Embed Size (px)

Citation preview

Conquering the Term Sheet:

Everything You Need to Know About Deal Terms

David StarkPartner, OurCrowd

@starkupnation

Zack MillerPartner, OurCrowd

@newrulesinvest

OurCrowd

Leading equity crowdfunding platform with 8000+ investors

from over 100 countries

Investment Checklist

1. Great team 2. Market 3. Easy to understand 4. Traction 5. Sponsorship 6. Good deal

A good (investment)

deal =risk-adjusted return

ample upside downside protection alignment of interests

The Naked Term SheetCrafting and Reading Deal Terms

“A non-binding agreement setting forth the basic terms and conditions under which an investment will be made.”

Term Sheet

Lesson 1

The Naked Term Sheet

Valuation Liquidation preferences

ESOP

Preemptive rights Anti-dilution protection Board representation

Control provisions

Convertible NotesDiscount

Cap Interest Maturity

Conversion Mechanics

Lesson 1 - Equity Lesson 3 (May 27)

Lesson 2 (May 20)

Deal term triumvirateValuation

ESOP Preferences

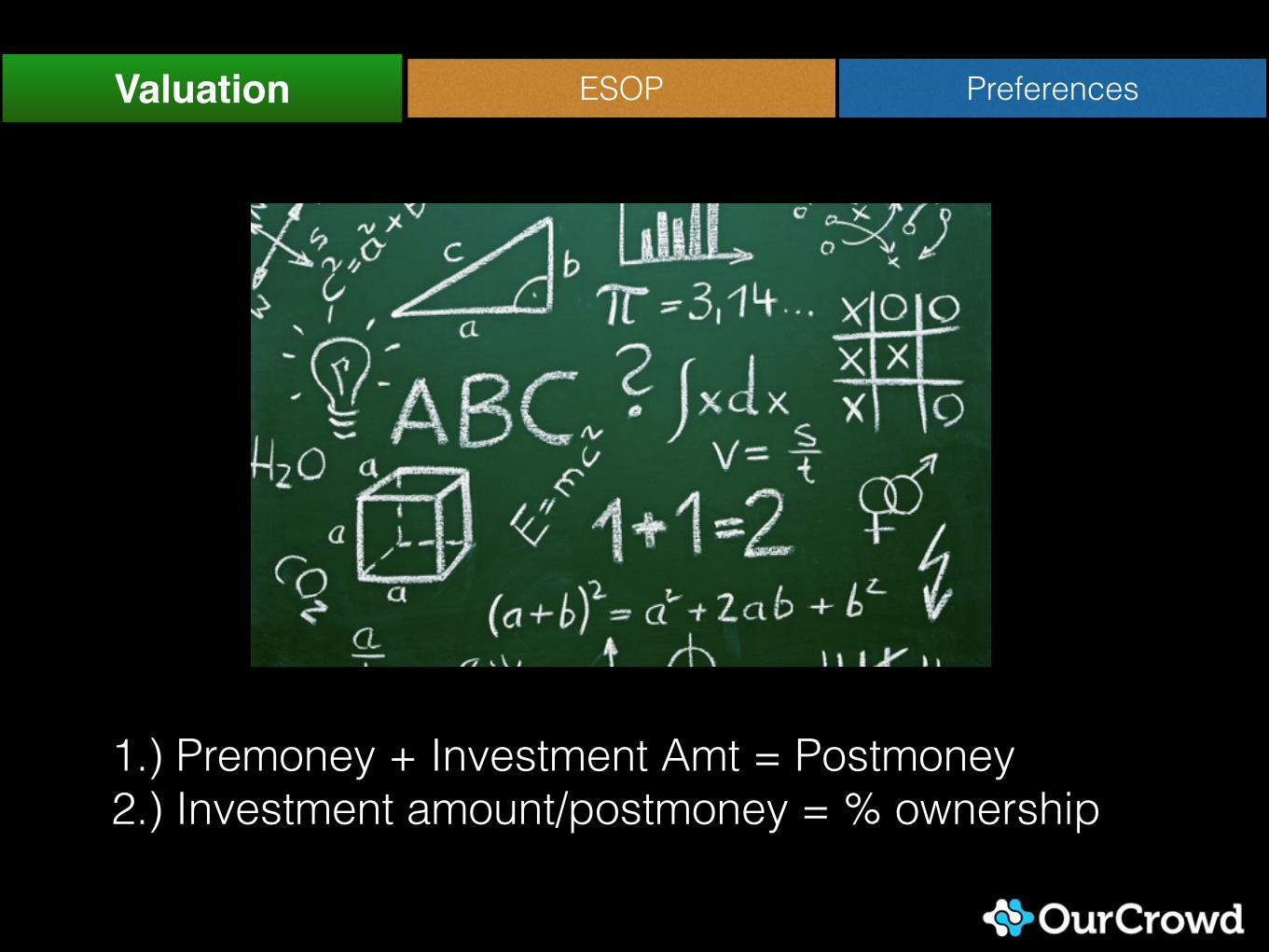

1.) Premoney + Investment Amt = Postmoney 2.) Investment amount/postmoney = % ownership

PreferencesESOPValuation

Art and a science of valuation: multiple methodologies

Early Stage

Mid Stage

http://blog.ourcrowd.com/index.php/2014/05/14/cashing-in-how-to-make-money-investing-in-startups/

Late Stage

Source:

PreferencesESOPValuation

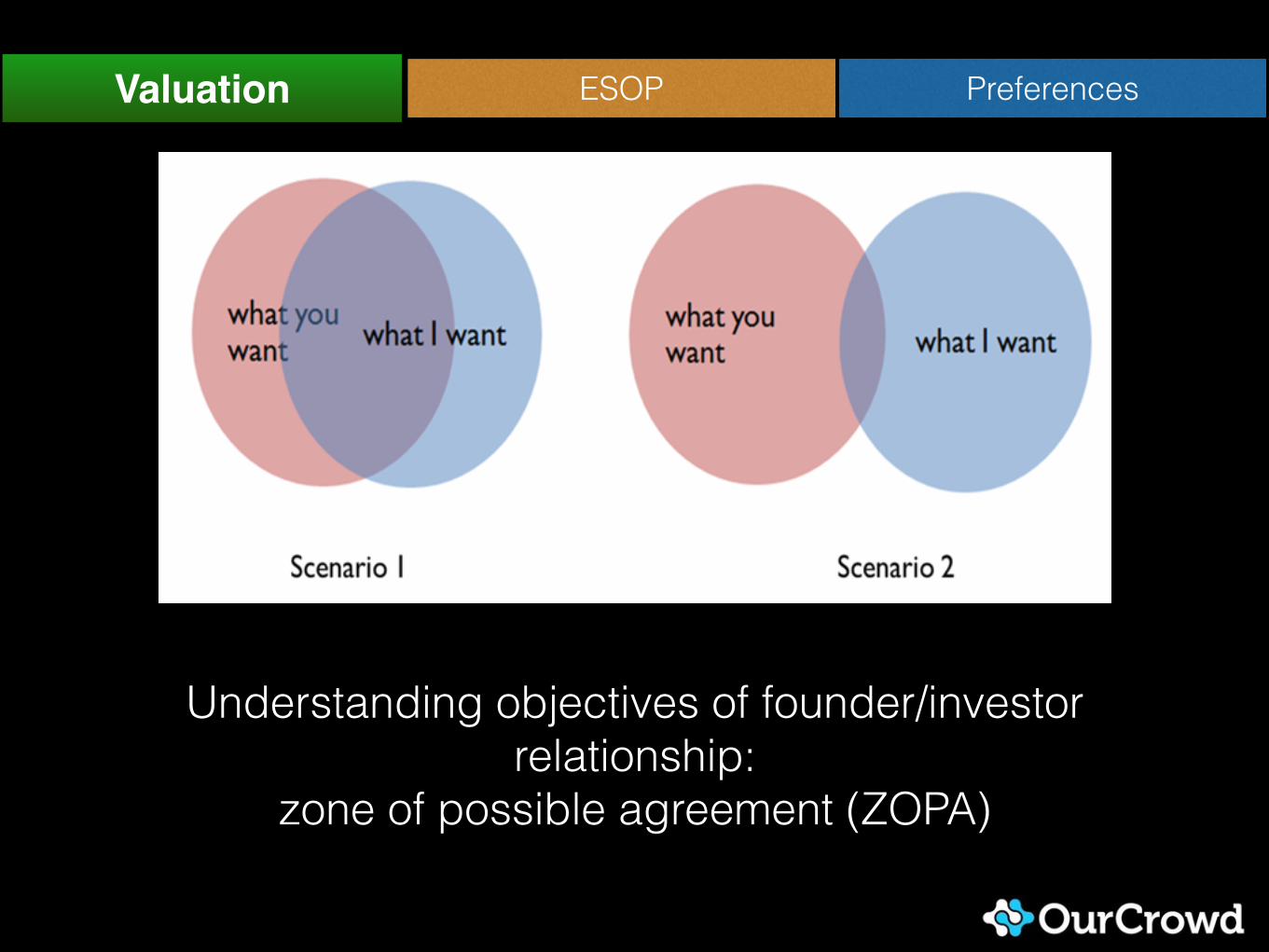

Understanding objectives of founder/investor relationship:

zone of possible agreement (ZOPA)

PreferencesESOPValuation

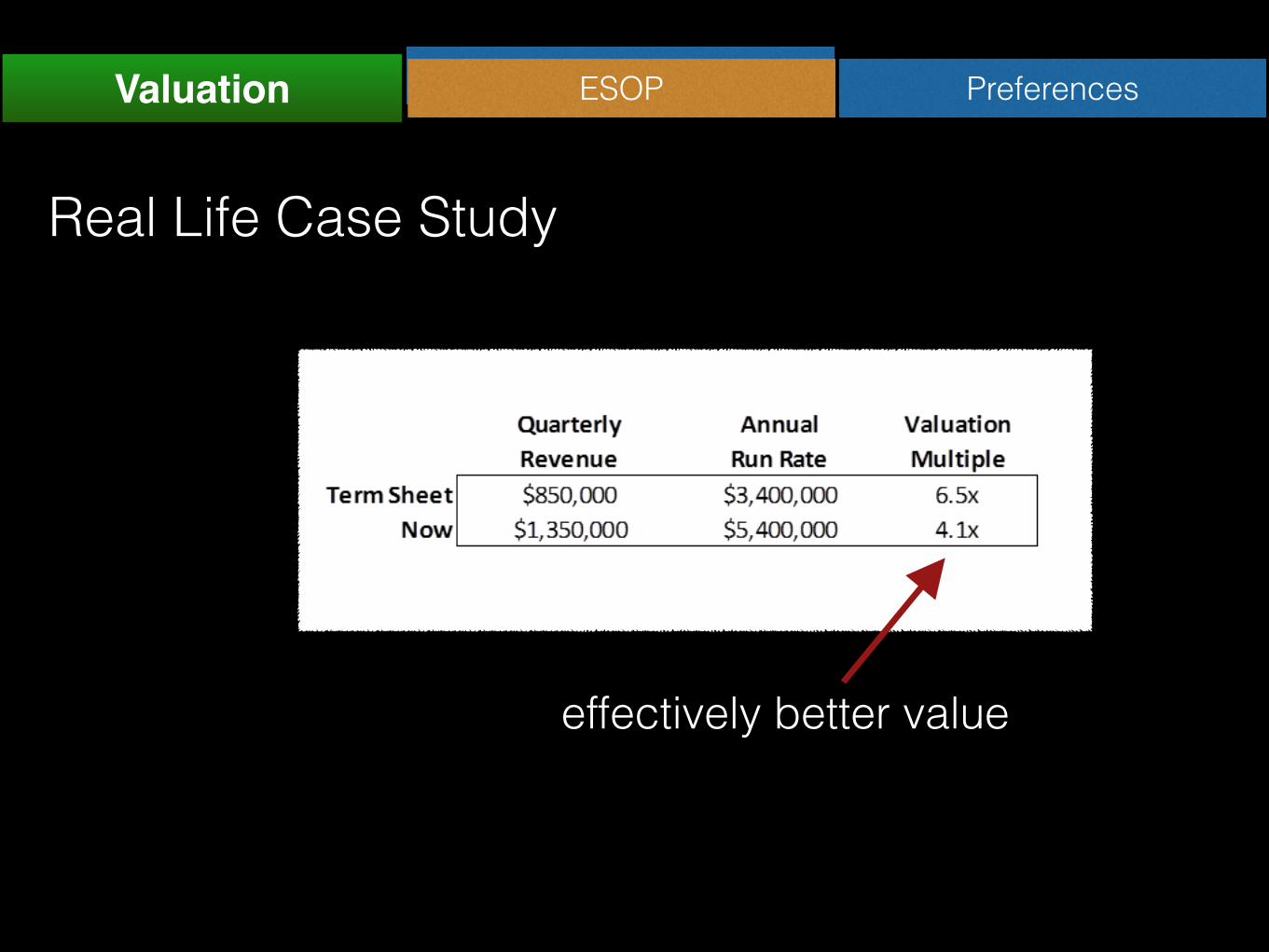

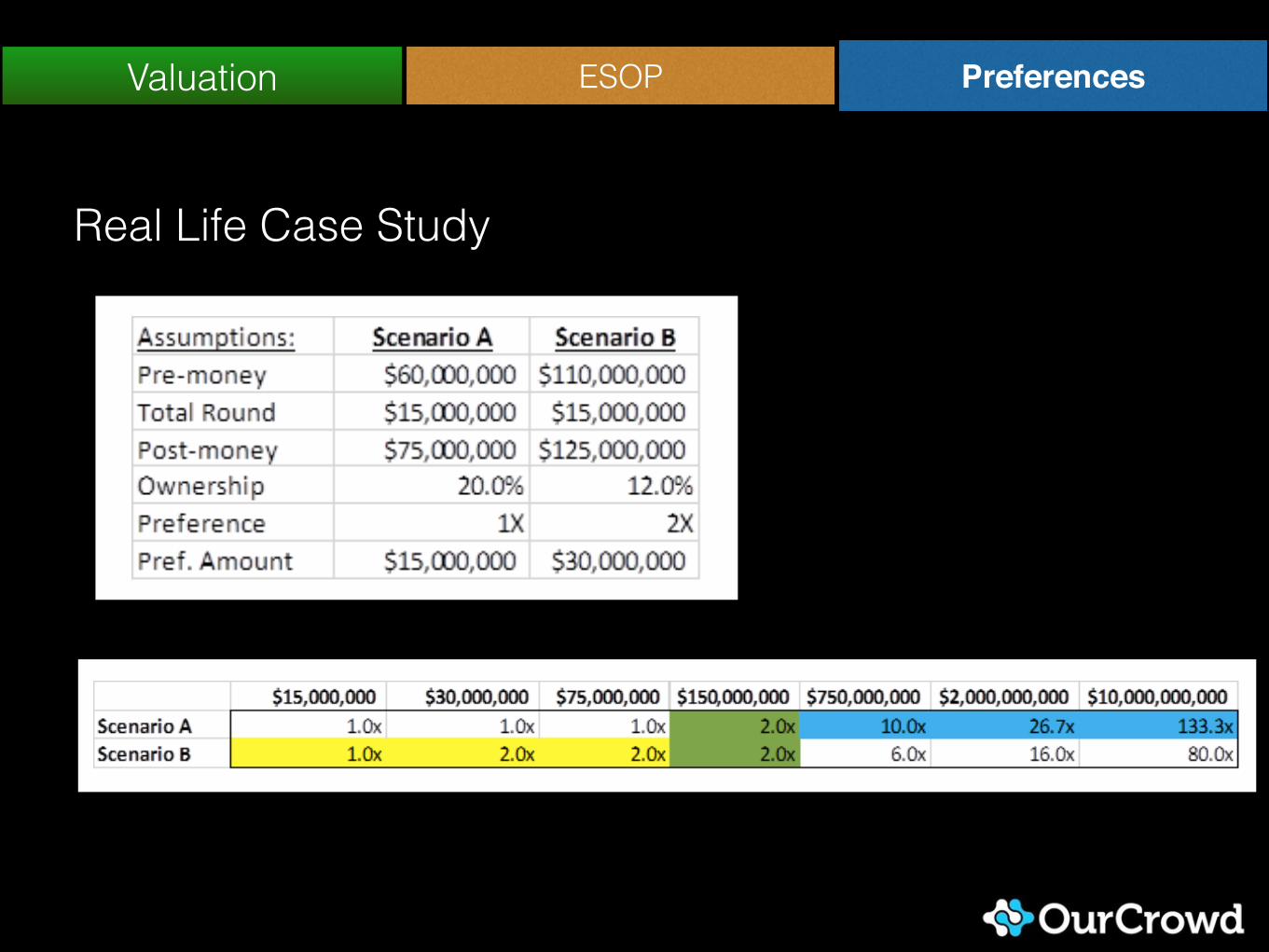

Real Life Case Study

Deal terms reflect the current reality at the time they’re crafted

PreferencesESOPValuation

Real Life Case Study

PreferencesESOPValuation

effectively better value

Valuation ESOP Preferences

Employee Stock Option Plan

Fluid over time, used to recruit and retain talent

Valuation ESOP Preferences

Investors want largerFounders want smaller ESOP

Counterintuitive

Valuation ESOP Preferences

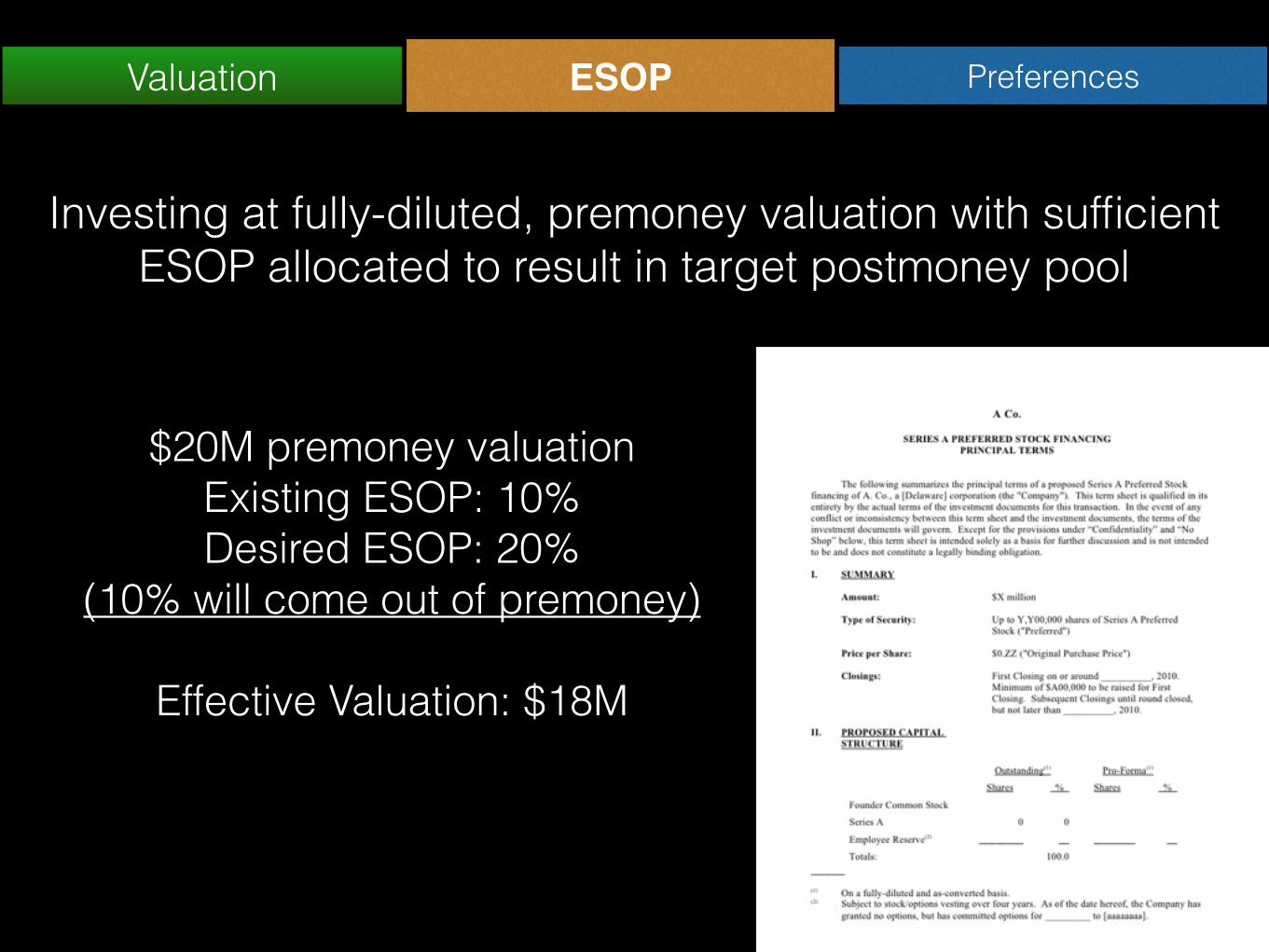

Investing at fully-diluted, premoney valuation with sufficient ESOP allocated to result in target postmoney pool

$20M premoney valuation Existing ESOP: 10% Desired ESOP: 20%

(10% will come out of premoney)

Effective Valuation: $18M

Valuation ESOP Preferences

High sticker price (valuation) vs.

Lower price per share

Something to look out for

Valuation ESOP Preferences

Preferences are the ultimate downside

protection

Valuation ESOP Preferences

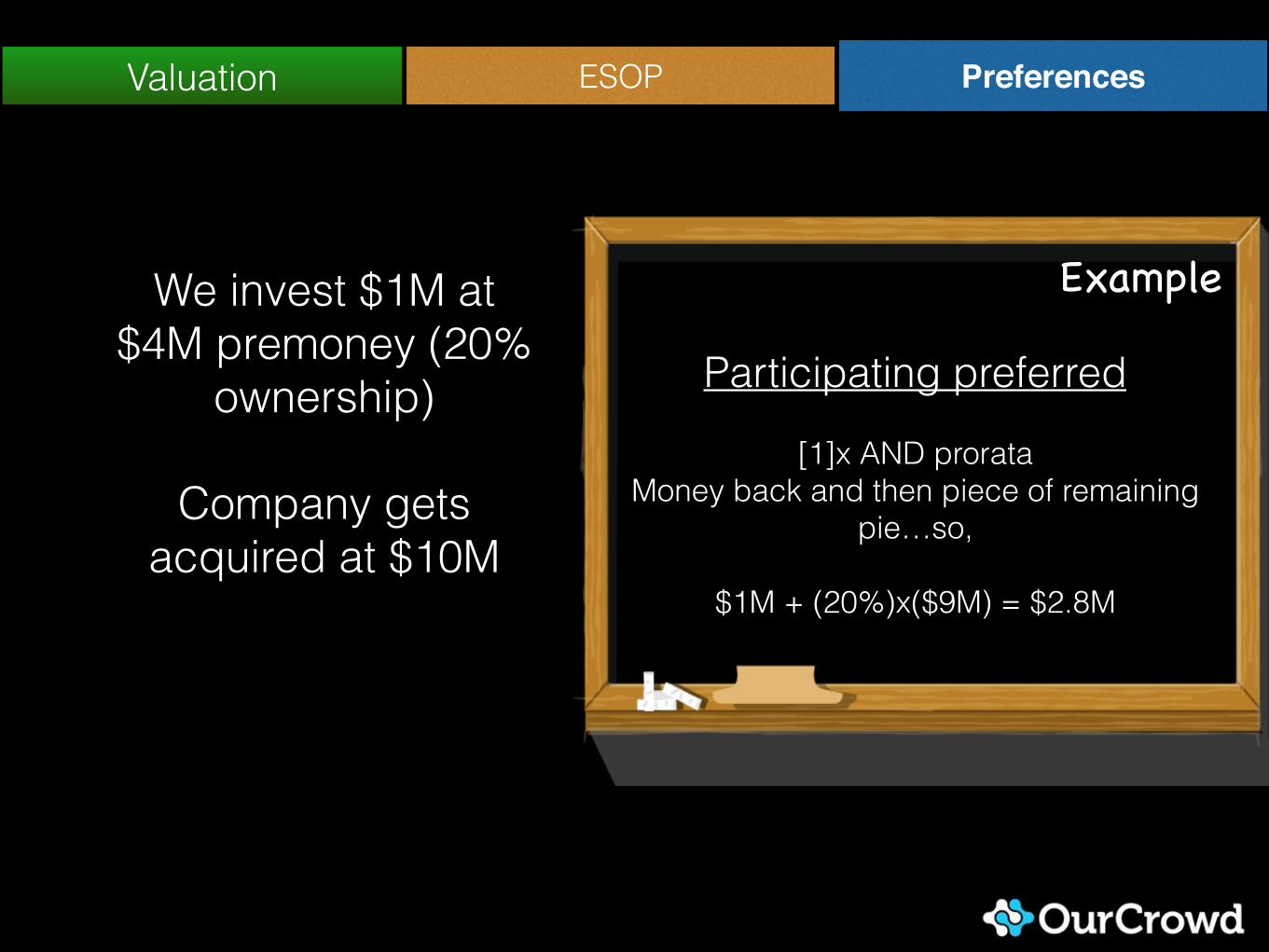

We invest $1M at $4M premoney (20%

ownership)

Company gets acquired at $10M

Example

Non Participating preferred

The greater of [1]x OR prorata $1M OR 20%*$10M

$1M < $2M

Valuation ESOP Preferences

We invest $1M at $4M premoney (20%

ownership)

Company gets acquired at $10M

Participating preferred

[1]x AND prorata Money back and then piece of remaining

pie…so,

$1M + (20%)x($9M) = $2.8M

Example

Valuation ESOP Preferences

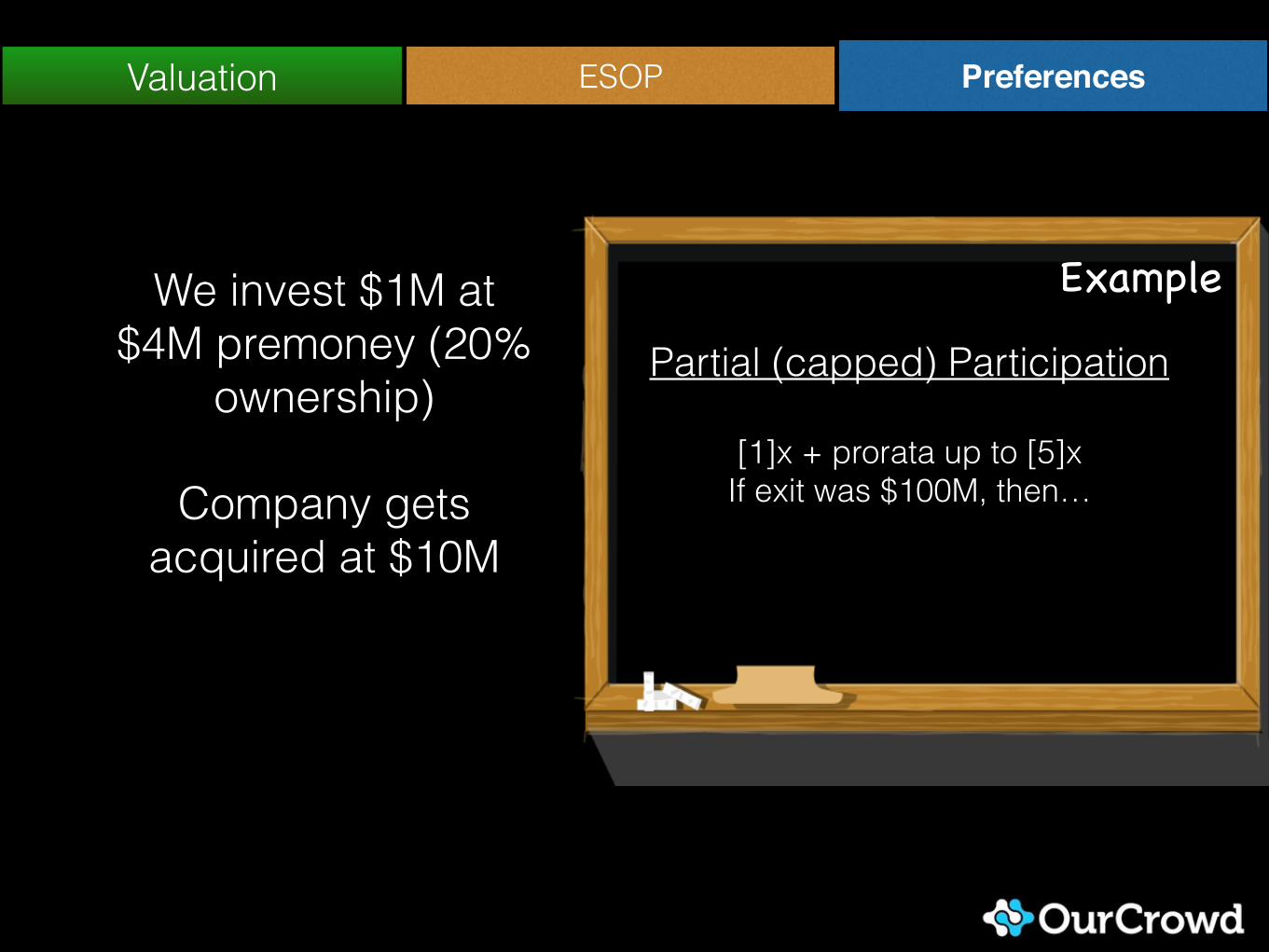

We invest $1M at $4M premoney (20%

ownership)

Company gets acquired at $10M

Example

Partial (capped) Participation

[1]x + prorata up to [5]x If exit was $100M, then…

Valuation ESOP Preferences

Liquidation prefs can create indifference towards certain exit scenarios

Tradeoffs: Relationship between valuation and preferences

Valuation ESOP Preferences

Real Life Case Study

Next step?

Join us next week for Lesson 2Anti-dilution protection Board representation

Control provisions OurCrowd.com

Check out our real-life term sheets by

accrediting on our website