Embed Size (px)

Citation preview

1

Evaluation of Share Price of A.G. Barr PLC

2

ABSTRACT

The main aim of this dissertation is to evaluate the share price of A. G. Barr Plc. and to provide

recommendations to investors. For this, the existing literature is reviewed and various theories on

capital structure decision are analysed. The traditional approach and MM approach of capital

structure are examined under this. Using weighted average cost of capital, A.G. Barr’s capital

structure is evaluated. It is mainly composed of equity and reserves and only 0.1 of the capital is

debt. As the company is less depending on debt, its interest rates are very low. The profitability,

liquidity and financial performance of the company are good. The cash flow statement analysis

reveals that the company efficiently meets its operating activities without any burden.

Using Dividend Discount Model, discounted cash flows and abnormal earnings method, A. G.

Barr’s share price is evaluated as per which the company’s current trading price is overvalued.

However, all these method have certain limitations. It mainly depends on the historic dividend

and forecasts the future dividends which may not be accurate in the real scenario. This method is

also not ideal for firms that do not pay dividends. The procedures of both discounted cash flow

method and discounted abnormal earnings are different, and the values mainly depend on

forecasts which may not be accurate in true situations. The trends of share price reveal that the

price is volatile to major up hills and down trends constantly. Furthermore, the forecasted share

price is far ahead of the current market price. Hence, ideally it is recommended buy the share.

3

Contents

1. Introduction ....................................................................................................................................8

1.1. Objectives ................................................................................................................................8

1.2. Structure ..................................................................................................................................8

1.3. Company Overview ..................................................................................................................8

1.4. Limitations of Analysis ........................................................................................................... 10

2. The Outlook for the Economy........................................................................................................ 12

2.1. Global Economy .................................................................................................................... 12

2.2. UK Economy ......................................................................................................................... 14

2.3. Implications for A. G. Barr Plc. ............................................................................................... 16

2.4. Conclusion............................................................................................................................. 16

3. The Structure and Outlook for the Industry ..................................................................................... 17

3.1. The UK Soft drink Industry..................................................................................................... 17

3.2. The Outlook for Soft drink Industry ......................................................................................... 18

3.3. The Five Forces...................................................................................................................... 19

3.3.1. Threat of New Entrants..................................................................................................... 19

3.3.2. Rivalry among the Existing Firms ..................................................................................... 20

3.3.3. Bargaining Power of Suppliers .......................................................................................... 21

3.3.4. Bargaining Power of Buyers ............................................................................................. 21

3.3.5. Threat of Substitutes......................................................................................................... 21

3.4. Conclusion............................................................................................................................. 22

4. Literature Review ......................................................................................................................... 23

4.1 Introduction ............................................................................................................................ 23

4.2 Dividend Policy theoretical framework ..................................................................................... 26

4.3 Hypothesis of Dividend Irrelevance .......................................................................................... 27

4.4 Common Irrelevance Thesis ..................................................................................................... 28

4.5 M&M Irrelevancy Proof ........................................................................................................... 29

4.6 The conception of earning theory............................................................................................. 30

4.7 Theoretical review of Macroeconomic factors and Dividends ..................................................... 31

4.8 Dividends and Models of Equilibrium....................................................................................... 32

4.9 Dividend policy Signaling effect .............................................................................................. 32

4.10 Dividend Policy behavioral models ......................................................................................... 33

5. The Capital Structure Decision ...................................................................................................... 37

4

5.1. Introduction ........................................................................................................................... 37

5.2. Various Theories on Capital Structure...................................................................................... 38

5.3. The Traditional Approach ....................................................................................................... 42

5.3.1. Explanation ..................................................................................................................... 42

5.3.2. Aside............................................................................................................................... 42

5.4. The Economic Approach......................................................................................................... 43

5.3.1. MM Propositions without Taxes........................................................................................ 43

5.3.1. MM Propositions with Corporate Taxes............................................................................. 45

5.5. Imperfections ......................................................................................................................... 46

5.6. Additional Research ............................................................................................................... 47

5.7. Conclusion............................................................................................................................. 47

6. Company Analysis ........................................................................................................................ 48

6.1. Introduction ........................................................................................................................... 48

6.2. Strategic Capabilities .............................................................................................................. 48

6.3. Board of Directors and Corporate Governance.......................................................................... 49

6.4. Capital Structure .................................................................................................................... 50

6.4.1. Shareholding.................................................................................................................... 51

6.4.2. Leverage.......................................................................................................................... 51

6.5. Financial Performance ............................................................................................................ 52

6.5.1. Profitability ..................................................................................................................... 52

6.5.2. Liquidity.......................................................................................................................... 54

6.5.3. Cash Flow Analysis .......................................................................................................... 55

6.6. SWOT Analysis ..................................................................................................................... 55

6.7. Conclusion............................................................................................................................. 57

7. Company Share Valuation ............................................................................................................. 58

7.1. Introduction ........................................................................................................................... 58

7.2. Dividend Discount Model ....................................................................................................... 58

7.2.1. Discount Rate .................................................................................................................. 58

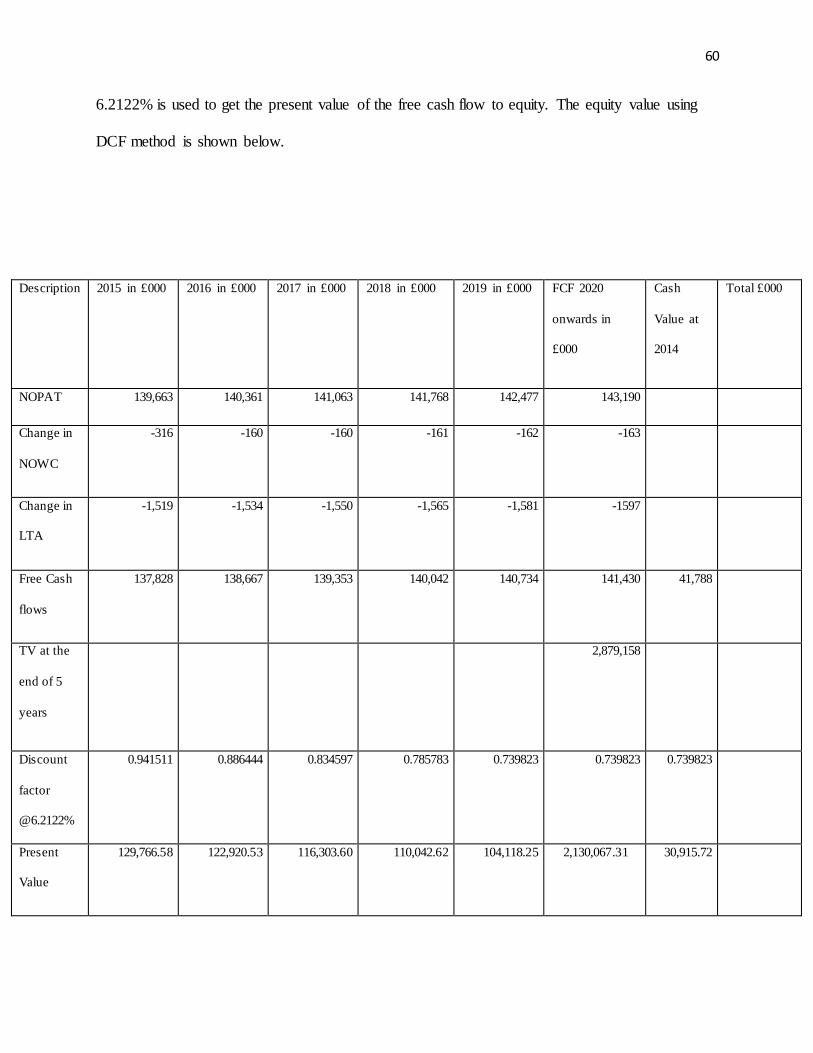

7.2.2. Discount Cash Flow Method ............................................................................................. 59

7.2.3. Discount Abnormal Earnings Method ................................................................................ 61

7.3. Sensitivity Analysis ................................................................................................................ 64

7.4. Limitations of Share Valuation Methods .................................................................................. 69

7.5. Technical Analysis ................................................................................................................. 69

5

7.6. Conclusion............................................................................................................................. 72

8. Conclusion and Recommendations ................................................................................................. 73

8.1. Summary ............................................................................................................................... 73

8.2. Share Price Performance ......................................................................................................... 74

8.3. Recommendations .................................................................................................................. 74

Appendices ...................................................................................................................................... 75

Appendix 1 Assumptions for Valuation Models .............................................................................. 75

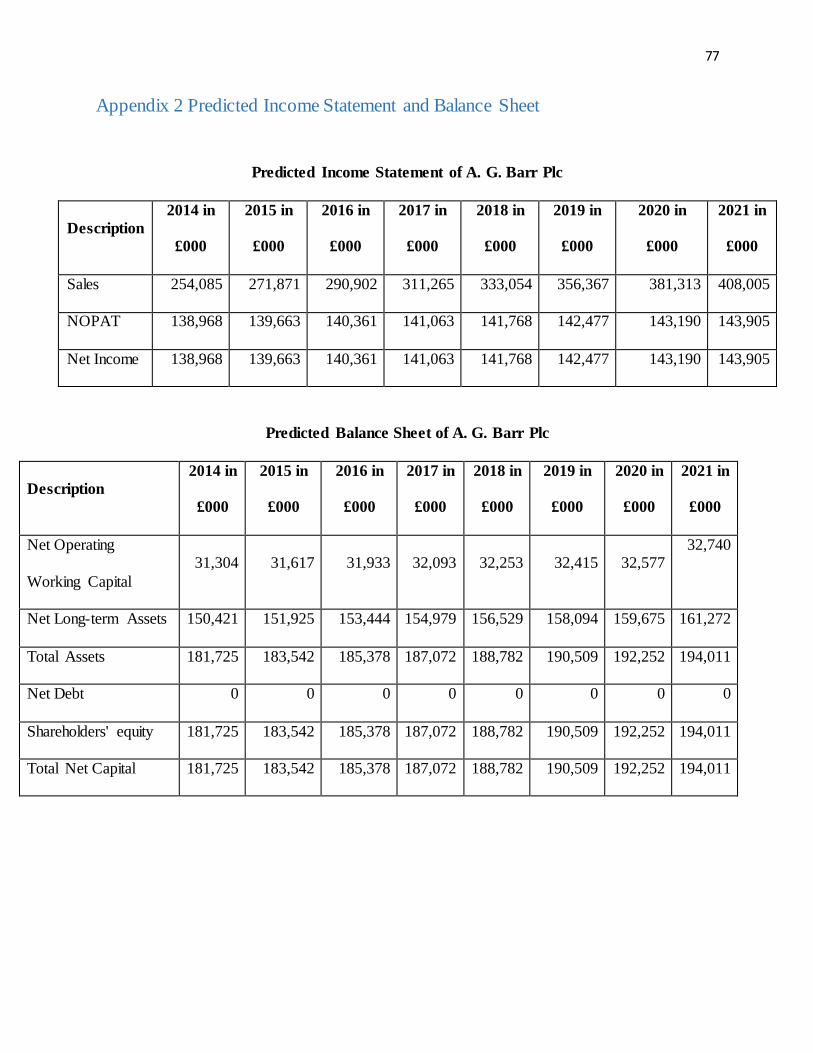

Appendix 2 Predicted Income Statement and Balance Sheet ............................................................ 77

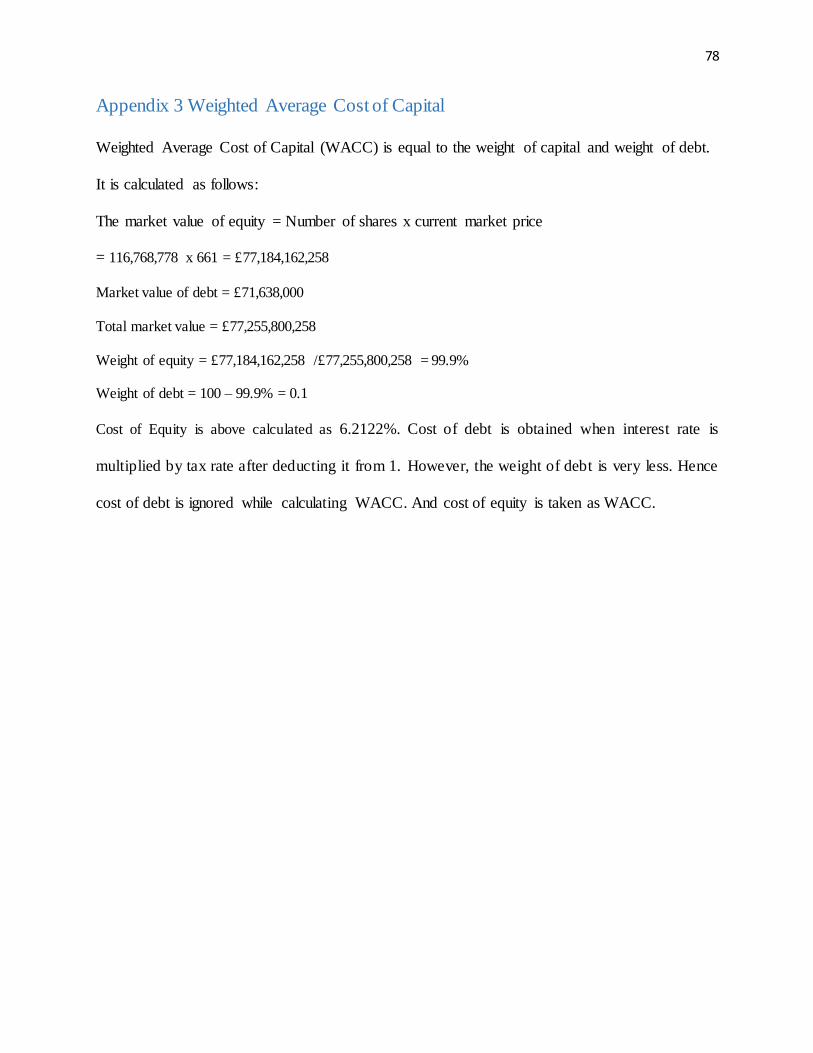

Appendix 3 Weighted Average Cost of Capital ............................................................................... 78

References ....................................................................................................................................... 79

6

List of Tables

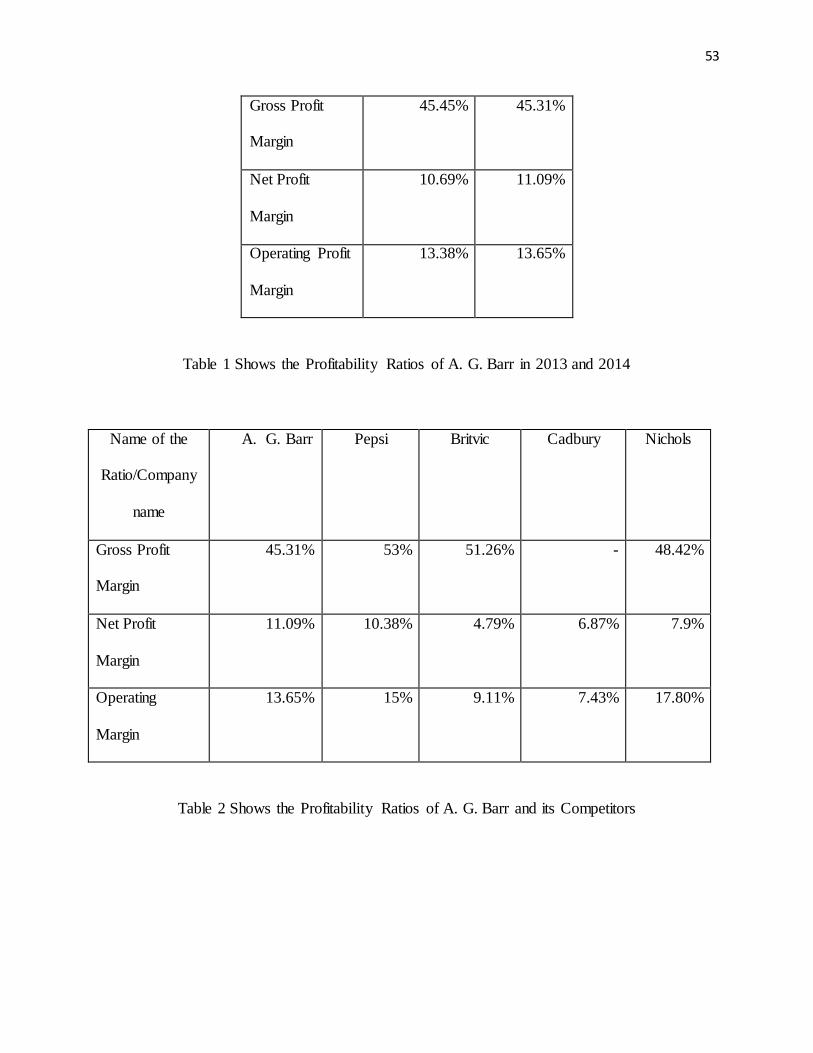

Table 1 Shows the Profitability Ratios of A. G. Barr in 2013 and 2014 38

Table 2 Shows the Profitability Ratios of A. G. Barr and its Competitors 38

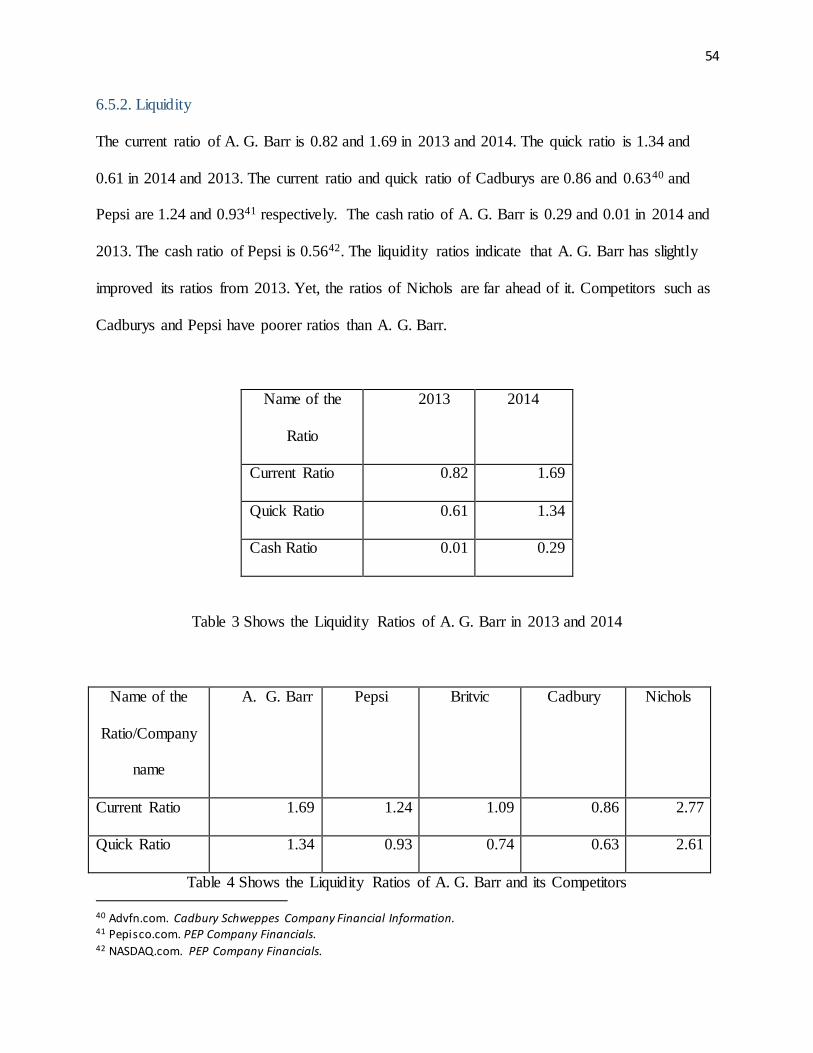

Table 3 Shows the Liquidity Ratios of A. G. Barr in 2013 and 2014 39

Table 4 Shows the Liquidity Ratios of A. G. Barr and its Competitors 39

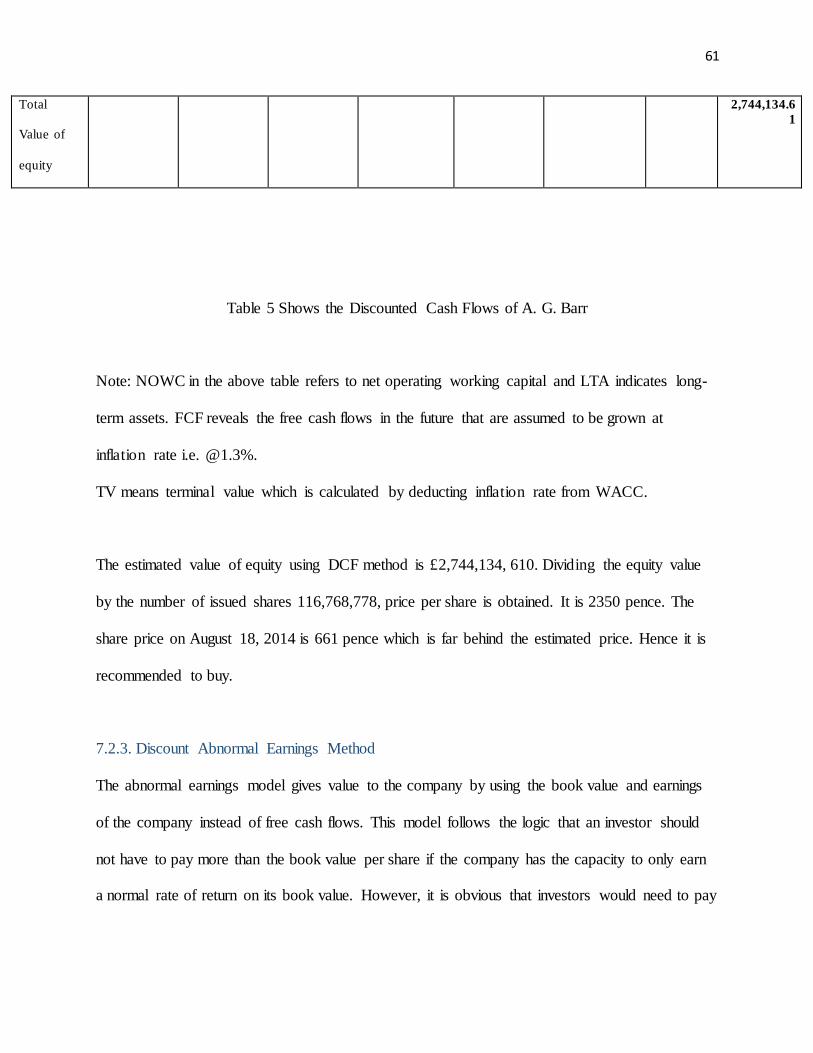

Table 5 Shows the Discounted Cash Flows of A. G. Barr 45

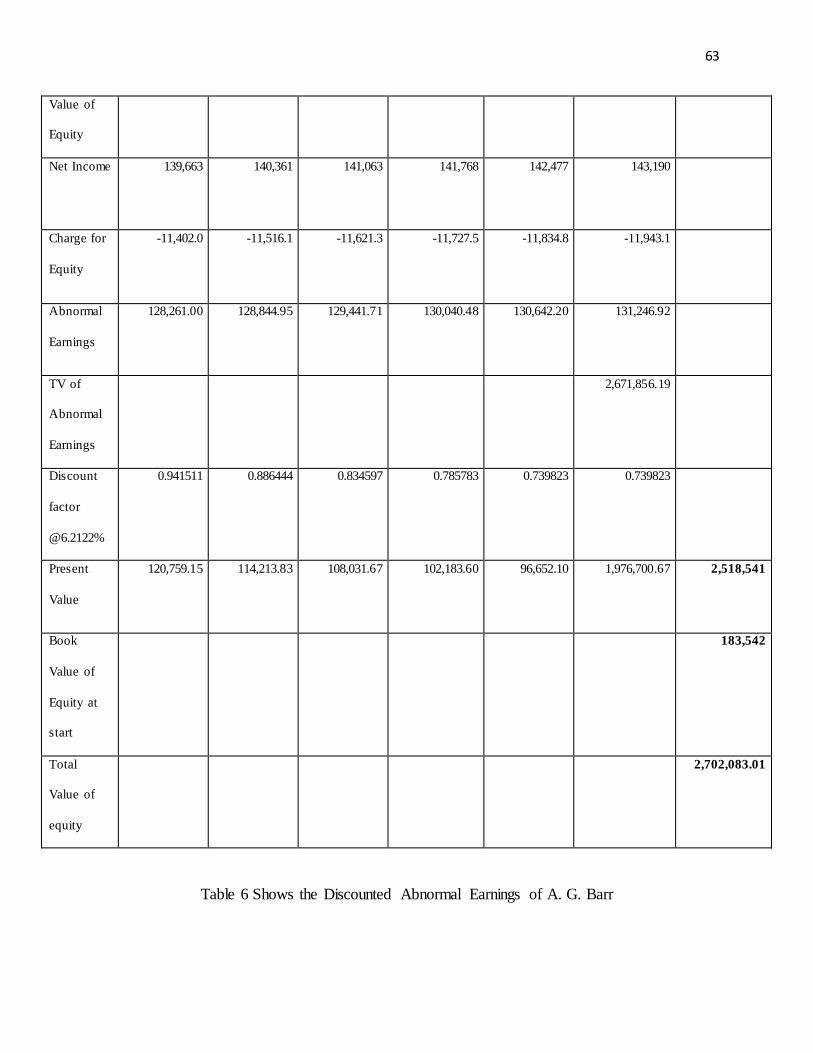

Table 6 Shows the Discounted Abnormal Earnings of A. G. Barr 48

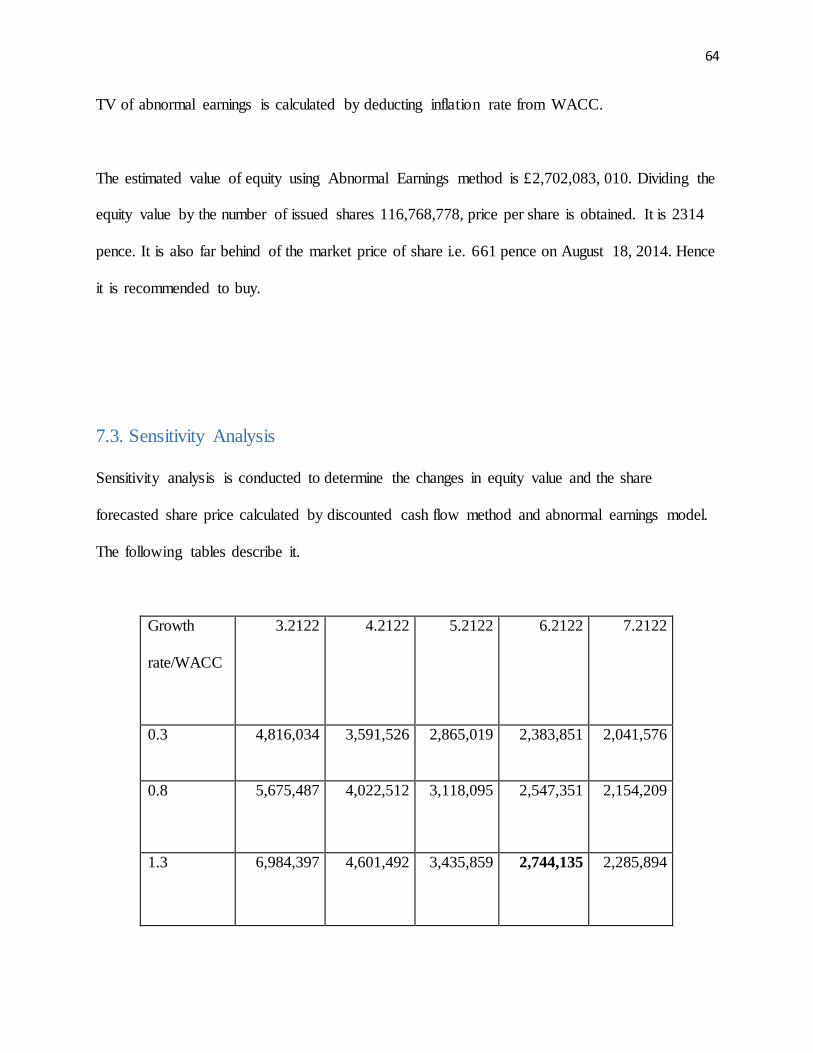

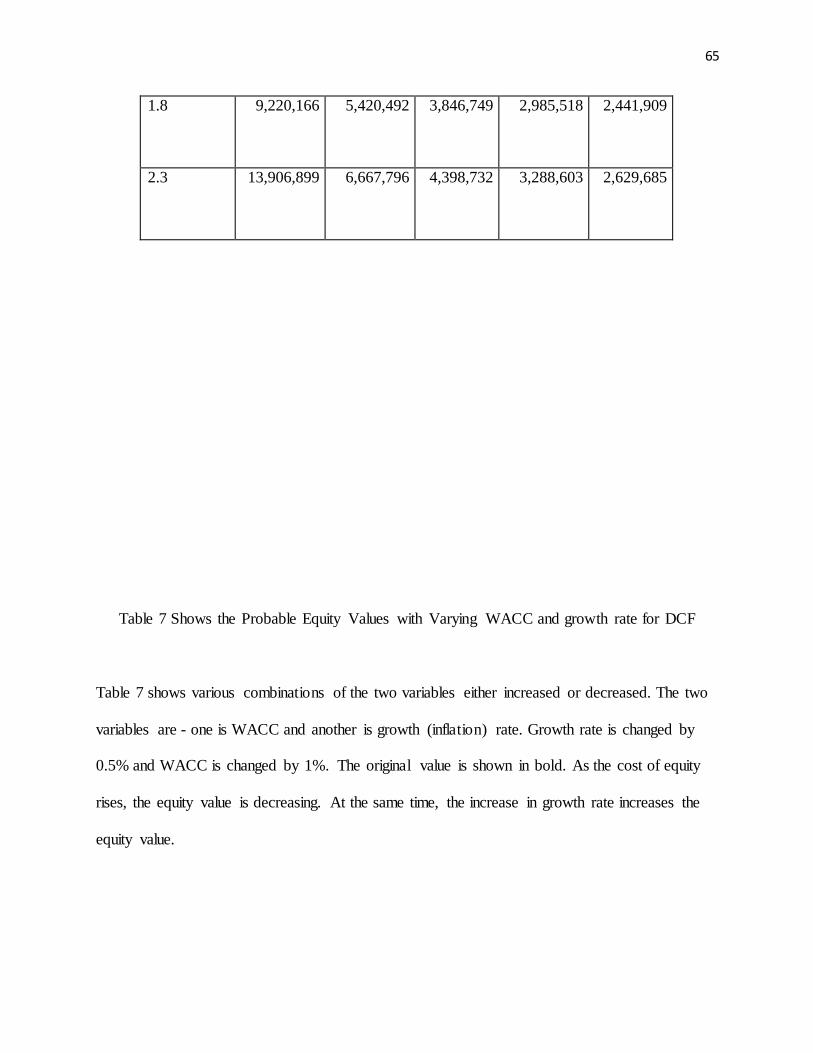

Table 7 Shows the Probable Equity Values with Varying WACC and growth rate for DCF

49

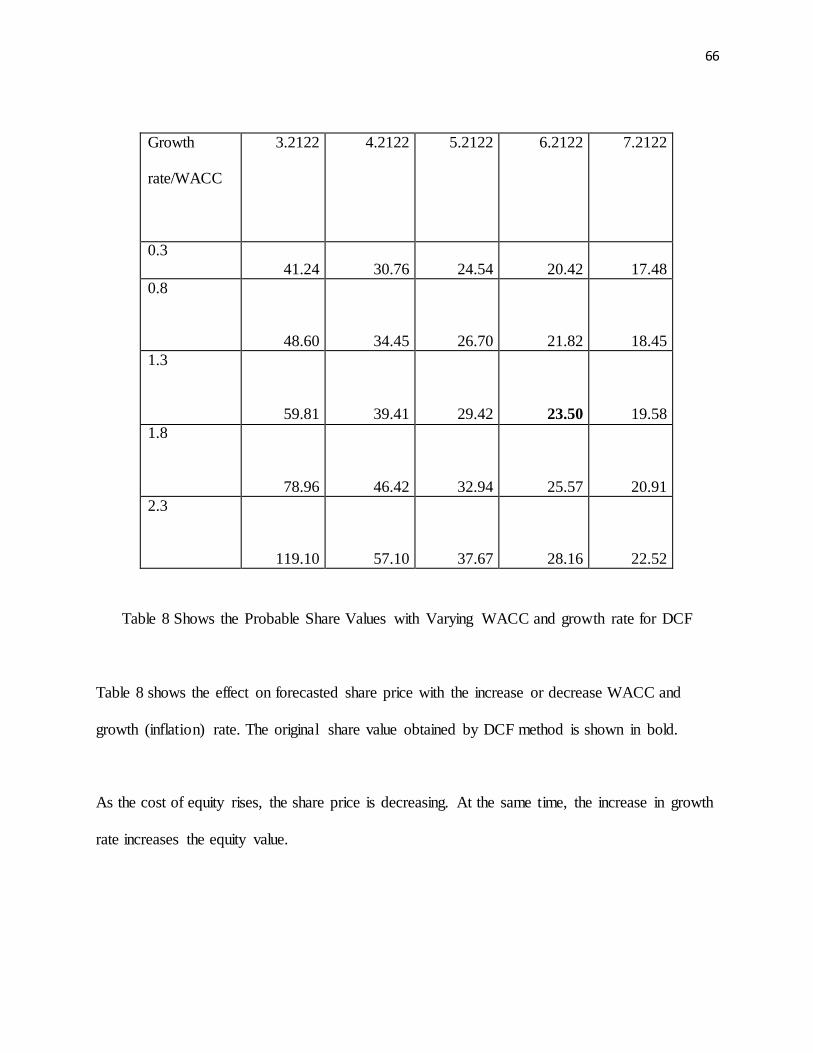

Table 8 Shows the Probable Share Values with Varying WACC and growth rate for DCF 50

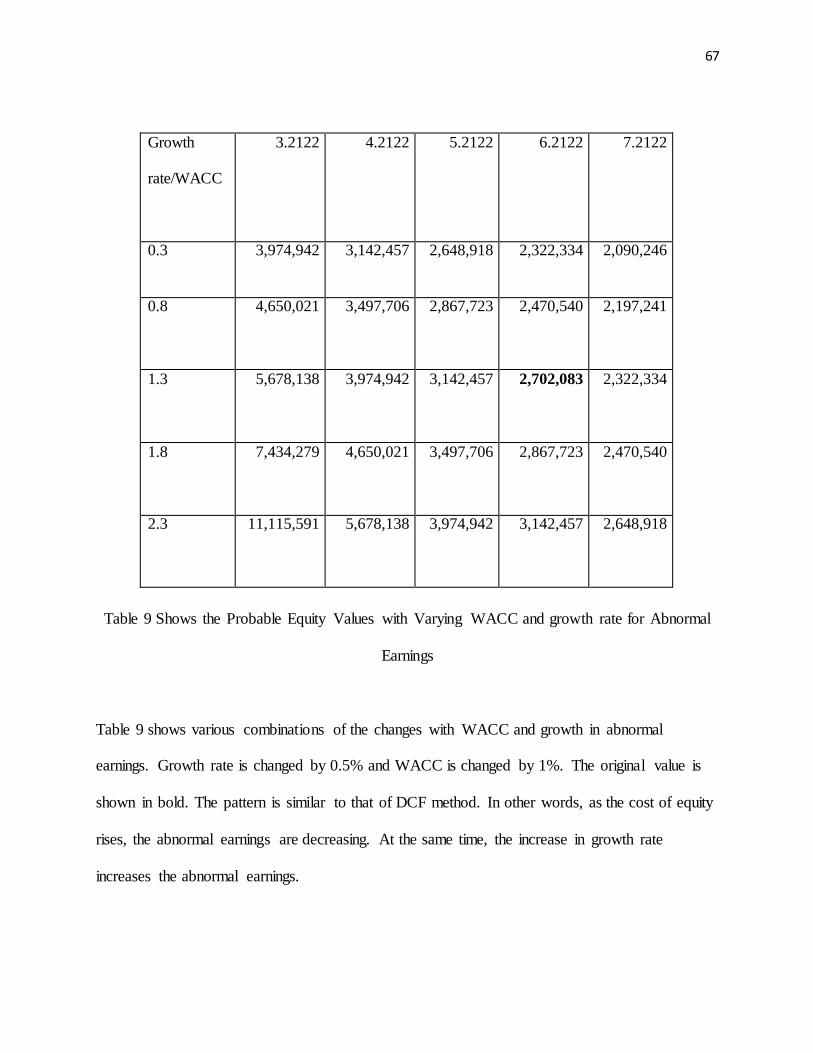

Table 9 Shows the Probable Equity Values with Varying WACC and growth rate for Abnormal

Earnings 51

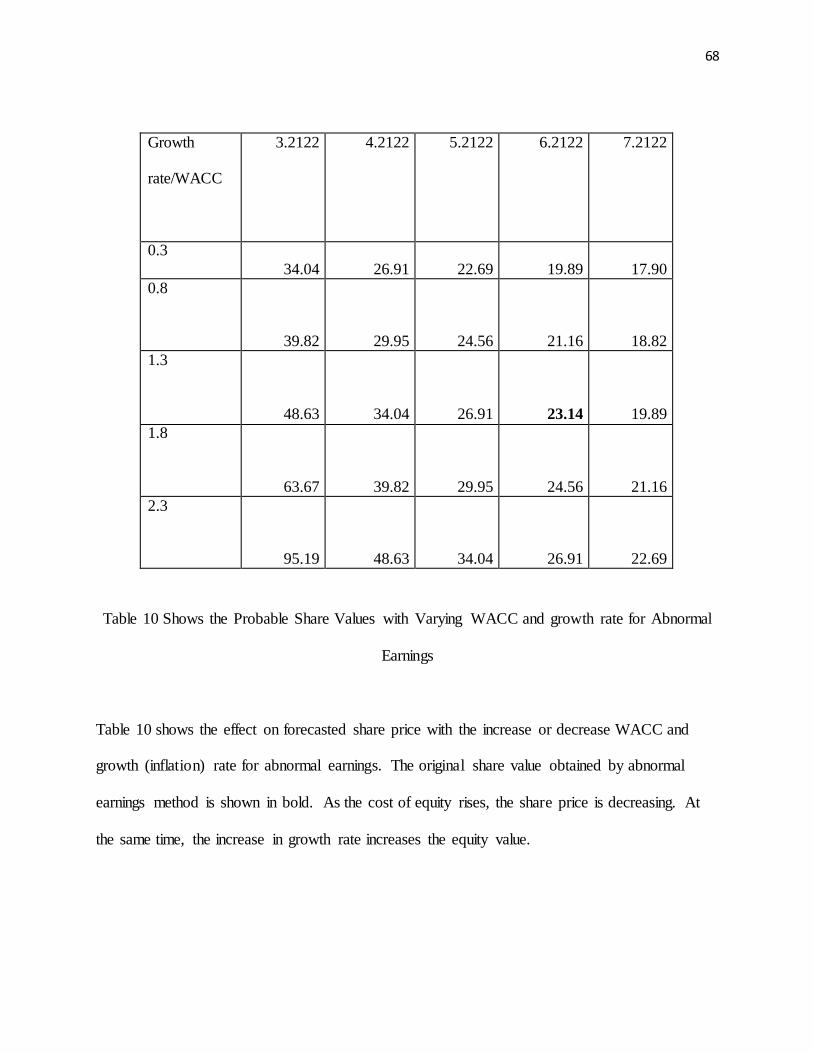

Table 10 Shows the Probable Equity Values with Varying WACC and growth rate for Abnormal

Earnings 52

7

List of Figures

Figure 1 Global outlook for GDP during 2014 – 2025 12

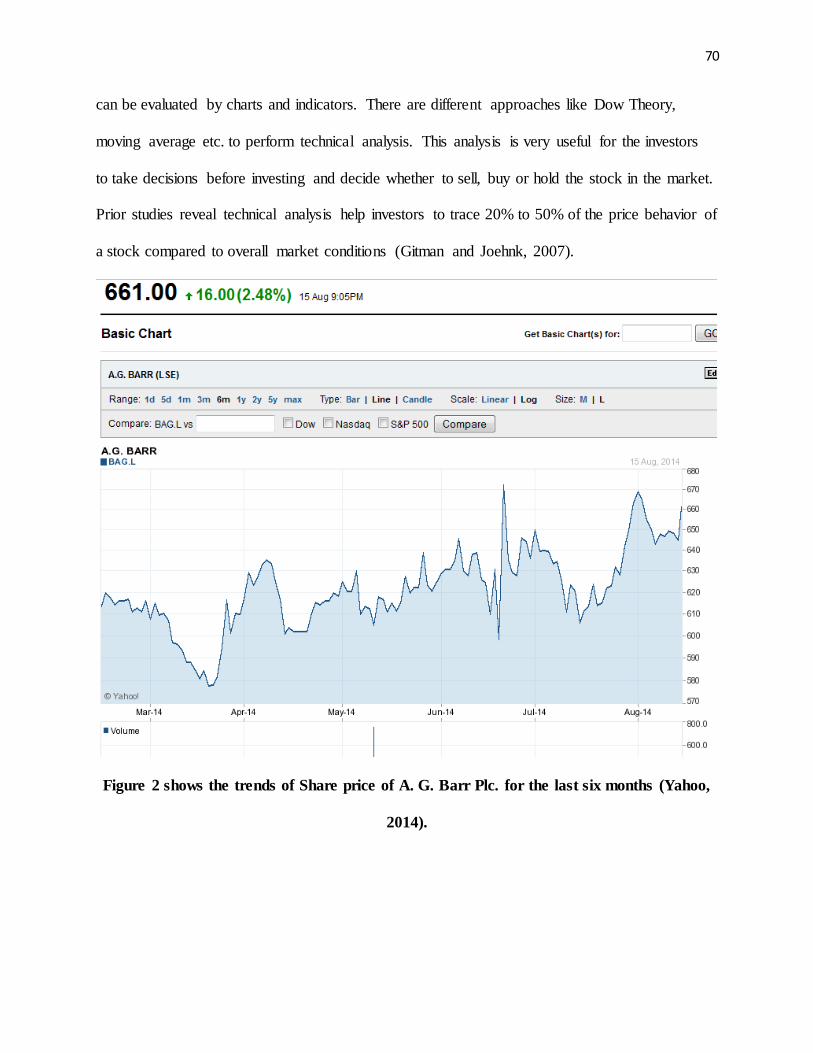

Figure 2 Trends of Share price of A. G. Barr Plc. for the last six months 41

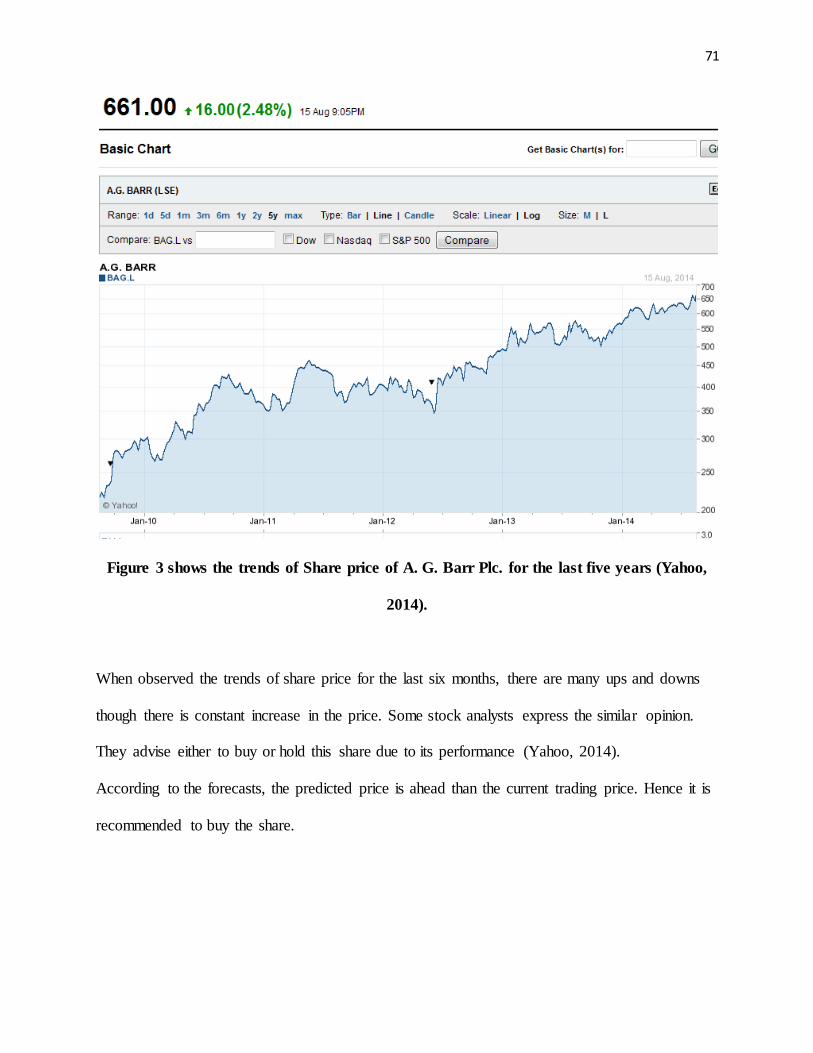

Figure 3 Trends of Share price of A. G. Barr Plc. for the last five years 42

8

1. Introduction

1.1. Objectives

This dissertation is written as part of Master’s degree. The objectives of this dissertation are to

evaluate the share price of A.G. Barr Plc. and make a forecast based on the annual reports of last

five years. It is also aimed to make recommendations to current and prospective investors

whether to buy, hold or sell the shares of the company.

1.2. Structure

This dissertation consists of total seven chapters. The first chapter begins with the objectives of

the dissertation and consists of the structure of dissertation, company overview and limitations of

analysis. Chapter 2 describes the outlook of economy and its implications for A.G. Barr Plc.,

chapter 3 states the structure and outlook for the industry, chapter 4 examines the existing

literature on the topic i.e. the capital structure of the company, chapter 5 indicates the analysis of

A.G. Barr Plc. with the help of ratios and SWOT1, chapter 6 discusses the valuation of company

shares using various available models such as Dividend Discount Model, and sensitivity analysis,

and chapter 7 contains the conclusions and recommendations.

1.3. Company Overview

A.G. Barr Plc. is a Scottish soft drink manufacturing company that is listed on the London stock

exchange. The Company in this dissertation is sometimes referred as A.G. Barr for the sake of

convenience. It was founded by Robert Barr in 1876 and headquartered at Cumbernauld. The can

line here can produce 690 million cans per year. The company is commonly known as Barr’s.

1 Strengths, Weaknesses, Opportunities and Threats

9

The company is renowned for its IRN-BRU for more than a century. It has a huge market

throughout the UK. Other brands of A.G. Barr Plc. include KA, Rubicon, Barr, Simply, St

Clements, Findlays, Abbot’s, Sun exotic, Strathmore Water, D‘N’B and Tizer (A.G. Barr Plc.,

2014). Their partnership brands are Orangina, Rockstar and Snapple (A.G. Barr Plc. Annual

Report, 2014).

The popular brand of A. G. Barr - IRN-BRU is famous in Scotland and the bestselling drink

there after scotch. The company has constantly growing year by year with their three vital

channels that distribute soft drinks in the UK. These include take home category that contains

several grocers, impulse that consists of newsagents, corner shops etc. and premise that has

hotels, pubs, cafes, restaurants, clubs etc. (A.G. Barr Plc. (a), 2014).

The turnover of the company has increased by 6.9%2 and the profit margin has increased by

13.5%3 in 2014. The company wants to establish long-term relationships by focusing on their

needs, creates brands accordingly using innovations. The performance of A.G. Barr is increased

due to growth in carbonate drinks which is raised by 8.2% in the total value. IRN-BRU and Barr,

the main carbonate brands promoted this growth. Except the brand KA all other brands exhibit

some growth in terms of sales and revenue (A.G. Barr Plc. Annual Report, 2014).

In terms of brands, IRN-BRU is the major brand that is sold more in 2014 and accounted for

4.3%4 growth in sales. In terms of geography, Scotland contributed to about 40% of sales

2 A.G. Barr Plc. Annual Report and Accounts 2014, p. 4 3 A.G. Barr Plc. Annual Report and Accounts 2014, p. 4 4 A.G. Barr Plc. Annual Report and Accounts 2014, p. 8

10

revenue. Wales and England contributed to the remaining of their domestic sales revenue which

has grown by 9% (A.G. Barr Plc. Annual Report, 2014).

Among their partnership brands, Rockstar is the best performing brand which is growing over

the years. Different flavors are introduced with various pack designs to attract customers. Even

though the growth for energy drink market is slow, Rockstar has been proving its performance

with a growth of more than 60%5 (A.G. Barr Plc. Annual Report, 2014).

The competitors of A. G. Barr Plc. in the UK are Britvic Plc., Cadbury Schweppes Plc. and

Nichols Plc. The main global competitors of the company are The Coca–Cola Company and

PepsiCo Inc. They are referred to as Britvic, Cadbury Schweppes or Cadbury, Nichols, Coca–

Cola and Pepsi for the sake of convenience. The company proposed to merge with one of its

competitors Britvic Plc. It was approved by both boards and also after getting the approval of

Competition Commission6. But, later the decision was aborted.

1.4. Limitations of Analysis

The share price valuation is done using Dividend Discount Model which is useful only for the

companies that pay dividends. Other models are also described but not done due to constraints

like time.

While comparing the performance of the company with its competitors, only the significant

rivals are taken. There are mainly three domestic competitors and two global companies that are

5 A.G. Barr Plc. Annual Report and Accounts 2014, p. 11 6 Competition Commission provisionally cleared the merger of A.G. Barr Plc. with Britvic Plc. (BBC News, 2013).

11

significant to compete with A.G. Barr as described in the previous section. The comparison of

performance with limited number of competitors may limit the results and analysis.

12

2. The Outlook for the Economy

Under this chapter, the outlook of global economy as well as the UK economy are studied. The

consequences of them on the chosen company i.e. on A.G. Barr Plc. are also discussed. The

global economy and the macro-economic factors that influence the industry are analyzed and the

UK economy as well. This chapter concludes with the consequences of these economies on A.G.

Barr.

2.1. Global Economy

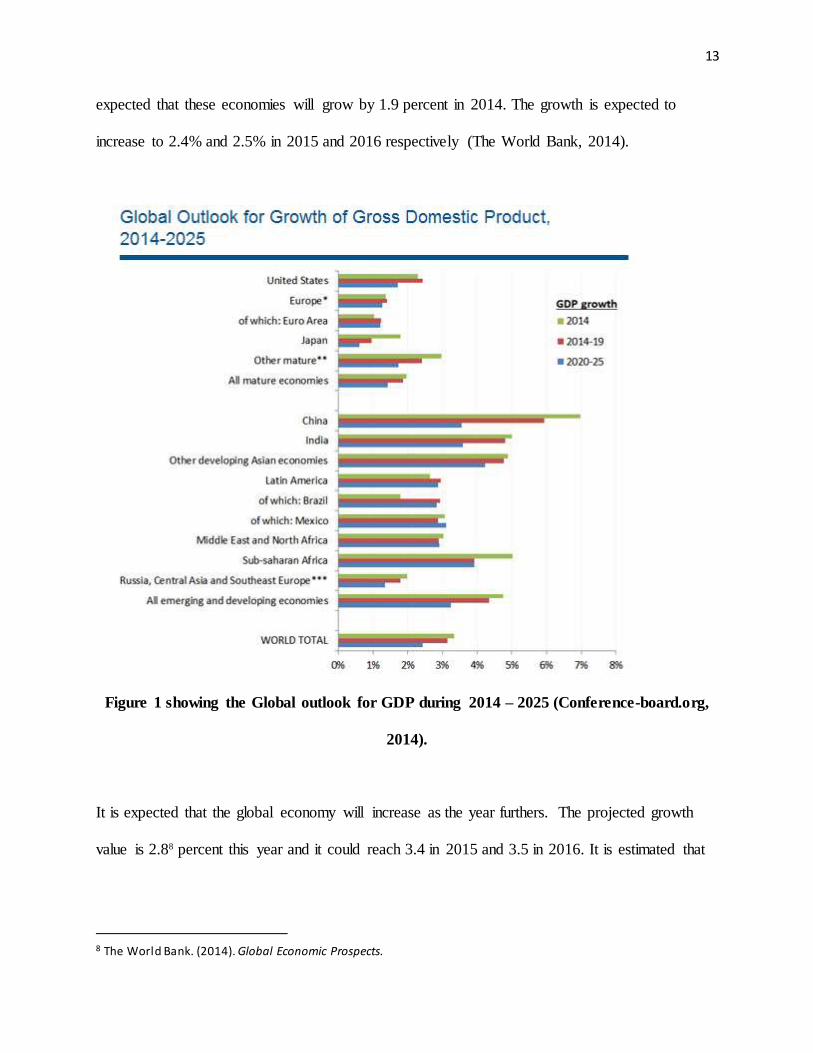

The GDP for global economy after adjusting for inflation has increased to 3.3%7 in 2014 from

2.9% in 2013 which is significant in developed economies. Though the Eurozone is expected to

grow, it is reversed in 2014 due to bad weather. The growth of GDP in developing economies

has decreased slightly in 2014. The economic transformations of China slowed down its

increase. Emerging economies such as Russia, Brazil and Central Asia exhibit a deceleration in

growth rates, whereas India, Mexico and other emerging nations in Asia witness minor

improvement in their performance (Conference-board.org, 2014).

For a third year in row, developing countries are facing a disappointing growth below 5 percent.

This is due to the weakness in first quarter of 2014 which hindered an anticipated increase in

economic activity according to recent Global Economic Prospects report of World Bank. This

report was delivered on 10 June, 2014. On the other hand, the recovery in high income countries

is increasing in a fast pace even though United States faced a weakness in the first quarter. It is

7 Conference-board.org. (2014). Global Economic Outlook 2014.

13

expected that these economies will grow by 1.9 percent in 2014. The growth is expected to

increase to 2.4% and 2.5% in 2015 and 2016 respectively (The World Bank, 2014).

Figure 1 showing the Global outlook for GDP during 2014 – 2025 (Conference-board.org,

2014).

It is expected that the global economy will increase as the year furthers. The projected growth

value is 2.88 percent this year and it could reach 3.4 in 2015 and 3.5 in 2016. It is estimated that

8 The World Bank. (2014). Global Economic Prospects.

14

high income countries will account for half of the worldwide growth in the years 2015 and 2016

where as they accounted for less than 40 percent in the year 2013 (The World Bank, 2014).

The GDP estimates of second quarter have shown expectations that the British economy has

increased beyond its peak in 2008. Another boost which supports these expectations is the IMF

forecast upgrade. All this puts Britain on the path of growing more than any other major

economy in the world (Stylianou, 2014).

However, it is not just Britain that has received such increases in the projections of IMF. IMF

projections have also given positive news to Spain on the day its unemployment rate fell to its

lowest level in two years. That was the largest quarterly increase in the number of people who

are employed since the second quarter of year 2005 (Stylianou, 2014).

2.2. UK Economy

The recovery of the UK seems to be continuing with a growth of around 3 percent in the year to

the first quarter of 2014. The main drive for the recovery seems to be the services sector.

However, there have been positive news from various other sectors like construction and

manufacturing. Several business surveys conducted on all three sectors have found that the

growth observed should continue to grow at a good pace during the second of half 2014.

It is found that the increase in GDP has been mainly due the increased employment and the

confidence in consumers. Over the past year, fixed investment has also increased as business

investment and house building have increased.

15

It is expected that UK economy could grow around 3 percent in 2014 which is an increase from

the 1.7 percent growth in 2013 (Pwc, 2014). However, the growth might slightly adjust to around

2.69 percent in 2015. It is expected that all the regions of UK to have a faster growth rate in the

year 2014 as opposed to 2013. It is also estimated that London will see the fastest growth rate of

3.4 percent and that Northern Ireland will see the slowest growth rate of 2.2 percent (Pwc, 2014).

However, there are still some significant downside risks that could affect the recovery of UK

economy. These include the slowdown in activity in the Eurozone, the unrest in Ukraine and the

Middle East which could have a potential impact on global energy prices, and potential problems

in some major emerging markets. On the other hand, there are some upside possibilities. These

include business investments being stronger than expected and an increase in real wage growth

which has led to the increase spending of consumers than predicted.

At present, the level of inflation is below the Bank of England’s target of 210 percent and it is

expected that the level will remain mostly stable over the next 18 months. It is however expected

that the interest rates might start to increase from the late 2014 or early 2015. This is to

overcome longer term inflationary risks which include overheating in the housing market.

In the year 2013, the UK had the sixth largest economy in the world and the third largest

European economy. It was right behind Germany and France. It is estimated that by the year

2030, the UK is expected to remain the sixth largest economy in the world by falling behind

India but overtaking France with which there is already a narrow margin. When it comes to

European economies, UK is expected to become the second largest EU economy before the year

9 Pwc. (2014). UK Economic Outlook July 2014. 10 Pwc. (2014). UK Economic Outlook July 2014.

16

2020 as it overtakes France. It is also expected that the gap between Germany and UK

economies will be narrowed by the year 2030 (Pwc, 2014).

It is found that the UK has ranked 5th in the G7 in 2013. This means it was down from 3rd in

2000 and 2007. This is because of the deep recession suffered by the UK during the years 2008 –

2009. This downfall in rank shows the slow recovery before 2013 (Pwc, 2014).

2.3. Implications for A. G. Barr Plc.

Since the global economy has expected to grow in the future years, A. G. Barr Plc. can expect

increase in its revenue. Though there are some significant downside risks in the UK economy, it

is anticipated to grow11 in the future years. The management of A. G. Barr is ready to make

adjustments to the capital structure according to the economic conditions. Their revenue by the

end of January in 2014 grew by 6.9%12, beating the wider soft drinks market. The volume of the

company grew more than double the market rate by 5.0%13.

2.4. Conclusion

This chapter describes the outlook for global economy and UK economy as well. It also reveals

the implications for A. G. Barr Plc. The global economy performance has been increased in 2014

from the previous year. Compared to developed economies, emerging economies have improved

their performance. A. G. Barr improved its revenue in 2014 even in the adverse economic

conditions. Expecting the growth of global economy and UK in the future years, A. G. Barr Plc.

expects bright future.

11 Pwc. (2014). UK Economic Outlook July 2014. 12 A.G. Barr Plc. Annual Report and Accounts 2014, p. 7 13 A.G. Barr Plc. Annual Report and Accounts 2014, p. 7

17

3. The Structure and Outlook for the Industry

Soft drink industry is a highly profitable industry. It is especially more profitable for concentrate

producers than the bottler’s. This can be amazing due to the fact that the product that is sold as a

commodity can even be made with ease. However, there are numerous reasons for this. With the

help of five force analysis we can easily understand how each reason contributes to the

productivity of the industry.

3.1. The UK Soft drink Industry

Since the year 2007 the UK carbonated soft drink have increased by almost 17 percent. It was

estimated that the value of the industry would reach 4.5 billion pounds in 2012. However, most

of this growth is due to inflation with the volume sales increasing 3.4 percent in that period

(Bainbridge, 2012).

Main members of the carbonated soft drink sector:

Coca-Cola, the most dominating company of the sector. It has market of share of almost 5014

percent. It increased global exposure by being the official sponsor of London Olympics. A. G.

Barr, one of the leading soft drink sellers in the UK market and popular for its IRN – BRU.

Though Coca-Cola is a major company it is led by Pepsi in the on trade. Pepsi makes best use of

its improved distribution with the help of partnership with Britvic. They have invested in staff

training which focused on serving consumers perfectly.

14 Bainbridge. (2012). Sector Insight: Carbonated Soft drinks.

18

The value of Schweppes has fallen by 1.515 percent between 2009 and 2011. Due to the price

rises in the market its lemonade was affected. This made it hard to compete against colas and

other fruit carbonates. Others include minor companies like Own-label. When compared to the

strength of other brands it has minor value in the soft drink market. It accounts for less than 1016

percent of value sales in take home market.

3.2. The Outlook for Soft drink Industry

Soft drink industry has mainly five trends. They are penetration, price, older consumers,

advertising and health. These are described in detail as below:

Carbonated soft drink generally tend to have a penetration of more than 90 percent which is

mainly associated with young mainly people under 35. Older consumers influence the soft drink

market. One of the major problems in soft drink market is that people over 55 generally are less

inclined to buy them. It is predicted that by the year 2017 this demographic will grow by 8.6

percent17 to 20 million.

Price also affect the soft drink market. CSD category has a relative benefit from low price point.

This can help it overcome competition from the more upmarket and recent entrants in the soft

drinks category. Big brands like Coca-Cola and Pepsi invest a lot of money on heavy

advertisement as it influences the sales and thereby profits. This makes them brands that come to

the mind of consumers when they think of soft drinks.

15 Bainbridge. (2012). Sector Insight: Carbonated Soft drinks. 16 Bainbridge. (2012). Sector Insight: Carbonated Soft drinks. 17 Bainbridge. (2012). Sector Insight: Carbonated Soft drinks.

19

Health conscious is growing among consumers. It is found that two out of five users have stated

that they try to avoid carbonated soft drink because they are not good for health. On the other

hand, more than half users drink sugar free variants of the carbonated drink for the sake of

health. The sales of sugar free variants has increased by 25 percent from 2009 to 2011

(Bainbridge, 2012).

3.3. The Five Forces

Michael Porter’s five forces are key to any business and industry. They are mentioned as below.

3.3.1. Threat of New Entrants

The following are the barriers to entry for new competition to enter the soft drink market:

Bottling Network: Coke and PepsiCo have agreements of franchisees with their respective

bottler’s. The bottlers have certain rights in certain geographic area. Using these agreements the

brands prevent the bottler’s in making similar products. Thus, they prevent new competing

brands from entering in the market for same products. Coke and Pepsi have bought the

significant percent of bottling companies. This, combined with the recent consolidation among

the bottler’s has made it very difficult for new companies entering the market to find bottlers.

The alternative for finding a bottler is to try and build their own bottling plants which would be

highly capital intensive.

Advertising Spend:

In the year 2000, the money spent in advertising and marketing in the soft drink industry was

around $2.618 billion. This money was mainly spent by Coke, Pepsi and their bottler’s. In the

18 Vulpala, L.G. (2007). Cola Wars: Five Force Analysis.

20

year 2000, 8.319 million was spent in the form of advertisement per point of market share

(Vulpala, 2007). Such a high number makes it difficult for any new entrants to compete and gain

visibility.

Brand Image/loyalty: Due to the long history of heavy advertising by Pepsi and Coke, they have

gained a lot of brand loyalty and image from customers across the world. This means that any

new entrant cannot virtually match up to their scale in the market place.

Retailer Shelf Space:

Generally, retailers get a significant margin of soft drink for the shelf space they offer (usually

15 – 2020 percent). This margin makes it difficult for new entrants as they cannot influence

retailers to carry their products instead of Coke and Pepsi.

Fear of retaliation:

A new comer entering a market in which giants like Pepsi and Coke already exist is not easy as it

could to lead to price wars which could affect the new comer.

3.3.2. Rivalry among the Existing Firms

In the concentrate producer industry, Pepsi and Coke are the two main firms competing and it

can be classified as a duopoly. The rest of the competition in this industry has a market share

which is too small to make any upheaval of pricing or industry structure. The competit ion

between Pepsi and Coke has mainly been regarding differentiation and advertising instead of

pricing except for a period in 1990s. This helped in the prevention of a big dent in profits

(Vulpala, 2007).

19 Vulpala, L.G. (2007). Cola Wars: Five Force Analysis. 20 Vulpala, L.G. (2007). Cola Wars: Five Force Analysis.

21

3.3.3. Bargaining Power of Suppliers

There are several basic commodities which are required as raw materials for the production of

concentrate. These are color, taste, caffeine or additives, sugar and packaging. These products

are produced by producers who have no power over the pricing. For this reason, the suppliers in

this industry are weak (Vulpala, 2007).

3.3.4. Bargaining Power of Buyers

In order to sell soft drinks there are several channels that are typically used in the Soft Drink

Industry. These include food stores, vending machines, Fast food fountains, convenience stores21.

Each of these has variations in the power of buyers. Food stores are mainly commanded by

buyers with lower prices. Fountains enable buyers to have freedom to negotiate. Hence, they are

also considered to have the power of buyers. The power of buyers is fragmented in convenience

stores and hence they pay higher prices. Buyers have no powers on vending channel.

3.3.5. Threat of Substitutes

Soft drink Industry has several substitutes like beer, water, coffee, juices etc. These are available

to end consumers with ease. However, these products are countered by the concentrate producers

by huge advertising, brand reputation, and increasing the availability of their products to

consumers22 (Vulpala, 2007). These strategies cannot be matched by the substitutes mentioned

above. Furthermore, the soft drink companies use diverse substitutes themselves to shield

themselves from competition.

21 Vulpala, L.G. (2007). Cola Wars: Five Force Analysis. 22 Vulpala, L.G. (2007). Cola Wars: Five Force Analysis.

22

3.4. Conclusion

This chapter explains the structure and outlook for the soft drink industry and the UK industry as

well. It also describes the Porter’s five forces that influence the soft drink industry. Advertising,

brand image, retailer shelf space and retaliation are some barriers that prevent new entrants in

soft drink industry. The soft drink industry is mainly leading by Coke and Pepsi. The threat of

substitutes is more in the industry. The threat of suppliers is weak and the threat of buyers

depends on the channels the companies use to sell them. Buyers have more power in food stores

and fountains, lower power in convenience stores and no power on vending channels.

23

4. Literature Review

4.1 Introduction

Dividend policy has an utmost relevance to AG Barr Plc. Dividend policy has always been a

crucial corporate finance area which can be analyzed with the help of rigorous model. There are

various theories associated with the policy of dividend and there are lesser evidences gained

from empirical studies. The conceptions behind the theories of corporate dividends are also very

different in nature. AG Barr Plc on the other hand has been using dividend policy only because it

has a responsibility to provide signal for its shareholders with respect to the status of capital

investment of their organization. In addition, this chapter has been prepared in order to discuss

the signals that AG Barr plc sends to its shareholders by the applicable dividend policies usage

and certain evidences for supporting those theoretical frameworks. There are various theories

associated with the policy of dividend and there are lesser evidences gained from empirical

studies. The conceptions behind the theories of corporate dividends are also very different in

nature.

Dividends are the payments that companies such as A.G Barr plc make from the total profit

made by the company to the associated shareholders either on annual or interim basis. The

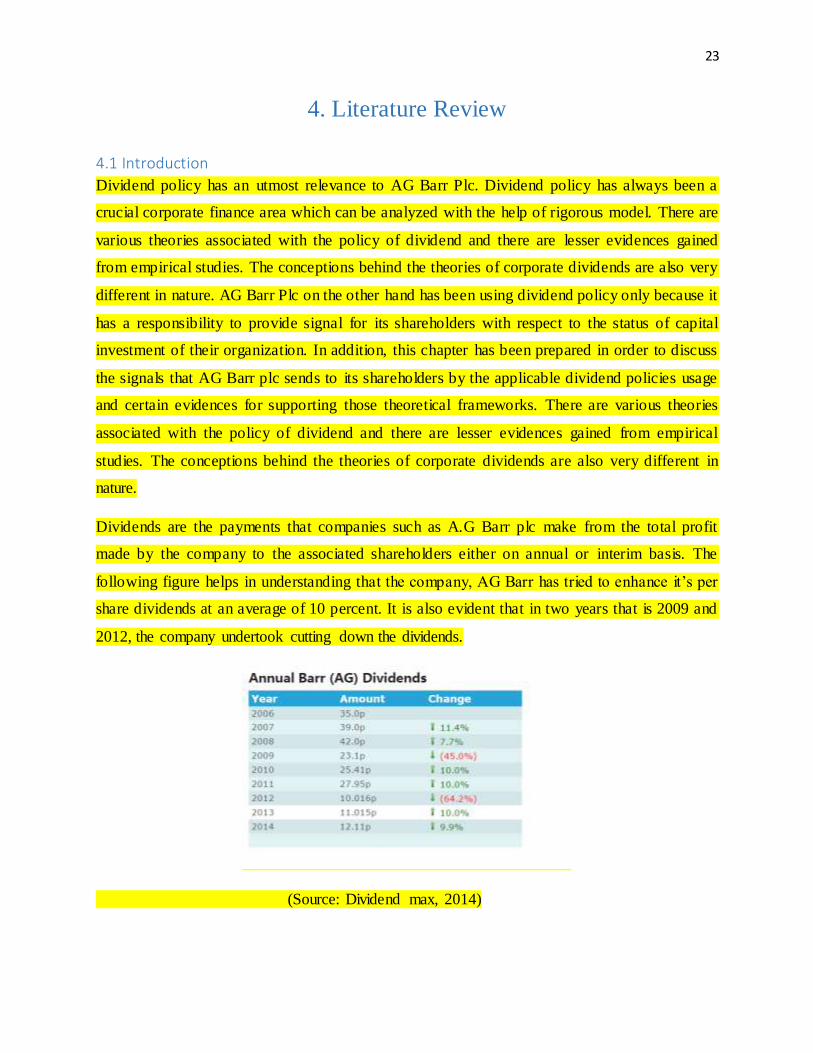

following figure helps in understanding that the company, AG Barr has tried to enhance it’s per

share dividends at an average of 10 percent. It is also evident that in two years that is 2009 and

2012, the company undertook cutting down the dividends.

(Source: Dividend max, 2014)

24

Additionally, during the year 2011, A.G Barr consistently made efforts to contribute to the

scheme of pension wherein total dividends distributed were 9 million euros. The resulting

dividend for the year attributable to shareholders equity totaled to 22.585 million Euros. A

dividend interim for 2011 was of 6.75 p for every general share. The final dividend proposed was

18.66 p per general share to be given if approval is given to this amount. From this perspective

and as evident from the annual report of the company for the year 2011, the distribution of

dividends at A.G Barr plc to its shareholders has been recognized as a financial statement

liability wherein the shareholders are responsible for the dividends approval. In addition, the

dividend policy advantage for AG Barr Plc lies in the fact that the company uses the policy to

manage capital risks. The capital structure and adjustments to be made by the company are done

by considering the changing economic conditions. For mainaining or even for adjusting the

capital structure, the company uses the dividends. These dividend payments are modified to

return the capital for the shareholders or they are issued new shares. This is the manner by which

AG Barr balances the shareholder returns between growth in long term and present returns

wherein capital discipline maintenance is related to activities of investment.

A dividend cut can take place when A.G Barr Plc was making an effort for reducing the payout

amount. This made A.G Barr Plc to experience stock prices to decline sharply. According to

Holder et al, 1998, dividends are cut due to reasons such as weak company earnings and limited

fund availability for meeting the payment required as the dividend policy. Furthermore, he also

stated that usually sharp declining stock prices imply weak position of finances with regard to a

specific company. At AG Barr plc the dividend reduction explains the lower price of stock

amounts after 2012. From this perspective the importance of dividend policy to A.G Barr plc can

be explained implying that it is the simple way that A.G Barr Plc adopts for communication its

well-being financially to the shareholder.

4.2 Literature Review

The corporate dividends issue has a wider historical perspective and as observed in the theories

of Frankfurter and Wood, the issue is bind with the corporate form of development. Dividends

on corporate have a historical perspective present since the 16th century wherein Holland and

Great Britain sailed their ships to start financial claims selling towards the investors. The

25

dividend policy literature has led towards producing a wide variety of theoretical research and

empirical research specifically being following by the dividend irrelevant publication presented

in the hypothesis based study of Miller and Modigliani, 1961. In the initial corporate history

stages, it was realized by the managers that an essential position is held by dividend payments

that are highly stabilized in nature. In certain ways, the reason behind this were the investor’s

analogy which with government bonds (Holder et al, 1998). A regular and stabilized payment of

interest was paid through these bonds and further corporate managers engaged in finding that

shares with the performance similar to bonds are preferred by investors.

However to the major extent, capital dividend theory helps in understanding that dividends are

not crucial when an organization needs to finance its actions whether in absence or presence of

taxes. It was the same period when researchers such as Miller-Modiliani, 1961 and Miller-

Scholes, 1978 presented their documentation to highly the statistically important relationship

present between the yields of dividends and prices of stock. The main issue however has still

remained unsolved that why dividends are paid by the companies (Holder et al, 1998). Dividend

policy in Finland for example has been the main issue in relation to certain studies of empirical

nature. There are various models which explain theoretical share in the market pricing value.

Most of the assumptions are based on separate security with intrinsic value on the basis of the

firm’s economic conditions. These conditions have their basis on earning, dividends, structure of

capital and potential growth from which the economic development conditions can be evaluated

(Holder et al, 1998). This is known as the fundamental analysis of stock. Common method used

in the analysis of fundamental methods are formulated basically for developing distinct types of

models of valuation which usually have their basis on 4 main criterion inclusive of earnings,

flowing cash, total assets and dividends. The analysis of fundamental stocks helps in explaining

26

that the share value can be divided into 2 classifications which are inclusive of dividend and

earning theories. The share value can be evaluated then based upon the dividends discounted.

4.3 Dividend Policy theoretical framework

The most commonly applied model is known as the share prices model of dividend having its

basis on the total earning that are gained by a shareholder over the shares. Future dividends are

presumed to be bought by private investors when shares are bought by them and the value of the

share then becomes only limited to what value it can offer to the shareholder on its selling. The

share prices market establishment is done by discounted the future dividends anticipated stream.

Models which have their basis on this perception are for example model of Walter, 1956 and the

model given by Gordon, 1959 (Gaver et al, 1993).

The model of Solomon, 1963 is inclusive of dividend discounts and even earnings, however on

the other side, the by discounting the earnings retained investments can be made. This model by

Solomon is only a widened version of models given by Walter and Gordon and therefore both

the models important features are also inclusive within both. Other models based on dividends

are propositioned by Lintner in 1962, conceptions of Portenfield’s in 1967 along with the

Malkiel-Cragg and Bower-Bower, 1970. These models have their basis completely limited on

dividend discounts. The presumption here is that the investor is already knowledgeable of the

dividends in future streams and so these models have complete information. The Whitbeck-

Kisord model, 1963 does not have a basis on dividends discounting but also within their dividend

based model is one of the main factors. A dividend signally model was developed by Eades,

1982 with regard to cost type dissipative signaling (Gaver et al, 1993). The stochastic process

market value on the other hand was determined by Hagen in the year 1973 wherein the process

was illustrated to represent the dividend policy of a company. It was reviewed by Ohlson, 1990

27

after synthesizing the security valuation theory for various uncertain settings that the result

determined the value of security to be an expected dividend adjustment function which has been

modified in order to adjust the risks. The discounted price here is done through the risk free rates

structure (Gaver et al, 1993). CAPM is one such model which is evident from historical literature

review to be in limited state. The view of earnings is of a data variable sufficing for determining

the payoff of security, the cost in addition to the dividends. It was postulated by Ohlson that

dividends only have the capability of serving as a common valid capital attributed with respect to

security. According to the re-examination done by Goetzmann-Jorion in the year 1995, it was

illustrated that the dividend ability for yielding long stock returns over the horizon are present

(Gaver et al, 1993). Two considerable series were used by them starting in the year 1873 wherein

they took U.S monthly series and the UK annual series. The result from this led towards

depicting that only marginal ability display is yielded by dividends for predicting the return of

stock market in either US or in UK. In Torkko, Finland, 1974, Gordon models application was

tested (Frankfurter et al, 2002). The sample selected constituted of 23 participating organizations

selected between the years 1971-1986 but the results appeared to be very discouraging in nature

because positive correlation was found to be present between the growth rate of dividends and

the market returns on the stock market.

4.4 Hypothesis of Dividend Irrelevance

There was a basic belief of an increment in the value of a firm if the dividends are higher, this

belief was in the place before the Miller and Modigliani’s seminal paper was published on the

policy of dividend. The bird-in-the-hand was considered to be the basis of this belief. Moreover,

in the very initial stages of the corporate history, it was considerably realized by the managers

that an essential position is held by dividend payments that are highly stabilized in nature. In a

very certain way, the reason behind this were the investor’s analogy which with government

28

bonds (Holder et al, 1998). A much stabilized amount of interest was paid through the bonds and

further corporate managers engaged in finding that shares that have the performance similar to

the bonds are the ones that are preferred by the investors. As per various researchers in the years

of 1930s clearly mentioned that the corporations’ only purpose was to pay for the dividends in

order to increase the prices of the shares.

4.5 Common Irrelevance Thesis It was a common belief that the organizations that pays higher amount of dividends must price

their shares at a higher level accordingly. However, the demonstration about calculated

assumptions on the capital markets, made by the M&M in the years of 1960’s, actively declared

the dividend policy to be of no relevance.

Applied the same in a capital market of assumed perfection as per M&M, the dividend policy

showed no change in an organization’s cost of capital or the stock. Moreover, the wealth of a

shareholder is not effected by the decision of the dividends which drives them to remain

indifferent between the capital gains and the devidents. The reasoning behind the indifference of

the shareholders was given by M&M that their wealth is primarily affected by the generation of

income from the investiment decisions that an organization takes. Hence, there is no affect by the

method of distributing the same income, by which the dividends become irrelevant. It was also

argues that the value of the firm is only determined by the core earning power that an

organization possess and by the decisions of its investments. The argument of M&M was

entirely based on the investors being rational and upon the perfect capital market’s assumptions

there were idealistic. It was also stated that the capitalized value of an organization’s future

earnings were the basis behind the calculations of evaluating an organization by the investors.

29

M&M strongly suggested the investors to look at all of the dividend policies as effectively same,

due to the ability that can be made in use by the investors to create dividends that can be

classified as homemade by the simple procedure of portfolio adjustments which can be carried

out by the investors in order to meet with their own preferences.

There are certain assumptions of the capital market being perfect that are necessary for the

hypothesis of dividend irrelevancy. The first is the indifferences between the taxes on capital

gains and dividends, the second factor asks for absolutely no costs of floatation or transaction

added between the duration of securities trade. Equal and free access to all of the participants in

market for the same information is considered to be the third. Fourthly, there is not supposed to

be any interests’ conflict between the security holders and the managers. It is also of a very vital

importance that all of the participants that are present in the market are considered to be the price

takers.

4.6 M&M Irrelevancy Proof

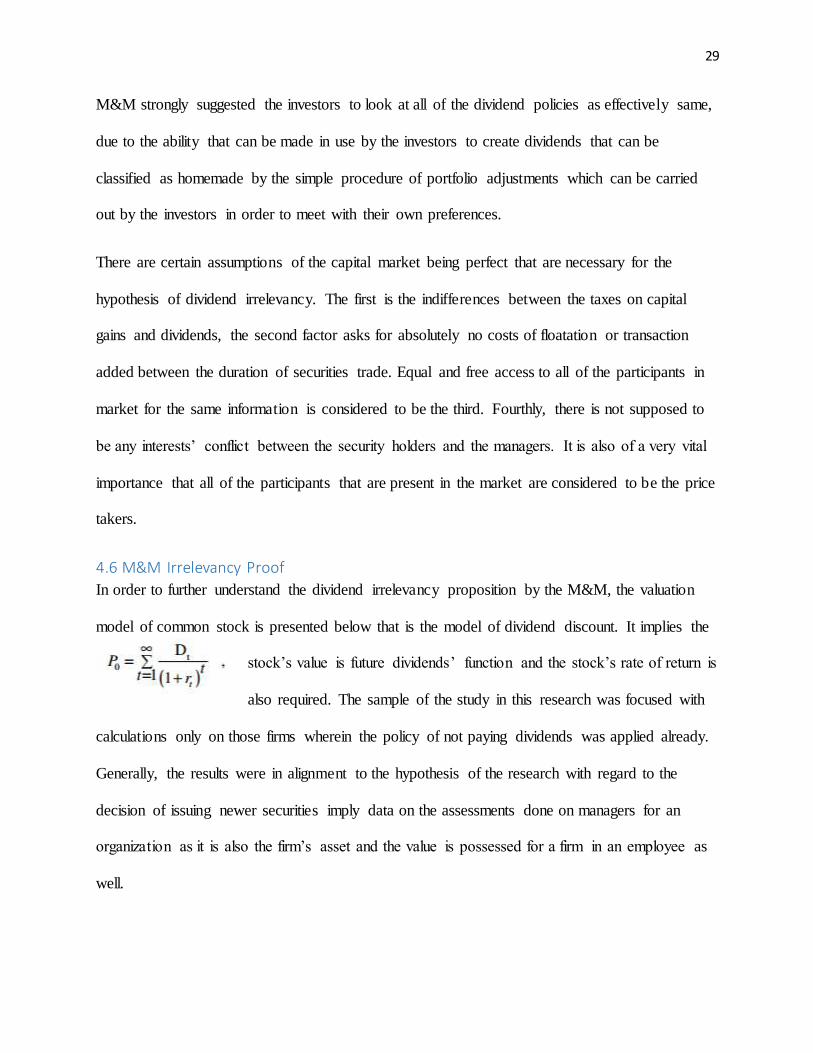

In order to further understand the dividend irrelevancy proposition by the M&M, the valuation

model of common stock is presented below that is the model of dividend discount. It implies the

stock’s value is future dividends’ function and the stock’s rate of return is

also required. The sample of the study in this research was focused with

calculations only on those firms wherein the policy of not paying dividends was applied already.

Generally, the results were in alignment to the hypothesis of the research with regard to the

decision of issuing newer securities imply data on the assessments done on managers for an

organization as it is also the firm’s asset and the value is possessed for a firm in an employee as

well.

30

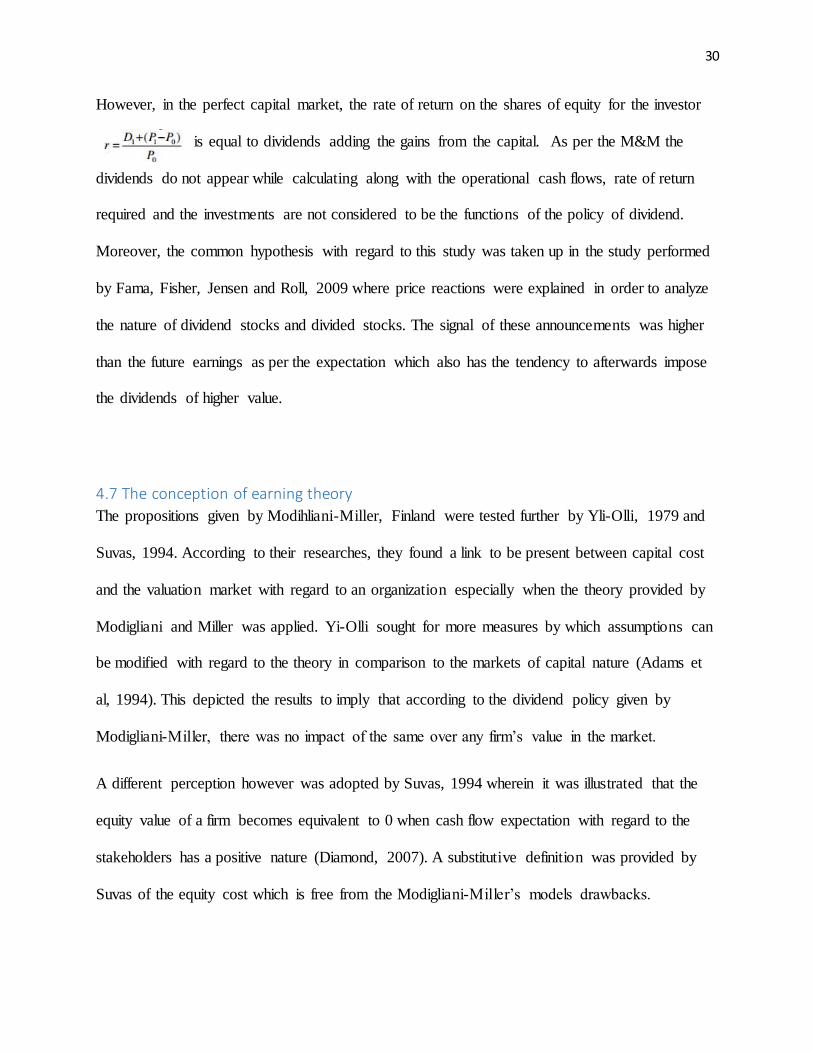

However, in the perfect capital market, the rate of return on the shares of equity for the investor

is equal to dividends adding the gains from the capital. As per the M&M the

dividends do not appear while calculating along with the operational cash flows, rate of return

required and the investments are not considered to be the functions of the policy of dividend.

Moreover, the common hypothesis with regard to this study was taken up in the study performed

by Fama, Fisher, Jensen and Roll, 2009 where price reactions were explained in order to analyze

the nature of dividend stocks and divided stocks. The signal of these announcements was higher

than the future earnings as per the expectation which also has the tendency to afterwards impose

the dividends of higher value.

4.7 The conception of earning theory

The propositions given by Modihliani-Miller, Finland were tested further by Yli-Olli, 1979 and

Suvas, 1994. According to their researches, they found a link to be present between capital cost

and the valuation market with regard to an organization especially when the theory provided by

Modigliani and Miller was applied. Yi-Olli sought for more measures by which assumptions can

be modified with regard to the theory in comparison to the markets of capital nature (Adams et

al, 1994). This depicted the results to imply that according to the dividend policy given by

Modigliani-Miller, there was no impact of the same over any firm’s value in the market.

A different perception however was adopted by Suvas, 1994 wherein it was illustrated that the

equity value of a firm becomes equivalent to 0 when cash flow expectation with regard to the

stakeholders has a positive nature (Diamond, 2007). A substitutive definition was provided by

Suvas of the equity cost which is free from the Modigliani-Miller’s models drawbacks.

31

Furthermore, valuation models were also derived by Suvas with regard to finding out more

opportunities of growth for the organizations.

4.8 Theoretical review of Macroeconomic factors and Dividends

There are various researches which have tried to provide explanation on the share’s market price

with the help from several information sources. The division of this information can be done in

the form of 2 categories inclusive of data under the manager’s control and data out of the control

of management (Gaver et al, 1993). The inclusion in second group is of factors of

macroeconomic considerations. It has been assumed that efficiency being semi-strong implies

that the markets for stock involve all information in published form. It simply seems from this

perspective that these market has a tendency towards reacting to earnings made and possess

some characteristic elements of economy. Announcements of dividends have obtained mixture of

results (Eastebrook, 1984). Factors of macroeconomic nature have a variable of explanatory

having their concern over US stock prices as evident from the stock market of US but the same is

not the situation in other countries such as Finland wherein performed studies by Kjellman-

Hansen have found managers of Finland view the issues of microeconomic as more essential

than the issues of macroeconomic perspectives and therefore the macroeconomic considerations

are not important for them especially when dividend decisions are to be made. Ina accordance to

the study performed by Kallunki-Martikainen, 2008, the connection between factors of macro-

economy and returns from stock are instead specific to samples and are variants of time (Eades et

al, 1984). As per the considerations on macroeconomic factors in Finland, there is no basis of

these factors on policy of dividends.

32

4.9 Dividends and Models of Equilibrium

2 models of equilibrium explain mostly the behavior of stock market inclusive of the model of

pricing the capital assets and the pricing theory arbitrage. The relationship present between the

firm value and dividends involve testing mostly in the perspective of the pricing model of

Capital Assets (Frankfurter et al, 2002). The most inherent presumption being made is the

application of general CAPM with regard to policy of dividend. Use of CAPM in an implicit

manner takes the assumption that hypothesis is irrelevant providing an indication towards a

strong capability of the researchers for accepting their irrelevant status. Expected returns from

equity and anticipated yields of dividends are related together leading towards a positively

related hypothesis to develop. The before tax return differential testing has also been done in

various studies such as Brennan, 2001 wherein formulation of the model of pricing based on

capital assets after payment of tax was developed.

4.10 Dividend policy Signaling effect

The dividends signaling effect takes up the assumption that dividends have the capability of

conveying data on earnings that can be gained by a company. Dividend changes provides a

message for the investors on the future flow of cash for an organization. It was further

hypothesized in the critical study presented by Modigliani-Miller, 1961 that the reduction of

dividend helps in conveying data that provides assurance on earning prospects for a firm in the

future (Friend et al, 1964). The general hypothesis however is inclusive of earnings in the future

and dividends being inter-related. Further the studies proceeded on examining the fundamental

reason by which the impact on future earnings can be laid by the policy of dividends. These

studies were inclusive of the propositions presented in the research study of Lintner, 1956 and

Warr, 2002 (Gaver et al, 1993). Under the signaling conception of dividend policy, there have

33

been various studies performed to analyze the stock market reaction towards the announcements

in dividends. In fact, these studies have also presented analysis on the market of stock efficiency

in the semi-strong nature.

The results from empirical studies have depicted that the dividends signaling effect is visible

efficiently from the data taken from U.S. The basic hypothesis with regard to this study was

taken up in the study performed by Fama, Fisher, Jensen and Roll, 2009 where price reactions

were explained in order to analyze the nature of dividend stocks and divided stocks. The signal

of these announcements was higher than future earnings expectation which also has the tendency

to later impose higher dividends on cash.

On the testing of dividends as per the study of Taylor, 1979, it was found that there is lesser

unanimity present in the concluding section rather than in several areas to test the reactions.

There was a further possibility that the announced earnings in the same stipulated time was

equivalent to the dividends raising concerns for the effect of signaling to develop.

4.11 Dividend Policy behavioral models

Dividend policy behavioral models have taken up the assumption that the changing dividends are

explainable by the dividends in the last period and the dividends targeted which can lead towards

being expressed in the form of periodic earnings fraction (Holder et al, 1998). The initial

publication of Lintner, 1956 illustrated the general model in order to investigate the application

of dividend policy. The basis of this model was on interview sets taken as a data collection

instrument wherein the participants were managers and they were providing their perspective

about their firm’s policies of dividend. It was further illustrated in the study that across firm’s

dividend policies do not have any uniformity (Howe et al, 1992).

34

The question of stable policy of dividends was tested by Mantripragada, 1976 in order to identify

the relationship of this policy with the prices of shares in the market. The hypothesis of stable

dividend argued that the share’s market price with stable payments of dividends need to be kept

at a high position that the similar share prices in the market with regard to payments because

they involve considerable fluctuation. There was however only less support gained by this

theoretical hypothesis as the dividend policies instable nature was evident to mostly all the

researchers.

By using the analysis of discriminants, a model was developed by Kolb 1981 on the basis of

economic factors and institutional factors for determining the dividends payment and for

predicting the annual cash changes dividend with regard to any particular firm (Gerald et al,

1992). The most crucial factor however in this study was given to liquidity and ability of profit

making of a firm.

Conclusion to the chapter

A.G Barr Plc has, what can be described as a progressive dividend policy, which implies that the

decision makers at the company wish to maintain or keep increasing dividend pay-outs year after

year. This year, the dividend payout has increased by about 7.7%. This does not imply that

earnings will not fluctuate over time, however, it can be seen as the Board’s confidence in the

future propositions of the business and the stability in its investment cycles. In doing so, they

endeavor to strike the perfect balance between the interests of the company (for future

expansions etc.) as well as managing the external stakeholders of the company (such as

creditors) and also providing confidence for the shareholders. Moreover, after ensuring there is

enough surpluses for business related investments, and financing the progressive dividend

35

policy, and handling the debt obligations of the company, the company may decide to give back

some extra cash to its shareholders in the form of buy back or repurchase of shares.

As discussed in the review of the literature on dividend policies and models, a growing dividend

payout is generally a sign that the company’s finances are in a good health. However, there is

also a risk of “window dressing” of the Financial Statements. However, higher dividend pay outs

do not suggest a window dressing, especially in the case of A.G Barr plc as the Total Income of

the company has seen consistent growth on a year to year basis, and this has resulted in better

compensation to its owners.

The dividend policy at A.G Barr plc gives a boost to share holder confidence. As evidenced by

Mantripragada, 1976, growing dividends point to stability in a company’s operation and hint at

good prospects for the future.

While almost all the researchers may argue that higher dividend payouts are a good sign for the

company, there is a small problem which most of them may have ignored. One of the many ways

of stock valuation, or estimating the price of a certain share, is also the dividend discount model

(DDM) the model suggests that the share price must be equal to the present value of all the future

dividends the company will pay. Based on this model, the share prices are generally inflated and

hence artificial in nature. Hence, while higher dividends are a good sign for the future, and

means extra cash in the hands of the shareholders, it cannot be looked upon as a measure of the

future stock price of the company. This is because given the market risks, economic instabilities;

a company’s fortunes may be best described as volatile. A high dividend payout and a policy of

progressive dividend will not be able to stand the test of time in adverse economic conditions.

36

Moreover, in order to maintain its progressive dividend policy, the company may sacrifice some

of its future expansion or operational plans, to meet its dividend requirements. This becomes a

sort of a paradox for the company, as it may declare higher dividends today, which may signal

some good health in the finances of the company, but, it is actually sacrificing future profits on

the basis of decision not to invest in such operations in the future, which, in turn may lead to

lesser profits in the future, and hence, a lower capacity to pay dividends.

To conclude, while growing dividends are a good sign of health at a company, and a move that is

welcomed by its shareholders, and looked upon favorably by its external stakeholders, it is a

mistake to look at it solely as a sign of prosperity. A greater analysis into the operations of the

company, in this A.G Barr plc needs to be called for, and not just a look at its growing dividends.

37

5. The Capital Structure Decision

5.1. Introduction

The capital structure is the mixture of debt and equity of a company. In other words, the capital

structure reveals the proportion of debt and equity. Hence, the capital structure can be considered

as the ratio of total debt to total equities. On the other hand, leverage is somewhat different from

the capital structure, yet it has association with the capital structure. Leverage can be measured

by the dividing the firm’s debt with its capital. It can be used to check the proportion of the debt

level in a firm. Hence it is used alternatively to explain the capital structure. Both debt and equity

methods are used to measure the firm’s capital structure. Identifying the proportion of

components of capital structure helps the company to maintain cost of capital. The optimal

capital structure varies with firms and sectors in which they operate.

Certain conditions influence the capital structure. These may or may not affect the firm’s value.

This can be identified with the help of theoretical and empirical work based on the Modigliani

and Miller (1958). This approach proposes the value with irrelevance of leverage. It is reasoned

by many researchers such as Scott (1976) and Leland (1994) that a balance between tax benefits

and the business disruption costs (also known as bankruptcy) of debt results in a perfect mix of

debt and equity. The reasoning that optimal mix of finance maybe resulted from balancing tax

benefits of debt and the distress costs of debt is further supported by the studies by Altman

(1984) and Opler and Titman (1994). Another type of reasoning argues that a balance between

agency costs and benefits of debt will help in resulting an optimal financing mix (Jensen and

Meckling, 1976; Jensen, 1986).

38

Capital structure is important to value the firm as it affects the cost of capital. Cost of equity can

be calculated by using the current dividend that the company pays, the current market price of

the company’s share and expected growth rate of dividend. As per the dividend discount model

the value of stock is determined by dividing the dividend per share by subtracting the dividend

growth rate from the present value at discount rate. This model is used by investors to estimate

the future dividends based on the historic dividend growth rate.

If firms evaluate the income-based valuation methods like discounted cash flow, they apply a

present value discount rate. The expected cash flows are turned into present value using the

discount rate which is based on the weighted average cost of capital (WACC). WACC indicates

the proportion of firm’s debt and equity in its capital structure (Cshco.com, 2012).

There are several valuation techniques used by firms. Companies need to evaluate their

intangible assets using separate valuation methods for two reasons: One - due to new

international accounting standards issued by the Board and two – the average required return

obtained for intangible assets is more than the WACC. DCF (the discounting cash flow method

is one of the ideal method to estimate the value of intangible assets especially in such situations

if is not possible to estimate their fair value based on the market conditions (Schauten, 2008).

5.2. Various Theories on Capital Structure

The manager versus outside shareholder conflict is generally reduced by the debt. This is done

by reducing dependency on the external equity and also by creating a commitment to pay out

cash in the form of interest. However, on the other hand debt might create a conflict of interest

39

between owners and the holders of bonds. This can be done for the problems of underinvestment

or substitution of assets. When shareholders let go of the positive NPV projects then they think

that profits will be used to pay the holders of bonds that is when the underinvestment problem

occurs. This problem is even higher in the case of mature firms. When the bondholders have a

fixed claim on the cash flow of the firm but shareholders hold the residual claim, then the asset

substitution problem occurs in a relationship. In this relationship, the asset substitution problem

occurs when the shareholders have an incentive for risk shifting. The shareholders can take an

action in order to increase the value of their claims at the same time imposing additional, and

uncompensated risk on bondholders (Rajagopal, 2010).

In the context of U.S. and several other developed countries, the capital structure theories

mentioned above have been tested widely. It is found by Bradley et al., 1984, that bankruptcy

risk and the existence of collateral form the most important factors in explaining the cross

sectional variations in leverage. These findings result in the suggestions that bankruptcy costs

and asset substitution problems are related to the capital structure decision (Rajagopal, 2010). It

is found by Mackie-Mason (1990), the probability that the firm will issue debt will be lessened

due to the existence of non-debt tax shields. This is pointing to how important the tax is to the

capital structure decision.

It is observed negative relationship between debt and growth options in certain instances. In such

instances, there has been indirect evidence which suggests the relevance of underinvestment

problems to debt policy (Graham, 1996; Johnson, 1997). Based on the results from Titman and

Wessels (1988), the financial hierarchy theory or pecking order has received substantial support.

40

The results have found that generally the more profitable the firm, the less likely it is found to be

dependent on external sources of financing. This theory has been further supported by Masulis

and Korwar (1986) and Mikkelson and Partch (1986) which show a negative market reaction to

seasoned equity issues.

The recent literature that has been produced in the corporate finance sector found that there has

been an increasing interest in financial management practices among firms which are in

emerging economies as well. The desire to compare the financial behavior of firms which are

placed in very different institutional settings is one of the main motivations for conducting such a

study. This comparison is now becoming easy with the help of the increasing availability of

trustworthy data. One of the examples of such study is the study on capital structure decisions

which are made by small and medium sized businesses in Vietnam, conducted by Nguyen and

Ramachandran (2006).

The results of the study have found the Vietnamese average leverage ratio is similar to that of

firms in the U.S. (an approximate of 40 percent) even though the country is characterized by a

bank based financial system. Furthermore, it is also found from the study that the Vietnamese

have a strong dependency on short term credit almost to the extent of completely ignoring long

term debt. The Vietnamese enterprises with higher amount of growth options tend to have a

higher leverage when compared with their counterparts of the U.S. (Rajagopal, 2010).

Moreover, it has been found that the tangibility of assets (which are presumed to mitigate the

asset substitution problem) have a negative effect on leverage. And on the other hand, the

41

business risk and firm size are found to have a positive effect to debt use. These findings have a

lot of variation with the theory and with the common behavior of firms in the U.S. corporate

sector. The variation observed in the findings above shows the value of a comparative study of

firms which are operating under different organized, governing, and structural regimes.

In order to obtain the value of equity, expected cash flows are discounted to equity. This includes

the residual cash flows are all the expenses have been met, tax obligations and interest and

principal payments at the cost of equity (Rajagopal, 2010). If the expected cash flows are

discounted to the firm, the value of the firm can be found out. This includes the residual cash

flows after all the operating expenses and taxes have been met.

From the variation observed in the findings, the importance of the comparative studies of firms

which operate under different institutional regulatory and structural regimes. Depending on the

climate in which a firm operates, the financing policy may be influenced in markedly different

ways by a give set of explanatory factors.

In order to contrast the results of the Vietnamese study, the results of Supanvanji (2006), can be

cited. This study has tested various received theories of capital structure by using data for firms

in Japan, Korea, Hong Kong, Singapore, Malaysia, Philippines, Thailand, and Taiwan. The study

has given results which are in line with the results for the firms in the U.S. It is found in the

study that the financial leverage of the Asian firms’ studies is positively related to tangibility,

and negatively related to growth options (Rajagopal, 2010).

42

5.3. The Traditional Approach

In traditionalist theory, people generally consider that a company’s value will be influenced

when the cost of the company is changed. They consider that the cost of capital will be the

lowest for the moderate level of debt. In this situation the value of a company will be the

maximum. This is the optimal capital structure of a firm.

5.3.1. Explanation

As per this model firm has an optimum capital structure and the value of firm increases if the

financial leverage increases. This implies the lower cost of capital with a rise in the debt share in

firm’s capital structure (Kaviyani et al., 2014). (Kanani Amiri, 2005). As per this approach firm

raise their debt to increase their market value. The increase of debt retains the capital structure in

an optimum due to which weighted cost of capital is minimum and market value is maximum.

Under this approach, it is assumed that the returns of shareholders are taxed at a mixed rate, the

distributions are subject to dividend tax rate and retained earnings are liable to capital gains tax.

However, the rate is reduced to depict the deferral tax advantages (Auerbach, 2005).

5.3.2. Aside

The traditional approach is logically defective for the grown-up firms whose equity capital

source is retained earnings. This is because this approach overlooks the primary tax befits of

retained earnings and avoids current taxes on dividends (Auerbach, 2005).

43

5.4. The Economic Approach

Under this approach the MM approach is analyzed. According to the Modigliani-Miller

proposition, if there were no costs of separation along with no government dairy support

program, then the cream plus would result in giving the same price as the whole milk. The

argument basically states that if the amount of debt is increased as the cream in the above

situation, the value of outstanding equity which can be equivalent to skim milk in the above

situation will be reduced (Villamil, 2008). This means that if the safe cash flows are sold off to

debt holders, the firm will have a lower value equity while keeping the total value of the firm

unchanged.

The above mentioned theorem has given two important and basic contributions. The first is that

it represent one of the first formal uses of a no arbitrage argument in the context of modern

theory of finance even though the law of one price is longstanding. Furthermore it has

contributed fundamentally why irrelevance fails around Theorem’s assumptions which are: there

will be unbiased taxes; there will be no capital market frictions; credit markets can be accessed

symmetrically and the financial policy of firms do not disclose any information (Villamil, 2008).

5.3.1. MM Propositions without Taxes

Modigliani-Miller theory (MM theory) is the foremost theory to encounter the traditional

thinking and the effect of capital structure of the firms. According to Modigliani and Miller

(1958), it was assumed that each firm belongs to a risk class. A risk class is a set of firms which

have common earning across states of the world. However, Stiglitz (1969) has shown that this

44

assumption is not needed. It is stated that the relevant assumptions are vital because they set

conditions to have an effective arbitrate.

According to the Modigliani-Miller approach both the value of firm and its cost of capital are

independent. Hence, the debt and equity mix is not relevant for determining the value of the firm.

Here the capital market is assumed as perfect without transaction costs, and corporate taxes.

The ability of the investors to undo the financial actions of a firm has given life to the question

whether firms which issued equity were losing stockholder money in the form of corporate

income tax payments. However this question has been resolved by Miller (1977). It has been

shown that higher after tax income can be generated by a firm if the firm increases the debt

equity ratio. It is also said that this additional income can be used to give higher payout to

stockholders and bondholder but cannot be used to increase the value of the firm.

The main core of the argument made is that the more debt is substituted for equity, the more the

proportion of firm pays in the form of interest on its debt increases relative to disbursements in

the form of dividends and capital gains on equity. It is also argued that higher amount of taxes on

interest payments when compared to equity returns will lessen or completely remove the benefit

of debt finance to the firm.

From the studies of Modigliani and Miller (1963) and Miller (1977) have resulted that the value

of a firm is not dependent on the dividend policy. On the other hand, Bhattacharya (1979) and

others have shown that the dividend policy of a firm is one of the expensive indicators of the

state of a firm and hence it is relevant in a class of models which have: stochastic firm earnings

45

have asymmetric information; the liquidity of shareholder (a requirement to sell makes firm

valuation relevant); and (iii) deadweight costs that are required to pay dividends, refinance cash

flow shocks or protection under-investment (Villamil, 2008).

When it comes to a separating equilibrium, the firms which high anticipated earning generally

tend to pay high amount of dividends. This helps in signaling the stock market about their

prospects.

5.3.1. MM Propositions with Corporate Taxes

In the original paper by Modigliani and Miller (1958), the importance of taxes was considered