Embed Size (px)

Citation preview

Does your workplace outsourcing create value beyond savings?A point of view on the future of real estate and facilities management

Contents

Executive summary 4

Thought leadership 5

Introduction 6

Chapter I: Recent developments in the REFM outsourcing market 8

Chapter II: Addressing the REFM outsourcing market challenges 10

Trends are born when challenges are resolved 10

Leading practice Nordic REFM outsourcing market 11

Chapter III: What is the future of the REFM outsourcing market? 16

Getting the sourcing model strategy right 16

Vested™: a model for designing the next-generation REFM deals 18

Chapter IV: Conclusions on the future of the REFM outsourcing market 20

EY’s Nordic REFM Team 23

3

4 | Real estate and facilities management

Executive summary

Historically, the approach to drive REFM outsourcing has been quite consistent across industries and organizations. “The classic approach” with competitive sourcing, transactional business models and transactional contracts has been the most widespread. However, if you look at the most common pitfalls, there are many inherent flaws in this approach. It is our experience that yesterday’s best practices will not equal tomorrow’s next great innovations within value-enabling REFM.

At EY, we believe that the classic way to conduct REFM business is still useful when a company wants to buy commoditized services at the lowest cost. However, if your objective is to create strategic results and generate value beyond savings and transformation, the classic approach falls short.

Your choice of business model is fundamental to achieving your strategic objectives. Similarly, your choice of sourcing business model strategy is integral to orchestrating the system that will enable you to achieve strategic objectives. Last but not least, the rules you choose to follow in the relationship with your business partners are crucial for joint success.

In this report, we have combined EY’s insights as a leading provider of REFM advisory services with viewpoints from workplace executives and opinion leaders in outsourcing. We aim to describe current challenges in the REFM market, the most evident future trends and — last but not least − how to respond to the upcoming changes. In other words, our themeis just as logical as it is exciting.

Magnus KuchlerLeader of REFM Advisory Services at EY in the Nordic Region

A strategic and well-orchestrated operating model for real estate and facilities management (REFM) can add value to a company’s overarching strategy. An increasing number of organizations understand how buildings and workplaces contribute to profits, but different approaches to REFM and workplace management result in different outcomes.

5Real estate and facilities management |

Thought leadership

EY is a leading provider of REFM Advisory Services, ranked number one globally by the International Association for Outsourcing Professionals (IAOP) in 2015.

In this report, we share observations and conclusions from the wide range of REFM projects we have been involved in across industries and countries. We have also asked leading REFM executives and outsourcing opinion leaders to share their take on current challenges, future trends, and their impact on strategic partnerships and business models. Their input has greatly enhanced this report, and we would like to express warm thanks to all for their invaluable contribution.

Participating executivesPeter Ankerstjerne, Head of Group Marketing, ISSSebastian Beronius, Global Account Director, CBRE Global Workplace SolutionsDavid Frydlinger, Partner, Lindahl law firmGuy Holden, EMEA President of Enterprise Accounts, CBRE Global Workplace SolutionsFredrik Justesen, Project Manager Global REFM, EricssonJuha Olkinoura, Vice President of Workplace Resources, NokiaXavier Marmasse, Global Sourcing Lead, CBRE Global Workplace SolutionsAnnika Martinson, Director Strategy & Operational Development, Volvo Cars GroupTimothy McParlane, Jones Lang Lasalle, COO, Procter & Gamble AccountJakob Moltsen, Former Head of Facilities Management, Sony Mobile CommunicationsAzita Shariati, CEO Sweden & Denmark, SodexoDavid Susoreny, Senior Managing Director & Regional Lead, Cushman & Wakefield Jesper Svensson, Vice President & Head of Workplace Solutions, Sony Mobile CommunicationsAnders Thorvik, Facility Management Specialist, StatoilKate Vitasek, Founder of Vested OutsourcingUlf Wretskog, CEO Sweden, Coor Service ManagementJörgen Zetterström, Vice President Global Indirect Sourcing, Sony Mobile Communications Magnus Åkerberg, Managing Director Integrated Facilities Management EMEA, Jones Lang Lasalle Inc.

EY’s Head of FM Roundtable

EY invites more than 150 facilities management (FM) leaders in the Nordics to join exclusive annual roundtable events. The events are a discussion forum where FM leaders can exchange experiences and discuss strategic priorities and operational improvements with peers.

EY’s REFM Benchmarking Programs

EY runs four different REFM Benchmarking Programs in the Nordic region. In 2015, these programs benchmarked REFM services in46 hospitals, 29 corporations, 17 counties and 9 municipalities.

Business knowledge

EY has performed over 300 REFM engagements, building extensive business knowledge. EY is also ranked as the top outsourcing advisor by the IAOP. https://www.iaop.org/Content/19/165/4149

Surveys, books and reports

EY has authored several reports based on in-depth surveys over the last years, including How can Nordicorganizations better leverage outsourcing opportunities? in 2009 and EY’s Real Estate & Facilities Management Nordic Survey 2013.

6 | Real estate and facilities management

Introduction

The REFM market as we know it is changing. The business is growing fast and, with ongoing consolidation of REFM companies, the focus on total cost of occupancy brings REFM management closer to the boardroom. More and more companies also expect their REFM operating model to deliver on both top and bottom lines. Consequently, leading companies see workplace management as a strategic concern for the executive team.

REFM executives are also increasingly being seen as strategic business partners, focusing on creating as much value as possible rather than a tactical and operational support function. In line with this, there is a growing trend to ensure that REFM business is based on facts and analytics. Governing through oversight is no longer enough – in today’s market, stakeholders must work together to harness as much insight as possible in order to harvest new value pools.

However, we have discovered that the REFM outsourcing market is confronting some very obvious challenges:

• Suppliers are not the proactive and innovative integrators that many wish for.• Buyer-demand organizations are often neither skilled nor organized optimally.• Both parties experience opportunistic behavior in their relations.• Last but not least, REFM deals do not drive strategic business transformation.

In other words, many REFM deals and relations in the current market neither satisfy the buyers nor the suppliers. Neither is procurement satisfied despite the fact that, in many cases, the total cost has dropped by up to 50% over just a few years while maintaining end-user satisfaction.

7Real estate and facilities management |

“ A current trend is to globalize and, sometimes, not to centralize. We are leveling up from executive sponsorship

to executive ownership.”

Magnus Åkerberg, Managing Director, Integrated Facilities Management EMEA, Jones Lang Lasalle Inc.

8 | Real estate and facilities management

Recent developments in the REFM outsourcing market

During the last 10 years, the REFM outsourcing industry has been reinventing itself. It is a market with fierce competition, relatively low supplier margins and huge differences in business maturity − even between neighboring countries. While the REFM operating models have delivered greatly on the bottom line all over the world, they have been, and to some extent still are, considered a necessary cost and a completely operative task.

The development of the “scope of services” has also evolved significantly as suppliers have become better at delivering. More suppliers are now focused on widening their service portfolios so as not to miss out in tendering processes. Most have started delivering single services and then moved into multiservice deliveries. Further along the line, some suppliers started to provide bundled services, with a few delivering integrated FM on an international scale. As a reaction to the increased amount of services, new ways of procuring them were born, such as buying on function-based rather than instruction-based service descriptions.

REFM professionals believe that REFM functions are becoming more intertwined. On the one hand, on the supplier side, Corporate Real Estate (CRE) and FM companies are merging: for example, CBRE and Johnson Controls Global Workplace Solutions, and Cushman & Wakefield and DTZ. On the other hand, on the buyer side, many demand organizations are now forming first-generation workplace concepts and strategies where RE and FM are joining forces.

This means that deal volumes increase significantly, putting a lot of pressure on suppliers to act much more as integrators. An integrator is responsible for performing services rather than delivering services that is delivering results in collaboration with all buyer stakeholders as well as other suppliers.

Despite the sheer volume of workplace deals and daily contact with employees, most REFM demand organizations still strive to reach the right strategic focus in their companies.

Most companies struggle to reach the appropriate strategic focus, and there are very few CXOs that can exemplify the contribution to top-line growth from an REFM perspective. Again, mature companies also tend to have quite interesting and productive dialogues with their CXOs.

In our interviews, we investigated the supplier side’s ability to enable top-line growth with the REFM operating model.

Chapter I

“ The global FM market has been attracting a lot more interest from investors, analysts and new market entrants for different reasons. Firstly, because the market is huge. Secondly, because it is relatively young and immature. Thirdly, because there are lots of opportunities.”

Peter Ankerstjerne, Head of Group Marketing, ISS

9Real estate and facilities management |

We asked Guy Holden, EMEA President of Enterprise Accounts at CBRE Global Workplace Solutions: Do you see deals where the REFM results connect with top-line growth of companies?

Absolutely – ideally, the starting point for any outsourcing deal should be the long-termbusiness strategy of the organization. To achieve maximum value from outsourcing,companies need to understand why they own or occupy buildings in the first place. In mostcases, their core business is not real estate (RE) or FM. They need facilities that allow themto focus on the activities that drive performance and business growth.

The retail business is a good example: there are specific components within those facilities that directly affect our clients’ bottom line. Chillers or pumps have an impact on revenue if they break down; if the environment is dirty, customers won’t return to buy the goods or services again. Understanding how your portfolio contributes to your top-line growth is key. Once you understand this, you can then measure it and hold your suppliers accountable for performance. This is the way FM outsourcing can provide strategic value and contribute to business growth.

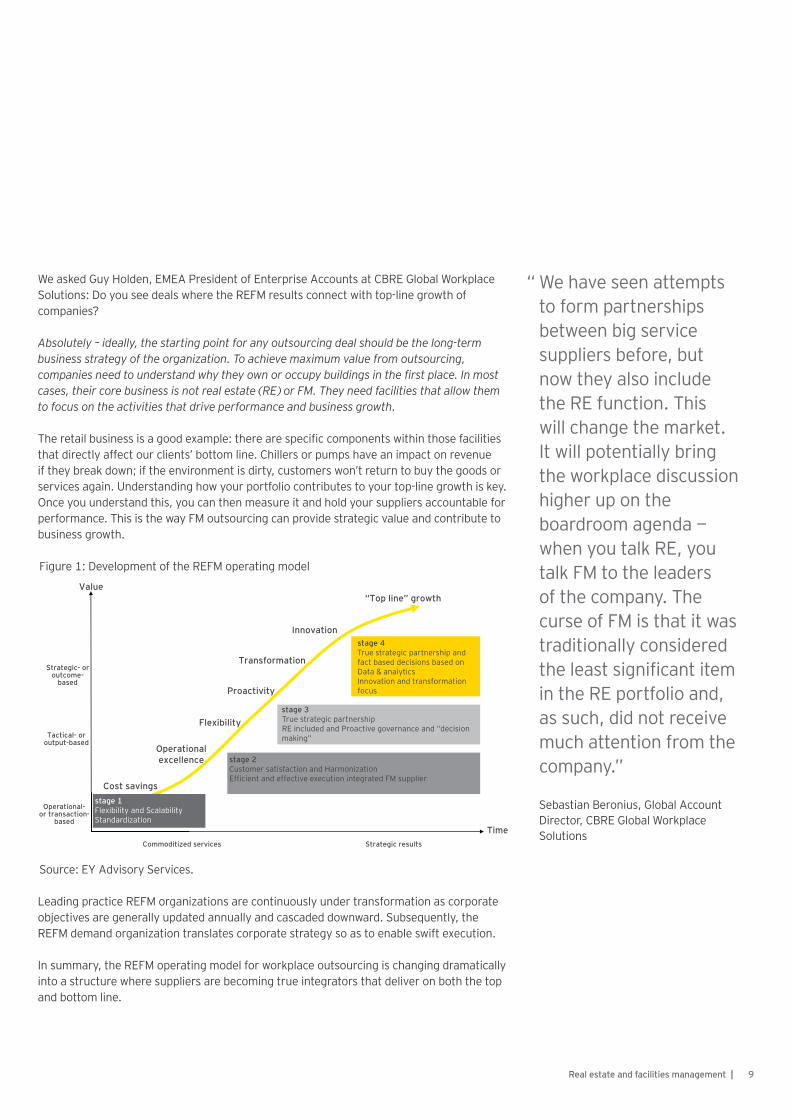

Figure 1: Development of the REFM operating model

Source: EY Advisory Services.

Leading practice REFM organizations are continuously under transformation as corporate objectives are generally updated annually and cascaded downward. Subsequently, the REFM demand organization translates corporate strategy so as to enable swift execution.

In summary, the REFM operating model for workplace outsourcing is changing dramatically into a structure where suppliers are becoming true integrators that deliver on both the top and bottom line.

“ We have seen attempts to form partnerships between big service suppliers before, but now they also include the RE function. This will change the market. It will potentially bring the workplace discussion higher up on the boardroom agenda − when you talk RE, you talk FM to the leaders of the company. The curse of FM is that it was traditionally considered the least significant item in the RE portfolio and, as such, did not receive much attention from the company.”

Sebastian Beronius, Global Account Director, CBRE Global Workplace Solutions

Value

Time

stage 3True strategic partnershipRE included and Proactive governance and “decision making”

stage 2Customer satisfaction and Harmonization Efficient and effective execution integrated FM supplier

stage 1Flexibility and ScalabilityStandardization

Strategic- or outcome-

based

Operational-or transaction-

based

Tactical- or output-based

Commoditized services Strategic results

stage 4True strategic partnership and fact based decisions based on Data & analytics Innovation and transformation focus

Cost savings

Proactivity

Flexibility

Transformation

Innovation

“Top line” growth

Operational excellence

10 | Real estate and facilities management

Addressing the REFM outsourcing market challenges

Trends are born when challenges are resolvedIn a volatile global marketplace, it is important that workplace delivery is flexible and can contribute with real value by adapting to the ever-changing needs of the business, i.e., scaling up and down as well as closing and opening new sites effectively and efficiently. In order to support transformation and to be in the forefront of workplace development, focus on innovation is crucial.

Mechanics must therefore be in place to support and incentivize innovation, which needs to be a joint priority for the supplier and the buyer. Currently, there is a movement away from traditional transactional contracts with power and zero-sum game-based negotiations to more partnership-oriented models based on trust and win-win ideology aiming for strategic value. Moreover, the focus is shifting toward more strategic and company-wide benefits such as proactivity, flexibility, innovation and contribution to corporate transformation.

We asked Jesper Svensson, Vice President & Head of Workplace Solutions, Sony Mobile Communications: what are the most evident trends in the global workplace market?

1. Focusing on the workplace in its entirety rather than FM or RE is a trend. The workplace is more at the core of the business, and we are wondering how to support it as a business partner. Focusing on how to enhance and support ways of working and productivity in the companies.

2. Connectivity and mobility, technology are components enabling the drive of productivity and efficiency. Not only people, but also machines and buildings. Digital transformation. From the REFM market perspective, digitalization of the business and data analytics will heavily impact the business and the way to operate.

3. Talents from a multifunctional perspective in a globalized world. How and what kind of new people skills we need impacts upon where we are located and how we are working. Most companies are too locked in past legacy instead of looking into the future. We are not optimally utilizing resources as shifting locations to find right people with right skills et cetera.

We asked Guy Holden, EMEA President of Enterprise Accounts at CBRE Global Workplace Solutions: How do you see commercial models shifting in the market?

Old service models were often based on a cost-plus model, which doesn’t fit the way most organizations want to operate today. Now, we see more performance-based commercial models. If we deliver strong results, we create a better world for our clients and get compensated accordingly. It is a win-win situation: everyone benefits from good performance and the relationship is based on mutual success. This tends to lead tolong-term partnerships.

EY Advisory Services has a global presence and is witnessing a shift in both the private and the public REFM outsourcing market. REFM Advisory Services is particularly strong in the Nordic market where we facilitate REFM Benchmarking Programs beyond our strategic REFM transformation engagements.

Chapter II

“ Conventional transaction-based approaches have inherent flaws because the economics of the deal structure keeps buyers and suppliers at arm’s length. This approach is not conducive to collaboration, innovation or sharing value, especially for complex, multi- dimensional business relationships.”

Kate Vitasek, Founder of Vested Outsourcing

11Real estate and facilities management |

Leading practice Nordic REFM outsourcing market The Nordic REFM market is divided between the more mature private sector, where several buyer-supplier relationships are on their third or fourth generation workplace deals, and the public sector in which many players still prefer an in-house delivery model, increasingly outsourcing single services, and where only very few have outsourced bundled or integrated contracts for REFM services.

However, our estimate is that there is an increased rate of outsourced service deliveries among private and public sector players, with an annual growth rate of approximately 2%−3% in addition to the already vast Nordic REFM market that has an annual turnover of around US$47 billion, made up of both in-house and outsourced workplace operating models.

Our studies show that there are two main aspects that drive Nordic companies to look for new ways of organizing their REFM strategy and operational model. Firstly, the Nordic business culture and mindset strives for long-term solutions, focusing on results rather than on how they are achieved. Secondly, the region has a natural partnership culture to draw from and business relationships are generally based on a high level of mutual trust, which is a result of relatively low corruption levels in the Nordic countries.

Secondly, mature private sector companies on their third or fourth generation workplace deal have managed to reduce costs greatly, but are yet not happy with what they receive in terms of innovation and proactivity. It is only natural that mature private sector companies look for alternative business models that better support their needs, as reflected clearly in participant feedback in EY’s REFM Benchmarking Programs.

In order to build long-lasting partnerships, buyers, suppliers and procurement will gradually have to revolutionize the way in which they organize the REFM contribution in the company. In order to respond to these new requirements, companies and suppliers must rethink how they create value.

The REFM markets development is characterized by three principal trends1. Mindset shift from focus on cost to focus on valueValue is a matter of definition, and value constitutes different things in different settings depending on what you want to achieve from a deal. What we see is a shift in the definition of value, interlinked with the desired outcomes. It has become a strategic choice to pursue either traditional competitive sourcing focused on cost reduction, or more partnership-based sourcing focused on other values.

When the corporate strategic agenda changes, the REFM agenda must change too. In addition, it should support the corporate transformation agenda, enabling efficient and effective changes where the workplace is concerned. This is not a one-off, large-scale transformation effort, but rather a continuous challenge for the workplace organization to respond to external and internal pressures. The workplace is increasingly being recognized as an important part of the business, not only in terms of business continuity and smooth running, but also as a lever for competitive advantage and a way of building company culture.

12 | Real estate and facilities management

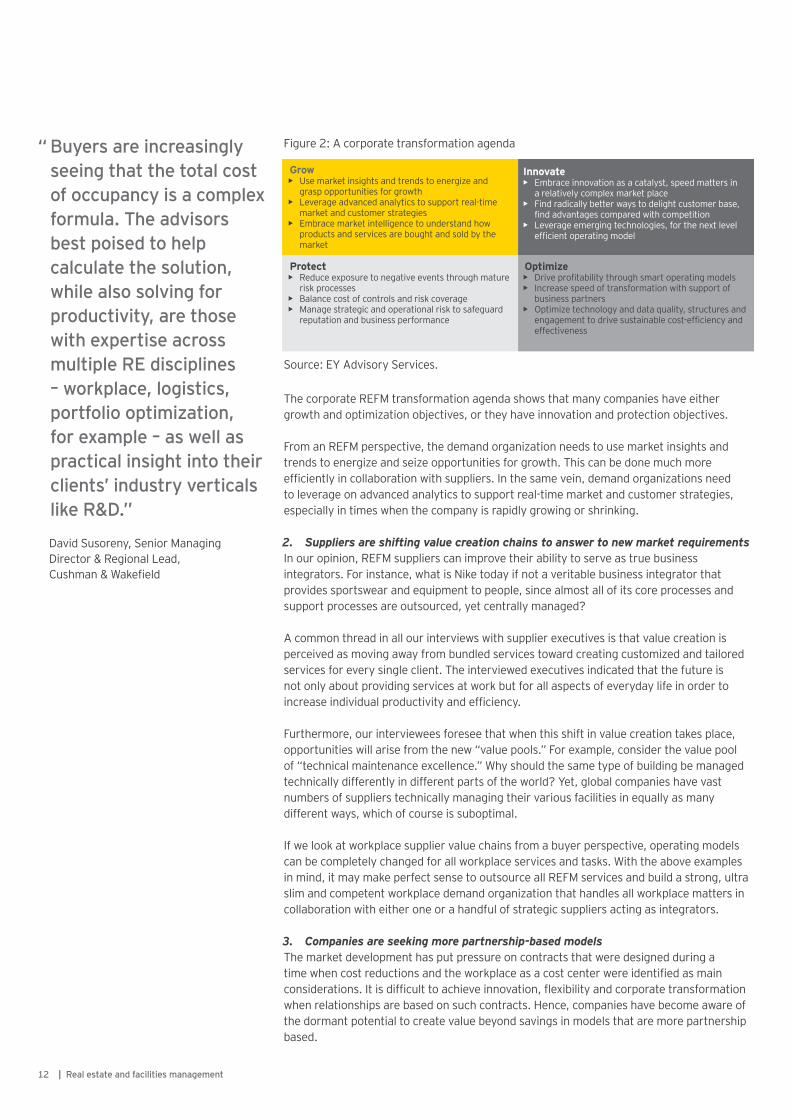

Figure 2: A corporate transformation agenda

The corporate REFM transformation agenda shows that many companies have either growth and optimization objectives, or they have innovation and protection objectives.

From an REFM perspective, the demand organization needs to use market insights and trends to energize and seize opportunities for growth. This can be done much more efficiently in collaboration with suppliers. In the same vein, demand organizations need to leverage on advanced analytics to support real-time market and customer strategies, especially in times when the company is rapidly growing or shrinking.

2. Suppliers are shifting value creation chains to answer to new market requirementsIn our opinion, REFM suppliers can improve their ability to serve as true business integrators. For instance, what is Nike today if not a veritable business integrator that provides sportswear and equipment to people, since almost all of its core processes and support processes are outsourced, yet centrally managed?

A common thread in all our interviews with supplier executives is that value creation is perceived as moving away from bundled services toward creating customized and tailored services for every single client. The interviewed executives indicated that the future is not only about providing services at work but for all aspects of everyday life in order to increase individual productivity and efficiency.

Furthermore, our interviewees foresee that when this shift in value creation takes place, opportunities will arise from the new “value pools.” For example, consider the value pool of “technical maintenance excellence.” Why should the same type of building be managed technically differently in different parts of the world? Yet, global companies have vast numbers of suppliers technically managing their various facilities in equally as many different ways, which of course is suboptimal.

If we look at workplace supplier value chains from a buyer perspective, operating models can be completely changed for all workplace services and tasks. With the above examples in mind, it may make perfect sense to outsource all REFM services and build a strong, ultra slim and competent workplace demand organization that handles all workplace matters in collaboration with either one or a handful of strategic suppliers acting as integrators.

3. Companies are seeking more partnership-based modelsThe market development has put pressure on contracts that were designed during a time when cost reductions and the workplace as a cost center were identified as main considerations. It is difficult to achieve innovation, flexibility and corporate transformation when relationships are based on such contracts. Hence, companies have become aware of the dormant potential to create value beyond savings in models that are more partnership based.

“ Buyers are increasingly seeing that the total cost of occupancy is a complex formula. The advisors best poised to help calculate the solution, while also solving for productivity, are those with expertise across multiple RE disciplines – workplace, logistics, portfolio optimization, for example – as well as practical insight into their clients’ industry verticals like R&D.”

David Susoreny, Senior Managing Director & Regional Lead, Cushman & Wakefield

Source: EY Advisory Services.

Grow• Use market insights and trends to energize and

grasp opportunities for growth• Leverage advanced analytics to support real-time

market and customer strategies• Embrace market intelligence to understand how

products and services are bought and sold by the market

Innovate• Embrace innovation as a catalyst, speed matters in

a relatively complex market place• Find radically better ways to delight customer base,

find advantages compared with competition• Leverage emerging technologies, for the next level

efficient operating model

Protect• Reduce exposure to negative events through mature

risk processes• Balance cost of controls and risk coverage• Manage strategic and operational risk to safeguard

reputation and business performance

Optimize• Drive profitability through smart operating models• Increase speed of transformation with support of

business partners• Optimize technology and data quality, structures and

engagement to drive sustainable cost-efficiency and effectiveness

13Real estate and facilities management |

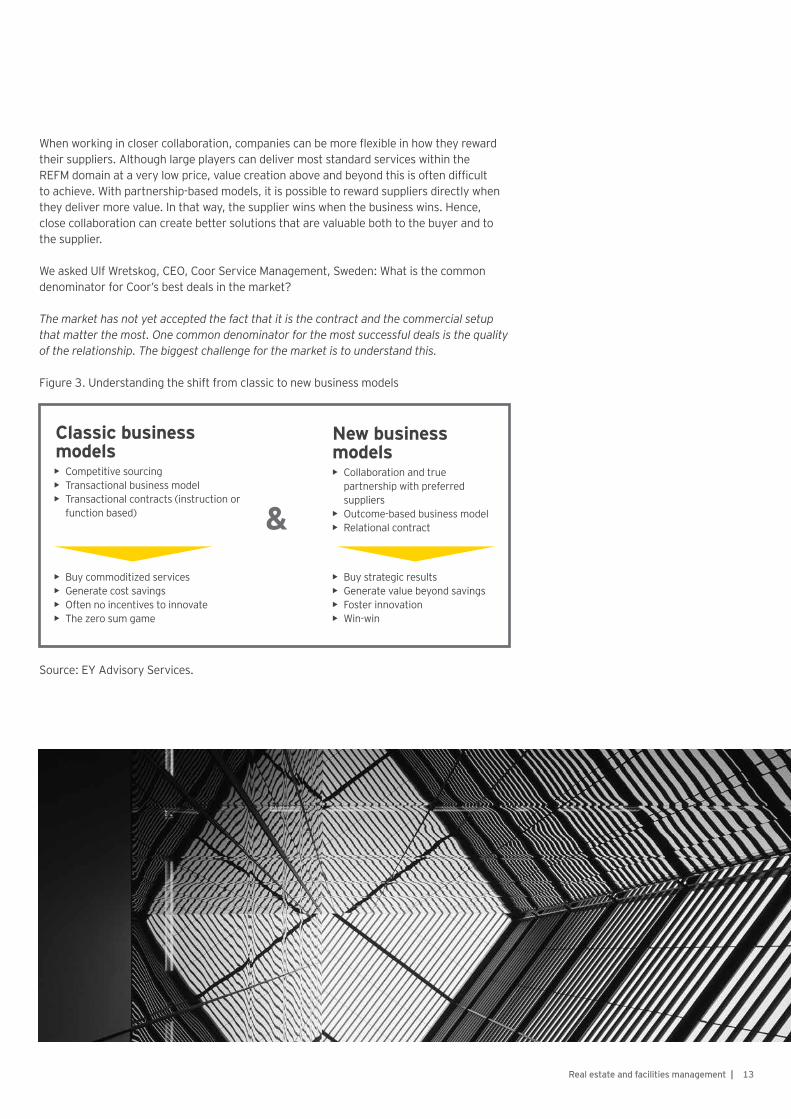

When working in closer collaboration, companies can be more flexible in how they reward their suppliers. Although large players can deliver most standard services within the REFM domain at a very low price, value creation above and beyond this is often difficult to achieve. With partnership-based models, it is possible to reward suppliers directly when they deliver more value. In that way, the supplier wins when the business wins. Hence, close collaboration can create better solutions that are valuable both to the buyer and to the supplier.

We asked Ulf Wretskog, CEO, Coor Service Management, Sweden: What is the common denominator for Coor’s best deals in the market?

The market has not yet accepted the fact that it is the contract and the commercial setup that matter the most. One common denominator for the most successful deals is the quality of the relationship. The biggest challenge for the market is to understand this.

Figure 3. Understanding the shift from classic to new business models

Source: EY Advisory Services.

Classic business models• Competitive sourcing• Transactional business model• Transactional contracts (instruction or

function based)

New business models• Collaboration and true

partnership with preferred suppliers

• Outcome-based business model• Relational contract

• Buy commoditized services• Generate cost savings • Often no incentives to innovate• The zero sum game

• Buy strategic results • Generate value beyond savings• Foster innovation• Win-win

&

14 | Real estate and facilities management

15Real estate and facilities management |

In what way do you see the focus on driving innovation within REFM changing?

“ Earlier, the suppliers did not offer and the buyers did not request

innovation, it was purely a negotiation of costs.

Now this is changing.”

Annika Martinson, Director Strategy & Operational Development, Volvo Cars Group

16 | Real estate and facilities management

What is the future of the REFM outsourcing market?

We know that fundamental change is required to be successful in the market, to overcome the challenges, to be proactive and innovative and to enable constant transformation. Proactivity, flexibility and innovation are values that the marketplace requires from REFM operating models.

“The more strategic and complex the deals that need to be designed, the more relational the contracts must be. Only relational contracts can enable the collaboration needed to achieve mutual strategic outcomes.” David Frydlinger, Partner, Lindahl Lawfirm

Simply put, to prepare for business, one must understand which sourcing business model to use.

Getting the sourcing model strategy rightIn our view, both transactional and outcome-based business models will continue to be used in future. However, we predict that a growing number of deals will be strategic partnerships by nature.

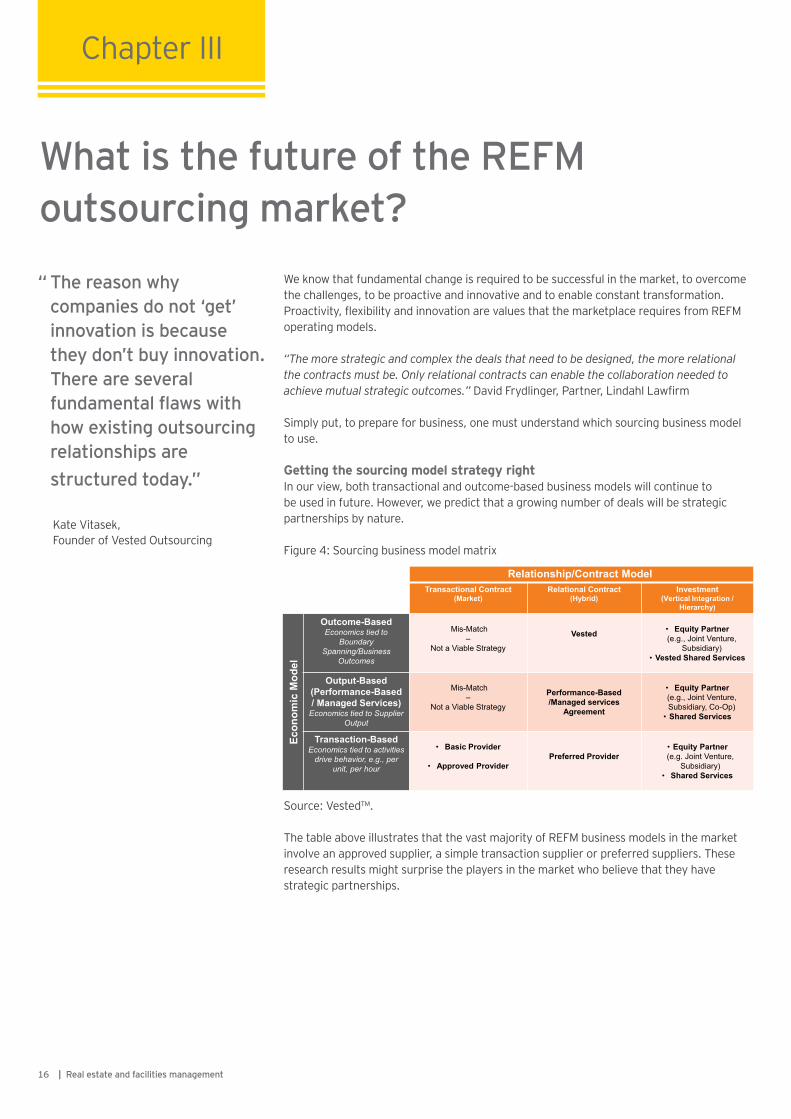

Figure 4: Sourcing business model matrix

Source: Vested™.

The table above illustrates that the vast majority of REFM business models in the market involve an approved supplier, a simple transaction supplier or preferred suppliers. These research results might surprise the players in the market who believe that they have strategic partnerships.

Chapter III

“ The reason why companies do not ‘get’ innovation is because they don’t buy innovation.

There are several fundamental flaws with how existing outsourcing relationships are structured today.”

Kate Vitasek, Founder of Vested Outsourcing

Relationship/Contract ModelTransactional Contract

(Market)Relational Contract

(Hybrid)Investment

(Vertical Integration / Hierarchy)

Econ

omic

Mod

el

Outcome-BasedEconomics tied to

Boundary Spanning/Business

Outcomes

Mis-Match–

Not a Viable Strategy

Vested • Equity Partner (e.g., Joint Venture,

Subsidiary)• Vested Shared Services

Output-Based(Performance-Based / Managed Services)

Economics tied to Supplier Output

Mis-Match–

Not a Viable Strategy

Performance-Based /Managed services

Agreement

• Equity Partner (e.g., Joint Venture, Subsidiary, Co-Op)

• Shared Services

Transaction-BasedEconomics tied to activities

drive behavior, e.g., per unit, per hour

• Basic Provider

• Approved ProviderPreferred Provider

• Equity Partner(e.g. Joint Venture,

Subsidiary)• Shared Services

17Real estate and facilities management |

In reality, most companies actually have a transactional business model and contract that they call a strategic partnership. Many adhere to a preferred supplier model combined with a transactional contract. Moreover, some companies have a performance-based business model where the suppliers are rewarded based on performance. More often than not, they are combined with a transactional contract, which we no longer consider to be a viable option.

The more value beyond savings you want to achieve, the more you will tend to move upward on the vertical axis. In addition to moving upward, you also need to move to the right in the matrix, i.e., choose a relational contract instead of a transactional contract.

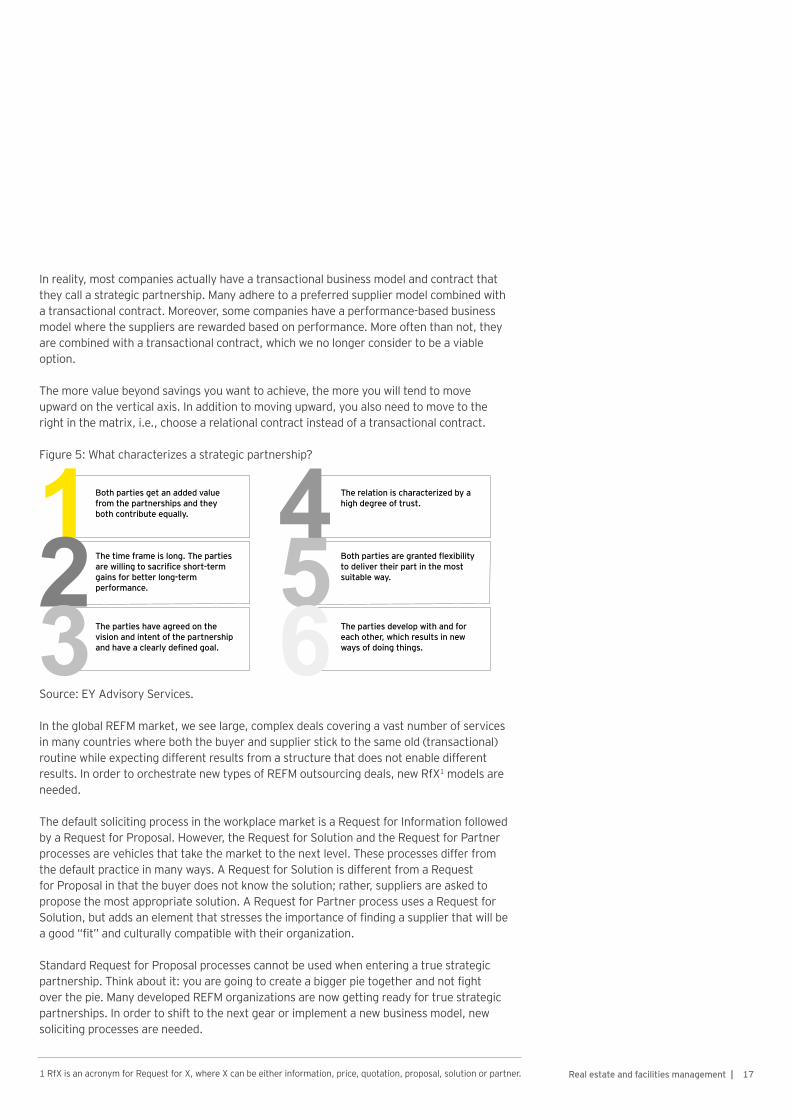

Figure 5: What characterizes a strategic partnership?

Source: EY Advisory Services.

In the global REFM market, we see large, complex deals covering a vast number of services in many countries where both the buyer and supplier stick to the same old (transactional) routine while expecting different results from a structure that does not enable different results. In order to orchestrate new types of REFM outsourcing deals, new RfX1 models are needed.

The default soliciting process in the workplace market is a Request for Information followed by a Request for Proposal. However, the Request for Solution and the Request for Partner processes are vehicles that take the market to the next level. These processes differ from the default practice in many ways. A Request for Solution is different from a Request for Proposal in that the buyer does not know the solution; rather, suppliers are asked to propose the most appropriate solution. A Request for Partner process uses a Request for Solution, but adds an element that stresses the importance of finding a supplier that will be a good “fit” and culturally compatible with their organization.

Standard Request for Proposal processes cannot be used when entering a true strategic partnership. Think about it: you are going to create a bigger pie together and not fight over the pie. Many developed REFM organizations are now getting ready for true strategic partnerships. In order to shift to the next gear or implement a new business model, new soliciting processes are needed.

123

456

Both parties get an added value from the partnerships and they both contribute equally.

The time frame is long. The parties are willing to sacrifice short-term gains for better long-term performance.

The parties have agreed on the vision and intent of the partnership and have a clearly defined goal.

The relation is characterized by a high degree of trust.

Both parties are granted flexibility to deliver their part in the most suitable way.

The parties develop with and for each other, which results in new ways of doing things.

1 RfX is an acronym for Request for X, where X can be either information, price, quotation, proposal, solution or partner.

18 | Real estate and facilities management

True partnerships that enable a win-win situation do exist, but they are rare. The obvious question is: How do these contracts work and how are they created?

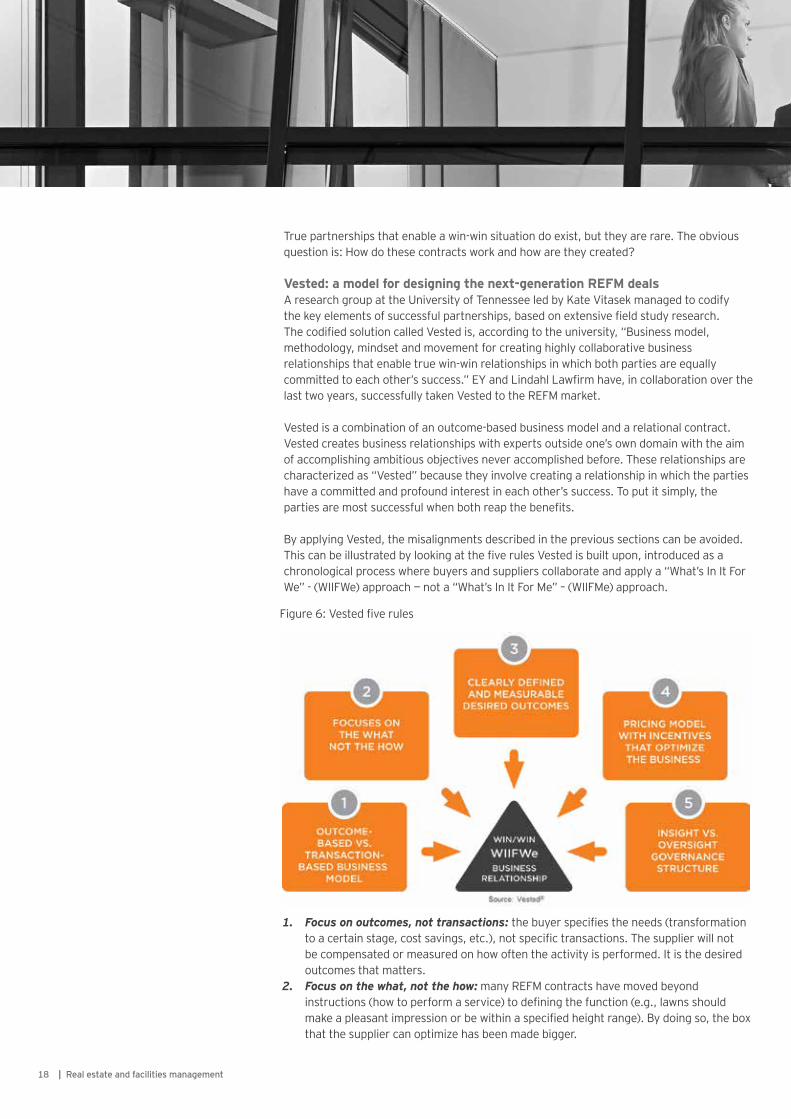

Vested: a model for designing the next-generation REFM dealsA research group at the University of Tennessee led by Kate Vitasek managed to codify the key elements of successful partnerships, based on extensive field study research. The codified solution called Vested is, according to the university, “Business model, methodology, mindset and movement for creating highly collaborative business relationships that enable true win-win relationships in which both parties are equally committed to each other’s success.” EY and Lindahl Lawfirm have, in collaboration over the last two years, successfully taken Vested to the REFM market.

Vested is a combination of an outcome-based business model and a relational contract. Vested creates business relationships with experts outside one’s own domain with the aim of accomplishing ambitious objectives never accomplished before. These relationships are characterized as “Vested” because they involve creating a relationship in which the parties have a committed and profound interest in each other’s success. To put it simply, the parties are most successful when both reap the benefits.

By applying Vested, the misalignments described in the previous sections can be avoided. This can be illustrated by looking at the five rules Vested is built upon, introduced as a chronological process where buyers and suppliers collaborate and apply a “What’s In It For We” - (WIIFWe) approach — not a “What’s In It For Me” – (WIIFMe) approach.

1. Focus on outcomes, not transactions: the buyer specifies the needs (transformation to a certain stage, cost savings, etc.), not specific transactions. The supplier will not be compensated or measured on how often the activity is performed. It is the desired outcomes that matters.

2. Focus on the what, not the how: many REFM contracts have moved beyond instructions (how to perform a service) to defining the function (e.g., lawns should make a pleasant impression or be within a specified height range). By doing so, the box that the supplier can optimize has been made bigger.

Figure 6: Vested five rules

19Real estate and facilities management |

3. Agree on clearly defined and measurable outcomes: the parties spend time on defining a limited number (preferably not more than five) of clearly defined and measurable outcomes for the entire service delivery. By doing so, the buyer will not micromanage the supplier − after all, the idea of outsourcing is to let someone that is better suited manage the services. It will also help ensure focus on the right areas.

4. Pricing model with incentives that optimize the business: the pricing model should be built on three principles. Firstly, there should be strong incentives to deliver results, not to deliver a service. Secondly, the buyer and service should share risk and reward based on aligned interests. Thirdly, only risk that the service provider can control should be transferred.

5. Insight versus oversight structure: instead of multiple reports on used volume of consumables and dashboards, the information between buyer and supplier must support the desired outcomes, where the parties collaborate to manage the business.

Vested thinking is different. It often means going against how suppliers and business partners traditionally approach working together. It requires long-term thinking, not short-term thinking. Vested is about working alongside suppliers as business partners rather than relying on default procurement processes that use transactional buy-sell principles. Moreover, it is about moving away from rigid contracts and statements of work, and instead creating flexible business agreements based on trust, transparency and fairness when business happens.

In our view, Vested is not just for big companies − it can be applied successfully in all kindsof contexts, be they private or public.

“When Vested contracts are conceived right they require less ongoing maintenance and less escalations. Shared savings and gain share programs are effective. The providers are now really impacting the buyers’ balance sheets.” Timothy McParlane, Jones Lang Lasalle Inc., COO, Procter & Gamble Account

Unlike previously, the value that companies will be looking for from an REFM operating model will be tightly connected to the corporate transformation.

20 | Real estate and facilities management

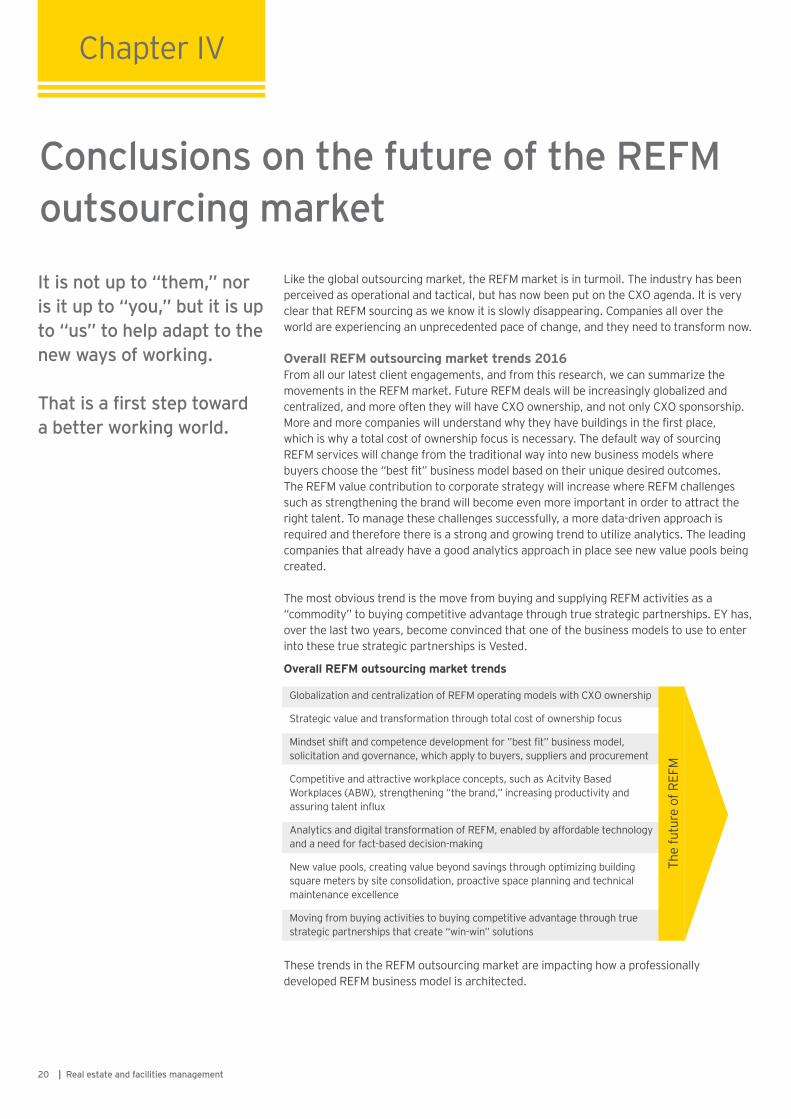

Like the global outsourcing market, the REFM market is in turmoil. The industry has been perceived as operational and tactical, but has now been put on the CXO agenda. It is very clear that REFM sourcing as we know it is slowly disappearing. Companies all over the world are experiencing an unprecedented pace of change, and they need to transform now.

Overall REFM outsourcing market trends 2016From all our latest client engagements, and from this research, we can summarize the movements in the REFM market. Future REFM deals will be increasingly globalized and centralized, and more often they will have CXO ownership, and not only CXO sponsorship. More and more companies will understand why they have buildings in the first place, which is why a total cost of ownership focus is necessary. The default way of sourcing REFM services will change from the traditional way into new business models where buyers choose the “best fit” business model based on their unique desired outcomes. The REFM value contribution to corporate strategy will increase where REFM challenges such as strengthening the brand will become even more important in order to attract the right talent. To manage these challenges successfully, a more data-driven approach is required and therefore there is a strong and growing trend to utilize analytics. The leading companies that already have a good analytics approach in place see new value pools being created.

The most obvious trend is the move from buying and supplying REFM activities as a “commodity” to buying competitive advantage through true strategic partnerships. EY has, over the last two years, become convinced that one of the business models to use to enter into these true strategic partnerships is Vested.

These trends in the REFM outsourcing market are impacting how a professionally developed REFM business model is architected.

Globalization and centralization of REFM operating models with CXO ownership

Strategic value and transformation through total cost of ownership focus

Mindset shift and competence development for ”best fit” business model, solicitation and governance, which apply to buyers, suppliers and procurement

Competitive and attractive workplace concepts, such as Acitvity Based Workplaces (ABW), strengthening “the brand,” increasing productivity and assuring talent influx

Analytics and digital transformation of REFM, enabled by affordable technology and a need for fact-based decision-making

New value pools, creating value beyond savings through optimizing building square meters by site consolidation, proactive space planning and technical maintenance excellence

Moving from buying activities to buying competitive advantage through true strategic partnerships that create “win-win” solutions

The

futu

re o

f REF

MOverall REFM outsourcing market trends

Chapter IV

Conclusions on the future of the REFM outsourcing market

It is not up to “them,” nor is it up to “you,” but it is up to “us” to help adapt to the new ways of working.

That is a first step toward a better working world.

21Real estate and facilities management |

From a buyer perspective, we found that the REFM business model needs to contribute to corporate strategy with value beyond savings. The REFM business model must enable execution of the full corporate transformation agenda. Through combined forces, sustainable business transformation can be achieved faster when a small, yet competent, demand organization collaborates with a “best fit” partner. With that in mind, REFM business as such must also change its way of structuring and soliciting its deals.

From a supplier perspective, we found that suppliers are shifting value creation chains in response to a very challenging business climate where a wider service portfolio (total cost of ownership) will enable suppliers to come closer to their clients. In the process, new value pools arise. Suppliers therefore welcome the movement toward true strategic partnerships, as strategic and complex deals are best orchestrated on the basis of outcome-based business models in collaborative contracts. In the future, REFM suppliers have a real opportunity to become true integrators that deliver real strategic client value closely aligned with the buyers’ strategic objectives.

From a procurement perspective, sourcing as we know it is slowly disappearing. Strategic relationship management is becoming a hot topic as new business models entering the market create completely new expectations for procurement. Procurement organizations need to become strategic business partners that focus more on value creation and less on savings. To achieve this, new competencies are needed along with knowledge about the REFM market and which approach to use when requesting information, quotations and proposals.

Our role as advisor is undergoing definite change, and we will be seen as taking sides less often. Our role will be that of a deal architect helping complex strategic businesses where we facilitate the process and support stakeholders in generating desired results. At the same time, our market is growing rapidly as we work with various market stakeholders. Moreover, we can play an even greater strategic role when REFM becomes a topic on the boardroom agenda. We believe that strategic partnerships and new business models represent the next level for the REFM business. Lastly, we acknowledge that the “classic” way of carrying out REFM outsourcing business will remain, but not as the default choice.

It is not up to “them,” nor is it up to “you”, but it is up to “us” to help adapt to the new ways of working. That is a first step toward a better working world.

22 | Real estate and facilities management

Building a better working workplace.

23Real estate and facilities management |

EY is a leading independent REFM advisor in the Nordic region with experience from more than 300 transformation projects.

NordicsMagnus KuchlerLeader of REFM Advisory Services at EY in the Nordic Region [email protected]

DenmarkClaus Frigård ChristensenREFM Advisory – responsible Nordics [email protected]

SwedenRobin WarchalowskiREFM Advisory [email protected]

NorwayDaniela HamborgREFM Advisory [email protected]

Finland Jaakko Hirvola REFM [email protected]

NordicsHenrik JärleskogREFM Advisory, Head of [email protected]

Authoring Management Consultants and Project TeamHenrik Järleskog Gustaf Leijonmarck (editor) Henrik Orre (editor) Josephine Bergström (editor) Alexander Lundin (editor)Amanda Lundell (editor)

Martin Cardell (Project Team)Niclas Elfström (Project Team)Rune L. Johannessen (Project Team) Daniela Milosevska Hamborg (Project Team) Victor Mannerholm Hammar (Project Team) Christine Bergan (Project Team)

EY’s Nordic REFM Team

EY | Assurance | Tax | Transactions | Advisory

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 EYGM Limited. All Rights Reserved.

EYG no: AU3717ED None

This material has been prepared for general informational purposes only and is not intended to be relied upon as accounting, tax, or other professional advice. Please refer to your advisors for specific advice.

ey.com

The views of third parties set out in this publication are not necessarily the views of the global EY organization or its member firms. Moreover, they should be seen in the context of the time they were made.