Embed Size (px)

Citation preview

IRR Viewpoint Caribbean Market Update – 2015 Annual Report By James V. Andrews MAI, CRE, FRICS, ASA, CVA Integra Realty Resources - Caribbean

Caribbean Market Update – 2015 Annual Report

Table of Contents Caribbean Regional Market 3 Overview 3 Economic Indicators 3 Regional Tourism 3 Travel Demand 5 Hotel Performance 6 Resort-Residential Projects 8 Financing 8 Notable Regional Developments and News 9 Conclusions and Forecasts 10

Country Reports 11 Cayman Islands Market Report 11 US Virgin Islands Market Report 17 Barbados Market Report 21 Puerto Rico Market Report 24 Dominican Republic Market Report 28 The Bahamas Market Report 31

3 | P a g e

Caribbean Regional Market 2015 Annual Report

By James V. Andrews, MAI, CRE, FRICS, ASA, CVA

Overview In this 2015 annual report, we look at various segments of the Caribbean regional economy, such as tourism, real estate, development and investment. Investment in the region is largely dependent on risk and economic growth; factors which are currently sending mixed signals.

Economic Indicators The World Bank estimates Gross Domestic Product (GDP) growth in the Caribbean to have been 4.6% in 2014, compared with 2.6% for the globe and 0.8% for the greater region of Latin America and the Caribbean (LAC). The superior GDP growth was attributed to stronger external demand and rising tourism receipts. Apart from the USA, growth forecasts have been revised lower for most countries in the world due to changing economic conditions such as the price of oil and reduced trade. The reduced World Bank forecasts for 2015 and 2016 for the Caribbean are 4.1% and 4.0% respectively; as compared with 3.0% and 3.3% for the globe. The highest performer is expected to be the Dominican Republic, with a forecasted 2015 growth of about 7% according to the country’s Central Bank.

Standard and Poor’s, as well as Moody’s have downgraded the long term sovereign credit rating for Barbados (“B” from “BB”, outlook: “negative”) and Puerto Rico (“BB+” from “BBB-“); and we note that several Caribbean countries that are rated are noted as having a “negative” outlook. Exceptions are the Cayman Islands, Cuba, Dominican Republic, Jamaica and Trinidad and Tobago, which are noted as having a “Stable” outlook. These downgrades in sovereign credit ratings mostly relate to poor fiscal management by the governments of these countries, and do not necessarily represent the perceived country risk premium that might be attached to private investments.

Meanwhile, all indications are positive for the tourism industry which is the largest contributor to GDP in the region. Hotel performance continues to show gains in both rates and occupancy; while arrival statistics continues to rise as well. The Caribbean Tourism Association reports that the anticipated growth in stop-over arrivals for 2014 is likely to have been 4% to 6%, or double what the same organization predicted at the beginning of the year. Real estate associations are reporting increasing sales in most markets, though the vacation-home and resort-residential markets in many resort communities appear to remain slow to revive from the recent recession.

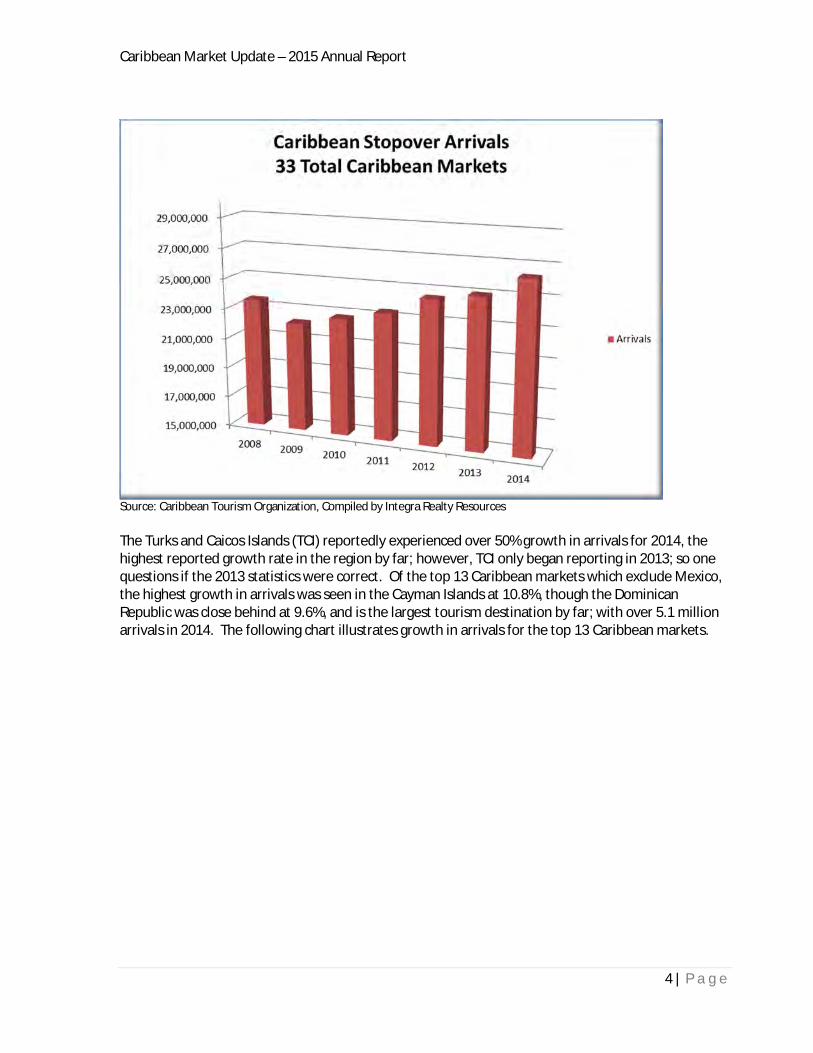

Regional Tourism Data from the Caribbean Tourism Organization (CTO) has reported that total estimated arrivals for the region’s 33 reporting markets including the Mexican Caribbean were 26.3 million, with a growth rate of 5.3%. This continues a long term growth trend which is ongoing since 2010.

Caribbean Market Update – 2015 Annual Report

4 | P a g e

Source: Caribbean Tourism Organization, Compiled by Integra Realty Resources The Turks and Caicos Islands (TCI) reportedly experienced over 50% growth in arrivals for 2014, the highest reported growth rate in the region by far; however, TCI only began reporting in 2013; so one questions if the 2013 statistics were correct. Of the top 13 Caribbean markets which exclude Mexico, the highest growth in arrivals was seen in the Cayman Islands at 10.8%, though the Dominican Republic was close behind at 9.6%, and is the largest tourism destination by far; with over 5.1 million arrivals in 2014. The following chart illustrates growth in arrivals for the top 13 Caribbean markets.

Caribbean Market Update – 2015 Annual Report

5 | P a g e

Destination 2012 Arrivals % Chg 2013 Arrivals % Chg YTD 2014 Arrivals % Chg2014

MonthsDominican Republic 4,562,606 5.90% 4,689,770 2.80% 5,141,377 9.60% Jan-DecCuba 2,838,169 4.50% 2,850,135 0.40% 3,001,958 5.30% Jan-DecJamaica 1,986,084 1.80% 2,008,409 1.10% 2,080,181 3.60% Jan-DecPuerto Rico 1,569,472 8.40% 1,588,677 1.20% 1,405,390 6.70% Jan-OctBahamas 1,419,275 5.40% 1,363,487 -4.10% 924,898 3.50% Jan-JulAruba 903,934 4.00% 979,256 8.30% 1,072,082 9.50% Jan-DecUS Virgin Is lands 737,651 8.60% 702,963 -4.70% 655,477 3.90% Jan-NovBarbados 536,303 -5.50% 508,520 -5.20% 458,510 0.20% Jan-NovMartinique 487,359 -1.80% 489,706 0.30% 489,561 0.00% Jan-DecSint Maarten 456,720 7.60% 467,259 2.30% 377,341 7.30% Jan-SepCuracao 419,621 7.50% 440,044 4.90% 450,953 2.50% Jan-DecBVI 351,404 4.00% 355,677 1.20% 337,843 3.00% Jan-NovCayman Islands 321,650 4.10% 345,387 7.40% 382,816 10.84% Jan-Dec

Average Increase 4.19% 1.22% 5.07%

CARIBBEAN STAYOVER ARRIVALS - LEADERS

Source: Caribbean Tourism Organization

Travel Demand American Airlines, the largest carrier to most of the Caribbean destinations reported lower passenger traffic in 2014; however, they also reduced the number of direct flights from Miami during the year. This reduction, which does not include US Airways’ passengers, is likely due to the merger between the two airlines and the desire to not compete with the Caribbean routes, which are generally through Charlotte or Philadelphia on US Airways.

In addition, AA now has new competition in the region. JetBlue is expanding its Caribbean presence, with new routes from U.S. gateways to Grenada, Curacao, St. Lucia, Montego Bay (Jamaica), Port of Spain (Trinidad) as well as Puerto Plata, Punta Cana and Santiago (all Dominican Republic).

During the year, Delta Airlines added new service to Grenada, St. Lucia and Barbados. United Airlines launched new service to Nassau (Bahamas), and Southwest announced new service to Aruba, Montego Bay (Jamaica) and Nassau (Bahamas).

According to Expedia, demand for Caribbean travel is expanding rapidly. The online travel store reported that travel demand for the Caribbean region as measured by bookings garnered via the company’s platforms grew nearly 30% year over year during the first three quarters of 2014. In terms of ranking by demand from Expedia, Dominican Republic remains the top producing market in the Caribbean with 60% growth, followed by Jamaica with nearly 40% growth and the Turks and Caicos with almost 50% growth year over year during the first three quarters of 2014.

Expedia also reports that demand for inter-Caribbean travel increased 50% in the first three quarters of 2014 when compared to the same time period in 2013. Not coincidentally, new and expanding inter-island carriers have helped fuel this demand, with the expansion of Seaborne, Cape Air, Inter-Caribbean Airways and JetBlue; all of which provide transportation between the islands. Demand for these new inter-Caribbean routes is partially driven by the recent departure of American Eagle who were regionally based in San Juan prior to 2012.

Caribbean Market Update – 2015 Annual Report

6 | P a g e

Hotel Performance Hotel performance in the Caribbean in terms of average daily rates and occupancy continued a trend of robust improvement through 2014 according to data from Smith Travel Research (STR, Inc.). Average Daily Rates (ADR) grew by 6.4% to $194.66, while occupancy was up 1.64% to 68%, leading to Revenue per Available Room (RevPar) growth of 8.03% ($132.28).

Source: Smith Travel Research (STR, Inc.)

The overall trend is an increase in all three metrics ongoing since 2010. Occupancy grew significantly in the years 2010-2012 but has been growing more linearly with rates since then.

Source: Smith Travel Research (STR, Inc.)

Caribbean Market Update – 2015 Annual Report

7 | P a g e

We note that the average ADR relative to occupancy rates was much higher during the recessionary years of 2009-2011, begging the question if hotel operators should have reduced rates to increase occupancy during that period. Alternatively, another question is whether or not we can expect to see more significant increases in ADR now that we have seen two years of moderate gains in both rate and occupancy.

In terms of profitability, the 2014 STR Caribbean Host study using 2013 data from participating Caribbean hotels reports that Gross Operating Profit was up over 25% and Net Operating Income up over 17% despite increasing expenses.

At the end of 2014, STR reported 40 Caribbean hotels totaling 8,800 rooms in the “in-contract” stage (“formerly active pipeline”). This represents a 13% decrease in rooms “under contract”, compared with the same period last year. The lack of increase in projects under construction provides further support that ADR will increase moderately in 2015. It should be noted, however, that over 2,200 rooms in the pipeline are from the Baha Mar project in the Bahamas which is set to open in May, 2015. The resulting effect on ADR and occupancy in the Bahamas once these rooms are added to inventory is yet to be seen. The most profound effect is likely to be on the Atlantis Resort and neighboring Ocean Club, which collectively represent more than 40% of the country’s room stock. These properties will likely compete closely with Baha Mar, and we predict a decrease in overall occupancy in New Providence/Paradise Island once Baha Mar is fully open.

The three largest projects in the Active Pipeline include two within the Baha Mar mega resort development (Baha Mar Casino and Hotel – 981 rooms, and Grand Hyatt Baha Mar – 844 rooms); with the third being the Palladium Hotel Grand Jamaica Resort and Spa in Jamaica with 850 rooms.

Most of the hotel transactions occurring in the Caribbean are hotels which are being purchased for renovation, repositioning and rebranding. The majority of these are all-inclusive properties which were faltering due to changing market metrics, but in solid locations with good beach frontage. Examples include:

Sandals Resorts International have purchased several mid-scale, all-inclusive hotels in the Southern Caribbean (Grenada, Barbados and Antigua), renovated them to a higher standard, and re-branded as either Sandals (for couples only) or Beaches (for families). Sandals is currently attempting to expand throughout the region and elevate the level of luxury and services associated with the brand, which is in keeping with the current trend of all-inclusive hotels within the upscale and luxury chain scales.

One recent entrant into the Caribbean luxury all-inclusive space is Spanish group Playa Hotels and Resorts who are active in Mexico. They recently acquired the Ritz Carlton in Montego Bay, Jamacia, and signed a management agreement with Hyatt to operate and segregate the resort into two brands: Hyatt Ziva and Hyatt Zilara, which are new, luxury all-inclusive brands - one for couples and the other for families.

The Caribbean based Sagicor Life Insurance company is investing in several all-inclusive hotel properties in Jamaica, such as the iconic Hilton Rose Hall in Montego Bay as well as two of the

Caribbean Market Update – 2015 Annual Report

8 | P a g e

former Superclubs properties. The former Hilton Rose Hall is being renovated and re-branded as a Jewell Resort. Other recent entrants into the Caribbean all-inclusive market include Blue Diamond Resorts (a division of Canada’s Sunwing Travel) and Palace Resorts out of Mexico. Blue Diamond acquired Smugglers Cove Resort in St. Lucia as well as the former Breezes in Trelawney, Jamaica; and Palace Resorts acquired the Sunset Jamaica Grande in Ocho Rios.

Capitalization rates for hotel sales in the Caribbean are mixed, and mostly related to upside potential for re-branding, re-positioning and development of excess land. We are aware of several transactions which represent cap rates of between 8% and 8.5% on trailing-12 net operating income; however, additional capital expenditures were injected in most of these cases, which suggests that the properties may have been underperforming; thus resulting in lower capitalization rates based on trailing-12 income. There are also several sales representing rates even lower than 8% due to potential expansion onto excess beachfront land which is ripe for development.

Resort-Residential Projects Many residential resort projects that were not mostly sold prior to the economic downturn are still stagnant or struggling to re-start development without alternative funding. Some of the major projects that are remaining active include those with no debt financing or unconventional financing such as from sales of limited partnerships or private-public joint ventures. In addition, some projects benefit from the reputation of the developer relative to prior projects (e.g. Bakers Bay, Abaco, Bahamas) and their extensive lists of existing clients/buyers who are high net worth individuals (e.g. Oil Nut Bay, Virgin Gorda, BVI). Other projects are maintaining reasonable sales pace due to Economic Citizenship Programs, such as Christophe Harbour and Kittitian Hill in St. Kitts.

Typical sales prices for vacant residential lots within branded resort communities are $35 to $50 per square foot for ocean view and golf course view, and $75 to $100 per square foot for oceanfront lots. Completed homes/villas/condos within 5-star projects are typically $1,200-$1,500 per square foot of interior living area, and these rates have changed very little in the last five years. Most projects are selling less than ten units per year with a few exceptions.

Financing Although there is certainly still some reluctance on the part of bank lenders to finance new projects, confidence appears to be increasing based on our conversations with lending clients. More lenders are likely to return to the practice of financing new Caribbean projects in 2015 or 2016, though underwriting criteria will likely be more stringent than before the recession.

In KPMG’s 2014 Caribbean Region Financing Survey, the Caribbean Financier Confidence Barometer for “Banks” reached 6.0, with 1 being “bearish” and 10 being “bullish”. This represents the highest confidence level since before 2008. The same result for non-bank financiers was 7.0. The survey indicates that the typical debt coverage ratio for hotels remains at 1.4 (same as 2012 and 2013), the average Loan To Value (LTV) rose to 60% from 55% in 2013, and the average interest rate dropped from 450 basis points above prime to 400.

Below we report the average results of the report’s survey of lending criteria, and have extrapolated overall capitalization rates based on the formula:

Caribbean Market Update – 2015 Annual Report

9 | P a g e

Ro = DCR x LTV x Rm

Ro = Overall Capitalization Rate; DCR = Debt Coverage Ratio; LTV = Loan To Value; Rm = Mortgage Constant

Average Financing IndicatorsAverage Indicator 2011 2012 2013 2014Debt Coverage Ratio 1.45 1.4 1.4 1.4Loan To Value 57% 57% 55% 60%Interest Rate Margin Above Prime 350 500 450 400Implied Interest Rate 6.75% 8.25% 7.75% 7.25%

Implied Mortgage Constant (15 yr) 0.10619 0.11642 0.11295 0.10954 Implied Overall Cap Rate 8.78% 9.29% 8.70% 9.20%Source: KPMG Caribbean Financing Survey, Integra Realty Resources

Source: KPMG Caribbean Financing Survey, Integra Realty Resources

Notable Regional Developments and News Citizenship by Investment (CBI) programs, which provide citizenship to investors who buy

interests in real estate within approved projects, are under increasing scrutiny due to questionable due diligence on the applicants. For example, the Canadian Government now requires citizens of St. Kitts and Nevis to acquire a visa to travel to Canada. Reportedly, this move is due to concerns about the issuance of St. Kitts/Nevis passports and identity management practices with its citizenship by investment program; which is the demand driver behind major resort projects in the territory such as Christophe Harbour and Kittitian Hill. Investors in the program are typically those from countries that have restrictive travel requirements such as China, Russia and the Middle East. Other countries with CBI programs are Antigua & Barbuda, Dominica and Grenada; and similar programs are being considered in St. Lucia, Barbados and Bermuda.

Caribbean Market Update – 2015 Annual Report

10 | P a g e

Royal Bank of Canada has announced plans to close its wealth management operations in the Caribbean. The move could cost the region about 300 jobs, according to The Financial Post, and appears to be a continuation of the bank’s efforts in exiting the international wealth business. This branch reportedly manages part of a CDN$43 billion portfolio of assets. This move comes on the heels of the sale of HSBC’s retail banking operations in the region to Butterfield Bank. There have also been news reports of major losses due to bad real estate loans by some of the Caribbean regional banks which are headquartered in Canada. All of these events echo concerns over the financial services sector in the region.

Conclusions and Forecasts Tourism statistics indicate metrics such as hotel performance and visitor arrivals to most countries nearly reaching or exceeding their pre-recessionary levels. Average Daily Rates are just below their pre-recessionary peak, yet are not as high as they have been on the basis of the ratio of rate to occupancy. In addition, the number of hotel rooms in the pipeline is slightly less than last year, which is another indication that rates and occupancy will both increase in 2015, leading to higher revenues for hotels and increased interest from investors and lenders for this property type. Our predictions are for increases in arrivals, hotel performance and new project development in 2015, buoyed by slight increases in the availability of financing. The increases in visitors to the islands should boost revenues for related industries such as restaurants, watersports and tours.

Sales in resort-residential projects are fairly stagnant at most developments, with some exceptions which have competitive advantages. New developments involving mixed use residential resorts are still fairly rare, given the reluctance of conventional lenders to take on these projects without employing more stringent underwriting criteria than in the past. We see little change in this sector in 2015 other than a potential for a modest increase in sales due to increasing disposable income from potential U.S. buyers.

Though the outlook for the tourism sector remains positive, many of the larger countries which have more diverse economic bases will continue to struggle economically without significant overall job growth from other industries, as their workforce continues to exceed that which can be sustained by the tourism sector. While the governments of these nations will see increased revenues from tourism taxes and import duties for raw materials, these revenues are often limited by incentives granted to developers of new projects. In addition, reducing unemployment and lowering the cost of living should be top priority so as to increase disposable income and spending by residents which would inject capital directly into the economy. Fiscal responsibility is also a crucial variable that can have a direct effect on lowering the perceived risk of investment into these countries who have a history of high debt to GDP ratios, and undesirable bond ratings as a result.

Other factors which will play significant roles in the development trends in the region will be the increasing presence of Public-Private-Partnerships, sustainable/alternative forms of energy and medical tourism. Overall, we see continuing gradual improvement in most of the local economies in the region, as a result of increased tourism and interest from investors.

Caribbean Market Update – 2015 Annual Report

11 | P a g e

Country Reports

Cayman Islands Market Report

Tourism The Cayman Islands market ranks 13th in the list of the top tourism markets in the Caribbean (excluding Mexico) in terms of the number of stay-over arrivals, with 382,816 arrivals in 2014. This market was second in the Caribbean in terms of growth in arrivals, with 10.84% growth over the prior period. The chart below illustrates the relationship between arrivals and GDP, and the overall dependence on tourism by the overall economy.

Source: Caribbean Tourism Organization, Economics and Statistics Office, Compiled by Integra Realty Resources

Hotel Performance Data from Smith Travel Research (STR, Inc.) indicates 2014 occupancy for reporting hotels in the Cayman Islands of 70.5%, up 0.88% over the prior year. The reported average daily rate (ADR) was $340.95 (up 4.03%), leading to Revenue Per Available Room Night (RevPar) of $240.27 (up 5.34%).

Caribbean Market Update – 2015 Annual Report

12 | P a g e

Note: Sample Size reflects the number of rooms within the STR participating hotels

Source: Smith Travel Research (STR, Inc.)

The active pipeline solely consists of the proposed 263-room Kimpton Grand Cayman on Seven Mile Beach, which would add 6.4% to the existing room stock of 3,862 rooms. This project will also include 66 residential units.

Financial Services Sector The offshore financial services sector is facing increasing pressures for transparency and other industry issues. These pressures continue have a negative effect on the offshore financial centers such as the Cayman Islands. In Cayman, according to data provided by the Economics and Statistics office for the first half of 2014, bank and trust licenses continued on a downward trajectory, this time by 5.0%, while insurance licenses increased by 1.8%. Mutual fund registrations increased 0.8%, stock

Caribbean Market Update – 2015 Annual Report

13 | P a g e

exchange listings declined by 5.2%; though new company registrations rose 12.4% following a dismal first half of 2013. Nevertheless, the office market in Grand Cayman continues to grow in size; as discussed in the section below.

Grand Cayman Office Market The Cayman Islands is home to the largest office markets of all of the offshore financial centers in the Caribbean. With an overall existing and planned inventory of over 2.9 million square feet – and growing, the country’s office sector is seemingly disproportionate to the size of the population and economic base. Based on the amount of space being marketed as available for lease, the overall vacancy rate is 12.5%; however, this does not include the new building in Camana Bay under construction. A summary of the office market statistics for Grand Cayman is indicated following, based on data cooperatively compiled by Integra Realty Resources and Coldwell Banker Cayman Islands Realty.

Source: Coldwell Banker Cayman Islands Realty and Integra Realty Resources

The amount of inventory has been gradually increasing over the last five years and the vacancy rate has been gradually decreasing. The reported net rents achieved for Class A space range from US$35.00 to US$50.00 per square foot with an average of about US$42.00 on a triple net basis. The achieved rates for Class B buildings range from US$26.00 to US$38.00, averaging about US$33.00.

Real Estate The value of freehold property transfers in the Cayman Islands for 2014 declined slightly (-1%) to just over US$640,000,000, following a 29% bump in the prior year. The number of transfers has held fairly steady at around 1,700 per year, though there has been a gradual downward trend since 2006. It should be noted that the trend in sales volume in Cayman is relatively erratic given the relatively small size of the market.

Caribbean Market Update – 2015 Annual Report

14 | P a g e

Source: Cayman Islands Department of Lands and Survey (www.caymanlandinfo.ky), Integra Realty Resources Note: Spike in value in 2011 due to large Dart acquisition of Stan Thomas portfolio Note: Spike in value in Q2 2013 due to sale of Ritz Carlton Resort

Seven Mile Beach Condominium Market One of the most dynamic real estate markets in the Cayman Islands is the Seven Mile Beach condominium market, which is said to emulate the overall Caribbean vacation home market fairly closely. Sales volume from transactions noted in the local MLS jumped 157% in 2014, though this is partly due to 14 closings of units previously under contract at The Watercolors; the area’s newest project which recently completed construction. Excluding sales at The Watercolors, sales volume for 2014 was slightly over $74.4 million; a 53% gain over 2013. Prices per square foot are about US$835 on average, a 9% gain above that of the prior year.

Caribbean Market Update – 2015 Annual Report

15 | P a g e

Source: Coldwell banker Cayman Islands Realty (CIREBA MLS), Compiled by Integra Realty Resources

Notable News and Developments Dart Realty, the developers of the large-scale urban town center known as Camana Bay, has

announced their long term plans for continuation of the 600-acre, mixed use, planned urban development known as Camana Bay; stating they plan to spend $1.3 billion in the next 10-15 years, including $400 million on infrastructure. These plans include a second beachfront resort on Seven Mile Beach which will be connected to the greater development. This proposed hotel project, which has yet to be branded, is in addition to the 263-room Kimpton Hotel currently under construction on Seven Mile Beach. Kimpton Hotels, who operates over 60 boutique hotels in 30 cities in the USA, was recently acquired by InterContinental Hotels Group.

The privately operated Cayman Enterprise City recently announced that it has 122

international companies signed up in the special economic zone and another 300 are in the sales pipeline. The CEC is utilizing temporary space while its new campus is being planned for development in a location that has yet to be announced. In addition to the tax benefits of having a company headquartered in a jurisdiction with no corporate, income or capital gains taxes, companies operating in one of the special economic zones take advantage of no import duties and special treatment of work permits/visas.

Health City Cayman Islands, the regions newest medical tourism facility, conducted its first heart surgeries in mid-2014, with the first LVAD (heart pump) installation. Conceived by Narayana Health’s Dr. Devi Shetty, a well-known neuro-surgeon and personal physician of the

Caribbean Market Update – 2015 Annual Report

16 | P a g e

late Mother Teresa, Health City opened its doors in February, 2014. The state-of-the-art medical facility in the western Caribbean is one of 27 facilities operating under Dr. Shetty’s administration across the globe.

Another new project recently announced in Cayman appears to be set to commence

construction following an agreement with the Government to complete a road project known as the East-West Arterial. This (reported) $360 million commercial, tourism and residential community covering 600 acres is planned for construction to commence in East End within a few months. The development known as “Ironwood” is to include a Town Centre with boutique shops, conveniences including a grocery store and entertainment; a sports training complex; an Arnold Palmer Signature championship 18-hole golf course and a vacation resort. The golf course is said to be Arnold Palmer’s first Caribbean Signature course. The developers agreed to finance construction of this road to the development from George Town, which was a contingency upon this project going forward.

Conclusions The Cayman Islands appears to be benefitting from increased interest in the tourism sector as well as the Financial Services sector which is actually a larger contributor to GDP. These factors, along with the large projects underway by developers such as Dart, Ironwood, Health City and Cayman Enterprise City, suggest that the economy could experience further recovery in 2015.

Caribbean Market Update – 2015 Annual Report

17 | P a g e

US Virgin Islands Market Report

Tourism The U.S. Virgin Islands market ranks 7th in the list of the top tourism markets in the Caribbean in terms of stay-over arrivals, with estimated year-end 2014 stay-over arrivals of about 730,000. The year 2014 indicated modest growth in arrivals, with 3.90% growth over the prior period based on data through November. The chart below illustrates the relationship between arrivals and GDP. We note that the continuing downturn in GDP is likely due to negative influences outside the tourism sector, such as the 2012 closure of the Hovensa oil refinery in St. Croix.

Source: Caribbean Tourism Association, WorldBank, Integra Realty Resources

Hotel Performance Data from Smith Travel Research indicates 2014 occupancy for reporting hotels of 67.8%, up 3.29% over the prior year. The reported average daily rate (ADR) was $308.98 (up 0.51%), leading to Revenue Per Available Room Night (RevPar) of $209.53 (up 5.63%).

Caribbean Market Update – 2015 Annual Report

18 | P a g e

Source: STR, Inc. According to STR, there are 453 rooms in the active pipeline, which would add 8.6% to the existing room stock of 4,818 rooms. These projects include the 153-room, proposed Embassy Suites in the mahogany Run area, and the 300-room, proposed Hyatt Regency in Mandal Bay. In addition, a hotel project was recently announced on Water Island; however, the developers have not yet announced a brand or number of proposed rooms.

Real Estate The value of real estate sales in the St. Thomas-St. Croix MLS grew by 54% in 2014 to nearly $200 million on 883 transactions; volume seen since 2008 and sales pace not seen since 2007. This growth

Caribbean Market Update – 2015 Annual Report

19 | P a g e

follows 20% growth in 2013 which came after six years of declines. The average sales price surpassed $300,000, a level also not seen since 2008.

Source: St. Thomas/St. Croix MLS

Notable News and Developments The US Virgin Islands senate has rejected the proposal that would allow the sale of the former

HOVENSA oil refinery in St Croix to Atlantic Basin Refining (ABR). The legislature had voted not to approve the operating agreement between the USVI government and (ABR), which agreement was a pre-condition to the sale. The rejection was due to legal issues in the contract which some senators felt were of too much risk for the country. The territory’s new governor also announced a lawsuit against Hovensa to attempt foreclosure of the property. The refinery was the largest employer in the territory until its closure in 2012.

The US House of Representatives has passed the Coast Guard Reauthorization Act, which should help level the charter yacht industry playing field. Prior to 1993 and the imposition of a six-passenger limitation on US uninspected vessels, the charter yacht industry in the US Virgin Islands was thriving, contributing over $100 million in annual revenue and hundreds of jobs to the local economy. A large chunk of the industry moved to the British Virgin Islands after the six-passenger rule limitation was initiated by the US Government. If the bill is adopted by the Senate and enacted into law, the ability of the USVI to compete in this industry should be significantly improved.

Plans to build a new pier at the Havensight cruise terminal in St. Thomas are reportedly in the works. The new pier would enable the busy port to accommodate more ships, including the

Caribbean Market Update – 2015 Annual Report

20 | P a g e

industry's largest ships. The project, known as Long Bay Landing, is for two 1,350-foot-long parallel berths that will be divided by a pier.

After an extensive search and vetting process, the USVI Government has selected a group of

local and regional investors to develop a hotel resort on Water Island, just off of St. Thomas. There are apparently eight hotel brands in discussions with the developers for branding the property.

A Texas-based EB-5 Regional Center has announced an EB-5 funded commercial project known as the Port of Mandahl Caribbean Conference Resort. When completed, the development is reportedly planned to include two full-service hotels, a golf course, a state of the art conference center, retail and commercial space, and high-end residential units. EB-5 is a type of economic citizenship program whereby the United States grants citizenship to investors of certain approved projects in areas where the economic boost is needed. Regional Centers are tasked with selling the investments such as limited partnerships to international buyers.

The Margaritaville (Wyndham) Vacation Club is under construction in Water Bay on the East End of the island of St. Thomas. The project is a renovation of the 290-room Renaissance Grand Beach Resort into 262 timeshare oriented condominium units.

The University of the Virgin Islands has announced plans to develop a medical school on St.

Thomas, which will be operated in collaboration between the hospitals on St. Thomas and St. Croix.

Conclusions Economic conditions in the U.S. Virgin Islands appear to be slower to recover than many areas of the region, particularly in St. Croix, where industrial development has been more of a focus than tourism. The closure of the Hovensa refinery and the inability of either the owners or the Government to facilitate a sale to a buyer who can re-open the facility as a refinery will continue to plague St. Croix until other new developments occur that can create new jobs. There appears to be some resurgence in tourism for St. Thomas and St. John, and real estate activity appears to be beginning to improve; however, many businesses – even those catering to cruise ship passengers – continue to struggle. Our forecast is for continued improvement in arrivals and hotel statistics, but only gradual economic improvement for the overall territory.

Caribbean Market Update – 2015 Annual Report

21 | P a g e

Barbados Market Report

Tourism Barbados ranks 8th in the list of the top tourism markets in the Caribbean, with estimated year-end 2014 stay-over arrivals of about 510,000, based on data and 0.20% growth over 2013 through October. The chart below illustrates the relationship between arrivals and GDP.

Source: Caribbean Tourism Association, WorldBank, Integra Realty Resources Note: Year End 2014 arrivals estimated based on data through October and growth rate Jan-Oct over 2013

Hotel Performance Data from Smith Travel Research indicates 2014 occupancy for reporting hotels of 65.0%, up 3.15% over the prior year. The reported average daily rate (ADR) was $337.48 (up 5.47%), leading to Revenue Per Available Room Night (RevPar) of $219.36 (up 10.83%).

Caribbean Market Update – 2015 Annual Report

22 | P a g e

Source: STR, Inc.

Notable News and Developments All three of the former Almond Resorts all-inclusive hotels in Barbados are now open under

new ownership. The Almond Club in Holetown was purchased in 2012 by Elite Island Resorts and re-branded The Club Barbados. The Almond Casuarina in St. Lawrence was purchased by Sandals Resorts in late 2013 and recently opened as Sandals Barbados after significant renovations. The Almond Beach Village in St. Peter was acquired in 2014 by the Government’s tourism authority, who put a temporary operator in place to re-open approximately ½ of the resort. Reportedly, the property is under contract for sale to Sandals, who will tear it down and build a new Beaches Resort (all-inclusive for families).

Caribbean Market Update – 2015 Annual Report

23 | P a g e

The long-term sovereign credit rating for Barbados was recently lowered by Standard and Poors (S&P) to “B” from “BB-“; with the outlook as negative. S&P reports that the downgrade reflects continued large fiscal deficits, a high debt burden that continues to rise, and narrower financing options.

Conclusions Barbados heavily relies on tourism, and its primary market is the UK and the rest of Europe. Unlike many other Caribbean destinations which rely more on the United States as the primary source market, Barbados has been slower to recover from the effects of the recent recession. This is partly due to the slower economy in the European region, as well as the effects of the UK airline passenger duty imposed on international passengers which was significantly raised in recent years.

Another factor that has had a negative effect is the loss of a number of flights to Barbados since the closure of the three Almond Resorts properties in 2012, which had an effect on the supply of rooms. Protecting the airlift is a high priority for Government, which is the primary reason for the acquisition of the Almond Beach Village in St. Peter. With the other two Almond properties having already re-opened and the St. Peter properties potentially soon to be re-built, the country should see interest from the airlines for more routes from source markets. Either way, a relatively low supply of rooms should continue to buoy rates and occupancy in 2015.

The negative credit rating placed on the public debt is evidence of investors’ perception of poor fiscal policy, however, may have less of an impact on private investments. Nevertheless, the overall economy will likely rebound at a slow pace until there is a resurgence of tourism from the European region.

Caribbean Market Update – 2015 Annual Report

24 | P a g e

Puerto Rico Market Report

Tourism Puerto Rico ranks 4th in the list of the top tourism markets in the Caribbean, with estimated year-end 2014 stay-over arrivals of about 1.4 million passengers. The year 2014 indicated strong growth in arrivals, with 6.70% growth over the prior period based on data though October. The chart below illustrates the relationship between arrivals and GDP. We note that while tourism is a major factor for GDP, Puerto Rico has other industries that contribute to GDP which many smaller island nations in the region do not.

Source: Caribbean Tourism Association, WorldBank, Integra Realty Resources Note: 2014 year end arrivals estimated based on growth rate and actual arrivals through October

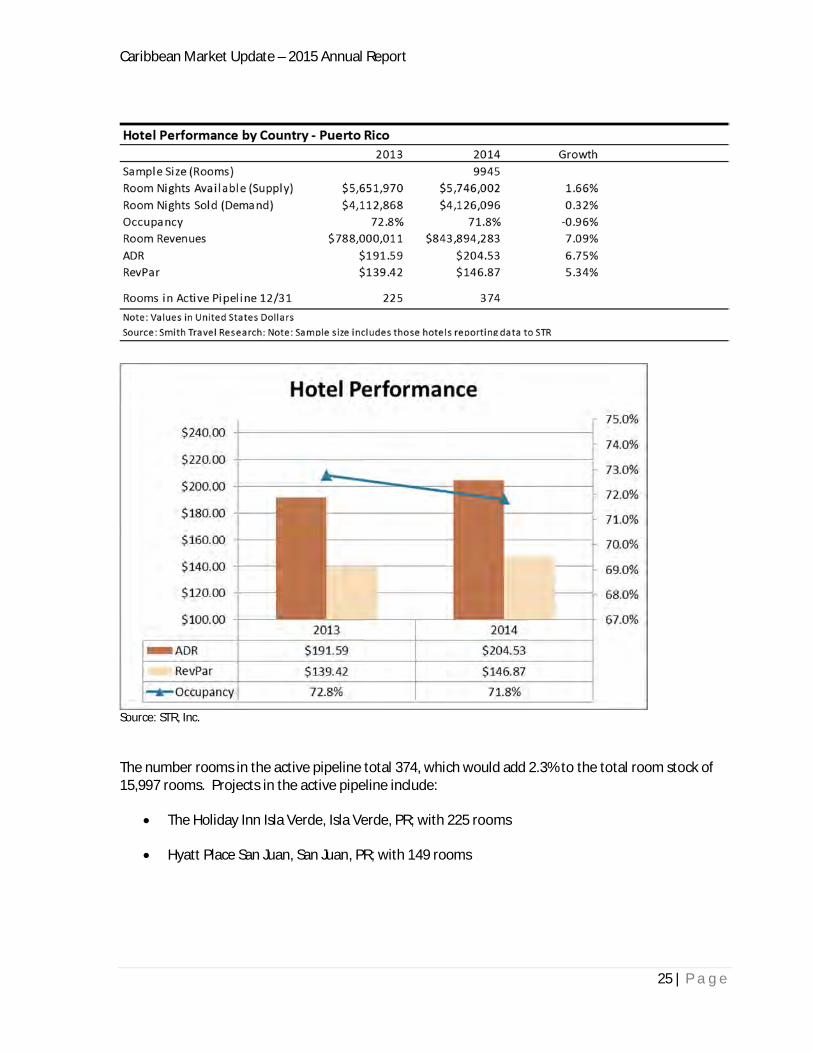

Hotel Performance Data from Smith Travel Research indicates 2014 occupancy for reporting hotels of 71.8%, a slight decline from the prior year. The reported average daily rate (ADR) was $204.53 (up 6.75%), leading to Revenue Per Available Room Night (RevPar) of $146.87 (up 5.34%).

Caribbean Market Update – 2015 Annual Report

25 | P a g e

Source: STR, Inc.

The number rooms in the active pipeline total 374, which would add 2.3% to the total room stock of 15,997 rooms. Projects in the active pipeline include:

The Holiday Inn Isla Verde, Isla Verde, PR; with 225 rooms

Hyatt Place San Juan, San Juan, PR; with 149 rooms

Caribbean Market Update – 2015 Annual Report

26 | P a g e

Economic Activity The best indication of economic activity in Puerto Rico is the Government Development Bank’s Economic Activity Index (GDB-EAI). The GDB-EAI is a valuable tool that summarizes the behavior of four major monthly economic indicators. Up to March 2012, these indicators were: total non-farm payroll employment, cement sales, gasoline consumption, and electric power consumption. As of April 2012, the electric power consumption variable was replaced by the electric power generation variable as the fourth indicator.

The EAI stood at 125.3, a 1.4% reduction from one year earlier, and a 0.3% decrease from the prior month. The index had experienced modest gains in late 2013, but otherwise has been hovering around the 125 level after a decline which continued from mid-2012 to mid-2013.

Source: Puerto Rico Government Development Bank

Over the long term, the EAI reached its peak of over 155 in 2005, following a long term upward trend that began in 1983. There have been nearly ten years of decline decline since the 2005 peak.

Notable News and Developments The Government of Puerto Rico is seeking a development partner in the form of an

established international port operator to work with on the development of the Port of the Americas. The commercial trans-shipment port sits on over 300 acres in Ponce, on the southern coast of the island. The Port of Americas is stated to be an important component in establishing Puerto Rico as a global business hub. There is expected to be significant growth in

Caribbean Market Update – 2015 Annual Report

27 | P a g e

the number of large vessels coming to the region considering the expansion of the Panama Canal, which is set to be completed in 2015.

Although statistics indicate that the Puerto Rican economy is relatively stagnant, there are

signs of increased optimism for investment in the territory for investors. Billionaire hedge fund manager John Paulson (Paulson & Co.) called the territory the “future Singapore of the Caribbean”; having taken a stake in the St. Regis Bahia Beach Resort and Golf Club last year; and planning to invest $1 billion in Puerto Rican projects over the next two year. Puerto Rico has introduced legislation that allows certain qualifying Americans who move to the territory full time to exclude the majority of income taxes and capital gains taxes. There is also an Economic Development Corporation (PRIDCO) which offers tax incentives to companies that relocate to the territory.

Taubman Realty Group has closed on a $320 million loan from US Bank to finance the continuing development of the 650,000 square foot, Mall of San Juan. What is likely the largest retail and entertainment complex in the Caribbean will be anchored by Nordstrom and Saks Fifth Avenue; and is scheduled to open in March, 2015.

Conclusions Puerto Rico’s economy traditionally mirrors that of the United States, though the territory has been struggling to recover from the recent recession. The agency tasked with providing tax incentives to businesses that relocate there (PRIDCO) appears to be reaping some benefits from their proactive efforts, with signs that investors seeing opportunities in the territory. Tourism is a large economic driver, though less so than smaller island nations and other large ones such as Jamaica, and the country will need improvement in other sectors to facilitate significant gains in the overall economy.

Caribbean Market Update – 2015 Annual Report

28 | P a g e

Dominican Republic Market Report

Tourism The Dominican Republic ranks number one in the list of the top tourism markets in the Caribbean, with year-end 2014 stay-over arrivals of about 5.14 million passengers. The year 2014 indicated strong growth in arrivals, with 9.63% growth over the prior period. The chart below illustrates the relationship between arrivals and GDP.

Source: Caribbean Tourism Association, WorldBank, Integra Realty Resources

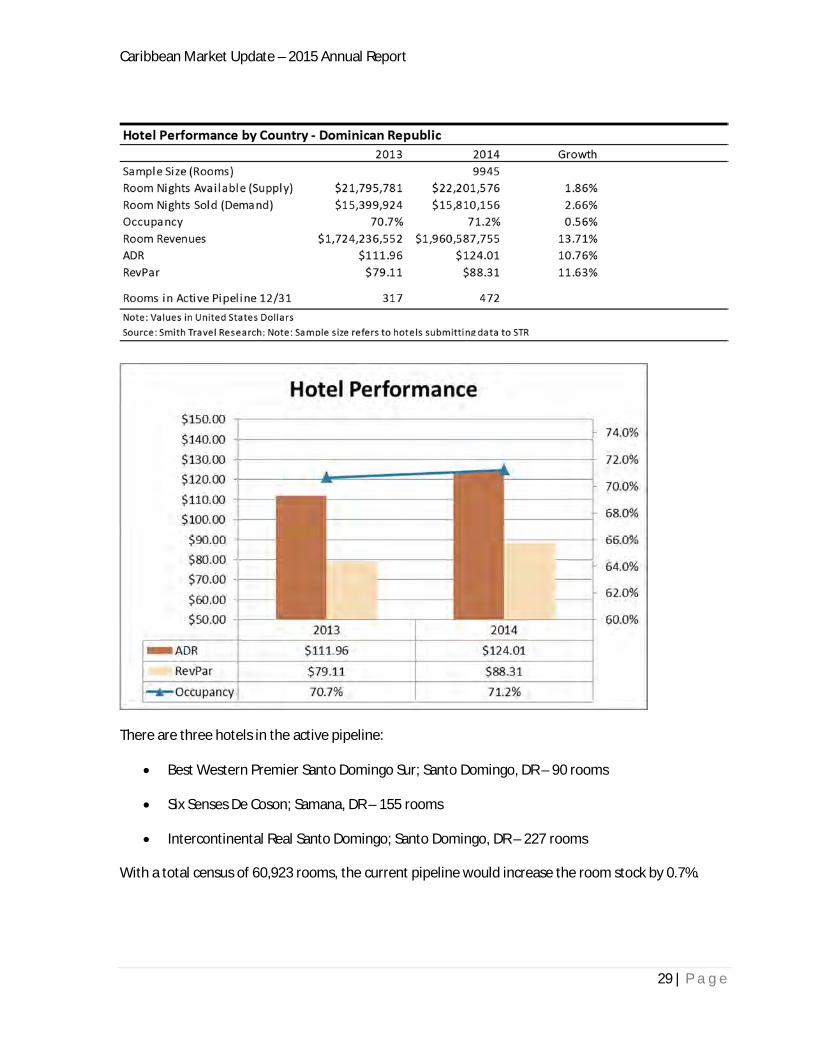

Hotel Performance Data from Smith Travel Research indicates 2014 occupancy for reporting hotels of 71.2%, up 0.56% from the prior year. The reported average daily rate (ADR) was $124.01 (up 10.76%), leading to Revenue Per Available Room Night (RevPar) of $88.31 (up 11.63%). The growth in hotel performance has been stronger than any other Caribbean destination.

Caribbean Market Update – 2015 Annual Report

29 | P a g e

There are three hotels in the active pipeline:

Best Western Premier Santo Domingo Sur; Santo Domingo, DR – 90 rooms

Six Senses De Coson; Samana, DR – 155 rooms

Intercontinental Real Santo Domingo; Santo Domingo, DR – 227 rooms

With a total census of 60,923 rooms, the current pipeline would increase the room stock by 0.7%.

Caribbean Market Update – 2015 Annual Report

30 | P a g e

Economic Activity GDP grew 6.3% in the third quarter of 2014 compared with the same period of the previous year, marking a slight slowdown in growth compared to Q2’s 7.5% increase. Even still, the economy showed significant growth rates in the first three quarters of 2014 due to increasing total consumption and growing exports. The Central Bank estimates that the economy grew 7.1% in 2014, which is significantly better than the 4.6% growth rate recorded in 2013. The annual figure for 2013 indicated an increase in economic activity in the fourth quarter. The Central Bank also reported that the external sector improved significantly in 2014 as the current fiscal deficit shrank along with an increase in international reserves compared to the previous year.

Conclusions The Dominican Republic is the largest and fastest growing tourism destination in the Caribbean. The tourism sector benefits from solid airlift, an abundance of resorts across a wide range of chain scales, and a relatively low cost of operations. There is seemingly increased interest in investment from international developers, and a significant amount of coastal land remaining undeveloped in this relatively large landmass. The country suffers from high unemployment and low per capita income, and also has a problem with immigration; mostly related to its neighbor, Haiti. Overall, the country is poised for economic growth along with much of Latin America, but also benefitting from increasing demand for tourism in the Caribbean region.

Caribbean Market Update – 2015 Annual Report

31 | P a g e

The Bahamas Market Report

Tourism The Bahamas market ranks 5th in the list of the top tourism markets in the Caribbean in terms of stay-over arrivals, with estimated year-end 2014 stay-over arrivals of about 1,411,000 based on year over year growth through July. The year 2014 indicated moderate growth in arrivals, with 3.50% growth over the prior period based on data through July. The chart below illustrates the relationship between arrivals and GDP.

Source: Caribbean Tourism Association, WorldBank, Integra Realty Resources

Hotel Performance Hotel occupancy figures continue to improve, with preliminary statistics for the year to date December, 2014 indicating overall occupancy improving by 5% to 56.9%. Average Daily Rates declined slightly for the period, however, to $197.04 (-3.9%). In the Family Islands, occupancy improved 4.2% to 43.3%, and rates improved 7.6% to $176.08.

The following graphs illustrate the trends regarding hotel performance. Once again, Grand Bahama underperforms the rest of the country in terms of hotel rates.

Caribbean Market Update – 2015 Annual Report

32 | P a g e

Source for Chart Data: TourismToday.com

Caribbean Market Update – 2015 Annual Report

33 | P a g e

According to Smith Travel Research (STR Inc.), there are eight hotels with 2,743 rooms in the active pipeline. Of these, 2,320 rooms are within the four new Baha Mar hotels under construction on Cable Beach, New Providence. This project has experienced some delays in opining, and is now slated to open in April, 2015. Additional projects in the pipeline include Montage Royal Island (Eleithera, 80 rooms), Langham Place Resort (Long Island, 224 rooms), Rock Resorts Rum Cay Resort (100 rooms), French Leave Eleuthera (19 rooms) and Resorts World Marina Hotel in North Bimini (350 rooms).

Real Estate The value of real estate sales in the Bahamas Real Estate Association (BREA) multiple listing service declined by nearly 29% in 2014 to about $162.7 million on 337 transactions; with the number of sales up from 318 (+6%) in the prior year. As a result, the average sale price dropped 24.5% to $482,678.

Source: BREA MLS

Notable News and Developments The stalled Abaco Club at Winding Bay finally has new owners, following a buyout by

Southworth Development LLC in partnership with the Abaco Club homeowners group. The development was previously owned by Marriott Vacations Worldwide and was branded a Ritz Carlton Club. The Abaco Club had been at the centre of a dispute between the property owners and Marriott who had been seeking to sell it for more than a year. They acquired it from original developer, UK entrepreneur Peter de Savary. Marriott had begun operating the resort-residential property as a hotel following a lack of sales of ownership units, a move that

Caribbean Market Update – 2015 Annual Report

34 | P a g e

the homeowners disputed. The new owners plan to inject $123 million into improvements of the development.

The mega resort Baha Mar remains incomplete, with the planned opening having been moved back from November 2014 to May 2015. Meanwhile there is some discontent in Nassau regarding the importation of over 4,000 Chinese construction workers for the project which is being financed by a Chinese government entity. Reportedly many of the citizens are complaining over a lack of economic benefit to the country, there have been reports of protest by the workers over working conditions, and reports by subcontractors of difficulties in getting paid.

The Government of the Bahamas is reportedly in advanced negotiations to bring a Four

Seasons branded hotel to the stalled Cotton Bay project on South Eleuthera. The current rendition of Cotton Bay contains 2,200 acres of land and plans for a mixed use resort with golf course. This project stalled after mostly completing its first phase of villa development and common area amenities. There are reportedly two other hotels in the overall development plan.

Conclusions There is a reasonable amount of activity on the island of New Providence, mostly as a result of the investment of the Chinese Government; including the development of the Baha Mar Resort, the expansion of the international airport, and the recent acquisition of the British Colonial Hilton in Nassau. Reportedly, the Chinese are also considering the proposed re-development of Bay Street in downtown Nassau; something the city very much needs for re-vitalization.

Outside of New Providence, the tourism statistics and general economic conditions appear to be relatively stagnant. Exceptions include a few developments in the Family Islands such as Bakers Bay in Abaco, which is being built and sold by a well-respected developer with a significant success record.

Our overall projections are for gradual improvement in the tourism sector and overall economy, yet it is likely that the opening of Baha Mar will have a downward effect on occupancy and rates in New Providence/Paradise Island for the next few years.

Caribbean Market Update – 2015 Annual Report

35 | P a g e

IRR-Caribbean provides real property and business valuation and consulting services throughout the Caribbean region; specializing in hotel and resort investment assets and businesses.

James V. Andrews MAI, CRE, ASA, FRICS, CVA Managing Director Integra Realty Resources – Caribbean Direct (345) 516-4508 Email: [email protected] Website: www.irr.com/caribbean Main Office P.O. Box 11905 Grand Cayman, KY1-1010 Cayman Islands Virgin Islands Office 6500 Red Hook Plaza Suite 206 St. Thomas, VI 00802 Bahamas Office P. O. Box N-9251 Nassau, Bahamas

Integra Realty Resources, Inc.

Corporate Profile

With corporate headquarters in New York City, Integra Realty Resources (IRR) is the largest independent commercial real estate valuation and counseling firm in North America, with 66 offices in 34 states and more than 200 Members of the Appraisal Institute (MAI) who are among its more than 900 employees across the United States and the Caribbean. IRR combines the intimate market knowledge of well-established local valuation and counseling experts with the powerful resources and capabilities of a national company. IRR offers its clients integrated technology, national data and information systems, and standardized valuation models and report formats for ease of review and analysis. An MAI-designated senior managing director runs each of IRR’s offices; the directors on average have 25 years of commercial real estate experience in their local markets. Founded in 1999, the IRR specializes in real estate appraisals, feasibility and market studies, expert testimony, and related property consulting services. Many of the nation’s largest and most prestigious financial institutions, developers, corporations, law firms, and government agencies are among its clients. For more information, visit www.irr.com or blog.irr.com.

A listing of IRR’s local offices and their Senior Managing Directors follows:

ATLANTA, GA - Sherry L. Watkins., MAI, FRICS AUSTIN, TX - Randy A. Williams, MAI, SR/WA, FRICS BALTIMORE, MD - G. Edward Kerr, MAI, MRICS BIRMINGHAM, AL - Rusty Rich, MAI, MRICS BOISE, ID - Bradford T. Knipe, MAI, ARA, CCIM, CRE, FRICS BOSTON, MA - David L. Cary, Jr., MAI, MRICS CHARLESTON, SC - Cleveland “Bud” Wright, Jr., MAI CHARLOTTE, NC - Fitzhugh L. Stout, MAI, CRE, FRICS CHICAGO, IL - Eric L. Enloe, MAI, FRICS CINCINNATI, OH - Gary S. Wright, MAI, FRICS, SRA CLEVELAND, OH - Douglas P. Sloan, MAI COLUMBIA, SC - Michael B. Dodds, MAI, CCIM COLUMBUS, OH - Bruce A. Daubner, MAI, FRICS DALLAS, TX - Mark R. Lamb, MAI, CPA, FRICS DAYTON, OH - Gary S. Wright, MAI, FRICS, SRA DENVER, CO - Brad A. Weiman, MAI, FRICS DETROIT, MI - Anthony Sanna, MAI, CRE, FRICS FORT WORTH, TX - Gregory B. Cook, SR/WA GREENSBORO, NC - Nancy Tritt, MAI, SRA, FRICS GREENVILLE, SC - Michael B. Dodds, MAI, CCIM HARTFORD, CT - Mark F. Bates, MAI, CRE, FRICS HOUSTON, TX - David R. Dominy, MAI, CRE, FRICS INDIANAPOLIS, IN - Michael C. Lady, MAI, SRA, CCIM, FRICS JACKSON, MS - J. Walter Allen, MAI, FRICS JACKSONVILLE, FL - Robert Crenshaw, MAI, FRICS KANSAS CITY, MO/KS - Kenneth Jaggers, MAI, FRICS LAS VEGAS, NV - Charles E. Jack IV, MAI LOS ANGELES, CA - John G. Ellis, MAI, CRE, FRICS LOS ANGELES, CA - Matthew J. Swanson, MAI LOUISVILLE, KY - Stacey Nicholas, MAI, MRICS MEMPHIS, TN - J. Walter Allen, MAI, FRICS MIAMI/PALM BEACH, FL - Scott M. Powell, MAI, FRICS

MIAMI/PALM BEACH, FL- Anthony M. Graziano, MAI, CRE, FRICS MINNEAPOLIS, MN - Michael F. Amundson, MAI, CCIM, FRICS NAPLES, FL - Carlton J. Lloyd, MAI, FRICS NASHVILLE, TN - R. Paul Perutelli, MAI, SRA, FRICS NEW JERSEY COASTAL - Halvor J. Egeland, MAI NEW JERSEY NORTHERN - Barry J. Krauser, MAI, CRE, FRICS NEW YORK, NY - Raymond T. Cirz, MAI, CRE, FRICS ORANGE COUNTY, CA - Larry D. Webb, MAI, FRICS ORLANDO, FL - Christopher Starkey, MAI, MRICS PHILADELPHIA, PA - Joseph D. Pasquarella, MAI, CRE, FRICS PHOENIX, AZ - Walter ‘Tres’ Winius III, MAI, FRICS PITTSBURGH, PA - Paul D. Griffith, MAI, CRE, FRICS PORTLAND, OR - Brian A. Glanville, MAI, CRE, FRICS PROVIDENCE, RI - Gerard H. McDonough, MAI, FRICS RALEIGH, NC - Chris R. Morris, MAI, FRICS RICHMOND, VA - Kenneth L. Brown, MAI, CCIM, FRICS SACRAMENTO, CA - Scott Beebe, MAI, FRICS ST. LOUIS, MO - P. Ryan McDonald, MAI, FRICS SALT LAKE CITY, UT - Darrin W. Liddell, MAI, CCIM, FRICS SAN ANTONIO, TX - Martyn C. Glen, MAI, CRE, FRICS SAN DIEGO, CA - Jeff A. Greenwald, MAI, SRA, FRICS SAN FRANCISCO, CA - Jan Kleczewski, MAI, FRICS SARASOTA, FL - Carlton J. Lloyd, MAI, FRICS SAVANNAH, GA - J. Carl Schultz, Jr., MAI, FRICS, CRE, SRA SEATTLE, WA - Allen N. Safer, MAI, MRICS SYRACUSE, NY - William J. Kimball, MAI, FRICS TAMPA, FL - Bradford L. Johnson, MAI, MRICS TULSA, OK - Robert E. Gray, MAI, FRICS WASHINGTON, DC - Patrick C. Kerr, MAI, SRA, FRICS WILMINGTON, DE - Douglas L. Nickel, MAI, FRICS CARIBBEAN/CAYMAN ISLANDS - James Andrews, MAI, FRICS

Corporate Office 1133 Avenue of the Americas, 27th Floor, New York, New York 10036 Telephone: (212) 255-7858; Fax: (646) 424-1869; E-mail [email protected] Website: www.irr.com