Embed Size (px)

Citation preview

Presented By:

Curtis L. Lyman,

J.D.

CEO

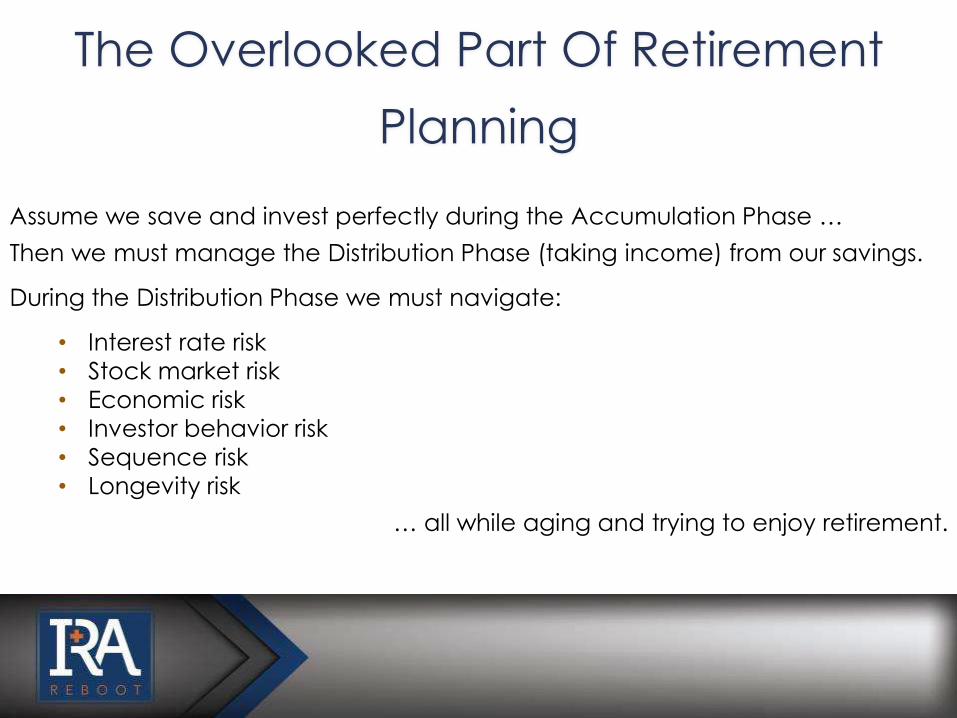

The Overlooked Part Of Retirement

Planning

Assume we save and invest perfectly during the Accumulation Phase …

Then we must manage the Distribution Phase (taking income) from our savings.

During the Distribution Phase we must navigate:

• Interest rate risk

• Stock market risk

• Economic risk

• Investor behavior risk

• Sequence risk

• Longevity risk

… all while aging and trying to enjoy retirement.

How Does The Government Raise

Revenue

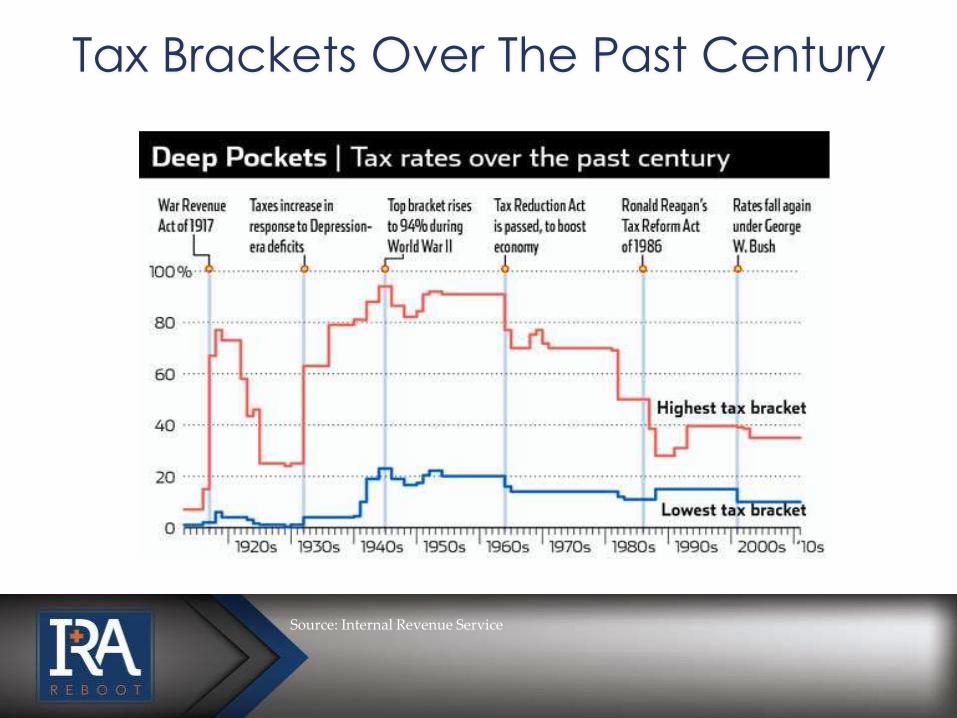

Tax Brackets Over The Past Century

Source: Internal Revenue Service

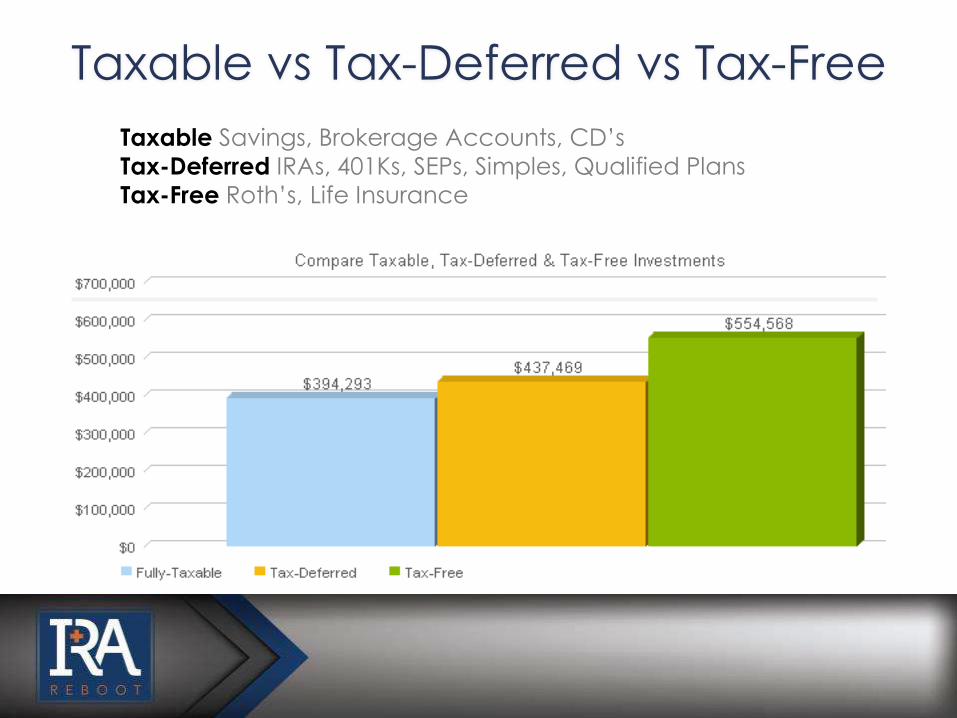

Taxable vs Tax-Deferred vs Tax-Free

Taxable Savings, Brokerage Accounts, CD’s

Tax-Deferred IRAs, 401Ks, SEPs, Simples, Qualified Plans

Tax-Free Roth’s, Life Insurance

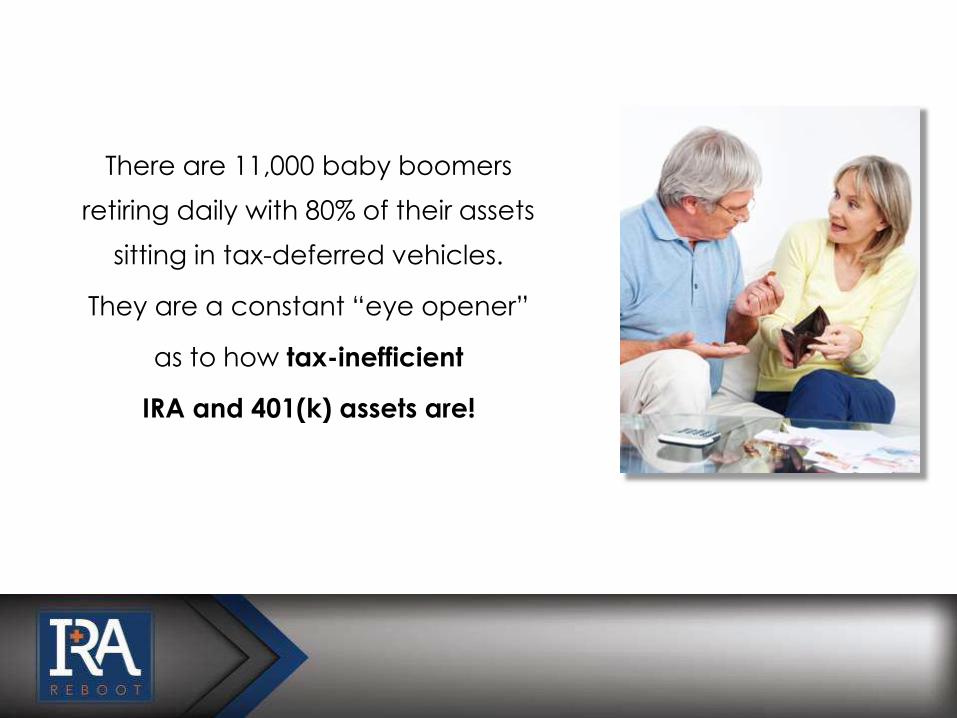

There are 11,000 baby boomers

retiring daily with 80% of their assets

sitting in tax-deferred vehicles.

They are a constant “eye opener”

as to how tax-inefficient

IRA and 401(k) assets are!

What is your

IRA or 401K

really worth

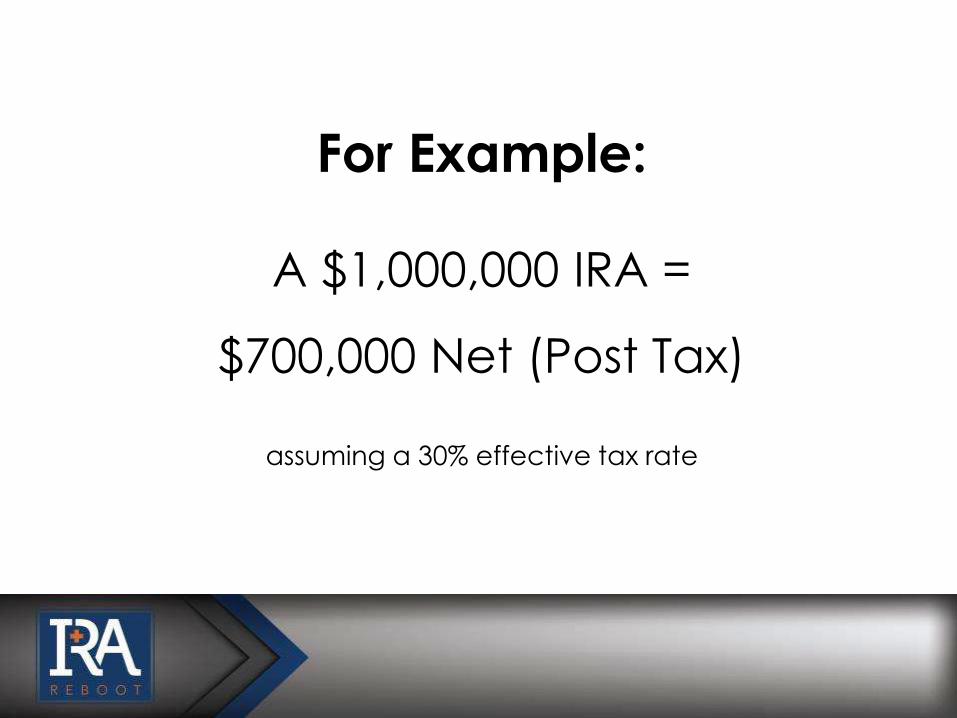

For Example:

A $1,000,000 IRA =

$700,000 Net (Post Tax)

assuming a 30% effective tax rate

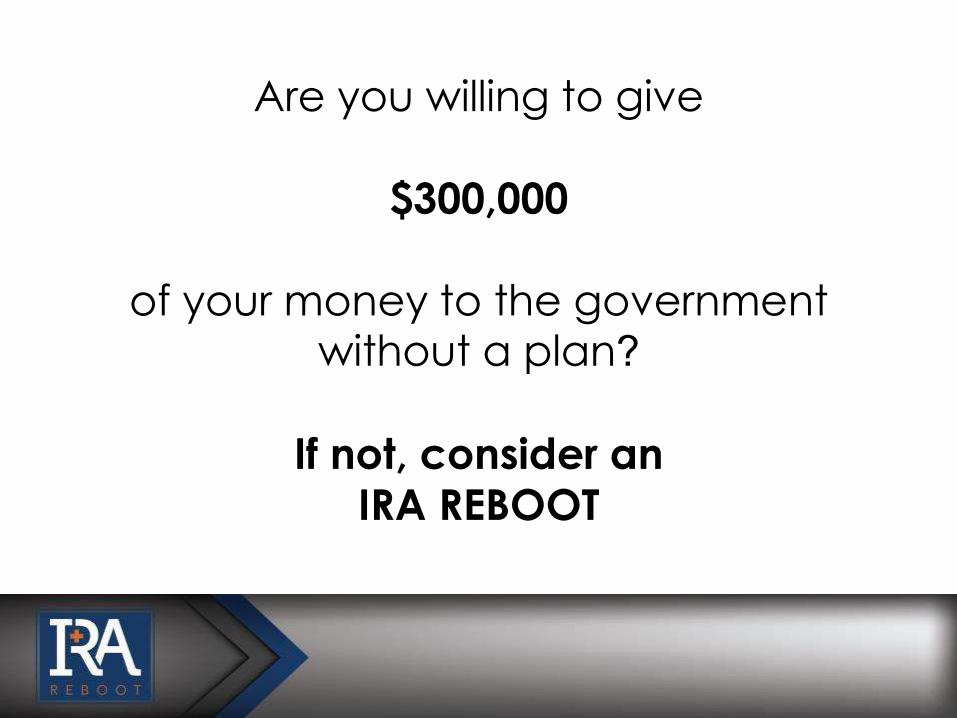

Are you willing to give

$300,000

of your money to the government without a plan?

If not, consider an

IRA REBOOT

Convert your taxable assets into a

vehicle

efficiently and effectively using

Index Universal Life Insurance!

IRA RESCUE

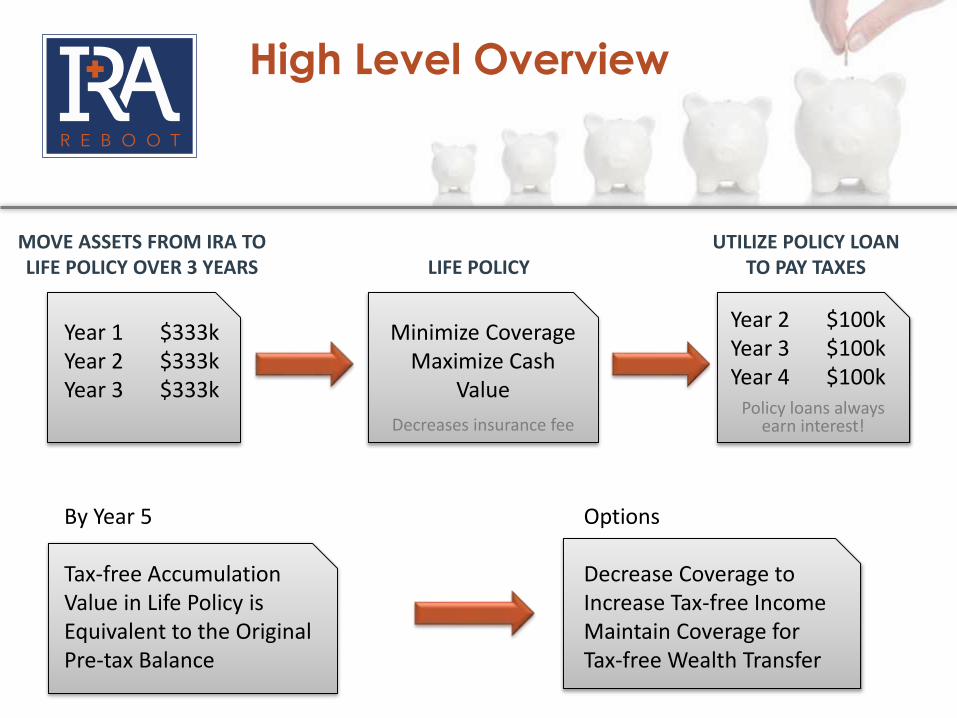

High Level Overview

Year 2 $100kYear 3 $100kYear 4 $100k

Policy loans always earn interest!

UTILIZE POLICY LOAN TO PAY TAXES

By Year 5

Tax-free Accumulation Value in Life Policy is Equivalent to the Original Pre-tax Balance

Options

Decrease Coverage to Increase Tax-free Income Maintain Coverage forTax-free Wealth Transfer

Year 1 $333kYear 2 $333kYear 3 $333k

MOVE ASSETS FROM IRA TO LIFE POLICY OVER 3 YEARS

Minimize Coverage Maximize Cash

Value

Decreases insurance fee

LIFE POLICY

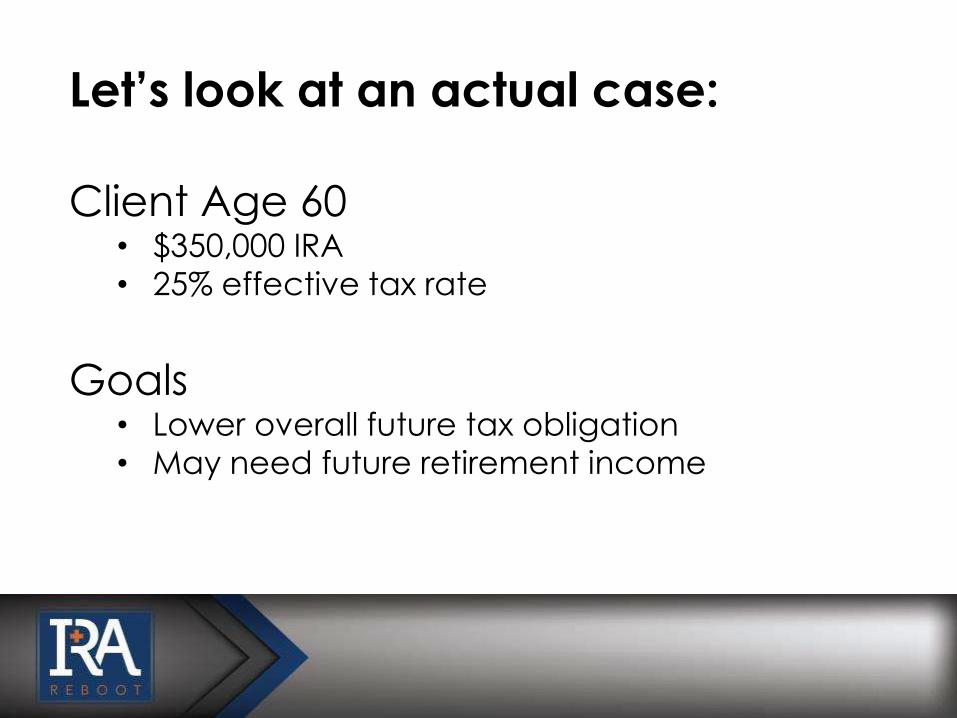

Let’s look at an actual case:

Client Age 60 • $350,000 IRA

• 25% effective tax rate

Goals• Lower overall future tax obligation

• May need future retirement income

Why This Method Works

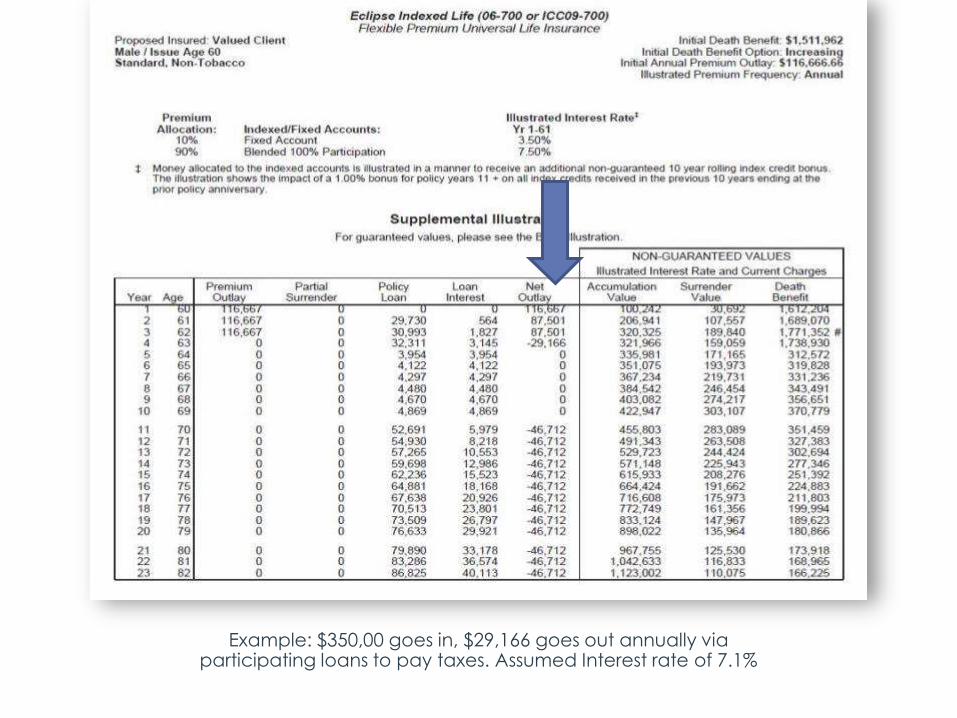

Example: $350,00 goes in, $29,166 goes out annually via participating loans to pay taxes. Assumed Interest rate of 7.1%

Why This Strategy Works

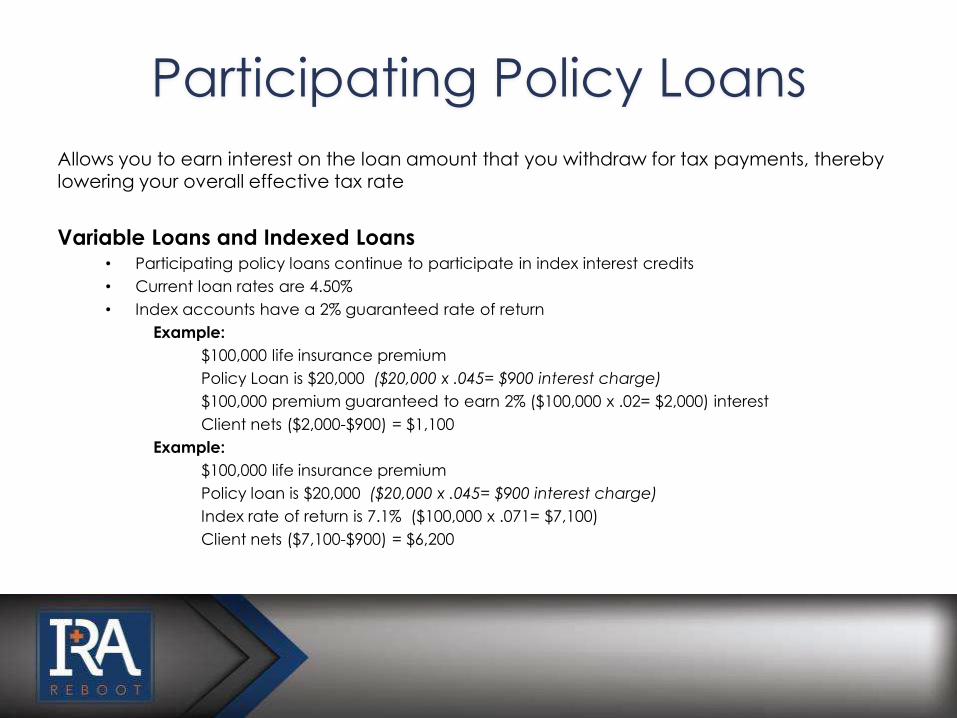

Participating Policy Loans

Allows you to earn interest on the loan amount that you withdraw for tax payments, thereby lowering your overall effective tax rate

Variable Loans and Indexed Loans• Participating policy loans continue to participate in index interest credits

• Current loan rates are 4.50%

• Index accounts have a 2% guaranteed rate of return

Example:

$100,000 life insurance premium

Policy Loan is $20,000 ($20,000 x .045= $900 interest charge)

$100,000 premium guaranteed to earn 2% ($100,000 x .02= $2,000) interest

Client nets ($2,000-$900) = $1,100

Example:

$100,000 life insurance premium

Policy loan is $20,000 ($20,000 x .045= $900 interest charge)

Index rate of return is 7.1% ($100,000 x .071= $7,100)

Client nets ($7,100-$900) = $6,200

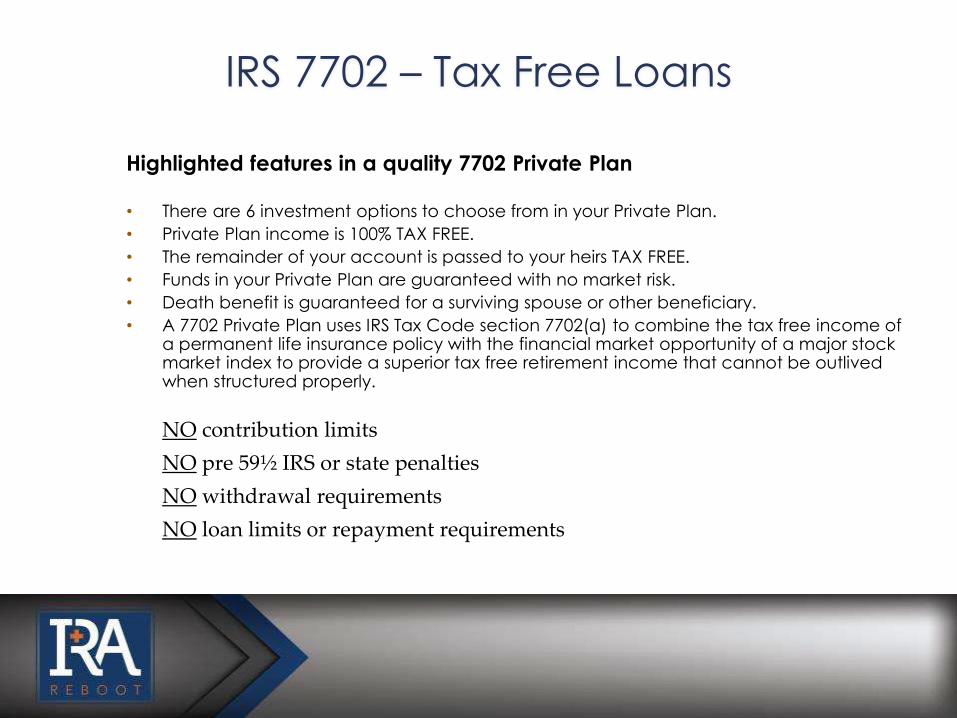

IRS 7702 – Tax Free Loans

Highlighted features in a quality 7702 Private Plan

• There are 6 investment options to choose from in your Private Plan.

• Private Plan income is 100% TAX FREE.

• The remainder of your account is passed to your heirs TAX FREE.

• Funds in your Private Plan are guaranteed with no market risk.

• Death benefit is guaranteed for a surviving spouse or other beneficiary.

• A 7702 Private Plan uses IRS Tax Code section 7702(a) to combine the tax free income of a permanent life insurance policy with the financial market opportunity of a major stock market index to provide a superior tax free retirement income that cannot be outlived when structured properly.

NO contribution limits

NO pre 59½ IRS or state penalties

NO withdrawal requirements

NO loan limits or repayment requirements

Death Benefit Reduction

Option to decrease the death benefit to increase tax-free income after

the MEC period

• The MEC “look back” period resets back to 30 days when a life contract

makes a “material change”

• This allows the 7-pay test to be fulfilled prior to 7 years

• What constitutes a material change?

Increasing coverage to level coverage

Premium stop and coverage reduction

Reducing the face amount after the MEC period is over allows you to

reduce your over all cost of insurance and maximize tax free cash

accumulation and interest.

Flexibility, Liquidity, Safety

• Flexibility to convert IRA to a tax free retirement vehicle over 3 to 7 years

• Liquidity to accommodate high effective tax rates

• Numerous investment options that limit downside risk during conversion period

Index options have a 2% lifetime guarantee floor

Various cap options reflecting 13 – 32%

Fixed account currently paying 3.5% guaranteed

• Ability to adjust your loan option annually between variable, indexed and

fixed to take advantage of any interest rate environment

This new tax-efficient vehicle can be used for:

• Guaranteed tax-free lifetime income

• Tax-free wealth transfer

Clients are not required to lower the face amount if their

legacy needs change

• Tax-free accumulation

• Long Term Care Coverage

Additional Benefits Of Over-Funded

Life Insurance

• No capital gains tax

• Not included in provisional income when calculating taxation

of SS benefits

• Eliminates taxable interest income as long as policy is in force

• No RMD’s are required at 70½

• Avoid 10% penalty for withdrawals pre 59½

Ideal Client

• Clients between the age 55-72

• Clients in reasonable health (standard or higher)

• Clients with large pools of qualified assets

• Clients with high effective tax rates

• Clients seeking tax free income

• Clients who are “tax Sensitive”

Isn’t Tax-Free Better Than Taxable?

Don’t wait! Let us show you how an IRA Reboot

can improve your retirement.

Curtis L. Lyman, J.D.

Isn’t Tax-Free Better Than Taxable?

Don’t wait! Let us show you

how an IRA Reboot can

improve your retirement.

Securities offered thru HighTower Securities, LLC - Member FINRA, MSRB and SIPC, and with HighTower Advisors, LLC, a Registered Investment Advisor with the SEC. Securities are offered through HighTower Securities, LLC; advisory services are offered through HighTower Advisors, LLC.

This is not an offer to buy or sell securities. No investment process is free of risk, and there is no guarantee that the investment process or the investment opportunities referenced herein will be profitable. Past performance is not indicative of current or future performance and is not a guarantee. The investment opportunities referenced herein may not be suitable for all investors.

All data and information reference herein are from sources believed to be reliable. Any opinions, news, research, analyses, prices, or other information contained in this research is provided as general market commentary, it does not constitute investment advice. Alpha Beta Gamma Wealth Management, The Lyman Group and HighTower shall not in any way be liable for claims, and make no expressed or implied representations or warranties as to the accuracy or completeness of the data and other information, or for statements or errors contained in or omissions from the obtained data and information referenced herein. The data and information are provided as of the date referenced. Such data and information are subject to change without notice.

This document was created for informational purposes only; the opinions expressed are solely those of The Lyman Group and Alpha Beta Gamma Wealth Management, Alpha Beta Gamma Retirement Solutions and do not represent those of HighTower Advisors, LLC, or any of its affiliates.

![[Conference] Building Websites that Matter - Agent Reboot Boston, Agent Reboot DC, Agent Reboot Austin](https://img.pdfslide.us/doc/110x75/558a27d9d8b42a98578b465c/conference-building-websites-that-matter-agent-reboot-boston-agent-reboot-dc-agent-reboot-austin.jpg)