Embed Size (px)

Citation preview

ArcelorMittal Mines

Americas Iron Ore Conference

12 November 2013 Kleber Silva – Head of Iron Ore

Disclaimer Forward-Looking Statements

This presentation may contain forward-looking information and statements about ArcelorMittal and its subsidiaries. These statements include financial projections and estimates and their underlying assumptions, statements regarding plans, objectives and expectations with respect to future operations, products and services, and statements regarding future performance. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,” “target” or similar expressions. Although ArcelorMittal’s management believes that the expectations reflected in such forward-looking statements are reasonable, investors and holders of ArcelorMittal’s securities are cautioned that forward-looking information and statements are subject to numerous risks and uncertainties, many of which are difficult to predict and generally beyond the control of ArcelorMittal, that could cause actual results and developments to differ materially and adversely from those expressed in, or implied or projected by, the forward-looking information and statements. These risks and uncertainties include those discussed or identified in the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de Surveillance du Secteur Financier) and the United States Securities and Exchange Commission (the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal’s Annual Report on Form 20-F for the year ended December 31, 2012 filed with the SEC. ArcelorMittal undertakes no obligation to publicly update its forward-looking statements, whether as a result of new information, future events, or otherwise.

Non-GAAP Financial Measures This presentation may contain supplemental financial measures that are or may be non-GAAP financial measures. Definitions of such supplemental financial measures and a discussion of the most directly comparable IFRS financial measures can be found on ArcelorMittal's website at http://www.arcelormittal.com/corp/investors/presentations/.

1

2

HSE and sustainability

* World steel association -standard: LTIFR = Lost Time Injuries per 1.000.000 worked hours; based on own personnel and contractors

ArcelorMittal Iron Ore operations segment injury

frequency rate* • 2012 LTIFR* of 0.41, a 67% improvement

compared with 2011

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2009

1.8

2008

1.6

2007

3.2

2006

4.5

2012 2010 2011

1.0

0.4

1.2

Safety remains the No1 priority for ArcelorMittal

ArcelorMittal Mining safety performance

Our focus

• Achieve our goal of zero fatalities and serious

injuries:

• Complete implementation of Fatality

Prevention Standards at all operations

and projects

• Base of the pyramid

• Risk assessment

• Manage occupational exposures:

• All operations to complete new health risk

assessments and develop control plans

for material risks

• Manage and reduce our impact on the

environment

Long term safety targets trending towards best in

class

South Africa

Iron Ore**

* Includes share of production

** Includes purchases made under July 2010 interim agreement with Kumba (South Africa)

Mining business portfolio

Key assets and projects

USA Iron Ore

Minorca

Hibbing*

Mexico Iron Ore

Las Truchas &

Volcan;

Pena* Liberia

Iron Ore

Algeria

Iron Ore

Brazil

Iron Ore

Serra Azul

Andrade

New projects /

exploration

Existing mines

Canada

AMMC

Bosnia

Iron Ore

Indian Iron

Ore & Coal

exploration

license

Ukraine

Iron Ore

Kazakhstan

Iron Ore

4 mines

Iron ore mine

Canada

Baffinland

3

Geographically diversified mining assets

4

Iron ore reserve and resource estimates Strong reserve and resource basis to support sustainable growth

• Highlights of 2012:

– Resource to Reserve conversion exceeded mining depletion to provide a net increase of ~500Mt in iron ore reserves

– Resource to reserve conversion was largely offset by resource additions due to exploration and re-evaluation of known mineralization

• Resource and reserve estimates supported by internal technical reports

• Updated life of mine plans with discounted cash flows to support demonstration of economic viability for all ore reserve estimates

• All resource estimates have potential for economic extraction to support future potential growth

2012 Iron ore reserves and resources (million metric tonnes)

Region

Proven &

probable

reserves

Measured &

indicated

resources

Inferred

resources

Mtonnes %Fe Mtonnes %Fe Mtonnes %Fe

Canada (AMMC) 1,952 28 4,931 29 1,082 29

Canada (Baffinland) 375 65 41 65 444 66

USA 473 20 421 20 92 23

Central America 395 26 146 26 78 27

South America 121 58 321 38 131 36

West Africa 526 48 39 44 2,061 41

Eastern Europe 301 36 866 38 0 0

Central Asia 188 40 1,455 40 123 34

TOTAL 4,331 35 8,219 32 4,010 39

Canada (Baffinland)

12%

USA

11%

Central America

3% South America

West Africa

45%

Eastern Europe Central Asia

4%

Canada (AMMC)

2012 Geographical breakdown of iron ore reserves & resources

2012 Iron ore reserves of 4.3bn metric tonnes

5

CA

PA

CIT

Y

* Includes consideration from JV partner (Nunavut Iron Ore) for additional equity stake increase from 30% to 50%.

Iron ore growth target on track – 84MT capacity by 2015

AMMC

• Spirals replacement project completed in 1Q’13

• Capacity expansion from 16Mt to 24Mt:

• In June 2013 first concentrate from new Line 7 produced

• Ramp up underway. Targeting 24mt annual equivalent by end of 2013

• Capex of $1.6bn

Liberia

• Phase 1 achieved new production record in 3Q’13 at 1.1Mt

• Phase 2 project underway for 15Mtpa premium sinter feed to replace 4Mtpa DSO by 2015

• Product specification changed to sinter feed; engineering scope change required

• Major equipment procurement complete

• Civil works at the port are advancing and will be completed this year

Baffinland

• Early Revenue Phase underway

• 3.5Mtpa of DSO trucked to Milne Inlet for export during open-water season by 2015

• $700m* project capex in 50:50 JV

Iron ore growing; plans on track

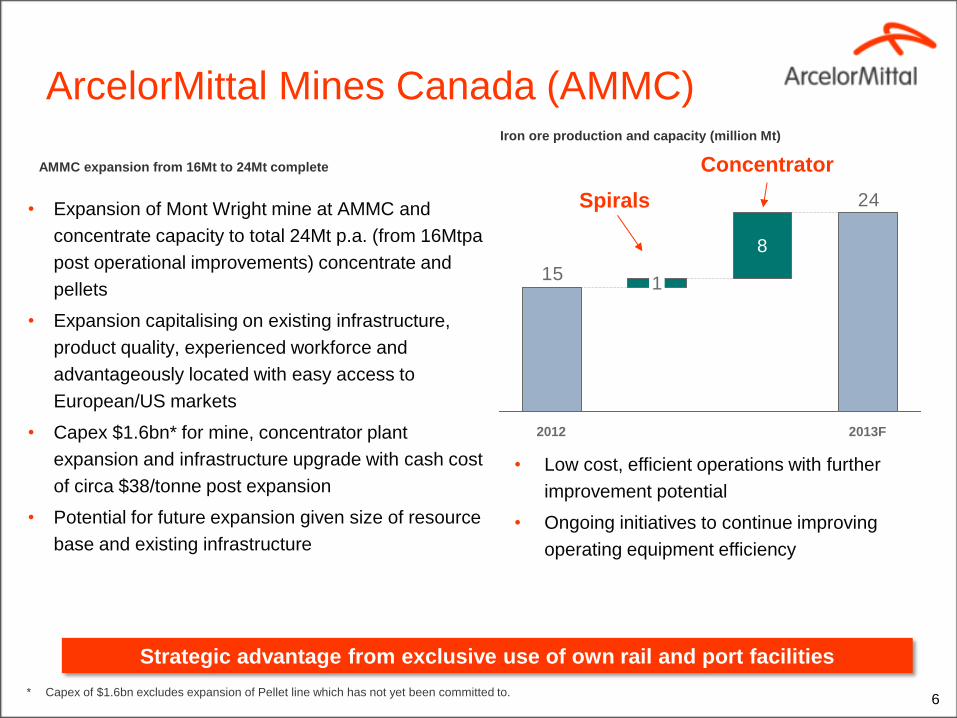

ArcelorMittal Mines Canada (AMMC)

• Expansion of Mont Wright mine at AMMC and

concentrate capacity to total 24Mt p.a. (from 16Mtpa

post operational improvements) concentrate and

pellets

• Expansion capitalising on existing infrastructure,

product quality, experienced workforce and

advantageously located with easy access to

European/US markets

• Capex $1.6bn* for mine, concentrator plant

expansion and infrastructure upgrade with cash cost

of circa $38/tonne post expansion

• Potential for future expansion given size of resource

base and existing infrastructure

* Capex of $1.6bn excludes expansion of Pellet line which has not yet been committed to. 6

• Low cost, efficient operations with further

improvement potential

• Ongoing initiatives to continue improving

operating equipment efficiency

Iron ore production and capacity (million Mt)

AMMC expansion from 16Mt to 24Mt complete

Strategic advantage from exclusive use of own rail and port facilities

24

15

2013F

8

1

2012

Concentrator

Spirals

Expansion

• Commission of new spirals line at concentrator

• New trucks operational

• Additional rail sidings completed

Railway

• Wholly-owned 420-km railway infrastructure

• Longer train with two locomotives commenced

• Linking mining operations to Port-Cartier

Port-Cartier

• One of Canada’s largest private ports

• Handling 160,000+ tonne ships

• Currently running at ~350 vessels per year

• Ability to handle cape-size vessels all year

round

7 7

ArcelorMittal Mines Canada (AMMC) Expansion from 16Mt to 24Mt complete

Expansion supported by captive infrastructure with operating leverage

Baffinland Early Revenue Phase: 3.5MT production rate in 2015

8

Product

• High grade: 66%+ Fe iron – lumps and fine ore

• Products expected to achieve full premium value

Proposed Early Revenue Phase rationale

• ERP budget approx. US$700m commenced in 1Q 2013

• Enables an early mining phase that requires less capital investment than full

project, creating training, employment, business opportunities for local region

• ERP will demonstrate quality of product and ability to operate

ERP components and difference between full rail project

• ERP requires trucking of ore to Milne Inlet, loading of ore in Milne Inlet, and

shipping of ore from Milne Inlet to markets

• Requires upgrades of the road connecting Milne Inlet and mine site

• Mining and trucking of 3.5mtpa from Deposit 1 to Milne Inlet throughout the year

• Shipping of ore from Milne Inlet during “open water season”

• Anticipate first ore to be shipped in 2H 2015, all product tonnage targeted for

Europe

Environment permitting

• Existing permits allow work to commence in 3Q’13

• Planned modification to existing permit to allow further optimization:

doubling of fuel capacity at Milne Inlet in 2013

• Completion of ERP amendments to “The Project Certificate” and licenses

scheduled in 1H 2014

Mary River Project is now a phased project –

ERP underway, Rail Phase to be considered according to market conditions

ERP phase underway : Road route

Proposed phase 2: Rail

Brazil ArcelorMittal operates two iron ore mines at Brazil – ArcelorMittal Brazil -

Andrade Mine and ArcelorMittal Mineracao Serra Azul

Andrade Mine

• Operates an open pit and a crushing facility

• Supplies sinter feed to ArcelorMittal Long Carbon – João Monlevade

integrated plant through an internal railway of 11 kilometers.

• Companhia Siderurgica Belgo-Mineira (CSBM) initiated mining

operations in 1944 to supply ore to its steel plant in Joao Monlevade.

In 2000, Vale acquired the property and in 2009 Vale returned the

Anadrade mine to CSBM, which, then transferred it to ArcelorMittal.

• The increase of the mine’s production capacity to 3.5mt per year of

sinter feed was completed in 2012

• Reserve estimates are dominated by directly shippable hematite ore

ArcelorMittal Mineracao Serra Azul

• Operates an open pit mine and a concentration facility

• Sinter feed production is shipped to ArcelorMittal plants in Europe,

local Brazilian market including the ArcelorMittal Brazil integrated

plants. Reserve estimates constitute rich friable Itabrites requiring

some beneficiation.

• Both Andrade & Serra Azul are located in the Iron Quadrangle

(Quadrilatero Ferrifero)

• Project of High Intensity Magnetic Separator (“HIMS”) to improve the

quality & Yields

• PFS studies underway to expand from 2mt to 8mt Itabirite ore 9

Focus on cost as well as growth

10

Relentless focus on cost control

• Operational excellence, rigour and discipline

underway across assets

• Share and apply best practice leveraging internal and

external benchmarks

• Key focal points:

• Labour productivity

• Maintenance and reliability

• Mining plan optimization

Rigorous capex investment management

• Focus on on-time and budget delivery

• Central project management office

• Regular expert project reviews

• Standardised projects controls

• Tracking time/cost divergence and risks

1st

US

$ F

OB

C

ost per

ton

AMMC ArcelorMittal

Liberia

Post capex FOB cash cost

Positioning key assets low on the cost curve

* Focus on AMMC and ArcelorMittal Liberia as our largest marketable tonnes assets. Illustrative for post expansion of AMMC

Illustrative cash cost curve (marketable

tonnes) post expansion

Relentless focus on costs and capex monitoring

2nd 3rd 4th

Quartile

Focus on value

and OEE

initiatives Focus on

quality

Mexico ArcelorMittal operates three iron ore mines in Mexico, the El Volcan and

Las Truchas mines and, through a joint ownership with Ternium S.A., the

Peña Colorada mine

El Volcan

• ArcelorMittal operates a concentrating facility along with a open pit

mine and a pre-concentration facility at the mine site. The Volcan

concession was bought from the Sonora provincial government in

2004, followed by the exploration at the property in 2005. The

development of the mine started in 2007. The Volcan operations

produced 2.15mt of concentrate in 2012

Las Truchas

• Fully integrated iron ore operation, It began operating in 1976 as a

government enterprise (Sicartsa) and its mining activities consist of

an open pit mine exploitation, crushing, dry cobbing, preconcentrate

and concentration plant. The aggregate 2012 production concentrate,

lumps and fines totaled 2.93mt

Peña Colorada

• ArcelorMittal holds 50% of Peña Colorada Ltd., and Ternium S.A.

owns the other 50% of the company. Peña Colorada operates an

open pit mine as well as a concentrating facility and a two line

pelletizing facility. Total pellet production of 4.07mt and 0.43mt of

concentrate (of which 50% is ArcelorMittal share).

11 7mt of Iron Ore Production in 2012

USA - ArcelorMittal USA Iron Ore Mines

• ArcelorMittal USA operates an iron ore mine through its wholly-

owned subsidiary ArcelorMittal Minorca & owns a majority stake

in Hibbing Taconite Company, which is managed by Cliffs Natural

Resources. ArcelorMittal Minorca production for 2012 was 3mt

and 5mt for Hibbing Taconite Company*

ArcelorMittal Minorca

• Located north of the town of Virginia in the northeast of

Minnesota

• The Minorca operations control all the mineral rights and surface

rights needed to the mine

• Concentrating and a Pelletizing facility along with two open pit

iron ore mines

• The processing operations consists of a crushing facility, a three

line concentration facility and a single line straight grate

pelletizing plant

• Pellets are transported by rail to ports on Lake Superior. Lake

vessels are then used to transport the pellets to Indiana Harbor

• The Minorca taconite plant was constructed and operated by

Inland steel between 1977 & 1988 when it was purchased by then

ISPAT International, a predecessor company of ArcelorMittal

*ArcelorMittal share of production

12