Embed Size (px)

Citation preview

Generating Income by Using Data to Better Manage Debt, Fraud, and Errors –2 Phase Approach

Local GovernmentEric Applewhite November 2015

2© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Local Government: The Current Situation

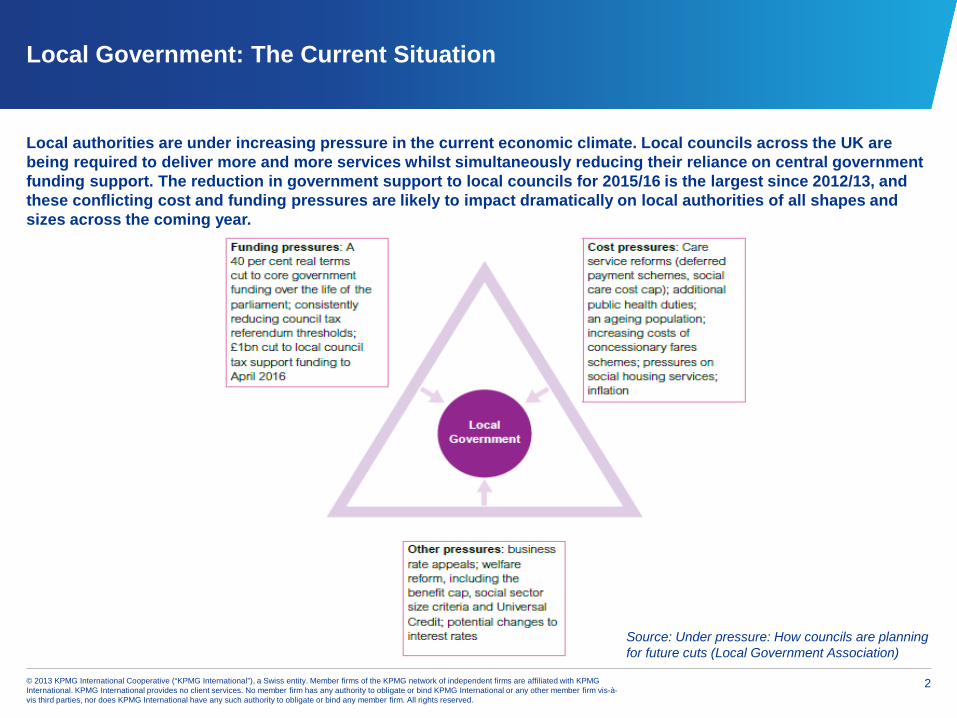

Local authorities are under increasing pressure in the current economic climate. Local councils across the UK are being required to deliver more and more services whilst simultaneously reducing their reliance on central government funding support. The reduction in government support to local councils for 2015/16 is the largest since 2012/13, and these conflicting cost and funding pressures are likely to impact dramatically on local authorities of all shapes and sizes across the coming year.

Source: Under pressure: How councils are planning for future cuts (Local Government Association)

3© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

The True Impact of Writing-off Debt

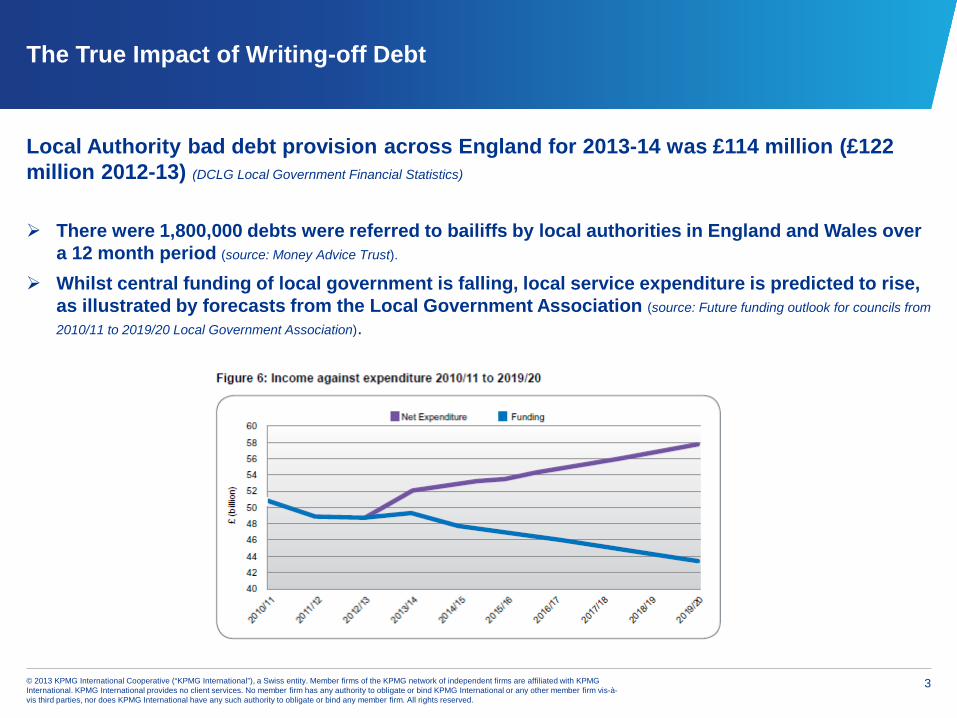

Local Authority bad debt provision across England for 2013-14 was £114 million (£122 million 2012-13) (DCLG Local Government Financial Statistics)

There were 1,800,000 debts were referred to bailiffs by local authorities in England and Wales over a 12 month period (source: Money Advice Trust).

Whilst central funding of local government is falling, local service expenditure is predicted to rise, as illustrated by forecasts from the Local Government Association (source: Future funding outlook for councils from

2010/11 to 2019/20 Local Government Association).

4© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Drivers for change

….typically a combination

Operational Effectiveness

Sustainability/Funding of new

services

Balancing the budget

5© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

So what is KPMG’s Debt, Fraud, and Error Proposition?

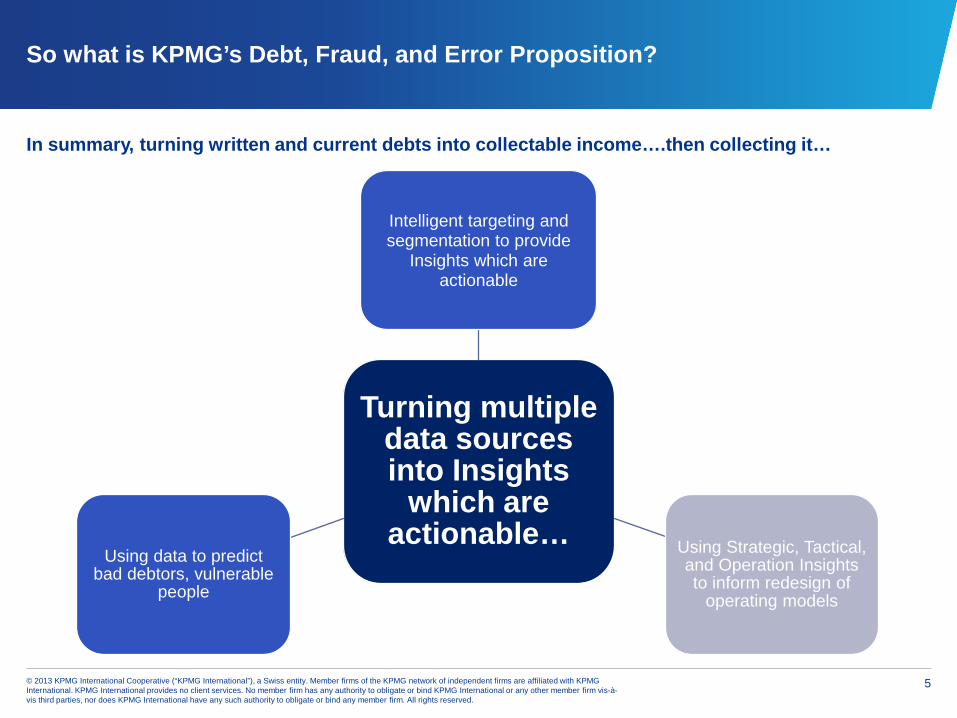

In summary, turning written and current debts into collectable income….then collecting it…

Turning multiple data sources into Insights

which are actionable…

Intelligent targeting and segmentation to provide

Insights which are actionable

Using Strategic, Tactical, and Operation Insights to inform redesign of

operating models

Using data to predict bad debtors, vulnerable

people

6© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

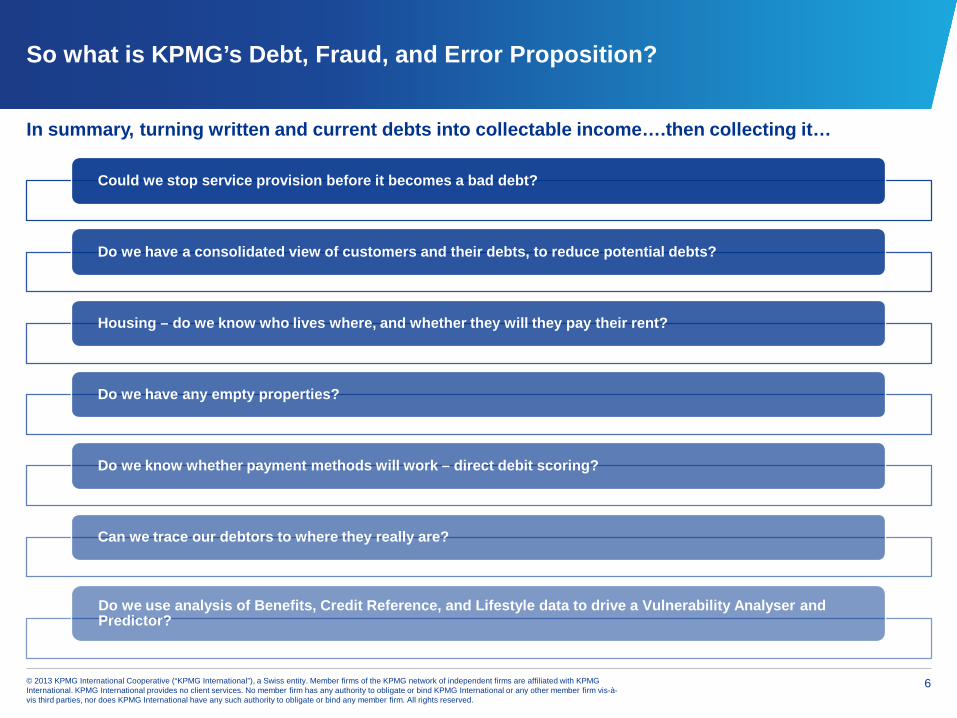

So what is KPMG’s Debt, Fraud, and Error Proposition?

In summary, turning written and current debts into collectable income….then collecting it…

Could we stop service provision before it becomes a bad debt?

Do we have a consolidated view of customers and their debts, to reduce potential debts?

Housing – do we know who lives where, and whether they will they pay their rent?

Do we have any empty properties?

Do we know whether payment methods will work – direct debit scoring?

Can we trace our debtors to where they really are?

Do we use analysis of Benefits, Credit Reference, and Lifestyle data to drive a Vulnerability Analyser and Predictor?

7© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

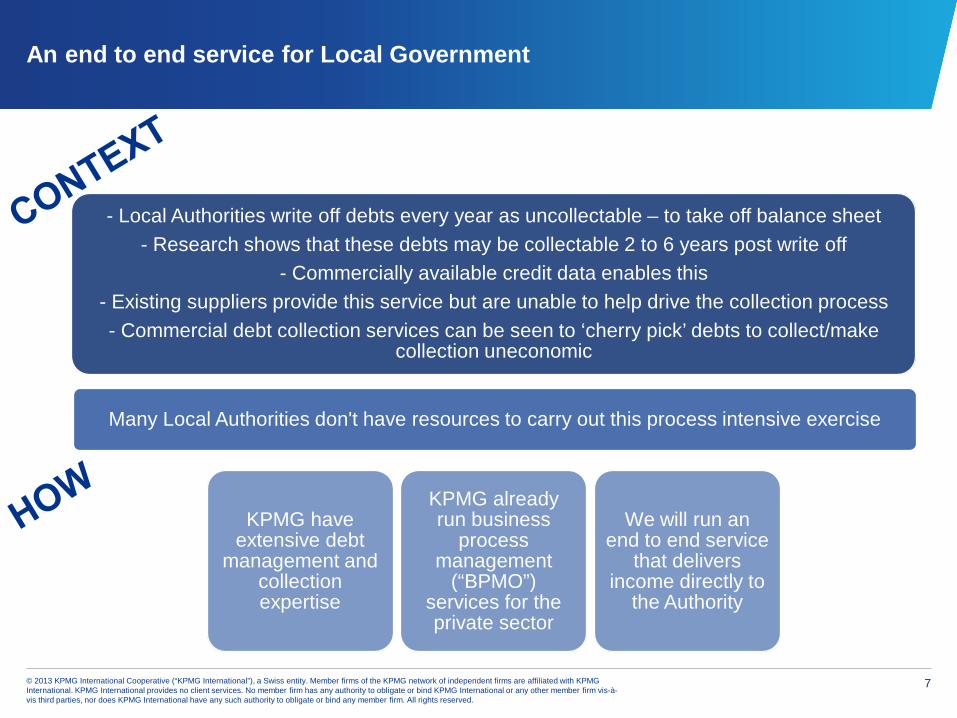

An end to end service for Local Government

- Local Authorities write off debts every year as uncollectable – to take off balance sheet- Research shows that these debts may be collectable 2 to 6 years post write off

- Commercially available credit data enables this- Existing suppliers provide this service but are unable to help drive the collection process- Commercial debt collection services can be seen to ‘cherry pick’ debts to collect/make

collection uneconomic

Many Local Authorities don't have resources to carry out this process intensive exercise

KPMG have extensive debt

management and collection expertise

KPMG already run business

process management

(“BPMO”) services for the private sector

We will run an end to end service

that delivers income directly to

the Authority

8© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

An end to end service for Local Government

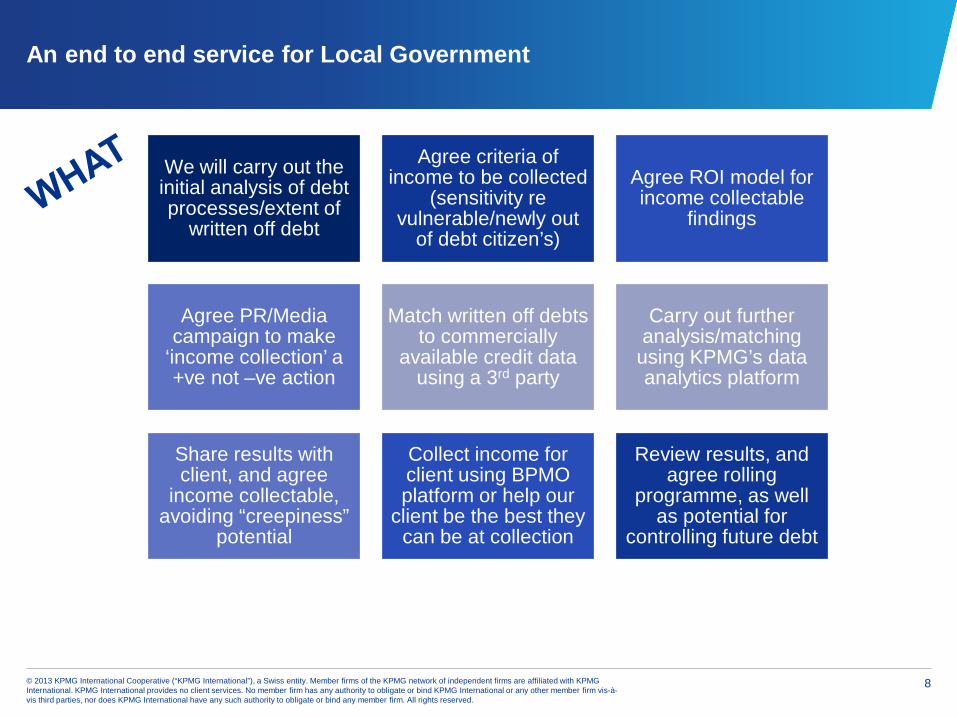

We will carry out the initial analysis of debt processes/extent of

written off debt

Agree criteria of income to be collected

(sensitivity re vulnerable/newly out

of debt citizen’s)

Agree ROI model for income collectable

findings

Agree PR/Media campaign to make

‘income collection’ a +ve not –ve action

Match written off debts to commercially

available credit data using a 3rd party

Carry out further analysis/matching

using KPMG’s data analytics platform

Share results with client, and agree

income collectable, avoiding “creepiness”

potential

Collect income for client using BPMO platform or help our

client be the best they can be at collection

Review results, and agree rolling

programme, as well as potential for

controlling future debt

9© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

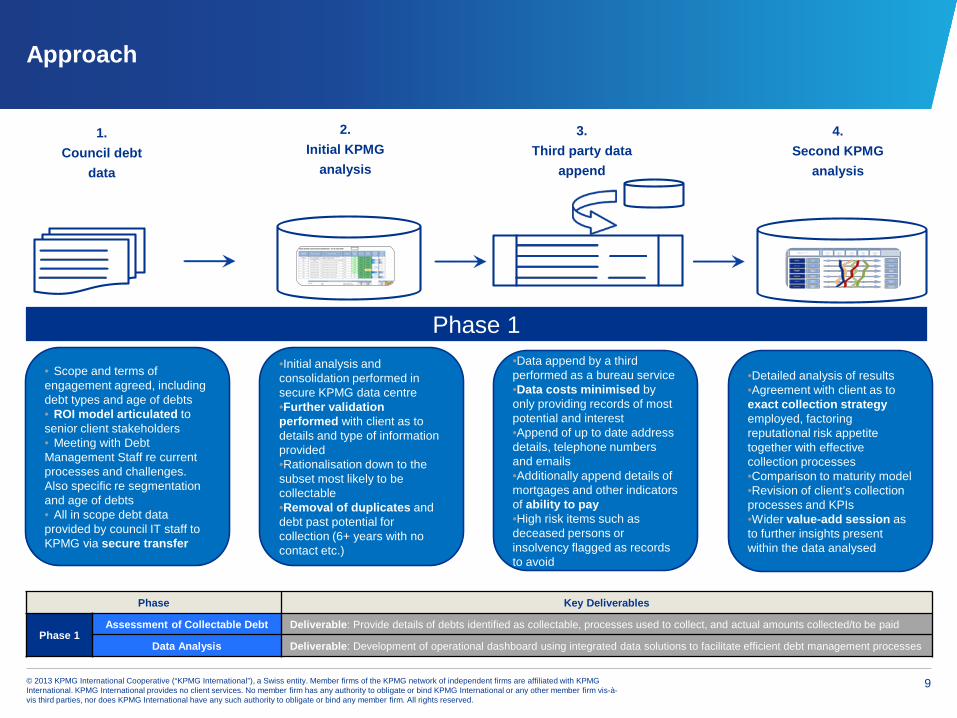

Approach

• Scope and terms of engagement agreed, including debt types and age of debts• ROI model articulated to senior client stakeholders• Meeting with Debt Management Staff re current processes and challenges. Also specific re segmentation and age of debts• All in scope debt data provided by council IT staff to KPMG via secure transfer

1.Council debt

data

2.Initial KPMG

analysis

3.Third party data

append

4.Second KPMG

analysis

•Initial analysis and consolidation performed in secure KPMG data centre•Further validation performed with client as to details and type of information provided•Rationalisation down to the subset most likely to be collectable•Removal of duplicates and debt past potential for collection (6+ years with no contact etc.)

•Data append by a third performed as a bureau service•Data costs minimised by only providing records of most potential and interest•Append of up to date address details, telephone numbers and emails•Additionally append details of mortgages and other indicators of ability to pay•High risk items such as deceased persons or insolvency flagged as records to avoid

•Detailed analysis of results•Agreement with client as to exact collection strategy employed, factoring reputational risk appetite together with effective collection processes•Comparison to maturity model•Revision of client’s collection processes and KPIs•Wider value-add session as to further insights present within the data analysed

Phase 1

Phase Key Deliverables

Phase 1Assessment of Collectable Debt Deliverable: Provide details of debts identified as collectable, processes used to collect, and actual amounts collected/to be paid

Data Analysis Deliverable: Development of operational dashboard using integrated data solutions to facilitate efficient debt management processes

10© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

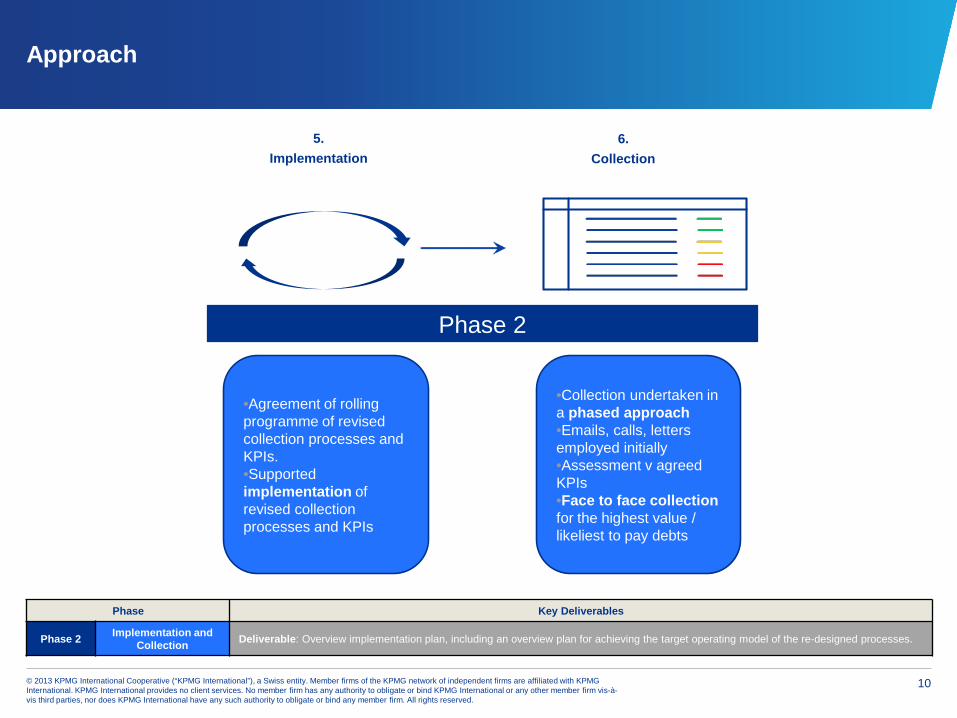

Approach

Phase 2

6.Collection

5.Implementation

•Collection undertaken in a phased approach•Emails, calls, letters employed initially•Assessment v agreed KPIs•Face to face collection for the highest value / likeliest to pay debts

•Agreement of rolling programme of revised collection processes and KPIs.•Supported implementation of revised collection processes and KPIs

Phase Key Deliverables

Phase 2 Implementation and Collection Deliverable: Overview implementation plan, including an overview plan for achieving the target operating model of the re-designed processes.

11© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Pilot Case Study

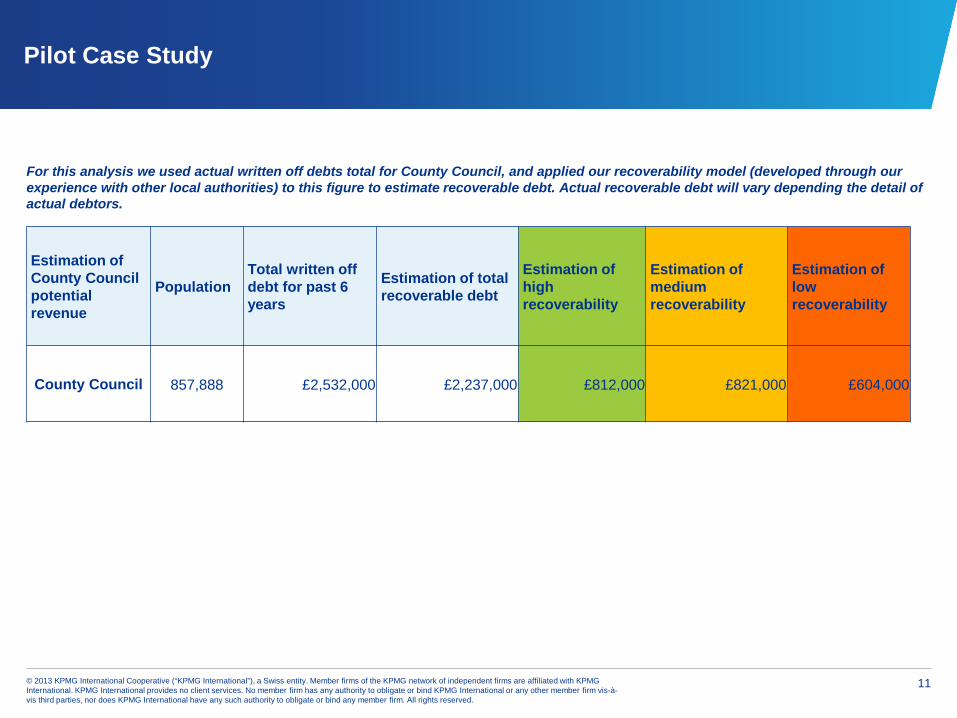

Estimation of County Council potential revenue

PopulationTotal written off debt for past 6 years

Estimation of total recoverable debt

Estimation of high recoverability

Estimation of medium recoverability

Estimation of low recoverability

County Council 857,888 £2,532,000 £2,237,000 £812,000 £821,000 £604,000

For this analysis we used actual written off debts total for County Council, and applied our recoverability model (developed through our experience with other local authorities) to this figure to estimate recoverable debt. Actual recoverable debt will vary depending the detail of actual debtors.

12© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Pilot Case Study

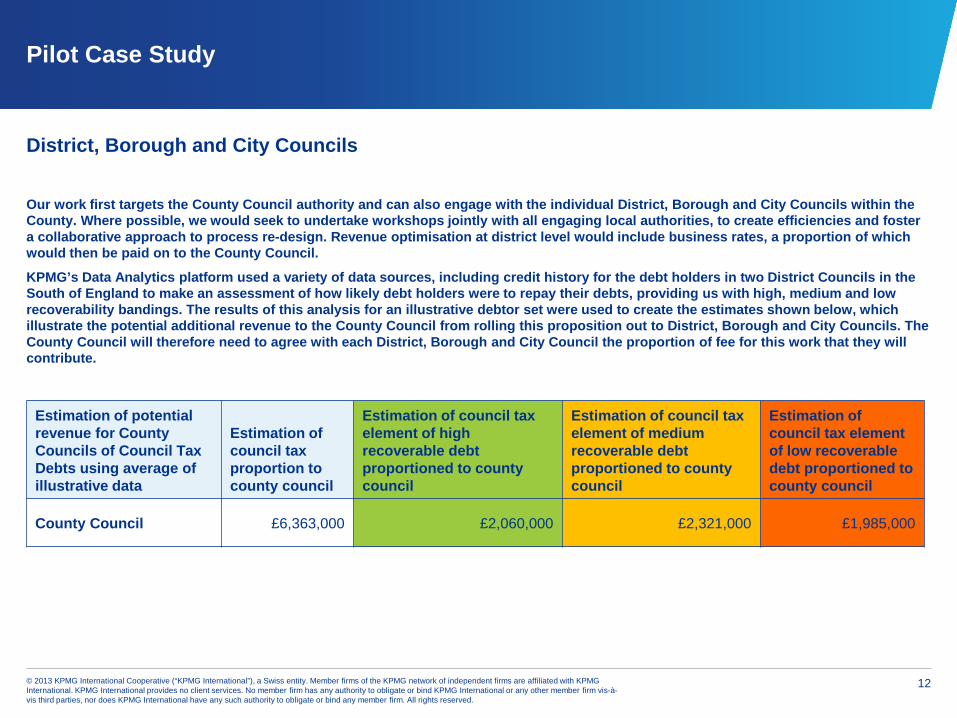

District, Borough and City Councils

Our work first targets the County Council authority and can also engage with the individual District, Borough and City Councils within the County. Where possible, we would seek to undertake workshops jointly with all engaging local authorities, to create efficiencies and fostera collaborative approach to process re-design. Revenue optimisation at district level would include business rates, a proportion of which would then be paid on to the County Council.

KPMG’s Data Analytics platform used a variety of data sources, including credit history for the debt holders in two District Councils in the South of England to make an assessment of how likely debt holders were to repay their debts, providing us with high, medium and low recoverability bandings. The results of this analysis for an illustrative debtor set were used to create the estimates shown below, which illustrate the potential additional revenue to the County Council from rolling this proposition out to District, Borough and City Councils. The County Council will therefore need to agree with each District, Borough and City Council the proportion of fee for this work that they will contribute.

Estimation of potential revenue for CountyCouncils of Council Tax Debts using average of illustrative data

Estimation of council tax proportion to county council

Estimation of council tax element of high recoverable debt proportioned to county council

Estimation of council tax element of medium recoverable debt proportioned to county council

Estimation of council tax element of low recoverable debt proportioned to county council

County Council £6,363,000 £2,060,000 £2,321,000 £1,985,000

13© 2013 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights reserved.

Pilot Case Study

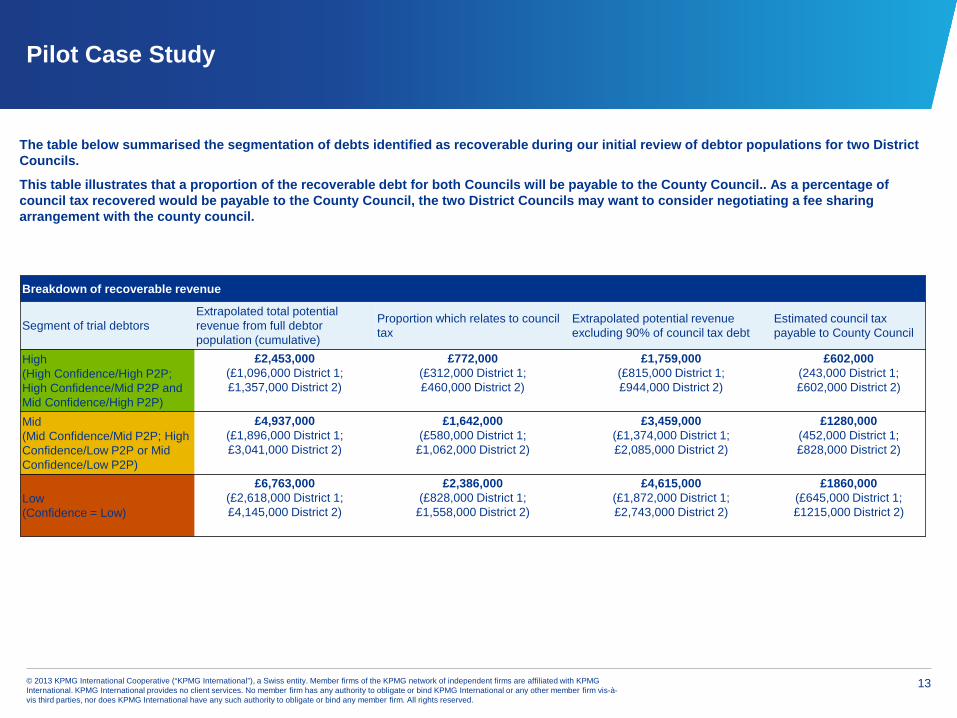

The table below summarised the segmentation of debts identified as recoverable during our initial review of debtor populations for two District Councils.

This table illustrates that a proportion of the recoverable debt for both Councils will be payable to the County Council.. As a percentage of council tax recovered would be payable to the County Council, the two District Councils may want to consider negotiating a fee sharing arrangement with the county council.

Breakdown of recoverable revenue

Segment of trial debtorsExtrapolated total potential revenue from full debtor population (cumulative)

Proportion which relates to counciltax

Extrapolated potential revenue excluding 90% of council tax debt

Estimated council tax payable to County Council

High(High Confidence/High P2P;High Confidence/Mid P2P and Mid Confidence/High P2P)

£2,453,000 (£1,096,000 District 1; £1,357,000 District 2)

£772,000(£312,000 District 1; £460,000 District 2)

£1,759,000(£815,000 District 1; £944,000 District 2)

£602,000(243,000 District 1; £602,000 District 2)

Mid(Mid Confidence/Mid P2P; High Confidence/Low P2P or Mid Confidence/Low P2P)

£4,937,000 (£1,896,000 District 1; £3,041,000 District 2)

£1,642,000(£580,000 District 1;

£1,062,000 District 2)

£3,459,000(£1,374,000 District 1; £2,085,000 District 2)

£1280,000(452,000 District 1; £828,000 District 2)

Low(Confidence = Low)

£6,763,000 (£2,618,000 District 1; £4,145,000 District 2)

£2,386,000(£828,000 District 1;

£1,558,000 District 2)

£4,615,000(£1,872,000 District 1; £2,743,000 District 2)

£1860,000(£645,000 District 1; £1215,000 District 2)

© 2013 KPMG LLP, a UK limited liability partnership, is a subsidiary of KPMG Europe LLP and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative, a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International Cooperative (KPMG International).

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

If you have any questions or would like further information please contact:

Eric ApplewhiteDirectorKPMG LLPMobile: +44 (0)7796 937808