Embed Size (px)

Citation preview

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

Global markets at a glance A tech share rally drove US stocks up sharply for a second day on Friday as earnings from companies including Micro-soft beat analysts' expectations, while healthcare shares rebounded from recent losses. The gains left the S&P 500 in positive territory for the year and above its 200-DMA for the first time since Aug. 19. An unexpected rate cut in China added to the positive tone for US stocks, which also registered gains for the week. Microsoft shares rose 10.1% to USD 52.87, their highest in 15 years, after adjusted reve-nue beat expectations for the ninth quarter in a row. The DJI average rose 157.54pts, or 0.9%, to 17,646.7, the S&P 500 gained 22.64pts, or 1.1%, to 2,075.15 and the Nasdaq added 111.81pts, or 2.27%, to 5,031.86. For the week, the Dow rose 2.5%, the S&P 500 gained 2.1 % and the Nasdaq jumped 3%. The S&P 500 is now up 0.8% for the year so far and up 7.1 % for October. European shares rose to 2-month highs on Friday, with ex-port-driven stocks such as autos leading the way as China announced a surprise rate cut just a day after the ECB sig-naled possibility of stronger stimulus measures. FTSEuro-first 300 index rose 1.95%, building on a 2.1% gain in past session. China's central bank cut interest rates for the sixth time since November on Friday in another attempt to jumpstart a slowing economy. The PBOC said on its website that it was lowering the one-year benchmark bank lending rate by 25 basis points to 4.35 %, w.e.f. Oct 24. 1-year benchmark deposit rate was also lowered by 25bps to 1.50 %. Previous day Roundup Benchmark indices gained strength on Friday after a con-solidation in previous two consecutive sessions, tracking rally in global peers on hopes of another fiscal stimulus package from ECB. Banks and FMCG stocks drove today's rally but broader markets underperformed benchmarks. The Sensex rose 183.15pts or 0.67 % to close at 27470.81 and Nifty climbed 43.75pts or 0.53 % to 8295.45 after hit-ting an intraday high of 8328.10. However, BSE Midcap in-dex lost 0.3% and Smallcap fell 0.4%. Index stats The Market was very volatile in last session. The sartorial indices performed as follow; Consumer Durables [up 19.75pts], Capital Goods [down 247.46pts], PSU [up 45.20pts], FMCG [up 87.10Pts], Realty [up 0.45pts], Power [up 7.76pts], Auto [down 135.09Pts], Healthcare [up 66.99Pts], IT [up 40.54pts], Metals [up 24.54pts], TECK [down 24.86pts], Oil& Gas [up 75.12pts].

World Indices

Index Value % Change

D J l 17464.70 +0.90

S&P 500 2075.15 +1.10

NASDAQ 5031.86 +2.27

FTSE 100 6444.08 +1.06

Nikkei 225 18825.30 +2.11

Hong Kong 23151.94 +1.34

Top Gainers

Company CMP Change % Chg

AXISBANK 527.00 15.25 2.98

ITC 358.35 9.80 2.81

CAIRN 158.00 3.75 2.43

HDFC 1,342.90 27.15 2.06

GAIL 325.60 6.55 2.05

Top Losers

Company CMP Change % Chg

IDEA 140.40 11.50 -7.57

BHARTIARTL 357.35 14.15 -3.81

VEDL 102.40 2.70 -2.57

LT 1,514.00 36.45 -2.35

MARUTI 4,383.00 91.70 -2.05

Stocks at 52 Week’s HIGH

Symbol Prev. Close Change %Chg

APLAPOLLO 545.00 -11.70 -2.10

GMBREW 525.05 25.00 5.00

ESCORTS 181.30 -5.20 -2.79

JUBILANT 417.70 1.20 0.29

KRBL 204.50 -5.45 -2.60

KWALITY 109.65 0.45 0.41

RUSHIL 270.90 1.30 0.48

Indian Indices

Company CMP Change % Chg

NIFTY 8295.45 +43.75 +0.53

SENSEX 27470.81 +183.15 +0.67

Stocks at 52 Week’s LOW

Symbol Prev. Close Change %Chg

- -

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

STOCK RECOMMENDATION [CASH] 3. DEEPIND [CASH]

DEEPIND made new 52 week high of 209.80 while before last session it was getting resistance at 202 which it broken at last session with gain of 2.60%, now all the indicator is positive so we advise to buy it above 210 for target of 215-220-225 use stop loss of 203

MACRO NEWS SadbhavInfra Projects looking to refinance 3 road assets KPIT Tech Q2 profit jumps 69% on strong EBITDA margin Bharti Infratel Q2 net up 0.6%; EBITDA, rev miss forecast Tata Steel, Britain offer more aid to steel town Glenmark Pharmaceuticals inks pact with Celon for ge-

neric Seretide Accuhaler The quick service restaurants sector in India is likely to

grow three-fold to Rs 25,000 crore within 5 yrs. Pulses slide as govt intensifies crackdown against hoard-

ing Payments banks to expand reach of banking in rural ar-

eas: World Bank Givaudan to invest Rs 368 crore in new Pune facility Cess bites into crude revenue on low prices New urea plant at Ramagundam gets Centre's green nod S&P downgrades Vedanta Resources credit rating Embassy Group to build 200-mw solar power plant in

Karnataka Tender to buy 1,000-mw short-term power soon Tata Motors launches bus dealership BusZone Fitch affirms JLR ratings at 'BB-' with positive outlook Arvind Ltd's 7000 workers on strike in Ahmedabad, com-

pany calls agitation illegal Drugmakers plan to get together to discuss how to get

out of FDA warnings and bans.

STOCK RECOMMENDATIONS [FUTURE] 1. CROMPTON GREAVES [FUTURE]

Last week CROMPGREAV FUTURE faced profit booking at higher level at last session in first half it try to recover some losses but in second half it loosed gain and end with bearish inverted hammer now it has support at 178 while RSI also has bearish pattern so we advise to sell it below 182.50 for target of 180.50-178 use stop loss of 186.60 otherwise short for positional around 187-188 use stop loss at 193 for target of 182-178-174.

2. ALBK [FUTURE]

Last week ALBK FUTURE cross important resistance or break-out level of 80 but it could not given close above this level since Stochastic given negative cross over for that it breached at last session it finished flat at 78.30 since mo-mentum indicator is negative so it will be good to sell around resistance at 79.50-80 use stop loss of 81.75 for target of 78–76-74.

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

FUTURE & OPTION

MOST ACTIVE CALL OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY PE 8,300 44.25 8,06,134 25,68,825

NIFTY PE 8,200 15.70 7,76,623 56,02,125

BANKNIFTY PE 17,500 50.70 76,760 5,28,225

RELIANCE PE 960 12.00 4,291 5,70,000

ASIANPAINT PE 840 12.00 3,521 2,41,250

LT PE 1,500 14.50 3,357 1,89,375

IDEA PE 140 2.05 2,864 7,02,000

TATAMOTORS PE 380 5.00 2,604 7,65,500

MOST ACTIVE PUT OPTION

Symbol Op-

tion

Type

Strike

Price

LTP Traded

Volume

(Contracts)

Open

Interest

NIFTY CE 8,000 90.30 4,66,515 37,15,925

NIFTY CE 8,100 120.50 3,81,905 32,23,875

BANKNIFTY CE 17,000 201.10 44,922 5,40,750

TATAMOTOR CE 320 8.45 3,749 6,79,500

RELIANCE CE 880 15.85 3,166 2,64,250

LT CE 1,500 24.50 1,917 1,80,500

TATASTEEL CE 220 6.95 1,725 6,51,000

INFY CE 1,100 29.50 1,510 2,31,750

FII DERIVATIVES STATISTICS

BUY OPEN INTEREST AT THE END OF THE DAY SELL

No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores No. of

Contracts Amount in

Crores NET AMOUNT

INDEX FUTURES 132460 4097.23 70155 2247.07 1010423 27434.1 1850.167

INDEX OPTIONS 391778 11290.9 412487 11343.1 2435939 78333.5 -52.207

STOCK FUTURES 215348 6301.56 207156 6754.51 1726506 49863.3 -452.946

STOCK OPTIONS 71113 1930.39 78135 2117.95 128028 3531.08 -187.555

TOTAL 1157.45

STOCKS IN NEWS Petronet pays hefty demurrage as PSUs refuse costly

gas import Govt rejects Cairn appeal to renew Rajasthan block

deal; asks for investment plan to assess projected profit

Strides Arcolab buys local J&J brands, picks majority stake in Medispan

Coal India takes IT route to track mining projects Vedanta mulls sweetening Cairn merger swap ratio FTIL in process of selling rest 6.58 pc stake in IEX NIFTY FUTURE

NIFTY stayed consolidated all the week and could move only around 100 points. Even after a long consolidation Nifty future finished with positive candlestick on weekly chart, but it has also prepared a channel and it is near its resistance so overall Nifty seems to be weak. We advise you to Sell Nifty Future on rise around 8380 for the tar-gets of 8290 and 8200 with strict stop loss of 8550

INDICES R2 R1 PIVOT S1 S2

NIFTY 8,350.00 8,322.00 8,301.00 8,273.00 8,252.00

BANK NIFTY 18,051.00 17,992.00 17,922.00 17,863.00 17,793.00

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

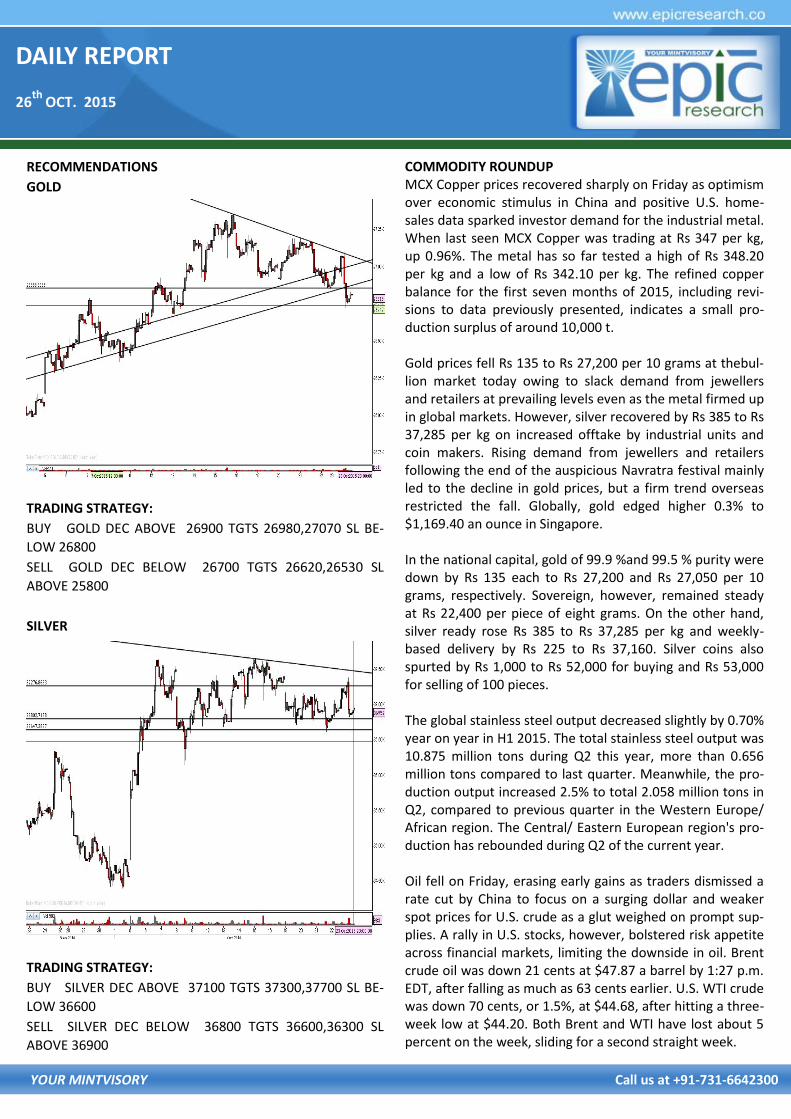

RECOMMENDATIONS

GOLD

TRADING STRATEGY:

BUY GOLD DEC ABOVE 26900 TGTS 26980,27070 SL BE-

LOW 26800

SELL GOLD DEC BELOW 26700 TGTS 26620,26530 SL

ABOVE 25800

SILVER

TRADING STRATEGY:

BUY SILVER DEC ABOVE 37100 TGTS 37300,37700 SL BE-

LOW 36600

SELL SILVER DEC BELOW 36800 TGTS 36600,36300 SL

ABOVE 36900

COMMODITY ROUNDUP MCX Copper prices recovered sharply on Friday as optimism over economic stimulus in China and positive U.S. home-sales data sparked investor demand for the industrial metal. When last seen MCX Copper was trading at Rs 347 per kg, up 0.96%. The metal has so far tested a high of Rs 348.20 per kg and a low of Rs 342.10 per kg. The refined copper balance for the first seven months of 2015, including revi-sions to data previously presented, indicates a small pro-duction surplus of around 10,000 t. Gold prices fell Rs 135 to Rs 27,200 per 10 grams at thebul-lion market today owing to slack demand from jewellers and retailers at prevailing levels even as the metal firmed up in global markets. However, silver recovered by Rs 385 to Rs 37,285 per kg on increased offtake by industrial units and coin makers. Rising demand from jewellers and retailers following the end of the auspicious Navratra festival mainly led to the decline in gold prices, but a firm trend overseas restricted the fall. Globally, gold edged higher 0.3% to $1,169.40 an ounce in Singapore. In the national capital, gold of 99.9 %and 99.5 % purity were down by Rs 135 each to Rs 27,200 and Rs 27,050 per 10 grams, respectively. Sovereign, however, remained steady at Rs 22,400 per piece of eight grams. On the other hand, silver ready rose Rs 385 to Rs 37,285 per kg and weekly-based delivery by Rs 225 to Rs 37,160. Silver coins also spurted by Rs 1,000 to Rs 52,000 for buying and Rs 53,000 for selling of 100 pieces. The global stainless steel output decreased slightly by 0.70% year on year in H1 2015. The total stainless steel output was 10.875 million tons during Q2 this year, more than 0.656 million tons compared to last quarter. Meanwhile, the pro-duction output increased 2.5% to total 2.058 million tons in Q2, compared to previous quarter in the Western Europe/African region. The Central/ Eastern European region's pro-duction has rebounded during Q2 of the current year. Oil fell on Friday, erasing early gains as traders dismissed a rate cut by China to focus on a surging dollar and weaker spot prices for U.S. crude as a glut weighed on prompt sup-plies. A rally in U.S. stocks, however, bolstered risk appetite across financial markets, limiting the downside in oil. Brent crude oil was down 21 cents at $47.87 a barrel by 1:27 p.m. EDT, after falling as much as 63 cents earlier. U.S. WTI crude was down 70 cents, or 1.5%, at $44.68, after hitting a three-week low at $44.20. Both Brent and WTI have lost about 5 percent on the week, sliding for a second straight week.

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NCDEX

NCDEX ROUNDUP

Chana prices moved down by 2.03% to Rs 4,815 per quintal as traders reduced exposure amid increased supplies at the spot market after the govt took steps to curb soaring prices. At NCDEX chana for delivery in Nov fell Rs 100, or 2.03%, to Rs 4,815 per quintal with an open interest of 55,180 lots. Chana for delivery in December contracts eased Rs 96, or 1.93%, to Rs 4,874 per quintal in 50,410 lots. Trimming of exposure by traders triggered by pick-up in supplies in the physical market after the raids by authorities on hoarders mainly kept pressure on chana prices. The govt's decision to import more pulses too helped prices decline. Meanwhile, over 35,000 tonnes of pulses have been seized form 10 states in two days after state govts intensified crackdown against hoarding and black marketing of the commodity.

As per the latest release from Ministry of Agriculture, the total area sown under Rabi crops as on 23rd October, 2015 reported at 28.20 lakh hectares as compared to 17.36 lakh hectare last year at this time. Wheat has been sown/transplanted in 0.20 lakh hectares, pulses in 9.83 lakh hec-tare coarse, cereals in 16.57 lakh hectares and oilseeds in 1.60 lakh hectares.

Mentha oil prices edged higher by 0.30% to Rs 895 per kg in futures trade today on higher demand from spot markets. Besides, tight stock position in physical markets on re-stricted supplies from producing region supported the up-side. At MCX mentha oil for delivery in October month rose Rs 2.70, or 0.30%, to Rs 895 per kg in business turnover of 172 lots. Similarly, the oil for delivery in October shed Rs 2, or 0.22%, to Rs 907.10 per kg in 88 lots. Pick up in demand from consuming industries in the spot market, restricted supplies from Chandausi in Uttar Pradesh, mainly led to rise in mentha oil prices at futures trade.

NCDEX INDICES

Index Value % Change

CAETOR SEED 4060 -1.55

CHANA 4866 -1.00

CORIANDER 10904 -5.99

COTTON SEED 1688 +0.24

GUAR SEED 4026 -1.40

JEERA 16135 +0.81

MUSTARDSEED 5117 +1.29

REF. SOY OIL 630.7 -0.31

TURMERIC 2775 +0.33

WHEAT 8440 +2.08

RECOMMENDATIONS

DHANIYA

BUY CORIANDER NOV ABOVE 10970 TARGET 10998 11078

SL BELOW 10943

SELL CORIANDER NOV BELOW 10870 TARGET 10842 10762

SL ABOVE 10897

GUARSGUM

BUY GUARGUM NOV ABOVE 8550 TARGET 8600 8670 SL

BELOW 8490

SELL GUARGUM NOV BELOW 8300 TARGET 8250 8180 SL

ABOVE 8360

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

RBI Reference Rate

Currency Rate Currency Rate

Rupee- $ 64.8815 Yen-100 53.7900

Euro 72.0639 GBP 99.8851

CURRENCY

USD/INR

BUY USD/INR OCT ABOVE 64.98 TARGET 65.11 65.26 SL BE-

LOW 64.78

SELL USD/INR OCT BELOW 64.78 TARGET 64.65 64.5 SL

ABOVE 64.98

EUR/INR

BUY EUR/INR OCT ABOVE 72.11 TARGET 72.26 72.46 SL BE-

LOW 71.91

SELL EUR/INR OCT BELOW 71.82 TARGET 71.67 71.47 SL

ABOVE 72.02

CURRENCY MARKET UPDATES:

Snapping its 2-day losing streak, the rupee gained 29 paise at 64.83 against the US dollar on fresh selling of the Ameri-can currency by banks and exporters in view of recovery in equity markets. The domestic unit opened sharply higher at 64.80 as against Wednesday’s closing level of 65.12 at the Interbank forex market. During the day, the rupee hov-ered in the range of 64.95 and 64.77 before settling at 64.83, showing a gain of 29 paise or 0.45%. The currency dropped 32 paise, or 0.49%, in previous two trading days.

The trading range for the Spot USD/INR pair is expected to be within 64.40 and 65.20. Besides, local equities closed on a positive note which further helped the rupee to gain and appreciate by almost half per cent for the day.

In forward market the premium for dollar inched up on mild paying pressure from corporate. The benchmark six-month premium payable in March closed steady at 182-184 paise and for far-forward Sept, 2016, it inched up to 396-398 paise from 396-397.5 paise on Wednesday. The rupee firmed up against the pound sterling to finish at 99.88 from 100.64 previously and also moved up against the euro to 71.98 from 73.92. The domestic currency ended higher against the Japanese unit to close at 53.71 per 100 yen from 54.26.

The dollar index was traded higher by 0.09% against a bas-ket of six currencies in late afternoon trade. Globally, the euro fell to its lowest level in two months after ECB Presi-dent all but promised the central bank would expand its program of quantitative easing at its December meeting.

The U.S. dollar posted its largest weekly gain against the euro since late May on Friday, supported by interest-rate cuts in China and the promise of more stimulus in Europe.

Higher interest rates in the U.S. would increase the return on dollar-denominated deposits, making it more attractive for foreign investors. Investors reasoned that, even though the Fed might delay its first interest rate hike until 2016, monetary policy across the globe will continue to diverge.

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

CALL REPORT

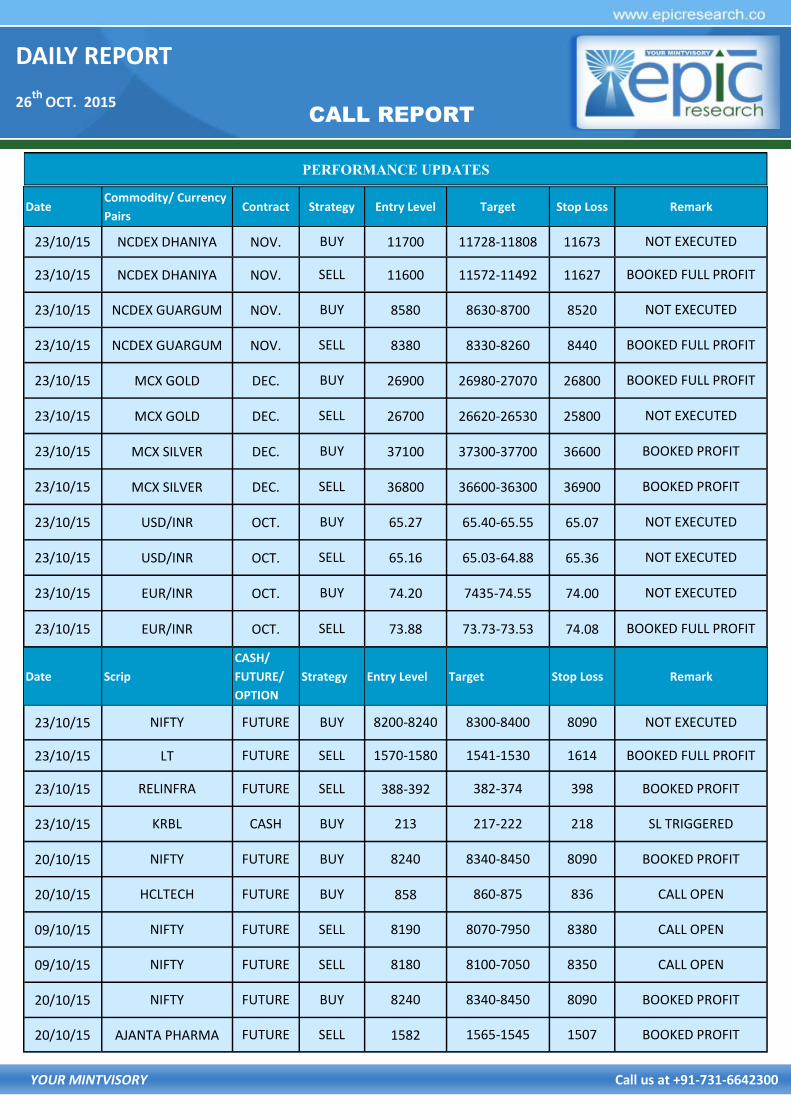

PERFORMANCE UPDATES

Date Commodity/ Currency

Pairs Contract Strategy Entry Level Target Stop Loss Remark

23/10/15 NCDEX DHANIYA NOV. BUY 11700 11728-11808 11673 NOT EXECUTED

23/10/15 NCDEX DHANIYA NOV. SELL 11600 11572-11492 11627 BOOKED FULL PROFIT

23/10/15 NCDEX GUARGUM NOV. BUY 8580 8630-8700 8520 NOT EXECUTED

23/10/15 NCDEX GUARGUM NOV. SELL 8380 8330-8260 8440 BOOKED FULL PROFIT

23/10/15 MCX GOLD DEC. BUY 26900 26980-27070 26800 BOOKED FULL PROFIT

23/10/15 MCX GOLD DEC. SELL 26700 26620-26530 25800 NOT EXECUTED

23/10/15 MCX SILVER DEC. BUY 37100 37300-37700 36600 BOOKED PROFIT

23/10/15 MCX SILVER DEC. SELL 36800 36600-36300 36900 BOOKED PROFIT

23/10/15 USD/INR OCT. BUY 65.27 65.40-65.55 65.07 NOT EXECUTED

23/10/15 USD/INR OCT. SELL 65.16 65.03-64.88 65.36 NOT EXECUTED

23/10/15 EUR/INR OCT. BUY 74.20 7435-74.55 74.00 NOT EXECUTED

23/10/15 EUR/INR OCT. SELL 73.88 73.73-73.53 74.08 BOOKED FULL PROFIT

Date Scrip

CASH/

FUTURE/

OPTION

Strategy Entry Level Target Stop Loss Remark

23/10/15 NIFTY FUTURE BUY 8200-8240 8300-8400 8090 NOT EXECUTED

23/10/15 LT FUTURE SELL 1570-1580 1541-1530 1614 BOOKED FULL PROFIT

23/10/15 RELINFRA FUTURE SELL 388-392 382-374 398 BOOKED PROFIT

23/10/15 KRBL CASH BUY 213 217-222 218 SL TRIGGERED

20/10/15 NIFTY FUTURE BUY 8240 8340-8450 8090 BOOKED PROFIT

20/10/15 HCLTECH FUTURE BUY 858 860-875 836 CALL OPEN

09/10/15 NIFTY FUTURE SELL 8190 8070-7950 8380 CALL OPEN

09/10/15 NIFTY FUTURE SELL 8180 8100-7050 8350 CALL OPEN

20/10/15 NIFTY FUTURE BUY 8240 8340-8450 8090 BOOKED PROFIT

20/10/15 AJANTA PHARMA FUTURE SELL 1582 1565-1545 1507 BOOKED PROFIT

DAILY REPORT

26th

OCT. 2015

YOUR MINTVISORY Call us at +91-731-6642300

NEXT WEEK'S U.S. ECONOMIC REPORTS

ECONOMIC CALENDAR

The information and views in this report, our website & all the service we provide are believed to be reliable, but we do not accept any

responsibility (or liability) for errors of fact or opinion. Users have the right to choose the product/s that suits them the most. Sincere ef-

forts have been made to present the right investment perspective. The information contained herein is based on analysis and up on sources

that we consider reliable. This material is for personal information and based upon it & takes no responsibility. The information given

herein should be treated as only factor, while making investment decision. The report does not provide individually tailor-made invest-

ment advice. Epic research recommends that investors independently evaluate particular investments and strategies, and encourages in-

vestors to seek the advice of a financial adviser. Epic research shall not be responsible for any transaction conducted based on the infor-

mation given in this report, which is in violation of rules and regulations of NSE and BSE. The share price projections shown are not nec-

essarily indicative of future price performance. The information herein, together with all estimates and forecasts, can change without no-

tice. Analyst or any person related to epic research might be holding positions in the stocks recommended. It is understood that anyone

who is browsing through the site has done so at his free will and does not read any views expressed as a recommendation for which either

the site or its owners or anyone can be held responsible for . Any surfing and reading of the information is the acceptance of this dis-

claimer. All Rights Reserved. Investment in equity & bullion market has its own risks. We, however, do not vouch for the accuracy or the

completeness thereof. We are not responsible for any loss incurred whatsoever for any financial profits or loss which may arise from the

recommendations above epic research does not purport to be an invitation or an offer to buy or sell any financial instrument. Our Clients

(Paid or Unpaid), any third party or anyone else have no rights to forward or share our calls or SMS or Report or Any Information Pro-

vided by us to/with anyone which is received directly or indirectly by them. If found so then Serious Legal Actions can be taken.

Disclaimer

TIME REPORT PERIOD ACTUAL CONSENSUS

FORECAST PREVIOUS

MONDAY, OCT. 26

10 AM NEW HOME SALES SEPT. 550,000 552,000

TUESDAY, OCT. 27

8:30 AM DURABLE GOODS ORDERS SEPT. -1.5% -2.3%

10 AM CONSUMER CONFIDENCE INDEX OCT. 101.0 103.0

WEDNESDAY, OCT. 28

8:30 AM ADVANCED TRADE IN GOODS SEPT. -$64.8 BLN -$67.2 BLN

THURSDAY, OCT. 29

8:30 AM WEEKLY JOBLESS CLAIMS OCT. 17 N/A N/A

8:30 AM GROSS DOMESTIC PRODUCT 3Q 2.1% 3.9%

FRIDAY, OCT. 30

8:30 AM PERSONAL INCOME SEPT. 0.2% 0.3%

8:30 AM CONSUMER SPENDING SEPT. 0.1% 0.4%

8:30 AM CORE INFLATION SEPT. 0.2% 0.1%

8:30 AM EMPLOYMENT COST INDEX 3Q 0.6% 0.2%

10 AM CONSUMER SENTIMENT INDEX OCT. -- 92.1