seasonal 1-2% increase in capacity utilization in the month of

September in the past few years.

� Flat steel prices recovered in Q3 2013 with a 7% q-o-q increase in U.S. Domestic HRC prices, 8%

increase in China HRC export prices and 4% increase in China HRC domestic prices.

� Low inventories in China and U.S. reflect an end to destocking in Q3’13 and overall pricing outlook

is favorable for the steel industry.

� Recent price increases in finished products coupled with stable raw material prices is expected to

increase profitability of steelmakers in the near term.

� Positive Global economic indicators in U.S., Europe and China strongly point towards a recovery of

steel market in the near term.

� Overcapacity, especially in China continues to remains the biggest threat for steel industry in the

near future. The pace and extent of execution of capacity reduction plan in China will have a strong

impact of global steel industry in the next few years.

5

PRIVATE & CONFIDENTIAL

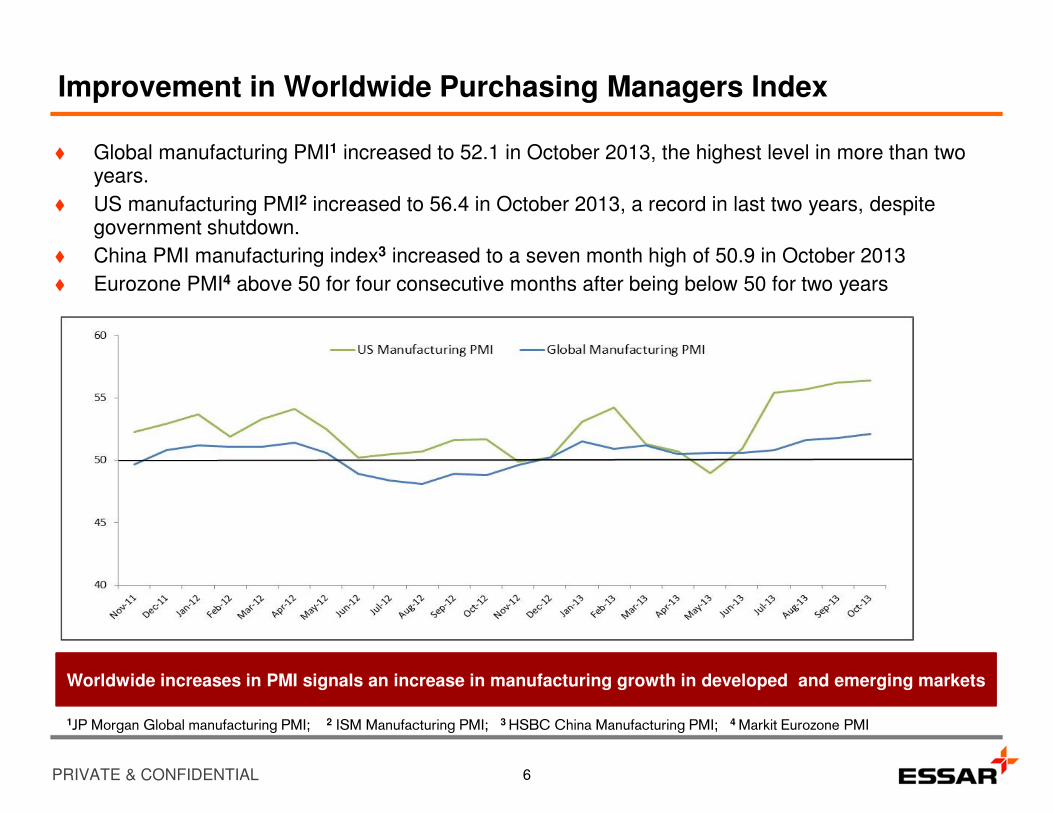

Improvement in Worldwide Purchasing Managers Index

� Global manufacturing PMI1 increased to 52.1 in October 2013, the highest level in more than two years.

� US manufacturing PMI2 increased to 56.4 in October 2013, a record in last two years, despite government shutdown.

� China PMI manufacturing index3 increased to a seven month high of 50.9 in October 2013

� Eurozone PMI4 above 50 for four consecutive months after being below 50 for two years

6

Worldwide increases in PMI signals an increase in manufacturing growth in developed and emerging markets

1JP Morgan Global manufacturing PMI; 2 ISM Manufacturing PMI; 3 HSBC China Manufacturing PMI; 4 Markit Eurozone PMI

PRIVATE & CONFIDENTIAL

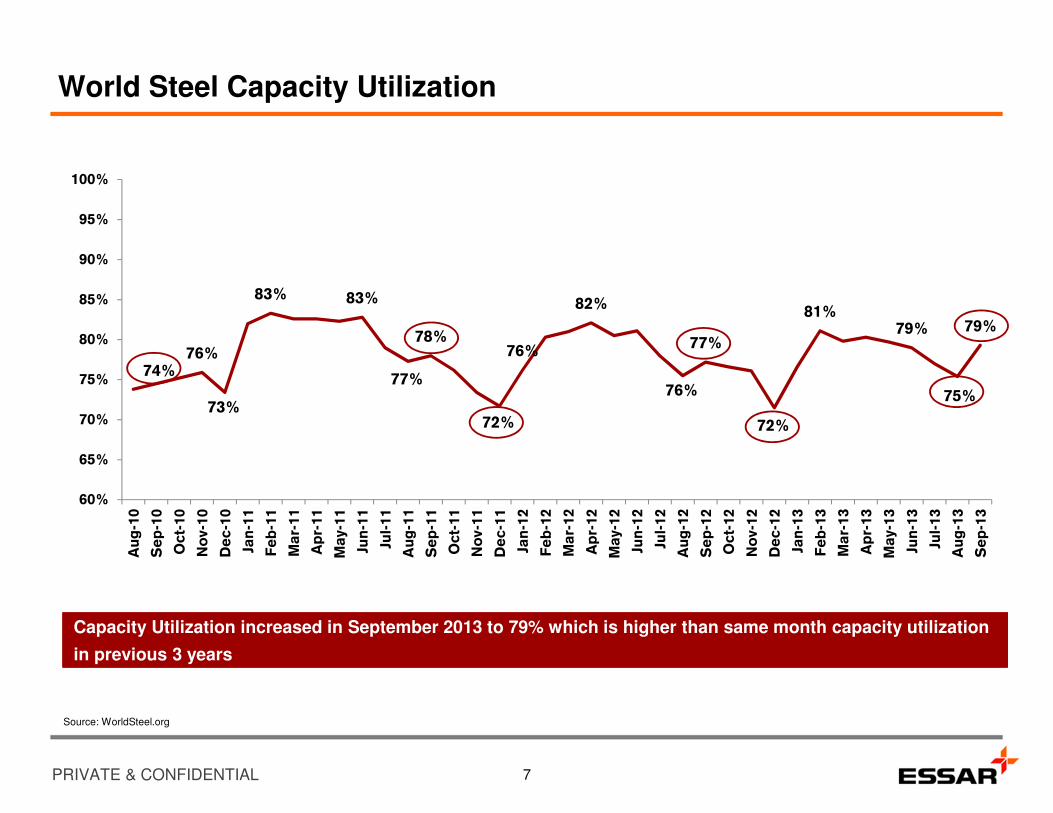

World Steel Capacity Utilization

7

Source: WorldSteel.org

Capacity Utilization increased in September 2013 to 79% which is higher than same month capacity utilization

in previous 3 years

74%76%

73%

83% 83%

77%

78%

72%

76%

82%

76%

77%

72%

81%79%

75%

79%

60%

65%

70%

75%

80%

85%

90%

95%

100%

Au

g-1

0

Se

p-1

0

Oct-

10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-11

Ap

r-11

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct-

11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-12

Ap

r-12

Ma

y-1

2

Jun

-12

Jul-

12

Au

g-1

2

Se

p-1

2

Oct-

12

No

v-1

2

De

c-1

2

Jan

-13

Fe

b-1

3

Ma

r-13

Ap

r-13

Ma

y-1

3

Jun

-13

Jul-

13

Au

g-1

3

Se

p-1

3

PRIVATE & CONFIDENTIAL

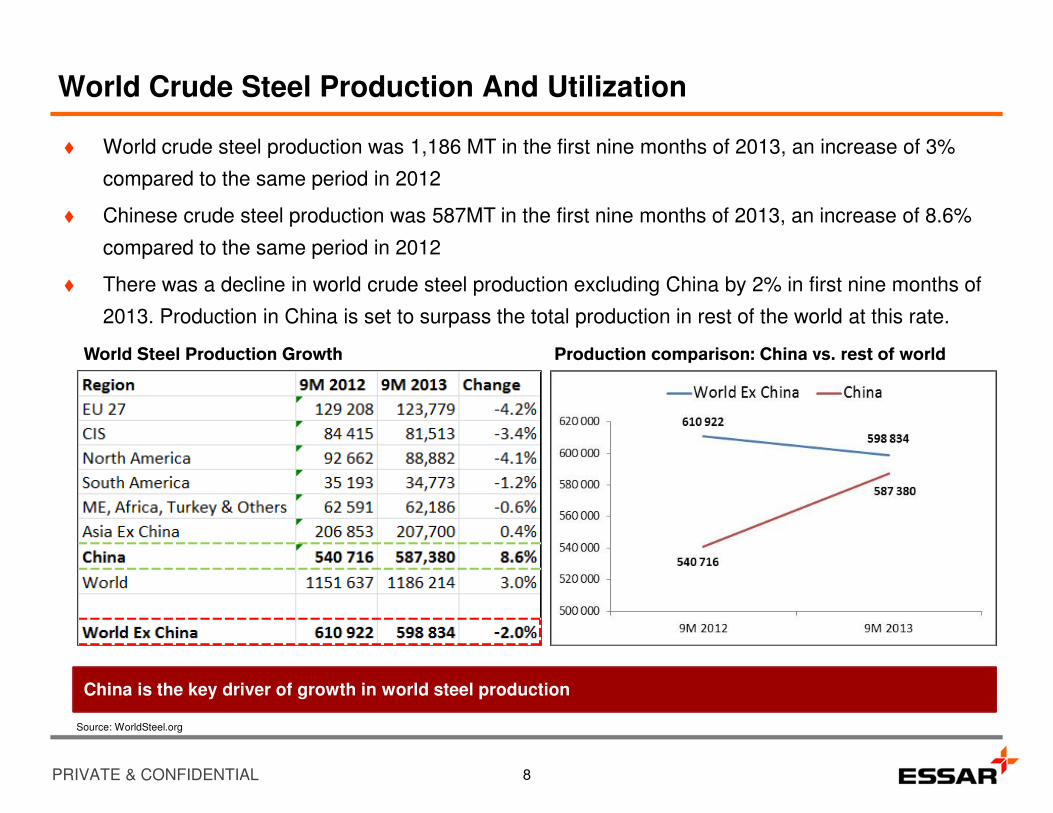

World Crude Steel Production And Utilization

� World crude steel production was 1,186 MT in the first nine months of 2013, an increase of 3%

compared to the same period in 2012

� Chinese crude steel production was 587MT in the first nine months of 2013, an increase of 8.6%

compared to the same period in 2012

� There was a decline in world crude steel production excluding China by 2% in first nine months of

2013. Production in China is set to surpass the total production in rest of the world at this rate.

8

World Steel Production Growth Production comparison: China vs. rest of world

China is the key driver of growth in world steel production

Source: WorldSteel.org

PRIVATE & CONFIDENTIAL

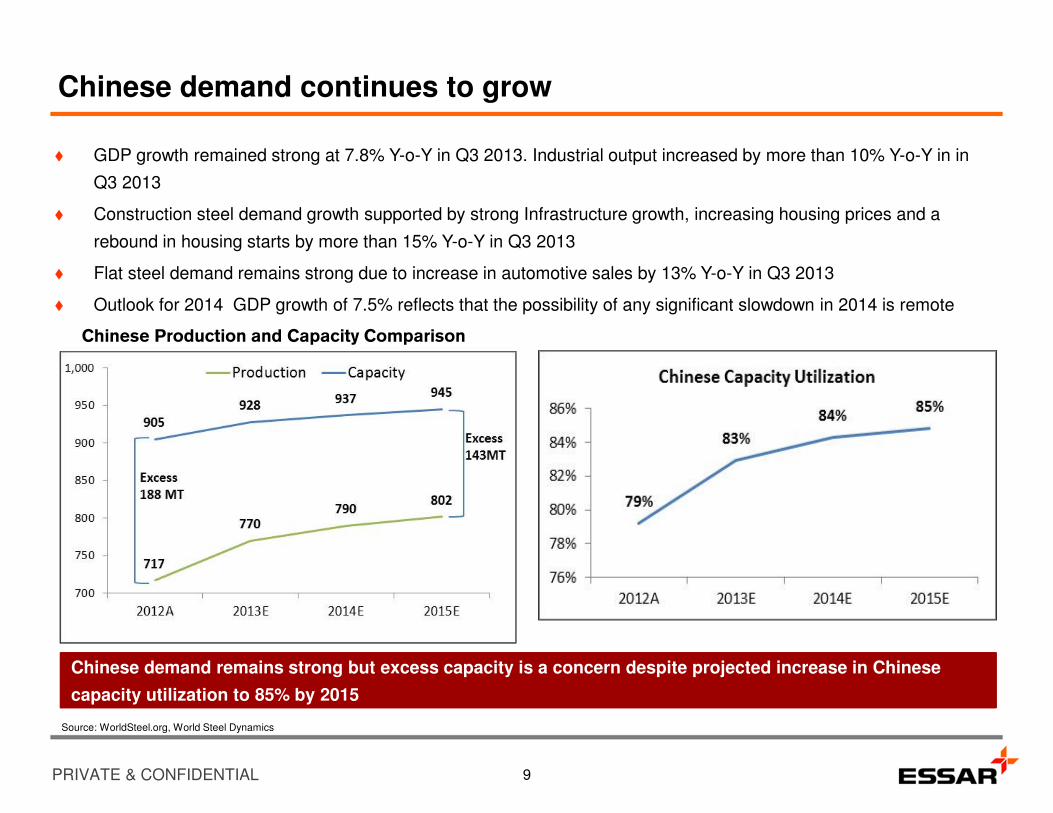

Chinese demand continues to grow

� GDP growth remained strong at 7.8% Y-o-Y in Q3 2013. Industrial output increased by more than 10% Y-o-Y in in

Q3 2013

� Construction steel demand growth supported by strong Infrastructure growth, increasing housing prices and a

rebound in housing starts by more than 15% Y-o-Y in Q3 2013

� Flat steel demand remains strong due to increase in automotive sales by 13% Y-o-Y in Q3 2013

� Outlook for 2014 GDP growth of 7.5% reflects that the possibility of any significant slowdown in 2014 is remote

9

Chinese Production and Capacity Comparison

Chinese demand remains strong but excess capacity is a concern despite projected increase in Chinese

capacity utilization to 85% by 2015

Source: WorldSteel.org, World Steel Dynamics

PRIVATE & CONFIDENTIAL

Chinese Steelmaking Capacity

� China's effective steelmaking capacity is still rising despite significant overcapacity.

� In 2013, crude steel capacity is estimated to be about 928 million tonnes, up 23 million tonnes from

2012 and by 2015, capacity may rise another 17 million tonnes to 945 million tonnes.

� Overcapacity is estimated at ~160 MTPA at present, consisting of 90 MTPA for long products , 40

MTPA for steel sheet products and 20 MTPA for plates.

� Capacity reduction goals will be difficult to achieve since all but four of China's larger steel

companies are partly owned by municipalities. As the objective of municipalities is maximization of

employment, output and tax revenues, they will maintain their resistance to capacity reduction

plans.

� Due to sizable oversupply and low domestic price for hot-rolled band, Chinese mills have put

downward price pressure in the export markets in the last few years.

� Consolidation is happening at a very slow pace. By 2020, the top 4 steel mills are expected to

have a market share of 35% versus 28% in 2012; for the top 10, the estimate is 60% and 48%,

respectively.

10

Chinese overcapacity will continue to remain the biggest threat for steel industry in the near future

Source: World Steel Dynamics

Un

sa

ve

d D

ocu

me

nt / 7

/11

/20

13

/ 2

2:5

5

North American Steel Market

PRIVATE & CONFIDENTIAL

Current North American Industry Scenario: Flat Products

� 2013 estimated North American (US & Canada only) flat roll consumption – 80 million NT

� Average USD YTD 2013 HRC price - $620/NT

� Flat Roll Capacity

– HSM – 95.5 million NT

– Reversing Plate Mill – 7 million NT

– Steckle Mill – 6.5 million NT

� YTD 2013 2013 Raw Steel Capacity Utilization averaging 77.2%, currently 76.5%

12

PRIVATE & CONFIDENTIAL

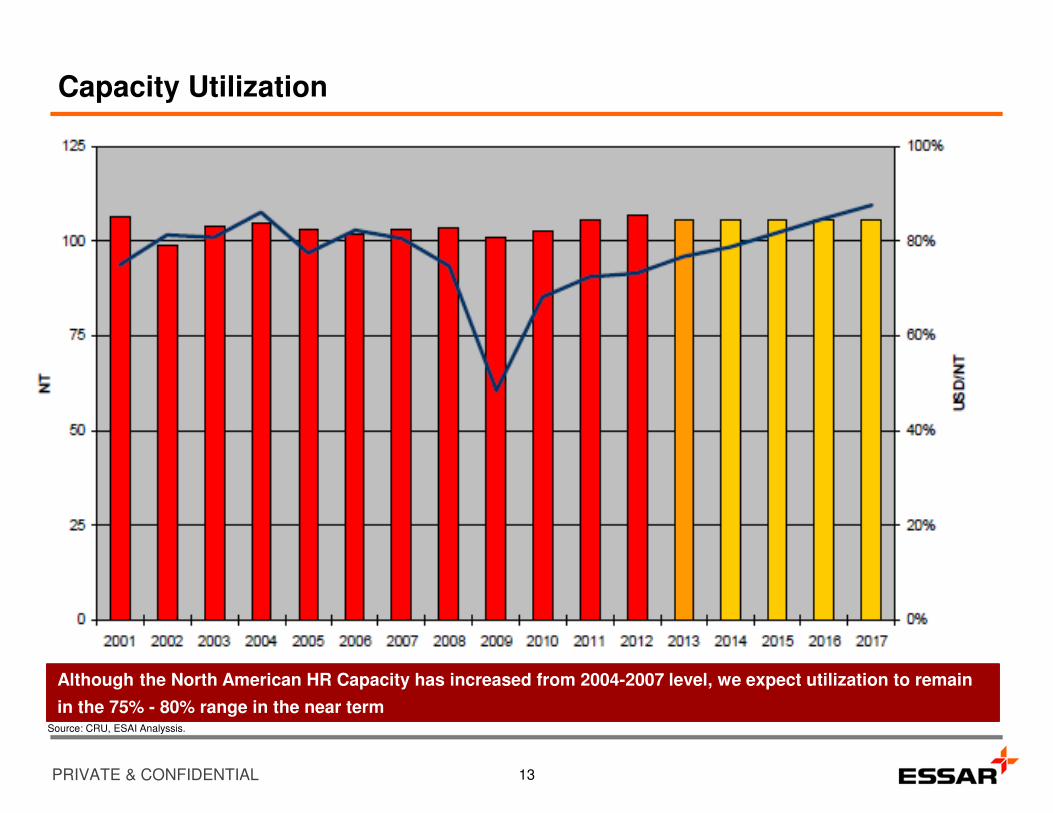

Capacity Utilization

13

Although the North American HR Capacity has increased from 2004-2007 level, we expect utilization to remain

in the 75% - 80% range in the near termSource: CRU, ESAI Analyssis.

PRIVATE & CONFIDENTIAL

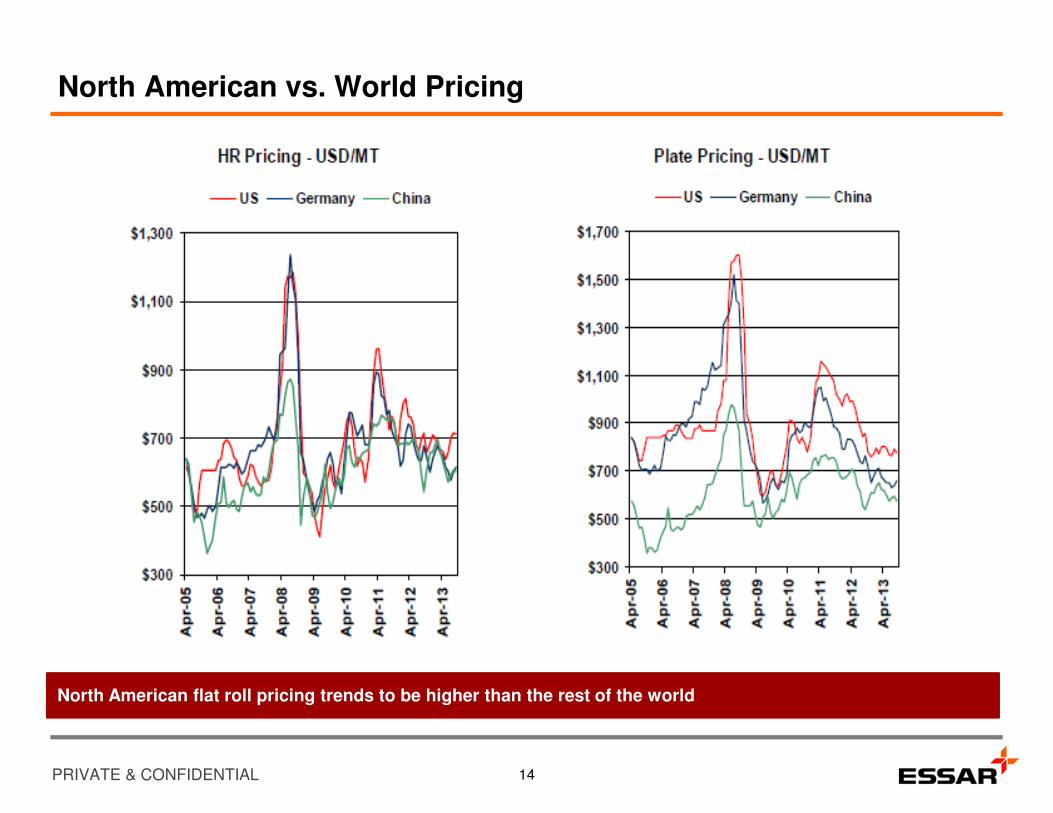

North American vs. World Pricing

14

North American flat roll pricing trends to be higher than the rest of the world

PRIVATE & CONFIDENTIAL

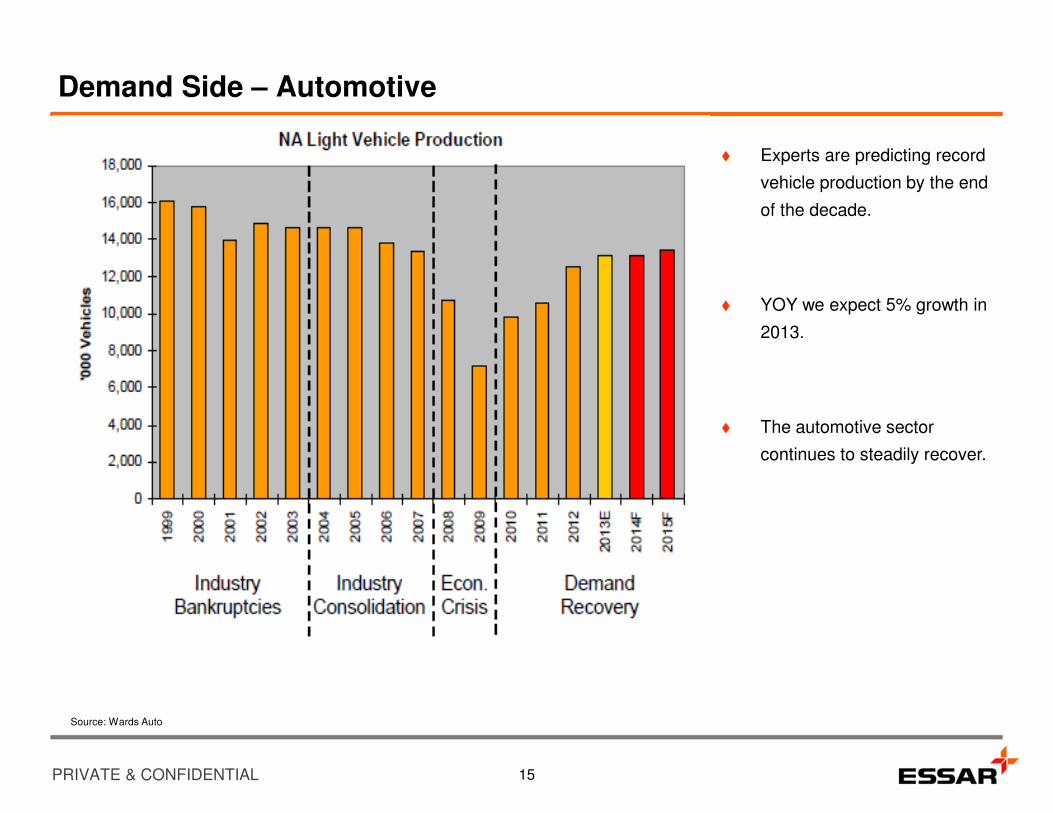

Demand Side – Automotive

15

� Experts are predicting record

vehicle production by the end

of the decade.

� YOY we expect 5% growth in

2013.

� The automotive sector

continues to steadily recover.

Source: Wards Auto

PRIVATE & CONFIDENTIAL

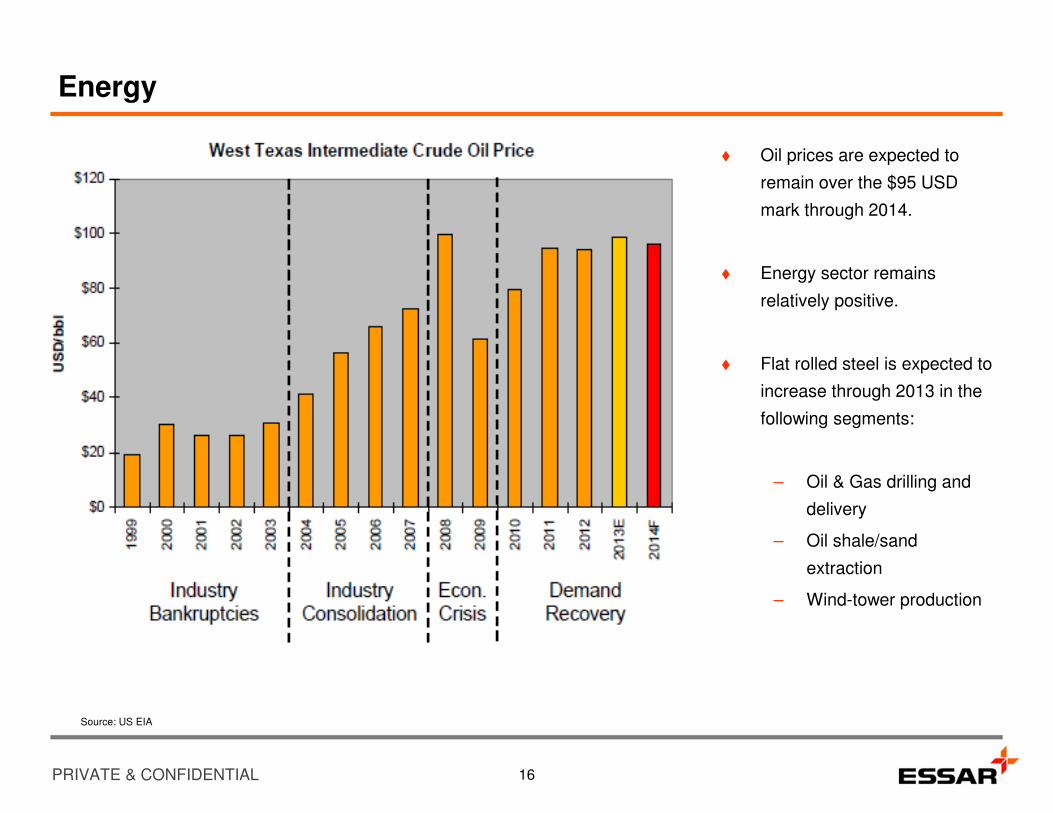

Energy

16

� Oil prices are expected to

remain over the $95 USD

mark through 2014.

� Energy sector remains

relatively positive.

� Flat rolled steel is expected to

increase through 2013 in the

following segments:

– Oil & Gas drilling and

delivery

– Oil shale/sand

extraction

– Wind-tower production

Source: US EIA

PRIVATE & CONFIDENTIAL

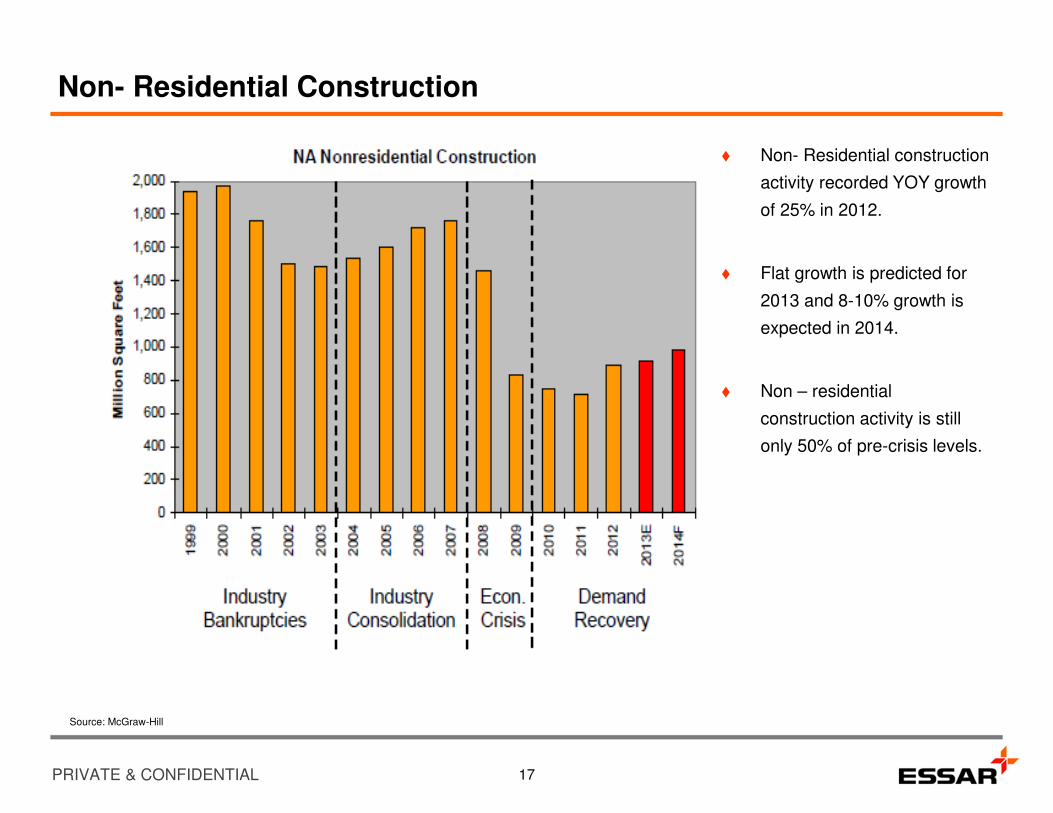

Non- Residential Construction

17

� Non- Residential construction

activity recorded YOY growth

of 25% in 2012.

� Flat growth is predicted for

2013 and 8-10% growth is

expected in 2014.

� Non – residential

construction activity is still

only 50% of pre-crisis levels.

Source: McGraw-Hill

PRIVATE & CONFIDENTIAL

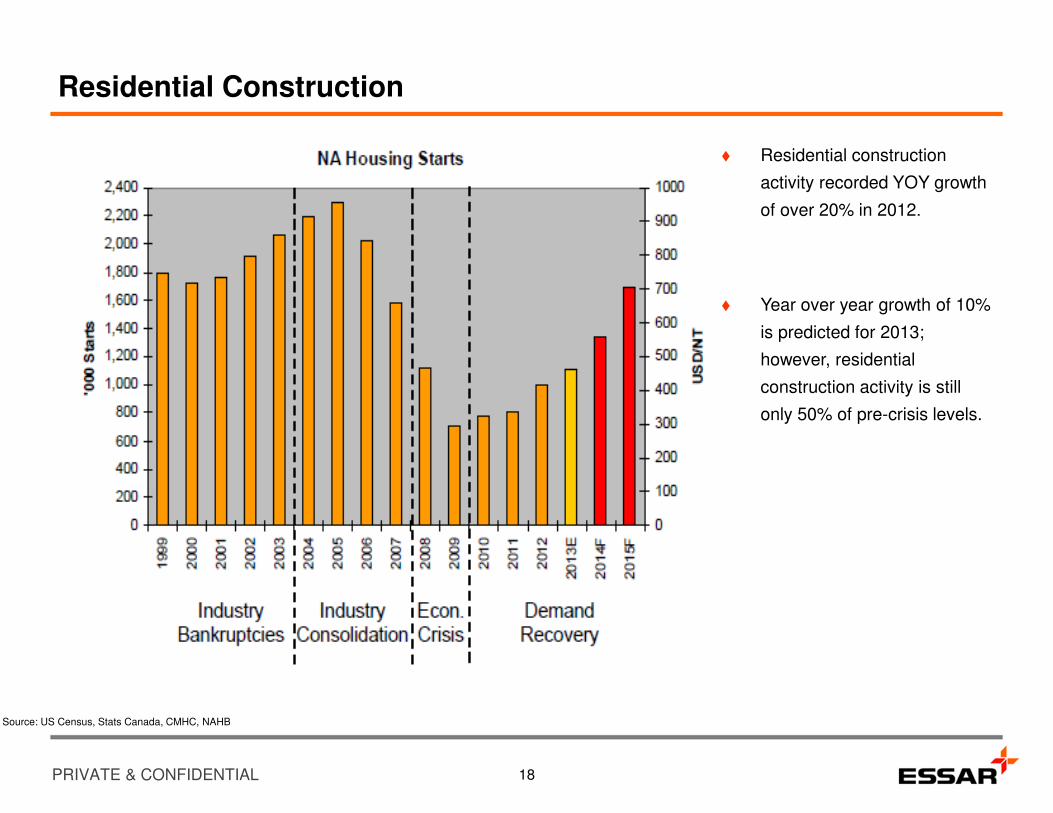

Residential Construction

18

� Residential construction

activity recorded YOY growth

of over 20% in 2012.

� Year over year growth of 10%

is predicted for 2013;

however, residential

construction activity is still

only 50% of pre-crisis levels.

Source: US Census, Stats Canada, CMHC, NAHB

Un

sa

ve

d D

ocu

me

nt / 7

/11

/20

13

/ 2

2:5

5

Essar Steel Minnesota Overview

PRIVATE & CONFIDENTIAL

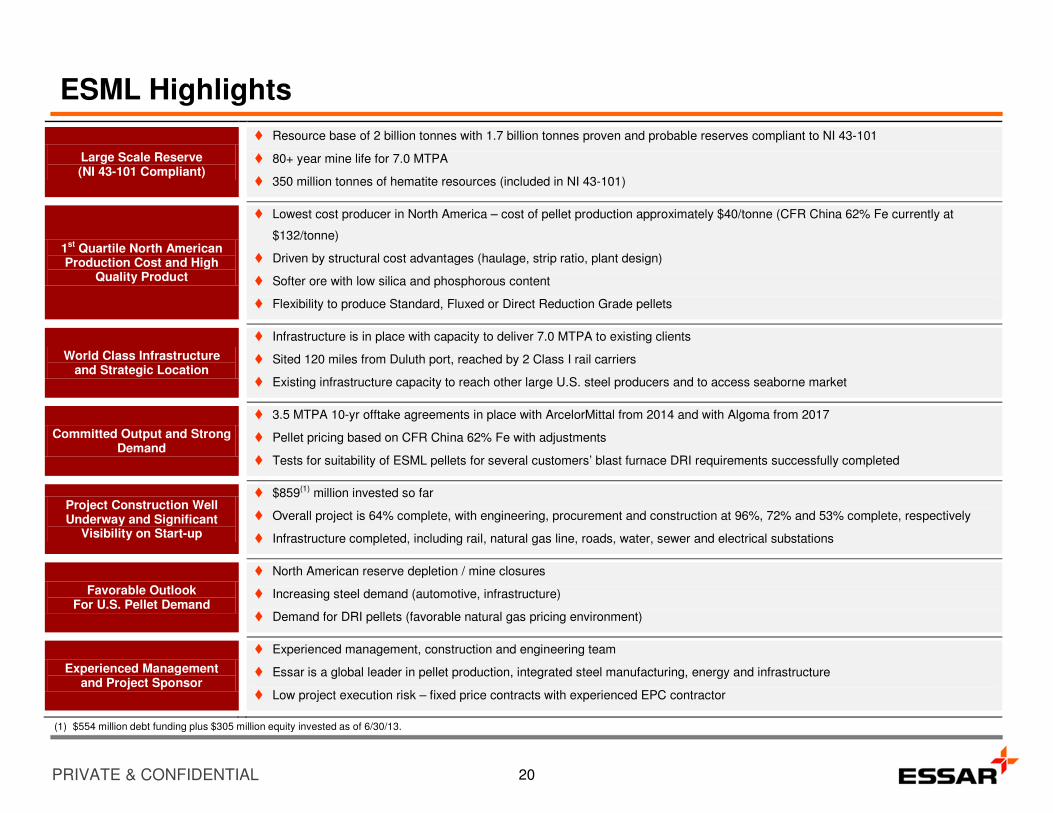

ESML Highlights

Large Scale Reserve (NI 43-101 Compliant)

� Resource base of 2 billion tonnes with 1.7 billion tonnes proven and probable reserves compliant to NI 43-101

� 80+ year mine life for 7.0 MTPA

� 350 million tonnes of hematite resources (included in NI 43-101)

1st Quartile North American Production Cost and High

Quality Product

� Lowest cost producer in North America – cost of pellet production approximately $40/tonne (CFR China 62% Fe currently at

$132/tonne)

� Driven by structural cost advantages (haulage, strip ratio, plant design)

� Softer ore with low silica and phosphorous content

� Flexibility to produce Standard, Fluxed or Direct Reduction Grade pellets

World Class Infrastructure and Strategic Location

� Infrastructure is in place with capacity to deliver 7.0 MTPA to existing clients

� Sited 120 miles from Duluth port, reached by 2 Class I rail carriers

� Existing infrastructure capacity to reach other large U.S. steel producers and to access seaborne market

Committed Output and Strong Demand

� 3.5 MTPA 10-yr offtake agreements in place with ArcelorMittal from 2014 and with Algoma from 2017

� Pellet pricing based on CFR China 62% Fe with adjustments

� Tests for suitability of ESML pellets for several customers’ blast furnace DRI requirements successfully completed

Project Construction Well Underway and Significant

Visibility on Start-up

� $859(1) million invested so far

� Overall project is 64% complete, with engineering, procurement and construction at 96%, 72% and 53% complete, respectively

� Infrastructure completed, including rail, natural gas line, roads, water, sewer and electrical substations

Favorable Outlook For U.S. Pellet Demand

� North American reserve depletion / mine closures

� Increasing steel demand (automotive, infrastructure)

� Demand for DRI pellets (favorable natural gas pricing environment)

Experienced Management and Project Sponsor

� Experienced management, construction and engineering team

� Essar is a global leader in pellet production, integrated steel manufacturing, energy and infrastructure

� Low project execution risk – fixed price contracts with experienced EPC contractor

20

(1) $554 million debt funding plus $305 million equity invested as of 6/30/13.

PRIVATE & CONFIDENTIAL

Mesabi Iron Ore Range – Established Location for Pellet Production

CliffsHibTac8.0 MTPA

CliffsUTAC5.2 MTPA

CliffsNorthshore5.7 MTPA7.0 MTPA

U.S. SteelKeeTac5.1MTPA

U.S. SteelMinnTac13.4 MTPA

Arcelor Mittal 2.8 MTPA

Captive mines of steel producers

Merchant mines

Key

21

ESML

(1) Figures represent flux pellet production.

(1)(1)

� Total 2012 pellet production in the Mesabi Range:� Standard: 24 MTPA� Flux: 16 MTPA

� ESML planned production:� Standard / Flux / DRI: 7 MTPA

PRIVATE & CONFIDENTIAL

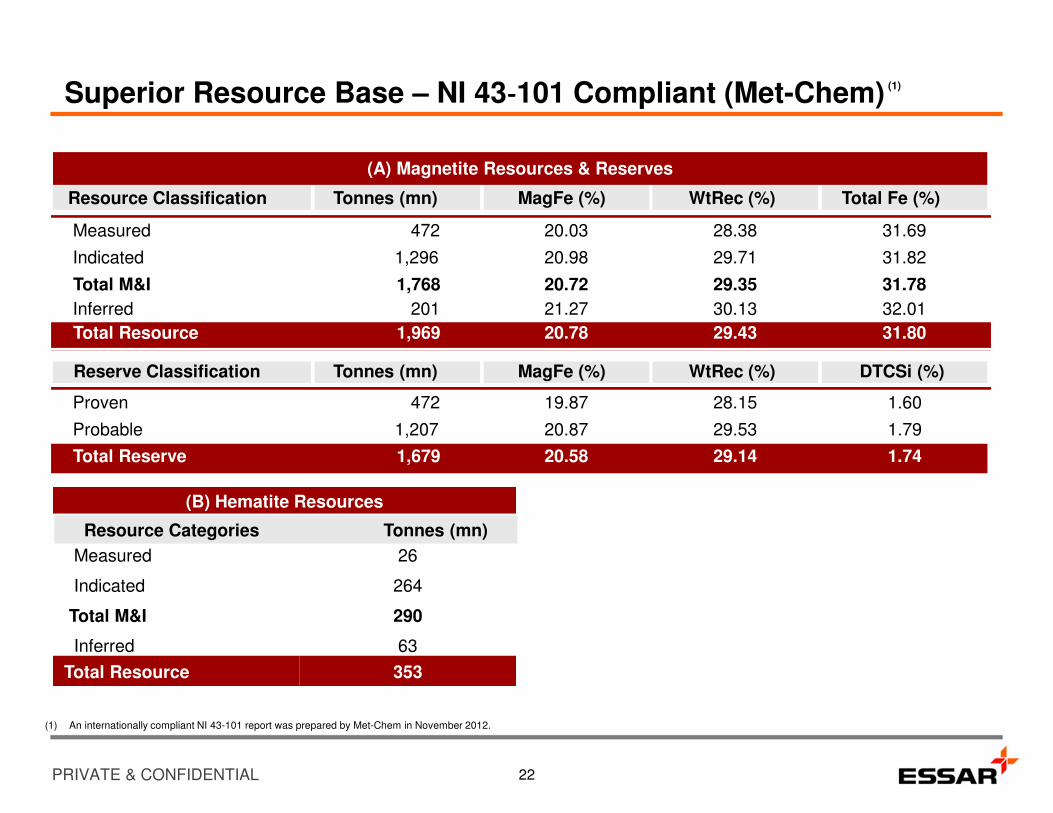

(1) An internationally compliant NI 43-101 report was prepared by Met-Chem in November 2012.

Resource Classification Tonnes (mn) MagFe (%) WtRec (%) Total Fe (%)

Measured 472 20.03 28.38 31.69

Indicated 1,296 20.98 29.71 31.82

Total M&I 1,768 20.72 29.35 31.78

Inferred 201 21.27 30.13 32.01

Total Resource 1,969 20.78 29.43 31.80

Reserve Classification Tonnes (mn) MagFe (%) WtRec (%) DTCSi (%)

Proven 472 19.87 28.15 1.60

Probable 1,207 20.87 29.53 1.79

Total Reserve 1,679 20.58 29.14 1.74

(A) Magnetite Resources & Reserves

Superior Resource Base – NI 43‐‐‐‐101 Compliant (Met-Chem)

(B) Hematite Resources

Measured 26

Indicated 264

Total M&I 290

Inferred 63

Total Resource 353

Resource Categories Tonnes (mn)

22

(1)

PRIVATE & CONFIDENTIAL

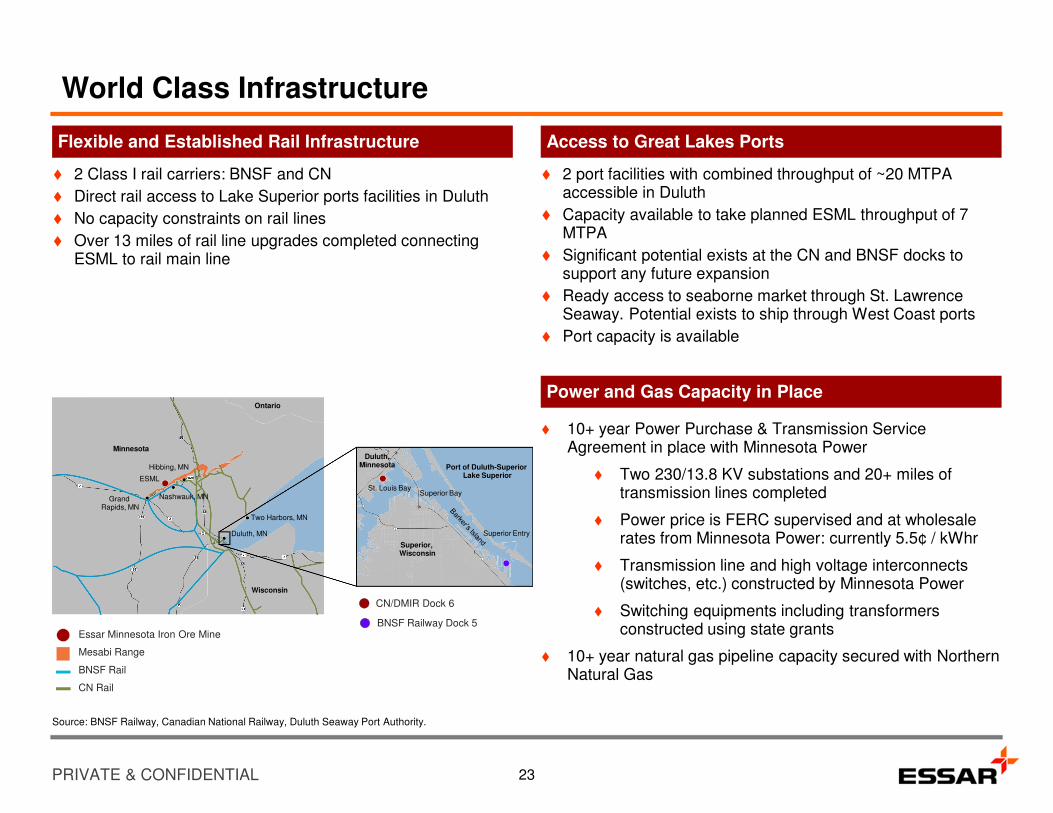

World Class Infrastructure

Flexible and Established Rail Infrastructure

� 2 Class I rail carriers: BNSF and CN

� Direct rail access to Lake Superior ports facilities in Duluth

� No capacity constraints on rail lines

� Over 13 miles of rail line upgrades completed connecting ESML to rail main line

Access to Great Lakes Ports

� 2 port facilities with combined throughput of ~20 MTPA accessible in Duluth

� Capacity available to take planned ESML throughput of 7 MTPA

� Significant potential exists at the CN and BNSF docks to support any future expansion

� Ready access to seaborne market through St. Lawrence Seaway. Potential exists to ship through West Coast ports

� Port capacity is available

Power and Gas Capacity in Place

Minnesota

ESML

Grand Rapids, MN

Nashwauk, MN

Hibbing, MN

Two Harbors, MN

Duluth, MN

Wisconsin

Ontario

St. Louis BaySuperior Bay

Duluth,Minnesota Port of Duluth-Superior

Lake Superior

Superior Entry

Superior, Wisconsin

Essar Minnesota Iron Ore Mine

Mesabi Range

BNSF Rail

CN Rail

CN/DMIR Dock 6

BNSF Railway Dock 5

Source: BNSF Railway, Canadian National Railway, Duluth Seaway Port Authority.

23

� 10+ year Power Purchase & Transmission Service Agreement in place with Minnesota Power

� Two 230/13.8 KV substations and 20+ miles of transmission lines completed

� Power price is FERC supervised and at wholesale rates from Minnesota Power: currently 5.5¢ / kWhr

� Transmission line and high voltage interconnects (switches, etc.) constructed by Minnesota Power

� Switching equipments including transformers constructed using state grants

� 10+ year natural gas pipeline capacity secured with Northern Natural Gas

PRIVATE & CONFIDENTIAL

–

20

40

60

80

100

120

140

– 29 54 79

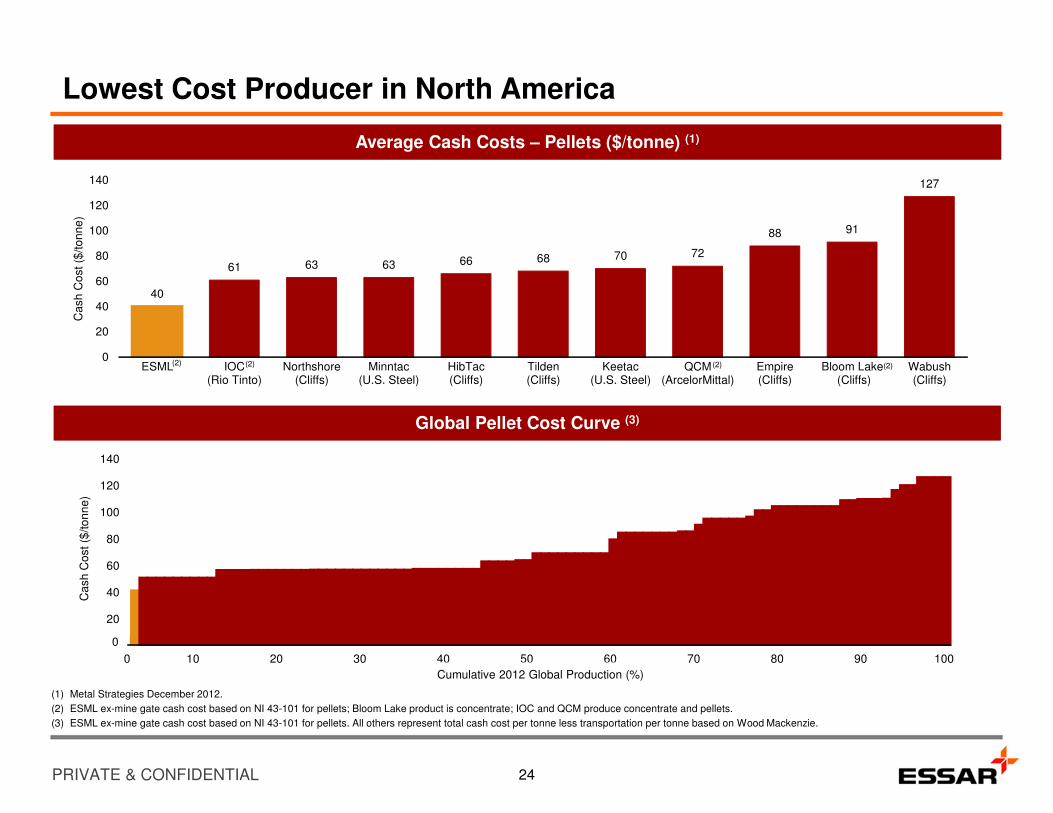

Lowest Cost Producer in North America

(1) Metal Strategies December 2012.

(2) ESML ex-mine gate cash cost based on NI 43-101 for pellets; Bloom Lake product is concentrate; IOC and QCM produce concentrate and pellets.

(3) ESML ex-mine gate cash cost based on NI 43-101 for pellets. All others represent total cash cost per tonne less transportation per tonne based on Wood Mackenzie.

24

40

61 63 63 66 68 70 72

88 91

127

0

20

40

60

80

100

120

140

ESML IOC(Rio Tinto)

Northshore(Cliffs)

Minntac(U.S. Steel)

HibTac(Cliffs)

Tilden(Cliffs)

Keetac(U.S. Steel)

QCM(ArcelorMittal)

Empire(Cliffs)

Bloom Lake (Cliffs)

Wabush(Cliffs)

Ca

sh

Co

st ($

/to

nn

e)

Average Cash Costs – Pellets ($/tonne) (1)Average Cash Costs – Pellets ($/tonne) (1)

Global Pellet Cost Curve (3)Global Pellet Cost Curve (3)

(2) (2) (2) (2)

10 20 30 40 50 60 70 80 90 100

Cumulative 2012 Global Production (%)

140

120

100

80

60

40

20

0

Ca

sh

Co

st

($/to

nn

e)

0

PRIVATE & CONFIDENTIAL

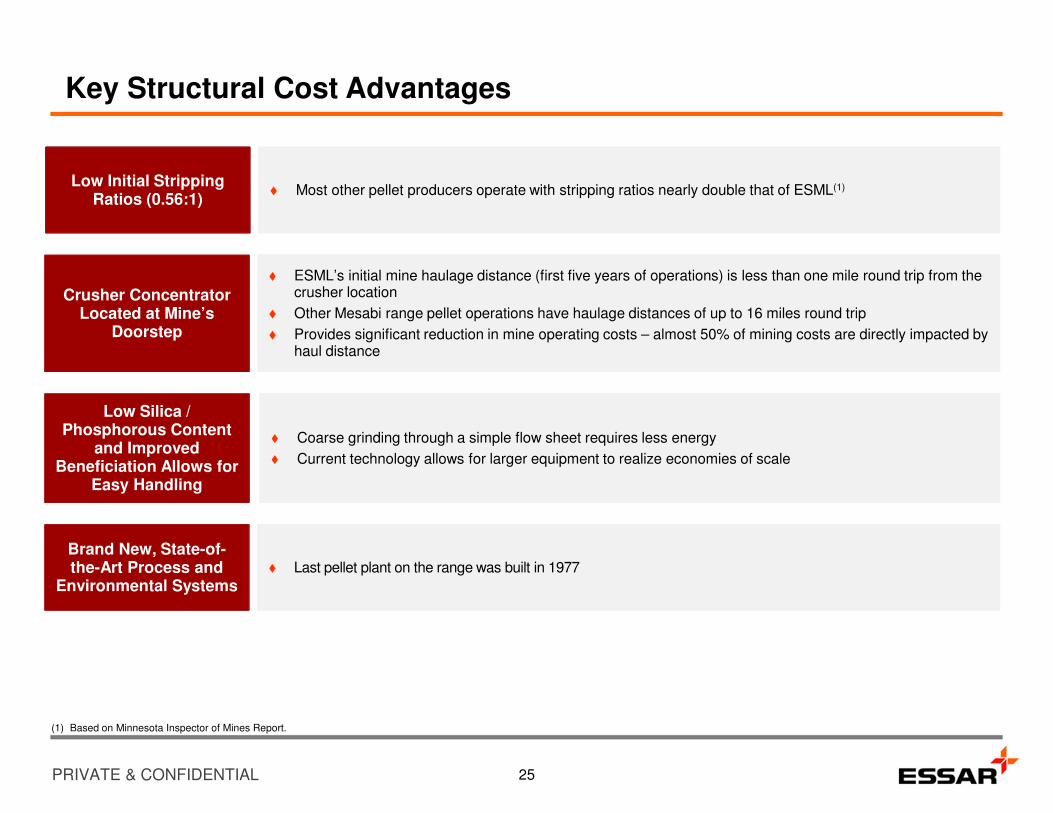

Key Structural Cost Advantages

� Most other pellet producers operate with stripping ratios nearly double that of ESML(1)Low Initial Stripping Ratios (0.56:1)

� ESML’s initial mine haulage distance (first five years of operations) is less than one mile round trip from the crusher location

� Other Mesabi range pellet operations have haulage distances of up to 16 miles round trip

� Provides significant reduction in mine operating costs – almost 50% of mining costs are directly impacted by haul distance

Crusher Concentrator Located at Mine’s

Doorstep

25

Brand New, State-of-the-Art Process and

Environmental Systems� Last pellet plant on the range was built in 1977

(1) Based on Minnesota Inspector of Mines Report.

� Coarse grinding through a simple flow sheet requires less energy

� Current technology allows for larger equipment to realize economies of scale

Low Silica / Phosphorous Content

and Improved Beneficiation Allows for

Easy Handling

PRIVATE & CONFIDENTIAL

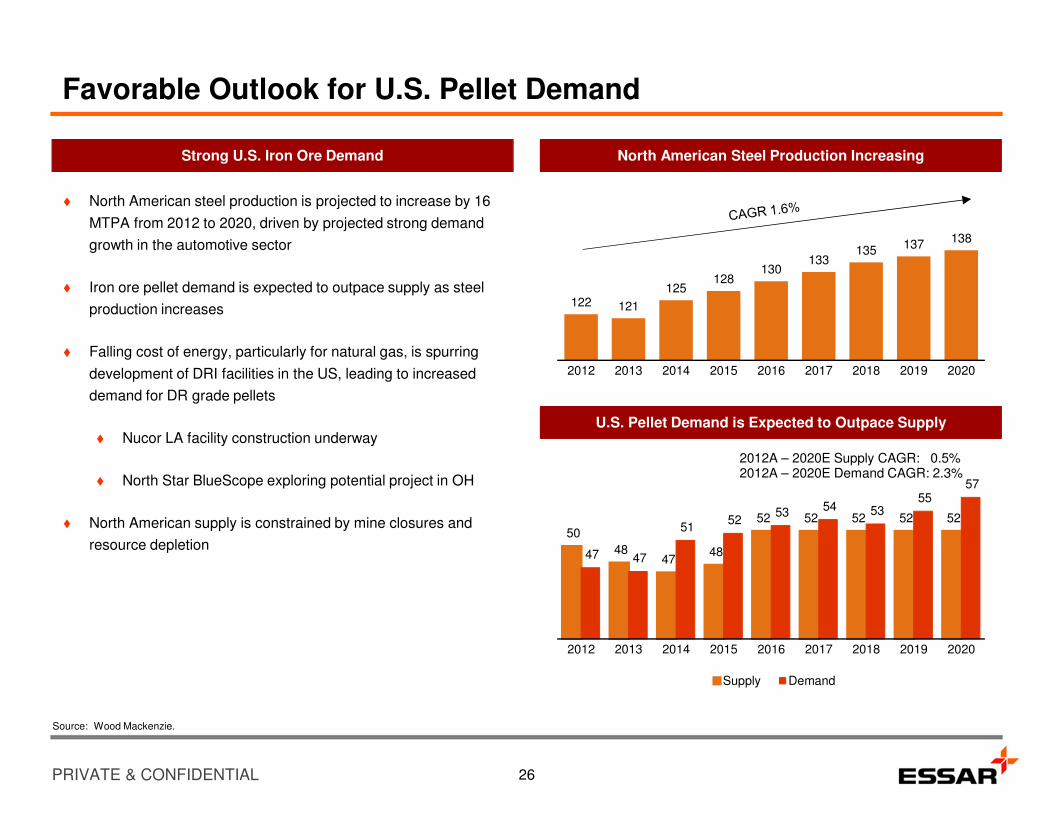

Favorable Outlook for U.S. Pellet Demand

Strong U.S. Iron Ore Demand

� North American steel production is projected to increase by 16

MTPA from 2012 to 2020, driven by projected strong demand

growth in the automotive sector

� Iron ore pellet demand is expected to outpace supply as steel

production increases

� Falling cost of energy, particularly for natural gas, is spurring

development of DRI facilities in the US, leading to increased

demand for DR grade pellets

� Nucor LA facility construction underway

� North Star BlueScope exploring potential project in OH

� North American supply is constrained by mine closures and

resource depletion

North American Steel Production Increasing

U.S. Pellet Demand is Expected to Outpace Supply

122 121

125128

130133

135 137 138

2012 2013 2014 2015 2016 2017 2018 2019 2020

50

48 47

48

52 52 52 52 52

47 47

51 52

53 54 53 55

57

2012 2013 2014 2015 2016 2017 2018 2019 2020

Supply Demand

Source: Wood Mackenzie.

2012A – 2020E Supply CAGR: 0.5%2012A – 2020E Demand CAGR: 2.3%

26

PRIVATE & CONFIDENTIAL

LAKESUPERIOR

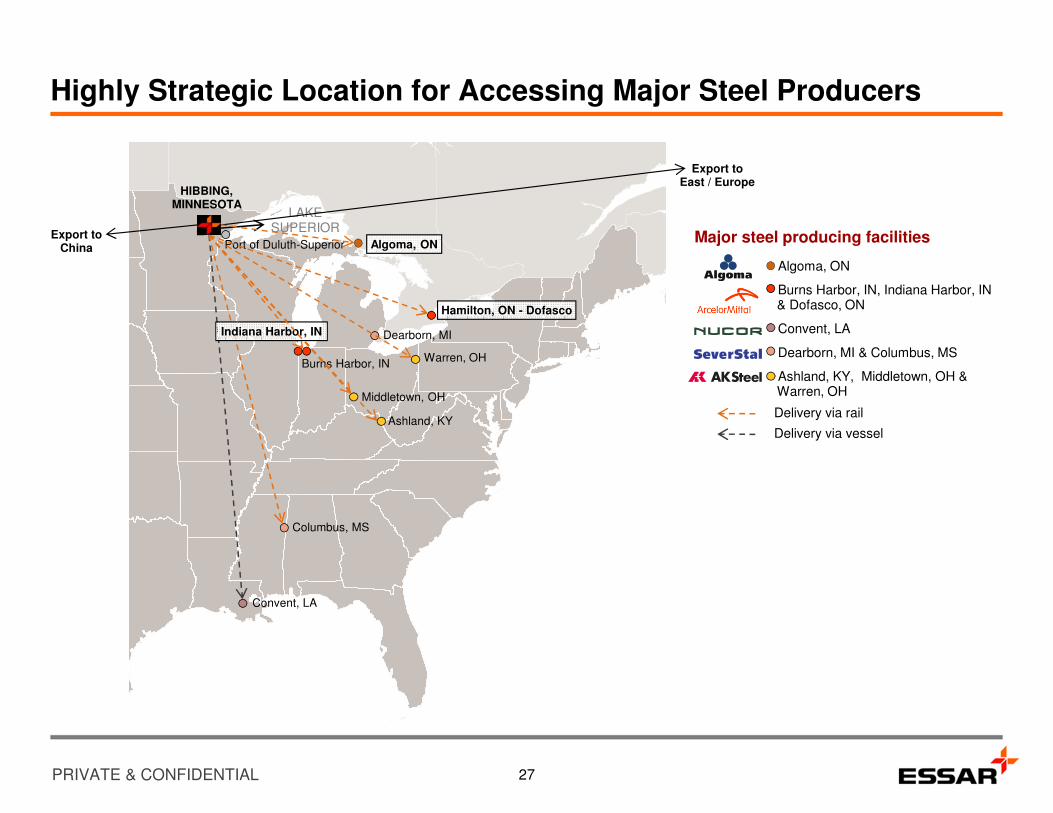

Highly Strategic Location for Accessing Major Steel Producers

27

Hamilton, ON - Dofasco

Algoma, ON

Warren, OH

Middletown, OH

Ashland, KY

Convent, LA

Columbus, MS

- Algoma, ON

- Burns Harbor, IN, Indiana Harbor, IN & Dofasco, ON

- Convent, LA

- Dearborn, MI & Columbus, MS

- Ashland, KY, Middletown, OH & Warren, OH

HIBBING, MINNESOTA

Export to China

Burns Harbor, IN

Export to East / Europe

Delivery via rail

Delivery via vessel

Port of Duluth-Superior Major steel producing facilities

Dearborn, MIIndiana Harbor, IN

PRIVATE & CONFIDENTIAL

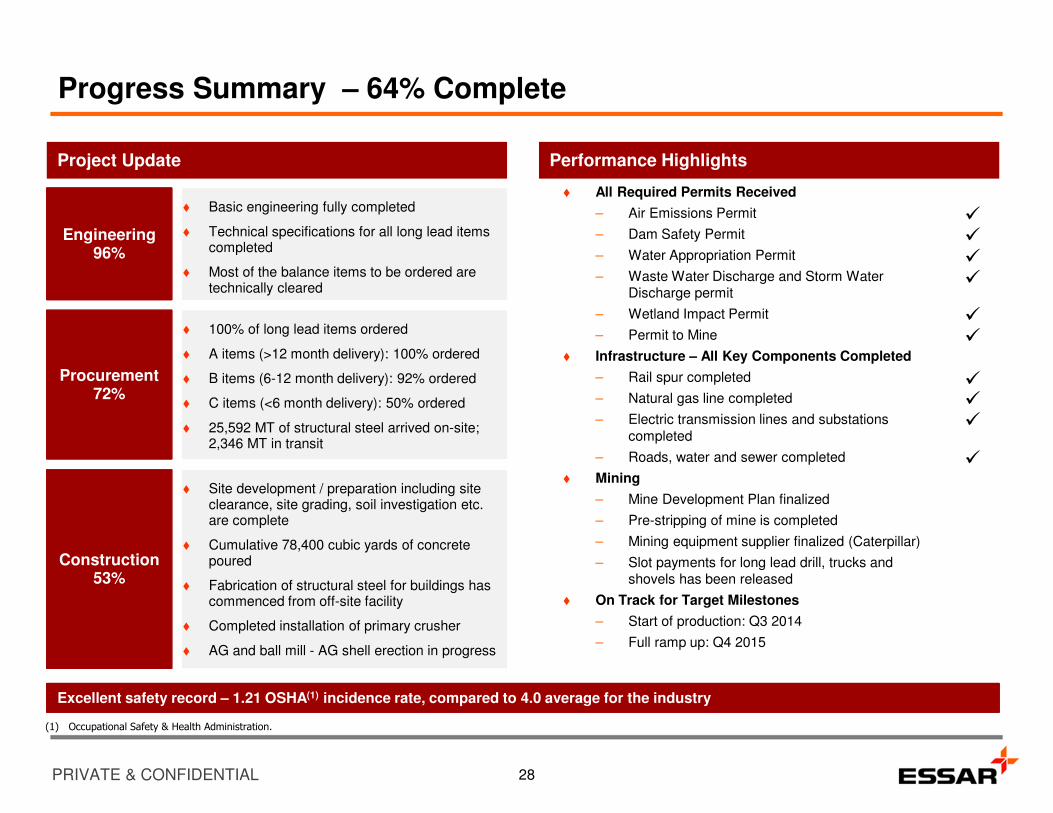

� All Required Permits Received

– Air Emissions Permit

– Dam Safety Permit

– Water Appropriation Permit

– Waste Water Discharge and Storm Water Discharge permit

– Wetland Impact Permit

– Permit to Mine

� Infrastructure – All Key Components Completed

– Rail spur completed

– Natural gas line completed

– Electric transmission lines and substations completed

– Roads, water and sewer completed

� Mining

– Mine Development Plan finalized

– Pre-stripping of mine is completed

– Mining equipment supplier finalized (Caterpillar)

– Slot payments for long lead drill, trucks and shovels has been released

� On Track for Target Milestones

– Start of production: Q3 2014

– Full ramp up: Q4 2015

Progress Summary – 64% Complete

Performance Highlights

28

Project Update

Engineering96%

� Basic engineering fully completed

� Technical specifications for all long lead items completed

� Most of the balance items to be ordered are technically cleared

� Basic engineering fully completed

� Technical specifications for all long lead items completed

� Most of the balance items to be ordered are technically cleared

Procurement72%

� 100% of long lead items ordered

� A items (>12 month delivery): 100% ordered

� B items (6-12 month delivery): 92% ordered

� C items (<6 month delivery): 50% ordered

� 25,592 MT of structural steel arrived on-site; 2,346 MT in transit

� 100% of long lead items ordered

� A items (>12 month delivery): 100% ordered

� B items (6-12 month delivery): 92% ordered

� C items (<6 month delivery): 50% ordered

� 25,592 MT of structural steel arrived on-site; 2,346 MT in transit

Construction53%

� Site development / preparation including site clearance, site grading, soil investigation etc. are complete

� Cumulative 78,400 cubic yards of concrete poured

� Fabrication of structural steel for buildings has commenced from off-site facility

� Completed installation of primary crusher

� AG and ball mill - AG shell erection in progress

� Site development / preparation including site clearance, site grading, soil investigation etc. are complete

� Cumulative 78,400 cubic yards of concrete poured

� Fabrication of structural steel for buildings has commenced from off-site facility

� Completed installation of primary crusher

� AG and ball mill - AG shell erection in progress

�

�

�

�

�

�

��

�

�

(1) Occupational Safety & Health Administration.

Excellent safety record – 1.21 OSHA(1) incidence rate, compared to 4.0 average for the industry

PRIVATE & CONFIDENTIAL

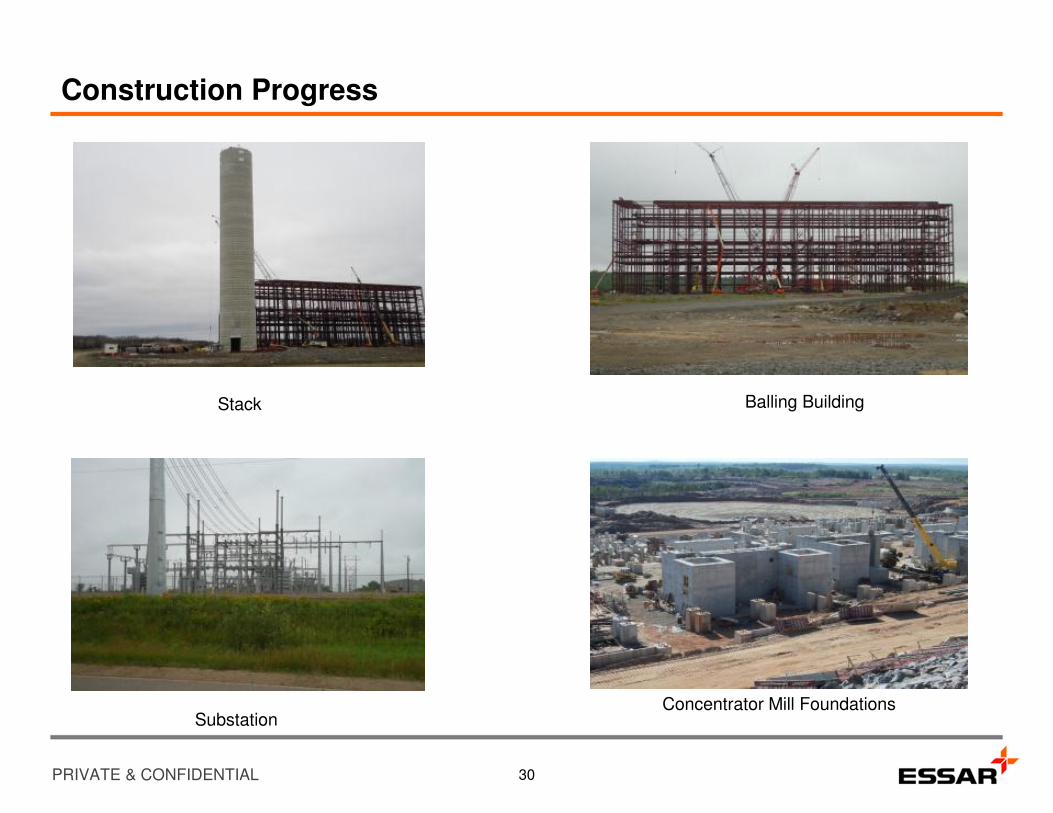

Construction Progress

Primary Crusher

Secondary CrusherConcentrator Line (1 of 3)

Mobile Equipment Shop

29

PRIVATE & CONFIDENTIAL

Construction Progress

Balling Building

SubstationConcentrator Mill Foundations

Stack

30

PRIVATE & CONFIDENTIAL

Cautionary Statement

CAUTIONARY STATEMENT

No stock exchange, securities commission or other regulatory authority has approved or disapproved the information contained in this presentation. The information contained in this presentation is current as of the date of the presentation, unless otherwise indicated. This information in a summary form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice, when deciding if an investment is appropriate.

By attending the presentation, or reading the presentation materials, you acknowledge and agree to the contents of this disclaimer.

No representation or warranty, express or implied, is made or given by or on behalf of Essar Steel Minnesota LLC (“ESML” or the “Company”) or any of their subsidiary undertakings or any of the directors, officers or employees of any such entities as to the accuracy, completeness or fairness of the information or opinions contained in this presentation and no responsibility or liability is accepted by any person for such information or opinions. This presentation is confidential and contains confidential information and may not be reproduce, further distributed or published. Distribution of this presentation may also be restricted or prohibited by law. Recipients are required to inform themselves of, and comply with, all such restrictions or prohibitions.

This presentation does not constitute or form part of any offer or invitation for the sale or purchase of securities or any of the assets, business or undertaking described herein nor shall it or any part of it form the basis of or be relied on in connection with, or act as any inducement to enter into, any contract or commitment whatsoever. It has been prepared by management of the Company for general information purposes only, and, in particular, is not intended to be, nor shall it be received or construed as, an “offering memorandum” or similar document.

Certain statements in this presentation have been derived from third party sources, including the Metal Strategies Inc. report, and are used by consent or are otherwise publicly available. The Company has not independently verified the information from such third party sources and takes no responsibility for such statements.

Certain Technical Information. Unless otherwise indicated, the Company has prepared the technical information in this presentation (“Technical Information”) based on information contained in the National Instrument 43-101 technical report for ESML obtained by the Company written by Met-Chem Canada Inc. and Barr Engineering Co. This report was prepared by or under the supervision of a qualified person (a “Qualified Person”) as defined in National Instrument 43-101 – Standards of Disclosure for Mineral Projects of the Canadian Securities Administrators (“NI 43-101”). For readers to fully understand the information in this presentation, they should read this report in its entirety, including all qualifications, assumptions and exclusions that relate to the information set out in this presentation which qualifies the Technical Information. Readers are advised that Mineral Resources that are not Mineral Reserves do not have a demonstrated economic viability. The NI 43-101 is intended to be read as a whole, and sections should not be read or relied upon out of context. The Technical Information is subject to the assumptions and qualifications contained in the NI 43-101.

The stated Mineral Reserves and Mineral Resources estimates have been prepared in accordance with NI 43-101 and are classified in accordance with the Canadian Institute of Mining, Metallurgy and Petroleum’s “CIM Definition Standards – For Mineral Resources and Mineral Reserves”. Mineral Reserves are equivalent to Proven and Probable Reserves as defined by the SEC Industry Guide 7. Mineral Reserve and Mineral Resource estimates reflect our reasonable expectation that all necessary permits and approvals will be obtained and maintained. Mining dilution and mining recovery have been applied in estimating the Mineral Reserves.

Certain of the Technical Information contained in presentation is based upon management’s expectations, which in some cases differ from the information that is contained in the Company’s NI 43-101 technical report. Such differences relate to, among other things, the anticipated start date of commercial production being in Q1 of calendar year 2014 vsJune 2013 and additional capital costs attributable to a debt offering vs no such additional cost being contemplated in the technical report.

Cautionary Note to United States and Other Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources: This presentation uses the terms “Measured”, “Indicated” and “Inferred” Resources. United States investors are advised that while such terms are recognized by Canadian regulations, the United States Securities and Exchange Commission (“SEC”) only permits United States mining companies, in filings with the SEC, to disclose those mineral deposits that a company can economically and legally extract or produce in accordance with SEC Industry Guide 7. United States and other investors are cautioned not to assume that all or any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves or that all or any part of an Inferred Mineral Resource exists, or is economically or legally mineable.

31

PRIVATE & CONFIDENTIAL

Forward-Looking and Qualified Persons Statements

FORWARD-LOOKING STATEMENTS

Certain statements in this presentation constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities laws (collectively, “forward-looking statements”). Such statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements or information. Such statements can be identified by the use of words such as “may”, “would”, “believe”, “plan”, “estimate”, and other similar terminology, or state that certain actions, events or results “may” or “would” be taken, occur or be achieved.

Forward-looking statements are based on a number of assumptions that may or may not prove to be correct, and involve significant risks and uncertainties, and accordingly should not be read as guarantees of future performance or results, and will not necessarily be accurate indicators of whether or not such results will be achieved. A number of factors could cause actual results to differ materially from the forward-looking statements set forth in this presentation.

The forward-looking statements contained in this presentation are based upon the Company’s current expectations and are made as of the date of this presentation. The Company cannot assure readers that actual results will be consistent with these forward-looking statements and they are expressly qualified in their entirety by this cautionary statement.

The Company does not assume any obligation to update or revise the forward-looking statements contained herein to reflect events or circumstances occurring after the date of this presentation.

QUALIFIED PERSONS STATEMENT

Met-Chem Canada Inc. and Barr Engineering Co. have prepared an independent NI 43-101 report for ESML’s iron ore project, including a 7.0 mtpa pellet plant with potential expansion to 14.0 mtpa. The NI 43-101 report was prepared by the following independent “qualified persons” as defined in NI 43-101: Daniel M. Gagnon Eng.; Yves A. Buro Eng.,; Denns Murr, a licensed professional engineer; and Michel L. Bilodeau, a licensed professional engineer.

Certain Technical Information in this presentation is derived from, and based upon, the aforementioned NI 43-101 report. Unless specifically noted otherwise, the disclosure contained herein relating to ESML’s iron ore project has been prepared and the data presented herein verified, including sampling, analytical and test data underlying the technical information under the authority and supervision of the authors, Daniel M. Gagnon Eng., Yves A. Buro Eng., or Michel L Bilodeau or Dennis Murr, “qualified persons” within the meaning of NI 43-101. Met-Chem Canada Inc. implemented a complete set of procedures aiming at checking the validity and reliability of the dataset used for the resources estimation in the NI 43-101 report. This verification included a review of databases, results from ESML and of the laboratory’s quality control samples, as well as a visit to the Lerchlaboratory and independent checks samples selected by Met-Chem Canada Inc’s qualified person.

Met-Chem Canada Inc. could not verify the results from Butler Taconite drilling since no core was available for viewing by Met-Chem Canada Inc. There are few examples of saved core from the early drilling programs and the only remaining core may be found in the Minnesota State core laboratory in Hibbing or Great Northern Iron Ore Properties. Surveying in the hole collars in ESML’s iron ore project area is probably precise, as the survey crew had to fulfill the need of good survey control for royalty payments. The practice used by the former operators generally favored saving pulps rather than drill core.

Based on these observations and results, Met-Chem Canada Inc. did not see any factor in the procedures applied in the core logging, sampling, sample preparation and analytical procedures that may significantly impact the integrity of the data. Met-Chem Canada Inc. believes the data is sufficiently reliable and adequate for the purposes of the resource estimation.

Each of Daniel M. Gagnon Eng., Yves A. Buro Eng., or Michel L Bilodeau or Dennis Murr consents to the inclusion in this presentation of the matters based on his information in the form and context in which it appears

32