Embed Size (px)

Citation preview

Monopoly

Dr. Andrew McGee

Simon Fraser University

Monopoly Assumptions & Implications

1. Single seller of a single good (many buyers)

– Something prevents entry into this market, resulting in a single seller

2. Monopolist chooses an output level

– Monopolist is not a price taker; monopolist faces the entire market demand curve

– Maintained assumption: monopolist maximizes profit

Monopoly and market power

Monopoly profits

• Unlike in perfect competition, the monopolist can make positive profits in the long run because no other firms can enter to compete and lower the market price

• What are these barriers to entry?

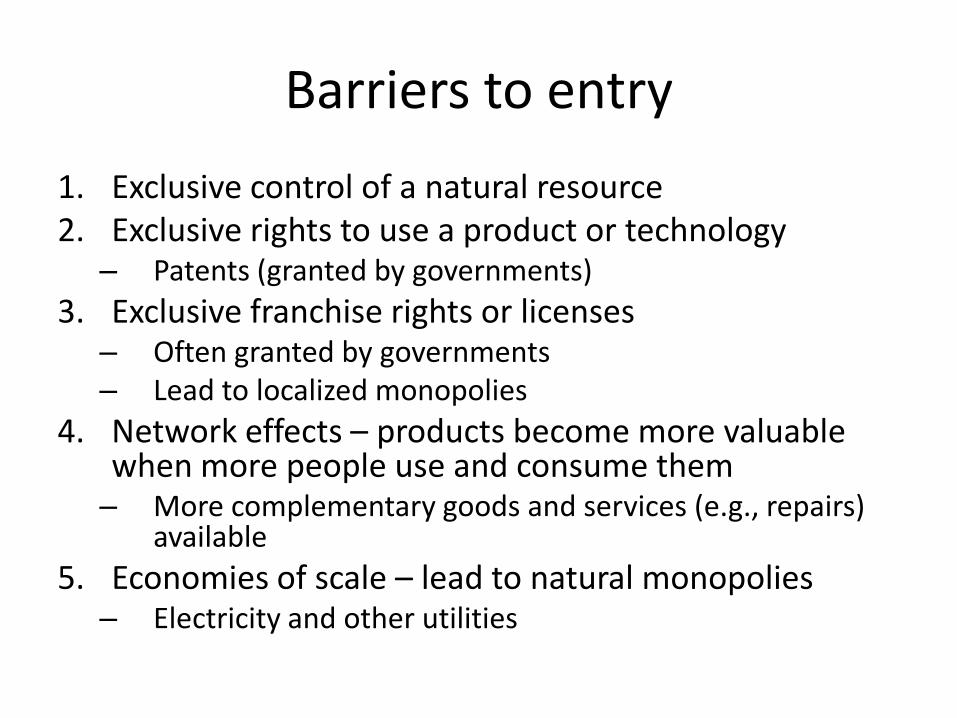

Barriers to entry

1. Exclusive control of a natural resource2. Exclusive rights to use a product or technology

– Patents (granted by governments)

3. Exclusive franchise rights or licenses– Often granted by governments– Lead to localized monopolies

4. Network effects – products become more valuable when more people use and consume them– More complementary goods and services (e.g., repairs)

available

5. Economies of scale – lead to natural monopolies– Electricity and other utilities

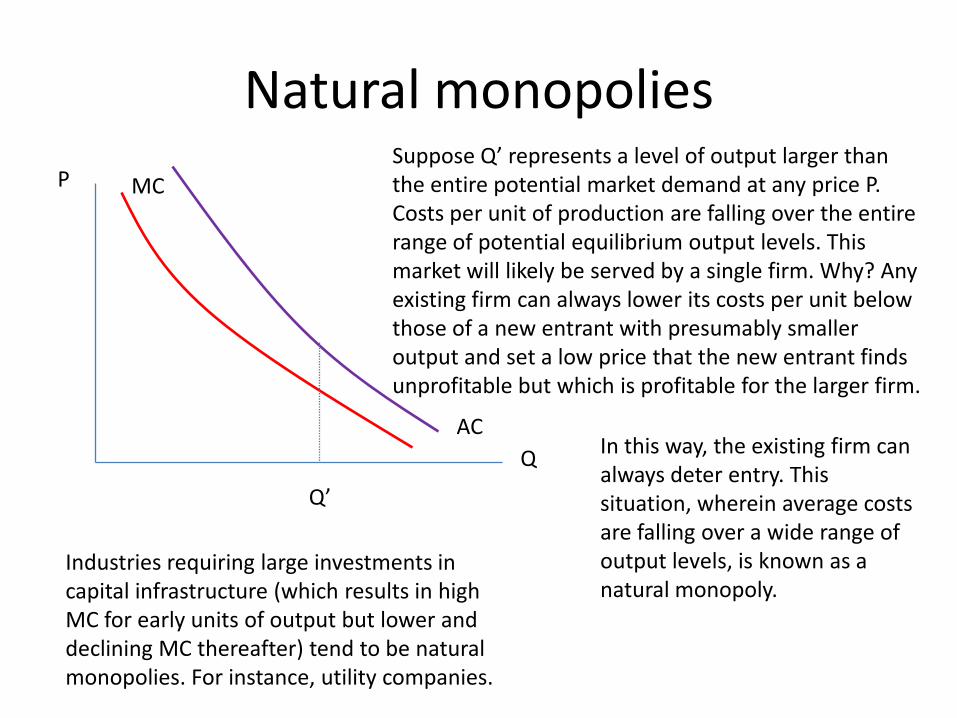

Natural monopolies

AC

MCP

Q

Suppose Q’ represents a level of output larger than the entire potential market demand at any price P. Costs per unit of production are falling over the entire range of potential equilibrium output levels. This market will likely be served by a single firm. Why? Any existing firm can always lower its costs per unit below those of a new entrant with presumably smaller output and set a low price that the new entrant finds unprofitable but which is profitable for the larger firm.

Q’

In this way, the existing firm can always deter entry. This situation, wherein average costs are falling over a wide range of output levels, is known as a natural monopoly.

Industries requiring large investments in capital infrastructure (which results in high MC for early units of output but lower and declining MC thereafter) tend to be natural monopolies. For instance, utility companies.

Persistence of monopolies in the LR

• Which barriers to entry are likely to persist in the LR?

– Firms can find substitutes for important inputs or develop synthetics

– Patents expire

– Franchise rights & licenses can be revoked

– New technologies can upend existing networks

• Beta vs. VHS, CDs and iTunes, iTunes & “the cloud”

Persistence of monopolies in the LR

• Natural monopolies may survive in the LR in the absence of major technological change

• Technological change is the enemy of monopoly

• Even natural monopolies can be displaced by technological change

– Land lines & cell phones, electricity & solar panels?

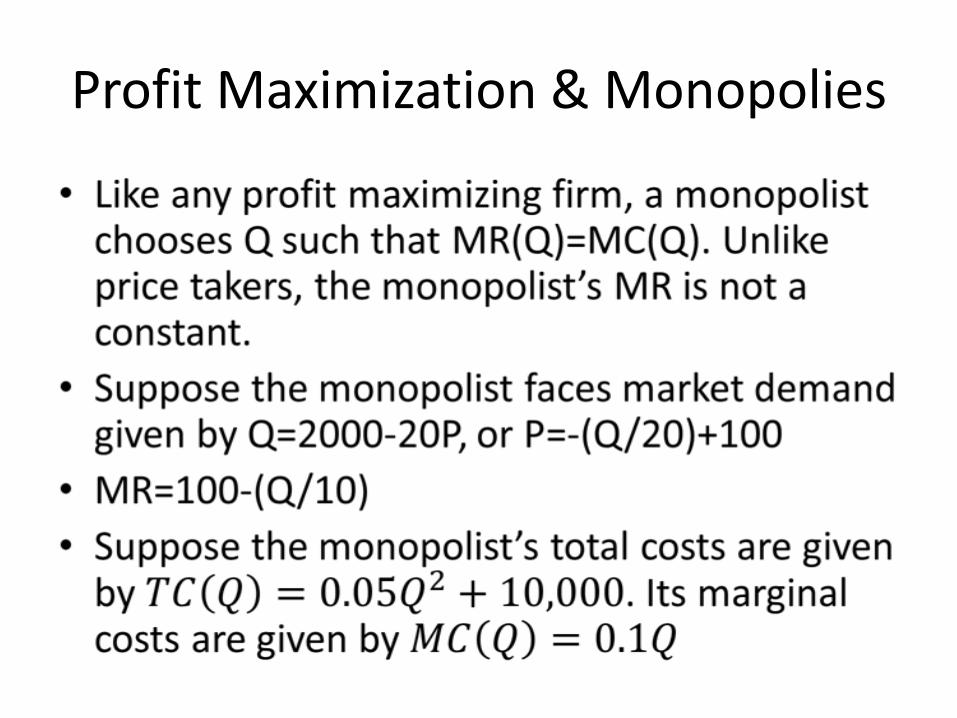

Profit Maximization & Monopolies

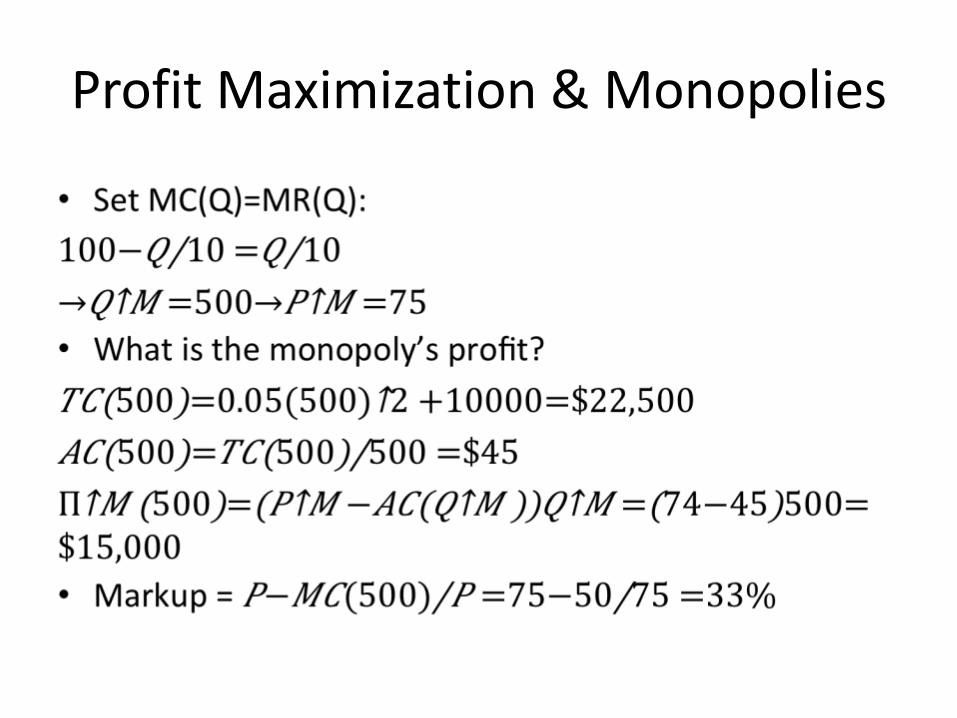

Profit Maximization & Monopolies

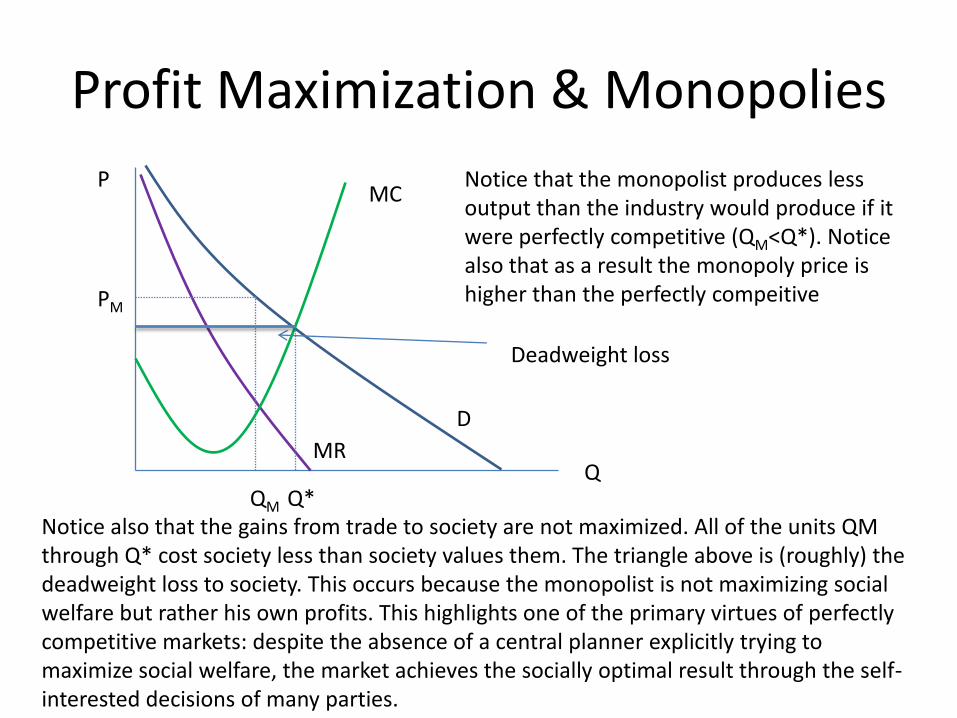

Profit Maximization & Monopolies

P

Q

MC

D

MR

PM

QM Q*

Notice that the monopolist produces less output than the industry would produce if it were perfectly competitive (QM<Q*). Notice also that as a result the monopoly price is higher than the perfectly compeitive

Notice also that the gains from trade to society are not maximized. All of the units QM through Q* cost society less than society values them. The triangle above is (roughly) the deadweight loss to society. This occurs because the monopolist is not maximizing social welfare but rather his own profits. This highlights one of the primary virtues of perfectly competitive markets: despite the absence of a central planner explicitly trying to maximize social welfare, the market achieves the socially optimal result through the self-interested decisions of many parties.

Deadweight loss

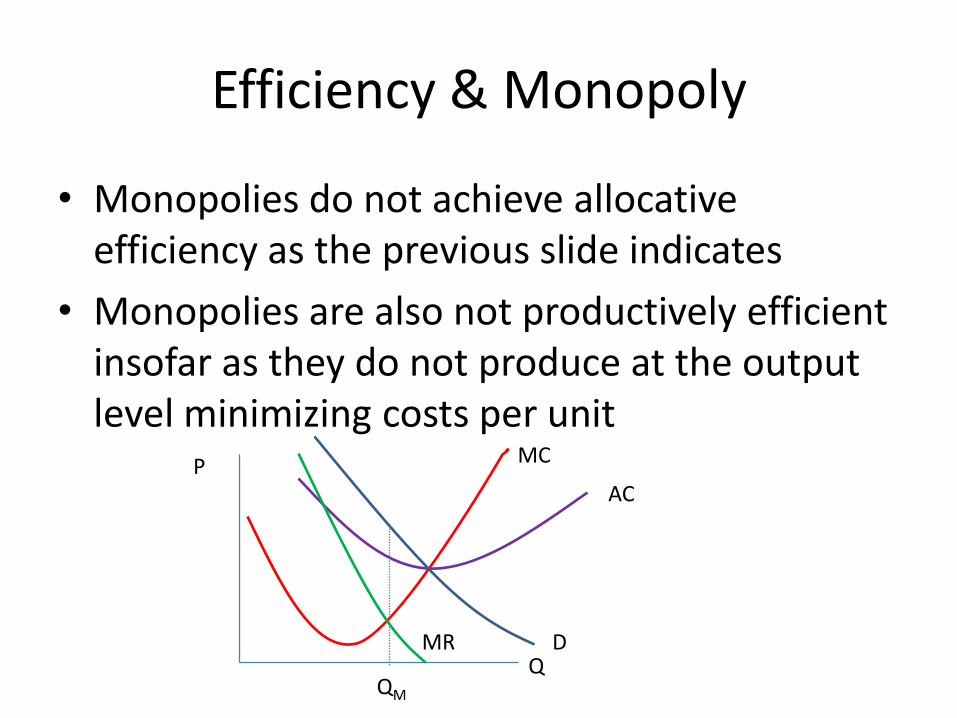

Efficiency & Monopoly

• Monopolies do not achieve allocativeefficiency as the previous slide indicates

• Monopolies are also not productively efficient insofar as they do not produce at the output level minimizing costs per unit

P

Q

MC

AC

D

QM

MR

Monopoly Supply Curve

• There is none.

• For any given demand, there is a unique profit-maximizing price-quantity pair for the monopolist. The only thing that would cause the monopolist’s price and output to change would be a change in consumer demand, which would change the monopolist’s marginal revenue. Supply curves, however, plot the change in quantity supplied at different prices. Here, quantity supplied varies not with price but with consumer demand, so there is no well-defined supply curve.

Price discrimination

• A monopoly engages in price discrimination if it sells otherwise identical units of output at different prices

• Examples: student & senior ticket prices at the movies—the movie is the same for all viewers

• Non-examples: differences in insurance premiums for different drivers—different drivers present different risks and hence the insurance product they receive differs

Law of one price

• If buyers are able to costlessly exchange goods amongst themselves, then a homogeneous good must sell everywhere for the same price

• Law of one price not satisfied with price discrimination

– Buyers must not be able to practice arbitrage

• Example: senior citizens hawking seniors tickets outside of a movie theater

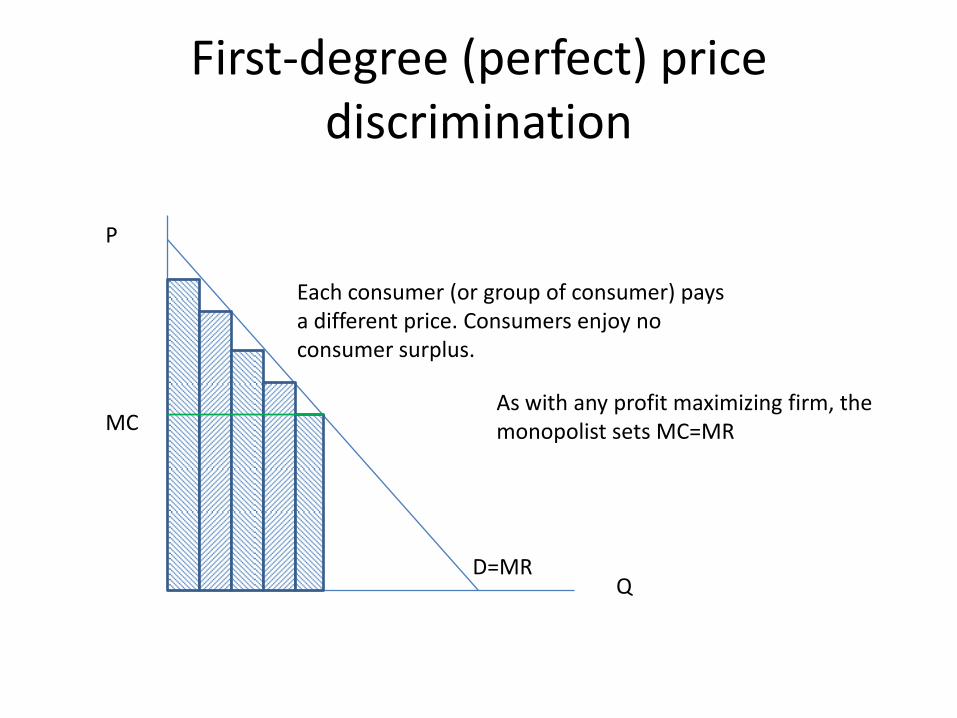

First-degree (perfect) price discrimination

• Selling to each buyer at the maximum price he or she is willing to pay

• Requires being able to identify each buyer and know their willingness to pay

• The demand curve becomes the marginal revenue curve• Under perfect price discrimination, the social surplus is

maximized (gains from trade are exhausted). The monopolist, however, extracts the whole surplus.

• Consumers are indifferent between consuming the monopolist’s product and going without it

• Perfect price discrimination is mainly a theoretical construct. In practice, the other types of price discrimination are much more common. Not surprising given the information a monopolist must have about all consumer in order to engage in perfect price discrimination

First-degree (perfect) price discrimination

P

QD=MR

Each consumer (or group of consumer) pays a different price. Consumers enjoy no consumer surplus.

MCAs with any profit maximizing firm, the monopolist sets MC=MR

Third degree price discrimination through market separation

• Far more likely than knowing each consumer’s willingness to pay is that a firm can separate its customers into different geographic markets. If (1) it knows that the willingness to pay (demand elasticity) differs in these markets and (2) can prevent customers in one market from re-selling to customers in another market, it can and will sell its output for different prices in these different markets

• Examples: foreign & domestic sales, differences in provinces, urban & rural markets

• Welfare effect of 3rd degree price discrimination is ambiguous

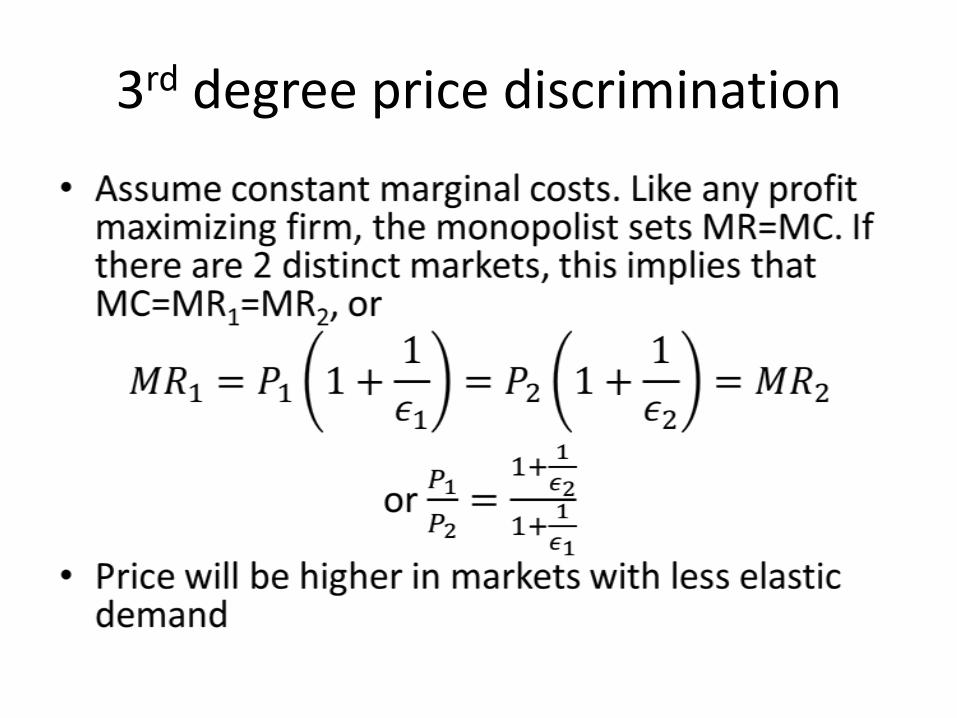

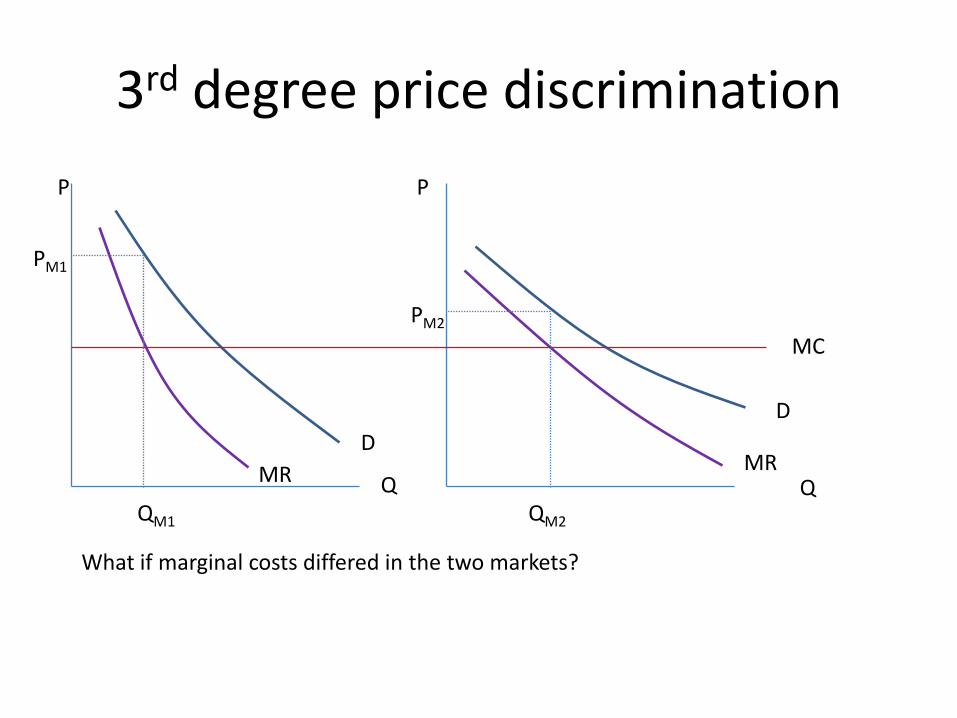

3rd degree price discrimination

3rd degree price discrimination

D

D

MR MR

P P

Q Q

MC

PM2

PM1

QM1 QM2

What if marginal costs differed in the two markets?

3rd degree price discrimination

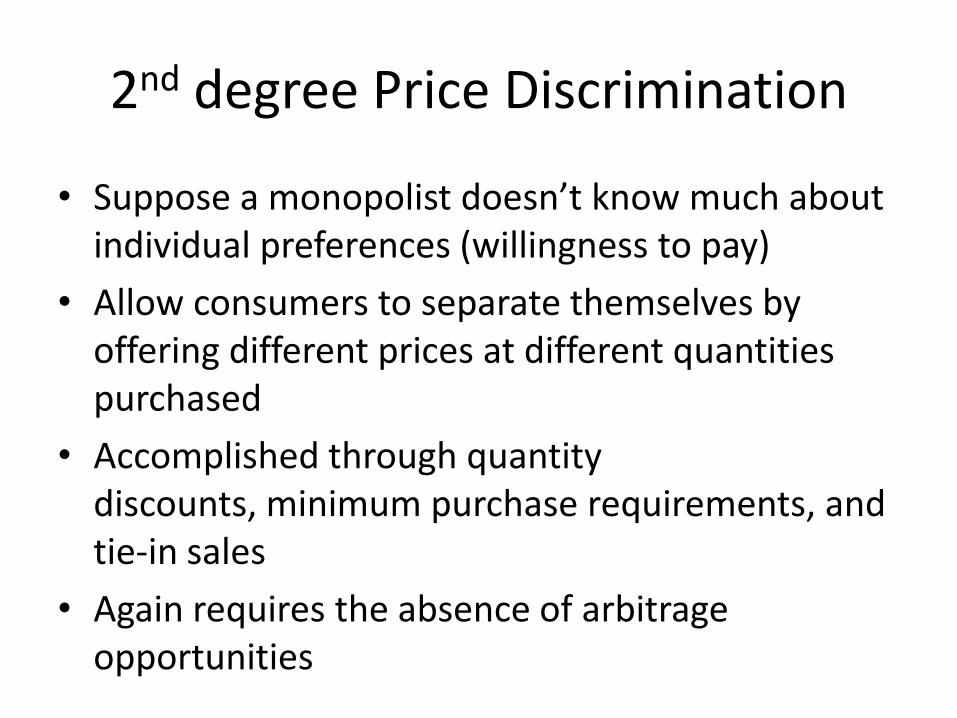

2nd degree Price Discrimination

• Suppose a monopolist doesn’t know much about individual preferences (willingness to pay)

• Allow consumers to separate themselves by offering different prices at different quantities purchased

• Accomplished through quantity discounts, minimum purchase requirements, and tie-in sales

• Again requires the absence of arbitrage opportunities

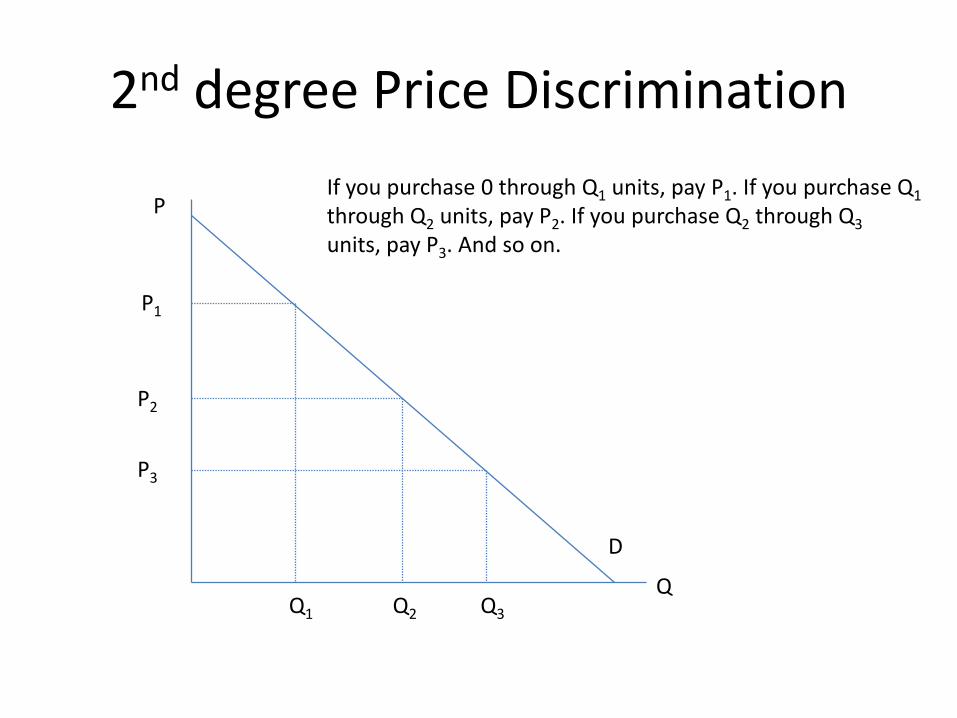

2nd degree Price Discrimination

P

Q

D

P1

P2

P3

Q1 Q2 Q3

If you purchase 0 through Q1 units, pay P1. If you purchase Q1

through Q2 units, pay P2. If you purchase Q2 through Q3

units, pay P3. And so on.

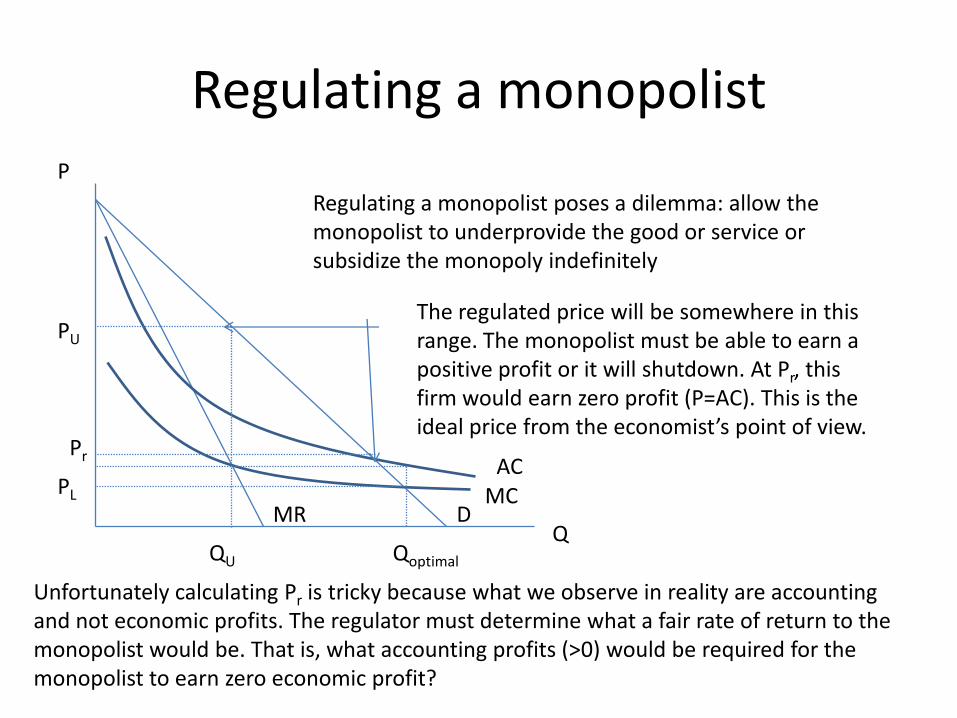

Regulating a monopolist

DMRQ

P

MCAC

PU

QU

PL

Regulating a monopolist poses a dilemma: allow the monopolist to underprovide the good or service or subsidize the monopoly indefinitely

Qoptimal

The regulated price will be somewhere in this range. The monopolist must be able to earn a positive profit or it will shutdown. At Pr, this firm would earn zero profit (P=AC). This is the ideal price from the economist’s point of view.

Pr

Unfortunately calculating Pr is tricky because what we observe in reality are accounting and not economic profits. The regulator must determine what a fair rate of return to the monopolist would be. That is, what accounting profits (>0) would be required for the monopolist to earn zero economic profit?