Embed Size (px)

Citation preview

Executive perspectives on Banking and Insurance

Disrupted

Content owned by Management Events. All rights reserved.

You can’t protect yourself from disruption, you have to be in it. Be prepared and make sure you go where the industry is going, you can’t fight back.

Director, Insurance

"

Content owned by Management Events. All rights reserved.

ONLINE survey

The report is based on the responses of 635 decision makers of the largest banking and insurance organizations in Europe and Southeast Asia who were surveyed as a part of Management Events’ Executive Trend Survey®. Our latest survey is the 10th in the ongoing series of studies covering strategic development initiatives and investment actions of these organizations.

FACE-TO-FACE interviewsTo deepen our insights, we interviewed the highest decision makers face-to-face to discuss further the trends and issues in the industry.

29%

28%

16%

13%

6%

4%

4%

IT Management

Business Management

Finance Management

Marketing and Sales Management

HR Management

Product Development Management

Other

DECISION MAKERS RESEARCHED

Content owned by Management Events. All rights reserved.

KEY REPORT TAKEAWAYS

Financial services sector has traditionally been an industry with high barriers for entry. As globalization and new technologies are shrinking the world to a smaller entity and creating cracks into whatever used to be untouchable, also financial services industry has lost its safe zone and is now competing in a new environment.

Most of the executives in the financial services sector are positive about their growth prospects. New product and service development is strongly perceived as the source for growth. Simultaneously, digital service models and automation are showing their effects, as a third of the decision makers state the employee count will decrease within the next 18 months.

The investment priorities of large banking and insurance organizations are now in process automation and business development for the customer. Financial service organizations attempt to take an outside-in perspective to create products and services the customers value. Still, many organizations struggle with customer experience-related issues.

Preparing for disruption and future competition is two-folded. Incumbents in the industry need to be able to build organizational structures that enable agile, startup-like operating model as their disruptive fintech challengers apply. Success also requires significant attention on customer and user experience, which is in the core of new industry entrants.

1 2

3 4

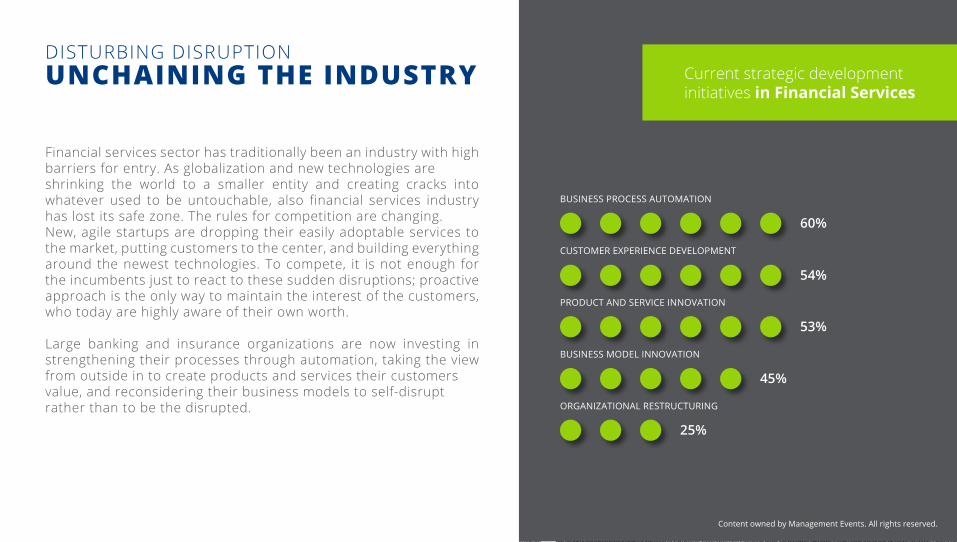

Financial services sector has traditionally been an industry with high barriers for entry. As globalization and new technologies are shrinking the world to a smaller entity and creating cracks into whatever used to be untouchable, also financial services industry has lost its safe zone. The rules for competition are changing. New, agile startups are dropping their easily adoptable services to the market, putting customers to the center, and building everything around the newest technologies. To compete, it is not enough for the incumbents just to react to these sudden disruptions; proactive approach is the only way to maintain the interest of the customers, who today are highly aware of their own worth.

Large banking and insurance organizations are now investing in strengthening their processes through automation, taking the view from outside in to create products and services their customers value, and reconsidering their business models to self-disrupt rather than to be the disrupted.

Content owned by Management Events. All rights reserved.

UNCHAINING THE INDUSTRYDISTURBING DISRUPTION

BUSINESS PROCESS AUTOMATION

CUSTOMER EXPERIENCE DEVELOPMENT

PRODUCT AND SERVICE INNOVATION

BUSINESS MODEL INNOVATION

ORGANIZATIONAL RESTRUCTURING

60%

54%

53%

45%

25%

Current strategic development initiatives in Financial Services

Content owned by Management Events. All rights reserved.

CRITICAL LEADERSHIP SKILLS IN FINANCIAL SERVICES TODAY

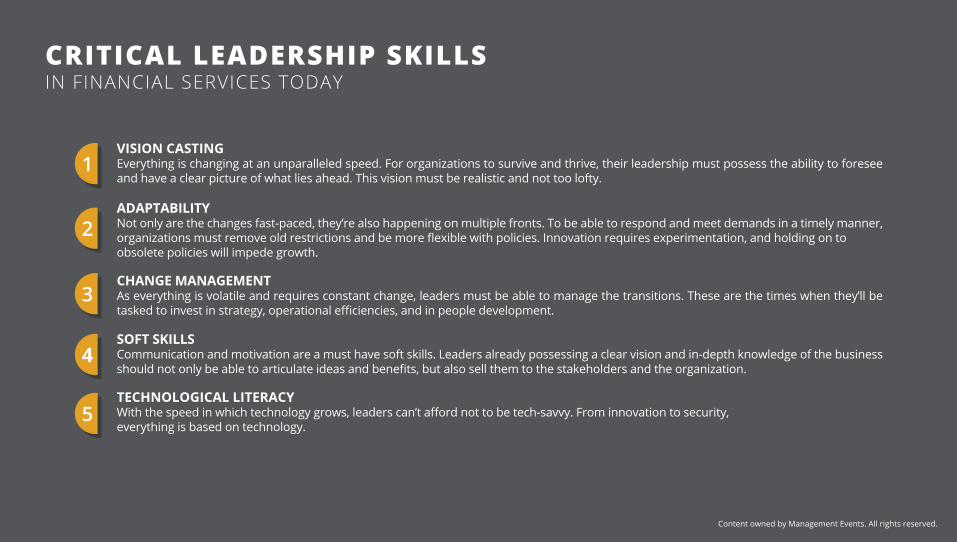

VISION CASTINGEverything is changing at an unparalleled speed. For organizations to survive and thrive, their leadership must possess the ability to foresee and have a clear picture of what lies ahead. This vision must be realistic and not too lofty.

ADAPTABILITYNot only are the changes fast-paced, they’re also happening on multiple fronts. To be able to respond and meet demands in a timely manner, organizations must remove old restrictions and be more flexible with policies. Innovation requires experimentation, and holding on to obsolete policies will impede growth.

CHANGE MANAGEMENTAs everything is volatile and requires constant change, leaders must be able to manage the transitions. These are the times when they’ll be tasked to invest in strategy, operational efficiencies, and in people development.

SOFT SKILLSCommunication and motivation are a must have soft skills. Leaders already possessing a clear vision and in-depth knowledge of the business should not only be able to articulate ideas and benefits, but also sell them to the stakeholders and the organization.

TECHNOLOGICAL LITERACYWith the speed in which technology grows, leaders can’t afford not to be tech-savvy. From innovation to security, everything is based on technology.

1

2

3

4

5

Content owned by Management Events. All rights reserved.

INDUSTRY GROWTH PROSPECTS

GROWTH IN CURRENT MARKETS

WE AIM FOR AGGRESSIVE GROWTH WE AIM FOR MODERATE GROWTH WE FOCUS ON OPERATIONALEFFICIENCY AND REDUCING COSTS

NEW PRODUCTS AND SERVICES

GEOGRAPHIC EXPANSION

MERGERS AND ACQUISITIONS, JOINT VENTURES, STRATEGIC ALLIANCES

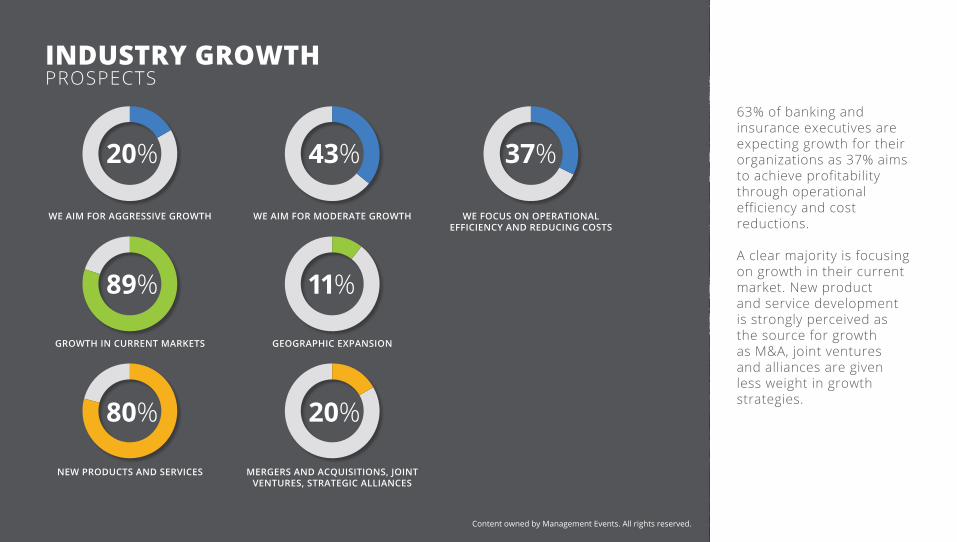

63% of banking and insurance executives are expecting growth for their organizations as 37% aims to achieve profitability through operational efficiency and cost reductions.

A clear majority is focusing on growth in their current market. New product and service development is strongly perceived as the source for growth as M&A, joint ventures and alliances are given less weight in growth strategies.

20% 43% 37%

11%

20%80%

89%

Content owned by Management Events. All rights reserved.

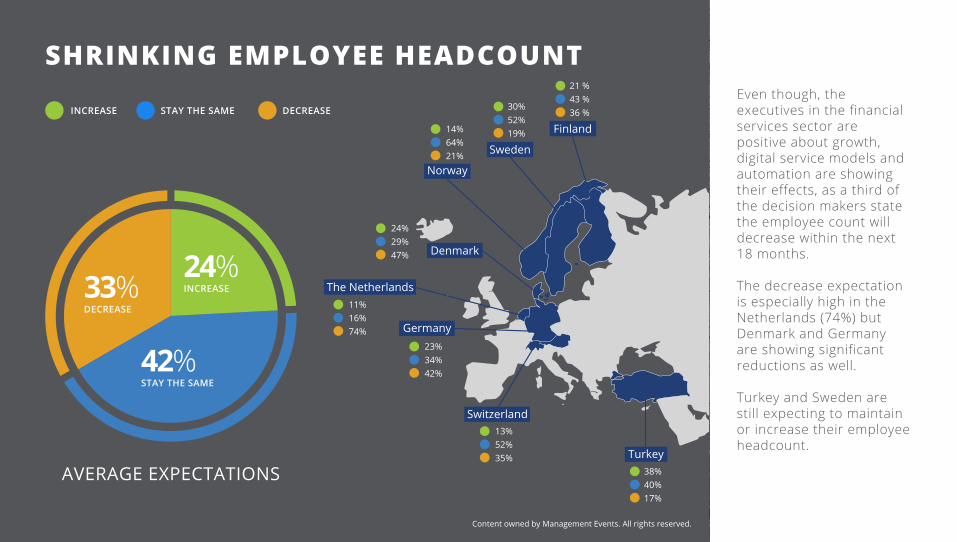

SHRINKING EMPLOYEE HEADCOUNTEven though, the executives in the financial services sector are positive about growth, digital service models and automation are showing their effects, as a third of the decision makers state the employee count will decrease within the next 18 months.

The decrease expectation is especially high in the Netherlands (74%) but Denmark and Germany are showing significant reductions as well.

Turkey and Sweden are still expecting to maintain or increase their employee headcount.

INCREASE STAY THE SAME DECREASE

24%

42%

33%

AVERAGE EXPECTATIONS

INCREASE

STAY THE SAME

DECREASE

Finland

Sweden

Norway

Denmark

The Netherlands

Germany

Switzerland

Turkey

13%52%35%

30%52%19%

21 %43 %36 %

14%64%21%

38%40%17%

11%16%74%

23%34%42%

24%29%47%

Content owned by Management Events. All rights reserved.

DROWNINGIN DIGITAL

Content owned by Management Events. All rights reserved.

Content owned by Management Events. All rights reserved.

Innovation is absolutely paramount in the ever increasing speed of competition we’re facing. We need to be innovative all the time.

Head of Tactical Asset Allocation, Insurance

"

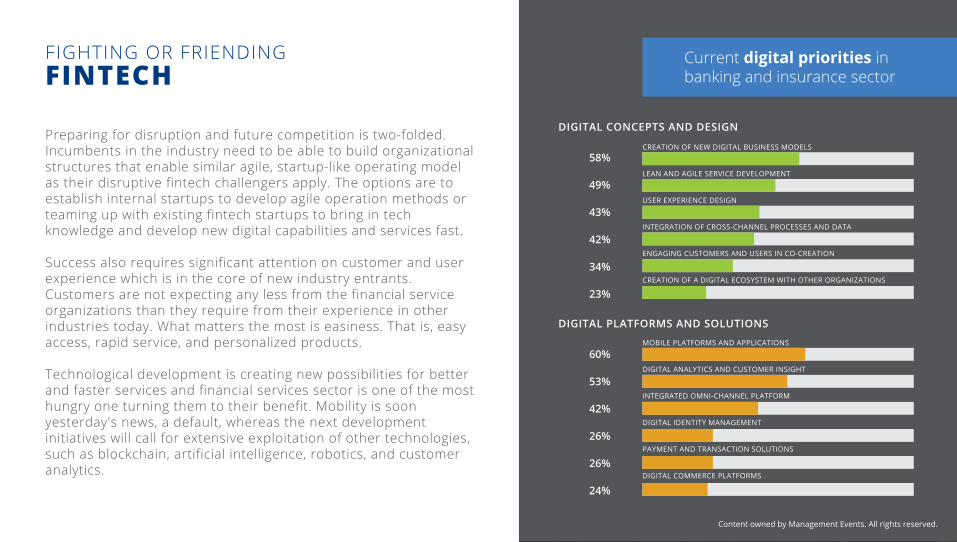

Preparing for disruption and future competition is two-folded. Incumbents in the industry need to be able to build organizational structures that enable similar agile, startup-like operating model as their disruptive fintech challengers apply. The options are to establish internal startups to develop agile operation methods or teaming up with existing fintech startups to bring in tech knowledge and develop new digital capabilities and services fast.

Success also requires significant attention on customer and user experience which is in the core of new industry entrants. Customers are not expecting any less from the financial service organizations than they require from their experience in other industries today. What matters the most is easiness. That is, easy access, rapid service, and personalized products.

Technological development is creating new possibilities for better and faster services and financial services sector is one of the most hungry one turning them to their benefit. Mobility is soon yesterday's news, a default, whereas the next development initiatives will call for extensive exploitation of other technologies, such as blockchain, artificial intelligence, robotics, and customer analytics.

Content owned by Management Events. All rights reserved.

FINTECHFIGHTING OR FRIENDING

DIGITAL CONCEPTS AND DESIGN

DIGITAL PLATFORMS AND SOLUTIONS

58%

49%

43%

42%

34%

23%

CREATION OF NEW DIGITAL BUSINESS MODELS

LEAN AND AGILE SERVICE DEVELOPMENT

USER EXPERIENCE DESIGN

INTEGRATION OF CROSS-CHANNEL PROCESSES AND DATA

ENGAGING CUSTOMERS AND USERS IN CO-CREATION

CREATION OF A DIGITAL ECOSYSTEM WITH OTHER ORGANIZATIONS

60%

53%

42%

26%

26%

24%

MOBILE PLATFORMS AND APPLICATIONS

DIGITAL ANALYTICS AND CUSTOMER INSIGHT

INTEGRATED OMNI-CHANNEL PLATFORM

DIGITAL IDENTITY MANAGEMENT

PAYMENT AND TRANSACTION SOLUTIONS

DIGITAL COMMERCE PLATFORMS

Current digital priorities in banking and insurance sector

Content owned by Management Events. All rights reserved.

We need to constantly evaluate the opportunities created by new technologies, and Blockchain is one of the most promising ones. Potentially, it will have huge implications on different areas like banking and finance, logistics, and on the public sector. However, results may totally differ from what we now believe. Looking back, hardly anyone predicted the implications of the Internet either.

CTO, Technology, Media, and Telecom

"

Mobile solutions and digital services are a must but digitizing the existing is only a stepping stone to the opportunities waiting ahead.Artificial intelligence is offering banks and insurance companies a chance for compete among their disruptors. The cognitive, self-learning capabilities of machines have opened a whole new vision of future in terms of customer analysis and risk assessment with highly advanced data processing, customer service with virtual assistants, and investment account management with robo-analysts to name a few.

Artificial Intelligence will have its effect on workforce, processes, and business models. It will revolutionize both business and society, financial services sector being one of the frontrunners.

Content owned by Management Events. All rights reserved.

ACTING ARTIFICIAL BUT INTELLIGENT

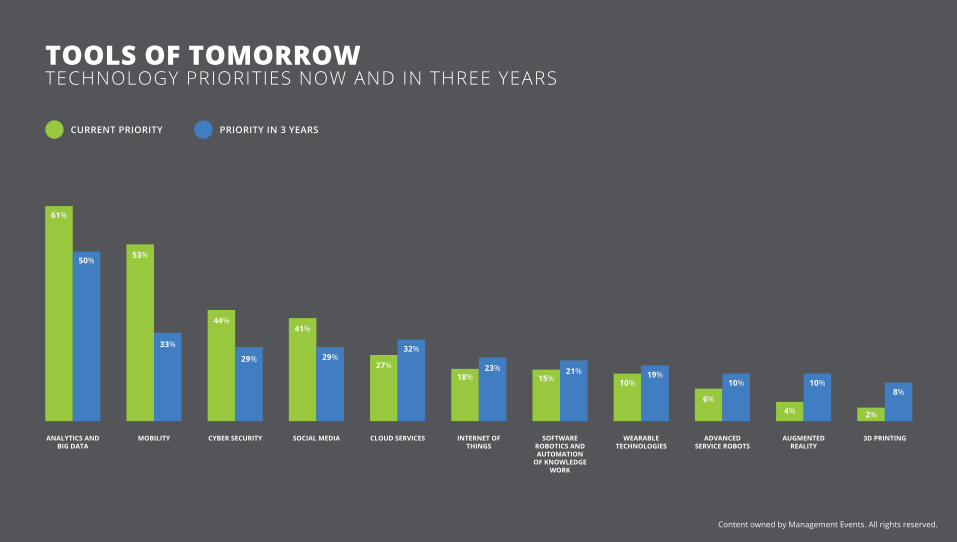

TOOLS OF TOMORROWTECHNOLOGY PRIORITIES NOW AND IN THREE YEARS

Content owned by Management Events. All rights reserved.

CURRENT PRIORITY PRIORITY IN 3 YEARS

CLOUD SERVICES

32%

3D PRINTING

8%

2%

ADVANCEDSERVICE ROBOTS

10%

6%

AUGMENTED REALITY

10%

4%

27%

CYBER SECURITY

29%

44%

INTERNET OF THINGS

23%18%

MOBILITY

33%

53%

SOCIAL MEDIA

29%

41%

SOFTWARE ROBOTICS AND AUTOMATION

OF KNOWLEDGE WORK

21%15%

WEARABLE TECHNOLOGIES

19%10%

ANALYTICS AND BIG DATA

50%

61%

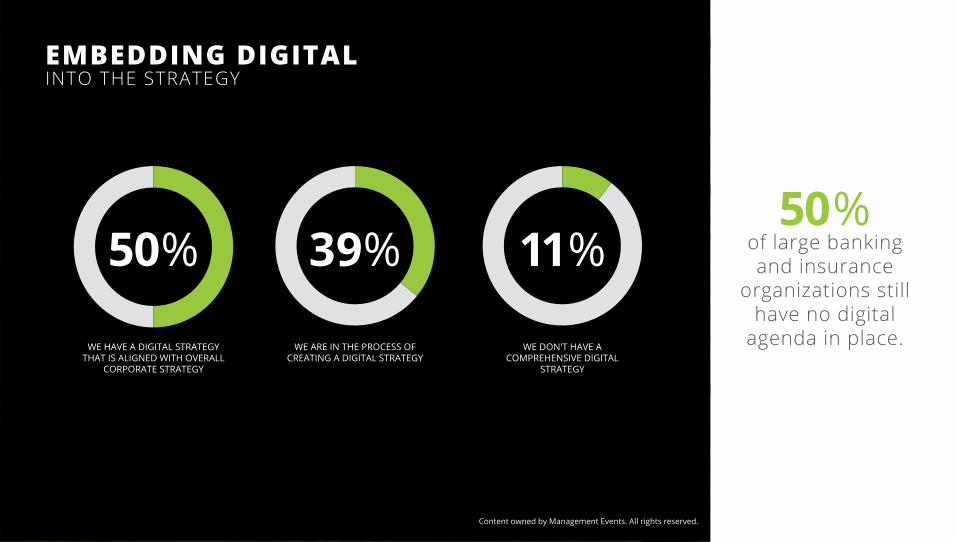

50%of large banking and insurance

organizations still have no digital

agenda in place.

Content owned by Management Events. All rights reserved.

EMBEDDING DIGITALINTO THE STRATEGY

WE HAVE A DIGITAL STRATEGYTHAT IS ALIGNED WITH OVERALL

CORPORATE STRATEGY

WE ARE IN THE PROCESS OFCREATING A DIGITAL STRATEGY

WE DON'T HAVE A COMPREHENSIVE DIGITAL

STRATEGY

50% 39% 11%

Content owned by Management Events. All rights reserved.

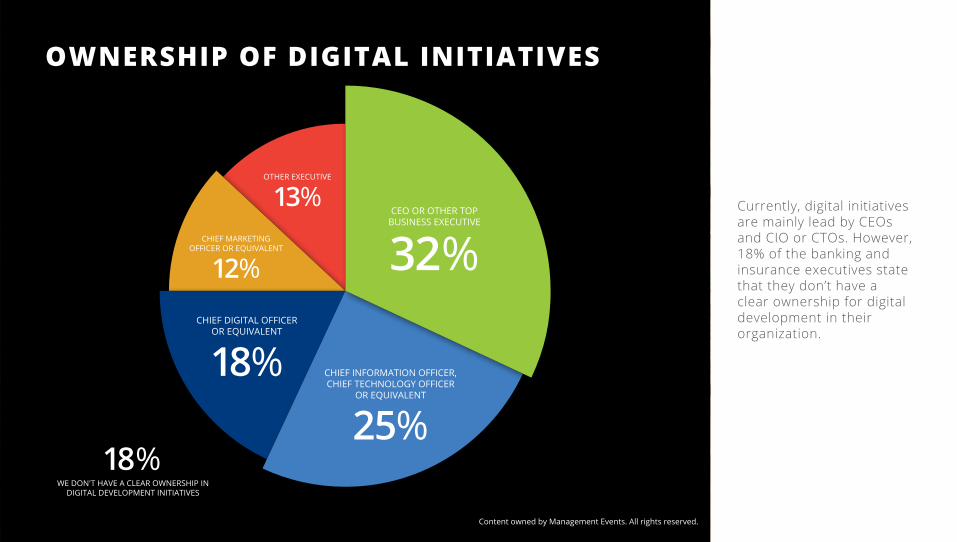

OWNERSHIP OF DIGITAL INITIATIVES

Currently, digital initiatives are mainly lead by CEOs and CIO or CTOs. However, 18% of the banking and insurance executives state that they don’t have a clear ownership for digital development in theirorganization.

CEO OR OTHER TOPBUSINESS EXECUTIVE

32%

25%18%

12%

13%

CHIEF INFORMATION OFFICER,CHIEF TECHNOLOGY OFFICER

OR EQUIVALENT

CHIEF DIGITAL OFFICEROR EQUIVALENT

CHIEF MARKETINGOFFICER OR EQUIVALENT

OTHER EXECUTIVE

WE DON'T HAVE A CLEAR OWNERSHIP INDIGITAL DEVELOPMENT INITIATIVES

18%

Content owned by Management Events. All rights reserved.

We have to make a very intuitive service from the customer’s point of view. A service that slides within customers’ everyday lives without them even noticing it. That requires us to study the customer path, to improve processes all the time, and most of all, to learn from the experience.

Chief Development Officer, Incurance

"

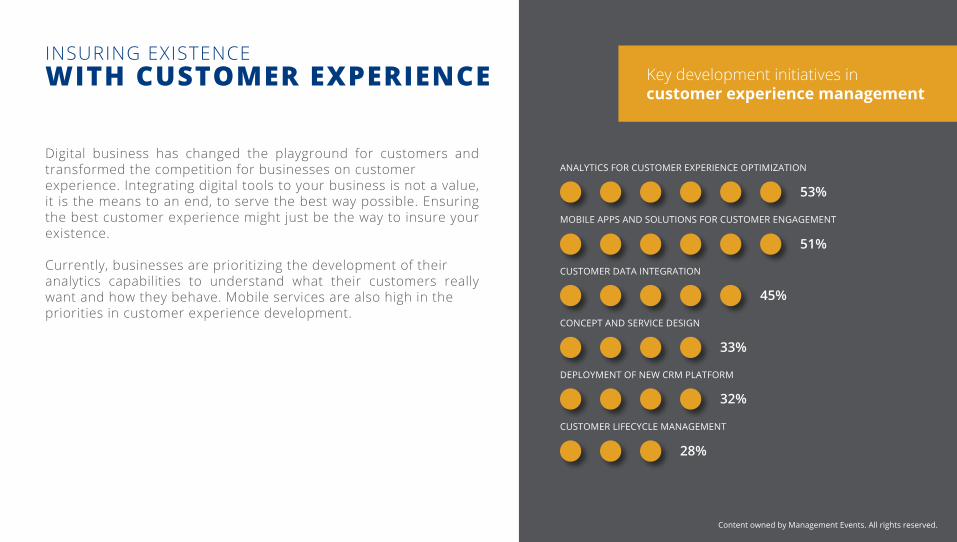

Digital business has changed the playground for customers and transformed the competition for businesses on customer experience. Integrating digital tools to your business is not a value, it is the means to an end, to serve the best way possible. Ensuring the best customer experience might just be the way to insure your existence. Currently, businesses are prioritizing the development of their analytics capabilities to understand what their customers really want and how they behave. Mobile services are also high in the priorities in customer experience development.

Content owned by Management Events. All rights reserved.

WITH CUSTOMER EXPERIENCE INSURING EXISTENCE

53%

51%

45%

33%

32%

28%

Key development initiatives incustomer experience management

ANALYTICS FOR CUSTOMER EXPERIENCE OPTIMIZATION

MOBILE APPS AND SOLUTIONS FOR CUSTOMER ENGAGEMENT

CUSTOMER DATA INTEGRATION

CONCEPT AND SERVICE DESIGN

DEPLOYMENT OF NEW CRM PLATFORM

CUSTOMER LIFECYCLE MANAGEMENT

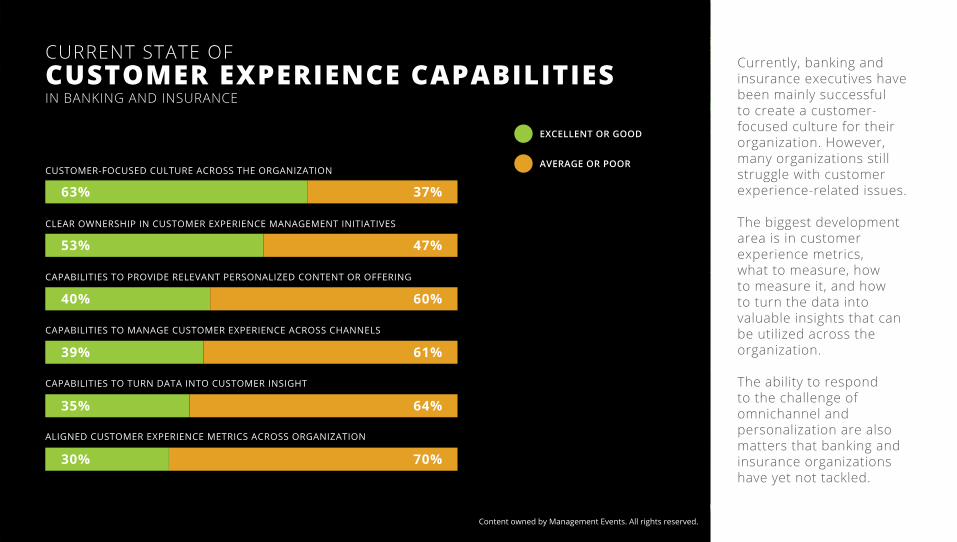

CUSTOMER-FOCUSED CULTURE ACROSS THE ORGANIZATION

CLEAR OWNERSHIP IN CUSTOMER EXPERIENCE MANAGEMENT INITIATIVES

CAPABILITIES TO PROVIDE RELEVANT PERSONALIZED CONTENT OR OFFERING

CAPABILITIES TO MANAGE CUSTOMER EXPERIENCE ACROSS CHANNELS

CAPABILITIES TO TURN DATA INTO CUSTOMER INSIGHT

ALIGNED CUSTOMER EXPERIENCE METRICS ACROSS ORGANIZATION

Currently, banking and insurance executives have been mainly successful to create a customer-focused culture for their organization. However, many organizations still struggle with customer experience-related issues.

The biggest development area is in customer experience metrics, what to measure, how to measure it, and how to turn the data into valuable insights that can be utilized across the organization.

The ability to respond to the challenge of omnichannel and personalization are also matters that banking and insurance organizations have yet not tackled.

Content owned by Management Events. All rights reserved.

CUSTOMER EXPERIENCE CAPABILITIESCURRENT STATE OF

IN BANKING AND INSURANCE

EXCELLENT OR GOOD

AVERAGE OR POOR

63%

53%

37%

47%

39% 61%

40% 60%

30% 70%

35% 64%

Content owned by Management Events. All rights reserved.

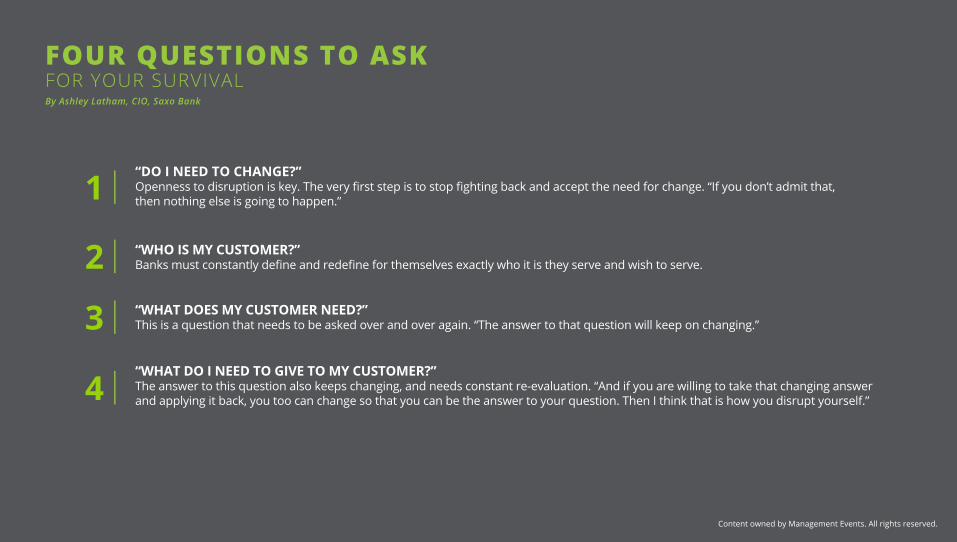

FOUR QUESTIONS TO ASKBy Ashley Latham, CIO, Saxo Bank

“DO I NEED TO CHANGE?” Openness to disruption is key. The very first step is to stop fighting back and accept the need for change. “If you don’t admit that,then nothing else is going to happen.”

“WHO IS MY CUSTOMER?” Banks must constantly define and redefine for themselves exactly who it is they serve and wish to serve.

“WHAT DOES MY CUSTOMER NEED?” This is a question that needs to be asked over and over again. “The answer to that question will keep on changing.”

“WHAT DO I NEED TO GIVE TO MY CUSTOMER?” The answer to this question also keeps changing, and needs constant re-evaluation. “And if you are willing to take that changing answer and applying it back, you too can change so that you can be the answer to your question. Then I think that is how you disrupt yourself.”

1

2

3

4

FOR YOUR SURVIVAL

Content owned by Management Events. All rights reserved.

"In order to stay competitive in the marketplace, you always need to feel a certain level of discomfort because you know that there’s another mountain to climb, another technology to learn, a new way of doing business. COO, Banking

Management Events brings together the needs of top decision makers and the offerings of solution providers, generating business opportunities for both parties. The exclusive, invitation-only event concept provides the opportunity to meet the most potential clients in pre-booked face-to-face meetings. The participants of our events are technologically driven leaders of the largest companies in Europe and Southeast Asia.

Annually, our 160 invitation-only business events gather 20 000 leaders and 2 500 solution providers, generating more than 70 000 face-to-face meetings. To identify the responsibilities, investments, and projects of the top decision makers, we conduct 35 000 interviews and receive over 10 000 online survey responses each year.

Share the report

managementevents.com

Content owned by Management Events. All rights reserved.