Embed Size (px)

Citation preview

Consumer Credit:

Life after FCA Authorisation

Prem Griffith

Managing Consultant at Bovill

September 2016

Greg Stevens

CEO of CCTA

Richard Ellison

Partner at Shakespeare Martineau

Prem Griffith

Managing Consultant at Bovill

3

FCA and consumer credit - what’s next?

FCA’s supervision model

When thing’s go wrong – FCA’s approach and powers

Anticipated future rule changes and areas of regulatory focus

What should you be doing?

4

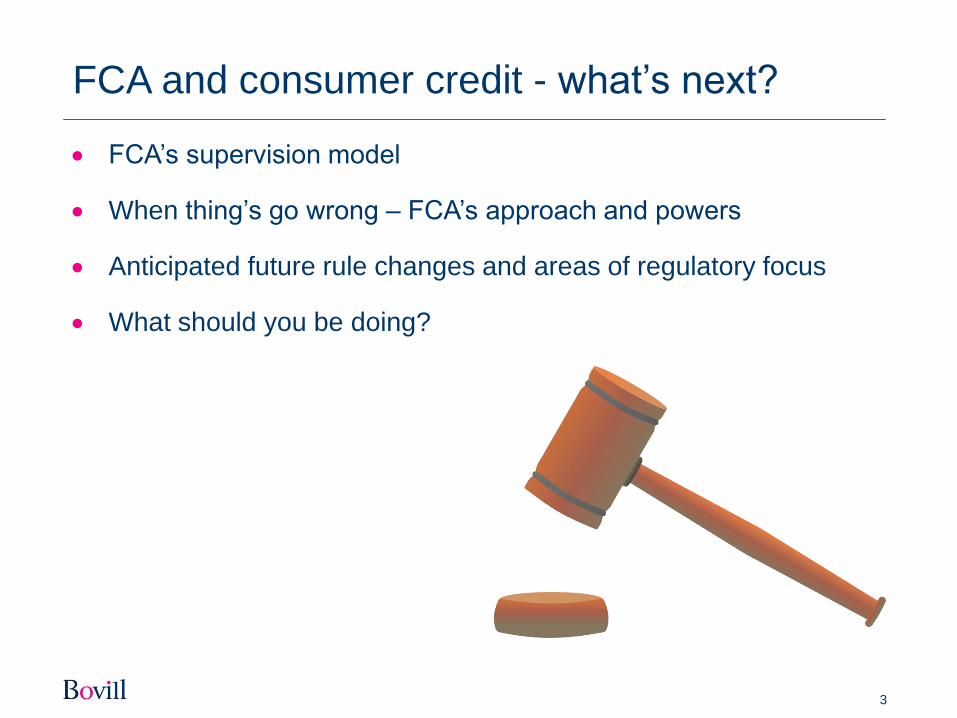

FCA threshold conditions (reminder)

LEGAL STATUS

LOCATION OF OFFICES

EFFECTIVE SUPERVISION

APPROPRIATE RESOURCE

SUITABILITY

BUSINESS MODEL

Authorised firms must meet the threshold conditions at all times

5

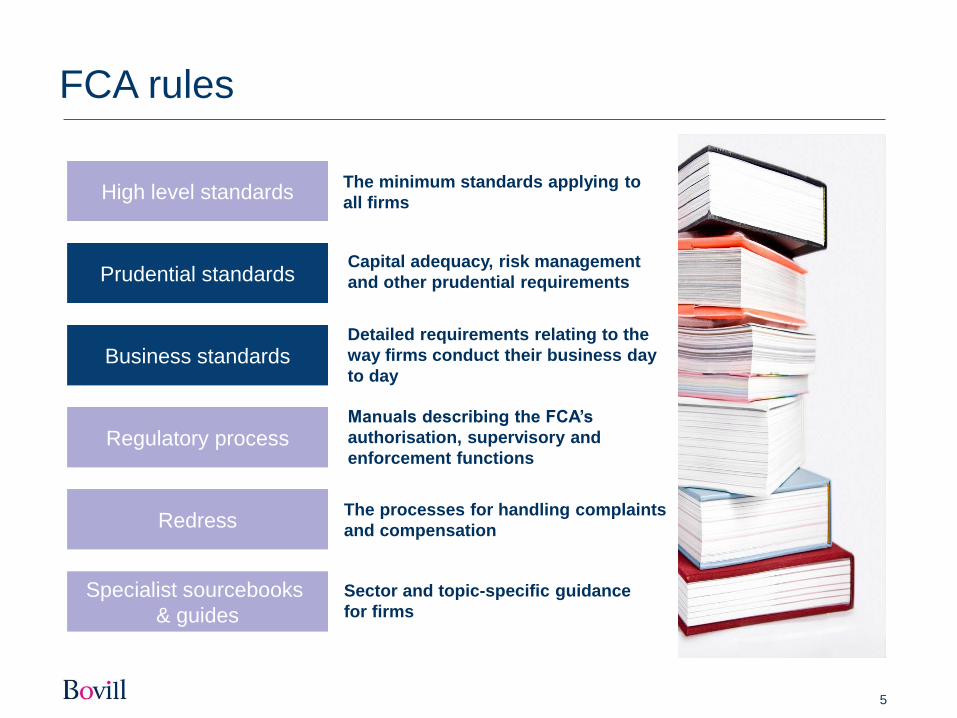

FCA rules

High level standards

Prudential standards

Business standards

Regulatory process

Redress

Specialist sourcebooks

& guides

The minimum standards applying to

all firms

Capital adequacy, risk management

and other prudential requirements

Detailed requirements relating to the

way firms conduct their business day

to day

Manuals describing the FCA’s

authorisation, supervisory and

enforcement functions

The processes for handling complaints

and compensation

Sector and topic-specific guidance

for firms

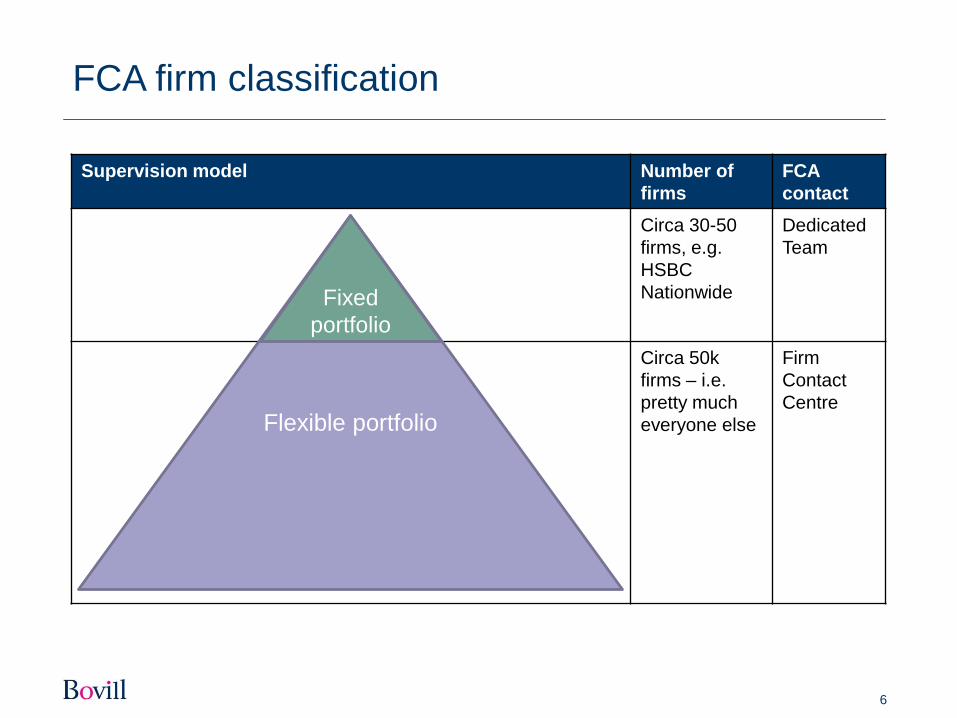

Supervision model Number of

firms

FCA

contact

Circa 30-50

firms, e.g.

HSBC

Nationwide

Dedicated

Team

Circa 50k

firms – i.e.

pretty much

everyone else

Firm

Contact

Centre

6

FCA firm classification

Flexible portfolio

Fixed

portfolio

7

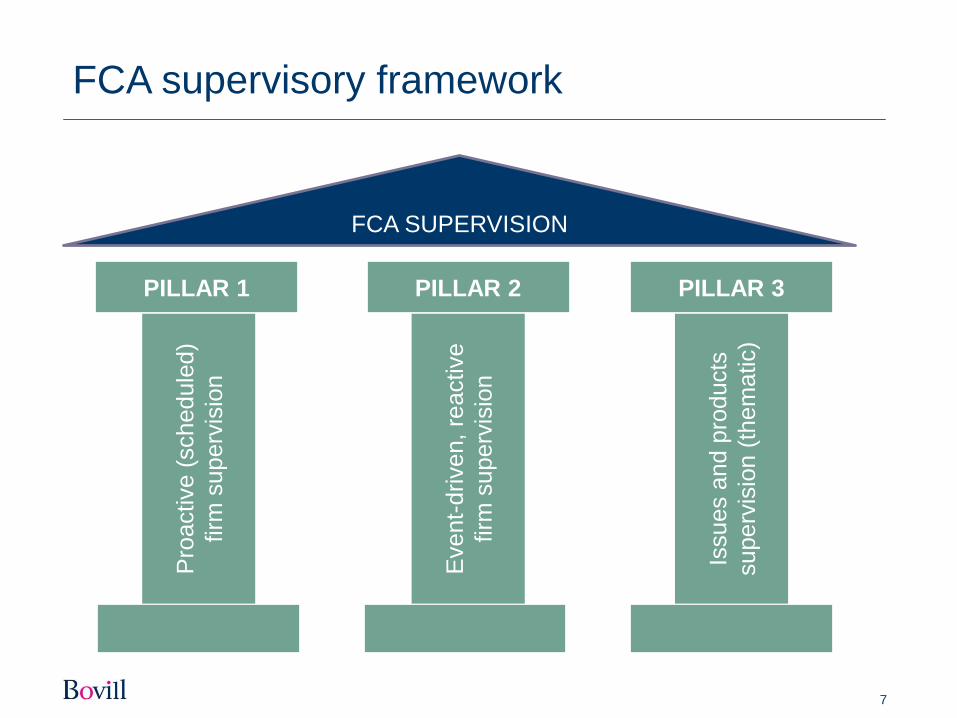

FCA supervisory framework

PILLAR 1 PILLAR 2 PILLAR 3

Pro

active (

schedule

d)

firm

superv

isio

n

Issues a

nd p

roducts

superv

isio

n (

them

atic)

Event-

driven,

reactive

firm

superv

isio

n

FCA SUPERVISION

8

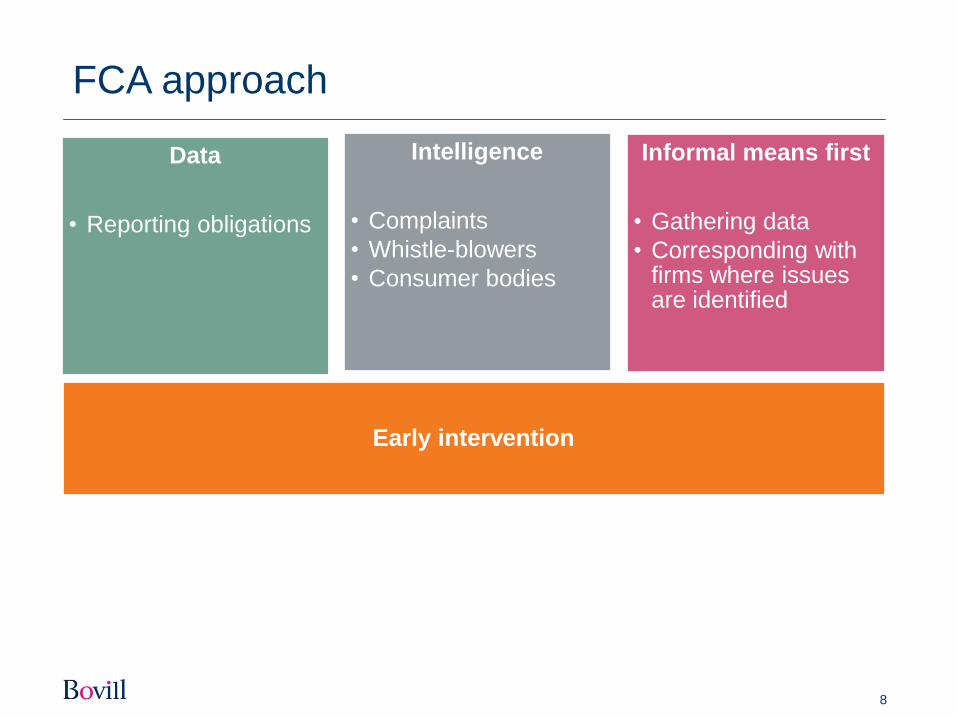

FCA approach

Data

• Reporting obligations

Intelligence

• Complaints

• Whistle-blowers

• Consumer bodies

Informal means first

• Gathering data

• Corresponding with firms where issues are identified

Early intervention

9

Supervisory / enforcement tools

Use of attestations

Increases personal accountability

Skilled Person (s166) reviews

Enforcement powers

Private warning

Restrictions on business

Withdraw (firm) authorisation

Public censure

Suspension (individual)

Prohibition (individual)

Prosecute (individual)

…and of course hefty fines

10

Recent examples of supervisory intervention

11

Areas of regulatory focus

Responsible lending: affordability and creditworthiness

Arrears and forbearance

Staff incentives / remuneration

Vulnerable customers

Culture

Poor treatment of existing customers

12

Future rule changes

Review of high-cost short-term credit price cap

Retained provisions in the CCA 1974 moved to CONC

Senior Manager Regime extended to all firms in 2018-19

13

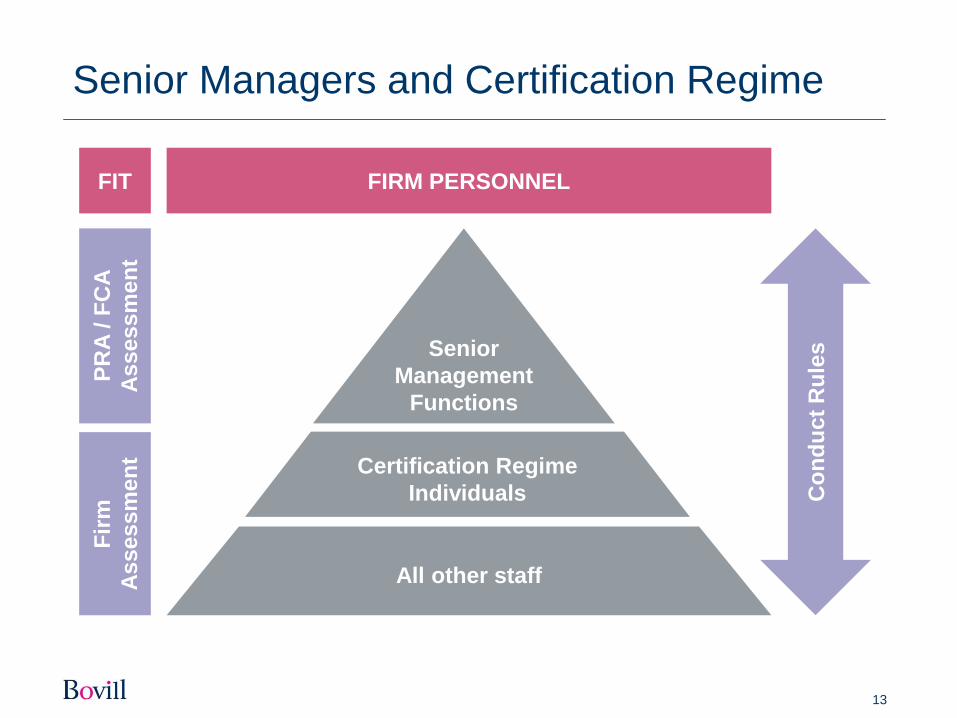

Senior Managers and Certification Regime

Senior

Management

Functions

Certification Regime

Individuals

All other staff

FIRM PERSONNELFIT

PR

A /

FC

A

As

se

ss

me

nt

Fir

m

As

se

ss

me

nt

Co

nd

uc

t R

ule

s

14

What you should be doing….

Embedding

Establish your compliance framework

Make sure your Board has the right MI and attitude

Identify relevant regulatory developments

Make sure your processes consider compliance e.g. new product

development

Day to day compliance

Financial reporting and non financial reporting

FCA notifications

Applications – variations of permission, approved persons etc.

Testing state of compliance

Regular compliance monitoring to identify issues early

Check policies and procedures to ensure they are fit for purpose

Test employees to ensure they have the right knowledge

Of course, Bovill can help…

Consumer Credit:

Life after FCA authorisation

Richard Ellison

Shakespeare Martineau LLP

• Life post interim permission

• The future of the Consumer Credit Act

• The CCA Call for Input

• The Senior Managers & Certification Regime

Richard Ellison: Shakespeare Martineau LLP

• Areas of FCA concern

• How are the FCA coping?

• Interim permission is only the start

• What can authorised firms expect?

Life post interim permission

• Brief overview to date

• CONC: 82 down, 167 to go

• The additional 26 sets of Regulations

The future of the CCA: Where have we come from?

• Very limited CONC guidance on the CCA

• 167 plus 26: fit for purpose?

• Practical, sensible and deliverable regulation

• The Call for Input

The future of the CCA: Where are we now?

• The Call for Input closed on 18 May

• 1 April 2019 deadline for HM Treasury report

• Prioritising particular CCA provisions for review/early

review

• How best to engage with stakeholders

The future of the CCA: What happens next?

• Who will conduct the review?

• Mix of in-house resource and expert Stakeholder

Consultative Group

• Timetable: update on progress by Q4 2016

The future of the CCA: What happens next?

• Balancing act: the appropriate degree of protection for

consumers

• Balancing act: avoid imposing disproportionate

burdens on regulated firms

• Balancing act: the greater flexibility and coherence of

CONC as opposed to statute and regulations?

The future of the CCA: What happens next?

• Mixed response to 2013 consultation

• At least one FCA interim report/further consultation to

come

• Impact of European Consumer Credit Directive

The future of the CCA: What happens next?

• More CONC guidance (but Guidance on enforcing

CCA security)

• Ongoing European Directive compliance

• Consumer protection

• Unfair contract terms guidance

The future of the CCA: What happens next?

Senior managers & certification regime

• No more Approved Persons and Controlled Functions

• Already in place for PRA regulated firms

• Focus on individual’s responsibilities for roles they

perform; accountability for their roles; and firms

certifying fitness and propriety

• Timetable for all FSMA authorised persons: during 2018

presented by

DWF Legal Update

Stronger TogetherGoing Forward

Greg Stevens

Chief Executive

presented by

END OF AN ERA?

• Soundbite Politics

• Knee jerk reactions

• Onerous regulation

• Lack of dialogue and collaboration

Stronger Together – Going Forward

presented by

• Angry World

• Secular Groups

• Connectivity

• ‘Want it now’ sentiment

• Millenials

CHANGING PATTERNS

Stronger Together – Going Forward

presented by

CLOSER TO HOME

• Working patterns

• Jobs for life

• Meaningful occupations

• New order

• Bubble mentality

Stronger Together – Going Forward

presented by

WHAT DOES IT MEAN FOR CONSUMER CREDIT?

• Major reliance on consumer spending

• Throw away society

• Style is a moving feast

• Housing market

• Opportunities

Stronger Together – Going Forward

presented by

POLITICAL OVERVIEW

• Where are we now?

• Where are we going?

• Why does it matter?

• What are we going to do?

Stronger Together – Going Forward

presented by

CCTA ACTION PLAN

• Future of Trade Associations

• Public Affairs agenda

• Policy Committees

• Project Centurion

Stronger Together – Going Forward

presented by

STRONGER TOGETHER - GOING FORWARD

• National Conference 2/3 November

• CCTA 125th Anniversary Year

• Fighting your corner

• Book early to avoid disappointment

Stronger Together – Going Forward

35

Questions?