Embed Size (px)

Citation preview

Interactive Brokers Group (IBKR)

How Do You Analyze & Value Rapid Growth?

In 1975, Charles Schwab disrupted the investing industry with discounted trading fees. By cutting costs and overhead it could undercut the full-service brokers on price.

By the boom of 1999, Schwab’s market cap

exceeded that of all the full-service brokers.

Is a competitor doing to Schwab what Schwab

did to Merrill Lynch et. al.?

Ticker:

IBKR

Stock Price:

$27

Market Cap:

~1.57B

EV:

FY2014 P/E:

Interactive Brokers

Background

Business Overview

• IBG began as a market maker in 1977

• Launched brokerage business in 1993

• As of 3Q14, 97% of pre-tax income is from brokerage segment

• Largest US e-broker by number of trades

• Offers access to 100+ markets in 24 countries

• #1 e-broker in Barron’s for past 3 years

• Highly automated & efficient - $1.2M revenue per employee

The Wealth Management Ecosystem

FinancingBanks, Investors

IT

Labor

GovernmentRegulation

Individual

InvestorsUltra-High Net Worth

High Net Worth

Mass Affluent

DIY Investors

ExchangesCME

NDAQ

ICE

CBOE

IEX

Dark Pools

Wealth ManagementE-Brokers, Wirehouses, RIAs,

Broker/Dealers

IntermediariesHedge Funds

Mutual Funds

Competition in the U.S. Wealth Management Industry

Business

Model

Customer

Segment

Low Touch

High Touch

DIYMass Affluent

$100,000-1,000,000HNW

$1,000,000-5,000,000

UHNW

$5,000,000+

DIRECT PROVIDERS (MUTUAL FUND SUPERMARKETS & E-BROKERS)

SCHW ETFC AMTD IBKR FIDELITY VANGUARD T. ROWE PRICE

INSURANCE BROKER/DEALER

AMERIPRISE

WIREHOUSES

BAC WFC

REGIONAL BROKER/DEALER

Raymond James Stifel Financial

BANK BROKER/DEA;ER

BNP Paribas Credit Suisee UBS

The E-Broker Industry Has Attractive Economic Characteristics

• Low asset-intensity and reinvestment

needs

• High fixed costs and scale advantages

• High switching costs. Once customers

open an account, inertia takes over.

• Very high ROICs

The Basic Business Model for E-Brokers is Simple

• E-brokers compete on price, selection and

convenience over their brick and mortar

competitors

• The formula for success is straightforward

Scale efficiencies permit low prices, better

customer experience

Low prices attract more customers

More customers drive greater scale

Greater scale permits further price decreases

And so on . . .

But, a business model is not a strategy.

Competitors’ “Strategy”• Schwab, E-Trade and Ameritrade serve the

same customers, meet the same needs and sell

at the same relative price. This is not a strategy.

• All 3 target the Mass Affluent segment and offer

basic stock trading and low commissions

complemented by higher-end wealth

management services.

• The best they can hope is the emergence of a

cozy oligopoly.

• In an industry where $/million traded has been

dropping for 40 years, this is unlikely.

IBG’s competitive strategy is fundamentally different.

• Basic business model is the same as the

other e-brokers

• But, IBG meets the “idiosyncratic” needs of

only a segment of the customers & offers

only a subset of the industry’s services

• IBG does not try to be all things to all people

Trade Offs Embedded in IBG’s Strategy• No physical locations

• No in-person service to customers

• No educational services or other amenities for

novice investors

• No banking services

• No sale of order flow revenue

• No asset management fees

IBG’s Target Customer

• Target Customer -

• Low Cost

• Self-Service/Reduced Hand Holding

• Latest in trading technology

• Derivatives expertise

• Worldwide access/Unusually broad

product offerings

• Frequent trading

• Examples: hedge funds, mutual funds,

introducing brokers, proprietary trading

groups and financial advisors and active

individual traders

Target Market

Management understands this trade off:

“We believe that the better the prices we get for

our customers, the better their performance will be

and the more business they will bring to us. On

the other hand, our competitors believe that most

customers can’t tell the difference between good

and bad executions. I think we both could be right.

As a result, they end up with the customers who

can’t tell the difference and we end up with those

who can.”

- Thomas Peterffy, CEO, Q3 2014 Earnings Call

Impact of IBG’s Strategic Choices

• IBG is using its cost advantages to compete on

price, gain share and drive its competitors out of

this segment of the business.

• Competitors are focused on asset management

and administration fees and de-emphasizing

trading revenue.

• IBG carved out a niche that relies on high

volume/low price. Competitors are not

interested.

IBG’s targeted strategy & defendable niche

results in structural advantages.

Revenue Sources of the Major E-Brokers

Schwab, E*Trade & Ameritrade are in the asset-

gathering business. IBG is in the trading business.

IBG Schwab

Ameritrade1

E-Trade

1. Ameritrade remains a strong player in trading because of its strong options business.

Growth is accelerating

Source: IBG Investor Presentation, 11/14.

Key Growth Rates

Item 5 Year CAGR

Revenue (Brokerage Only) 15%

Pre-Tax Income (Brokerage

Only)*

18%

Total Accounts 16%

Customer Equity 32%

Total Customer DARTs 10%

Margin Receivable 43%

*Excludes 2013 non-recurring expense.

Competitive Advantages

Competitive Advantage #1 – Cost Structure/Pricing

2013 Expenses

Per Trade

100 Share

Commission

Amount

$25K Margin

Loan Rate

Charles Schwab $28.71 $8.95 8.00%

E*TRADE

$27.02

$7.99 7.94%

Ameritrade $16.33 $9.99 8.50%

Interactive Brokers $2.75 $1.00 1.57%

Source: Expenses per trade are per my calculations. Prices are per IBG website.

IBG dramatically undercuts competitors on costs

and price.

IBG can be profitable at a price level that leaves their

competitors losing money.

Better

Customer

Experience

Virtuous Circle of Scale Advantages

More Traffic

More

Selection

Lower

Cost

Structure

Lower

Prices

Better

Execution Growth

Based on a napkin sketch prepared by Jeff Bezos to illustrate Amazon’s

model.

Operating Leverage at Work

Operating expenses are growing much slower than

revenue.

Brokerage Revenue & Operating Expense, 2005-13*

Growth spreads fixed costs across more sales, thus

reducing cost per unit.

*2013 expenses does not include non-recurring expense of $64.

Changing Business Mix

Operating Income by Segment, 2005-2013

The declining market maker business masks the

high growth of the brokerage business.

Competitive Advantage #2 – Best Customer ExperienceIBG offers compelling advantages to its target

customer:

• Best Execution - IBG does not sell order flow

• Widest Breadth of Product - 5 million equities,

mutual funds, ETFs, options and futures from 24

countries.

• Superior Trading Technology

Scale provides ability to invest heavily in

customer experience.

Competitive Advantage #3 – Owner-Operator owns 75% of company

• Like Schwab, the founder of IBG continues to

own the vast majority of the shares and run the

company

• Peterffy is 70 and just named successor

• Strong culture

Valuation Process*

*This process was inspired by Charlie Munger & Prof. Sanjay Bakshi, See “The Final Relaxo Lecture”

Step #1 Identify Future Value Drivers

The critical driver for IBG will be sales growth

(rather than capital turns, expense reduction, etc.)

driven by (1) business volume growth and (2)

average realization growth propelled by changes in

customer mix, product mix, inflation and price

power of the business.

The table below shows historical results.

2006 2007 2008 2009 2010 2011 2012 2013 8 Yr. CAGR 5 Yr. CAGR

Net Revenue USD Millions 298.4 425.2 505.8 474.4 547.3 691.5 670.4 814 15% 14%

Total Trades Millions 50 77 94 87 94 112 104 125 14% 9%

Margin Receivable USD Millions 0.85 1.91 1.55 3.23 7 7 9.85 13.6 49% 43%

Commission/DART USD 4.48 4.27 3.86 4.36 4.35 4.07 4.24 4.23 -1% -1%

Step #2 Project the Future Drivers Forward

The average annual growth in DARTs over the past

8 years was 14% and over the past 5 years was

10%.

I assume that DARTs will grow at 10% per year for

a decade. This means that in 2023, IBG will be

doing 1,294K DARTs versus 499K in 2013.

The margin receivable has been growing at 49%

rate for the past 8 years. This is not sustainable. I

assume a 20% CAGR for the next 10 years.

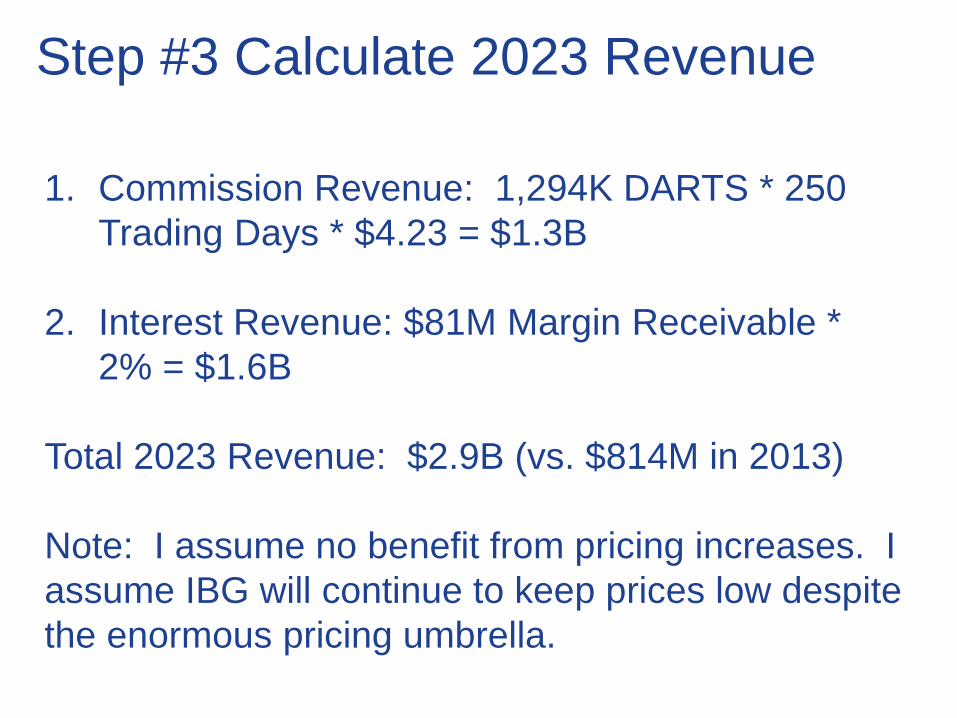

Step #3 Calculate 2023 Revenue

1. Commission Revenue: 1,294K DARTS * 250

Trading Days * $4.23 = $1.3B

2. Interest Revenue: $81M Margin Receivable *

2% = $1.6B

Total 2023 Revenue: $2.9B (vs. $814M in 2013)

Note: I assume no benefit from pricing increases. I

assume IBG will continue to keep prices low despite

the enormous pricing umbrella.

Step #4 Calculate 2023 Value

• After-Tax Income: $2.9B 2023 Revenue * 50%

Margin* – 35% income tax = $968MM

• $968MM * 15 P/E = $14.5B

• Current value = $10.2B (12/8/14)

Assumptions:

1. I used 5 year average margin. I assume no

benefit from further cost reductions or scale.

2. I assigned no value to the market maker

business.

Why Am I Comfortable Making 10 Year Projections?• The industry has been successful since the late

1990s

• IBG’s competitive advantages are sustainable

• Stock trading volume has been increasing for 200

years and is likely to continue.

Thus, (1) IBG can continue to grow faster than the

industry for at least 10 years and (2) even after a

decade of growth there should be plenty of growth

ahead.

Does it make any sense at this value?• Based on my conservative estimates, IBG stock will

appreciate 40% over the next 10 years with limited

risk.

• This is an annual return of 3.42% and not

particularly attractive.

![Interactive Brokers Group (IBKR) Q1 2016 Results - Earnings Call … · 2016. 4. 20. · First Quarter Financial Results Conference Call. [Operator Instructions] As a reminder, this](https://img.pdfslide.us/doc/110x75/5ff0d03c70df2535280c3724/interactive-brokers-group-ibkr-q1-2016-results-earnings-call-2016-4-20.jpg)