Embed Size (px)

Citation preview

Electricity Industry Analysis & EnerjiSa Competitive Strategy

MGMT906 Business Strategy

Team 7

Rev PA5

Page 1 / 32

EMBA 2011-2012

Koç University

MGMT906 – BUSINESS STRATEGY

Akin Garzanlı, Bora Buyruk, Dağhan Güçlü, F. Semin Bal Sözen , Hasan Basri Akırmak Graduate School of Business, Koç University

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 2 / 32

Contents

1 Electricity Industry Structure ............................................................... 3 1.1 Electricity Market Overview..................................................................... 3 1.2 Industry Description ................................................................................ 4 1.3 Supply Chain .......................................................................................... 5 1.3.1 Generation .............................................................................................. 5 1.3.2 Whole sale .............................................................................................. 6 1.3.3 Transmission .......................................................................................... 7 1.3.4 Distribution & Retail ................................................................................ 7 1.3.5 Consumers ............................................................................................. 8 1.4 Five Forces Analysis .............................................................................. 8 1.4.1 Threat of New Entrants & Substitutes ..................................................... 8 1.4.2 Bargaining Power of the Buyers & Suppliers .......................................... 8 1.4.3 Rivalry .................................................................................................... 9 1.5 Price Structure ........................................................................................ 9 1.6 Power & Profit Drivers .......................................................................... 11

2 Competitive Strategy of EnerjiSa ...................................................... 12 2.1 Company History .................................................................................. 12 2.2 Competitors .......................................................................................... 13 2.3 Competitive Advantages of EnerjiSa ..................................................... 13 2.4 Competitive Disadvantages .................................................................. 14 2.5 Sustainability Profile of EnerjiSa ........................................................... 15 2.6 Customer Value Proposition ................................................................. 15

3 Electricity Industry Structure: A Five Year Outlook ......................... 17 3.1 Changes in Supply Chain Dynamics & Profitability ............................... 17 3.1.1 Macroeconomic changes and expectations (2012-2017) ...................... 17 3.1.2 Changes & Expectations in Electricity Industry (2012-2017) ................. 17 3.1.3 Changes & Expectations in Regulatory Outlook (2012-2017) ............... 18 3.2 Intention of players to change supply change dynamics ....................... 18 3.3 Scenario for Profitability Outlook (in Generation, Distribution) ............... 18

4 Strategic Options & Recommendations ............................................ 19

5 Appendix A – Exhibits ........................................................................ 20

6 Appendix B - List of Exhibits ............................................................. 30

7 Abbreviations...................................................................................... 31

8 References .......................................................................................... 31

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 3 / 32

1 Electricity Industry Structure

1.1 Electricity Market Overview

The vertically integrated electricity market, once state owned, has been gradually going through liberalization since 1990’s [Exhibit 5-1] [1]. As of today, it has a competitive market structure with a capacity of 49,523 MW (Y2010) dominated by the private sector (except transmission).

Production

The electricity production in Turkey was 222.1 TWh in 2011 [Exhibit 5-2]. In 2011, 45.2% of total production is based on imported natural gas and 11.2% on imported coal and oil derivatives [Exhibit 5-4]. The power generation based on natural gas and coal increased between 2004 and 2010 due to Turkey’s geographic proximity to reserve holder countries (Iran, Azerbaijan, Ukraine) and the advantages in terms of efficiency and environment. The Electricity Market Regulation Authority (EMRA) has set policy measures to promote use of domestic coal, renewable as well as nuclear energy [1].

Consumption

The consumption structure is as follows [5]:

45% of the consumption by industrial customers

20.4 % is consumed by services sector

25 % by households

the remainder by other sectors and street illumination purposes.

In order to make sure that privately-produced power is sold in the free market, EMRA has been gradually reducing the eligibility threshold since 2002. As of 2011, customers consuming more than 30,000 kWh annually are allowed to have direct access to wholesale market and choose their supplier via bilateral contracts under free market conditions. This threshold corresponds to 75% of the consumers. Further reductions in eligibility threshold are expected, and by 2015 all consumers will become eligible [Exhibit 5-5] [6].

Market Dynamics

Electricity demand growth rate and GDP growth rate are highly correlated [Exhibit 5-6]. A study shows that the demand growth rate outstripped the GDP growth rate by 1.4 % on average between 2000 and 2010 [1]. As depicted in the figure below, with a demand growth rate of 55%, Turkey is the 3rd largest growth market after China and India.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 4 / 32

The recent high GDP growth of Turkey and the ambition to become world’s 10th largest economy by 2023 makes it an attractive market for domestic and foreign investors because an annual demand growth rate of 7% is forecasted until 2020 which requires 94 billion USD of investment [2].

As described above, due to dependency on natural gas; 22% of Turkey’s import budget is spent on energy inputs. 50% of Turkey’s Current Account Deficit is caused by energy imports[3] and it is continuously growing [Exhibit 5-7].

1.2 Industry Description

The growing need for energy in Turkey has been driven by growth of population, urbanization, increasing level of industrialization and economical growth. The future projections show that the demand will keep increasing [Exhibit 5-2].

Until 1970, electricity generation, transmission and distribution was being held by the private, public or private-public partnership companies. Industry reorganization took place in 1970 by the establishment of TEK (Turkish Electricity Administration). TEK was a vertically integrated establishment which controlled electricity generation, transmission and distribution as a monopoly [Exhibit 5-1].

In 1993, TEK was separated in TEAS responsible of generation & transmission and TEDAS responsible of distribution. After the enforcement of the Electricity Market Law, TEAS was further unbundled into three organizations; EUAS (Generation), TEIAS (Transmission), TETAS (Wholesale).

In 2004, Electricity Sector Strategy Paper was issued which regulates the different levels in value chain to have a competitive, efficient free market and to avoid monopolistic behavior. Furthermore in 2006, privatization of state owned distribution companies was launched which started the last phase to a full liberal market. Today, except for transmission and wholesale (TEIAS and TETAS), distribution is fully privatized.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 5 / 32

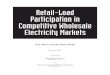

1.3 Supply Chain

T ransmission Distribution Consume rGeneration

The figure below summarizes the players, their value-add and highlights of each supply chain component.

INDUSTRY STRUCTUREELECTRICITY VALUE CHAIN

Generation Wholesale TransmissionDistribution &

Retail

Raw Materials (Coal, Gas,

Hydro, Wind)

Input materialElectricity

Production

Sales to distributors

& direct consumets

Wirelinenetwork for transmitting

electricity

Last mile access.

Customer ownership.

• 22% of import (54BUSD) is spent on energy inputs (gas & oil).

• 50% of CAD is caused by energy imports.

• Spot market for sales of output or through bilateral contracts

Consumer

Import (Iran, Russia),

Mines, Nature (Water, Wind)

EUAS.EnerjiSa

Aksa…

TETASEnerjiSa

…

Owned by government

(TEIAS)

Distribution companies(EnerjiSa,

Aksa…)

Valu

eP

layers

Hig

hlig

hts

• Government monopoly

Electricity consumption

Industry, commerce, households

• Industry consolidation

• Oligopolistic market, high concentration

• Nuclear & renewable two extreme options

• Private distribution companies

• Addressable market 32.5 Million

• Eligible customers free to select supplier (75% of all subscribers)

1.3.1 Generation

Turkey’s total installed capacity is 51,076 MW [Exhibit 5-3].

Generation is continuously being privatized. The figure below shows that the government share (EUAS) fell drastically from 85% in 1984 to 53% in 2009 [7].

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 6 / 32

In terms of input materials, the largest resource of electricity is natural gas which is almost totally imported. The second main resource of electricity in Turkey is water power. Turkey has several rivers which are very eligible to build dams. Today 503 dams are active. Third largest resource of electricity is coal, which is a local resource [Exhibit 5-10].

1.3.2 Whole sale

Wholesale market functions as follows: There are two types of wholesalers:

Public Wholesaler: Electricity Generation Company (excluding autoproducers and autoproducer groups) selling its output either through bilateral contracts or to the market.

Private Wholesaler: Private companies engaged in the wholesale, direct sale to the eligible consumers and power import & export [9].

Wholesalers primarily purchase electricity from EUAŞ in the spot market as well as the futures market. Wholesalers can make annual purchase contracts to meet contractual obligations to distribution companies, or make short notice purchases (e.g. if consumption exceed production capacity). The wholesale price of electricity can range from 0.13 TRL up to 2 TRL depending on demand conditions.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 7 / 32

1.3.3 Transmission

Transmission is not included in this study, as there is only government monopoly (TEIAS), owning the high/medium voltage wires from the generation to distribution networks. The infrastructure is shared by all players, and TEIAS charges for the infrastructure operations and maintenance costs from the distribution companies, which charge the consumer [6].

Turkish power system is synchronized with the interconnected power systems of Continental Europe.

1.3.4 Distribution & Retail

The distribution network is divided into 21 regions. The distributors purchase electricity from generators and sell it to consumers. The privatization program of the 21 distribution companies is carried on with success. The sector was totally privatized in 2010. Total privatization revenue of all distribution companies is around 15.8 billion USD [6]

Privatization Complete

Privatization Status of TEDAŞ (Distribution)

Başkent EDAŞ

Meram EDAŞ

Sakarya EDAŞ

Osmangazi EDAŞ

Çamlıbel EDAŞ

Uludağ EDAŞ

Çoruh EDAŞ

Menderes EDAŞ

Yeşilırmak EDAŞ

Kayseri EDAŞ*

Contract Pending

Yeşilırmak EDAŞ

Fırat EDAŞ

Vangölü EDAŞ

Approval Pending

Aras EDAŞ

Boğaziçi EDAŞ

Gediz EDAŞ

Trakya EDAŞ

Dicle EDAŞ

Tender Complete

İstanbul Anadolu EDAŞ

Toroslar EDAŞ

Akdeniz EDAŞ

Gediz EDAŞ was removed from the privatization portfolio in 2009

(*) Kayseri and Vicinity EDAŞ was privatized in 1990

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 8 / 32

1.3.5 Consumers

Consumers are segmented as follows. 46% of the electricity consumption is by industrial customers, while 25 % is by residential customers [5].

Total186 TWh

Total186 TWh

ConsumptionIndustrial 73 (46%)Residential 39 (25%)Commercial 23 (15%)Public 07 (04%)Public Light 04 (03%)Other 11 (07%)Total 157

TWh

ConsumptionIndustrial 73 (46%)Residential 39 (25%)Commercial 23 (15%)Public 07 (04%)Public Light 04 (03%)Other 11 (07%)Total 157

TWh

Transmission & Distribution Loss

28 TWh

Transmission & Distribution Loss

28 TWh

Source : TEIAS Capacity Projection Report, June 2009TEDAŞ Annual Report, 2009

Note : 1TWh=1 billion kWh

ExportIraq 1.21 (78%)Syria 0.33 (22%)Total 1.54 TWh

ExportIraq 1.21 (78%)Syria 0.33 (22%)Total 1.54 TWh

Auxiliary Consumption

9 TWh

Auxiliary Consumption

9 TWh

84%

1%

15%

1.4 Five Forces Analysis

1.4.1 Threat of New Entrants & Substitutes

Generation

There is very little entry threat because entry requires license to operate and heavy investment muscles. Substitution is also not an issue as direct import from other players is not possible.

Transmission

Not applicable since there is government monopoly.

Distribution & Retail

There is no more entry threat because the privatizations are complete, and the number of players are 21. Substitution is also not an issue, as there is no alternative for industrial, commercial and household consumers.

1.4.2 Bargaining Power of the Buyers & Suppliers

Generation

Natural gas, the largest raw material for electricity production is imported. The exporting countries have enormous bargaining power, they can increase prices freely, set minimum purchase amounts. For instance, Turkey and Iran had several disputes about price increases and went to arbitration recently.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 9 / 32

Distributors purchase electricity in free market conditions, therefore buyer market is competitive.

Transmission

Not applicable since there is government monopoly.

Distribution & Retail

Distributors purchase electricity in free market conditions, therefore supplier market is competitive.

75% of the eligible customers purchase electricity in free market conditions, and the remaining 25% will be able the change their distribution company in a few years. Therefore, the buyer market is competitive.

1.4.3 Rivalry

Generation

There is a competition among the private generation companies for market share, investment financing and government incentives.

Transmission

Not applicable since there is government monopoly.

Distribution & Retail

There is a competition among the distribution companies to acquire eligible customers beyond their region. The addressable market for consumers is provided in [Exhibit 5-14].

1.5 Price Structure

The main purpose of the market liberalization is to achieve lower tariffs by increasing overall system efficiency. The end-user tariffs are determined by the distribution companies and are subject to the Regulator’s approval.

The tariffs are calculated as “cost-reflective” based on predetermined operating and loss/theft improvement targets. Tariff components are as follows:

Retail sales component: It has a “price cap” which is set as the basket price of the energy purchased by the distribution company

Distribution & retail services component: It has “revenue cap” which cover OPEX and investment requirements.

Transmission component: It is a complete pass-through of transmission costs as charged by the national transmission company (TEIAS).

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 10 / 32

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 11 / 32

1.6 Power & Profit Drivers

Studying the industry price structure above reveals the following: The dashed arrows show the revenue flow:

Consumer pays the Distribution company, which pays the Transmission + Wholesale companies. Wholesale companies pay to generation companies, which further pay the raw material suppliers.

Tariff c

om

ponent

Electricity Industry DynamicsPower & Profitability

Generation Wholesale TransmissionDistribution &

RetailRaw Material

SuppliersConsumer

Reference

electricity

price

Theft & loss

tariff

Retail Svc

Opex

CoC & Deprn

Operational

rights

transfer val.

Operating

margin

Transmission

tariffBilateral

contract

or

wholesale

tariff

Passed

through to

generation

The raw material suppliers, generators, distributors and finally the consumers are increasing bargaining power:

Raw material suppliers: The market growth and the competitive environment as a result of the privatizations are expected to accelerate the electricity generation investments. The demand for natural gas is increasing since it is the most preferred energy source for the industry [Exhibit 5-12]. Increasing cost of natural gas due to import dependency causes price appreciation and search for alternative energy sources.

Generation companies: Turkish electricity demand is increasing, and investments on energy generation especially by renewable energy sources will give a competitive advantage to the big players. As with vertical integration trends, we foresee industry consolidation with mergers and acquisitions.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 12 / 32

Distribution companies: They own the customer relationship, and with eligible consumer concept, they are able acquire customers from competition. The distributors, which invest in information and communication technologies with the aim of improved operational processes can reduce their OPEX, therefore increasing margins.

Consumers: With eligibility limit concept, 75% of the consumers are able to select their supplier, and remaining 25% will be able to do the same by 2014. Competition empowers the consumers.

In summary, following power and profit drivers are concluded based on the analysis above:

Energy demand growth.

Search for alternative energy sources to avoid import dependency.

Industry vertical integration.

Industry becoming more competitive through the liberalization process.

2 Competitive Strategy of EnerjiSa

2.1 Company History

EnerjiSA was founded in 1996 in order to cover the needs of the Sabancı Group (a major player in Turkish Economy, having companies in a wide variety of sectors). In 2007, EnerjiSa signed a 50:50 joint venture agreement with Verbund, Austria's largest electric utility.

The strategic goal of EnerjisSa is being the market leader in the Turkish electricity sector a with a minimum of 10% market share by the year 2015 in a vertically integrated structure, by combining generation, distribution, supply, wholesale and trading activities.

The acquisition of Baskent in 2009, the distribution company of central Anatolia, with some 3.5 million customers, is a major milestone towards this goal. The Group is also working actively on seeking opportunities along the natural gas value chain.

Planning to attain a total installed capacity of 5,000 MW by 2015 and a six-million customer portfolio, Enerjisa has accelerated its efforts to expand and diversify its generation portfolio. In addition to the existing generation portfolio of 455 MW currently operated by Enerjisa Power Generation Company, the implementation of a well balanced generation portfolio has started. Several new hydro and wind power plants are financially committed, and are under implementation and construction.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 13 / 32

Enerjisa invests heavily in renewable energy. 2011 was announced as kick off year for renewable energy and 1000 MW renewable energy license was purchased. The largest wind power plant of Turkey on a single site is BARES, which will generate nearly 500 GWh of electricity per year.

2.2 Competitors

Major Competitors of EnerjiSA can be listed as follows:

Aksa Elektrik Toptan Satış A.Ş.

Akenerji Elektrik Üretim A.Ş.

Limak Yatırım, Enerji Üretim İşletme Hizmetleri ve İnşaat A.Ş.

Akköy Enerji A.Ş. (Kolin)

A brief comparison can be seen below table: AKSA * Akenerji * Limak Kolin EnerjiSA

Installed Capacity (MW) 2.036,00 686,00 429,00 297,00 1.642,00

Establishment Date 1997 1989 1997 1999 1996

Market Share 2011 3,10% 2% - - -

Number of facilities 40 9 5 2 11

Revenue (2011) 1.307.427.464,00 559.970.769,00 - - -

Distribution Areas Çoruh - Fırat Sakarya Uludağ Çamlıbel Başkent

Consumption 11.409.334,00 8.405.333,00 11.049.990,00 2.146.351,00 11.134.261,00

* Traded at the exchange

For brevity, the company profiles are not included in this report, they can be obtained from the corporate web sites.

2.3 Competitive Advantages of EnerjiSa

Joint venture of two large industrial groups

Sabanci group is present in financial services, energy, cement, retail and industry as primary sectors of operation. In 2011, the consolidated revenue of Sabancı Holding was TL 22.4 billion (US$ 13.4 billion) with EBITDA of TL 4.5 billion (US$ 2.7 billion) [[16].

The group invested 53% of their 2011 investment portfolio to the Energy Group [Exhibit 5-15]

Sabancı group’s joint venture partner for Enerjisa, Verbund is one of the leading electricity companies in Europe. Verbund is Austria’s largest power generation company and one of the most valuable companies. Verbund has its major concentration to the Turkish market with Enerjisa [Exhibit 5-16].

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 14 / 32

Turkey is a High Growth Market

Turkey is one of the highest growing economies globally and energy demand increase is in parallel, which gives energy investors a high business potential. From a global perspective, it is a unique advantage for Enerjisa and Verbund to be in the Turkish market. As one of the largest conglomerates of Turkey, EnerjiSa can best exploit this growth potential.

Advantage of investments in Renewable energy

Turkey has in renewable energy category important areas to growth. Only 1/3rd of the hydro potential, and 2/3rd of the wind potential is utilized [Exhibit 5-17]. Enerisa has the goal to be the largest largest renewable energy supplier with no dependency on natural gas imports [15].

In visible future 30 % of Enerjisa’s generation will be renewable [16]. Enerjisa started construction of a major wind power plant in Turkey. The 142.5 MW BARES wind power plant will be one of the largest wind power plants of Turkey when completed (expected by second half 2012) [15].

2.4 Competitive Disadvantages

Distribution: No acquisition strategy in Electricity Retail Customers

For instance, EnerjiSa is the 3rd largest distributor with 12% market share. The addressable market share for EnerjiSa can go hypothetically up to 75% (eligible consumers). Defining the right target group would be the right focus for EnerjiSa since it has important unique advantages comparing to its competitors. However, in their current strategy we could not identify actions of an acquisition goal.

0

20

40

60

80

100

2011 2014 2017 2020

EnerjiSa

Eligible

Consumers

50/50 Joint Venture can complicate decision making process

Sabanci Group is used to running 50/50 joint ventures in other industies like automorive. However, Electricity market is highly local, and this structure may slow down the decision making process.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 15 / 32

2.5 Sustainability Profile of EnerjiSa

The sustainability profile of EnerjiSa is illustrated below. In terms of size dimension, EnerjiSa has scale and learning advantage. In terms of the time dimension, it has the installed base and trial cost/time advantage. Overall, we believe EnerjiSa has Size dimension as the main competitive advantage.

EnerjiSa

Resources & Skills

Size Time

Efficiency

Scale

Scope

Learning

Bargaining power

Buyers

Supplier

Network effect

Installed base (3rd largest customer

base, Baskent is one of the biggest regions,

customer satisfaction).

Complementary products (Same

for all players)).

Experience effects

Trial cost / time (Operational

effcoemcy )

Durability

Absolute

preemption

Relative:

Time / Cost penalties

Legal: License to operate.

Physical: -

Mental: -

+

+

-

+

+

+

(Ambitions for 2015)

(From acqsn & partnership)

No bargaining power because of

regulation

Very weak as natural gas is the

main input resource

+

2.6 Customer Value Proposition

EnerjiSa shall approach large and medium enterprises (both industrial and commercial), with a customer value proposition as follows: `The EnerjiSa renewable energy helps my sustainability goal. I switch to Enerji Sa to make my energy consumption greener.`

Targets shall be the BIG FISH first!

Large Companies: For large corporations with monthly bill of 75,000TL or higher, and are willing to find the most competitive and green solution for their corporation.

Middle Enterprises: Entrepreneurs looking for the best solution for their companies and are interested for external consultancy for energy efficiency.

The positioning of the customer benefits are:

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 16 / 32

CORE COMPETENCE

FUNCTIONAL BENEFITS

EMOTIONAL BENEFITS

Renewable

Energy: Better

future for

tomorrow

Decreased

carbon

footprint

Marketing

benefit for the

company

Comfort of

protecting

environment

The financial benefits of this value proposition are calculated below (Calculation is from our group assignment on MKTG901 Marketing Management Course, Koç EMBA 2012

Spring 2012).

Source of VolumeAcquisition / Steal Share Strategy

BodiesTotal Electricity Customers 32.000.000

Eligible customers 75*%

Total Acq / Steal S Customers 24.000.000

% who consider dynamic variable important 71**%

Acquisition population 16.000.000

Behaviours% probability of conversion 21**%

New customer stolen/transferred 3.000.000

Avg $ units/yr consumed by stolen/transferred customers (460 T x12 months ~=5500TL -> ~3000 Usd)

BucksTotal $ Rev from Aqcuired Customers 9 Billion USD

* Reference: See [2][3], enerjisa.com.tr

** 2011 Yeşil Tüketim Araştırması [8]

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 17 / 32

3 Electricity Industry Structure: A Five Year Outlook

3.1 Changes in Supply Chain Dynamics & Profitability

3.1.1 Macroeconomic changes and expectations (2012-2017)

Turkey is world’s 16th largest economy. The 2023 vision of Turkey is to become the world’s 10th largest economy in the 100th anniversary of the Turkish Republic. Since 2002, Turkey has been showing economic growth except for 2009. [Exhibit 5-19] [17].

The growth rate of 8,5 % in 2011 is a striking success; because after China, Turkey had the second largest growth rate in the world. Forecasted growth rates for upcoming three years are lower than 2011 growth rates of Turkey, but compared to many European countries and US, Turkey’s growth rate is expected to be larger [Exhibit 5-20] [18].

Like all other global countries Turkey was affected in 2008 crisis, but recovered well in a short time period. This sharp recovery enables Turkey to break away from many European countries and made it a distinguishing star. Although four years have passed still some countries like Greece could recover and there is not much of a sign of hope.

While Europe is struggling with economic crisis, the Arab spring shaked the ground for the long term leaders and costed them regime breakdowns

Countries like Egypt, Libya, Algeria, Yemen, Bahrain, Tunisia and Syria faced the affects. The uprisings impacted the economies badly. Imports, exports and investments were halted.

The global economic crisis, the Arab Spring and the depression in EU countries served Turkey a lot. Foreign investment funds are coming in, exports to emerging countries of Africa, Middle East and Asia is increasing.

3.1.2 Changes & Expectations in Electricity Industry (2012-2017)

Energy will be a hot topic for the 2023 vision.

Turkey plans to have nuclear energy until 2020.

Government provides incentives for renewable energy investments.

Distribution companies are incentivized to make investments on operational efficiency. In 2012, it is expected to start deployment of Automated Meter Reading (AMR) and Smart Metering solutions.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 18 / 32

The electric vehicle market is just starting in Turkey. Renault produces Electric Cars ( Fluence ZE - Zero Emission) in Turkey, and major municipalities and some governmental institutions are already using it (very few). Starting from September 2012, it will be purchasable by everyone [19]. There are tax subsidies to EV cars. Istanbul Municipality is testing charging stations in parking lots. In the Electricity Market Distribution Regulation, an amendment is specified to allow the fast, medium fast and slow charging units to be installed to charge the electrical vehicles are connected to the system [4].

3.1.3 Changes & Expectations in Regulatory Outlook (2012-2017)

Electricity market liberalization will be concluded. Privatization of the remaining generation infrastructure will continue.

Regulations are created to promote Energy efficiency: Starting from 2011, all new buildings will have an Energy Certificate. As of 2011, micro-generation, producing unlicensed electricity for own use is allowed. The excess energy can be sold to the electricity grid.

3.2 Intention of players to change supply change dynamics

We don’t see a risk of changing supply chain dynamics. As explained in this report, the electricity value chain is highly regulated and many activities are subject to license.

3.3 Scenario for Profitability Outlook (in Generation, Distribution)

Average loss / theft rate of Turkey is around 40% which is a high figure. In some regions, this amount goes up to 80% (Dicle Region). Today, the revenue loss is distributed to customers. The cost of theft is charged from everyone. In a few years, this will be discontinued. It is expected that distribution companies setup the IT systems to avoid theft.

Electricity production is calculated based on historical data, and meteorological forecasts. If the demand and supply does not match, either energy is wasted (excess electricity supply cannot be stored), or distribution company has to buy additional electricity from the spot market (this can be expensive if the demand is high). Smart grid prevents both by providing bidirectional communication between the generators and the consumers.

Electricity generation from renewable resources decrease input costs drastically.

Distribution companies shall transform to service providers. They shall create different tariffs to address different customer segments.

We believe, companies shall investigate renewable energy sources, and implement information technologies to decrease OPEX, increase margins and aim customer satisfaction.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 19 / 32

4 Strategic Options & Recommendations

The existing strategic goals in 10% market share and the fast momentum in renewable energy investments are perfect way forward from a business perspective. The former will make EnerjiSa the market leader – an advantage when further industry consolidation will take place-, and the latter will shield EnerjiSa from price appreciation risks on natural gas.

In addition, we recommend the following way forward to EnerjiSa:

1. Create a brand out of renewables: Having a substantial potential for the renewable energy resources, Turkey ranks seventh in the world and first in Europe in terms of geothermal energy. Turkey also aims at further increasing its use of hydro, wind and solar energy resources. Turkey envisages producing 30% of its electricity need from the renewables by 2023. Europe 2020 plans contains to raise renewable energy consumption from 11.7% to 20% by 2020, decrease carbon emissions by 20%. This gives an opportunity for EnerjiSa to create an ambitious marketing objective and highlight more its plans about renewable energy. Renewables can be used as a positioning statement to acquire customers, to create a brand image that is linked with sustainable development of Turkey. For instance, e-On in Germany is running a very long term marketing program focusing on children at Kindergarten age. They will be the consumers in 20 years [20].

2. Analyze the impact of nuclear in Turkey: To Compete or to Cooperate? Nuclear is on the agenda of Turkey. Turkey envisions reducing dependency on imported fossil fuels through the sequential commissioning of nuclear power into the Turkish electricity grid. In this respect, Turkey intends to establish around more than 10.000 MW of nuclear capacity by 2030. There is an already signed an intergovernmental agreement with the Russian Federation concerning the construction and operation of a nuclear power plant at the Akkuyu site. Turkey supplies 74 percent of its energy needs with petroleum and natural gas, of which 90 percent are imported. This planned nuclear plant will meet 17 percent of Turkey’s energy demands by itself, helping reduce the dependence on foreign gas and oil. On the other side, nuclear energy is criticized especially due to the disaster happened in Fukushima by 2011. The existing Verbund Joint Venture does not cover nuclear energy investments. The impact of nuclear energy in the electricity supply chain shall be studied: Does EnerjiSa want to be present in this domain? Shall EnerjiSa compete or cooperate?

3. Investigate Business Potential in Electric Vehicle Charging Network: Electric Vehicles will disrupt the transportation industry. It has a host – complement relationship with the electricity distribution network. EV charging stations are required for adoption of EVs. In Europe and US, the automotive industry is working closely with electricity service providers to create a critical mass of charging stations. EnerjiSa, shall investigate the business potential in this area.

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 20 / 32

5 Appendix A – Exhibits

1970

1994

2001

20032004

2007

TEKGeneration, Transmission, Distribution

TEASGeneration, Transmission

TEDASDistribution

EUASGeneration

TEDASDistribution

TEIASTransmission

TETASWholesale

ADUAS(2008)

ADUAS(2008)

EUASRiver plantsPriority PPs

Gen. portfolios

EUASRiver plantsPriority PPs

Gen. portfolios

Year Market Structure Legislative Milestones

2010

Legal Framework set up with new Energy Law Unbundling of TEAS EMRA Established as Market Regulatory Body

2008 Amendmends to Energy Law

2009

Split of Distribution

Electricity Market and Security Supply Strategy Issued

All Privatization tenders complete. Transition in WIP. Consumers >0.1Gwh/y. are free to choose their supplier

Privatization of Generation Companies Started

Gradual opening of Market. Consumers >9Gwh/year are free to choose their supplier

Unbundling of TEDAŞ with Privatization Programme

2011 All industrial consumers will be free to choose supplier

All non industrial consumers wiil be free to choose supplier by 2014

Public17

Private4

Public15

Private6

Public11

Private10

21 Dis. Co. Under TEDAS

Source : TETAŞ 2009 Annual Report, Privatization Board Information Memorandum, 2010

Establishment of TEK with Law No 1312

Exhibit 5-1 – History of Liberalization – Turkish Electricity Industry

Exhibit 5-2 – Electricity Demand Projection (2010-2019)

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 21 / 32

Exhibit 5-3 – Turkey’s Installed Capacity according to generation type (2011)

Exhibit 5-4 – Turkey’s Breakdown of Electricity Generation (2011)

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 22 / 32

Exhibit 5-5 – Eligibility Threshold- Market Openness

Exhibit 5-6 – GDP vs Electricity Demand Growth Rates

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 23 / 32

Exhibit 5-7 – Current Account Deficit – Energy (red) and Others (blue) (2010-2012 Quarterly)

List of Players in Electricity Wholesale TETAŞ ( Türkiye Elektrik Ticaret ve Taahhüt A.Ş.) EFT Elektrik Enerjisi İthalat İhracat ve Toptan Satış A.Ş. Büyük Potansiyel Elektrik Enerjisi Toptan Satış A.Ş. Ata Elektrik Enerjisi Toptan Satış Limited Şirketi GENT Elektrik Enerjisi Toptan Satış A.Ş. Hidiv Elektrik Enerjisi Toptan Satış A.Ş. Can Enerji Toptan Elektrik Ticaret A.Ş. Setel Elektrik Enerjisi İhr.İth. Ve Toptan Satış Ltd. Şti. Enko Toptan Elektrik Enerjisi Ticaret A.Ş. EGL Elektrik Toptan Ticaret A.Ş. Gates Elektrik Enerjisi Toptan Satış A.Ş. Bir Enerji Elektrik Toptan Satış İthalat İhracat A.Ş. Nuh Enerji Elektrik İthalat İhracat ve Toptan Tic.A.Ş. Ado Elektrik Enerjisi İthalat İhracat ve Toptan Satış A.Ş. AES- IC İçtaş Elektrik Toptan Satış ve Ticaret Anonim Şirketi D Tes Elektrik Enerjisi Toptan Satış A.Ş. TGR Enerji Elektrik Toptan Ticaret A.Ş. Atom Elekt. Enerjisi İth. İhracat San. ve Toptan Satış Tic. A.Ş. Unit Elektrik Enerjisi Toptan Satış İhracat ve İthalat A.Ş. Mega Toptan Elektrik Ticareti A.Ş. Park Toptan Elektrik Enerjisi Satış San. ve Tic. A.Ş. Akenerji Elektrik Enerjisi İthalat İhracat ve Toptan Tic. A.Ş. Eltek Elektrik Enerjisi İthalat İhracat ve Toptan Ticaret A.Ş. Aksa Elektrik Toptan Satış A.Ş. Ayen Elektrik Tic. A.Ş. Enerjisa Elektrik Enerjisi Toptan Satış A.Ş. Türkmenin Altın Asrı Elektrik Enerjisi Toptan Satış A.Ş. Marmara Elektrik Enerjisi İthalat İhracat ve Toptan Tic. A.Ş. Şavk Elektrik Enerjisi Toptan Satış A.Ş. Enimeks Elektrik Enerjisi Toptan Ticaret A.Ş. Zorlu Elektrik Enerjisi İthalat, İhracat ve Toptan Tic. A.Ş. Sönmez Enerji Elektrik Toptan Ticaret A.Ş. KARTET-Karadeniz Elektrik Toptan Ticareti A.Ş. Turcas Elektrik Toptan Satış A.Ş. Transpower Enerji Elektrik Toptan Satış A.Ş.

Exhibit 5-8 – List of Players in Electricity Wholesale

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 24 / 32

Exhibit 5-9 – Stages in the history of the Turkish Electricity Market

Exhibit 5-10 – Allocation of actual generation among types (2011)

Exhibit 5-11 – Electricity Input Material (Natural Gas) Import Contracts

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 25 / 32

Current Contracts Amount (Billion

Sm3/year) Contract Date Period (Years) State

Russian Fed 6 14.02.1986 25 Extended 1 year

Algeria (LNG) 4 14.04.1988 20 Active

Nigeria (LNG) 1,2 09.11.1995 22 Active

İran 10 08.08.1996 25 Active

Russia 16 15.12.1997 25 Active

Russia 8 18.02.1998 23 Active

Turkmenistan 16 21.05.1999 30 Passive

Azerbaijan 6,6 12.03.2001 15 Active

Exhibit 5-12 – Evolutuion of Electricity Energy Sources in Turkey

Exhibit 5-13 – List of Distribution Companies in the Value Chain

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 26 / 32

Exhibit 5-14 – Number of Subscribers per Distribution Companies

Exhibit 5-15 – Sabanci Group – Investment Portfolio

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 27 / 32

Exhibit 5-16 – Verbund Group – Investment Portfolio

Renewable Energy Resource

Gross Potential (Gwh/Year)

Technicaly Feasible Potential (Gwh/Year)

Economicaly Feasible Potential (Gwh/Year)

Current Usage (Gwh/Year)

Usage Percentage

Wind 400 124 98 61 62%

Hydro 430 - 450 215 100 - 130 35 30%

Geothermal 16 8* 4** 0,89 23%

Biogas 1,58 0,79* 0,4** 0,067 17%

Sun 365 182* 91** 4,07 4,5%

* Half of Gross Potential

** Half of Technical Potential

Exhibit 5-17 – Renewable Energy Potential in Turkish Electricity Industry

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 28 / 32

Exhibit 5-18 – Electricity Consumption by Customer Segment (1980-2004)

Exhibit 5-19 – Turkey’s Growth Rate (2002-2014)

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 29 / 32

2011 2012 2013

World 3,60% 3,40% 4,20%

OECD 1,80% 1,60% 2,20%

ABD 1,70% 2,40% 2,60%

Japan -0,70% 2,00% 1,50%

Euro Zone 1,50% -0,10% 0,90%

Germany 3,10% 1,20% 2,00%

France 1,70% 0,60% 1,20%

Italy 0,50% -1,70% -0,40%

Spain 0,70% -1,60% -0,80%

Portugal -1,60% -3,20% -0,90%

Greece -6,90% -5,30% -1,30%

Ireland 0,70% 0,60% 2,10%

Britain 0,70% 0,50% 1,90%

Canada 2,50% 2,20% 2,60%

Exhibit 5-20 – Economic Growth Forecast (2012-2013) – Developed Countries

Exhibit 5-21 – Europe 20/20/20 Act

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 30 / 32

6 Appendix B - List of Exhibits

Exhibit 5-1 – History of Liberalization – Turkish Electricity Industry 20

Exhibit 5-2 – Electricity Demand Projection (2010-2019) 20

Exhibit 5-3 – Turkey’s Installed Capacity according to generation type (2011) 21

Exhibit 5-4 – Turkey’s Breakdown of Electricity Generation (2011) 21

Exhibit 5-5 – Eligibility Threshold- Market Openness 22

Exhibit 5-6 – GDP vs Electricity Demand Growth Rates 22

Exhibit 5-7 – Current Account Deficit – Energy (red) and Others (blue) (2010-2012 Quarterly) 23

Exhibit 5-8 – List of Players in Electricity Wholesale 23

Exhibit 5-9 – Stages in the history of the Turkish Electricity Market 24

Exhibit 5-10 – Allocation of actual generation among types (2011) 24

Exhibit 5-11 – Electricity Input Material (Natural Gas) Import Contracts 24

Exhibit 5-12 – Evolutuion of Electricity Energy Sources in Turkey 25

Exhibit 5-13 – List of Distribution Companies in the Value Chain 25

Exhibit 5-14 – Number of Subscribers per Distribution Companies 26

Exhibit 5-15 – Sabanci Group – Investment Portfolio 26

Exhibit 5-16 – Verbund Group – Investment Portfolio 27

Exhibit 5-17 – Renewable Energy Potential in Turkish Electricity Industry 27

Exhibit 5-18 – Electricity Consumption by Customer Segment (1980-2004) 28

Exhibit 5-19 – Turkey’s Growth Rate (2002-2014) 28

Exhibit 5-20 – Economic Growth Forecast (2012-2013) – Developed Countries 29

Exhibit 5-21 – Europe 20/20/20 Act 29

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 31 / 32

7 Abbreviations

EPDK Electrik Piyasası Denetleme Kurumu

EMRA Electricity Market Regulation Authority

TEDAŞ Türkiye Elektrik Dağıtım Anonim Şirketi

TEİAŞ Türkiye Elektrik İletim Anonim Şirketi

TETAŞ Türkiye Elektrik Ticaret Taahhüt Anonim Şirketi

8 References

[1] Turkish Electricity Market - Investors Guide.pdf

[2] http://www.hurriyet.com.tr/ekonomi/20563314.asp

[3] http://www.internethaber.com/enerji-akaryakit-elektrik--398808h.htm

[4] EMRA, 2011

[5] TEDAS, 2011

[6] Overview of the Turkish Energy Market, 2011, EMRA

[7] turkey-en_er_ElektrikEPiyasasi2010_221010.pdf Deloitte

[8] Electricity Market & the Security of Supply Strategic Paper, 2009

[9] PWC – Electricity Industry in Turkey, 2008

[10] Market report TETAŞ

[11] http://www.turcas.com.tr/en/yazi.php?id=6

[12] http://www.infogrok.com/index.php/company-profiles/energy/trakya-elektrik-

uretim-ve-ticaret-a.s.html

[13] http://www.borusanenbw.com.tr/en/Corporate/BorusanEnBWEnergy.aspx

[14] Ref: http://www.zoren.com.tr/en/companies/companies1.asp

[15] Turkey’s Potential in Terms of Sustainable Energy (TÜRKİYE’ NİN YENİLENEBİLİR ENERJİ KAYNAKLARI VE HİDROELEKTİRİK ENERJİ POTANSİYELİ Turgut GÖREZ* AHMET ALKAN* Dokuz Eylül Üniversitesi)

Electricity Industry Analysis & EnerjiSa Competitive Strategy

Page 32 / 32

[16] Source:Sabancı Group 2011 Annual Report http://www.sabanci.com.tr/pdf/2011en/sa_fr_2011_en.pdf

[17] http://www.hazine.org.tr/tr/index.php/ekonomi/ueretim-ve-bueyueme

[18] http://www.cnnturk.com/2012/ekonomi/genel/05/22/oecdden.turkiye.icin.buyume.tahmini/661917.0/index.html

[19] http://www.renault-ze.com/tr/#/tr.html

[20] http://www.eon.com/content/dam/eon-com/en/downloads/e/E.ON_CSR_2004_en.pdf