Embed Size (px)

Citation preview

The Services Research Company

Webinar:The State of Operations and Outsourcing 2017

January 12th, 2017

Host:PhilFershtChiefAnalystandCEOHfS [email protected]@pfersht

JamieSnowdonEVPMarketForecastingHfS [email protected]

DaveBrownGlobalLead,SharedServices&[email protected]

StanLepeakDirector&Head,Research&ThoughtLeadership,[email protected]

Overview:• 20years’businessexperienceintheglobalITandbusinessprocess

outsourcingandsharedservicesindustry• Coinedthe“As-a-ServiceEconomy”in2014• Industryanalyst,author,speaker,strategistandblogger• Advisedandcogitatedon100’sofglobalITservices,BPOandshared

servicesengagements• Meddleswiththelargestglobalnetworkofenterpriseservicesand

operationsprofessionals

CareerExperience:• PracticeLead,ITServices&BPOResearch,Gartner,Inc• GlobalBPOMarketplaceLeader, DeloitteConsulting• ConsultingPracticeLead,IDCAsia/Pacific• ITMarketsPracticeLead,IDCEurope

Education:• BSwithHonorsinEuropeanBusiness&Technology,CoventryUniversity,

UnitedKingdom• DiplômeUniversitairedeTechnologieinBusiness&Technologyfromthe

UniversityofGrenoble,France

Phil Fersht, Chief Analyst and CEO, HfS Research

JamieSnowdonEVPMarketForecastingHfS Research

DaveBrownGlobalLead,SharedServices&OutsourcingAdvisoryKPMG

StanLepeakDirector&Head,Research&ThoughtLeadership,GlobalManagementConsultingKPMG

The all-star panel

…With a More Serious Side Too! www.hfsresearch.com

AboutKPMG’sSharedServicesandOutsourcingAdvisorypractice

KPMGmemberfirmshavetheabilitytosupportclientstransformenterpriseservicesandhelpimprovevalue,increaseagilityandcreatesustainablebusinessperformance.

Who

What

How

TheSharedServicesandOutsourcingAdvisorypracticebringsaspecializedteamofmorethan1,000professionalswithinKPMG’sglobalnetworkofindependentmemberfirmsoperatingin155countries.Theyhelpclientsdesign,buildandmanageinformationtechnologyandbusinessprocessesacrosstheenterprise.

KPMGprofessionalshelpclientsaligntheirbusinessstrategy,organizationandexecutiontoenablethemtomanagetheentireITandbusinessprocesslifecycle,improvingbusinessperformanceandlayingthegroundworkforgenuinebusinesstransformation.

KPMGprofessionalsapplyfocusedresearch,automatingtools,proprietarydata,clearbusinessacumenandaforward-thinkingmind-settoprovidetimely,objectiveandactionableadviceandpracticalapproachesforclients.

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

ValueLeversOf

As-A-Service

TheWhat:ServicesToday

DataData

IntelligentAutomation

Efficiency, Labor, Data Augmentation

Software Platforms

Standardize processes, Scale, Write Off Legacy

Self Learning,Cognitive

Continuous Process Improvement, Innovation

Core Digital

Holistic View of CustomerOneOffice

Cost/Expertise/Scale

GlobalLabor

Shared Services, GICS

Centralization/Efficiency

B2BDigitalSpendCouldreach$2

TrillioninNorthAmericain

2020,ashighas$7

TrillionGlobally

The Innovation Killer Org Chart

©2017HfSResearch,Proprietary

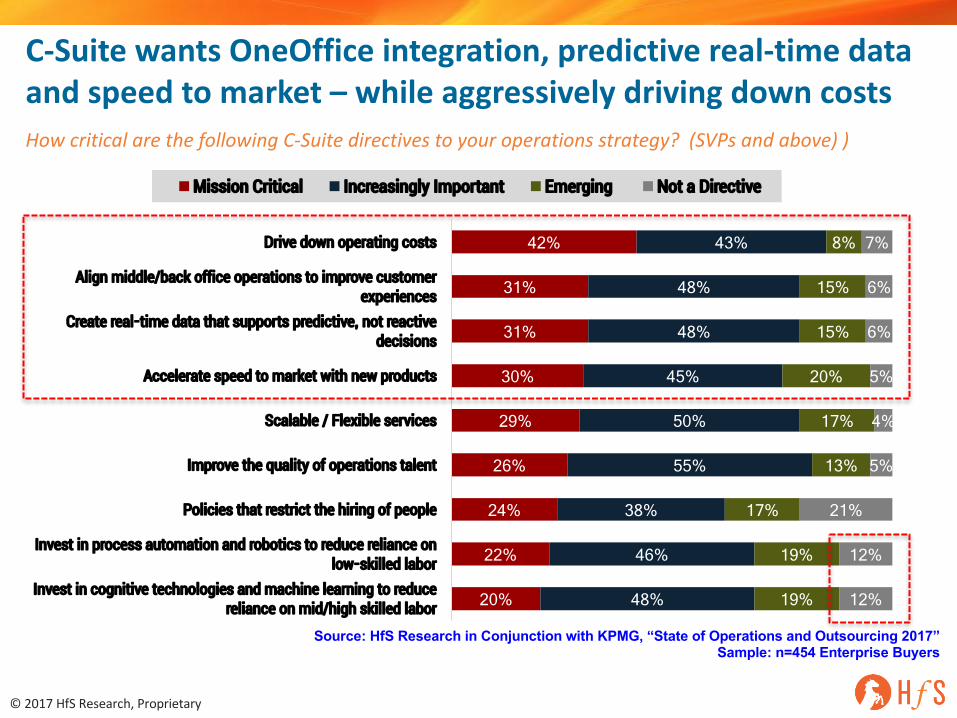

C-SuitewantsOneOfficeintegration,predictivereal-timedataandspeedtomarket– whileaggressivelydrivingdowncostsHowcriticalarethefollowingC-Suite directivestoyouroperationsstrategy? (SVPsandabove))

20%

22%

24%

26%

29%

30%

31%

31%

42%

48%

46%

38%

55%

50%

45%

48%

48%

43%

19%

19%

17%

13%

17%

20%

15%

15%

8%

12%

12%

21%

5%

4%

5%

6%

6%

7%

Invest in cognitive technologies and machine learning to reduce reliance on mid/high skilled labor

Invest in process automation and robotics to reduce reliance on low-skilled labor

Policies that restrict the hiring of people

Improve the quality of operations talent

Scalable / Flexible services

Accelerate speed to market with new products

Create real-time data that supports predictive, not reactive decisions

Align middle/back office operations to improve customer experiences

Drive down operating costs

Mission Critical Increasingly Important Emerging Not a Directive

Source: HfS Research in Conjunction with KPMG, “State of Operations and Outsourcing 2017” Sample: n=454 Enterprise Buyers

©2017HfSResearch,Proprietary

TheEndgame:TheDigitalOneOfficeTMOrganization

• Source:HfSResearch2016

The Service Providers will bifurcate into two groupings

BackOfficeOutsourcersEfficiency,Automation,LaborArbitrageandScalability

OneOfficeEnablersDataOrchestrationandHumanCollaboration

©2017HfSResearch,Proprietary

C-SuiteDirectives:Hi-techmostfocusedonchangeandgrowthHowcriticalarethefollowingC-Suite directivestoyouroperationsstrategy?(“MissionCritical”responses– allbuyers)

0%

20%

40%

60%

80%

Drive down operating costs

Accelerate speed to market with new products

Create real-time data that supports

predictive, not reactive

decisions

Align middle/back

office operations to improve customer

experiences

Improve the quality of

operations talent

Policies that restrict the hiring

of people

Invest in process automation and

robotics to reduce reliance on low-skilled

labor

Invest in cognitive

technologies and machine learning

to reduce reliance on

mid/high skilled labor

BFSI Manufacturing Healthcare&LifeSciences Retail Software&HiTech Energy&Utilities

Source: HfS Research in Conjunction with KPMG, “State of Operations and Outsourcing 2017” Sample: n=454 Enterprise Buyers

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

©2017HfSResearch,Proprietary

EnterpriseLeadershiphasAutomationastopInvestmentPriorityfor2017-2018

20%

19%

20%

23%

27%

29%

30%

25%

20%

30%

28%

28%

32%

34%

33%

43%

Hiringmillennials

Publiccloudinvestments

Cognitivecomputingsolutions

Trainingandworkforcedevelopment/changemanagement

SaaSplatformsreplacingon-premisesolutions

Analyticssolutions

Customer-centricdigitalenablement (Social/Mobile/Interactive)

Roboticautomationofprocesses

SVP+

VPandBelow

Q.Howmuchinvestmentisyourorganizationintendingtomakeinthefollowinginitiativesinthecomingtwoyears?(significantinvestmentselected)

• Source:HfSResearchinConjunctionwithKPMG,“StateofOperationsandOutsourcing2017”• Sample:n=454EnterpriseBuyers

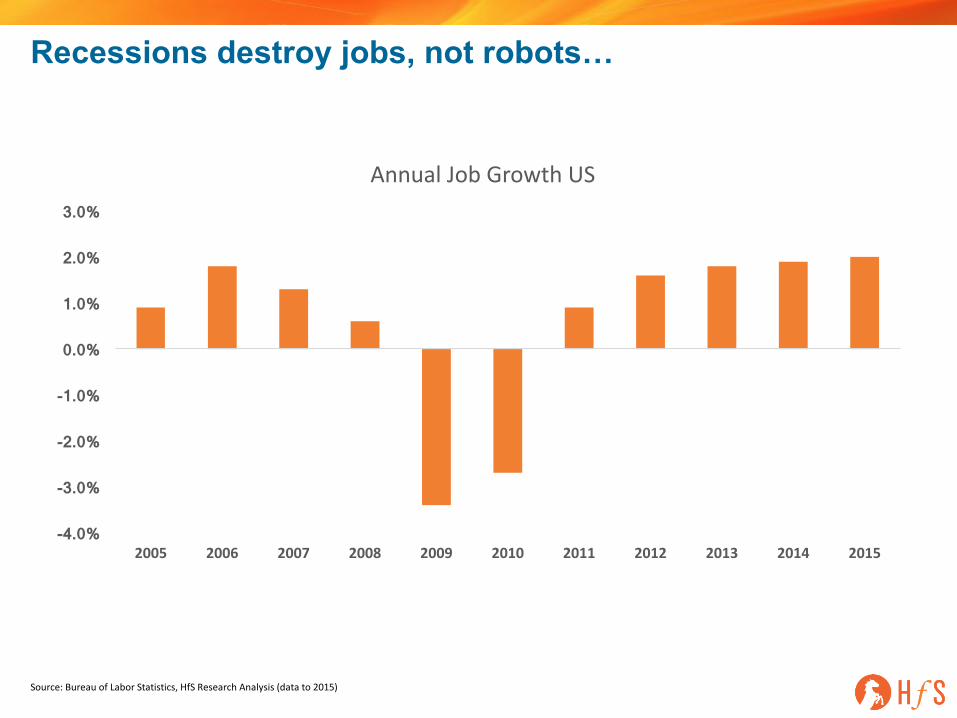

Source:BureauofLabor Statistics,HfSResearchAnalysis(datato2015)

Recessions destroy jobs, not robots…

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

AnnualJobGrowthUS

Total Impact of Automation on IT/BPO Services Workers by Major Country (likely scenario, low-skilled workers)

0.73 0.74

2.282.34

0.67

0.54

1.641.57

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0% 0.0

0.5

1.0

1.5

2.0

2.5

Philippines UK India US

%DecreaseinW

orkforce

ServicesW

orkers(M

illions)

2015 2021 %Change

Researchsources:1477industrystakeholderinterviews2015-16,NASSCOM,USNationalBureauofLaborStatistics,UKONS,Selectedothers,HfSAnalystjudgment

Total Impact of Automation on IT/BPO Services Workers by Major Country (likely scenario, mid-high skilled workers)

0.28

0.80

1.11

2.56

0.41

0.94

1.27

2.73

0%

10%

20%

30%

40%

50%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Philippines UK India US

%In

creaseinW

orkforce

ServicesW

orkers(M

illions)

2015 2021 %Change

Researchsources:1477industrystakeholderinterviews2015-16,NASSCOM,USNationalBureauofLaborStatistics,UKONS,Selectedothers,HfSAnalystjudgment

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

©2017HfSResearch,Proprietary

OperatingModelsContinuetoDriveTowardFullGBSPleaseindicatewhichofthefollowingbestdescribesyourorganization'soperatingmodelfordeliveringservicestoday?(Pleaserefertooperatingmodeldiagram)

HfS Research in Conjunction with KPMG, State of Business Operations 2017 N=454 Enterprise Buyers

16% 34% 18% 20% 11%

Decentralizedoperatingmodels

continuetodeclineas

enterprisesshiftrighttowardGBS

©2017HfSResearch,Proprietary

OperatingModel– AllModelsExpecttoGrowExceptDecentralized

Overthenext2yearswillyourcompanyincrease/reduceitsrelianceonthefollowingoperatingmodelsforyourgeneralandadministrativefunctions?(Staythesamenotlabelled)

HfS Research in Conjunction with KPMG, State of Business Operations 2017 N=454 Enterprise Buyers

36% 38% 40% 35% 25%

26% 21% 22% 24%

13%

-7% -7% -4% -7% -16% -2% -3% -1% -1%

-10%

IT Outsourcing Business Process Outsourcing

Shared Services Global Business Services De-centralized processes

Increase moderately Increase significantly Reduce moderately Reduce significantly

25

Document Classification: KPMG Confidential

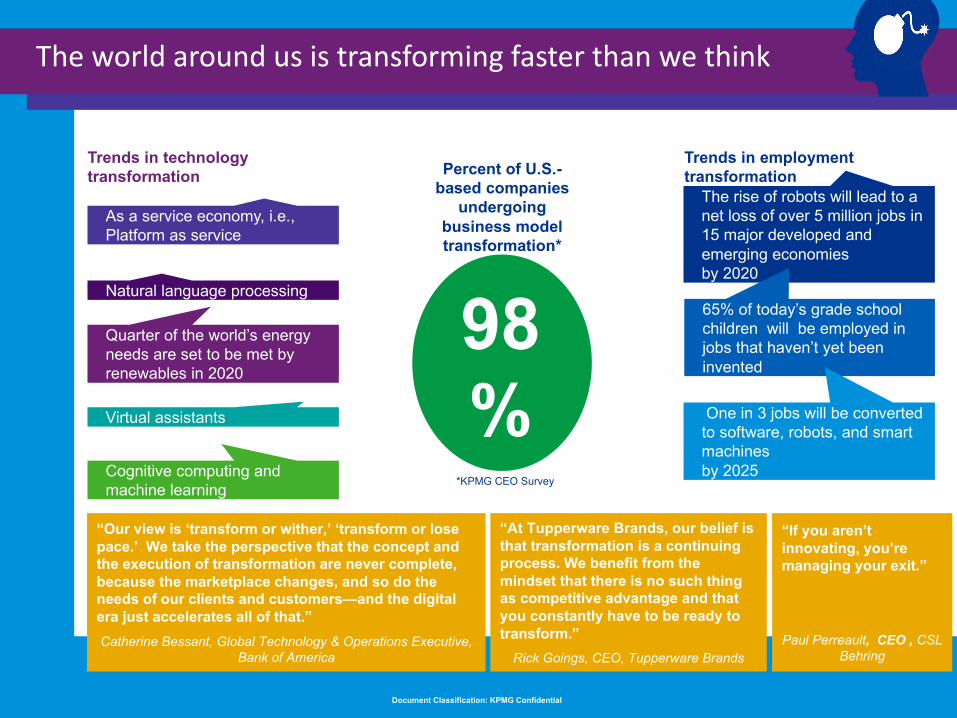

Theworldaroundusistransformingfasterthanwethink

“Our view is ‘transform or wither,’ ‘transform or lose pace.’ We take the perspective that the concept and the execution of transformation are never complete, because the marketplace changes, and so do the needs of our clients and customers—and the digital era just accelerates all of that.”Catherine Bessant, Global Technology & Operations Executive,

Bank of America

“At Tupperware Brands, our belief is that transformation is a continuing process. We benefit from the mindset that there is no such thing as competitive advantage and that you constantly have to be ready to transform.”

Rick Goings, CEO, Tupperware Brands

Percent of U.S.-based companies

undergoing business model transformation*

98%

*KPMG CEO Survey

Trends in employment transformation

The rise of robots will lead to a net loss of over 5 million jobs in 15 major developed and emerging economies by 2020

Trends in technology transformation

As a service economy, i.e., Platform as service

65% of today’s grade school children will be employed in jobs that haven’t yet been invented

One in 3 jobs will be converted to software, robots, and smart machines by 2025

Natural language processing

Quarter of the world’s energy needs are set to be met by renewables in 2020

Virtual assistants

Cognitive computing and machine learning

“If you aren’t innovating, you’re managing your exit.”

Paul Perreault, CEO , CSL Behring

26

Document Classification: KPMG Confidential

AndthesechangesarecausingGBSleaderstorethinktheirstrategy

With robotics we can give center mangers both operational and regional responsibility. This is a general trend to having people wear two or three hats. – Money Center Bank

All of our new people are mainly focused on process and risk. We think of information processing not RTR. Away from product to process. – European Bank

Our transformation journey included linking IT within GBS to support processes whether in or outside of GBS. It is critical to have a cultural link to the organizing the different parts of the delivery organizations wish to serve. – European Pharma

Some of our service locations will not survive the automation process, a major AP location being one. We need to move to locations to provide high value added services as low cost transactional mission diminishes in value. – Money Center Bank

We try to perfect process but don’t know outcomes in most cases – movement away from process optimization to automation .–Global Pharma

GBS optimization is not just about improving SS operations but also changing nature of retained organization and possibly reducing staff there too. – Global Retailer

27

Document Classification: KPMG Confidential

GBSisonthecuspofanothermajorleap…

— Internal delivery of core services; predominantly regional models

— Outsourcing/multiregional outsourcing with select global providers

— Focus on transactional activities

— Emergence of right shoring; near-shore becoming key element of delivery models

— Vendors delivering niche services

— Introduction of multi-vendor deals

— Emergence of COE solutions

— Integrated service delivery models

— Lower value activities typically outsourced; increasing focus on analytical, judgment, and expert services

1990s – Shared services 2000s – Multi-sourcing Since 2010 – Integrated GBS 2020

?

28

Document Classification: KPMG Confidential

…withkeychangedriversloominglargeonthehorizon

Change is accelerating and solutions are converging

—Human-centric process is morphing to human-centric design

—Robotics has disrupted the traditional levers of an optimal service delivery model

—Cloud has hit mainstream and is driving the “as-a-service” revolution

—Big Data riding the “as-a-service” wave available to all corners of the organization

—New value generation and ROI models based on shift from labor to capital

—Social and Mobile have disrupted the buy-sell relationship

—Shifting focus to external customer facing services

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

©2017HfSResearch,Proprietary

ChangingUseofOffshoring– Outsourcing

Howwilloffshoreusechangeinoutsourcingandsharedservicesoverthenext2years?(Netincrease/decrease)

HfS Research in Conjunction with KPMG, State of Industry 2014 N=312 Enterprise Buyers

22% 13%

18% 20% 23%

12% 15% 19% 15%

-4% -3% 5%

12% 16% 7% 3% 3% 6%

2014 Today

Increase

Decrease

©2017HfSResearch,Proprietary

ChangingUseofOffshoring– SharedServices

Howwilloffshoreusechangeinoutsourcingandsharedservicesoverthenext2years?(Netincrease/decrease)

HfS Research in Conjunction with KPMG, State of Industry 2014 N=312 Enterprise Buyers

20% 16% 16%

10% 14% 12% 13% 14%

10% 2%

-1% 5%

11% 6% 4%

-2%

1% 9%

Finance and Accounting

Human Resources

Procurement App maintenance &

dev'ment

IT and Network infra Spt

Customer Service / Sales

Spt

Supply Chain and Logistics

Industry-specific Process

Marketing

2014 Today

Increase

Decrease

©2017HfSResearch,Proprietary

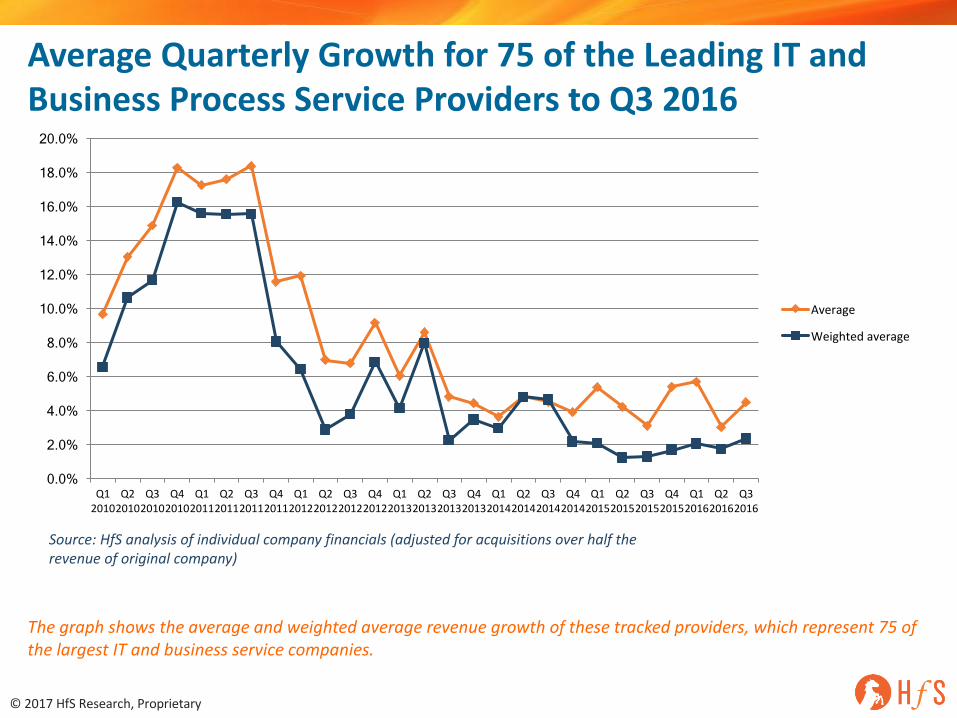

AverageQuarterlyGrowthfor75oftheLeadingITandBusinessProcessServiceProviderstoQ32016

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

Q12016

Q22016

Q32016

Average

Weightedaverage

Source:HfSanalysisofindividualcompanyfinancials(adjustedforacquisitionsoverhalftherevenueoforiginalcompany)

Thegraphshowstheaverageandweightedaveragerevenuegrowthofthesetrackedproviders,whichrepresent75ofthelargestITandbusinessservicecompanies.

©2017HfSResearch,Proprietary

AllOutsourcing- TraditionalvAs-a-Service2015– 2020($b)

59 70 81 92 105 121 136

310 308 306 302 298 295 290

369 378 386 394 404 415 426

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

2014 2015 2016 2017 2018 2019 2020

TraditionalOutsourcing AASOutsourcing

CAGRUSDbillion

-1.2%

14.2%

Source: HfS Research, 2017

Agenda

• ManagingthroughtheDigitalFog

• ApproachingRoboticProcessAutomationin2017

• OperatingModelDynamicsandtheGlobalBusinessServicesEvolution

• OffshoringisDead,Long-liveOffshore?

• WrapUp

©2017HfSResearch,Proprietary

4%

10%

14%

22%

5%

18%

10%

19%

13%

3%

13%

20%

10%

10%

20%

10%

3%

6%

8%

10%

11%

14%

24%

25%

Other(pleasespecify)

Nomorevisaissues

Eliminateratecards

LessPowerPoint

Badqualityteleconferencelines

Lesshypearoundautomation

Clients/servicebuyerstellingtheirstories

Morewomeninleadershiproles

Buyers Advisors ServiceProviders

WhatwouldyouchangeabouttheOutsourcingIndustryifyouhadonewish?Ifyoucouldchangeonecharacteristicofthisindustry,whatwoulditbe?

Source: “Making that leap from effective to strategic BPO/BPM" Study, HfS Research 2016Sample: 343 Industry Stakeholders (Enterprise Buyers = 115, Advisors = 55, Service Providers = 173)

§ Workasateam:Healthedisconnect andunrealismbetweenleadershipambitionandmiddlemanagementoperationalchallenges...Internalandexternal

§ Thinkbig!withanattitudetowrite-offlegacy.Incrementalfixesclearlydonotwork– forallstakeholders.Stopretro-fitting!

§ Becomeastudentagain:Thisisabouthumanscreatingmorecreativevalue,findingmoreproblemsthroughcollaboratingandlearninghowembracetheDigitalandIntelligentAutomationtoolsavailable

§ Thisisnotaboutjobsgoingaway,it’saboutthenatureofworkchanging.Athirdoftoday’sworkforceismadeupofMillenniumsseekingdifferentworkexperiences

§ Tocreateanewexperienceintheindustryandforresults…wemustbebravetobeginwriting-offorlegacyorwe’llneverevolve…

Actions to drag ourselves into the Digital World

HfS ResearchisTheServicesResearchCompany™—theleadinganalystauthorityandglobalcommunityforbusinessoperationsandITservices.Thefirmhelpsorganizationsvalidateandimprovetheirglobaloperationswithworld-classresearch,benchmarkingandpeernetworking. HfSResearchwasnamed"IndependentAnalystFirmoftheYearfor2016"bytheInstituteofIndustryAnalystRelationswhichvotedon170otherleadinganalysts.HfS ChiefAnalyst,PhilFersht,wasnamedAnalystoftheYearin2016forthethirdtime.

HfS coinedtheterms"TheAs-a-ServiceEconomy"and"OneOffice™",whichdescribeHfS Research'svisionforthefutureofglobaloperationsandtheimpactofcognitiveautomationanddigitaltechnologies.HfS' visioniscenteredoncreatingthedigitalcustomerexperienceandanintelligent,singleofficetoenableandsupportit.HfS’ coremissionisabouthelpingclientsachieveanintegratedsupportoperationthathasthedigitalprowesstoenableitsorganizationtomeetcustomerdemand-asandwhenthatdemandhappens.WithspecificpracticeareasfocusedontheDigitizationofbusinessprocessesandDesignThinking,IntelligentAutomationandOutsourcing,HfS analystsapplyindustryknowledgeinhealthcare,lifesciences,retail,manufacturing,energy,utilities,telecommunicationsandfinancialservicestoformarealviewpointofthefutureofbusinessoperations.

Readmoreatwww.hfsresearch.com/about

About HfS Research: The Services Research Company