Embed Size (px)

Citation preview

RISK MANAGEMENT TECHNIQUESLoreto “Jong” Dumlao Azores, Jr.

Polytechnic University of the Philippines, Graduate School

DBA 737 Risk Management & Development

1st Semester 2014-2015

Dr. Rodolfo De Lara

Professor

RISK MANAGEMENT TECHNIQUESHTTP://WWW.RISCARIO.COM/RISK-MGMT-TECHNIQUES

A. Pure risks (chance of loss but no chance of gain) A category of risk in which loss is the only possible outcome; there is no beneficial result. Pure risk is related to events that are beyond the risk-taker's control and, therefore, a person cannot consciously take on pure risk. This is the opposite of speculative risk. 1. risk avoidance2. loss control

B. Speculative risks (chances of gain or loss ). A category of risk that, when undertaken, results in an uncertain degree of gain or loss. All speculative risks are made as conscious choices and are not just a result of uncontrollable circumstances. Speculative risk is the opposite of pure risk.1. risk retention2. risk transfer

RISK AVOIDANCE

1. Elimination of risk at any cost (e.g., drop a hazardous product)

2. Most aggressive and effective … but not practicaleg, staying in bed all day to avoid risk of injury or death

LOSS CONTROLHTTP://WWW.ATLENVATLANTA.COM/LOSS.HTML

Loss Control – Are all the methods taken to reduce the frequency and/or severity of losses including exposure avoidance, loss prevention, loss reduction, segregation of exposure units and non-insurance transfer of risk.

1. loss prevention: reduce frequency of lossusually impossible or impractical

(e.g., to maintain income —> insurance or adopt a healthier lifestyle

2. loss reduction: reduce the severity and financial impacteg, upon disability —> physical rehabilitation, crosstrain a backup

3. safety measures, pooling, segregating (e.g., key employees travel separately), diversifying (not imperiling group by one member’s actions)

TOTAL LOSS CONTROL: A concept of accident investigation and prevention which takes into account such factors as damage to property and equipment, lost time, and wasted resources. This approach includes recording and evaluating “near misses” and “incidents” that may have resulted in an interruption of production, spill or leak of material, unscheduled maintenance of equipment, or event where an individual narrowly avoided an injury

Such an approach attempts to take advantage of not waiting for a loss to occur but identifies actions or events that could have resulted in injury or loss and using this information to prevent losses in the future.

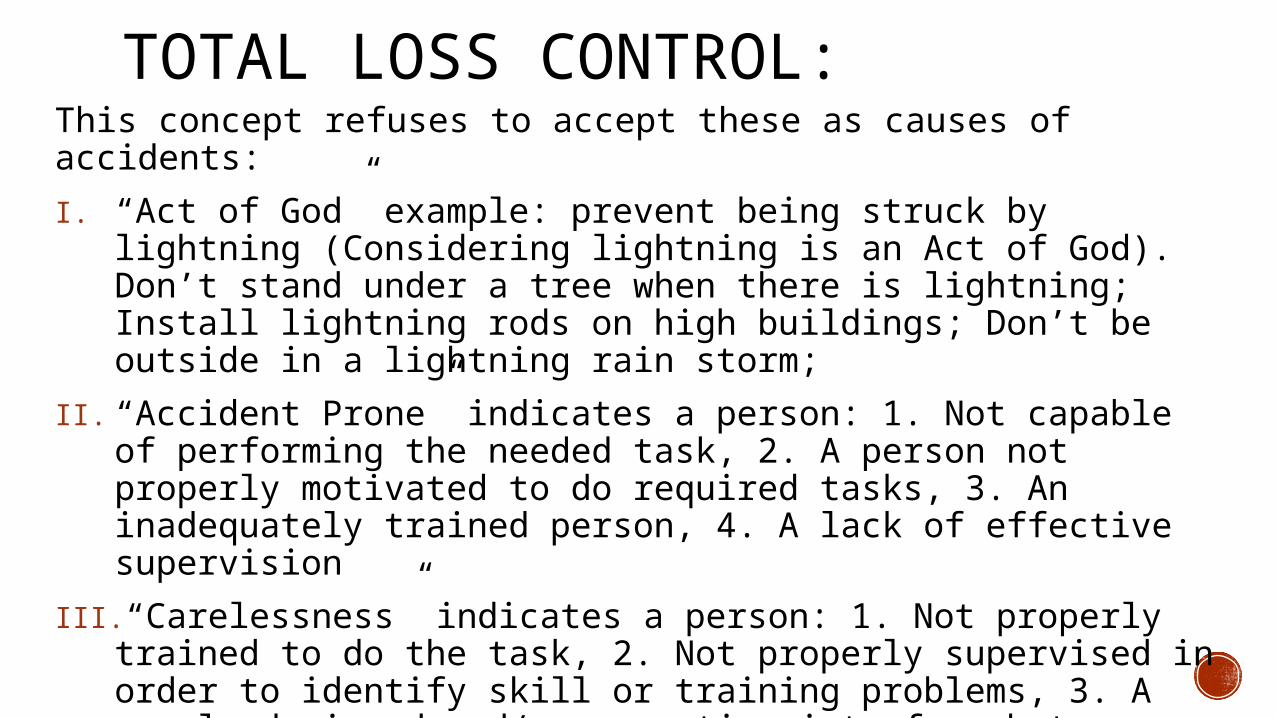

TOTAL LOSS CONTROL: This concept refuses to accept these as causes of accidents:

I. “Act of God” example: prevent being struck by lightning (Considering lightning is an Act of God). Don’t stand under a tree when there is lightning; Install lightning rods on high buildings; Don’t be outside in a lightning rain storm;

II. “Accident Prone” indicates a person: 1. Not capable of performing the needed task, 2. A person not properly motivated to do required tasks, 3. An inadequately trained person, 4. A lack of effective supervision

III. “Carelessness” indicates a person: 1. Not properly trained to do the task, 2. Not properly supervised in order to identify skill or training problems, 3. A poorly designed and/or operating interface between man and machine, 4. An ergonomic problem of work speed, body position, and or weight of materials, 5. A poorly motivated person due to lack of training or supervision

TOTAL LOSS CONTROL: LOSS CONTROL IS GAMBLING – but potentially very profitable gambling! The greater the effort to prevent losses – the greater the odds that there will be fewer and fewer losses as time goes on. Injuries to employees, damaged equipment, and loss of raw materials and product, are all means of reduction of profits and increase in losses. Total Loss Control is an ideal way to increase profits without increasing prices even when raw material prices or “cost of goods sold” increase.

RISK RETENTION/ REDUCTION

Finance some or all of the losses yourselfeg, health insurance has deductibles and waiting period

RISK TRANSFER

1. Noninsurance eg, relatives help out

2. Insurance formal arrangement between you and an insurer

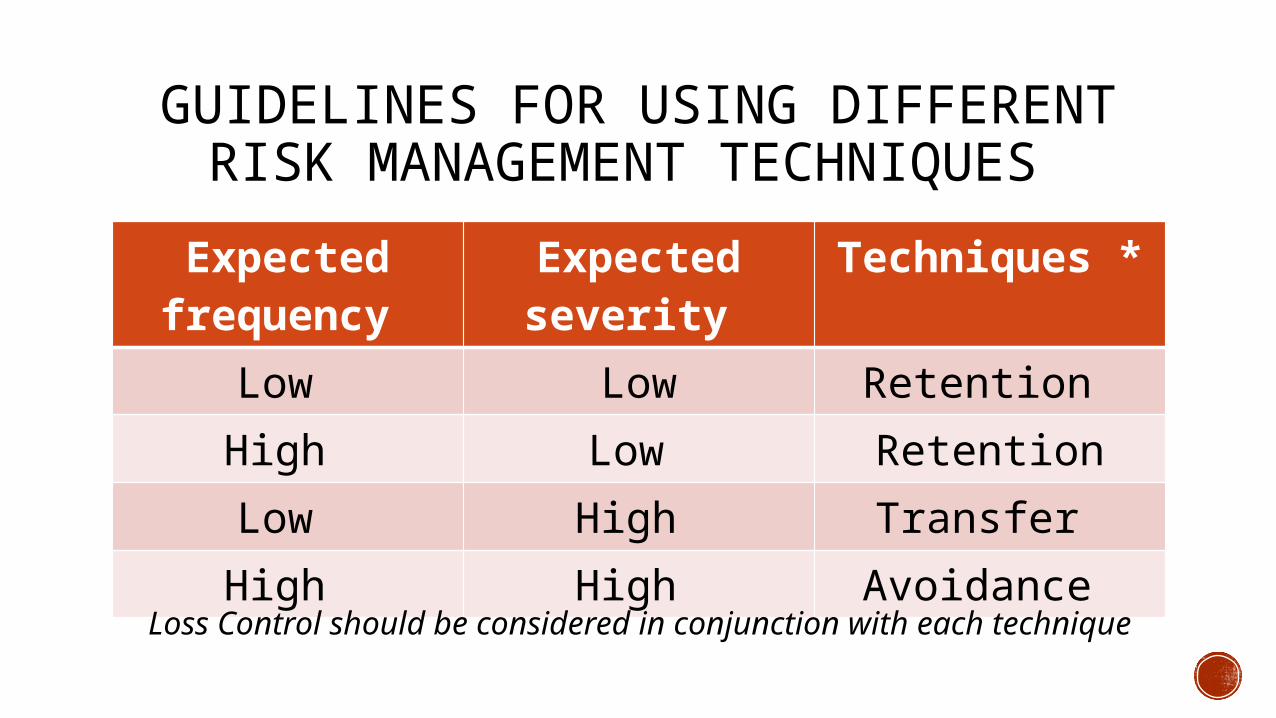

GUIDELINES FOR USING DIFFERENT RISK MANAGEMENT TECHNIQUES

Expected frequency

Expected severity

Techniques *

Low Low Retention High Low RetentionLow High Transfer High High Avoidance

Loss Control should be considered in conjunction with each technique

Thank You