Embed Size (px)

Citation preview

1

GST AND ECOMMERCE

By: Ca Sanjay GuptaPh:[email protected]

M/s Sanjay Ram Shanker & AssociatesChartered Accountants

2

3

ASSOCHAM REPORT ON E COMMERCE IN INDIA

• E-commerce market in India will likely to touch $38 billion mark in 2016, a huge 67 per cent jump over the $23 billion revenues for 2015, reveals the ASSOCHAM latest paper. The industry has witnessed an unprecedented growth of 52 per cent over 2015 and has emerged as one of the fastest growing sectors. “Increasing internet and mobile penetration, growing acceptability of online payments and favorable demographics has provided the e-commerce sector in India the unique opportunity to companies connect with their customers”, adds ASSOCHAM paper.

• India's e-commerce market was worth about $3.8 billion in 2009, it went up to $17 billion in 2014 and to $23 billion in 2015 and is expected to touch whopping $38 billion mark by 2016

4

NASSCOM ON E COMMERCE

5

E Commerce models under FDI• E-commerce activities Sector FDI Cap Entry Route E-commerce activities 100% Automatic • 1 Subject to provisions of FDI Policy, e-commerce entities would engage only in Business

to Business (B2B) e-commerce and not in Business to Consumer (B2C) e-commerce. • Definitions: i) E-commerce- E-commerce means buying and selling of goods and services

including digital products over digital & electronic network

• ii) Inventory based model of e-commerce- Inventory based model of e-commerce means an e-commerce activity where inventory of goods and services is owned by e-commerce entity and is sold to the consumers directly.

• iii) Marketplace based model of e-commerce means providing of an information technology platform by an e-commerce entity on a digital & electronic network to act as a facilitator between buyer and seller.

E-commerce marketplace may provide support services to sellers in respect of warehousing, logistics, order fulfillment, call centre, payment collection and other services.

6

Various models of E commerce in India

• Inventory based Model• Market Place Model• Aggregators-“aggregator” means a person, who

owns and manages a web based software application, and by means of the application and a communication device, enables a potential customer to connect with persons providing service of a particular kind under the brand name or trade name of the aggregator;-like Ola,Uber etc.

7

Problems of E commerce under current indirect tax regime -Entry Tax & Multiple rate of taxes

• The Supreme Court, in a historic judgment of Jindal Stainless Steel Ltd. vs Union of India pronounced IN Nov,2016 has upheld the validity of entry tax legislations.

• Multiple rate of tax exists across India in various States for same products

8

Problems-VAT

DUAL TAXATION: Interstate sales are taxable in the state from which

goods commence their interstate movement; however, states into which e-commerce consignments are delivered often seek to tax the sale citing conclusion of sale upon delivery in their states. This issue is particularly more convincing in cases of sale on approval basis including cash on delivery sales (where the customer accepts the consignment upon payment at the stage of delivery of goods)

9

AMAZON- KARNATAKA VAT ISSUE

• The term dealer is defined under Section 2(12) of the Karnataka Value Added Tax Act, 2005 as under (relevant portions only):

• 'Dealer' means any person who carries on the business of buying, selling, supplying or distributing goods, directly or otherwise, whether for cash or for deferred payment, or for commission, remuneration or other valuable consideration, and includes-

• (c) a commission agent, a broker or del credere agent or an auctioneer or any other mercantile agent by whatever name called, who carries on the business of buying, selling , supplying or distributing goods on behalf of any principal;

• Karnataka VAT authorities are of the view that in such cases, the e-commerce companies are involved in supplying and distribution of goods and, therefore, would qualify as ‘dealers’.. The authorities are also of the view that these companies act as commission agents or consignment agents of sellers. Therefore, these companies are covered under the definition of ‘dealers’ and, therefore, are liable to discharge VAT

• Further, the authorities in Karnataka are insisting that e-commerce companies register their premises / warehouse and undertake other compliances like maintenance of statutory records and filing of returns.

10

Problems-Discounts-Reporting• Discounts and incentives are very common in e commerce model .State Vat

authorities demand Vat on full consideration without discount• Taxation of new transaction types such as e-wallet, sale by trial, redemption

of e-vouchers, subvention of discount to name a few. Absence of a specific direction on treatment of the above transactions under Central and State tax legislations including differential taxation of the same across States has led to diverse practice being adopted by the e-commerce sector.

• Several States have made reporting mandatory by E commerce portals of transactions executed through their portals. Like in Delhi

• In case any Indian citizen residing in UP decides to order any product online, which costs Rs 5000, then he will be required to file a VAT declaration, along with mentioning the vehicle number which brought in the good from outside the state. Further registration as SPN required vide Circular dt. 30-10-2015

11

Advantages under GST regime

• Entry Tax subsumed in GST- Though as per FM Local bodies/Municipal corporations may levy some entry tax under their jurisdiction ?

• Common rate of Tax across India-One Nation One Tax ?

• HSN code bring common classification of goods/services . Thus reducing litigation

• Seamless flow of input credit -?• One set of reporting and registration, compliance

requirements PAN India

12

GST MODEL LAW AND E COMMERCE

1.Chapter-1 Definitions 2.Chapter-III3. Chapter-XIV

13

DEFINITIONS UNDER MODEL GST LAW

• Chapter-1 Definitions• 2(41) ‘electronic commerce’ means supply of goods

and/or services including digital products over digital or electronic network;

( Same as provided in FDI policy)• • 2(42) ‘electronic commerce operator’ means any

person who owns, operates or manages digital or electronic facility or platform for electronic commerce;

14

Chapter-III8. Levy and Collection of Central/State Goods and Services Tax -Sub Section (4)

• The Central or a State Government may, on the recommendation of the Council, by notification, specify categories of services the tax on which shall be paid by the electronic commerce operator if such services are supplied through it, and all

the provisions of this Act shall apply to such electronic commerce operator as if he is the person liable for paying the tax in relation to the supply of such

services: PROVIDED that where an electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic

commerce operator for any purpose in the taxable territory shall be liable to pay tax: PROVIDED FURTHER that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such

person shall be liable to pay tax

15

Inventory based Model e commerce

• E Commerce entity is supplier of Goods/services. • All normal provisions of Model GST ACT applicable regarding registration, returns,

Assessment etc.• The definitions given in Sec 2(41) and 2(42) is comprehensive and apparently covers

this model under E commerce • Sec.8. Levy and Collection of Central/State Goods and Services Tax – Plain reading

of this section says that the Online retailers who supply goods/services on their own behalf/account are not covered under the definition of electronic commerce operator.

They will fall under Sub section 1,2,and 3 and therefore the process of tax collection at source and other requisite compliances provided in Chapter-XIV shall not be applicable.

NEED FOR CLARRIFICATION FROM GOVERNMENT/ COUNCIL-otherwise again

interpretation issues will arise

16

Discounts –Sec.15 Value of Taxable Supply

• Sub Section (3) The value of the supply shall not include any discount that is given:

• (a) before or at the time of the supply provided such discount has been duly recorded in the invoice issued in respect of such supply; and

• (b) after the supply has been effected, provided that: (i) such discount is established in terms of an agreement entered into at or before the time of such supply and specifically linked to relevant invoices; and (ii) input tax credit has been reversed by the recipient of the supply as is attributable to the discount on the basis of document issued by the supplierSimilar Provisions under DVAT and source of litigationApparently post sales incentives & discounts under GST may remain teasing

17

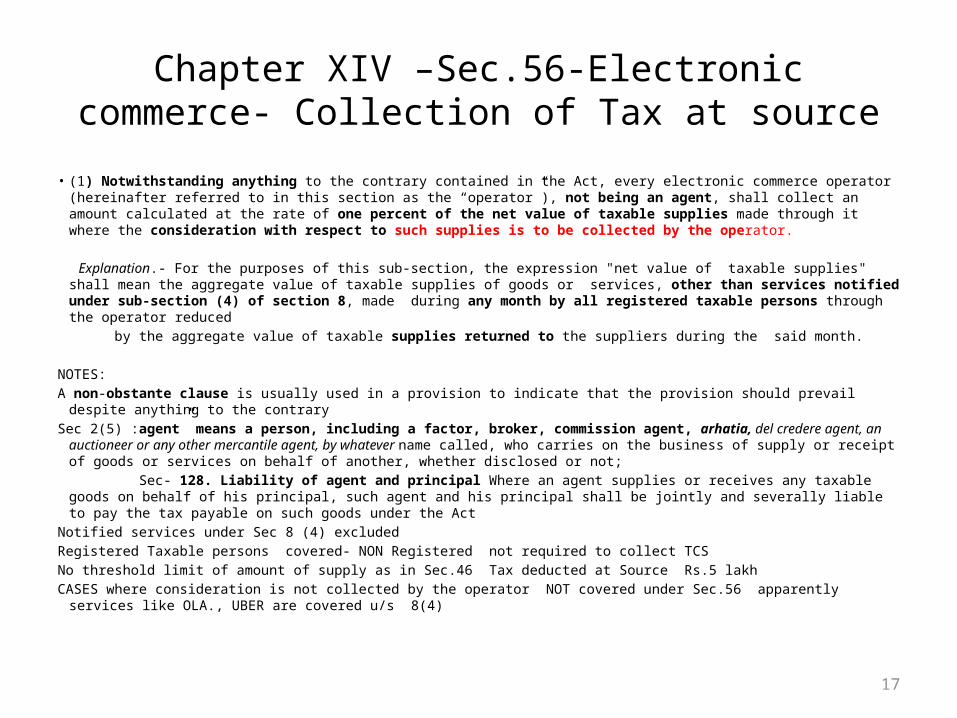

Chapter XIV –Sec.56-Electronic commerce- Collection of Tax at source

• (1) Notwithstanding anything to the contrary contained in the Act, every electronic commerce operator (hereinafter referred to in this section as the “operator”), not being an agent, shall collect an amount calculated at the rate of one percent of the net value of taxable supplies made through it where the consideration with respect to such supplies is to be collected by the operator.

Explanation.- For the purposes of this sub-section, the expression "net value of taxable supplies" shall mean the aggregate value of taxable supplies of goods or services, other than services notified under sub-section (4) of section 8, made during any month by all registered taxable persons through the operator reduced

by the aggregate value of taxable supplies returned to the suppliers during the said month.

NOTES:A non-obstante clause is usually used in a provision to indicate that the provision should prevail despite anything to the contrary Sec 2(5) :agent” means a person, including a factor, broker, commission agent, arhatia, del credere agent, an auctioneer or any

other mercantile agent, by whatever name called, who carries on the business of supply or receipt of goods or services on behalf of another, whether disclosed or not;

Sec- 128. Liability of agent and principal Where an agent supplies or receives any taxable goods on behalf of his principal, such agent and his principal shall be jointly and severally liable to pay the tax payable on such goods under the Act

Notified services under Sec 8 (4) excludedRegistered Taxable persons covered- NON Registered not required to collect TCSNo threshold limit of amount of supply as in Sec.46 Tax deducted at Source Rs.5 lakhCASES where consideration is not collected by the operator NOT covered under Sec.56 apparently services like OLA., UBER are

covered u/s 8(4)

18

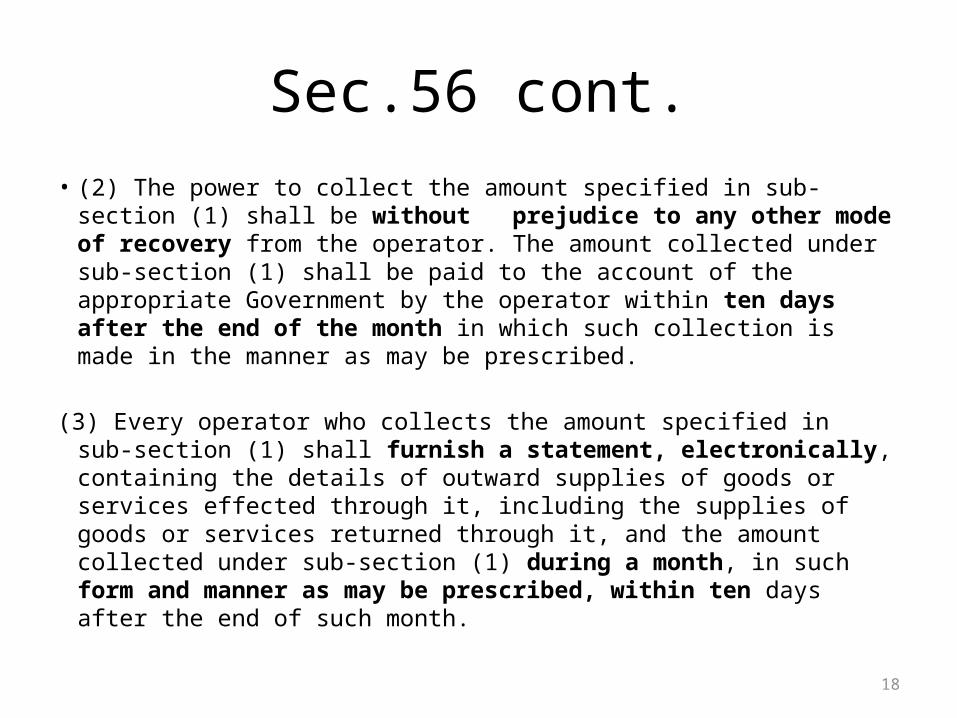

Sec.56 cont.• (2) The power to collect the amount specified in sub-section (1) shall be

without prejudice to any other mode of recovery from the operator. The amount collected under sub-section (1) shall be paid to the account of the appropriate Government by the operator within ten days after the end of the month in which such collection is made in the manner as may be prescribed.

(3) Every operator who collects the amount specified in sub-section (1) shall furnish a statement, electronically, containing the details of outward supplies of goods or services effected through it, including the supplies of goods or services returned through it, and the amount collected under sub-section (1) during a month, in such form and manner as may be prescribed, within ten days after the end of such month.

19

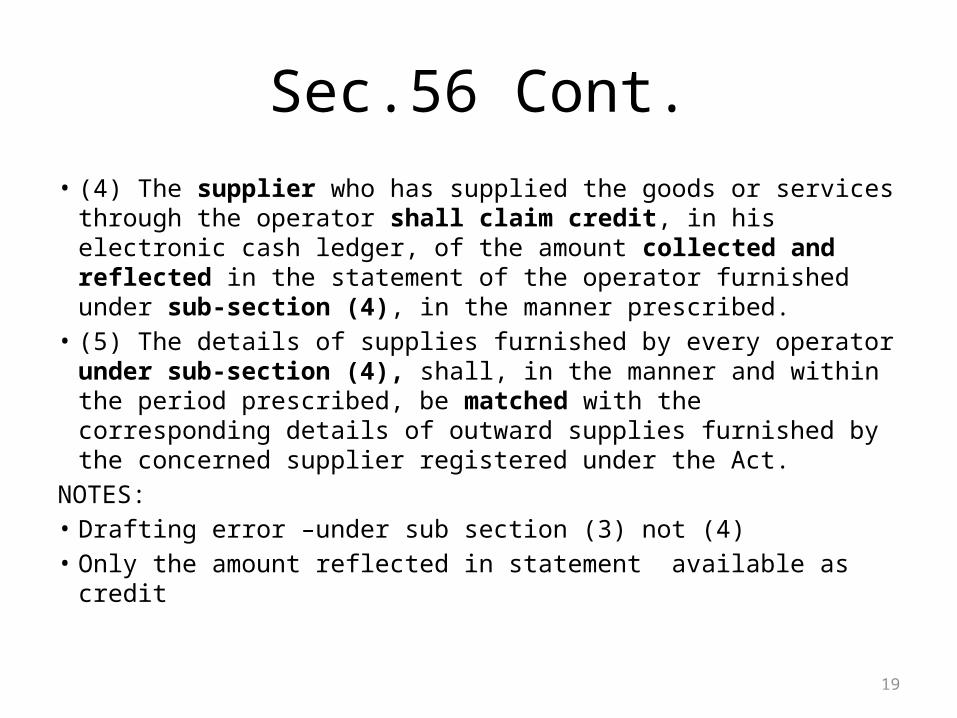

Sec.56 Cont.• (4) The supplier who has supplied the goods or services through

the operator shall claim credit, in his electronic cash ledger, of the amount collected and reflected in the statement of the operator furnished under sub-section (4), in the manner prescribed.

• (5) The details of supplies furnished by every operator under sub-section (4), shall, in the manner and within the period prescribed, be matched with the corresponding details of outward supplies furnished by the concerned supplier registered under the Act.

NOTES:• Drafting error –under sub section (3) not (4)• Only the amount reflected in statement available as credit

20

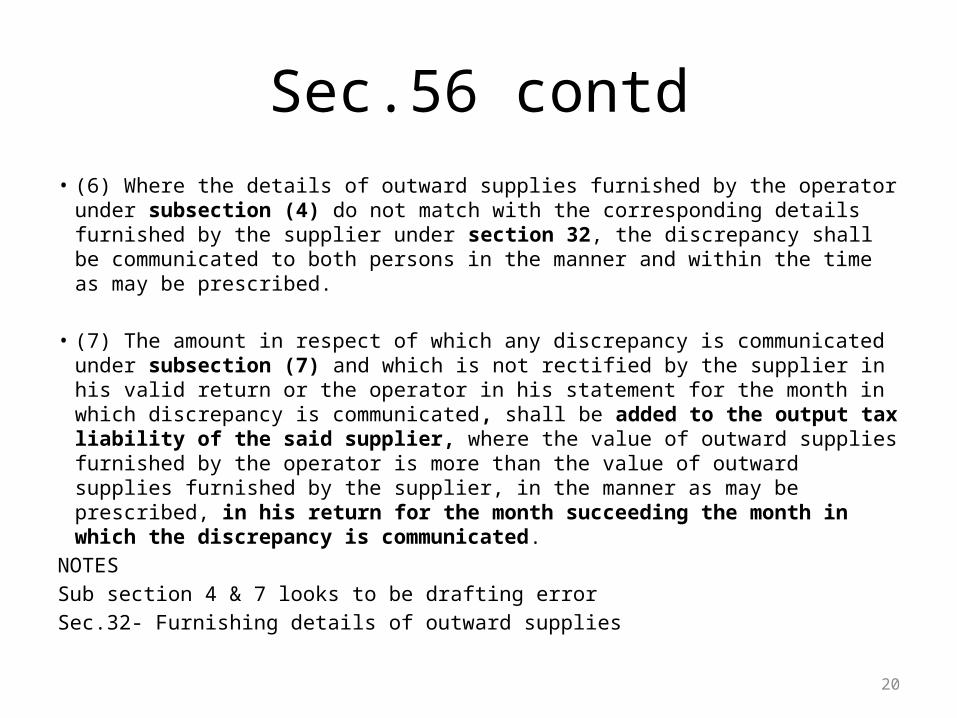

Sec.56 contd• (6) Where the details of outward supplies furnished by the operator under

subsection (4) do not match with the corresponding details furnished by the supplier under section 32, the discrepancy shall be communicated to both persons in the manner and within the time as may be prescribed.

• (7) The amount in respect of which any discrepancy is communicated under subsection (7) and which is not rectified by the supplier in his valid return or the operator in his statement for the month in which discrepancy is communicated, shall be added to the output tax liability of the said supplier, where the value of outward supplies furnished by the operator is more than the value of outward supplies furnished by the supplier, in the manner as may be prescribed, in his return for the month succeeding the month in which the discrepancy is communicated.

NOTESSub section 4 & 7 looks to be drafting errorSec.32- Furnishing details of outward supplies

21

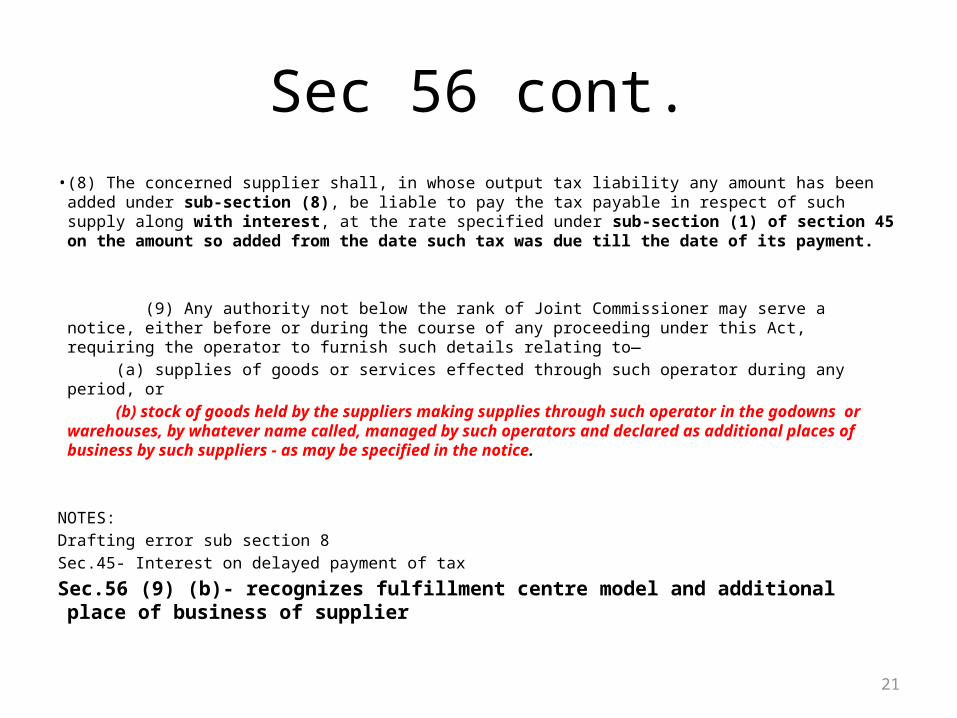

Sec 56 cont.• (8) The concerned supplier shall, in whose output tax liability any amount has been added under sub-section

(8), be liable to pay the tax payable in respect of such supply along with interest, at the rate specified under sub-section (1) of section 45 on the amount so added from the date such tax was due till the date of its payment.

(9) Any authority not below the rank of Joint Commissioner may serve a notice, either before or during the course of any proceeding under this Act, requiring the operator to furnish such details relating to—

(a) supplies of goods or services effected through such operator during any period, or (b) stock of goods held by the suppliers making supplies through such operator in the godowns or

warehouses, by whatever name called, managed by such operators and declared as additional places of business by such suppliers - as may be specified in the notice.

NOTES:Drafting error sub section 8Sec.45- Interest on delayed payment of tax

Sec.56 (9) (b)- recognizes fulfillment centre model and additional place of business of supplier

22

Sec 56 contd.• (10) Every operator on whom a notice has been served under

sub-section (10) shall furnish the required information within fifteen working days of the date of service of such notice.

• (11) Any person who fails to furnish the information required by the notice served under sub-section (10) shall, without prejudice to any action that is or may be taken under section 85 , be liable to a penalty which may extend to twenty-five thousand rupees.

• Explanation.— For the purposes of this section, the expression ‘concerned supplier’ shall mean the supplier of goods and/or services making supplies through the operator.

23

Stock Transfers- Taxed under Model GST Law

• Under the Model GST Law Intra-state and inter-state stock transfers, between branches or warehouses of a single e-commerce entity, would be deemed to be supplies, subject to GST.

• Though the tax paid would be available as credit to the entity, this may result in cash flow blockages. Example, where large quantities of goods are stock transferred even from one godown to another godown tax liability would arise at this first stage which can only be offset at the time of final supplies by the e-commerce entity.

• NOTESRelevant both for Inventory based model as well Market place model.

24

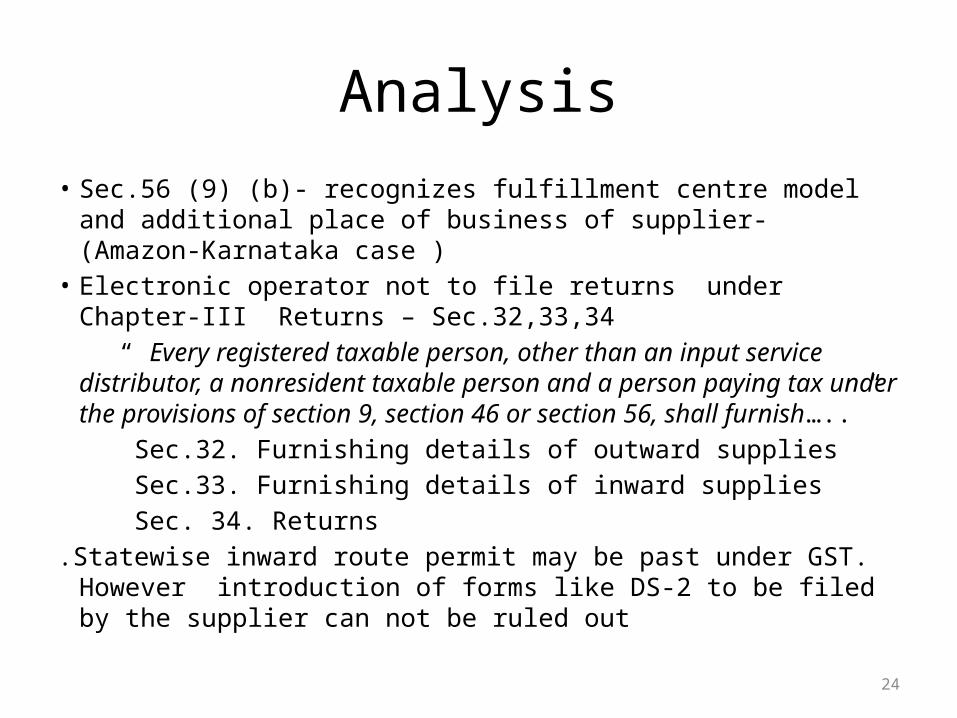

Analysis• Sec.56 (9) (b)- recognizes fulfillment centre model and additional place

of business of supplier- (Amazon-Karnataka case )• Electronic operator not to file returns under Chapter-III Returns –

Sec.32,33,34 “ Every registered taxable person, other than an input service distributor,

a nonresident taxable person and a person paying tax under the provisions of section 9, section 46 or section 56, shall furnish…..”

Sec.32. Furnishing details of outward supplies Sec.33. Furnishing details of inward supplies Sec. 34. Returns.Statewise inward route permit may be past under GST. However

introduction of forms like DS-2 to be filed by the supplier can not be ruled out

25

Analysis cont.• Schedule-V PERSONS LIABLE TO BE REGISTERED Sec.6 Notwithstanding anything contained in paragraph 1 and 3 above, the

following categories of persons shall be required to be registered under this Act: (vii) persons who are required to collect tax under 56, whether or not separately

registered under the Act;

* E Commerce operator required to registered under the ACT even if it does not cross threshold limit of registration.

*Required to charge GST on the services provided by it whenever crosses the threshold limit and file its return and pay taxes as per normal provision of GST

*Fulfillment centres/ godowns should be carefully planned to avoid any issues under GST.

26

A BIG THANK YOU TO ALL OF YOU.

• Queries/ suggestions are welcome

• By: Ca.Sanjay Gupta, Ph: 9311025900 M/s Sanjay Ram Shanker & Associates Chartered Accountants 4799/2,Ram Bazar, Cloth Market,Delhi-110006 Email: [email protected] Website: wwww.sanjayramshanker.com