Embed Size (px)

Citation preview

beyond accounts

What can EIS & Seed EIS do for your business?

Presentation by Peter Hedgethorne & Laura Salt

beyond accounts

Introduction

• Introduction – Peter Hedgethorne & Laura Salt

• Attendees to introduce themselves & advise what they hope to take away from today

• Brief outline of the format for today

beyond accounts

Find out how the process works

• What is EIS & how does it work?

• What is different about Seed EIS?

beyond accounts

What are the rules for EIS?

• History – Business Start Up Scheme, BES, EIS (Major –1990s)

• Individual investor limit - £1m pa 2013/14

• Company investment limit - £5m pa 2013/14

beyond accounts

What are the rules for EIS?

• Income tax relief for investor - 30%, can be carried back subject to p/y limit

beyond accounts

EIS Relief Example

Gross investment in EIS shares £10,000

Income tax relief at 30% £3,000

Net cost of EIS investment £7,000

beyond accounts

What are the rules for EIS?

• Capital gains on disposal of shares after 3 years are exempt

beyond accounts

What are the rules for EIS?

• Income tax relief available on losses on disposal of shares, net of income tax relief obtained

EIS Relief Example:Loss Relief

• You may also have claimed capital gains deferral

relief of £2,800

beyond accounts

What are the rules for EIS?

EIS Relief Example:Capital Gains Deferral Relief

NB The deferred charge of £2,800 is brought back into charge when the EIS shares are disposed of but investors have an opportunity to defer this again

by reinvesting in another EIS company.

Assumes top rate CGT of 28%

Can apply to gains 3 years before or

1 year after investment

beyond accounts

What are the rules for EIS?

• Tax relief clawed back if company rules not met for 3 years

• Paid directors and employees excluded, unless director where entitlement to payment starts after issue of shares (business angels)

• Individual can have no more than 30% of shares/votes/capital – includes associates’ rights (ancestors/descendants/spouses)

• Company employees – less than 250

• Company gross assets - £15m before and £16m after

beyond accounts

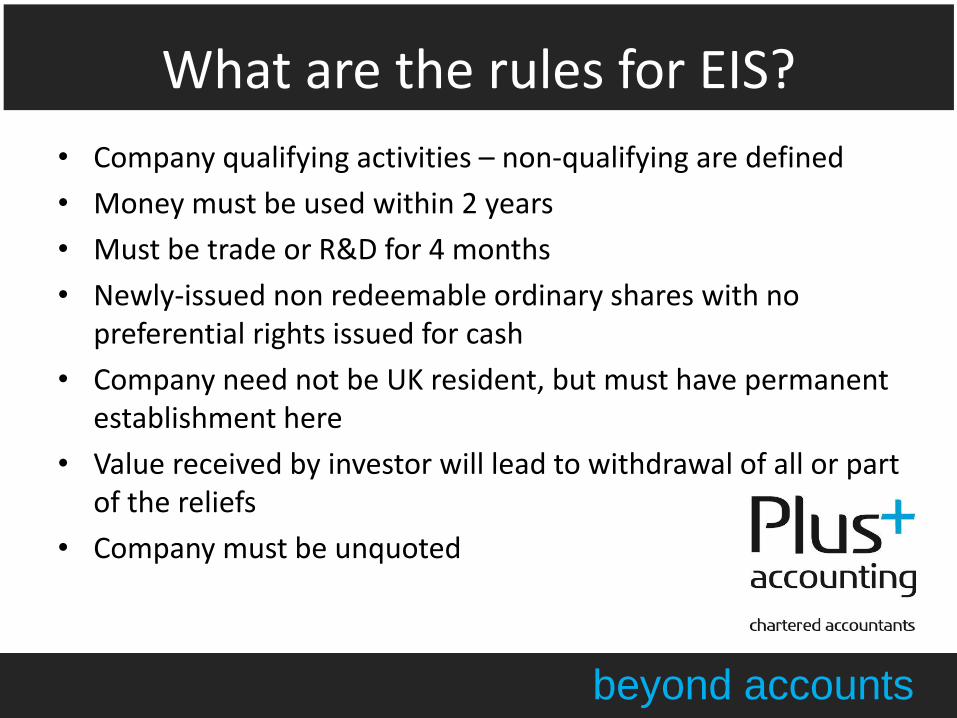

What are the rules for EIS?

• Company qualifying activities – non-qualifying are defined

• Money must be used within 2 years

• Must be trade or R&D for 4 months

• Newly-issued non redeemable ordinary shares with no preferential rights issued for cash

• Company need not be UK resident, but must have permanent establishment here

• Value received by investor will lead to withdrawal of all or part of the reliefs

• Company must be unquoted

beyond accounts

What are the rules for SEIS?

• History – From April 2012 and originally until April 2017, now indefinite.

• Individual investor limit - £100k pa 2013/14

• Company investment limit - £150k pa 2013/14

beyond accounts

What are the rules for SEIS?

• Income tax relief for investor - 50%, can be carried back subject to p/y limit

beyond accounts

SEIS Relief Example

Gross investment in SEIS shares £10,000

Income tax relief at 50% £5,000

Net cost of SEIS investment £5,000

beyond accounts

What are the rules for SEIS?

• Capital gains on disposal of shares after 3 years are exempt

SEIS Relief Example:

Capital Gains Tax Relief

beyond accounts

What are the rules for SEIS?

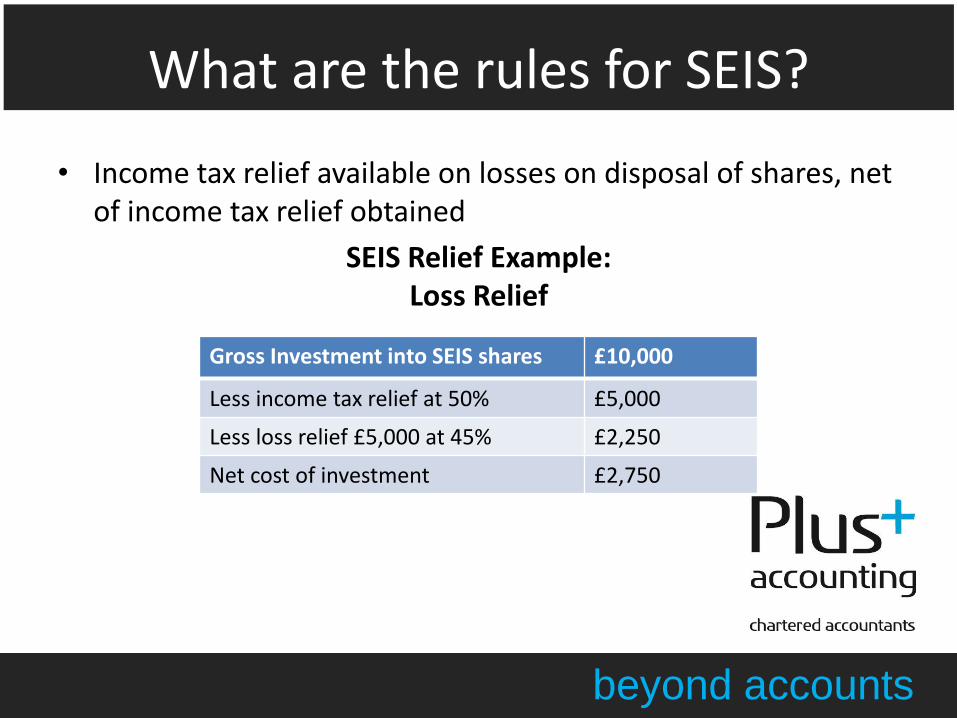

• Income tax relief available on losses on disposal of shares, net of income tax relief obtained

SEIS Relief Example:Loss Relief

Gross Investment into SEIS shares £10,000

Less income tax relief at 50% £5,000

Less loss relief £5,000 at 45% £2,250

Net cost of investment £2,750

beyond accounts

What are the rules for SEIS?

SEIS Relief Example:Capital Gains Exemption

Assumes top rate CGT of 28%

Applies to gains made in year of investment

Gross Investment into SEIS shares £10,000

Less income tax relief at 50% £5,000

Less capital gain exemption £1,400

Net cost of investment £3,600

beyond accounts

What are the rules for SEIS?

• Tax relief clawed back if company rules not met for 3 years

• Employees and their associates (ancestors/descendants/spouses) excluded, but not directors even if already paid.

• Individual can have no more than 30% of shares/votes/capital – includes associates’ rights

• Company employees – less than 25

• Company gross assets - £200k before investment

• Company must not have been trading for more

than 2 years

beyond accounts

What are the rules for SEIS?• Company qualifying activities – non-qualifying are defined

• Company must use money within 3 years

• Company must use 75% of invested funds before relief can be allowed

• Newly-issued non redeemable ordinary shares with no preferential rights issued for cash

• Company need not be UK resident, but must have permanent establishment here

• Company must be unquoted

• Value received by investor will lead to withdrawal

of all or part of the reliefs

beyond accounts

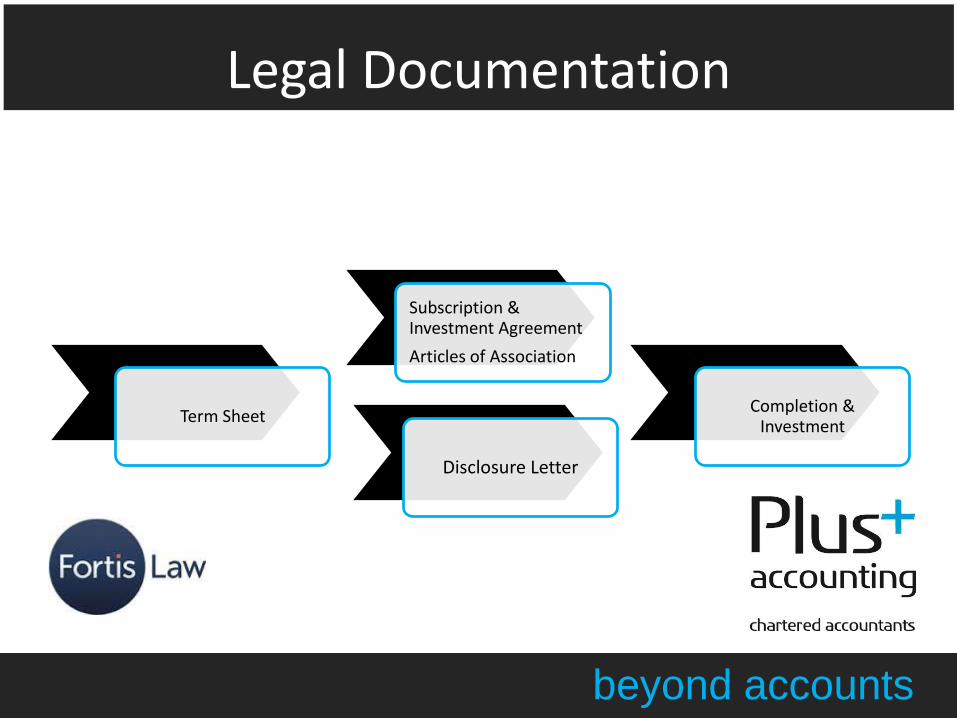

Legal Documentation

Term Sheet

Subscription & Investment Agreement

Articles of Association

Completion & Investment

Disclosure Letter

beyond accounts

Term Sheet/ Heads of Terms

• Key Financial & Legal Terms

– Subscription Price & Investment Schedule*

– Conditions Precedent*

– Completion timetable*

– Confidentiality

– Exclusivity

– Costs• Generally NOT legally binding*

beyond accounts

Common Drafting Pitfalls

Common Pitfalls

“Qualifying Trade”

Independence

Timings

Connected Parties

Use of Money Raised

Requirement

Companies in “Difficulty”

beyond accounts

Subscription & Investment Agreement

Key Consideration Issues

Decision Making • Founder -v- Investor Control• Flexible -v- Rigid Reporting• Reserved Matters• Deadlock

Investor Protection • Warranties/Indemnities• Anti-dilution• Tag Along provisions• Access to Information• Restrictive Covenants

Founder Protections • Board Protection• Drag Along• Good Leaver/Bad Leaver

Exit Longstop date

beyond accounts

Disclosure - EIS

Purpose

•Investor Protection against wrongful inducement•Complete and accurate disclosure of the condition of the company and its history•Limitation of liability•Liability for breach of warranty to the extent disclose•Warranty –v- Indemnity protection

Scope

• Legal Status

• Accuracy of Financial Statements

• Business Plan

• Assets including IP

• Liabilities

• Material Contracts

• Litigation

beyond accounts

Completion

Investor Board Minutes

Shareholder Consents

• Issue of Shares

• Adoption of articles

Point of Investment & Payment for

Shares

Execution of Documents

beyond accounts

Costs involved?

• We will briefly explain the costs for the work completed by both Accountants & Solicitors

• It is important that you advise both your Accountant & Solicitor from the outset so that they work can together.

beyond accounts

Any comments?

Do you have any questions about any of the matters discussed today?

We appreciate that this topic is complex and some of the issues you have may need to be discussed at a later date.

Contact details:

Thank you for listening.

Disclaimer: The information in this presentation is an overview and

does not contain all information necessary to action EIS & SEIS.