Embed Size (px)

Citation preview

Black, Brown, Red & Green:

Transition to a low emissions energy environment

Alinta Energy Footprint

2

Contents

Coal generation and the barriers to exit

Who pays the bill and why?

Market dynamics and a soft landing

Life in a low emissions future

1

2

3

4

3

Coal generation and the barriers to exit

Pressure is mounting on coal-fired power stations to close…

…but the reality of shutting down is much more complicated

4

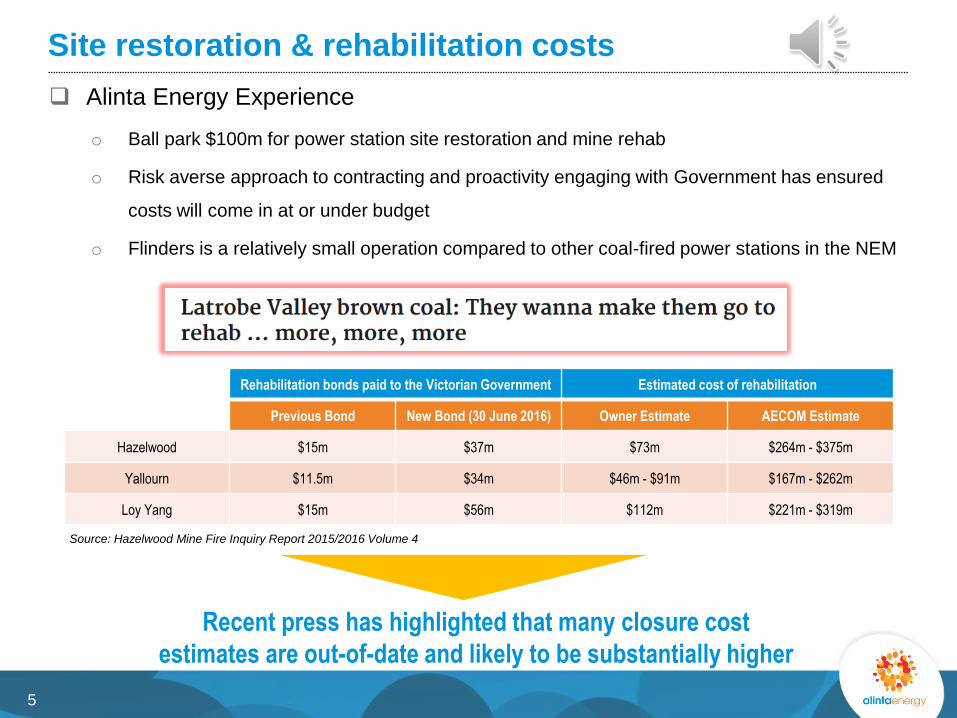

Site restoration & rehabilitation costs

Alinta Energy Experience

o Ball park $100m for power station site restoration and mine rehab

o Risk averse approach to contracting and proactivity engaging with Government has ensured

costs will come in at or under budget

o Flinders is a relatively small operation compared to other coal-fired power stations in the NEM

Recent press has highlighted that many closure cost

estimates are out-of-date and likely to be substantially higher

Rehabilitation bonds paid to the Victorian Government Estimated cost of rehabilitation

Previous Bond New Bond (30 June 2016) Owner Estimate AECOM Estimate

Hazelwood $15m $37m $73m $264m - $375m

Yallourn $11.5m $34m $46m - $91m $167m - $262m

Loy Yang $15m $56m $112m $221m - $319m

Source: Hazelwood Mine Fire Inquiry Report 2015/2016 Volume 4

5

The (ageing) workforce dilemma

Employee reskilling & vocational transitioning

o Numerous programs developed and implemented (eg. transition centre, wellbeing services)

o Several million dollars of costs incurred

Redundancy entitlements

o More than a quarter of Flinders total closure costs

Labour union resistance

o Alinta had unprecedented levels of engagement for a blue collar work force, which fostered an

open and respectful working relationship during closure

An ageing workforce creates challenges and

significantly adds to overall closure costs

6

The (ageing) workforce dilemma – cont’d

7

$180k p.a. base salary for a 4 day working week in the

final year of pay deal

Time spent walking from car park to work to be paid

$15 per week mobile phone allowance

$800 prescription glasses allowance every two years

Right for employees to not use company email

And many more…

Source: http://www.heraldsun.com.au/news/victoria/la-trobe-valley-power-plant-workers-demands-may-drive-up-electricity-prices/news-story/6523ca01bd0f278a09fabf5a70a4bd69

Unwinding derivative positions / contracting in a tight market

Legal obligations

o Critical to avoid deceptive/misleading conduct with market counterparties in lead up to closure

announcement

o Requirement to keep AEMO advised of running expectations under short, medium and long

term PASA

o ASIC obligations make derivatives trading difficult in lead up to closure announcement

Market dynamic (unscrambling the egg)

o A coal-fired generator typically provides baseload cover for retail businesses, which needs to

be replaced in the event of closure

o Market prices will quickly shift to reflect the removal of plant from the merit order – SA forward

curve rose from $51/MWh to $75/MWh within 3 months

Strict legal obligations add to the complexity and cost of

closing a coal-fired power station

8

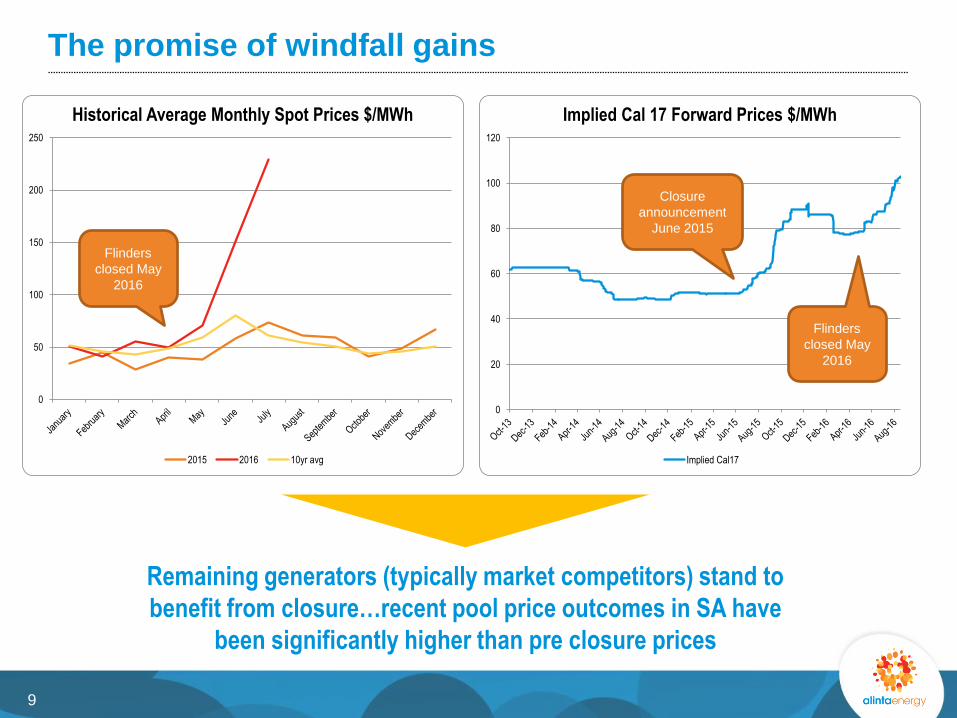

The promise of windfall gains

Remaining generators (typically market competitors) stand to

benefit from closure…recent pool price outcomes in SA have

been significantly higher than pre closure prices

9

0

50

100

150

200

250

Historical Average Monthly Spot Prices $/MWh

2015 2016 10yr avg

0

20

40

60

80

100

120

Implied Cal 17 Forward Prices $/MWh

Implied Cal17

Flinders

closed May

2016

Flinders

closed May

2016

Closure

announcement

June 2015

Contents

Coal generation and the barriers to exit

Who pays the bill and why?

Market Dynamics and a soft landing

Life in a low emissions future

1

2

3

4

10

Who pays the bill and why?

? Customer

? Shareholder

? Employees

? Government

The answer is all of the above!!!

11

The SA experience

Customer

o Rising wholesale prices leads to higher retail prices

Shareholder

o Alinta shareholders to incur total closure costs of c$200m

Government

o Governments wear the backlash from higher electricity prices and job losses

o Pressure to have a policy response

Most energy market stakeholders in SA have been forced to

cop a level of pain in relation to the Flinders closure process

12

Alternative solutions

Contract for closure

Cap & trade emissions scheme

Market redesign / capacity market

Several alternative solutions could change the allocation of

costs across different market sectors

13

Contents

Coal generation and the barriers to exit

Who pays the bill and why?

Market dynamics and a soft landing

Life in a low emissions future

1

2

3

4

14

Market dynamics and a soft landing

A national market framework is a necessity

o State-based goals & solutions can lead to outcomes that don’t contemplate the “bigger picture”

Medium to long term forward planning is the key

o Large energy infrastructure projects require significant leadtime

o Predicting future regulatory test outcomes can be problematic

o New power projects require at least 1-2 years of planning and a similar amount of time to

construct

A national framework with a focus on long-term planning can help to

mitigate risks, reduce costs and pave the way for a “soft landing”

15

Contents

Coal generation and the barriers to exit

Who pays the bill and why?

Market Dynamics and a soft landing

Life in a low emissions future

1

2

3

4

16

Life in a low emissions future

“Affordable, competitive, reliable and environmentally responsible energy supply”

Alinta Energy is committed to embracing renewables as a

core part of our strategy and vision…

FED GOV’T OBJECTIVE:

17

Low emission energy mix challenges

Transmission connectivity – what is needed and why?

o Planning is challenging when uncertainty around future energy mix

o However new transmission projects should be supported where economically feasible

Renewables - too much wind and not enough solar?

o Is “banding” sensible?

What is thermal generation’s role during the transition?

o Rising east coast gas prices make baseload/intermediate generation a challenge?

o Will closure of coal together with new renewables require more gas-fired peaking generation?

What should the role of storage be?

o Battery capex on a rapid downwards trajectory and can heighten grid stability

o Other alternatives exist (eg. pump storage, solar thermal)

…but finding the most optimal answers is going to represent a major

challenge over the coming years

18

Storage has significant potential to aid the transition

19

-

10

20

30

40

50

60

70

80

90

100

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

Queensland - Electricity Spot Prices $/MWh

Bottom Quartile Median Price Top Quartile

-

20

40

60

80

100

120

140

160

2007

Q1

2007

Q2

2007

Q3

2007

Q4

2008

Q1

2008

Q2

2008

Q3

2008

Q4

2009

Q1

2009

Q2

2009

Q3

2009

Q4

2010

Q1

2010

Q2

2010

Q3

2010

Q4

2011

Q1

2011

Q2

2011

Q3

2011

Q4

2012

Q1

2012

Q2

2012

Q3

2012

Q4

2013

Q1

2013

Q2

2013

Q3

2013

Q4

2014

Q1

2014

Q2

2014

Q3

2014

Q4

2015

Q1

2015

Q2

2015

Q3

2015

Q4

2016

Q1

2016

Q2

2016

Q3

South Australia - Electricity Spot Prices $/MWh

Bottom Quartile Median Price Top Quartile

Significant

spread

between

high and low

price periods