Embed Size (px)

Citation preview

day and

The Fundraising Series (Part One) –“Building Your Story”“Building Your Story”

April 8, 2014

Featuring:• Niko Bonatsos, General Catalyst Partners• Noah Lichtenstein, Cowboy Ventures• Glenn McCrae, Early Growth Financial Services• Stephanie Palmeri, SoftTech VC

Agenda

8:00 am – 8:05 am

Chad Lynch - Introduction

8:05 am – 8:40 am

Glenn McCrae – Creating Your 3-Year Financial Plan with Q&A

8:45 am – 9:15 am

Noah Lichtenstein – Constructing Your Value Proposition with Q&ANoah Lichtenstein – Constructing Your Value Proposition with Q&A

9:20 am – 9:55 am

Stephanie Palmeri – Understanding Your Competitive Landscape / Market Sizing / Q&A

10:00 am – 10:35 am

Niko Bonatsos – Go-To-Market Strategy / Q&A

Building Your Financials:Creating Your 3-Year Financial Plan

1

Creating Your 3-Year Financial Plan

Glenn McCraePartner and Chief Strategy OfficerEarly Growth Financial Services

About Early Growth Financial Services

• Outsourced financial services firm that provides small to mid-sized companies with an integrated financial solutionsized companies with an integrated financial solution

• 4 platforms of services and support: transactional accounting,CFO, tax, and valuation

• Services include: AP/AR, financial forecasts, cash management,financial statements, monthly close, 409a valuations, corporatetaxes, investor relations, fundraising support

• 300+ successfully funded clients nationwide

• #5 Silicon Valley Business Journal Fastest Growing PrivateCompany Award 2013

2

Building Your Story with Numbers

“The point of financial projections is totell a story with numbers—a story aboutopportunity, resource requirements,market forces, growth, milestoneachievements, and profits.achievements, and profits.

Your job is to create a numericalframework that complements andreinforces the vision you’ve painted withwords.” – Guy Kawasaki

www.earlygrowthfinancialservices.com 3

Presentation OverviewThe essentials of startup financial management

• What are investors looking for in yourfinances?

• What is a financial model?

• Setting financial goals and objectives

• Milestone funding• Milestone funding

• Bottom-up financial projections

• Spend

• Budgeting

• Top-down projections

• Cost assumptions

• Reforecasting

www.earlygrowthfinancialservices.com4

Why a 3-Year Financial Model?A comprehensive financial pictures serves as the road-mapfor your business

• Helps you understand your cash burn

• Forces you to evaluate keyperformance drivers

• Validates your assumptions

Puts challenges into perspective• Puts challenges into perspective

• Iterative process continuouslyimproves your assumptions

• Insight into your business model

• Clarifies decision-making process(short-term and long-term)

• Gives you leverage of accuratebaseline valuation

www.earlygrowthfinancialservices.com5

What Goes Into a 3-Year Financial Model?Essential components to your model

Majorobjectives

MilestonesTimeline

www.earlygrowthfinancialservices.com3

Keyassumptions

Trendinganalysis

Key variables

Identify Major Objectives for YourCompanyAssess where you are and what you want to achieve

Venture funding andnegative cash burn

Positive cash burn andno venture funding

www.earlygrowthfinancialservices.com

What do you want to accomplishwith next raise?

What are the goals you want to achieveduring this time period?

Process for Creating Your Financial ModelHow to approach the process and get buy-in

1. Go to stakeholders and members ofexecutive team – what do they need toachieve objectives (revenue, product,market, strategic, etc.)?

2. What is needed from a2. What is needed from aprogrammatic perspective?

3. Compile information and discusswith CEO (maybe executive team):

total amount requested relative tomilestone

4. Dialogue about wants and tradeoffs

5. Use dialogue to create bottom-upforecasting budget

www.earlygrowthfinancialservices.com8

Bottom-Up Financial ProjectionForecast for realistic revenue potential

www.earlygrowthfinancialservices.com9

Spend for Bottom-Up ProjectionsConsider relevant operational costs

• Customer/Cost details

• Human resource costs

• Consultant and professional services• Consultant and professional services

• Research and development

• Office and admin

• Sales and marketing

• Capital spending

www.earlygrowthfinancialservices.com10

BudgetingUse your budget to plan your actions

• Budgeting created on accrual basis: budgetingversus actual results

• Difference between cash and accrual isaround capital expenditures

• Report budget by department and major costdrivers (expense categories and revenue

www.earlygrowthfinancialservices.com11

drivers (expense categories and revenuecategories)

• Plan actions: how quickly will this impactrevenue and what will you be able to achievebased on spending

• Identify key variables• Identify key revenue assumptions• Run different scenarios

Budgeting ExerciseStart from a milestone perspective

• If company has been around fora while, look at historical costs

• What do you need toaccomplish before you run outaccomplish before you run outof money, or in a specific timeperiod

• Ask budget owners what theyneed to accomplish goals

• Tradeoffs

• Trending analysis

• Trending initiative

www.earlygrowthfinancialservices.com12

Top-Down Projection?Not particularly useful, but necessary for investors to showmarket potential

www.earlygrowthfinancialservices.com13

ReforecastingYour financial plan is always evolving

• Don’t do a 5-year plan, atmost 3-year

• Update your budget on aquarterly basis (at least)quarterly basis (at least)

• For investors budget on aquarterly basis for first yearand then annually

• What’s realistic in terms oftimeline and reforecastingon monthly or quarterlybasis?

www.earlygrowthfinancialservices.com14

Thank You and Q&A

Glenn McCrae

415.320.5753

www.earlygrowthfinancialservices.com15

www.earlygrowthfinancialservices.com

Follow us @EarlyGrowthFS

Value Proposition

Noah Lichtenstein Partner, Cowboy Ventures

April 8, 2014

At a Glance: Cowboy Ventures • Founded in late 2012, $40m seed stage fund • 2 partners, 6 ninjas, focus on community • Our mission: to back the most beloved new

consumer + enterprise companies at seed stage – companies re-imagining “Life 2.0”

Confiden'al -‐ Cowboy Ventures 2014 2

The “Re-Imagination of Everything” Life 2.0, via Web/Mobile

New Content & Commerce

Mobile-first Consumer

New Connected Devices

Consumerization of Enterprise

16 investments to date*

New Gaming

*does not include some of our Stealth and “non-anchor” investments

Cowboy Ventures Current Portfolio

Confiden'al -‐ Cowboy Ventures 2014 3

Brief Bio: Noah Lichtenstein

• Partner, Cowboy Ventures (2013-present) • Founding Team, HomeRun (2009-2012)

– Acquired by Rearden Commerce (Sept. 2011) – Raised from Foundation, First Round, Founder

Collective, Angels • Business Development, Climate Corp

(2008-2010) – Acquired by Monsanto (MON) for ~$1bn (Oct. 2013) – Raised from Index, NEA, Khosla, GV, First Round, etc.

• Other: – Board of Directors, United Way – Advisor, Life360 – Stanford University (B.A. 2004)

Confiden'al -‐ Cowboy Ventures 2014

@Noah_L [email protected]

4

What We’ll Cover Today

1. Company Value Proposition 2. Investor Value Proposition

Confiden'al -‐ Cowboy Ventures 2014 5

What We’ll Cover Today

1. Company Value Proposition 2. Investor Value Proposition

Confiden'al -‐ Cowboy Ventures 2014 6

Company Value Prop – What is it?

Purpose of the Value Proposition: To help inform the customer so that he or she can make a choice.

Confiden'al -‐ Cowboy Ventures 2014 7

Value Proposition is… A positioning statement that explains WHAT benefit you provide for WHO and HOW you do it uniquely well.

--Michael Skok, North Bridge Venture Partners

Value Proposition is not… A mission statement or company vision

Confiden'al -‐ Cowboy Ventures 2014

Company Value Prop – What is it?

8

Value Prop – Examples

Uber provides on-demand personal transportation through a simple mobile application that enables users* to request, ride, and pay for transportation at the push of a single button. Unlike with taxis, Uber passengers get reliable pickups, clear pricing, and convenient cashless transactions.

*Because Uber is a marketplace, there is a distinct value proposition for Drivers

Confiden'al -‐ Cowboy Ventures 2014 9

Value Prop – Examples

Dropbox enables users to store and access their photos, docs, and videos anywhere and share them easily. Unlike local storage solutions, it does this by storing digital copies of these files in the Cloud, and automatically synchronizing them across a user’s multiple devices.

Confiden'al -‐ Cowboy Ventures 2014 10

Company Value Prop – The What

The What • What is the specific problem you are solving? • Do consumers view this as a problem?

• How big is the problem?

Confiden'al -‐ Cowboy Ventures 2014 11

Company Value Prop – The Who

The Who • Who will benefit from your product or service? • Why do they care?

• How many are there?

Confiden'al -‐ Cowboy Ventures 2014 12

Company Value Prop – The How

The How • What is your unique solution to the problem • What are other existing solutions to the problem? • Why is this better than existing alternatives?

Confiden'al -‐ Cowboy Ventures 2014 13

Quick Recap: Company Value Prop

Confiden'al -‐ Cowboy Ventures 2014

The Company Value Proposition is… The What, Who and How of your company that helps inform the customer so that he or she can make a choice.

14

1. Company Value Proposition 2. Investor Value Proposition

Confiden'al -‐ Cowboy Ventures 2014 15

What We’ll Cover Today

Investors: A bit of Background

• What keeps investors up at night? • Needles in a (growing) haystack • It’s not personal • There is no right investor; there is only the right

investor for you

Confiden'al -‐ Cowboy Ventures 2014 16

What do Investors Care About?

The Four Things Investors Care Most About: • Team • Market • Plan • Traction (or some proof you can rock it)

Confiden'al -‐ Cowboy Ventures 2014 17

What do Investors Care About?

The Team • Team make-up • Relevant skills + background • Unfair advantage • The intangibles

Confiden'al -‐ Cowboy Ventures 2014 18

What do Investors Care About?

The Market • Think big – market size >$1bn • Addressable vs. total market size • Growing market • Comparable exits + strong multipliers

Confiden'al -‐ Cowboy Ventures 2014 19

What do Investors Care About?

The Plan • Product roadmap • Metrics and milestones • Financials / projections • Hiring plan

Confiden'al -‐ Cowboy Ventures 2014 20

What do Investors Care About?

Traction (or some proof you can rock it) • Traction • Other “proof”

Confiden'al -‐ Cowboy Ventures 2014 21

Meeting with Investors

What to do and expect… • Before • During • After

Confiden'al -‐ Cowboy Ventures 2014 22

Meeting with Investors

Before • Do your homework • Reaching investors • Arranging a time

Confiden'al -‐ Cowboy Ventures 2014 23

Meeting with Investors

During • The goal of the first meeting à get a second meeting • Start strong • Show > tell • Know and mention potential competitors • Concrete next steps

Confiden'al -‐ Cowboy Ventures 2014 24

Meeting with Investors

After • Send a follow-up note thanking them and

summarizing any next steps or action items • The investor’s process

Confiden'al -‐ Cowboy Ventures 2014 25

Other Thoughts

• Is VC right for you? • Every investor meeting is an opportunity to get

better

Confiden'al -‐ Cowboy Ventures 2014 26

Common Mistakes

• Settling for a cold intro • Asking an investor to sign an NDA

• Thinking too small / not selling the dream • Discussing exits in an early stage pitch • Focusing too much on valuation in the early stage • Not knowing the VC’s investment thesis • Making the investor do all the work • Game-playing • Huge spikes in revenue from year to year

Confiden'al -‐ Cowboy Ventures 2014 27

Some Things I Love

• Be data driven – If you have data already, speak to what it is telling you – If you don’t have data, speak to what data is important and

what metrics you will be tracking • CAC, WoW growth, churn, DAUs/MAUs, etc.

• Run tests – Run a limited test to see if data will help you prove a

hypothesis or help demonstrate product-market fit

• Product roadmap – A well thought-out roadmap for building and executing on

product development

Confiden'al -‐ Cowboy Ventures 2014 28

Closing Thoughts

• A strong company value proposition is a pre-requisite for seeking investment

• Team, Market, Plan, and Traction (or some proof you can rock it) are the four most important things to investors when evaluating an opportunity

Confiden'al -‐ Cowboy Ventures 2014 29

THANK YOU

Questions?

Confiden'al -‐ Cowboy Ventures 2014 30

MARKET SIZING& COMPETITIVE LANDSCAPE& COMPETITIVE LANDSCAPE

Steph Palmeri, SoftTech VC / @stephpalmeri

TOTAL ACCESS Fundraising Series, Part I

April 8, 2014

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

Our Three Asses RuleThis

Presentation’sFocus

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistributeproprietary &confidential

blackbox.vc

Big-Ass Market

* “Big enough” stress test

– Greater than $1B market opportunity

– Company, not feature

– How does your startup get to $100M in revenue?

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– How does your startup get to $100M in revenue?• 10% of $1B market v. 50% of $200M (unrealistic!)

* By raising capital, you commit to match returnexpectations

Market Types

ExistingMarket

ResegmentedMarket

NewMarket

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

better, faster,cheaper

fundamentalshifts, niche

brave newworld

which one is you?

Market Analysis 101

* Problem definition:– What are the underlying needs you solve?

* Identify your customers– What do they look like?– How are you helping them?

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– How are you helping them?– Are your users also your buyers? (who pays?!)

* Addressable Market = # Customers * LTV– What is the relevant market?– Your expected share? (be reasonable, its not 100%!!)– Growth / overall market potential?

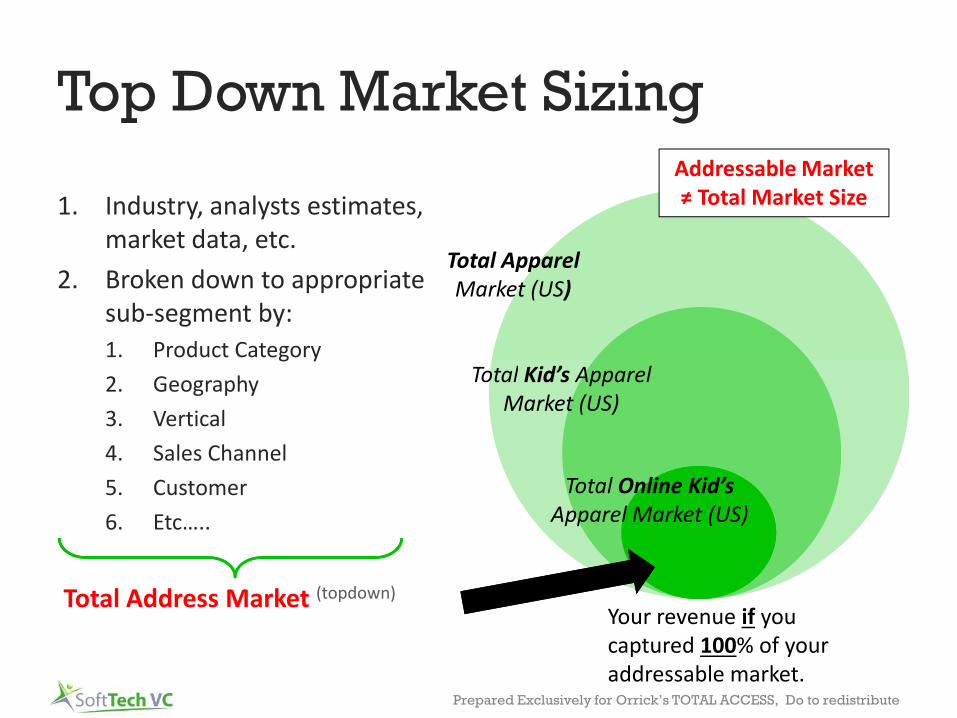

Top Down Market Sizing

1. Industry, analysts estimates,market data, etc.

2. Broken down to appropriatesub-segment by:

1. Product Category

Addressable Market≠ Total Market Size

Total ApparelMarket (US)

Total Kid’s Apparel

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

1. Product Category

2. Geography

3. Vertical

4. Sales Channel

5. Customer

6. Etc…..

Total Address Market (topdown)

Your revenue if youcaptured 100% of youraddressable market.

Total Kid’s ApparelMarket (US)

Total Online Kid’sApparel Market (US)

Bottom Up Approach

Identify & multiply the following:

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

# of potential customers x est. revenue per user per year

Total Addressable Market(bottom up)

Now Compare

Top DownAddressable

Market

Bottom UpAddressable

Market

V.

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

Market Market

…. are they reasonably close?

Market Sizing Tips

* Existing: Known customer + understood need– Know entities make it ‘easier’, for you and investors

– Understand market nuances, don’t be careless

* New markets: New customer + new use case

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

* New markets: New customer + new use case– Emerging macro trends

– Adoption rate assumptions

– Timing matters

creativity + basic algebra + educated guesses

= bullshit but shows us how you think about your space

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistributeproprietary &confidential

blackbox.vc

Market Attractiveness

Size matters…

(but don’t overlook)

* Competition

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

* Competition

* Monetization potential

* Market Growth

* Market Share

* Timing

Competitive landscape

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

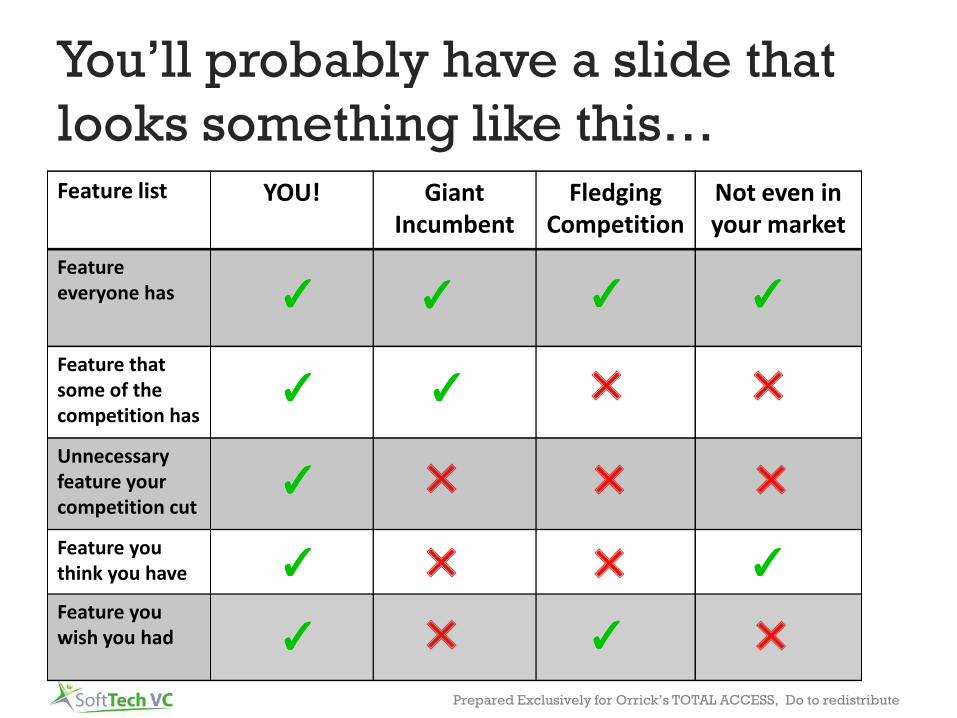

You’ll probably have a slide thatlooks something like this…Feature list YOU! Giant

IncumbentFledging

CompetitionNot even inyour market

Featureeveryone has

Feature that

✓✓ ✓✓ ✓✓ ✓✓

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

Feature thatsome of thecompetition has

Unnecessaryfeature yourcompetition cut

Feature youthink you have

Feature youwish you had

✓✓

✓✓

✓✓

✓✓ ✓✓

✓✓

✓✓

… or this...Fast

Your LogoHere!

Others

Others

Others

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistributeproprietary &confidential

blackbox.vc

Slow

Traditional ModernOthers

Others

Others

Others

Others

Others

… or more recently this...

AdjacentMarket Segment

AdjacentMarket Segment

AdjacentMarket Segment

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

YourLogoHere

AdjacentMarket Segment

AdjacentMarket Segment

but regardless…

explain your startup in the context

of the environment in which you

operate including those who you

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

operate including those who you

partner with and those who you

compete against and those

who keep you awake at night

proprietary &confidential

blackbox.vc

overview

* Competitive Landscape

– Examine the macro business environment

– Review your competition (past, present, future)

– Benchmark yourself

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– Benchmark yourself

* Competitive analysis

– The classic SWOT analysis

* Competitive advantage

Classic completive analysis

* Examine the macro business environment– Economic + political trends– Cultural + social shifts– Technological innovation– Regulations + legislation

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– Regulations + legislation

* Know the industry ecosystem surrounding your startup– Competitors (direct, indirect, potential entrants)– Suppliers/Partners– Substitutes– Customers

Pop Quiz

Q: Is your industry one or more of the following:

a. Considered crowded?

b. Fairly complex?

c. Scary to investors?

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

c. Scary to investors?

A: Consider making an

ecosystem slide

Show investorshow much youknow (and they

don’t) about yourspace… OWN IT!

Competitive analysis

* Comparisons you might put in a competitive grid:

– Products / feature set

– Customers

– Market share

You Them

Feature #1

Feature #2

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– Distribution strategy

– Technology

– Pricing

– Resources are they well funded?

Feature #2

Feature #3

Wow, your startuptakes all the boxeson your arbitrary

grid!

SWOT Analysis –Your Competitive Position

Strengths: why you kick ass- Team- Technology- Scalability- Execution- Customer acquisition & retention

Weaknesses: why you don’t kick ass- Team- Lack of Technology- Scalability issues- Inability to execute- Unreliable product/service

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

- Customer acquisition & retention- Distribution

Opportunities: why you might kick ass- Early mover- Emerging segments- New technology- New distribution channel- Changing tastes- Etc.

- Unreliable product/service- Poor distribution

Threats: why you might not kick ass- Competitors w/ more $- Emerging segments- New technology- New distribution channel- Changing tastes- Etc.

Competitive advantage

* Barriers to entry

* Create a long-term sustainable advantage

– Continuous learning & innovation

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

– Continuous learning & innovation

– Excellence and speed in execution

* Don’t obsess about others

– A little competition is healthy

– Keep an eye on competition but don’t loose focus onwhat’s really important … the customer

VC’s perspectiveWhat VC’s MeanWhat VC’s Say

Who will you compete withtomorrow?

When does Facebook plan to dothis?

How are you different from the 15other dating services I this week?

Who do you compete withtoday?

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

tomorrow?

[Insert name here] just raised$50M from these 10 firms, howare you differentiated?

this?

Your competition has deeppockets…will anyone be willing to fundyour next round?

How to reach Steph Palmeri:

w: www.softtechvc.com

b: www.stephpalmeri.com

t: @stephpalmeri

Prepared Exclusively for Orrick’s TOTAL ACCESS, Do to redistribute

Niko Bonatsos

@bonatsos General Catalyst Partners

@bonatsos General Catalyst Partners

You always face competition◦ It gets worse over time.

◦ Copying is the best form of flattery.

Why will your company break out?

What is your real advantage? What is your real advantage?◦ Is it a technology advantage?

◦ Unique insights about the market?

◦ Timing re: seizing regulatory changes?

◦ Unique growth model?

@bonatsos

@bonatsos

@bonatsos

$20 billion

@bonatsos

@bonatsos

@bonatsos

@bonatsos

@bonatsos

@bonatsos General Catalyst Partners

@bonatsos

@bonatsos

Seek for FREE PR

◦ Techcrunch et al need to report on something

◦ Recruiting

◦ Fundraising

◦ Early Adopters

Facebook Mobile Ads, New channels (e.g. Snapchat) Facebook Mobile Ads, New channels (e.g. Snapchat)

◦ “Golden Time” -> Cheap

NEVER pay for users/customers early on

◦ Spend that $$ improving your product/dating life

@bonatsos

Invest in growth and strategic value◦ Revenue and profit$ will follow in time (we hope)

◦ Leverage your strengths

Don’t focus on breaking even◦ Diminish profits and slow growth◦ Diminish profits and slow growth

Set personal goals (be realistic)◦ Funding requirements

◦ Exit expectations

◦ Time horizon

◦ Social life

@bonatsos

Iterate all the time

Every business is different

Great product is “table-stakes” today

Advisors & experts vs. customers & market

Startup = Growth (Paul Graham) Startup = Growth (Paul Graham)

@bonatsos

@bonatsos General Catalyst Partners